In this edition of Ghost Bites:

- Fairvest upgrades full year guidance

- Ninety One returns to net positive flows

- Putprop invests in Kramerville

Fairvest upgrades full year guidance (JSE: FTA | JSE: FTB)

The interim period has been kind to the property fund

Fairvest’s results for the six months to March 2026 reflect 12.3% growth in the distribution per B share. The dual-share structure is allowing the B shareholders to enjoy double-digit growth despite the tricky environment. This is because the A shares are capped to the lower of CPI or 5% growth, with the B shares then carrying the variability in earnings.

For the full year, Fairvest expects the B shareholders to enjoy distribution per share growth of between 11% and 13% (an upgrade vs. previous guidance of 9% to 11%).

Underpinning this interim result is like-for-like net property income growth of 8.0%, along with positive rental reversions of 5.7% (rare in this environment – especially for such a diversified fund with 130 properties across multiple types).

The loan-to-value ratio of 26.6% tells us that the balance sheet is in good shape. This is also supportive of distributions going forwards, especially with interest rates heading higher and putting funds with more leverage under pressure.

Ghost Bite: A property fund upgrading its guidance in this environment is a nice surprise. The B shares are up 36% in the past year, delivering fantastic returns to those willing to carry more risk!

Ninety One returns to net positive flows (JSE: NY1 | JSE: N91)

The market movements were also in their favour

Ninety One’s assets under management (AUM) may have increased by 31% for the year ended March 2026, but there’s a big chunk from the Sanlam (JSE: SLM) take-on that we need to adjust for. If you remove that £18.3 billion from the numbers, then you’ll find that the rest of the AUM grew by 17.4%.

That’s still an impressive outcome, but it’s always worth looking at whether this is primarily due to market movements or net inflows. The former is largely outside of Ninety One’s control, while the latter is a direct measure of marketing and distribution strength.

In this period, they achieved net inflows of £2.8 billion. That’s an excellent swing from net outflows of -£4.9 billion in the prior period. Market and forex movements of £19.9 billion did the rest of the work (vs. £9.7 billion in the base period).

As a quick note on the shape of the AUM, only 29% sits in pure equity portfolios. The largest allocation is actually fixed income funds (38%), followed by multi-asset funds (32%). Alternatives now represent a significant 18% of total AUM.

The geographical split is also fascinating. Africa is the largest region at 44% in terms of where clients sit. Next up we find Asia Pacific at 35%, mainly because of clients in the Middle East. The UK is all the way down as 12%, below both Europe (20%) and the Americas (17%).

This should add up to an exciting performance, but HEPS was only up by 2% as reported. There are various reasons for this, including the shares issued to Sanlam in the active asset management transaction that gave AUM such a boost.

Ninety One also reports adjusted earnings per share growth of 12%, with one of the longest list of adjustments I’ve ever seen. To their credit, at least they disclose them on a line-by-line basis in the SENS, which is more than we can say for most companies.

To give some credence to the adjusted growth percentage, the dividend per share is 10% higher.

Ghost Bite: A return to net positive flows is a very important sign here. The next period’s results will hopefully show the true benefit of the Sanlam deal and the resultant scale.

Putprop invests in Kramerville (JSE: PPR)

They aren’t wasting any time in recycling their capital

Property fund Putprop has been busy lately. After announcing a couple of property disposals, they’ve now told the market about the acquisition of a property in Kramerville for R124.5 million.

This is a multi-tenant retail centre that currently houses design and décor retailers. It generated profit after tax of R10.2 million for the year ended February 2026.

This is an after-tax yield of 8.2%. Importantly, this isn’t directly comparable to the net operating income (NOI) yield that property funds would usually disclose, as NOI is typically gross of tax.

Before making any major conclusions on this deal, it would be best to wait for the circular to shareholders. As Putprop is a small fund, this is a Category 1 transaction.

Ghost Bite: It’s been years since I was in Kramerville, but it’s probably one of the more interesting areas in Joburg from a property perspective.

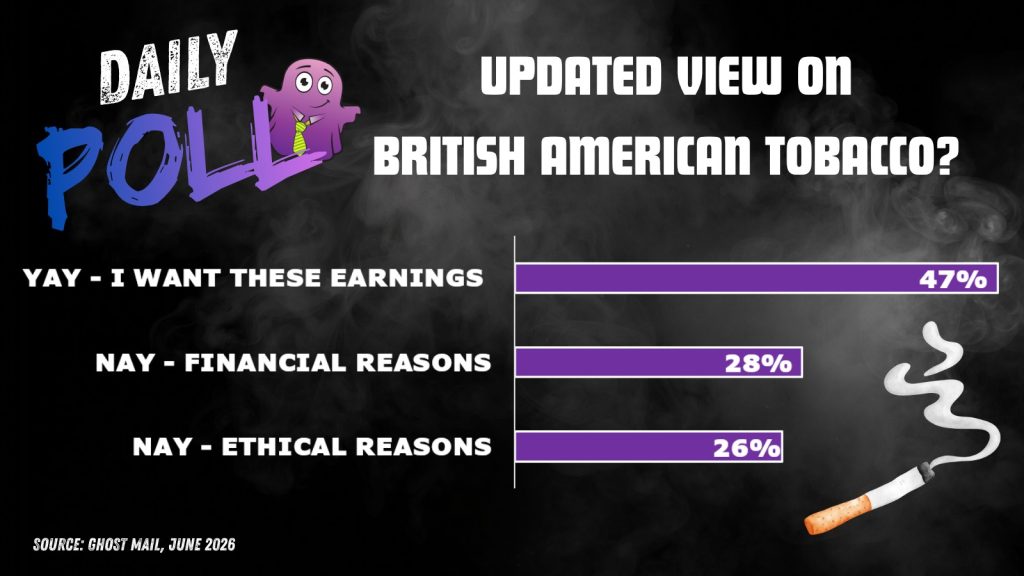

Results of previous poll:

Nibbles:

- Director dealings:

- Des de Beer is back on the bid at Lighthouse Properties (JSE: LTE), picking up R4.1 million worth of shares.

- The CFO of Altron (JSE: AEL) bought shares worth R1.6 million.

- A non-executive director of Richemont (JSE: CFR) bought shares in the company worth R346k.

- A non-executive director of Gold Fields (JSE: GFI) acquired shares worth just over R300k.

- SPAR’s (JSE: SPP) public image took another knock from a Business Day article referencing a BDO report that alleges VAT fraud at a corporate-owned SPAR store. The report was done as part of a due diligence by Amaan Sayed on a potential acquisition of that store for R4 million (in case you’re wondering how much a small grocery store is worth). The announcement includes limited commentary about how SPAR is rejecting the claim of VAT fraud. There’s a whole lot of other stuff in there to try and discredit Sayed, including declined membership at the SPAR Guild and a note that there was a non-disclosure agreement related to the BDO report that has been breached. There are some pretty wild accusations going up and down, but one thing is clear: the relationship between SPAR and its independent retailers is extremely strained. Each time we see bad press around that situation, sentiment towards SPAR deteriorates.

- ArcelorMittal (JSE: ACL) has renewed the cautionary announcement related to a potential transaction with the Industrial Development Corporation. This has been going on for quite some time now. Importantly, ArcelorMittal notes that there has been some progress made on other critical interventions, like customs duties and other trade remedies, as well as the negotiations on reduced electricity tariffs.

- The fight at RMB Holdings (JSE: RMH) is far from over. We now know that Breede Coalitions, an Albie Cilliers investment company, holds over 20% in RMB Holdings. It’s going to be very interesting to see how this plays out in future with a shareholder activist holding such a big stake.

- Trematon (JSE: TMT) has achieved another step in its value unlock process. The company is selling a property in Noordhoek for just over R19 million. This land was being held in the Generation Education part of the business. Trematon is still in discussions to sell that education group, but this land would’ve been separate from the deal anyway. It tells you everything you need to know about the upper-LSM birth rate that a schools business is easier to sell without a land parcel for future expansion.

- Shuka Minerals (JSE: SKA) has completed the second drill hole at the Kabwe Zinc Mine. As usual, most of the announcement is useful only to geologists and mining engineers who know what “mostly zinc silicate – probably willemite” means. For the rest of us, I’ll just refer to the CEO’s commentary about how drilling results continue to deliver “some amazing zinc grades” – that sounds promising. Separately, the company announced that it raised £150k through a share issuance to an African based mining investor that approached the company. They are also paying one of their consultants in shares rather than cash at the moment, which is very helpful for a junior mining company where cash is the most scarce resource of all.

- If you’re a shareholder in Afine Investments (JSE: ANI), then be aware that the company is offering a dividend reinvestment alternative up to a maximum of 25% of each shareholder’s eligible shareholding. A circular has been distributed accordingly.

- Shareholders in Datatec (JSE: DTC) should note that the company has released the circular dealing with the scrip dividend alternative. In such a case, the company issues new shares to shareholders in lieu of a cash dividend, which helps the company retain cash on the balance sheet.