Collins Property Group just banked 17% growth in the distribution per share

The market paid Pick n Pay a premium to VWAP for Boxer, but a discount to spot

Spear REIT is in talks to acquire a property – in the Western Cape, of course

Here’s a first for South African property funds: Vukile Property Fund is going to invest in Italy

Collins Property Group just banked 17% growth in the distribution per share (JSE: CPP)

But they need to get that debt balance down

One thing I’m confident about is that the Collins Property Group earnings announcement hasn’t been written by AI. The introduction is so “human” in its approach, with management lamenting the significantly diminished likelihood of interest rate cuts this year.

I’m all for formal writing in company announcements, but there’s also something to be said for a fireside style – especially when thinking out loud about how the macroeconomic environment has turned against you!

The theme of inflation and interest rate risk is going to come through strongly in many company announcements over the next few months. Brace yourself for outlook statements that include cautious commentary.

Collins will need to be particularly careful, as they run a loan-to-value ratio of 49% (slightly down from 50% as at February 2025). This is well above the levels we see in most REITs.

Management believes that conservative property valuations are a factor here. I think the market would prefer to see valuations done in a way that reflects the actual value, not a conservative view. There’s no point in being conservative if you are spooking the market with a frightening ratio (especially one that kicks you out of most stock screeners that investors would use).

The good news is that distributable income per share was up by 12.8% in the year ended February 2026. They ramped up the payout ratio and delivered 17% growth in the distribution per share. It’s also worth highlighting the impressive 10% growth in net asset value (NAV) per share.

Unlike some of the other names in the sector that are focused on bringing capital home, Collins is busy shifting capital to Europe. I don’t mind a strategy of selling assets in Mozambique and buying in the Netherlands. Mozambique is for beaches and red drinks that give you earth-shattering headaches. It’s not a place I would want to take my money to.

Collins isn’t shying away from local opportunities, though. They are busy with developments in Paarl and Somerset West. They have also completed a development in Namibia, which is definitely a better choice than Mozambique.

The company has already reduced debt by R106 million in March and April. This isn’t much of a dent in the R6.2 billion debt balance as at February, but it’s a start. Given the outlook on interest rates, they need to do a lot more.

Ghost Bite: With pressure on consumers from the oil price and now the impact of inflation on interest rates, 2026 is deteriorating rapidly in terms of the outlook for the property sector. I expect to see more capital raises in the sector over the next few months. Funds will probably look to raise at what might be a near-term peak in the cycle.

The market paid Pick n Pay a premium to VWAP for Boxer, but a discount to spot (JSE: PIK | JSE: BOX)

It looks like Pick n Pay was expecting more

As I discussed with Stephen Grootes on CapeTalk / 702 last night (listen to it here), a good way to understand Pick n Pay is to imagine yourself in a situation where you can’t make ends meet and you’re forced to dig around in grandma’s jewellery to see what you can sell.

The risk is that you’ll run out of nice things to sell before fixing the core problem around your income vs. expenses!

Pick n Pay told us on Monday that they would be selling approximately an 11.5% stake in Boxer. In the end, they offloaded a 12.5% stake. This leaves them with a shareholding of 53.1% in Boxer.

They were targeting proceeds of R4.7 billion and they were successful in reaching this number. But they had to sell more shares than planned to do it, which tells us that they didn’t get the price they expected.

The market paid R82 per share, which is a 3.2% premium to the 30-day VWAP. But Boxer was trading above R88 per share before the accelerated bookbuild was announced, so the shares were placed at a discount of around 7.5% to the previous day’s closing price.

Although a premium to the 30-day VWAP is still a decent outcome, this shows us that institutional investors are wise to (1) the stretched valuation of Boxer, and (2) the likelihood of further sales of Boxer shares.

Pick n Pay’s share price closed 3% lower on the day. Boxer closed 7.5% lower at R82, a rare example of the share price settling at precisely the bookbuild price!

Ghost Bite: Pick n Pay is committed to two things: keeping a controlling stake in Boxer, and taking the core Pick n Pay Stores segment back to cashflow break-even. I remain unconvinced that either of those scenarios will be achieved in the medium-term. If this latest capital raise doesn’t achieve that outcome, then I think you’ll struggle to find many people who will be bullish on a Pick n Pay turnaround. But what do you think?

Spear REIT is in talks to acquire a property – in the Western Cape, of course (JSE: SEA)

They made it clear in the latest results that they are looking at deals

Spear REIT certainly isn’t wasting any time in growing its portfolio after the release of recent results.

Having indicated an expectation to do deals worth between R500 million and R1.5 billion in FY27, they’ve now released a cautionary announcement regarding negotiations for the potential acquisition of a Western Cape property.

The only other information we have right now is that this would be a Category 2 transaction. That’s not really a surprise in the context of a market cap of R6.6 billion. They would have to announce a monster of a transaction to fall into the Category 1 bucket!

Ghost Bite: To their absolute credit, Spear REIT remains one of the only geographically focused REITs on the JSE. Investors appreciate it when management teams stay in their lane and focus on what they are good it. In Spear’s case, they are very good at Western Cape property!

Here’s a first for South African property funds: Vukile is going to invest in Italy (JSE: VKE)

I suspect that fund managers are volunteering for site visits as we speak

Over the years, we’ve seen local property funds execute a number of offshore deals. Many went to Eastern Europe, particularly countries like Poland. Vukile Property Fund was an early adopter of the opportunities in Spain and Portugal, with other funds having followed suit. Now Vukile is once again leading the sector into a new market: Italy.

That may be amore, but it also requires more capital.

The company has announced an accelerated bookbuild of R2.8 billion. Part of the proceeds will fund the acquisition of three shopping centres in Italy (with a gross value of €115 million and an expected yield of 10%). The rest will fall into that bucket the REITs love so much: optionality and financial flexibility.

In other words: pay us now, and we will tell you later what we did with the money.

Given Vukile’s track record, I have no doubt whatsoever that institutions will throw money at this. As always, retail investors will be diluted here, and probably at a small discount. Such is life when we are in a capital raising cycle in REIT land.

To make sure that institutions are ready to dig into their pockets, Vukile also released an update confirming the guidance for FY26 of 9.3% growth in the dividend per share. Looking ahead to FY27, they expect to achieve growth in Funds From Operations (FFO) per share of between 8% and 10% for the year ending March 2027. That’s solid.

Just to further sweeten the deal, Vukile plans to increase the payout ratio from 83% to 85%. This is expected to take dividend per share growth to between 10% and 12% in FY27.

Notably, the guidance for FY27 has taken into account the planned transaction in Italy.

The announcement also confirms that the proceeds from the October 2025 capital raise of R2.65 billion, as well as the proceeds of Castellana’s retail park portfolio of €280 million, have been deployed. In South Africa, the acquisition of Botshabelo Mall for R432.5 million is expected to be approved by the Competition Commission in July.

It’s not all good news, though. Spanish subsidiary Castellana is fighting with the Spanish Tax Authority. Yes, the same tax authority who just got moered in the Spanish tax courts by none other than Shakira!

Her hips don’t lie and we can only hope that Castellana isn’t lying either, as management believes that the Spanish tax assessment (a cool €8 million) has a “remote” likelihood of being successful. More disclosure on this issue will be made when the financials are released in June.

Ghost Bite: I’m sure that many professionals in Claremont are busy justifying trips to Italy to go see this opportunity for themselves. Perhaps they can throw in a trip to Spain to speak to a tax lawyer.

Results of previous poll:

Nibbles:

Director dealings:

For once, there’s nothing relevant to report here!

Netcare (JSE: NTC) has announced that Melanie Da Costa, currently the group’s executive director in charge of strategy and health policy, will be taking over from Dr Richard Friedland as CEO. Friedland will formally retire on 31 December 2026 after co-founding Netcare and being there for around thirty years! Da Costa will get the top job from 1 January 2027. As is common in the market, the outgoing CEO will be available on a consultancy basis for a period of six months. I’m quite excited to see that Da Costa is a CFA, so we will see some proper capital allocation skills at the head of this company!

Orion Minerals (JSE: ORN) is expecting to release a material announcement related to a planned capital raise. The mismatch between listing rules on the JSE and the ASX in Australia has been highlighted once more. Pending the announcement, there’s a trading halt on Orion shares on the ASX but not on the JSE. Orion’s share price fell 9.4% on this news.

Novus (JSE: NVS) is in the process of disposing of the print letting enterprise. They previously agreed to extend the date for fulfilment of conditions precedent. They’ve now had to enter into revised agreements, with the good news being that the commercial terms are unchanged and the conditions are being treated as fulfilled.

RMB Holdings (JSE: RMH) has received the compliance certificate from the TRP for the offer by AttBid. As approval was previously received from the Competition Commission as well, this now makes the offer unconditional. The offer remains open for acceptance until 29 May. Those who accepted by 15 May will already be paid on 22 May.

Greencoat Renewables (JSE: GCT) is transferring its listing from the AltX to the Main Board of the JSE. This is a promising step. The challenge is that I keep hearing about investor frustrations related to the withholding tax process on dividends. They really need to find a solution there to address investor concerns.

Zeder (JSE: ZED) announced a special dividend approximately a month ago. They still haven’t received approval from the SARB to pay the dividend, so the timeline is being revised. It’s truly beyond me how a regulator can make it this hard for a company to pay a special dividend.

Lesaka Technologies (JSE: LSK) announced that Executive Chairman Ali Mazanderani’s contract has been extended. The expiration date has moved out from 31 January 2028 to 30 June 2029. Interestingly, he isn’t eligible for cash incentives beyond his salary and travel costs being covered. But he does have the option to buy 1,000,000 shares at $5 per share. That’s roughly in line with the current spot price, so the incentive is to grow the share price significantly over the next few years.

Anglo American will sell the steelmaking coal business for up to $3.875 billion

Astral Foods had a spectacular year

Calgro M3 has been in an infrastructure investment phase

enX’s remaining businesses look tough

Famous Brands is a mixed bag

Harmony Gold is on track to meet full-year guidance

Nutun is reducing losses far too slowly

Pick n Pay is eating the golden goose

Santam’s prior period was the eye of the storm(s)

SPAR doesn’t have to pay anyone to drag the South-West England business away

Spear REIT remains bullish as ever on the Western Cape

WeBuyCars – but can they sell more of those cars this year?

Anglo American will sell the steelmaking coal business for up to $3.875 billion (JSE: AGL)

Much of the purchase price is structured as an earn-out

Anglo American has found a buyer for the steelmaking coal mines in Australia. Dhilmar Limited (a UK-based private company) is willing to pay up to $3.875 billion in cash for the mines, with $1.575 billion in an up-front payment and $2.3 billion as an earn-out.

Together with the prior sale of the Jellinbah mine, this means Anglo American has exited its overall steelmaking coal operations for up to $4.9 billion in cash.

And in case you’re wondering, Anglo American is still fighting with Peabody about the latter’s decision to walk away from a deal for these assets based on an alleged material adverse change.

Ghost Bite: As we saw with Peabody, a deal is never a deal until the regulatory conditions are met. There’s also a big earn-out here to worry about, running for five years with quarterly payments. Still, this is a step in the right direction for Anglo’s strategy. Now if only they could find a buyer for De Beers…

Astral Foods had a spectacular year (JSE: ARL)

Yet the share priceremains under pressure

When poultry businesses do well, they do really well. Astral Foods has proven this with their interims for the six months to March, reflecting a rather outrageous jump in HEPS of 467% despite a revenue increase of just 11%!

Welcome to the world of operating leverage, something that the chicken industry is famous for. With structurally low margins and a high proportion of fixed vs. variable costs, profits can do wild things in response to modest moves in revenue. In case you need more convincing, net operating profit margin has jumped from 2.5% to 10.2%. You won’t see that kind of move in many industries.

Despite a significant increase in working capital in response to revenue, the group still improved its net cash balance by 13.7% to R1.15 billion.

The Feed division isn’t where you’ll find the major jump in profits. Despite volumes being up 9.8%, revenue was flat due to lower selling prices. But with operating profit up by 23.2% to R366 million, the benefit of solid cost control is visible here. Margins improved from 5.6% to 6.9%.

The Poultry division is the wild child in the group. Revenue increased by 14% thanks to an uplift in margins and selling prices. Here’s the real kicker though: they swung from an operating loss of R26 million to an operating profit of R848 million! This took operating margin from -0.3% to 8.4%.

The outlook statement is sobering after such exciting numbers. Management has correctly flagged inflation risks in this environment of high oil prices. They’ve also pointed to an expected drought in the 2026/2027 summer growing season, as well as the ever-present risk of bird flu.

Ghost Bite: This is a tough industry that can turn paupers into kings – and back into paupers just as quickly. The share price usually isn’t as volatile as the earnings, as the market knows that earnings will average out to something more reasonable over time. The share price is up 29% over 12 months, but dipped almost 3% after the release of these results. Technical traders may want to check out the chart as it drops towards an interesting support level.

Calgro M3 has been in an infrastructure investment phase (JSE: CGR)

This significantly impacts the cash flow story

Calgro M3’s latest period (the year ended February 2026) has been defined by the commencement of infrastructure installation at Bankenveld District City. This is one of the main reasons why net cash from operations has swung from positive R34 million to negative R99 million. During a heavy investment period, they absorb cash that is subsequently released when the units are sold.

This is just one of the things that makes the property development model tricky to operate. Bulls would argue that this is also what contributes to the company having a moat!

The Bankenveld project is described as a landmark project. Just the initial infrastructure phase will unlock a pathway to 6,000 serviced opportunities over the next five years, rolled out in phases. They’ve taken on a huge project in an unforgiving time in the world, so execution will have to be perfect.

Gross profit margin for the segment contracted from 27% to 24%. Management has been warning the market that gross margin was running at unsustainable levels.

The Memorial Parks business is designed to smooth out the cash flows and bring them a capex-light source of income. Revenue increased from R68 million to R86 million. For context, revenue in the property segment was R942 million. Memorial Parks may be a lot smaller, but the division runs at a gross profit margin of 54.9%! The goal is for cash collections in Memorial Parks to be at a level that covers group overheads.

If we look at the overall numbers, we find that HEPS fell by 8.4%. The final dividend was flat in an effort to cushion the blow to investors. Net debt to equity has increased from 0.64x to 0.74x. Periods of major infrastructure development don’t look great in the financials.

Ghost Bite: Property development is one of the most challenging games out there. I have plenty of questions planned for management on Unlock the Stock this week. Be part of the discussion by registering here to attend.

enX’s remaining businesses look tough (JSE: ENX)

Be cautious of the long tail of businessesin listed groups

enX has been a typical value unlock story, with disposals of businesses and subsequent returns of capital to shareholders. What often happens in these scenarios is that groups are left with the least appealing businesses at the end. This makes sense, as they would be the hardest to sell. Squeezing out that last bit of value is very important.

In the six months to February 2026, enX has demonstrated exactly how hard this can be. Revenue is down 37% and they’ve swung from a profit of R16 million to a loss of R6 million. They were actually already in an operating loss position of R12 million in the prior period – it was just shielded by the R29 million return on large cash balances in the group that took them to a net profit. With cash returned to shareholders, there’s nothing to mitigate the losses.

One of the sources of revenue decline is the lumpiness that is inherent in project-based work on data centres. This makes it really difficult for investors to forecast earnings. They have other headaches as well, like a business that sells generators – a less lucrative space now that Eskom is working.

Ghost Bite: These continuing operations sound like a tough scenario to manage. With the imminent release of escrow funds from the West African International sale, enX still has value to return to shareholders. I just wouldn’t underestimate how difficult the remaining stuff will be.

A mixed bag at Famous Brands (JSE: FBR)

The supply chain is driving their performance

The Famous Brands share price has been under pressure and is currently sitting close to 52-week lows. The market is becoming increasingly scared of consumer businesses as we head into an inflationary period, so it will take special numbers to inject some positive momentum into the share price.

The results for the year ended February 2026 aren’t going to do it. There are some positives, but there are also big question marks around the scrappy performance in the operating segments outside of supply chain.

As group context, revenue growth was 5.6% and HEPS jumped by 12.1%. The dividend per share increased by 10.7%. The shape of this income statement wasn’t thanks to operating leverage, as operating profit margin dipped from 11.0% to 10.9%. Operating profit only increased by 4.5%. Instead, it was all about the financial leverage, with a 13.3% decrease in borrowing costs that drove the jump in HEPS.

Notably, free cash flow has dropped by 9.1% to R662 million. You have to really dig to figure out why, as capital expenditure was actually flat at R214 million. The culprit is tax payments, so that’s probably more of a timing thing than an indication of deteriorating return on capital over time.

Net debt has declined by 5.4%, so net debt to EBITDA has improved from 0.89x to 0.82x. This gave them the balance sheet flexibility to introduce a share buyback programme in January 2026. With R54 million invested thus far, this is a positive signal around capital allocation discipline in the group. Being able to accelerate this programme into a weakening market would make a big difference!

We now move to the segmental information, where it becomes clear that Famous Brands is fighting every day to keep things moving in the right direction.

Leading Brands (the typical takeaway brands that you’ll find everywhere) achieved revenue growth of 6% in South Africa. Like-for-like growth was just 2.8%, so most of the growth is coming from an expanding footprint. Operating profit increased by 5% to R516 million.

The SADC region saw a decline in revenue of 6% and a nasty drop in operating profit from R51 million to R29 million. The decrease in profit in SADC offset most of the incremental operating profit gain in South Africa.

In Africa and the Middle East, revenue fell by 17%. Despite this, the operating loss somehow improved from R43 million to R35 million.

It’s the oldest story in the world: why don’t they just focus on Leading Brands in South Africa, instead of trying to operate in multiple regions?

The scrappy set of numbers in Leading Brands is joined by a poor performance in Signature Brands. They are blaming consumer pressure, but I personally think they are just getting smoked by Spur Corporation (JSE: SUR) and their excellent businesses like Hussar Grill.

The Famous Brands portfolio is extremely uninspiring by comparison, with only a small uptick in revenue and an increase in the operating loss from R9 million to R11 million. Famous Brands should stick to takeaways instead of trying to beat Spur (and others) at their own game.

In the UK, revenue fell by 10% and the operating loss was R10 million vs. an operating profit of R7 million. My prior comments about different regions are still relevant.

By now, you must be wondering where Famous Brands actually makes any money!

The answer lies further back in the value chain. Supply chain – SA increased revenue by 7% to R6.2 billion. Operating profit improved by 14% from R444 million to R504 million. This is where they make up for the challenging performance in the franchising side of the business.

The truth is that these things go hand-in-hand. They can’t really operate one segment without the other. By controlling more of the value chain, they can make decisions like not passing coffee and beef cost pressures onto the underlying franchisees. They’ve used other initiatives to drive growth as well, like bringing Coca-Cola and frozen retail product distribution in-house.

Ghost Bite: Like so many other relics of the Lost Decade in South Africa, Famous Brands would do a lot of good for its valuation by simplifying its exposure and focusing on its home market instead of random international operations.

Harmony Gold is on track to meet full-year guidance (JSE: HAR)

If they do, it will be the 11th consecutive year of doing so

Harmony Gold’s operational update for the nine months to March 2026 was met with smiles from investors. The company is on track to meet full-year guidance across key metrics for both gold and copper.

As always, “meeting guidance” and “increasing production” are two different things. Sometimes, mining companies guide for flat production, or even a decrease, depending on underlying operational needs. Sure enough, gold production was up 5% in the third quarter, but still down by 3% year-to-date in line with the plan.

The average gold price has shot up by 39%, so that’s doing a great job of offsetting the dip in production. The other pressure point that needed to be overcome is the 14% increase in all-in sustaining cost (AISC) in gold. Free cash flow in the gold business jumped by 87% year-on-year!

The balance sheet has been quite the story. They’ve moved from net debt of R5.6 billion to net cash of R1.3 billion over a period of just three months. With a critical 24-month programme ahead (including the Eva Copper project in Australia), they need a strong balance sheet and no execution missteps.

In case you’re wondering, the company explicitly notes that labour and electricity are its major input costs. Although they are monitoring higher oil prices, they don’t expect any risks to guidance from the spike in energy prices. Of course, if oil prices stay higher for longer, then the inflationary pressures will come through indirectly.

Harmony’s share price is only slightly in the green over 12 months. It’s down 21% year-to-date due to the correction in the gold price.

Ghost Bite: If volatility bothers you, then the mining sector probably isn’t where you should be investing your money.

Nutun is reducing its losses far too slowly (JSE: NTU)

How did such a successful part of TransactionCapital end up in this position?

We know what happened to SA Taxi. We know that WeBuyCars (JSE: WBC) ended up separately listed. But what I struggle to understand is how the remaining business in Transaction Capital, now called Nutun, has ended up being such a difficult story.

Years ago, Transaction Capital Risk Services (the division that became Nutun) was a very good business. They made proper money by collecting debt books either on a principal basis (they buy the book for cents in the rand and collect it) or on behalf of clients on an agency basis.

Looking in from the outside, the business model hasn’t changed. But the results sure have, as despite a revenue increase of 10% and an EBITDA increase of 36% in the South African business, Nutun has still ended up in a loss-making position. The amortisation of the underlying book plus the interest costs in the group add up to more than the EBITDA generated by the collection business.

Instead of focusing exclusively on delivering improvements to that business, Nutun has been building out a business process outsourcing operation that targets international clients. Revenue dipped by 1% in that segment and EBITDA fell by 15%. EBITDA was just R80 million vs. R710 million in Nutun South Africa. Although this segment is more profitable right now than the South African business, it’s much too small to make up for the decline in the core operations.

Bring it all together and you’ll find a headline loss from continuing operations of R63 million vs. a headline loss of R122 in the prior period. They also report a metric called continuing core loss, which was R63 million in this period and R71 million in the prior period. If we use management’s metric, this tells us that the losses are being reduced far too slowly.

There’s a lot of talk in the outlook statement about the use of AI. This has positive and negative elements. Although AI might improve Nutun’s internal operations, it’s also putting pressure on margins due to a negative impact on contact centre demand.

Ghost Bite: It’s very hard to remain patient with this particular stock. The price is down 44% over 12 months.

Pick n Pay is eating the golden goose (JSE: PIK)

As I suspected, the “value unlock” trade is really hard to catalyse

I’ve been having a number of debates on social media and in investment circles around Pick n Pay. The bull case is simple: Pick n Pay currently trades at a vast discount to the underlying look-through exposure to Boxer (JSE: BOX). The bear case requires more analysis, including an allowance for marketability discounts and potential tax on disposal of Boxer, as well as a look at the balance sheet to see how enormous the lease obligations at Pick n Pay are.

The big win for shareholders would be an offeror swooping in and buying the entire Pick n Pay group. The problems are that (1) this is unlikely to happen while Pick n Pay is still going backwards and (2) the Competition Commission would probably add so many conditions to the deal that it would destroy the economic appeal.

So where does this leave Pick n Pay? They have little choice but to reduce the Boxer stake by selling it at the favourable current market price. The latest update is that they will sell 11.5% of Boxer, leaving them with a controlling stake of 54%. There isn’t much room left for them to keep dripping shares into the market without losing control of Boxer.

If the turnaround was going well, they could use the proceeds of up to R4.7 billion (subject to bookbuild pricing) for share buybacks at Pick n Pay level, a genuine catalyst for a major positive move in the price. Alas, things are still going badly based on the most recent trading update, so they need to eat these proceeds by investing them in the turnaround.

According to management, the entire Pick n Pay store estate has been upgraded and they’ve improved in-store execution. I must be honest that I haven’t heard positive feedback from even a single person in my friend group. Even if the corporate stores are doing better, Pick n Pay has a large franchise estate that has been performing poorly (and irritating customers along the way).

If there’s a successful turnaround happening, it’s hidden under a lot of ugly numbers.

Ghost Bite: Thus far, I haven’t been proven wrong about Pick n Pay’s performance in recent years and how they are being crushed to death by much stronger competitors. I look forward to being wrong, as we need a competitive grocery market that provides jobs.

Santam’s prior period really was the eye of the storm(s) (JSE: SNT)

Underwriting margins have come back down to earth

Santam’s latest numbers for the three months to March 2026 are a great reminder of the risks that insurers carry in their business. Underwriting margins can spike higher in a lucky period of only a few major disasters. But when mother nature strikes, these insurers quickly see their margins return to targeted levels (or worse).

Notably, this update doesn’t include the recent flooding in the Western Cape. Will will only see that come through in the quarter ending June.

The conventional insurance business achieved 9% growth in gross written premium. Within that performance, there are fast growing parts of the business (like Miway and Santam Direct) and areas that had a slow start to the year (like Santam Re).

The underwriting performance is where you’ll see the impact of flooding in the northern part of South Africa and the wildfires in the Western Cape. This led to a loss (net of reinsurance that offsets some of the pain) of R430 million. Despite this, underwriting margin was still above the mid-point of the 5% to 10% target range. This shows you just how fat the margins can be in a period of no major disasters.

The other critical source of value for shareholders is the return earned on insurance funds. The market wasn’t particularly kind to them in this quarter, with a return on insurance funds of 2% of net earned premium. Similarly, the group’s own capital experienced underperformance in investment returns. It won’t surprise you that the Alternative Risk Transfer business was also impacted, with the investment returns offsetting some of the progress made in the operating results of that segment.

The market is particularly interested in the Lloyd’s insurance syndicate that Santam has put together in London. They started writing business on 1 January 2026. They expect a strong contribution to premium growth over the rest of this year, although an operating loss of R300 million is expected in the first year.

The group is also developing its business in India, with a licence to establish a reinsurance brand in India’s GIFT City, the first operational greenfield smart city in India and an International Financial Services Centre.

Aside from market pressures this year and the impact of Western Cape flooding (which is still to be quantified), Santam has flagged the oil price as a source of inflation and thus upside risk to the cost of claims.

Ghost Bite: The share price is down 12% year-to-date, so the market is already aware of at least some of the issues. I wouldn’t underestimate the impact of the Western Cape storm – it’s a densely populated area with valuable property that has suffered considerable damages.

SPAR doesn’t have to pay anyone to drag the South-West England business away (JSE: SPP)

That’s good news, if you can believe it

After the horrors of SPAR’s disposal of the business in Poland, the market learnt that equity actually can go below zero if a balance sheet is bad enough. SPAR literally had to pay someone to take Poland away. They were thankfully more proactive with the Swiss business to avoid a similar disaster.

Now there’s another disposal on the table: the South-West England business with 71 company-owned stores and the associated infrastructure.

The price? £13 million. The expected proceeds after costs? Zippo. Nothing.

On the plus side, they are also in talks to sell 63 stores to third-party operators, with the hope being that they will complete the deals by September 2026. If shareholders are really lucky, perhaps there will even be some cash!

Ghost Bite: There’s all to play for in this turnaround story. To learn more about the strategy, check out this recent podcast that I did with SPAR CEO Reeza Isaacs.

Spear REIT remains bullish as ever on the Western Cape (JSE: SEA)

They are looking to do more acquisitions in the province

Spear REIT is a rare example of a focused REIT on the local market. Where so many funds have gone offshore in search of growth, Spear is like one of those kids from the southern suburbs who hasn’t ever left the Western Cape!

Jokes aside, they need to be cautious of making statements like “the Western Cape from a real estate perspective will continue to outperform the rest of South Africa”. Market cycles have a way of humbling those who use the word “will” – especially as governance changes in Gauteng could be the catalyst to stem capital flows from Gauteng to the Western Cape.

The reality is that Cape Town is at breaking point in terms of property prices, access to schools and traffic on busy routes. At some point, semigration will slow down to a crawl – just like the morning traffic on the N1. I don’t think Joburg will claw back all of the lost ground in my lifetime, but investments are forward-looking in nature. We could reach a point where Gauteng outperforms the Western Cape in terms of year-on-year growth.

Nonetheless, Spear is eyeing a number of acquisitions in the Western Cape. They expect to do deals worth between R500 million and R1.5 billion during FY27.

With 6% growth in the distribution per share for the year ended February 2026 and a 5.8% uplift in tangible net asset value (NAV) per share, I’m not surprised that they are confident enough to keep building the portfolio. A loan-to-value ratio of just 22.9% also helps!

If we dig into the portfolio, we find that the industrial portfolio is 43.7% of the group’s asset value. It boasts occupancy levels of 98.7% and lease escalations of 7.1%, so this is an excellent underpin to the growth story.

The retail portfolio has been boosted by the acquisition of Maynard Mall. It’s hardly a shiny and exciting centre, but they got it on a yield of 9.54%. The centre is in a busy commuter-focused area and gives them more exposure to national tenants, so they are excited about this recent addition to the story. The retail portfolio’s occupancy rate of 97.56% is solid, with in-force escalations of 6.61% and negative reversions of only 0.71%

The commercial portfolio has 92.55% occupancy, a rate that many office funds can only dream of. The in-force average escalations of 7.23% are high relative to the market though, leading to negative rental reversions of 6.05% on new leases.

The outlook for FY27 is growth in distributable income per share of between 6% and 8%. That’s the kind of real growth (i.e. in excess of inflation) that investors are looking for.

Ghost Bite: Spear REIT is seen as one of the safe bets in the local property sector, with an excellent total return in recent years. The big question is whether the Western Cape can maintain the level of outperformance that is now baked into this share price.

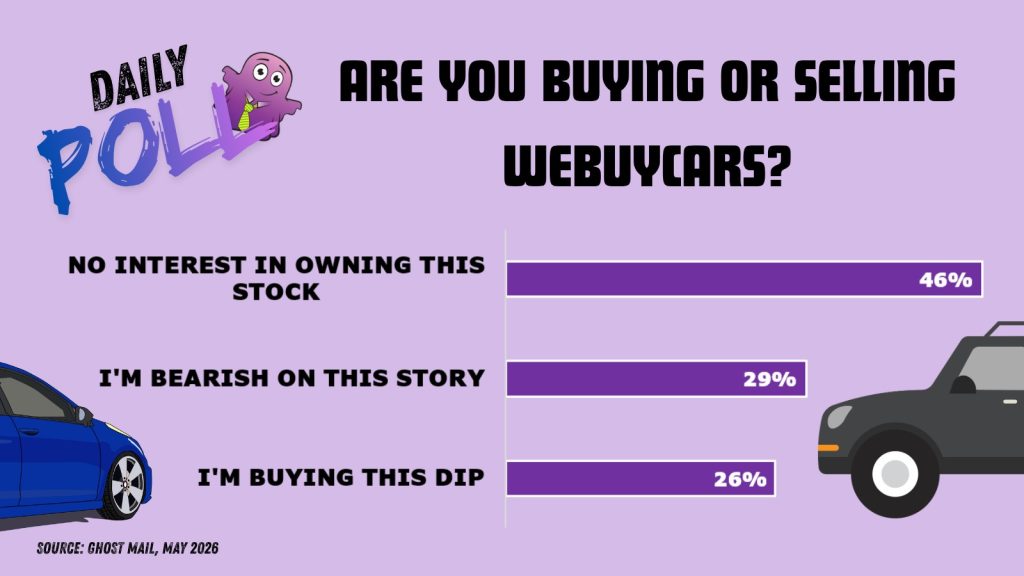

WeBuyCars – but can they sell them quickly enough? (JSE: WBC)

A market in a state of flux has driven some tough numbers

Let me begin by confirming that I remain a shareholder in WeBuyCars. I still believe in the long-term power of this business. If the biggest, most efficient used car player in South Africa is struggling right now, then what do you think is happening to the marginal names? In long-term plays, you need to be willing to ride the volatility.

Unless you’ve been living under a rock, you would’ve noticed that the brands on the road around you have changed. Instead of only Japanese and European cars, we are seeing plenty of Chinese and Indian names. This has filtered through into the used market, where prices have been hurt by how compelling the new car alternatives are. This is why we’ve seen an uptick in new car sales.

This transition in the market needed to churn through the WeBuyCars inventory base. The market hasn’t exactly been patient with this, as the share price has lost a quarter of its value year-to-date. It didn’t help that the founders reduced a big chunk of their holdings to go off and do the RMB Holdings (JSE: RMH) deal alongside Atterbury. Then again, I can’t blame them for diversifying their wealth into something as different as property!

Looking at the performance for the six months to March 2026, units bought increased by 3.2% and units sold only increased by 2.3%. They are living up to their name around buying cars, but the market doesn’t enjoy seeing this differential and a build up of stock – even if it happened during a period of expansion of trading space!

Revenue increased by 7.8% though, so this must mean that the average price per vehicle sold has increased. The official corporate speak is that they are following a “more disciplined percentile-based buying strategy” in more affordable inventory, which they correctly identify as their core competitive position. But with underlying mix effects and other factors at play, this doesn’t mean that they are chasing more expensive vehicles. It’s actually quite the opposite, as they are looking to stick to their range that works well.

This revenue uplift wasn’t enough to protect HEPS, which dipped by 1.7%. The 10% increase in the dividend sends a positive message to the market, but that message is watered down by the HEPS story.

The first and most obvious source of pressure on profits has been the impact on gross margin of the inventory needing to decrease in price to offer value vs. new car alternatives. Those Chinese brands will be entering the used market at an increasing rate though, so part of my investment thesis is that this issue will be worked through the system soon.

A source of pressure on HEPS has been the roll-out of three new supermarkets. It takes a while for the new facilities to become profitable.

Momentum into the end of the period is one of the reasons why the share price found some support on the day of these results. The group achieved an all-time sales record in March 2026, having bought more cars during January 2026 than ever before.

With the national parking bay footprint up by 23.6%, there’s plenty of space for growth here. The market will be looking for a meaningful upswing in sales in the next period. They are also open to smaller new facilities where this makes sense, like a 380 bay property in Bloemfontein (vs. 1,300-bay facilities recently opened in Cape Town and Pretoria).

Bolt-on acquisitions are also part of the story, with the deal for a 49% equity stake in GoBid being concluded in this period. Importantly, the deal comes with a pathway to control and even full ownership over time. This supports the strategy of operating in more areas of the used vehicle market, with GoBid focusing on damaged vehicles that cannot be sold through the usual channels.

How do you feel about these numbers and the share price?

Results of previous poll:

Nibbles:

Director dealings:

The CEO of Choppies (JSE: CHP) and a senior management member sold shares worth a collective R2.8 million.

A director of Labat Africa (JSE: LAB) acquired shares worth R285k in off-market transactions.

Glencore (JSE: GLN) and Anglo American (JSE: AGL) have a headache at Collahuasi, the important copper mine in Chile that they each have a 44% stake in. A tribunal in the country has set aside the Environmental Authorisation that was granted in December 2021. It specifically relates to a project to develop a water desalination plant and its effects on the local community and the marine environment. Although there’s no immediate impact on production, the plant is nearly complete and so this is a potentially serious issue. Collahuasi seems to have been blindsided by this, as they are seeking clarification from regulators on the specific aspects of the ruling.

Lesaka Technologies (JSE: LSK) found an error in its headline earnings calculation. This relates to the treatment of fair value movements on equity securities. It looks scarier in percentage terms than in absolute terms. Headline earnings for the three months to March 31 2026 is 15% lower than first reported, but that’s a difference of $378k in the real world. The comparable period is a much bigger change, with a headline loss of $22.3 million instead of $5.4 million. Although it hits the comparable period far more than the recent period, investors still don’t enjoy seeing stuff like this.

Nu-World (JSE: NWL), a consumer products company with a market cap of around R660 million, wants shareholders to give the board a general authority to issue shares. Although many companies have such an authority in place, investors tend to be nervous of giving management the right to dilute them over time. For maximum flexibility, the company is also asking shareholders for a general repurchase authority as well! Sometimes, you just want to have all options available to you. A circular has been sent to shareholders for the meeting scheduled for 17 June.

RMB Holdings (JSE: RMH) has given an update on acceptances of the offer by AttBid. Thus far, holders of 4.11% of shares in issue have accepted the offer. Together with the existing holdings of Atterbury Property Fund and AttBid, this would take the concert parties to a holding of 47.88% in RMH. The closing date for acceptances is 29 May.

ASP Isotopes (JSE: ISO) is running a bit late on the filing of its 10-Q form (its quarterly financials in the format required on the US market). They expect to get it done within five calendar days of the deadline, so hopefully they won’t irritate the SEC too much with this.

Say what you will about Africa Bitcoin Corporation (JSE: BAC), but at least they are a persistent bunch. Despite having suffered many setbacks on the journey as a listed company, they are moving ahead with transferring their AltX listings to the General Segment of the Main Board of the JSE. This was made possible by a share sub-division that increased the number of shares in issue. With a market cap of just R170 million, this will be among the smallest names on the Main Board. Can they finally find some sustained positive momentum?

Trustco (JSE: TTO) has renewed the cautionary announcement related to a potential delisting of the company. This has been going on for a while now.

Accelerate Property Fund has suffered a setback on its turnaround journey.

Deneb has flagged a juicy earnings uplift.

Stefanutti Stocks shows why it has been one of the most rewarding speculative punts on the JSE in recent years.

A bump on Accelerate Property Fund’s road (JSE: APF)

The stock is back where it started a year ago!

Accelerate Property Fund is a rare example of me taking a position on a speculative stock. It’s worked out well so far, thanks to the incredible progress they’ve made in cleaning up the balance sheet and achieving improved metrics at Fourways Mall.

All looked good until the world started to come to terms with oil at $100/barrel (or more). Now, with yields rising and inflation expectations going up, any marginal property funds are under pressure.

To add insult to injury, the disposal of the Bosveld Bela Bela Shopping Centre by Accelerate for R88 million has fallen through due to the purchaser repudiating the agreement.

Accelerate is looking at options to pursue a damages claim. More importantly, they are now engaging with other potential buyers.

Ghost Bite: The perfect hindsight trade was to sell above R0.70 per share. The stock is now back at R0.50. I’m still more than 20% up at these levels, so I’ll sit tight on this one and allow management to continue with their turnaround efforts despite the macroeconomic pressures.

Deneb flags a juicy earnings uplift (JSE: DNB)

I’m looking forward to the details on this one

Deneb Investments has released a trading statement for the year ended March 2026 that looks very encouraging. HEPS is expected to increase by between 47% and 67%, putting it in a range of 36.8 cents to 41.8 cents.

For context, the share price is R2.53. Deneb is a typical example of a local small cap (on the verge of being a mid cap with a R1.1 billion market cap) with a single-digit P/E multiple. One of the reasons for the low multiple is that Hosken Consolidated Investments (JSE: HCI) has 84% of the shares in the company, so that leaves a very thin layer for public trade.

A lack of liquidity makes it almost impossible for institutional investors to get involved directly in Deneb, so they focus on HCI as an entry point into the group instead.

Ghost Bite: Deneb is interesting, but this is a small part of the HCI empire. A detailed update from the entire group must only be a few days away.

Stefanutti Stocks has richly rewarded punters in recent years (JSE: SSK)

The latest trading statement shows how much things have improved

Stefanutti Stocks has seen its share price skyrocket by 555% in the past three years. They are up 64% year-to-date – an astonishing rally in an otherwise risk-off environment for many risky stocks.

This is a perfect example of why many investors are willing to make a small allocation to turnaround stories and highly speculative plays. When they go well, they more than make up for a few that didn’t! It’s a bit like a venture capital portfolio.

For Stefanutti Stocks, one of the huge wins has been the settlement with Eskom regarding the Kusile Power Project. Net of costs and tax, Stefanutti Stocks received R492 million from Eskom! When you consider that the group market cap is under R1.4 billion, you can see how the prospect of a settlement was a big part of the bull case when the share price was in the doldrums.

The group has also made progress on other corporate actions. These include the disposals of SS-Construcoes (Mocambique) Limitada and Stefanutti Stocks Construction Limited with effect from 12 December 2025. This is why the results for the year ended 28 February 2026 will include continuing and discontinued operations.

Drumroll please… we now arrive at the latest numbers in the trading statement for that period.

For continuing operations, HEPS jumped by between 195% and 215% to a profit of between 369.13 cents and 394.16 cents. For total operations, HEPS was up by between 220% and 240% to between 349.95 cents and 371.82 cents.

Whichever way you cut it, profits have tripled in the past year. This explains the share price move, with the stock currently trading at R7.20.

Be careful of jumping at what looks like a P/E multiple of 2x, as the settlement with Eskom is a non-recurring item that you would want to strip out in assessing the earnings multiple.

Detailed results are expected on 26 May.

Ghost Bite: These trades always look incredible in hindsight. When playing in speculative stocks, it is absolutely critical to spread the risk! I really wasn’t joking in the comparison to venture capital investing, where such investors take many small positions and hope that at least a handful will work out.

Results of previous poll:

Nibbles:

Director dealings:

The CEO of Pan African Resources (JSE: PAN) has unwound a collar structure and sold shares worth R86 million that were pledged as security for a loan. This leaves him with shares worth just over R100 million across his direct and indirect interests.

The recently appointed CEO of KAL Group (JSE: KAL) bought shares worth R505k.

The spouse of a director of Cell C (JSE: CCD) bought shares worth R15.2k.

As a reminder of how deep the debt capital markets are on the JSE, Valterra Platinum (JSE: VAL) has concluded its inaugural auction under the R10 billion Domestic Medium Term Note Programme. It references the ZARONIA rate, which always makes me think of a fictional location in a kids movie! There are various tranches in the auction of R2 billion in notes, with maturity dates from one year to five years. Naturally, the longer-dated debt becomes more expensive. This is the “curve” that people refer to in fixed income investing.

Eastern Platinum (JSE: JSE) is a rather tricky name on the JSE. There’s very little liquidity in the stock. More importantly, the auditors have been flagging going concern risks for as long as I can remember. In the latest numbers for the first quarter ended March 2026, current liabilities are more than double current assets! Even at current PGM prices, the group was only slightly profitable at mine operating income level. The group is still reporting losses overall. It all comes down to the ramp-up at the Crocodile River Mine, with the biggest concern being that they were below target on run-of-mine tonnages at that mine.

Newpark REIT (JSE: NRL) has no liquidity in its stock whatsoever. This is rather ironic, as the building occupied by the JSE is one of just three properties in this company’s portfolio! I’ll give the numbers for the year ended 28 February 2026 a passing mention down here, with funds from operations down by a nasty 36.1% and the dividend following suit. The positive is that the loan-to-value ratio has improved significantly, from 43.1% to 37.7%. The company has taken quite a knock from the revised rental agreement with the JSE. The vacancy rate at the adjoining 24 Central building is material though, so there’s room for upside. I used to work in Sandton many years ago and I have such fond memories of that building!

Look outside quickly and check if it’s going to snow – the suspension of trading in Salungano Group (JSE: SLG) shares has been lifted at last! We were coming up for the three-year anniversary of that suspension in August this year. The company has now fully caught up on its financial reporting.

There are always a few repurchase programmes in progress on the JSE, but one that hasn’t been given much attention is Tsogo Sun (JSE: TSG). Between 23 March 2026 and 14 May 2026, they’ve repurchased 6.94% of shares in issue! The average price paid is R6.962 per share. The current share price is R6.95. Together with other recent repurchases, they’ve bought back shares representing 8.06% of shares that were in issue at the end of August 2025 when the authority to repurchase shares was obtained at the AGM.

Here’s something you won’t read every day: the AGM for SAB Zenzele Kabili (JSE: SZK) at the Johannesburg ExpoCentre (Nasrec) was suspended for safety concerns. The announcement doesn’t go into any further details on what happened.

In Season 2 of this podcast, The Finance Ghost talks to South African entrepreneurs about the ideas, choices and turning points behind building a business from scratch.

Most entrepreneurs don’t dream of becoming accounting software founders. Yet, in the back of a Joburg shuttle, Tayla Dandridge and her co-founders spotted a glaring gap: everyday businesses were being left behind by global ‘whales’ like QuickBooks and Sage. stub was born to serve the trader in Durban, the side hustler in Soweto and the small business owner who needs simplicity, intelligence and local relevance instead of intimidating spreadsheets.

In this episode, Tayla shares how stub grew from a bootstrapped idea into a well-funded Software as a Service (SaaS) platform used by thousands of entrepreneurs across 14 countries. She explains why partnerships, including with Capitec, are critical to unlocking real-time financial insights, and how stub integrates payments to become a true ‘business-in-a-box.’

Episode 1 covers:

How stub was born in a Joburg shuttle and grew into a global SaaS platform

Why simplicity, intelligence and local relevance are at the heart of stub’s product design

How the route-to-market and the product decisions are interlinked

Why partnerships matter, including stub’s integration with our Business Banking

How to choose the right co-founder and what entrepreneurs can learn from Tayla’s experience

Bootstrapping, angel investment and the realities of raising money for a tech startup

How stub is embracing AI to cut admin and empower entrepreneurs

Listento the podcast:

The Finance Ghost plugged in with Capitec is made possible by the support of Capitec Business. All the entrepreneurs featured on this podcast are clients of Capitec. Capitec is an authorised Financial Services Provider, FSP number 46669.

Read the transcript:

The Finance Ghost: Welcome to this episode of the Finance Ghost Plugged in with Capitec. And in fact, it’s not just welcome to this episode, it’s welcome to this season!

Because this is season two – I’m thrilled to report that I will be working with Capitec on another season of this wonderful podcast, where we get to expose people to some of the fantastic entrepreneurs in the broader Capitec ecosystem, and also some of the very important partners and people just making things happen.

Today we are speaking to someone who is both an entrepreneur and a partner to Capitec. So this is going to be a particularly interesting conversation.

That is Tayla Dandridge. She is the co-founder of stub. Tayla, thank you so much for your time joining me from Joburg and I’m very excited to dig into the story with you.

Tayla Dandridge: Thank you so much, Ghost. I’m so excited to be here.

The Finance Ghost: So, interestingly enough, accounting software startups are quite thin on the ground. I think when people talk about IT startups, things like fintechs come up a lot, and lots of payments businesses and all that kind of thing always seem to feature.

But you’re not building one of those. You are building an accounting software startup, and there are some serious whales in that market that you are up against, right? It’s QuickBooks, Xero, it’s Sage, and a lot of others. It’s a tough game to actually break into.

How and why did you actually set out on this journey? When you were in school and they asked you what you wanted to be when you grew up, did you say, “I want to be an accounting software nerd”? Probably not. How did you get here, Tayla?

Tayla Dandridge: It’s a question on everybody’s lips. And I think most people don’t wake up in the morning and think, “sheepers, today I want to build accounting software”. And to be honest, it didn’t necessarily start that way for us either.

Stub was actually started at the back of a shuttle in the Joburg central business district (CBD). We were surrounded by loads of everyday businesses. So think of your spazas, your traders, your service providers.

And with the continuous stat that around 80% of small businesses are failing in South Africa, it was obvious to us that it was a market that was being massively underserved, and we wanted to do something about it.

If you think about the whales that you mentioned, they’re built for a different kind of customer. Their customer is the accountant or someone who has a strong financial or finance background. And that’s for us where the opportunity sits.

If you think of some of the global players in this space, if you think of maybe not this space in particular, but some of the fintechs that are doing epic things overseas, like Monzo or Revolut – they didn’t necessarily come into the market and just think, “Let’s do something slightly better than the high-street banks”. They came and did something fundamentally different – and that’s what excited us at stub.

In verticals where they are whales, there’s almost always a massive underserved layer – and that’s the market that we’re building for.

The Finance Ghost: That is very cool. I love the way you’re thinking about this, and you’ve raised a point that I wanted to bring up later, but let’s touch on it now.

This concept of when you are disrupting, as we say, “whales” – very big, scary things in the ocean (well, not that scary, but they can be) – you need to be quick and you need to be smart, and you need to dart around them, and you need to do things that are fundamentally different, as you say. I think Revolut’s a great example.

From a product perspective, you’ve talked about how stub is built for entrepreneurs rather than for accountants. And as someone who uses QuickBooks, and I am a Chartered Accountant by profession, I can absolutely understand what you’re saying – you go into something like QuickBooks, and I would imagine if you have no accounting background, that’s a very scary thing to be logging into and trying to understand.

You’re very much in the hands of your accountant, and they know that, which is why they distribute through accountants to such a large extent over at Intuit (owner of QuickBooks).

In your world, you are targeting business owners, and that means that stub is probably built quite differently to some of these names. So from a product perspective, what actually makes stub different? When you say you’ve built it for entrepreneurs, what does that mean?

Tayla Dandridge: Well, firstly, Ghost, before we carry on, hopefully by the end of this podcast, you’ll be a new stub customer. That’s the goal.

The Finance Ghost: I was waiting for you to upsell me on stub. I knew it.

Tayla Dandridge: Yeah!

The Finance Ghost: You wouldn’t be an entrepreneur if you didn’t attempt to pitch me. That’s key.

Tayla Dandridge: Definitely! That’s going to be on my 2026 KPIs – move Ghost over to stub.

But when we think about product, and we think about building technology, and we think about how we do things differently at stub, there are three things.

The first thing, and top of my list, and something I fight for on a daily basis, is around simplicity. So how do we make sure that stub is incredibly simple and easy to use, and that it’s a fantastic customer experience?

It shouldn’t feel like a hack, and it shouldn’t feel like it’s a tax on your time. So, how do you get on and get genuinely excited to use your accounting software? That’s a challenge in itself.

The second thing, and probably quite a high priority item on most people’s lips at the moment, is around intelligence. So how do we make sure that stub does the work for you?

And there we’re talking about real time reconciliation, automated insights, focusing on eliminating the admin that entrepreneurs really shouldn’t be doing. They don’t have time for that stuff.

And third, but definitely not least important, and something that we’re incredibly passionate about, is: how do we build localisation? How do we ensure that there are deep integrations and functionality for the markets we serve, considering both price and functionality?

So if you think about our whales and our incumbents, they weren’t built for the trader in Durban. We are.

The Finance Ghost: Yeah, I like that. Local businesses for local solutions.

I just want to understand a bit more about the team behind this, and where you guys actually sit, because I know that you split your time to a large extent between London and South Africa, so you kind of bring that global lens to it as well, which I think is important.

And it’s not just you who’s built this thing. As I said at the start, you are a co-founder and we’ll get into the details of the team and some of those dynamics later.

But perhaps in the meantime, this is a homegrown business, right? I mean, this thing has been built in South Africa by South Africans.

How does that actually work in terms of the localisation, as you say, but also longer term ambitions to grow it elsewhere in the world? Because it’s difficult to scale into profitability in South Africa. It’s not impossible, but it’s obviously quite difficult.

Tayla Dandridge: I’ll try to touch on all of those different pieces, but I think from a founder perspective, we are South Africans, and I think South Africans by nature are generally ambitious and bullish in the things that they do. So we’ve 100% got global ambition just baked into our DNA.

Our team is deliberately split. If you think about London, you think about capital and access. If you think about the US, you think product innovation – and what’s happening overseas. What are the guys on that side of the world really pushing, and where are they placing their big bets?

And then when I think of South Africa (SA) personally, I think it’s an incredible place for execution. So if you are building technology, if you’re looking to work with great people, I couldn’t think of a better place to do it. It’s also obviously the proximity to our core market, which is South African entrepreneurs.

With that said, we are currently serving entrepreneurs in 14 different countries today, but the bulk of them sit in SA. If you think of a product like ours, I think we have it a little bit easier than the large regulated institutions.

A tool like ours doesn’t respect borders. It’s relatively easy for us to move. So think of the problems entrepreneurs are facing in Joburg. There are probably entrepreneurs sitting in Lagos, Kenya or London experiencing similar things. And that’s the opportunity we’re going after.

The Finance Ghost: Yeah, absolutely. It makes a world of sense. I’ve been looking at your website and all the language is just so fun. The entry level product is called Sneaky Side Hustle, which is brilliant. Whoever came up with that, well done. Tayla, I don’t know if that was you or one of your co-founders – whoever it was, that’s very cool. I really like that.

That’s how people come into your ecosystem. That’s how people start to understand what’s going on. And interestingly enough, I see this includes the ability to accept payments online.

So that’s something quite interesting that I’ve only just seen, which is that you’ve actually integrated payments and the accounting software.

That starts to feel more like an entire back-end for a business, as opposed to just “Okay, this is my ledger, my accountant knows where to find it”. Can we talk about that a little bit? Because that’s very interesting.

How does that work in terms of being able to accept payments? It sounds like a “business-in-a-box” for not just a side hustle, but a business to grow into it.

Tayla Dandridge: Right, Ghost. I’m not going to claim Sneaky Side Hustle. I would love to, but I’ll have to give some credit to the team.

But when you think of what I touched on briefly earlier, around the question: “How do you ensure that we are eliminating administrative tasks from an entrepreneur’s daily life?” – you have to think about utility, and you have to think about how you help entrepreneurs get things done.

Accepting payments or getting paid is a big part of that. So ensuring we’re able to integrate solutions that entrepreneurs use and need on a daily basis is incredibly important to us. So at the moment we integrate through a third party to collect payments.

You’ll see a lot evolving in this space over the next couple of months in terms of how we enable entrepreneurs to use payment capabilities that they already use, know, and love.

That’s important for us: to make sure that it’s as easy and simple as possible. But think of payment links on invoices, payment links on checkout. All of the above is covered in our suite.

The Finance Ghost: Yeah, very cool. It’s a pretty interesting offering. And then once you actually go up into the paid tiers, it’s pretty affordable. I see Growing Business sits at R189 a month. I can tell you, compared to the international names, this is definitely cheaper. So very, very interesting. Very cool, what you’re building.

I want to move on then to your route to market, having dealt with some of the stuff around the product.

How have you managed to find the several thousand entrepreneurs who seem to be using this? I must say there are some very, very cool testimonials on your side. One made me laugh. There seems to be someone called Pamela from a business called “Not Anderson”, which I thought was amazing, brilliant. I guess that tells us a lot about the sort of fun people who are using this, and businesses who are disruptors at the end of the day.

They need to stand out, they need to do something different – and I guess that’s where you would appeal. So how do you find these people? What has the route to market been, to get to the level you’ve already gotten to – with quite a few thousand users, from what I can see?

Tayla Dandridge: A lot of people think of distribution as an add-on, and you’re either building a great product, or you’re solving for distribution. And you’re generally tracing one or the other.

But for us, we critically think about distribution as a product decision, and not a growth hack. I like to talk about things in threes. You’ll generally hear that come into our dialogue. There’s either three things that make us better, or three ways to market.

Our distribution looks at three specific angles, and one is direct. So when we think of our direct channel, those are self-serve, our inbound customers, the customers that find us. And we drive a lot of that through great content.

We’re hugely passionate about content that focuses specifically on the entrepreneur, their self-learned experiences, and what we can do to really help make their lives easier. It’s also our fastest feedback loop. So our direct distribution and community channels are where stub’s biggest advocates live.

Some of that feedback that you’ve seen on our website is where our most vocal customers come forward and help us shape the product. It’s an incredibly important channel for us.

Our second channel, which is probably as exciting, and also sits in my vertical, is partnerships and ecosystems. Ecosystems that are already servicing SMEs and entrepreneurs. Where entrepreneurs already feel the value, know the value and trust brands.

I think Capitec is a great example here for us. But it’s important to think of partnerships not as a one-off, but more of categories. So when you think of these categories, what do they look like? Think of large financial institutions, think of tools that small businesses use.

Our third: we haven’t really switched this on yet. It’s been requested a lot through customers around community and referral.

When you’re an entrepreneur building in the entrepreneurial space, probably the person or the people you trust the most are other entrepreneurs. So how do we enable other entrepreneurs to share the stub story? And if they really are enjoying something, how do they tell somebody else about it?

Watch this space – we’re not there yet!

The Finance Ghost: Very cool. That’s great. You are 100% right about entrepreneurs. I think they tend to flock together, and then they always want to know what other entrepreneurs are doing, what’s worked for them, because it’s the hardest thing in the world, right?

I know, you know, a lot of people listening to this podcast will know that starting a business, and scaling it, and getting to the point where you finally feel like it works, and then dealing with the big headaches – it’s extremely difficult. It’s really, really tough.

So I think if you can get entrepreneurs to trust you, and then share that message with other entrepreneurs, that’s a big part of the battle won, absolutely.

You mentioned partnerships there, and I want to touch on that, because you’ve now announced a really interesting partnership with Capitec. Congratulations. That’s obviously how you’ve come onto their radar and hence why you and I are doing this podcast. So I’m glad that you did this partnership because I am certainly enjoying chatting to you.

Capitec Business is growing quickly. I’ve got to say, in season one, the authentic feedback from guests on the show about their experience with Capitec was amazing. People think it sounds like, “oh, you know, they were forced to say that”. But I can tell you it’s the conversations before and after the podcast, the stuff that doesn’t go into the wilderness, where you also get really authentic feedback. And honestly, it was very positive.

I think Capitec Business is on a good wicket here. Well done on getting a partnership in place with them. They are obviously one of South Africa’s best examples of a disruptor, that is for sure. How does that partnership actually work between stub and Capitec?

Tayla Dandridge: I’ll speak about partnerships broadly as a start, and just how we think about partnerships and working with other brands at stub, because that’s really important.

The principle that it sits on is, “how do we work with another brand or another business to really solve an actual problem for entrepreneurs?” Because that’s where the value really sits.

I think you hit the nail on the head. Capitec is a great example in this space. And both on the record and off the record, they’ve been a phenomenal business to work with and build with. It was a great experience.

How it works is, if an entrepreneur has to export bank statements every day, every week or every month, or deal with duplicate transactions from a bad feed, they’re losing time and creating gaps in their financial history.

And those gaps lock them out of multiple things. Locks them out of credit, out of insight and out of real-time decision making, which we know can cause a lot of pain in a small business’s life.

The integration between Capitec and stub absolutely kills that. It’s real time, it’s automatic, and it’s clean. So that, for me, was one of the really exciting parts about it. It was a prime example of how deep, great integration should work. It was also a great example of what happens when a fintech and a large financial institution work together.

We can start unlocking pieces of value in spaces where entrepreneurs have previously been underserved, or largely locked out.

The Finance Ghost: And obviously partnerships are just a very important way to grow, as you’ve highlighted. So I don’t doubt that we’ll see lots more of them from you.

It also goes to that localisation point, right? If you want to actually really embed yourself in a business ecosystem, then you need to partner with the brands and the platforms that people in that country are using. I mean, that’s what it comes down to, right?

Tayla Dandridge: 100%.

The Finance Ghost: Let’s talk then about integration with the other people you are building this with, because you have a few co-founders, which is awesome. And building with co-founders is either the best decision you’ll ever make or the worst.

It seems to be going very well for you. And long may that last. That is excellent. You talked about how this business started in the back of a shuttle. So I’m curious, how many of these co-founders were in the shuttle? Did you guys just go on this ride around Joburg until you thought of a business? Was it like a forced thing? No, I’m just kidding.

Tayla Dandridge: [Laughs].

The Finance Ghost: Tell us that story of how you guys came together, the different skills being brought to the table, and just other advice you have for entrepreneurs in a similar situation where they’re deciding, “do I build with co-founders? Do I rather go to loan and hire people?”. Not necessarily on the partnership level.

This is always a really interesting topic and very helpful feedback for other founders.

Tayla Dandridge: Yeah, of course, Ghost. So I’ll start with a little bit around the shuttle story. So we didn’t just jump in a shuttle and decide to go drive around Johannesburg CBD, but there was a time when the highway in Joburg was sort of broken or being fixed, and…

The Finance Ghost: What do you mean there was a time, Tayla? [Laughs]. The highway in Joburg is always broken or being fixed. If that’s the secret to figuring out how to start a business, we would have way more entrepreneurs. Just drive around Joburg roadworks and figure something out.

Tayla Dandridge: [Laughs]. Just jump in your car and take it for a spin, and something will drop.

No. So, the highway was closed, and three out of the four co-founders were then forced to jump on the Gautrain to commute to work. On the other side of the Gautrain, we then jumped in a shuttle to take us to the office. That’s where it sort of started.

We started thinking about these ideas around, “how do we solve problems in the entrepreneurial space?” Stub wasn’t initially conceptually thought of as accounting software. We found our way there, but when we landed on that, there were three co-founders.

Specifically, one: myself, focused on growth and distribution and partnerships. Two: our CPO and product guy. He built all of our front-end from the ground up, initially. A super talented, smart, product-focused guy. Our third co-founder is a full-stack engineer, and a bit of a pirate. I often say, he can build anything you want him to build, just ask.

And the three of us were initially building accounting software. There was a blaring, huge gap: no accountant.

The Finance Ghost: Exactly. I was about to say, the plumber’s taps here are not just leaking, they’re just not there.

Tayla Dandridge: Yeah. And let me tell you, you run into a couple of things when you’re building accounting software without an accountant. All of a sudden you hear debits and credits and sherbet, they don’t all add up, which is a bit of a crisis.

So we brought on our fourth co-founder a year or two into the conceptual thinking of this product, and that’s when it really came to life.

So as you can see, there’s four of us, with very distinct roles and lanes. And I think that goes to your other question. What works? And why does it work? And why do we feel like it’s working so well? And it’s really simple in my eyes: we all run our own lane, we all trust each other deeply to execute, and we push each other daily.

Someone once said to me, in the beginning of this journey, “Building with co-founders is either the best decision you’ll ever make, or the worst decision you’ll ever make. And there’s very rarely a middle ground”.

The Finance Ghost: Yeah, that person is wise.

Tayla Dandridge: Yeah!

The Finance Ghost: That’s exactly how I thought about this question, right? It’s a binary outcome. It’s not some middle-of-the-road situation.

Tayla Dandridge: It’s a hard thing to put together, but it’s an even harder thing to untangle. So my advice to other founders would probably be: don’t just pick your co-founders based on people that you like. Pick co-founders who share your vision, and bring a skill you genuinely don’t have, so they’re able to fill a gap.

And they’re really good people when things get hard. And I think the “when things get hard” bit is probably when you’ll find out if you’ve struck gold or not.

The Finance Ghost: Yeah, that’s such good advice. And one of my really good mates is a very, very, very successful entrepreneur and he’s built stuff with one partner more than once. They’ve done a few things now.

And I remember when I was getting to know him, I said to him, “You guys have done so much together, you must also be really good mates”. He was like, “Not really”. They don’t spend time together on weekends. They have their own personal lives. “We’re very different”.

It’s a huge amount of mutual respect. But they’re not necessarily friends, not because they don’t like each other, it’s just, they’ve kept it at that level. And I think that’s very important, because it allows you to have that time away from each other, and to come back to each other – and then to be able to have those tough conversations.

These dynamics are not easy. And I think you’re right. I think a lot of people just start a business with a friend or someone they like, and then unfortunately, you end up with a scenario where actually it’s not the right mix of skills, or work ethics are not the same, or for whatever reason, it’s just not congruent.

Then it becomes really unfortunate, and often it ends the friendship at the same time as ending the business. So, yeah, there’s a lot to think about in the world of co-founders. You’ve got to almost put on your – not your corporate hat, but just think to yourself, if you were a big business, you wouldn’t hire people based on your friend group at the braai.

So be careful doing that when you start a small business, even though that’s the default that so many people go to, right?

Tayla Dandridge: 100% Ghost. I think you’ve touched on a few really good points as well. And I think the mutual respect piece is also massive, making sure you’re all running in the same direction to the end goal, because that’s important to you.