Rainbow Chicken’s earnings have doubled (JSE: RBO)

There may not be a pot of gold at the end of this rainbow, but the chickens ain’t bad either

The poultry industry is a bit like going on a night out with your wildest friend. You’re either going to have an absolutely incredible time, or you’re going to lose your phone and end up sleeping under a tree as the precursor to a morning of serious regret.

In other words, if you’re the type who prefers a quiet night with a book, then chicken is best left for your plate rather than your portfolio.

For the six months to 28 December 2025, Rainbow Chicken achieved growth in HEPS of between 94.9% and 114.9%. As jols go, this is the one you look back fondly on when you turn 35 and realise that you’re probably too old for this now.

The reason for the volatility in earnings is that poultry businesses run at paper-thin margins. A relatively modest improvement further up the income statement has a significant impact on margins by the time you reach the bottom. Likewise, a seemingly minor deterioration in e.g. gross margin can have a nasty impact on profits.

When several things go well, you can see earnings double like this. In this case, Rainbow enjoyed a lovely cocktail of operational efficiencies, strong demand and lower feed costs thanks to improved commodity input prices.

Detailed results are due on 11 March. It’s a pity I’m not a shareholder, otherwise I could treat them as my birthday present that day!

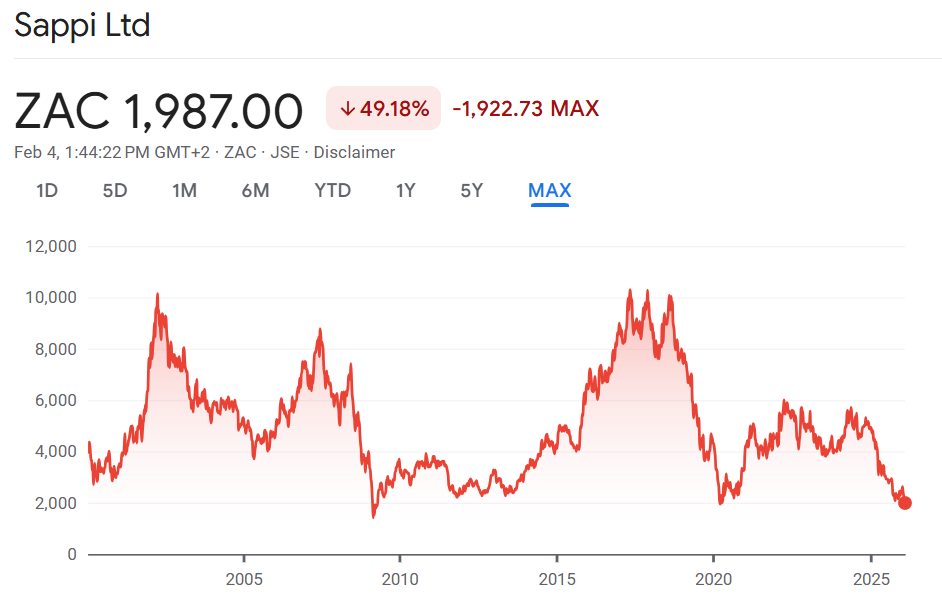

Another loss-making quarter at Sappi (JSE: SAP)

At least Q1’26 was a bit better than Q4’25

Sappi released results for the quarter ended December 2025, the first quarter of the 2026 financial year. Although they reflect a smaller net loss than in the quarter ended September 2025 (a sequential view), adjusted EBITDA is actually lower. And if you apply a year-on-year view rather than sequential, it’s particularly ugly.

This isn’t a surprise to the market, with the share price down 60% over 12 months coming into this release. If anything, the market got a better set of numbers than expected here, based on the share price trading nearly 5% higher by lunchtime and closing 3.6% higher.

The announcement only provides the year-on-year comparison, so a sequential view requires you to dig out the September 2025 results. Revenue fell 6% year-on-year and 7.4% quarter-on-quarter. As for adjusted EBITDA, they were down by a nasty 56% year-on-year and 19% quarter-on-quarter.

Net debt spiked 39% year-on-year, but is only slightly higher sequentially.

The headline loss per share for the quarter was 6 US cents. That’s smaller than the headline loss per share of 19 US cents in Q4’25, so there’s some sequential improvement at least. But compared to positive HEPS of 12 US cents a year ago, it makes for unpleasant reading.

The trouble for Sappi investors is that there are numerous external factors that affect the results each quarter. For example, as we’ve seen in other industrial names, the stronger rand actually creates difficulties for profitability in the Southern African region, particularly when combined with lower international prices for products like dissolving wood pulp.

It’s a real pity that even a 10% increase in pulp segment volumes year-on-year wasn’t enough to offset the pricing declines. Volumes in packaging and speciality papers were also higher by 6%, yet lower prices impacted that business as well. Graphic papers suffered a 9% drop in sales volumes, but managed to keep margins above historical trends.

Then you get all the usual risks in a manufacturing business, like scheduled maintenance shuts and unplanned operational disruptions. This is what we’ve seen play out at the Somerset Mill in North America.

Sappi has been reducing costs in Europe and rationalising the business, but it wasn’t enough to offset these pressures.

There aren’t many highlights in here, but one thing that investors will like is that capex was $56 million in this quarter. That’s way down on $101 million a year ago. When Sappi released full year FY25 numbers, they committed to the market that capex would be below $300 million per annum for the next two years in an effort to repair the balance sheet. This is a promise that they seem to be keeping, with a revised target of $260 million for FY26.

The guidance for the second quarter is filled to the brim with forecasting risk, as Sappi operates in such a difficult environment with multiple factors at play. Overall, they expect adjusted EBITDA to be worse in the second quarter than in the first quarter. Ugh.

Cyclical stocks tend to offer the best buying opportunities when it appears as though nobody could possibly want the shares. That’s what a chart of this phenomenon looks like:

Your eyes are not deceiving you – Sappi is trading at COVID and Global Financial Crisis levels! Have we reached the bottom or will rand weakness drag it even lower? Thanks to a fun new element in Ghost Bites, you can vote in the poll below and we can do a proper sentiment check as a community:

Even more good news at Sea Harvest (JSE: SHG)

Both the seafood and dairy businesses had a strong year

Primary agriculture is a tough gig, especially when you involve the unpredictability of the ocean. Financial performance tends to reflect the volatility of Mother Nature herself: some years are glossy blue days with perfect skies, while others look like they could inspire disaster movies.

Thankfully, the 12 months to December 2025 was a financial year straight out of a tourism brochure. Sea Harvest released an initial trading statement in November that indicated a jump in HEPS from total operations of at least 200%. Fast forward to February and we have a further trading statement that is even better, with an expected increase of between 293% and 303%!

This means that group HEPS has approximately quadrupled from 55 cents to between 216 and 222 cents. You can almost imagine the coconut cocktails with a view of sunset over the ocean.

One of the nuances in the results is that Ladismith Cheese is being sold to Fairfield Dairy based on an enterprise value of R840 million. This deal was announced in November 2025 and makes sense in the context of the company’s push to reduce debt. This means that Ladismith Cheese is reflected as a discontinued operation.

If we therefore dig deeper into the numbers, we find that discontinued operations (i.e. Ladismith Cheese) achieved HEPS growth of 25% to 35%. The continuing operations were particularly crazy, up by between 434% and 444%! The oceans are a lot more unpredictable than fields of cows and cheese facilities.

Aside from the higher catch rates that make a significant positive difference to the numbers, Sea Harvest also locked in efficiency gains in the hake business. To add to the party, pricing improved significantly. This combination can only ever lead to higher earnings, especially in a business with high operating leverage (it costs the same to send out a fishing boat regardless of how much you catch and what the fish are worth).

It’s not all good news of course. There are some impairments that sit in Earnings Per Share (EPS). As a reminder, these impairments are excluded from Headline Earnings Per Share (HEPS).

The impairments relate to the Shark Bay prawn fishery in Australia, the mothballing of abalone farms based on depressed consumer demand in the East, and Cape Harvest Food in relation to the disposal of Ladismith Cheese where the assets exceed the selling price of the business.

The share price closed 4.9% higher on the day.

Egypt takes Vodacom to new heights (JSE: VOD)

The share price has continued where it left off in 2025

2025 was a year to remember for the telcos sector. With the dollar giving frontier markets a breather, Vodacom (and MTN (JSE: MTN)) took full advantage. Suddenly, those earnings in Africa actually meant something, as they weren’t being washed away by currency depreciation.

Africa became investable in 2025 thanks to a new era of US politics. It turns out that when the elephants are fighting, most of the grass has a surprising opportunity to grow.

Results for the quarter ended December 2025 reflect ongoing momentum in the business, especially in Egypt. Group revenue was up 11%, but the segmental view really tells the story. South African service revenue was up just 1.4%, while Egypt grew by 39%!

There’s been a lot of focus on local prepaid revenue recently, with a price war underway across the South African service providers. Vodacom doesn’t give an exact number, merely referring to “revenue under pressure” based on the consumer backdrop and promotional pricing. With contract revenue up 2.6% and data traffic up 32.3%, prepaid revenue must be a fairly nasty number to drag South African service revenue growth down to just 1.4%.

Financial services revenue is another important growth lever, up 24.7% at group level and 59.4% in Egypt.

Encouraged by the current macro environment and the opportunity in Africa, Vodacom announced in December that they would be acquiring an additional 20% stake in Safaricom. Kenya and Ethiopia are attractive markets, so I can see why Vodacom would want to have a controlling stake (55% after the acquisitions) in this business.

In South Africa, the major deal is of course the Maziv fibre transaction, which Vodacom had to fight incredibly hard for at the Competition Commission. Approval finally came in November and implementation began on 1 Deember 2025.

Vodacom and MTN look like heroes right now, but a different result in the US election would almost certainly have resulted in a very different conversation around African earnings. Policies can change quickly, so investors need to always remember that frontier markets are risky places.

With 27.5% of Vodacom group revenue now being generated in Egypt, they will ride this macro wave for as long as possible and be rewarded for it in the market. But if the dollar starts putting pressure on these currencies again, Vodacom will be highly exposed.

There isn’t much of an alternative though, as sitting back and defending market share in South Africa is a strategy that would attract a very low valuation. It’s also incredibly difficult to do acquisitions here, as evidenced by the Competition Commission’s approach to the Maziv deal.

It’s literally a case of nothing ventured, nothing gained. Africa is where the opportunity lies.

Nibbles:

- Director dealings:

- A director of Stefanutti Stocks (JSE: SSK) bought shares worth R34.7k.

- The spouse of a director of Afine Investments (JSE: ANI) bought shares worth R7k. There’s very little liquidity in this thing, with average daily value traded of around R15k!

- With Zeder (JSE: ZED) having announced the disposal of Zaad, the company has relooked at its management function and decided to restructure things in light of how much smaller the group is becoming. Johann le Roux will step down as CEO and FD with effect from 28 February 2026. He will be replaced by Dries Mellet as FD and acting CEO. Don’t feel too sorry for le Roux here: in a separate announcement, Zeder noted net cash settlement of options to le Roux worth around R5.2 million! That’s like a memorable goodbye kiss after a successful first date.

- It’s now Investec’s (JSE: INL | JSE: INP) turn to welcome Standard Bank (JSE: SBK) to the share register, with a shareholding of 5.95%. I’m now even more convinced that these must be stakes held via Liberty within the Standard Bank group, or some other broad investment vehicle. You may recall that Nedbank (JSE: NED) recently announced a similar stake held by Standard Bank.