Life Healthcare has declared a gross special dividend of 600 cents per ordinary share. The dividend is payable from income reserves and is the distribution of the net proceeds received following the disposal of the Group’s interest in Alliance Medical Group. Payment date is expected on 8 April 2024.

Trustco reminded shareholders in its cautionary announcement that the company is in the process of concluding several pivotal transactions with key shareholders. There is a planned equity investment in the amount of c. N$950 million by Riskowitz Value Fund by way of a fresh issue of Trustco shares to RVF. In addition, Trustco is also considering increasing its equity stake in Legal Shield to 91.35% by acquiring 11.35% from RVF. To top this off, the company is also considering a Rights Offer to minority shareholders – so to enable them the opportunity to participate in the company’s growth and to minimise the dilutionary effect.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 19 – 23 February 2024, a further 3,510,037 Prosus shares were repurchased for an aggregate €99,24 million and a further 237,724 Naspers shares, for a total consideration of R780,48 million.

AB InBev has repurchased a further 224,067 shares at an average price of €58.37 per share for an aggregate €13,08 million. The shares were repurchased over the period 19 – 23 February 2024.

Santova has advised that it has applied to the JSE for the cancellation of 4,328,877 shares which were repurchased by the company at an average price of 743,50 cents per share. Following the cancellation of the Treasury Shares, the share capital of the company will comprise 129,609,951 ordinary shares of no par value.

Collins Property Group was granted REIT status by the JSE with effect from 21 December 2023. The company’s shares will now be transferred from the Real Estate Holding and Development subsector to the Industrial REITs’ subsector with effect from the commencement of trade on 18 March 2024.

Six companies issued profit warnings this week: Mustek, Thungela Resources, Ellies, Putprop, African Rainbow Minerals and Murray & Roberts.

Five companies either issued, renewed, or withdrew cautionary notices this week: Afristrat Investment, Salungano, Trustco, Chrometco and PSV.

Creating value from environmental, social and governance (ESG) considerations has gained importance in M&A1. Companies are examining how they can leverage a target’s ESG strengths to promote revenues, profits and balance sheet efficiencies for the combined business. Such synergies often feature prominently in the equity story presented to investors, and can play a major role in boosting total shareholder returns.

Acquirers face numerous challenges, however. Although the quality of ESG reporting has improved among large companies over the past five years, the use of multiple standards and frameworks complicates efforts to understand and compare their ESG performance. Additionally, relatively few middle-market companies fully report their ESG performance. This makes it difficult to pinpoint ideal targets for bolt-on acquisitions, both from an immediate standpoint and with regard to long-term ESG-related value drivers, such as talent retention and brand visibility.

To overcome the challenges of unlocking ESG synergies, acquirers need to integrate ESG considerations throughout the M&A process, from pre-deal due diligence to post-merger integration.2

ESG synergies are often significant

Traditionally, acquirers have mainly addressed ESG during the risk assessment in their due diligence efforts, in order to mitigate the risks and preserve the target’s value. ESG risk mitigation continues to be a fundamental aspect of the pre-deal assessment. An acquirer needs to integrate targets into its ESG compliance and reporting standards, and avoid potential downgrades of the combined entity’s ESG score. It also must assess the impact on integration costs if the target does not comply with its ESG objectives.

But ESG synergies go beyond risk mitigation. They encompass the ways in which an acquirer can generate value for the combined entity by utilising its own ESG practices and those of the target, as well as by implementing new operating models and generating scale effects. This value can be quantifiable or nonquantifiable.

Quantifiable value is created by ESG synergies that directly affect the income statement. These include, for example: • Driving recurring cost savings through measures such as enhancing operational efficiency in conjunction with decarbonisation,3 and implementing more sustainable procurement and supply chains. • Increasing revenue, such as by overcoming regulatory barriers to access new markets, increasing customer engagement or raising prices. • Improving the cost of capital, such as by mitigating risks, gaining access to alternative funding, or optimising capital expenditures, investments and assets.

Nonquantifiable value arises from the impact of ESG synergies on the acquirer’s equity story and total shareholder return (TSR). A BCG study4 found that deals emphasising ESG considerations tend to outperform other deals, in terms of cumulative abnormal returns upon announcement and two-year relative TSR.

For example, enhanced ESG scores and ratings may lead to higher valuations by reducing the cost of capital and facilitating better access to capital markets. Moreover, if an acquirer materially improves its ESG performance by integrating a target, it may attract new types of investors and broaden the investor base, leading to further capital-raising opportunities and long-term growth.

Addressing ESG synergies in three phases

Acquirers can extract maximum value from their ESG investments by utilising a traditional approach to synergies. The following steps serve as a guide for unlocking ESG synergies.

Conduct ESG due diligence before signing the deal

Before the due diligence phase or the initial stages of public takeovers, it is vital to pinpoint the most significant ESG factors for both the target company and the potential combined entity. Utilise publicly accessible data to perform an outside-in assessment of material ESG-related risks and opportunities. Gain a clear understanding of the most important sustainability issues in the industry, along with the trends and technologies that should be prioritised and accelerated. If ESG presents substantial risks or is central to value creation, leverage data from the target during the due diligence process to evaluate risk exposure, identify mitigation opportunities, and formulate preliminary synergy hypotheses.

Validate ESG risks and opportunities between signing and closing

After signing the deal, use the additional information available to validate the assessment of ESG-related risks and opportunities, describe the synergies in detail, and develop an implementation plan. Support from a “clean team” composed of third-party personnel is valuable during this stage. Although antitrust laws prohibit merging companies from sharing sensitive information before the closing, the clean team can analyse data from both companies and share sanitised, interim results with both integration teams.

The validation process includes collecting data, harmonising ESG metrics and taxonomies, consolidating ESG baselines, and synthesising hypotheses. The output is a prioritisation of material ESG factors, along with initial estimates of savings potential. Substantiate synergies by having the clean team conduct initial analyses, and refine top-down synergy targets derived during due diligence. This phase also includes prioritising ESG initiatives by materiality, assigning and communicating targets, and refining integration costs.

Finally, plan the execution of ESG synergies. Start by validating bottom-up synergy targets with functional teams from, for example, finance, procurement, sales, marketing and HR. This provides the basis for prioritising longer-term opportunities and aligning on new or renewed ESG priorities and ambitions to include in detailed implementation plans.

Implement ESG Synergies from Day 1

After the deal closes, start implementing ESG synergies right away. To obtain comprehensive data about the acquired company, engage in open-book discussions, town hall meetings or small group sessions. Use this detailed information to validate targets and plans developed in earlier phases, execute risk management and savings initiatives and, if necessary, reprioritise longer-term opportunities. The execution phase is also the time to fine-tune the new or renewed ESG priorities and ambitions for the combined entity, as well as to define a roadmap for capturing the value. Finally, create a culture of collaboration among teams from acquirer and acquiree so that they can pursue shared goals aimed at enhancing the combined entity’s ESG performance and unlocking further value.

As ESG topics gain importance as motivations for M&A, acquirers should determine the forward-looking actions that the combined entity can take to generate value through ESG synergies. Acquirers that succeed will promote sustainability goals and ensure that the combined entity’s performance is more than the sum of its parts.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AECI calls this a “year of transition” – and shareholders will hope that’s the case (JSE: AFE)

Nobody likes to see a final cash dividend drop by 79%

AECI has released results for the year ended December 2023. They reflect revenue up 5.4% and EBITDA up just 3.2%. Once you factor in the nasty things below EBITDA at this stage in the interest rate cycle, you end up with HEPS down 11.7%.

Despite unlocking some working capital in this period (and cash from operations increasing by 4.3%), the final cash dividend has dropped by 79% to 119 cents.

AECI is celebrating its 100th anniversary in 2024 and is calling it a year of transition, with the goal of doubling profitability of the core businesses (mining and chemicals) by 2026. It’s interesting that both are referenced here, as the mining business did really well in 2023 (EBIT was a record, having grown 18.2%) and chemicals had a tough year (EBIT down 8.5%).

And in case you’re wondering about the problematic AECI Schirm business, it sits in AECI Agri Health. This segment grew revenue by 8% to R7.6 billion but reported an EBIT loss of R192 million.

There aren’t a lot of highlights in the 2023 numbers as the pre-cursor to the centenary year, but at least net debt improved from R5.345 billion to R4.338 billion coming into 2024.

African Rainbow Minerals flags a big drop in HEPS (JSE: ARI)

A drop in PGM and thermal coal prices are to blame here

African Rainbow Minerals released a trading statement for the six months to December 2023. HEPS is expected to be roughly 40% to 50% lower, coming in at between 1,319 cents and 1,583 cents for the period. This is because of a 43% decline in the PGM basket price (in dollars) and lower thermal coal prices. The weaker rand couldn’t offset these impacts.

Due to substantial impairments, EPS will be between 70% and 80% lower.

Cashbuild drops another 8% after releasing results (JSE: CSB)

This is despite a previously released trading statement

I’ve been writing extensively on the challenges faced by South African retailers, particularly in the home improvement and DIY sector. Cashbuild is a great way to see how bad it has been, with Italtile added to this chart for further context:

Things didn’t get any better in the six months ended 24 December 2023, with Cashbuild’s revenue up only 2% and HEPS down by 20%. The dividend of 325 cents is down 19%, tracking HEPS lower.

The metrics simply don’t work right now. Gross profit margin deteriorated from 25.3% to 24.7% and operating expenses increased by 5% in existing stores, so the profits never really stood a chance.

If you include the impairment of R137 million, then basic EPS decreased by 98%. I’m not usually one to mention EPS, but that’s a particularly nasty outcome that talks to value destruction in this environment.

To make things worse, stock levels increased by 10% despite the asthmatic performance in revenue, so that’s not good for the working capital cycle either.

There’s no sign of improvement, with revenue for the six weeks subsequent to period end showing a flat performance vs. the comparative period.

Harmony signs off on an excellent period (JSE: HAR)

You won’t often see HEPS growth of 226%

Harmony has released results for the six months ended December 2023. As we already knew, they are excellent.

HEPS is up by a whopping 226% to R9.56 per share and there’s a record interim dividend of R1.47 per share. Operating free cash flow? That was also a record, up 265% to R7.1 billion.

No matter where you look, the numbers are great year-on-year. Not only did Harmony enjoy higher gold prices, but they took advantage of them with a strong jump in production and a 5% decrease in all-in sustaining costs.

It all looks good for the full-year numbers, with annual production and grade expected to be at the upper end of guidance and costs well below the guided level.

When gold mines do well, they do really well. The share price has nearly doubled in the past 12 months.

The hard times continue at KAP (JSE: KAP)

The share price has lost over 70% of its value over 5 years and profits have plummeted

KAP has reported on a period that the company will want to forget. For the six months to December, revenue was down 2% and operating profit fell by 17% as operating leverage worked against the company (a larger percentage decrease in profits than in revenue due to fixed costs). HEPS fell by 36%!

If you’re looking for silver linings, you could consider the R914 million improvement in net working capital, or the R708 million reduction in net interest-bearing debt. Much as this helped to mitigate some of the pain of the finance costs, a 20% increase in net finance costs is why the HEPS performance looks so ugly.

KAP is really just the outcome of various businesses mixed together, so it’s critical to look at the segments.

PG Bison grew revenue by 9% to nearly R2.9 billion, while operating profit increased by 18% to R575 million. This is one of the good news stories. Safripol is at the other end of the spectrum, with revenue down 8% and operating profit down 67% to R178 million as raw material margins deteriorated. Unitrans is another tough story, with revenue down 7% and operating profit down 21% to R264 million, with non-recurring restructuring costs of R30 million playing a significant role there.

Moving into the smaller segments, Feltex enjoyed an improvement in South African vehicle assembly volumes, growing revenue by 24% and operating profit by 31%. Restonic saw revenue increase 8% and operating profit almost triple from R34 million to R99 million. Restonic’s operating profit margin of 10.2% is still below the long-term guidance of 13% to 15%.

Finally, Optix could only manage a flat revenue performance and break-even at operating profit level, down from profits of R10 million a year ago. Let this be an ongoing lesson in how hard it is to scale a business.

Don’t get your hopes up for much improvement in the latter half of the year, as the company expects elevated levels of debt due to the extent of capital projects. One of the biggest and most exciting is PG Bison’s MDF project, which will increase the division’s total production capacity by 33%. Perhaps most of all, KAP needs the supply and demand situation to improve in the polymer business, with no immediate improvement expected.

Kibo has finally laughed off the Proventure joint venture (JSE: KBO)

It’s been pretty obvious to everyone else for a while that it wasn’t going to happen

When the smell of nonsense starts to emanate from a transaction, it’s usually because there are layers of the brown stuff hidden underneath. As soon as you see things like a payment that couldn’t be made due to an administrative issue, or a banking problem, the red flags should be going up in your brain.

Kibo Energy hasn’t exactly had many alternatives for funding in subsidiary Mast Energy Developments (MED), so they had to flog this delightfully dead horse for a long time just in case it came back from the dead. Thankfully, due to an alternative deal with RiverFort, the Proventure joint venture is now dead and the company will try and claim damages etc. from Proventure under the terms of the joint venture agreement. Good luck to them.

Onto the new deal then, which will see RiverFort provide an initial funding facility of up to £4 million. The goal here is to lift MED’s Pyebridge 9MW flexible power generation asset out of care and maintenance and into a revenue generating state during April 2024. Make no mistake here: RiverFort will get its pound of flesh, with the facility being convertible into preference shares in Pyebridge.

The market doesn’t seem to care, with the Kibo share price not budging off R0.01 per share. There are so few bids in the market for this thing and there are many offers at R0.02, so it will take a lot to lift this share price off the lowest possible level.

Life confirms the quantum of the special dividend (JSE: LHC)

Investors have been waiting to see what they will get from the Alliance Medical disposal

After quite a wait, shareholders of Life Healthcare now know that the special distribution will be 600 cents per share. This means that R8.8 billion is being distributed to shareholders, which is higher than the estimation of R8.4 billion that was provided in the circular.

To give more context to this amount, the company received £845.9 million for the disposal of Alliance Medical (roughly R20.5 billion) and repaid R10.2 billion to the South African holding company after settling international debt, as well as transaction and hedging costs. Life Healthcare is retaining R1.4 billion to partly fund the acquisition of the renal businesses of Fresenius Medical Care and to support growth opportunities at Life Molecular Imaging.

After the distribution, the level of gearing will be 0.8x net debt to EBITDA.

On a share price of R17.44, a special dividend of R6 per share is material.

Canal+ must make a mandatory offer for MultiChoice (JSE: MCG)

The Takeover Regulation Panel (TRP) has also flexed its muscles here

MultiChoice didn’t win any friends at the TRP recently by making rather unusual announcements related to the Canal+ saga. The TRP needs to approve announcements when a takeover process has been triggered, so a compliance notice has been issued against MultiChoice due to that breach in process. MultiChoice is taking that on appeal.

The more important news is that the TRP has also ruled on whether Canal+ needs to make a mandatory offer to shareholders of MultiChoice, having breached the 35% ownership threshold that triggers a mandatory offer.

The debate here was how to apply the provisions of the Memorandum of Incorporation that limit voting rights of a foreign shareholder to 20%, regardless of how many shares they hold. The TRP didn’t accept that this avoids a mandatory offer, as there are circumstances where the 20% voting restriction wouldn’t apply and Canal+ would have more than 35% voting rights on such matters.

If you’re terribly bored (or very keen on the law) and want to read the entire TRP ruling, you’ll find it here.

We don’t know for sure what the mandatory offer price will be, but we can be very confident that it is below the R105/share that Canal+ was happy to offer shareholders (and which the MultiChoice board gave a resounding “no” to). In other words, I think Canal+ would be very happy to pick up shares at the mandatory offer price.

The dividend is higher at Primary Health Properties (JSE: PHP)

But the share price hasn’t gotten off to a good start on our market

South African investors don’t have much love in their hearts for UK-based property funds that achieve limited growth in rental income. This is why many local property funds have looked to higher inflation regions, like Poland or Spain, as this is seen as friendly territory for South Africans.

Still, it’s not bad going that Primary Health Properties grew net rental income by 5.5% and the dividend per share by 3.1% to 6.7 pence. Goodness knows that the rand does a good job of driving a larger increase when expressed in ZAR.

With a loan to value ratio that has moved from 45.1% at the end of December 2022 to 47.0% at the end of December 2023, along with the average cost of debt going from 3.2% to 3.3%, there are reasons to be cautious about this property fund. Although it is true that debt may be fixed rate in nature, the reality is that any refinancing of debt in the near-term is likely to increase the weighted average cost of debt even further.

It’s rather interesting to note that Ireland is the focus area for investment, with the goal being to grow the portfolio there to 15% of total group exposure from the current level of 9%.

The share price is down 27% just this year. It has more than halved since listing.

Standard Bank keeps waving its flag (JSE: SBK)

It’s a good time to be a bank – especially a good bank

This is a point in the cycle where banks should be doing very well, as interest rates are high and companies have to keep borrowing to fund balance sheets that need to get bigger due to inflation. Not every bank is taking advantage of this properly, but Standard Bank certainly is.

HEPS is up by between 23% and 28% for the year ended December 2023, coming in at between R25.22 and R26.24. The market seems to have priced this in, with the share price closing 0.5% lower at just under R204.

Texton reports a sharp drop in distributable earnings (JSE: TEX)

And there’s no dividend for the interim period

Texton is a short story about a company that doesn’t understand what to do when the share price is trading miles below the NAV per share. Instead of doing buybacks at R2.51 on a NAV per share of R7.12, they choose to keep investing in properties.

This tells you that minority shareholders probably aren’t going to experience a great outcome here. If that doesn’t convince you, then perhaps a 17.1% decrease in distributable earnings will.

The only highlight is that the NAV per share is up 16.8%, with the share price up 23% over 12 months. This means that the discount to NAV has closed slightly. Now just imagine what a few share buybacks would do!

Even Woolworths can’t do well in this environment (JSE: WHL)

Stock availability challenges plagued the FBH business– but was it an own goal?

It’s tough out there. Really it is. Woolworths could only manage 5.4% growth in turnover and concession sales from continuing operations (i.e. excluding David Jones from the prior period) for the 26 weeks ended 24 December 2023, which sadly led to a drop in adjusted diluted HEPS of 5.6%.

And if you aren’t sure about whether to use adjusted numbers, then you could just consider the 6.6% decrease in the interim dividend per share as a way to gauge performance.

With group return on capital employed of 22.3%, I am not sure why the company retained the Bourke Street property in Melbourne as an investment asset after the disposal of David Jones. Woolworths needs to be generating returns way in excess of what property can deliver. When times are tough, having drags on the balance sheet doesn’t make a whole lot of sense.

Digging into the operations, Woolworths Food grew turnover and concession sales by 8.4% overall and 7.2% on a comparable store basis. Price increases were 9.1%, which is below food inflation as Woolworths continues to “invest in price” – a nice way of saying that volumes would be worse unless they tried to price products closer to competitors like Checkers, especially in this environment. Space grew by 3.3% and online sales were up 46.6%, now contributing 5.1% of South African sales. Where they did do well is in the supply chain in the Food business, unlocking an 80bps gross margin improvement to 24.6% despite the investment in price. This helped adjusted operating profit grow by 13.0%, with an operating profit margin of 7.0%.

In Fashion, Beauty and Home (FBH), turnover could only increase by 2.2% with comparable sales up 1.5%. This is an incredibly poor result, especially viewed against apparel competitors that generally had a strong end to 2023. Woolworths blames congestion at the ports, but competitors somehow found a way to navigate that. Volumes dipped badly, as full-price sales meant that price movement was 11.4%. The gap between price movement and comparable sales is volumes, so they fell almost 10%. Net trading space grew 0.3% and online sales grew 26.9%, contributing 5.4% of local sales. Gross profit margin was maintained at 48.0% and expense growth was tightly controlled at 4.7%, so adjusted operating profit fell 5.3% and operating margin was 12.2%.

In Woolworths Financial Services, profit after tax increased from R60 million to R122 million despite the annualised impairment rate increasing as consumers came under strain.

I’m afraid that it doesn’t get any better in Australia, where Country Road Group saw sales decline by 5.0% and 9.5% in comparable stores. Although there’s a high base effect, they acknowledge near-record lows in consumer sentiment in Australia and a 140 basis points decrease in the gross profit margin to 62.1%, so there are reasons to worry here. Adjusted operating profit fell by 46.1% and operating profit margin was 8.5%.

Silver linings? Well, in the last six weeks of the period (the all-important festive weeks), growth accelerated to 7.2%. In the Food business, growth was 8.6% and product inflation was 7.9%, so volumes were positive. FBH grew by 3.8% in those weeks, so don’t think that the excitement was in that part of the business. Country Road Group swung into positive growth at least, up 1.3%.

The outlook for the rest of the financial year isn’t particularly positive. Shareholders can quite justifiably be irritated with the performance, particularly when clothing retailers were generally the winners of the festive season.

Little Bites:

Director dealings:

The CEO of Datatec (JSE: DTC) isn’t shy to buy shares in the company, with an off-market acquisition worth R50.1 million.

Sean Riskowitz, acting through Protea Asset Management, has bought another R1.63 million worth of shares in Finbond (JSE: FGL).

Thibault REIT, an associate of a director of Safari Investments (JSE: SAR), has acquired another R639k worth of shares in the company.

An associate of a director of Huge Group (JSE: HUG) has acquired shares worth just over R4k.

Vodacom (JSE: VOD) released an announcement highlighting all the reasons why they believe that the Supreme Court of Appeal got it wrong in the Please Call Me matter, leading to Vodacom applying for leave to appeal the judgment to the Constitutional Court.

Trustco (JSE: TTO) is trading under cautionary as the company is considering a host of different things. One potential transaction is an investment of up to NAD950 million by Riskowitz Value Fund, enabling a share buyback programme of undervalued shares. And no, issuing shares so that you can do share buybacks doesn’t make any sense to me unless the issue price is far above the price that the buybacks would be made at. Another potential deal is an increase in Trustco’s equity stake in Legal Shield Holdings to 91.35% by acquiring 11.35% from Riskowitz Value Fund. Then, there’s a change to the terms under which the founding family was granted an option to convert NAD1.4 billion in loans into ordinary shares. Finally, there’s a potential rights offer to minority shareholders to enable them to participate in growth and avoid dilution. Again, I guess that’s a precursor to buybacks, for whatever reason. There’s never a dull moment at Trustco. There’s rarely a bright one either, with the share price down 94% in five years.

Anglo American Platinum (JSE: AMS) has signed a renewable energy offtake agreement with Envusa Energy, an energy trading company that will source around 460MW of renewable energy and sell it to Amplats via the Eskom electricity grid. The power will be generated by the Koruson 2 solar and wind projects, with construction due to begin this year and reach commercial operation in 2026. It’s worth highlighting that the deal is for 20 years will the option to extend beyond that. The tariff is a 30% saving vs. the current Eskom tariff. Finally, to sweeten this even further, Envusa is a joint venture between RDF Renewables and Anglo American – the mothership of Amplats.

In further ESG-themed news from Anglo American (JSE: AGL), the company announced that the 10th LNG dual-fuelled bulk carrier has been delivered in Saldanha Bay, having finalised its maiden voyage from China. These vessels offer a 35% reduction in emissions compared to ships fuelled by conventional marine oil fuel. They will be used to transport iron ore and steelmaking core across global shipping routes. Now, if only there was a reliable railway system to get the stuff to the port!

Tiny property fund Putprop (JSE: PPR) has released a trading statement for the six months ended December 2023, reflecting a decrease in HEPS of between 2.3% and 22.3%.

Efora Energy (JSE: EEL) is acquiring the Alrode Depot for R3.8 million. Due to delays in rates clearance account finalisation, the transfer has been pushed out from February to April.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

In the 30th edition of Unlock the Stock, we welcomed Afrimat back to the platform. Ahead of the March year-end, the executive team helped attendees understand the strategic thinking in the business that has led to the deservedly strong reputation on the local market.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Grindrod achieved a strong increase in HEPS (JSE: GND)

Whichever way you cut it, 2023 was a happy time for Grindrod

Grindrod closed 6% higher after releasing a trading statement that has great news for the year ended December 2023. There are a bunch of metrics, including total operations, continuing operations and core operations.

If you know a bit about Grindrod, the different metrics make sense. Total operations include Grindrod Bank which was disposed of in November 2022, so I would ignore that. Core operations include only the Port and Terminals, Logistics and Group segments, so that’s the best indication of how things are going with an increase of between 27% and 30%.

And in case you’re only prepared to work off HEPS from continuing operations, that’s up by between 33% and 39%.

Higher finance costs ruin the party for Motus (JSE: MTH)

You can never ignore the impact of the balance sheet

Motus is a great lesson in how the income statement and the balance sheet interact. Despite revenue being up 11%, HEPS has fallen 27%.

EBITDA stands for Earnings Before Interest, Tax, Depreciation and Amortisation. In other words, this captures profitability before the impact of the balance sheet (both in terms of fixed assets and how they are funded), as well as tax obviously. That part is less interesting.

With revenue up 11% and EBITDA up 13%, the group did well in terms of how costs were managed relative to revenue growth. Sadly, it uses a lot of working capital to have cars on the floor for sale, so everything below EBITDA is where it goes badly wrong. Not only did the cost of funding go up, but net debt to EBITDA jumped from 1.6x to 2.1x. Net finance costs jumped by R639 million to R1.1 billion.

Return on invested capital has fallen from 17.4% to 11.8%.

The South African business contributed 55% to revenue and 66% to EBITDA in this period. It was 65% and 77% respectively in the base period, so the poor state of the South African economy is leading to Motus being less exposed in relative terms over time. It’s also not surprising to see that bolt-on acquisitions in this period were in the UK and Australia rather than South Africa.

We can look at the stats to see why. Industry car sales in South Africa were down 3.5% for the six months to 31 December 2023. Motus has 18.1% market share in the local market. Looking ahead, naamsa is forecasting growth of around 5% in car sales for the 2024 calendar year. Clearly, naamsa isn’t reading enough company updates showing how tough it is for consumers. I struggle to see how this will be achieved.

In contrast, the UK showed new vehicle sales growth of 18.3% for the six months to December 2023. The problem is that used vehicle prices fell significantly in October and November 2023, leading to write-downs in inventory at Motus (and every other car dealer). Interestingly, 70% of Motus’ dealerships in that market are in the van and commercial business.

In Australia, 2023 was a record year for vehicle sales, with the market up 16.8% for the six months to 31 December 2023.

It’s very important to note that Motus generates higher revenue from parts sales (R2.7 billion) than new car sales (R2.2 billion) and parts sales carry a higher margin, so the sheer number of cars on the road is arguably more important than new car sales.

Still, the balance sheet pressures aren’t likely to reduce materially in the near-term, as they cannot execute a “quick and rapid” de-stocking because of commitments made to OEMs. In other words, OEMs don’t allow dealerships to cause damage to customers by selling remaining stock at a discount. Where possible, Motus will obviously try and unlock cash to reduce debt.

Rainbows and sweet sugar at RCL Foods (JSE: RCL)

Earnings growth is a lot higher than the initial trading statement suggested

When RCL Foods released a trading statement in February 2024, the guidance was that HEPS from total operations would be at least 30% higher for the six months ended December 2023. In a further trading statement, the company has delivered the excellent news that the increase will be between 31% and 45.9%.

The improvement has largely come from the Rainbow and Sugar business units, with detailed results due for release on 4th March.

Redefine releases a pre-close presentation (JSE: RDF)

This includes stats as at December 2023

With the closed period about to start on 1 March in relation to the six months to end February, Redefine released a detailed pre-close presentation that you’ll find here.

Aside from the usual stuff dealing with the strategy, it shows that occupancy dipped from 93% at the end of September (the full year) to 92.7% at the end of December. Renewal reversions did improve though, from -6.7% to -2.9%.

The office portfolio is an ongoing headache, with vacancies up from 11.4% to 12.1% and reversions worsening from -12.1% to -13.4%. The biggest problem is lower grade offices, with Secondary Grade reporting a 26% vacancy vs. Premium Grade at 6%.

The industrial portfolio saw vacancies increase from 4.8% to 5.0%, but reversions are positive at +4.8% vs. +2.1% for FY23.

In EPP, the portfolio in Poland, vacancies are pretty steady at 1.5% and reversions swung beautifully from -7.2% to +2.8%. The logistics portfolio in Poland has seen vacancies of 7.8% (up from 7.5%) and renewals up 4% vs. 6% in FY23.

The loan-to-value is expected to be 42.8% for the half-year, dropping to 42.0% by the end of the year. The target range is 38% to 41%.

SARS is shaking the tree in a big way at Sasfin (JSE: SFN)

This tax claim is over 7.5x the size of Sasfin’s market cap!

This update certainly set Twitter / X abuzz when it was announced on SENS, with SARS putting in a truly eyewatering claim of R4.87 billion related to the receiver’s inability to collect income tax, VAT and penalties allegedly owed by former foreign exchange clients of the bank.

This harks back to the syndicate that was using former employees of the bank to expatriate money.

Sasfin believes that the claim has a “very remote likelihood of success” and makes reference to a legal opinion obtained from top lawyers at ENS and endorsed by a senior counsel. This is going to be a huge overhang for an already battered share price, as it will take years until this is eventually dealt with in court.

Super Group also got hit hard by financing costs (JSE: SPG)

The banks are smiling here, even if shareholders aren’t

Super Group’s results were expected by the market as the group previously released a detailed trading statement. Although revenue was up 11.9% in the six months ended December, EBITDA was only up by 5.1% (so that’s a sign of operating margin pressures) and HEPS fell by 16.2% (a sign that finance costs went through the roof).

It’s worth noting that the revenue growth was boosted by acquisitions, so 11.9% isn’t an indication of organic growth.

The biggest part of the business on the revenue line is Dealerships, generating just under R14 billion of the group’s R33 billion in revenue. Next up is Supply Chain Africa at R9.3 billion, followed by Fleet Solutions with R7 billion and Supply Chain Europe at nearly R3 billion.

It’s a totally different story at profit before tax level, with structurally different margins across the segments and financing costs that hurt the businesses that are more working capital intensive. For example, Dealerships SA generated profit before tax of R125.5 million and Dealerships UK was just R13.2 million, which is a combined contribution of under 10% of group profit before tax. Remember, these segments were around 42% of group revenue! The Dealerships UK business was way off the comparable period profit of R91 million, having suffered the same inventory write-down problems that Motus also highlighted in that market.

Still, it could be worse. If you want to depress yourself, you could look at Supply Chain Europe which swung from a profit before tax of R38.3 million to a loss before tax of R132.2 million. Ouch.

Little Bites:

Coronation (JSE: CML) has announced an odd-lot offer that has two strange things about it. The first is that the entire amount is a dividend, which makes it sound like individual shareholders would pay 20% tax on the entire amount received, which is more punitive than paying CGT on it. I don’t know why the company would take this route. Secondly, Coronation is trying to make allowance for opportunistic buying of odd-lots ahead of the offer, noting that they reserve the right not to make payment to shareholders that seem to have bought purely for the offer. In practice, I have no idea how they will get that right without prejudicing shareholders. Odd-lot holders (fewer than 100 shares) will be deemed to sell the shares unless they choose otherwise. Holders of 200 to 500 shares will be allowed to accept a specific offer on the same terms i.e. the default isn’t to sell.

Quantum Foods (JSE: QFH) announced the retirement of CEO Hendrik Lourens, effective 1 April 2024. Adel van der Merwe moves into the role, having been in the eggs business since 2016 and holding previous roles at Pioneer Foods.

Salungano Group (JSE: SLG) announced that Keaton Mining has launched an application to be put under business rescue. This is after trying to reach a compromise with creditors, which was a positive process save for one creditor who elected to proceed with a provisional liquidation application instead. This company holds the operations at the Vanggatfontein Colliery in Mpumalanga and doesn’t have anything to do with the main revenue-generating operations at Moabsvelden Colliery.

The CEO of Datatec (JSE: DTC) entered into an equity funding arrangement that includes a put and call option structure (collectively a collar) with a put strike price of R40.40 and call strike price of R63.78. Expiry is between 30 October 2026 and 31 August 2027. The share price is R40.25. This hedges against downside risk and gives up a portion of potential upside.

MiX Telematics (JSE: MIX) has obtained Competition Commission approval for the proposed merger with PowerFleet. Although the approval comes with conditions (as usual), they are acceptable to the parties involved.

If you are a shareholder in NEPI Rockcastle (JSE: NRP), look out for a circular dealing with the dividend for the year and whether you want it as a capital reduction (the default option) or a taxable dividend.

Zeder’s (JSE: ZED) special distribution has received SARB approval and will be paid on 18 March.

Adcorp (JSE: ADR) shareholders have approved the odd-lot offer. At a share price of around R3.85, baskets of 100 shares aren’t exactly worth much.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I covered these important stories on the local market:

NEPI Rockcastle just released record distributable earnings per share and Vukile easily raised R1 billion on the local market, so there’s demand for offshore property strategies and with good reason – in some cases at least.

Italtile gives us a lot of insight into the start of the local economy and particularly the mindset of higher income earners.

Bidcorp is doing a great job of building its global empire, but margin pressure in the UK is biting.

Spar certainly has its challenges right now, but they seem far easier to overcome than what is happening at Pick n Pay.

Sasol’s performance for the first six months of 2024 continued to be negatively impacted by the continued volatile macroeconomic environment, with weaker oil and petrochemical prices, unstable product demand and continued inflationary pressure. Despite some operational improvements in South Africa, persistent underperformance of the state-owned enterprises involved in Sasol’s value chain and the weaker global growth outlook continue to impact Sasol’s business performance.

Revenue of R136,3 billion is lower than the prior period of R149,8 billion, mainly as a result of the lower chemical product prices across all regions.

Earnings before interest and tax (EBIT) of R15,9 billion is R8,3 billion (34%) lower than the prior period.

The variance to the prior period is mainly due to lower revenue and lower gains on the valuation of financial instruments and derivative contracts, offset by lower chemical feedstock prices in Europe, Asia and the United States of America (US).

The current period includes remeasurement items of R5,8 billion mainly due to:

Impairments of the Secunda liquid fuels refinery cash generating unit (CGU) of R3,9 billion driven by a further deterioration assumed of the macroeconomic outlook, including Brent crude oil and electricity prices, resulting in the full amount of capital expenditure incurred during the period being impaired; and

Impairments of the Chemicals Africa Chlor-Alkali & PVC and Polyethylene CGUs of R1,2 billion due to lower selling prices associated with reduced market demand.

The prior period included impairments of R6,4 billion mainly due to the Secunda liquid fuels refinery CGU (R8,1 billion), Chemicals SA Wax CGU (R0,9 billion), China Essential Care Chemicals CGU (R0,9 billion), offset by a reversal of the US Tetramerisation CGU impairment (R3,6 billion).

The Energy business, including Mining, EBIT increased by 22% to R12,9 billion compared to the prior period with both periods impacted by remeasurement items. Excluding remeasurement items, EBIT decreased by 10% due to lower export coal prices, higher external coal purchases to support Secunda Operations (SO) coal requirements and increased maintenance and electricity expenditure. This was partially offset by improved production at SO, better refining margins, higher export coal sales volumes and the weaker exchange rate.

EBIT for the Chemicals business decreased by 93% to R0,7 billion, compared to the EBIT of R9,6 billion in the prior period with both the current and prior periods impacted by remeasurement items. Excluding remeasurement items, EBIT decreased by 68% compared to the prior period with margins and associated profitability under pressure due to challenging market conditions.

These conditions included macroeconomic weakness especially in China and Europe and continued customer destocking which negatively impacted demand. The average sales basket price for the first half of 2024 (H1 FY24) was 24% lower than the first half of 2023 (H1 FY23), driven by a combination of lower oil, feedstock and energy prices and weak market demand. Despite these continued market headwinds, H1 FY24 total chemicals sales volumes were 4% higher than H1 FY23, largely due to higher ethylene and polyethylene sales in the US, improved production and supply chain performance in Africa offset by continued lower demand in Eurasia.

Core HEPS decreased from R24,55 per share in the prior period to R18,39 per share. The decrease in Core HEPS is due to the decline in EBIT detailed above.

At 31 December 2023, our total debt was R124,1 billion (US$6,8 billion) compared to R124,3 billion (US$6,6 billion) at 30 June 2023. Sasol issued R2,4 billion in the local debt market under the domestic medium term note (DMTN) programme during the reporting period. The US$1,5 billion (R27,5 billion) bond will be repaid in March 2024.

Cash generated by operating activities decreased by 31% to R14,7 billion compared to the prior period in line with the decrease in EBIT and the movement in working capital.

Capital expenditure, excluding movement in capital project related payables, amounted to R15,9 billion compared to R15,6 billion during the prior period. Capital expenditure relates mainly to Secunda shutdown activities, the Mozambique drilling campaign and continued spend on Synfuels renewal and environmental compliance activities.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Higher finance costs hit AECI’s business (JSE: AFE)

HEPS has decreased year-on-year

AECI has released a trading statement for the year ended December 2023. HEPS is expected to decrease by between 7% and 16%. This means an expected range of between R10.77 and R11.99 for HEPS, with the share price currently trading at around R95.

If you’ve been following the company, you’ll know that the business in Germany has been a source of headaches. Finance costs are also biting, with the balance sheet needing to support revenue growth through higher working capital levels.

Altron’s HEPS moved higher in continuing operations (JSE: AEL)

As for total operations, the story looks different

Altron had to recognise some non-cash adjustments in the first half of the year that ruined the full-year result. This included issues in Altron Nexus and Altron Document Solutions of R334 million and R95 million respectively, as well as an impairment of R33 million related to Altron Nexus. Both of these businesses are recognised as discontinued operations for the full year numbers, which is why the HEPS result looks so different for continuing vs. total operations.

Starting with continuing operations, HEPS will be between 16% and 24% higher. For total operations, this swings horribly from HEPS of 29 cents in the comparable period to a headline loss per share of between -21 cents and -16 cents for this period.

Altron Document Solutions and Altron Nexus are the subject of active disposal processes. In other words, just ignoring them as discontinued operations is dangerous. If they do badly, they may not be easy to sell and hence Altron shareholders could continue to suffer losses. The other discontinued operation is Altron Rest of Africa.

Looking deeper, the group notes Netstar as a highlight of the second half of the year, reaching over 1.7 million subscribers and over 2 million connected devices. They can’t help but mention Big Data (including the capital letters), of course.

CA Sales Holdings just keeps delivering (JSE: CAA)

This company just keep impressing

The CA Sales Holdings business is all about helping FMCG product providers reach their market. The model is based on driving volumes, which can grow even in a slow growth market through winning market share.

The results speak for themselves, with the company achieving HEPS growth of 23% to 28% in the year ended December 2023. This has been achieved through growth in existing and new clients.

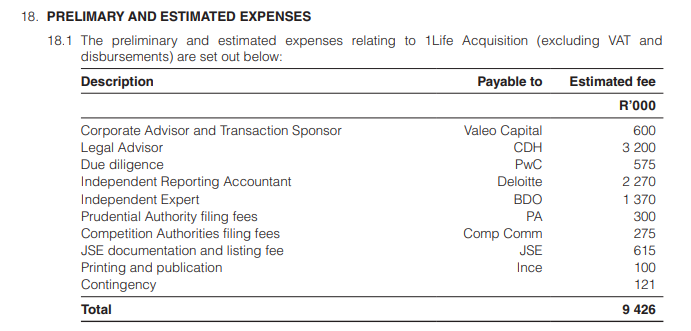

Clientele releases the 1Life acquisition circular (JSE: CLI)

This is a category 1 transaction, so it’s a big one for Clientele

Clientele announced this deal back in November 2023, with the plan being to acquire 100% of 1Life from Telesure Investment Holdings. The idea is that this will create a larger mass and middle income insurance business with a combined embedded value of around R7.8 billion and 1.5 million contracts. The scale benefits are obviously part of the plan here.

The price is based on the embedded value of 1Life being calculated in a similar way to that of Clientele, plus a premium of 6.23% for control. This is a modest control premium, with the trick here being that Telesure will receive shares in Clientele as consideration for the deal. Don’t feel too bad as a Clientele shareholder, because Telesure is receiving the shares at a price of R16.25 per share. That’s much higher than the current market price of Clientele shares, reflecting the embedded value per share rather than the market’s view on value.

Long story short, this is a deal based on embedded value for embedded value, with a small control premium for 1Life. That seems like a sensible approach to me. I must also give credit to Clientele for managing the deal in such a way that expenses are reasonable, coming in at under R9.5 million for the entire thing:

For a deal worth R1.9 billion, that’s a modest cost indeed. This tells me a lot about the Clientele management team. For all the details, get the circular here.

Jubilee is growing, but margins are taking strain (JSE: JBL)

Jubilee bucks the mining trend

Jubilee Metals has released results for the six months to December 2023. Group revenue is up 18.4%, driven by higher levels of production. EBITDA is only up by 13.6% though, which looks somewhat spectacular vs. other mining groups but reflects margins under pressure at Jubilee when you view it alongside revenue growth.

By the time we get to earnings per share, the increase is only 6.7%. It’s worth noting that a placing of shares took place in January, so earnings per share will have that headwind to contend with in the 2024 year as well.

Looking further into the numbers, the highlight is copper production increasing by 46.5% in Zambia. The growth in South Africa is far more modest, yet it remains a stable cash generating base for the group.

Normalised HEPS drops at Libstar (JSE: LBR)

And in this case, this is the right metric to look at

Libstar has released a trading statement dealing with the year ended December 2023. It’s a long one, giving far more details than a trading statement usually does.

The good news is that revenue growth improved from 4.0% in the first half to 7.3% in the second half, taking full-year growth to 5.8%. The pricing vs. volume analysis is quite something, with volumes down 4.8% and prices (and mix) contributing growth of 10.6%.

Gross profit margin was 21.2% in the second half, which is an improvement of 120 basis points vs. the first half. Full-year margin is 20.7%, which is slightly lower than the 2022 result.

Despite all the diesel costs of load shedding, operating expenses only increased by 1.9%. That’s an impressive display of cost control. Sadly, the banks got the bulk of the benefit, as finance costs were up a whopping 53.3% thanks to higher financing costs. This is despite net debt to normalised EBITDA decreasing from 2.1x at 30 June 2023 to 1.6x at 31 December 2023.

If you look at HEPS without normalisation adjustments, it includes insurance proceeds of R120 million related to the Denny Mushrooms fire incident. That’s not a sensible way to consider performance, so the group quite correctly reports normalised HEPS without this number.

Unfortunately, normalised EBITDA fell between 2.2% and 4.3% for the full year, as the second half performance couldn’t make up for the 18.3% decline in the first half. Combined with the impact of finance costs, this is why normalised HEPS from continuing operations fell by between 9.7% and 12.7%.

Lower revenue hits profits at Sasol (JSE: SOL)

There is also a notable decrease in the dividend payout ratio

Sasol has released results for the six months to December 2023, showing why the share price has come under great pressure. Weaker prices for the commodities are not a helpful environment alongside inflationary pressures on costs. Of course, there are also the challenges of poor local infrastructure to contend with.

Revenue has fallen by just over 9%, with lower chemical prices as the major driver. Operating leverage has worked against the company here, with EBIT down by 34%. Aside from the drop in revenue, there were other issues for EBIT like valuations of financial instruments and derivative contracts. On a segmental basis, the biggest loser was Chemicals Africa with a massive negative swing in EBIT from R8.99 billion to R3.44 billion. The rest of the Chemicals business (America and Eurasia) moved from the green into the red, reporting losses. A strong improvement in the Energy Fuels business from R5.1 billion to R9.6 billion couldn’t offset this.

Shareholders only enjoyed a slightly less severe impairment in this period than the prior period. After writing down its assets by R6.4 billion in the comparable period, this period saw write-downs of R5.8 billion.

Headline earnings excludes the impact of impairments, so the 34% drop in HEPS happens to be in line with the drop in EBIT in this period. The interim dividend is 71% lower though, so the payout ratio has decreased considerably.

The CEO of Marshall Monteagle (JSE: MMP) has acquired shares in an off-market transaction to the value of R13.7 million.

Sean Riskowitz, acting through Protea Asset Management, has bought another R726k worth of shares in Finbond (JSE: FGL).

The CEO and Dr. Christo Wiese are at it again, each buying shares in Invicta (JSE: IVT) worth R202k.

The company secretary of Trematon (JSE: TMT) has sold shares worth R135k.

An associate of a non-executive director of Mondi (JSE: MNP) has bought shares in the company worth R120k. Here’s the thing: the trade happened in April 2023 and wasn’t disclosed due to an “administrative oversight” – the punishment for undisclosed trades really does need to get more severe for it to be taken seriously.

The CEO of Primary Health Properties (JSE: PHP) has purchased shares worth £3.2k under the company dividend reinvestment plan.

Hammerson (JSE: HMN) has sold Union Square, a shopping centre in Aberdeen, for £111 millon in cash. Importantly, the net initial yield is 11% and the sale is at a discount of 8% to the 31 December 2023 book value, so that’s a disappointing price. This reduces net debt for the fund and concludes the £500 million non-core asset disposal programme communicated to the market at the start of 2022.

Sea Harvest (JSE: SHG) achieved 100% approval from shareholders who attended the meeting for the proposed acquisition of the businesses from Terrasan Beleggings. Related to the same deal, Brimstone (JSE: BRT) as the controlling shareholder of Sea Harvest received 99.95% approval from its own shareholders for the transaction.

Sibanye-Stillwater (JSE: SSW) released a mineral resources and mineral reserves declaration. This is really aimed at more technical modelling of mining company prospects so I don’t usually write on these in any detail in Ghost Bites. I thought it was worth a mention that mineral reserves for SA PGMs are down 10.4% and for SA gold are down 15.7%, impacted by a combination of depletion and cessation of activities in the case of gold. The shift towards green metals is clear in the group strategy.

Ellies (JSE: ELI) is in business rescue and it’s not hard to see why, with a headline loss per share of between 12.80 cents and 13.66 cents for the six months ended October 2023. Keep in mind that the share price is only R0.01!

There are two types of people in this world: those who know what Vantablack is, and those who are about to go on a rollercoaster ride of discovery.

Friedrich Nietzsche once famously said “If you gaze long into the abyss, the abyss also gazes into you”. I reckon he was only able to make that kind of statement because Vantablack wasn’t invented in his lifetime, because there’s no doubt that Vantablack represents the very essence of nothingness. There is no light and no life at the bottom of this shade of black. Nothing is reflected. Nothing gazes back.

How is it that scientists came to create a black so black that it absorbs 99.96% of light – and how did one artist manage to corner the market on it?

The science-y bit

The name “Vantablack” represents a category of ultra-black coatings that exhibit total hemispherical reflectance (THR) levels below 1% across the visible spectrum. In other words – if a surface or object is coated with Vantablack, it will absorb up to 99.965% of visible light. Furthermore, these coatings possess the remarkable quality of maintaining consistent light absorption from nearly all viewing perspectives, meaning that Vantablack is capable of creating the illusion of two-dimensionality even when applied to a three-dimensional surface.

Vantablack was invented by Ben Jensen, the founder and CTO of Surrey NanoSystems, in 2014. In case you’re wondering how it actually works, I’ll give you the high-level explanation: a forest of vertical carbon nanotubes is “grown” on a substrate using a modified chemical vapour deposition process. When light strikes Vantablack, instead of bouncing off, it becomes trapped and continually deflected amongst the tubes, absorbed, and eventually dissipated as heat.

The use case for the world’s blackest black is interesting, ranging from scientific applications right through to luxury (think watch faces and really expensive custom car paint jobs). Within the scientific realm, Vantablack created a stir regarding its potential applications in cameras, telescopes and sensors. Its unique attributes render it an appealing substance for a variety of purposes, ranging from enhancing cinema projectors and lenses to adorning luxury goods and design pieces. Moreover, its remarkable light-absorbing capabilities hold promise for revolutionising the efficiency of solar panels and cells.

Sharing is for the poor

Sadly, you can’t go to your local hardware store, pick up a litre of Vantablack paint and transform your kitchen into a black hole. That’s because Surrey NanoSystems does a great job of controlling access to Vantablack, outright refusing to supply it to private individuals. Samples are provided only for applications that the company deems “valid” (like when BMW was allowed to cover a whole X6 in Vantablack for the International Motor Show in Germany in 2019).

And yet, by some method of persuasion, the British artist Anish Kapoor managed to get Surrey NanoSystems to sell him the exclusive rights to use Vantablack S-VIS, a sprayable version of Vantablack, in artistic applications. As you can imagine, artists around the world were less than impressed that Kapoor could be allowed to corner the market on what is essentially a colour, thereby prohibiting everyone else from using it to make art. Many felt that Kapoor was given access to Vantablack due to his immense wealth and fame, rather than his artistic merit, and those critics decried what “more talented artists” could do if they were given access to the same materials.

The capitalist readers in the audience will remind us that Surrey NanoSystems is a business, and this is how business works: the highest bidder always wins. Yet there is undeniably still an emotional pull and a feeling of unfairness that kicks in when someone monopolises something as intangible as a colour. Obviously we know that Vantablack isn’t a standard colour, and it requires much more time, skill and money to produce than the standard black pigment, which is why it holds more value. But still, that doesn’t erase the image of Anish Kapoor as the petulant child at the kindergarten table, holding onto the black crayon so that no-one else can colour with it.

Sooner or later, the other children at the table get tired of waiting for their turn. And in 2016, one artist decided to take a crack at Kapoor’s monopoly.

The revolution will be pink

Stuart Semple is a painter who has been mixing his own pigments since his varsity days. One of these pigments was a fluorescent shade of pink, which Semple dubbed “the pinkest pink”. Frustrated by the Vantablack situation, Semple introduced sales of The World’s Pinkest Pink pigment through his online store in 2016, accompanied by the following caveat:

“By adding this product to your cart you confirm that you are not Anish Kapoor, you are in no way affiliated to Anish Kapoor, you are not purchasing this item on behalf of Anish Kapoor or an associate of Anish Kapoor. To the best of your knowledge, information and belief this paint will not make its way into the hands of Anish Kapoor.”

Of course it didn’t take long for troops of equally-irritated artists to rally behind Semple and his pink. Orders began trickling in initially, then quickly escalated to a surge, and eventually, an inundation. Five thousand jars were demanded, prompting Semple to recruit his family for assistance in grinding ingredients and fulfilling orders.

Artists who bought Semple’s pink went on to create art with it, and shared their pink creations online under the hashtag #sharetheblack. For anyone out of the loop at that time, it must have been a twilight-zone-esque experience to see so many people on the internet making art with pink while talking about black.

Of course it was only a matter of time before Kapoor rose to Semple’s challenge and got his hands on a tub of The World’s Pinkest Pink. And when he did, he promptly did this:

Nothing stays exclusive forever

For the longest time, Kapoor appeared to be doing nothing with Vantablack aside from hoarding it, which obviously didn’t endear him any further to his fellow artists. In the meantime, Semple kept at his one-sided feud, developing The Glitteriest Glitter as well as a cherry-scented superblack pigment called Black 2.0, both of which – you guessed it – were available to buy by anyone but Anish Kapoor. After Black 2.0 came Black 3.0, and then Black 4.0, which is capable of absorbing 99.96% of visible light. And unlike the highly technical, expensive and difficult-to-work-with Vantablack, Semple’s Black 4.0 is non-toxic and can be applied with a normal brush. It costs only $49.99 for a 150 ml bottle and can be bought online in just a few clicks.

It seems like too much of a coincidence that Semple went live with sales of Black 4.0 right before the debut of Kapoor’s first ever collection of Vantablack paintings at the Venice Biennale in 2022. The works on display apparently took 10 years of experimentation, scientific collaboration and careful application to create, which is how Kapoor is justifying selling each of them for £850 000 ($1.04 million, or roughly R20.03 million).

Spite is a powerful motivator. And while Stuart Semple will never make nearly as much money from his pigments as Anish Kapoor will make from selling one Vantablack painting, he will go down in history as the man that made the blackest black available to everyone.

Everyone except Anish Kapoor, that is.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AngloGold enjoyed a much stronger six months (JSE: AGL)

The second half of the financial year more than offset the first half

After the first half of the year ended December 2023 saw AngloGold report a free cash outflow of $205 million, shareholders will be relieved to know that the second half of the year was a free cash inflow of $314 million. This was thanks to an increase in production of 15% and a decrease in cash costs per ounce of 9%. It also helps that the average gold price moved higher in the second half of the year.

Other good news includes the important gold discovery made in Nevada in the US, which the CEO of the company refers to as the largest new discovery in the US in more than a decade. Of course, that’s also a great part of the world in which to strike gold – literally!

Perhaps the Bytes ex-CEO struggles with reading the rules? (JSE: BYI)

Or just doesn’t care?

With the news of Neil Murphy resigning suddenly at Bytes, the market started speculating about what the cause might be. We still don’t actually know. What we did learn at the time of the announcement is that there were undisclosed trades in the company shares.

Now, when this happens, it’s usually an isolated oopsie. Not so for Murphy.

There are well over 100 individual trades over the past three years that weren’t disclosed. He merrily bought up lots of shares in 2021 – 2022 and started selling them in 2023, all without telling the market.

I’m not sure what the punishment is for this, but it really is a pathetic situation that deserves the maximum possible punishment. There’s no point in having rules if people can break them to this extent.

City Lodge’s margins are under pressure (JSE: CLH)

I have great respect for the strategic pivot in this business in the post-pandemic period

The City Lodge management team really has done a lot to try and mitigate not just the way the pandemic changed behaviour, but also the ongoing challenges of operating in South Africa. There’s unfortunately only so much that they can do, particularly with an offering that still has a business travel angle. When you’re competing with Zoom and Teams as an alternative, you have a more cost sensitive customer than in the leisure travel space.

The six months to December 2023 is being compared to a period that was also free of COVID restrictions, so this is a proper view on the business. Occupancy moved higher from 57% to 61%, which speaks to some normalisation in consumer behaviour and solid resonance with customers, particularly as this is 600bps higher than the same period in 2019. Accommodation revenue is up 16%, with an increase in average room rates of 9%.

The food and beverage side is where the company has done particularly well, with revenue up 36%. This part of the business has been the major strategic pivot and now contributes R188.5 million in revenue vs. R806.7 million on the accommodation side. Food and beverage gross margin increased from 56% to 59%. Bravo!

The not-so-local-is-lekker part of the story is that total operating costs were up 11% per room sold and 19% overall. Substantial inflationary pressures on staff and property costs are a big part of the blame.

So, despite all the hard work, HEPS is only up by 10%. The group must be feeling more confident about the operating environment, with the dividend up by 20%. It seems as though trade in January and February is largely positive despite a slow start to the year.

Someone didn’t like what they saw in this update, with the share price down 7.7% for the day.

The turnover numbers at Dis-Chem look solid (JSE: DCP)

A trading update has been released that shows double-digit growth

Despite all the troubles for South African consumers, the health and beauty / pharmacy combination continues to work. You can see it not just at Clicks and Dis-Chem, but also the pharmacy businesses within other retailers e.g. at Spar.

The latest update is from Dis-Chem and it deals with the period from 1 September 2023 to 28 January 2024. Group revenue is up 12.2%, with an 11.2% increase in retail revenue and a 20% increase in external wholesale revenue.

Within retail, like-for-like revenue growth was 8.2% and selling price inflation was 6.8%, so volumes moved higher. On the wholesale side, total revenue (i.e. including internal customers) increased 11%, with externals up 20% as already noted and internal sales up 9.4%. They also specifically mention wholesale revenue from independent pharmacies, which increased 24.8%.

Revenue growth at The Local Choice was 14.5%, with the group now boasting over 200 franchise stores – up from 165 a year ago.

Mustek’s profits have more than halved (JSE: MST)

The share price closed 8.7% lower on the day

Mustek released a trading statement dealing with the six months to 31 December 2023. It’s not pretty, with HEPS expected to be between 55% and 65% lower than the comparative period.

The culprit? There are a few of them, actually. Aside from the general local economic conditions, there was a decline in the sale of green energy products vs. a strong comparative period. Whether this is due to more competition in the space or other reasons, we don’t know. Higher interest rates also impacted finance costs.

HEPS is expected to be 77.61 cents to 99.78 cents. The net asset value per share will be between R27.20 and R27.30, up from R25.75 as at 31 December 2022. The share price closed 8.7% lower at R11.23.

Quantum Foods seems to be navigating the HPAI outbreak (JSE: QFH)

Some of the relief has come from reduced load shedding

Quantum Foods has released an update on trading conditions for the four months ended January 2023. It says something about how bad load shedding was last year that the company is pulling off a better result than before, despite the outbreak of HPAI and all the difficulties that brings.

Some of the mitigating strategies included the importation of layer hatching eggs and the contracting of independent egg production farmers in geographical areas where the HPAI risk was lower. Despite these efforts, the egg supply was 60% down vs. the prior period. Egg prices were up more than 60%, so that managed to offset much of the revenue pain. It didn’t fix the cost problems though, as a large dip in supply means an under-recovery of overhead costs.

Egg production in South Africa is expected to remain muted for the next six to eight months and the HPAI risk is high.

On the broiler farming side, the Western Cape business improved significantly as the migration to Ross 308 genetics was completed before the start of the current period. Elsewhere in the country, the news wasn’t so positive – like in Hartbeespoort where operations were affected by HPAI.

In the feed business, the lower demand within Quantum because of HPAI impacted sales volumes. Total volumes fell by 14% vs. the prior period.

In the businesses in the rest of Africa, the company managed to navigate the more usual challenges (like feed costs) and took advantage of a solid recovery period that saw these businesses contribute “satisfactorily” to the company’s financial performance.

Sibanye has concluded the Section 189 process (JSE: SSW)

The job losses in the PGM business are lower than they could’ve been, at least

Sibanye-Stillwater has wrapped up the s189 process in the local PGM operations that was announced in October 2023. Initially, 3,500 employees and 595 contractors were expected to be affected.

For now, the 4B shaft is being allowed to continue operations, provided there are no losses. This employs 1,496 employees and 54 contractors. Natural attrition of 467 staff helped reduce the impact further. 351 employees accepted transfers elsewhere within the group to fill vacancies. 1,281 employees were granted voluntary separation or early retirement packages. 47 employees were retrenched and 805 contractors were also impacted.

Thungela: another example of cyclical profits (JSE: TGA)

What went up has certainly come down

Eventually, investors will learn not to buy resources companies on high trailing dividend yields. Inevitably, it leads to a scenario where the dividends over a period of time aren’t even enough to offset the capital losses caused by a change in the cycle. Thungela peaked at over R375 in September 2022. Fast forward barely 18 months and the share price is R106.

A trading statement for the year ended December 2023 gives us a clue why. HEPS has decreased by between 72% and 76% and this is despite consolidating 85% of the results from the Ensham business since 31 August 2023.

Detailed results are expected to be released on 18 March.

Little Bites:

Director dealings:

The CEO of Datatec (JSE: DTC) has bought shares worth R2 million.

JD Wiese (yes, of that Wiese family) is a non-executive director of Collins Property Group (JSE: CPP) and has bought shares worth R367k.

An associate of a director of Huge Group (JSE: HUG) has bought shares worth R3.5k.

Shareholders of Textainer (JSE: TXT) have approved the merger proposal from Stonepeak.

Sasfin (JSE: SFN) announced amended terms for the disposal of the Capital Equipment Finance and Commercial Property Finance businesses to African Bank. Long story short, there are some amendments to conditions precedent and a couple of loan receivables have been excluded from the deal. This is a Category 1 deal and a circular will need to be sent to shareholders. The JSE has given the company an extension until 29 March.

In a good example of spraying a water pistol towards the sun and hoping it makes an impact, the JSE has censured Carl Grillenberger based on closed period trades at the end of 2022 in Advanced Health Limited shares. The company is no longer listed anymore and there’s no financial penalty for this, so I strongly doubt he cares about a public censure.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")