It’s not called “a golden age” for nothing! The gold sector is absolutely cooking at the moment, with money just about falling out of the sky on a daily basis for the large mining houses.

AngloGold Ashanti is just the latest example, with numbers for the quarter ended March 2026 reflecting record free cash flow of R1.2 billion.

Although production was only 1% higher year-on-year, free cash flow increased by 190% to $1.2 billion (vs. $403 million a year ago). This was thanks to a 69% increase in the average gold price received.

They refer to “controllable costs” reducing by $22/oz thanks to various operating initiatives that offset residual operating cost pressures. But once you add in exchange rates and higher royalties, cash costs increased by $168/oz to $1,391/oz – that’s a 13.7% increase.

With the gold price moving so much higher though, cash margin jumped from 57% to 71%. Like I said: a golden age!

With three months of the year behind them, full year guidance for production, costs and capex is unchanged. In the meantime, shareholders can enjoy a record interim dividend and a share repurchase programme of up to $2 billion.

Greencoat Renewables could do with more wind (JSE: GCT)

They really need to make a trip to Cape Town

Greencoat Renewables has released a quarterly update for the three months to March 2026. The net asset value per share has ticked up by €0.50 to €0.995.

Net cash generation for the quarter was in line with budget and equated to 2.4x dividend cover. This allowed them to easily handle the Q1 dividend of around €0.017 per share.

Power generation was 10% below budget though, with 6% attributed to low wind resources. It’s mildly ironic writing this while I listen to a massive storm in Cape Town. Perhaps it really is time that Greencoat looked at opportunities down here?

Although they are running at 52% gearing at the moment, there’s a decent amount of cash on the balance sheet and they have even been doing share buybacks.

They’ve also made progress with their Green Digital Infrastructure Platform, which acquired its first asset.

Pan African Resources is making progress with the Emmerson acquisition in Australia (JSE: PAF)

The scheme booklet has been sent to Emmerson shareholders

Pan African Resources is looking to acquire 100% of the listed shares in Emmerson Resources in Australia. As part of this, Pan African will look to list on the Australian Securities Exchange (ASX), making it much easier to get shareholders in Emmerson across the line on this share-for-share deal.

It’s only a Category 2 transaction for Pan African Resources, so a circular isn’t necessary and neither is shareholder approval. But on the other side, Emmerson shareholders need to give 75% approval to the transaction.

Pan African has highlighted the pro forma financial information in Emmerson’s scheme booklet (the Australian equivalent of a circular). It shows that the enlarged group would have a net asset value per share that is 28.35% larger than the current level at Pan African.

The meeting of Emmerson shareholders is scheduled for 15 June. If you would like to check out the scheme booklet, you’ll find it here.

Sea Harvest bids farewell to Ladismith Cheese (JSE: SHG)

With this deal out of the way, the company is more focused

Sea Harvest, as the name suggests, has its DNA firmly in the ocean. They are a large and important fishing group, although the volatility of that sector had previously led them down a path of diversification.

It’s almost always better for a company to focus on its core strengths than to diversify for the sake of it, so I think the company has done the right thing by disposing of Ladismith Cheese. The deal was announced at the end of 2025 and has now closed thanks to the receipt of Competition Commission approval.

If you’re keen to understand more about the company, including the initial entry into Ladismith Cheese and how the proceeds will filter into the group’s capital allocation policy, then you’ll enjoy the podcast I recorded with Sea Harvest in March. CEO Felix Rathed and Muhammad Brey delivered exceptional insights that you’ll find here.

The Foschini Group’s 50% off sale – in its share price! (JSE: TFG)

Things are going from bad to worse

The Foschini Group (which we can refer to as TFG for our collective sanity) has seen its share price roughly halve in the past 12 months. The good ol’ “50% off sale” is what you want to see at end of season, not when you look at the share price chart!

There’s not much indication of things getting any better, with the company releasing a trading update dealing with the three months to 28 March 2026.

In TFG Africa, sales were up 7.5% in total and 5.5% on a like-for-like basis. For the full year, sales increased 5.0% in total and 3.5% on a like-for-like basis. This may sound like a great acceleration towards the end of the year, but sales growth is only one part of the equation.

The other is of course margin, with TFG Africa’s EBIT for FY26 declining at a mid-teens percentage rate. There was some margin recovery in the final quarter, but it clearly wasn’t enough to make up for the awful numbers in the rest of the year.

To make it even worse, TFG Africa is the highlight of the numbers.

TFG London, one of the headaches, suffered flat sales for the year if you exclude the acquisition of White Stuff. If we isolate that acquisition, then pro forma sales growth was 4.3%.

TFG Australia is rapidly becoming another meme, just like Woolworths‘ (JSE: WHL) misadventures with David Jones in the land of animals that want to kill you. Sales fell by 1.3% for the quarter and 1.5% for the year. On a like-for-like basis, sales were down by a shocking 3.4% for the full year.

The trading update doesn’t give specific movements in profit for TFG London and TFG Australia individually, but it’s not hard to guess the direction of travel. The presence of large non-cash impairments in both businesses is another strong clue that all isn’t well.

Add it all together and you get a group performance (excluding White Stuff) of just 2.8% growth in sales. And at HEPS level, there’s a shocking drop of between 30% and 40% for the full year.

TFG Africa is doing all the heavy lifting here, but acquisitions over the years have led to the local business contributing only 68.3% to group turnover.

This is a prime example of “diworsification” instead of diversification, as TFG Africa’s modest positive momentum is being more than offset by the international businesses.

The other big risk is that management distraction in faraway lands can easily contribute to underperformance in TFG Africa, the one part of the business that actually has a right to win in its market.

What do you believe needs to happen here?

Results of previous poll:

Nibbles:

Director dealings:

A prescribed officer of African Rainbow Minerals (JSE: ARI) sold shares worth a meaty R34.8 million. Separately, two directors of different group subsidiaries sold shares worth R16.3 million in total.

An entity associated with Marcel Golding, the CEO of Rex Trueform (JSE: RTO | JSE: RTN) bought “N” ordinary shares worth over R2.5 million.

A director of a major subsidiary of Kumba Iron Ore (JSE: KIO) sold shares worth R97k.

A number of Anglo American (JSE: AGL) directors bought shares by reinvesting their dividends. Ditto for British American Tobacco (JSE: BTI) directors. These dividend-related trades don’t carry nearly as much weight for me as buying shares outside of the dividend cycle. I’m just mentioning them for the sake of completeness.

Araxi (JSE: AXX) received resounding approval from shareholders for the transaction to acquire an 80% stake in Pay@ Group. Just as importantly, the Competition Commission has unconditionally approved the acquisition. They will now work to get the final conditions across the line, with the big ones out of the way.

Sibanye-Stillwater (JSE: SSW) is having no difficulties in the debt market. The company priced an oversubscribed offering of $500 million in senior notes due 2031. The coupon on the notes is 6.25%. This five-and-a-half-year debt is being used to fund the repurchase of notes due in 2026 and 2029. Overall, the group is planning to reduce gross debt by 50% over the next two to three years.

Finbond (JSE: FGL) has released a trading statement for the year ended 28 February 2026. HEPS is expected to swing positive, moving from a headline loss per share of -1.9 cents to a profit of at least 2.9 cents. The share price is R1.09 though, so this profitability is still marginal relative to the share price.

Newpark REIT (JSE: NRL) has very thin trade in its stock, but it owns some really interesting and iconic buildings in Sandton. The company initially expected the dividend per share for the year ended February 2026 to be in line with the revised funds from operations per share of between 41.50 and 48.50 cents. But thanks to lower than expected operating costs, the dividend will actually be 50.07 cents for the year. This is unfortunately still a decrease of 36.1% vs. the prior year.

JSE Limited (JSE: JSE) – the company that is listed on its own exchange – announced a couple of changes to roles on the board. The big one is that Ian Kirk has been appointed as lead independent due to the retirement of Ben Kruger.

This isn’t something you can invest in directly (well, not yet at least), but African Bank’s deal to buy the home loan book from Eskom Finance has fallen through. African Bank is putting a positive spin on it, with the board deciding to focus on pursuing growth from the acquisitions made between 2022 and 2025. I must point out that the bank has a new CEO, so perhaps the change in management during the implementation of the deal has led to its demise. This wouldn’t be uncommon, as CEOs aren’t always happy to inherit the deals of their predecessors.

The modern lawn is more than just a patch of grass. It’s a story we’ve been retelling for centuries.

Winter is bearing down on Cape Town as I write this article, and while it may not be my favourite season, there is one thing about it that I love: for the next few months, I won’t have to water my lawn.

In the height of the dry summer, I have to set reminders on my phone so I don’t forget to go out and drag hosepipes and sprinklers across the grass (for the eco-conscious readers – don’t worry, it’s borehole water), and then set more alarms in 40 minute intervals so I don’t also forget to go out and reposition said sprinklers.

I’m always either neglecting my grass to the point that it turns yellow or overwatering it to the point that it turns yellow. So when winter comes around, I breathe a sigh of relief, sit back and let nature take care of the watering schedule for a while.

Ubiquitous though it may be, grass certainly didn’t earn its popularity by being a low maintenance addition to the garden. That’s probably why so many of my neighbours are defecting to astroturf – none of the watering or mowing required, and if you turn your head and squint at it from a distance, it kind of looks like the real thing. I can’t fault the logic, but there’s just something a little too dystopian about a plastic lawn; it gives me the shivers.

How did we get to the point where most of our outside spaces are dominated by a singular plant species? It won’t surprise you to learn that there’s an interesting story there.

An idea as old as grass

Before they were bestowed upon homeowners as part of their private property, lawns were in fact a communal thing.

The first “lawns” were probably what we would call village greens or town commons. This is a concept that developed in England during the Middle Ages, and the use case back then was more practical than decorative. Villagers found it useful to have a central green space where animals like cows, sheep and horses could be gathered overnight in order to protect them from wild animals or human thieves. By day, an open green space came in handy for setting up markets and conducting trade.

Any animal that belonged to a villager had the right to graze on this communal pasture; as a result, the perpetually-getting-eaten grass was always at a cropped length. In time, this short-length grass became known as lawn.

Very soon, those who lived outside the village – the aristocracy in their castles – adopted the idea of lawns as well. There were multiple reasons why this made sense for them: for one thing, it kept their livestock grazing close to home, right outside the castle walls, where they were easier to keep an eye on. A lawn dotted with peacefully grazing animals also did good things for the landowners image, as it aligned them well with the pastoral images of sheep and shepherds so often mentioned in the Bible. Having sheep grazing outside your castle was therefore considered a sign that you were a good and pious Christian.

And then there was the downright practical fact that enemies approaching your castle were that much easier to spot if they were trying to sneak up on you over a closely cropped lawn versus, say, from a densely wooded forest. Clear the trees, clear the view of trouble approaching.

Popularity up, practicality down

Fast forward a few centuries to the 1700s, and the popularity of lawns was only going up. Thanks to their adoption by the aristocracy in the Middle Ages, flat expanses of grass had gained a powerful aspirational appeal.

This appeal was fanned by the fact that nobles soon tired of having their lawns maintained by animals, as was the original, mutually beneficial arrangement. The height of luxury now was having the ability to stroll across your grounds without encountering a grazing animal (or a grazing animal’s droppings).

So lawns stayed, but the animals that maintained them got put out to pasture (quite literally). But then what was going to stop the grass from growing to knee-grazing lengths? Well, people, of course. Not the nobles themselves, but people they employed, similarly to how they employed people to pick fruit in their orchards or harvest barley in their fields.

Herein lies the flex, as we Millennials like to say. Much like today, land in the 18th century was a signal of wealth. The more land you had, the more food you could cultivate, animals you could keep, or mills you could put up. All of the work that went into your land produced things that you could either eat or sell, and that was why you were rich.

Now imagine you have fertile land, and you use it to grow something that adds absolutely no value beyond its aesthetic. You cannot eat your lawn or cut it down and sell it. In fact, keeping it costs you money – you have to water it regularly and then pay someone to cut it down with a scythe once a fortnight so it continues to look nice.

To someone living through the 18th century, seeing a rolling expanse of lawn implied one thing: that the landowner had so much land and so many resources that they could afford to waste some of it on something as useless and demanding as grass. It was the horticultural equivalent of spotting a golden Rolex on someone’s wrist.

Remember, even back then, grass was hard work – one could argue that it was probably even harder work then than it is now, because sprinkler systems and lawnmowers hadn’t been invented yet. A lawn was therefore as much a symbol of wealth as it was a symbol of the landowners ability to (pay someone to) control nature, exert power over it and shape it to their will.

Grass goes global

If we accept that lawns were first conceptualised and idealised in the Northern Hemisphere, then how did they manage to spread all over the world? Well, as it happens, the British were on somewhat of a world tour between the 16th and 17th centuries, and adding many exotic colonies to their collection along the way.

The British lawn fetish was transferred to these new colonies through a number of turf-based British sports like cricket, football, rugby and golf. Before long, lawns were springing up in places like India and North America – climates that were not necessarily ideal for a plant species that required a temperate climate and a steady supply of water.

With every apparent restriction that nature tried to put on the growing of grass, humanity doubled down on our desire for it. Consider the fact that, from a climate perspective, the USA is actually a very hard place to maintain a green lawn. Approximately 40% of the continent is arid or semi-arid. 70-75% of the continent gets winter snow, with around 50% receiving significant amounts of it.

While it isn’t technically impossible to grow grass under these conditions, it takes a lot of resources to do so – significantly more so than it would to grow indigenous plants that are adapted to each region’s climate and soil. Yet to this day, a green lawn is an unshakeable part of the American Dream™ (white picket fence sold separately).

Is the grass still greener?

Lawns were never about practicality or ecology. They were never even really about grass. They were about signalling.

First, it was the signal of order in a chaotic world: a neatly cropped space where animals gathered and communities met. Then it became a signal of power: land cleared to expose enemies, to project control, to frame a castle just so. Later, it evolved into a signal of wealth: land so abundant it could be rendered useless, labour so cheap it could be spent maintaining something purely ornamental.

That signal survived the centuries. It followed ships across oceans, embedded itself in suburban dreams, and arrived here, in a water-scarce corner of Cape Town, borehole-water hosepipe in hand.

Because if you strip it back, the modern lawn is a kind of default setting we rarely question. We water it, mow it, fertilise it; not because it makes sense, but because it’s what a “proper” home is supposed to look like.

But what exactly are we trying to prove? That we have control over nature? That we can afford the water? That we belong to a centuries-old aesthetic rooted in European climates and aristocratic ideals?

So maybe the question isn’t why lawns are a thing.

Maybe it’s: why are they still?

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

Her first book, Lessons from Loss, has been published by Penguin Random House.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Altron has tightened up its earnings guidance (JSE: AEL)

And the numbers look good!

Altron has released an updated trading statement for the year ended February 2026.

In their initial trading statement released in February, they had guided an increase in HEPS from continuing operations of at least 30%, and a jump in HEPS from group operations of at least 50%.

We now know that the increase in HEPS from continuing operations will be between 31% and 37%. From group operations, HEPS will increase by between 68% and 74%.

This has been one of the most impressive turnaround stories on the JSE. Through various important corporate actions and an overall improvement in performance, they’ve achieved share price growth of 160% over the past three years!

Datatec is doing extremely well (JSE: DTC)

Understanding the momentum through the year will be important

Datatec has released a trading statement for the year ended February 2026. The numbers look spectacular, with HEPS expected to jump by between 51% and 58.8% (in US cents – the company’s reporting currency).

If you use underlying earnings per share, which excludes share-based payments, the increase is between 31.7% and 37.3%. This is to help make the results more comparable to peers. Either way, these are excellent numbers.

The results were driven by Westcon International and Logicalis International, with Logicalis Latin America experiencing only a slight increase in gross profit.

Something to note is that the interim period was actually even better. In the six months to August 2025, underlying earnings per share had increased by 43% and HEPS had jumped by 109.5%.

When detailed results are released on 26 May, the market will want to look at the momentum in earnings and figure out the reasons for the significant difference in H1 vs. H2 performance.

Gold Fields gives us great data points on inflation (JSE: GFI)

For now at least, the gold price is more than making up for it

With the first quarter of the financial year behind them, Gold Fields remains on track for full-year guidance.

They just achieved an increase in attributable gold-equivalent production of 15% year-on-year, so they are looking to take full advantage of favourable gold prices. The Salares Norte mine’s first full year of production is an important driver of this increase.

Quarter-on-quarter production figures fell by 7%, so that’s something to keep an eye on. There was also a jump in all-in sustaining costs (AISC) of 13% year-on-year and 9% quarter-on-quarter, with inflation as one of the drivers of higher costs.

They give excellent disclosure on some of the underlying inflationary pressures. It goes beyond just diesel, with other inputs like cyanide and LNG also increasing substantially.

If the oil price sticks at around $100/barrel, then Gold Fields forecasts an impact on costs of $40/oz to $50/oz on a portfolio level.

For now, the gold price is protecting them from this issue. Despite the dip in quarter-on-quarter production, revenue increased by 16% in this quarter vs. the three months to December.

The balance sheet is even healthier as a result. Net debt has decreased by 34% over the past 12 months. Net debt to EBITDA is just 0.19x now vs. 0.26x at the end of December 2025. It’s not hard to see why the company feels confident to do share buybacks.

As you would imagine at a group of this size and importance, there are many underlying projects underway. They have no fewer than 21 active projects in the greenfields portfolio, including 13 in drilling!

Sustaining capex for the year is forecast to be between $1.3 billion and $1.4 billion. They will also spend between $600 million and $700 million on growth capex.

Lesaka Technologies has raised FY26 guidance (JSE: LSK)

This is the kind of thing that investors want to see

Lesaka suffers from thin liquidity in its stock, which is why the share price closed flat on a day that probably should’ve seen some fireworks.

They released an update for the third quarter that reflected performance at the upper end of profitability guidance. They even raised guidance for FY26! But for whatever reason, the market wasn’t particularly interested.

If we dig a bit deeper, we find that net revenue increased by 16% year-on-year in rand terms. Adjusted EBITDA increased by 45%, so the shape of the income statement in response to that revenue growth is encouraging.

Operating income increased by a casual 804% – and yes, that means it was 9x higher year-on-year. Perhaps most importantly, they’ve swung from a net loss to net income.

The disappointment in the numbers is the Merchant segment, where net revenue dipped by 4%. This is exactly what the market doesn’t want to see, especially from the largest segment. Consumer revenue jumped 41% and Enterprise was up 78%.

Worries around the Merchant business aside, Lesaka’s other growth engines are firing on all cylinders. This has led to the increase in guidance, with adjusted earnings per share for the year ending June 2026 expected to be between R5.50 and R6.00.

This guidance still excludes the Bank Zero acquisition, which remains subject to regulatory approvals.

Life Healthcare’s share price landed up in the hospital (JSE: LHC)

The market hated the latest update

Life Healthcare dropped by a 11% on Thursday, after releasing a trading update that was heavily impacted by a medical scheme being placed into curatorship. Other online reports suggest that Sizwe Hosmed is the scheme in question.

Either way, paid patient days were down by 0.4% thanks to the loss in volumes from this issue. If you exclude the curatorship, then paid patient days would’ve been up by 0.9%. The market doesn’t seem to have been very interested in that argument though.

With revenue up by between 2.2% and 2.6% for the six months to March 2026, it’s surprising (and impressive) that the company managed to achieved normalised EBITDA growth of between 4.9% and 5.3%.

The increase in HEPS is unfortunately a useless metric, as the prior period was heavily distorted by the Piramal liability associated with the Life Molecular Imaging deal. Instead, it’s better to just look at the expected HEPS range from continuing operations of between 50.6 cents and 52.6 cents.

The company has wisely split out the LMI issues and given us a pro forma movement. This is the key metric to remember: HEPS on that basis has moved by between 0% and 4% for continuing operations.

The market was clearly looking for more.

Sappi goes from bad to worse (JSE: SAP)

The share price is plumbing new depths

I’ve been keeping an eye on Sappi to see if the share price would find some positive momentum and deliver excellent cyclical returns. My worry has been that this time, it really is different in the paper market.

First, let me show you what this chart looks like over the long term:

The idea here is to buy at the extreme lows, strap yourself in and wait for the cycle to turn.

But with the share price dropping another 13% on Thursday in response to the second quarter update, it’s clear that the market still hates this thing and is losing faith in its ability to weather the storm.

There are two major problems here.

The first is that the digital age is unfriendly towards paper, so a cyclical industry has perhaps transformed into an industry in structural decline.

The other problem is that Sappi’s balance sheet has taken more punishment than a northern hemisphere prop after 70 minutes against the Boks, so they are in no shape to actually deal with disasters like the spike in energy prices and a potential recession.

In the latest quarter, revenue dipped by 1% and adjusted EBITDA tanked by 51%. That is truly awful. They are now deep in the red, with a loss of $413 million vs. a loss of just $20 million a year ago.

Net debt is up 18% to just under $2 billion, with efforts to reduce capex proving to be insufficient to address the slide. I somehow doubt that lenders are sleeping very well at night right now, with the net asset value having decreased by 24% in the space of 12 months.

There are pockets of hope, like a 27% increase in North American paperboard volumes. But with selling prices under pressure and inflation assaulting their manufacturing margins, I think Sappi’s share price is going to plumb new depths.

This time, it seems to be different. But what do you think?

Southern Sun had a fantastic second half (JSE: SSU)

They are dealing with a difficult macroeconomic period from a position of strength

In the six months to September 2025, Southern Sun struggled with a 6% decline in operating profit and flat adjusted HEPS. But the second half of the year clearly told a very different story, as a trading statement for the year to March 2026 notes adjusted HEPS growth of a delightful 17% to 21%!

In case you’re wondering, HEPS on an unadjusted basis increased by 18% to 22%, so there’s not much of a difference there.

Strong occupancy levels were a major driver here, with overall occupancy of 62.9% vs. 60.8% in 2025. It’s certainly worth noting that the Paradise Sun in the offshore business had been closed for refurbishment in the first half of the year, so that’s clearly part of the H1 vs H2 skew.

The South African portfolio ran at 64.3% (vs. 61.9% in 2025), with demand driven by foreign inbound travel and demand in the MICE segment – Meetings, Incentives, Conferences and Exhibitions. The G20 in Gauteng was just one example in the second half of the year.

It’s more than slightly funny that a hotel group describes one of its key drivers as being MICE!

Mozambique still sounds like a difficult situation, with only marginal improvements in trading performance in the second half of the year. The company has also flagged the impact of the war in the Middle East, with oil prices making travel far more expensive.

They have a strong balance sheet to weather any storms, with net cash of R86 million. With the share price up 4.5% year-to-date, the market is shrugging off the risks and giving the management team the credit they deserve. The reality is that even the best management team in the world can’t do much about the cost of inbound travel skyrocketing, so I worry about the impact on the next financial period of the prolonged spike in oil prices.

Results of previous poll:

Nibbles:

Director dealings:

In the latest game of musical shares at the Wiese dinner table, various entities related to Dr. Christo Wiese and Adv. Jacob Wiese have entered into swaps and associated transactions over Shoprite (JSE: SHP) shares worth R943 million.

On such a busy day of news, MTN’s (JSE: MTN) update on the performance at MTN Uganda must land in the Nibbles. This is one of the smaller subsidiaries in the group, which is a pity as MTN Uganda has historically proven to be a dependable performer in Africa. But in the latest quarter, service revenue was up by only 7.7% and EBITDA margin actually declined by 180 basis points to 50.6%. Profit after tax dipped by 3.8%. Unlike in Nigeria and Ghana where MTN is growing rapidly in this environment, Uganda could only manage a “resilient” performance. This is why diversification is important.

4Sight Holdings (JSE: 4SI) – a small cap that behaves like a company that wants to be a large cap – announced some positive news around the X4 Group acquisition that they made in 2025. For the year ended February 2026, that business exceeded 110% of its agreed net profit after tax target of just over R6 million. These are small numbers in the greater scheme of things, but small successful deals add up very nicely over time. I’ve been very tempted to take a small position here.

Tharisa (JSE: THA) is in the process of transitioning to underground mining. The latest update is that the company has concluded a five-year contract with Cementation Africa regarding the underground mining development and construction work at the Tharisa mine. They refer to the contract as being structured on a cost-plus-fee basis with “aligned principles” rather than a “traditional rates-based, risk transfer model” – interesting! And if the name Cementation Africa sounds familiar to you, it’s because this company was acquired out of the charred remains of Murray & Roberts by Differential Capital and a consortium of investors.

Montauk Renewables (JSE: MKR) has released results for the quarter ended March 2026. They put literally zero effort into the SENS announcement, merely pointing investors in the direction of the SEC filing. They are still slightly loss-making despite a 9% increase in revenue.

Sebata Holdings (JSE: SEB), which is currently suspended from trading, has issued a cautionary announcement – just in case there are people who are willing to do off-market trades! Jokes aside, cautionary announcements are still a requirement even if the shares are suspended from trading. The reason for the cautionary is that the company has entered into negotiations with a non-related third party regarding the potential disposal of assets. They haven’t indicated which assets, or given any other information at this time.

Although PPC has not released any information to shareholders, and is currently not trading under cautionary, reports in the media suggest that Heidelberg Materials, a German building materials firm, is considering making a bid for the local cement maker. This is not the first time that PPC has attracted attention. Past suitors have included Fairfax Africa Investments, Holcim, Dangote Cement, CRH and AfriSam.

Diversified technology group 4Sight acquired X4 Solutions and XFour Technology in April 2025 in a move to expand its digital enterprise ecosystem and strengthen its footprint in workforce technologies. The acquisitions, which specialise in integrating and optimising HR and payroll systems in 20 countries across Africa, can tailor enterprise-grade offerings to the unique dynamics of the African labour market. The purchase consideration payable was split into two separate tranches with an initial payment of R21,2 million comprising equally of cash and share components. The second tranche, in the form of an earn-out of R21,2 million, was subject to the financial performance of the companies over the year to 28 February 2026, which the group exceeded, resulting in payment of the related earnout.

Burstone’s disposal of the rentable office property located at 2 Ncondo Place in Umhlanga in KZN to Pappamia for an undisclosed sum has been approved by the Competition Commission.

Unlisted Companies

Black woman-owned and managed Siyanqoba Ngamandla Engineering Services (Siyanqoba) has received undisclosed funding support from the Abadali Fund, a black Business Growth Fund which forms part of the Abadali Equity Equivalent Investment Programme (EEIP). The programme is an economic inclusion initiative by the Department of Trade, Industry and Competition in partnership with J.P. Morgan and managed by Edge Growth Ventures. The facility will enable Siyanqoba to acquire specialised mining equipment, expand its operational capacity and create additional jobs. Siyanqoba services the likes of Seriti Resources, Thungela and Glencor.

Pan-African infrastructure fund, the Africa50 Infrastructure Acceleration Fund which had raised US$300 million by the end of its third close in December 2025, is looking to add a further $100 million in the final round. The fund will invest in equity and quasi-equity in infrastructure companies and projects in Africa focusing on power and energy, transportation and logistics, water and sanitation, and digital and social infrastructure.

In August 2024, MC Mining signed an agreement with Kinetic Development Group (KDG) which would see KDG subscribe for shares in aggregate of 51%. The deal was structured to be completed in two tranches. The first tranche, completed in 2024 and equal to a 13.04% stake, was valued at the time at US$12,97 million (R230,88 million). The second tranche valued at $77 million (R1,43 billion) has now been completed, raising KDG’s shareholding in MC Mining to 51%.

This week the following companies announced the repurchase of shares:

During the month of April AIMIA repurchased and cancelled a total of 228,900 of its shares representing 0.3% of the company’s issued share capital. The shares were purchased at an average price of US$2.79 for an aggregate $638,344.

Quilter announced it would commence a share buyback programme to repurchase shares with a value of up to £100 million in order to reduce the share capital of the company and return capital to shareholders. This week Quilter announced the repurchase of a further 1,655,272 shares on the LSE with an aggregate value of £3,03 million and 59,963 shares on the JSE with an aggregate value of R2,46 million.

Ninety One plc announced the extension of its repurchase programme from 31 March 2026 to 3 June 2026. The shares to be purchased on the open market are cancelled to reduce the Company’s ordinary share capital. This week the company repurchased a further 732,914 ordinary shares at an average price 213 pence for an aggregate £1,277 million.

GreenCoat Renewables has implemented a share buyback programme totalling €100 million over 12 months with a first tranche amounting to €25 million beginning on 5 March 2026 – representing 13% of the issued share capital. This week 1,071,217 shares were repurchased for and aggregate €1830,378.

Anheuser-Busch InBev’s US$6 billion share buy-back programme continues. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 26 April – 1 May 2026, the group repurchased 1,017,064 shares for €64,12 million.

In December 2025, British American Tobacco extended its share buyback programme by a further £1.3 billion for 2026. The shares will be cancelled. This week the company repurchased a further 517,811 shares at an average price of £42.83 per share for an aggregate £22,18 million.

During the period 28 – 30 April 2026, Prosus repurchased a further 1,528,155 Prosus shares for an aggregate €62,21 million and Naspers, a further 515,869 Naspers shares for a total consideration of R460,58 million.

One company issued or withdrew a cautionary notice: Sebata.

Fintech platform, Kaleidofin, has closed Kenya’s first private-sector local currency securitisation in the smallholder agriculture sector, in partnership with Apollo Agriculture and with investment from the IDH Farmfit Fund. The transaction mobilised KES276 million (approximately US$2,5 million) through the securitisation of receivables originated by Apollo Agriculture, covering a portfolio of 23,839 smallholder farmers, 51% of whom are women, with an average loan size of KES 17,942 and approximately 22% first-time borrowers. Structured through Kaleidofin’s ki platform, a dedicated debt capital market infrastructure, the transaction enables the conversion of granular agricultural loans into investable assets for institutional investors.

Botswana-listed, African multinational financial services group, Letshego Africa, has announced the sale of 100% of the issued share capital of five of its East and West African subsidiaries to Axian Digital Venture Holdings and Management Limited. The subsidiaries, Letshego Ghana Savings and Loans PLC; Letshego Faidika Bank Tanzania Limited; Letshego Microfinance Bank Nigeria Limited; Letshego Rwanda PLC Limited and Letshego Uganda Limited were sold to the UAE-based company for an undisclosed sum.

Nigeria’s BFREE, a Pan-African debt recovery and distressed credit investor, has secured new funding aimed at expanding its ability to purchase bad loan portfolios from banks and digital lenders across Africa. The funding round was led by AfricInvest through its Financial Inclusion Vehicle (FIVE) and also included Algebra Ventures and existing investors Capria Ventures, VestedWorld, Axian CVC, Angaza Capital, and 4Di Capital.

Trafigura Pte Ltd. has entered into exclusive negotiations with the Egyptian Aluminium Company (Egyptalum) and the Metallurgical Industries Holding Company (MIH) to develop a new primary aluminium smelter in Egypt. The trio intend to establish a newly-incorporated company that will construct, own and operate a 300,000 tonne per annum primary aluminium smelter, alongside a 150,000 tonne per annum anode plant, at Egyptalum’s Nag Hammadi complex. The new facilities would nearly double the site’s current annual production capacity. Trafigura will participate as a minority equity investor in the new company, as well as a debt provider and long-term offtake and feedstock supply counterparty. Total investment costs for the project are estimated at between US$750 million and $900 million.

The Africa Ecosystem Catalysts Facility, a US$4 million pilot investment facility managed by Village Capital with funding from the Dutch Entrepreneurial Development Bank (FMO) and the Netherlands Enterprise Agency (RVO), has announced its first two investments in Ghana. The Facility is investing in Rivia Clinics, a tech-enabled primary healthcare startup ($200,000), and VDL Fulfilment, an e-commerce logistics platform built for African SMEs ($150,000), both based in Accra.

The Emerging Africa & Asia Infrastructure Fund (EAAIF) has committed a US$40 million senior secured loan to support the development of Egypt’s first sustainable aviation fuel (SAF) production facility. The $212,4 million project will be located in Egypt’s Sokhna Special Economic Zone and developed by Green Sky Capital Limited and its local subsidiary, SAF Fly Egypt. Once operational, the facility is expected to produce 200,000 tonnes per year of biofuels, including SAF, hydrotreated vegetable oil, bio-propane and bio-naphtha. Additional financing was provided by Qatar National Bank, through its Egyptian subsidiary, with a commitment of up to US$31,4 million, and by The Arab Energy Fund, which contributed $71,4 million.

Markets are moving fast but are investors moving with intent?

In this episode of No Ordinary Wednesday, we go beyond market headlines to unpack what investors are actually doing in a volatile, news-driven environment.

From trading the news cycle to navigating currency swings and concentrated markets, Investec’s Tinus Rautenbach and Bongani Nhleko share real insights from the Clarity platform, revealing where capital is flowing, how behaviour is shifting, and the risks investors may not see.

Listen now to understand the gap between perception and portfolio reality and what it means for your investment decisions. Read more on www.investec.com/now

Please scroll down for the transcript if you wish to read instead of listen.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Also on Apple Podcasts, Spotify and YouTube:

Transcript:

[00:00:00] Jeremy: Investors in South Africa are navigating a market shaped less by fundamentals… and more by reaction.

In recent weeks, geopolitical tension has driven sharp moves across oil, currencies and global equities. The rand has swung – weakening, recovering, and shifting again, often within days.

And yet, despite the volatility, equity markets have remained relatively resilient, with returns increasingly concentrated in a narrow set of sectors and stocks.

Because what feels like active decision-making is often just exposure playing out beneath the surface. A concentrated local market can mean portfolios are less diversified than they appear. And a volatile currency means offshore returns are driven as much by the rand as by the underlying assets.

So, in an environment like this, the real question isn’t just what markets are doing… but how investors are responding.

I’m Jeremy Maggs, and this is No Ordinary Wednesday – Investec’s podcast on what’s moving markets, shaping economies and influencing investment decisions.

In this episode, I’m joined by Investec’s Tinus Rautenbach, Head of Clarity, and Bongani Nhleko, Operations Consultant for Clarity – an online trading platform that provides instant access to local and global markets, in rands or foreign currency, with a low minimum investment.

Together, we’ll go beyond theory to unpack what investors are doing in real time, where capital is flowing, and the risks that may not be immediately visible.

Tinus, Bongani, welcome to No Ordinary Wednesday.

[00:01:43] Jeremy: So Bongani, I want to start with you. When headlines hit, whether it’s escalation in the Middle East or a sharp oil move, how do Clarity users react within 24 hours? Are they stepping into volatility or stepping away from it?

[00:01:59] Bongani: Well, what we usually see is a mix, but the dominant reaction is pausing rather than panicking. There’s an initial spike in connectivity as you’d expect, people logging in, checking their balances, scrutinising the share prices, but fewer impulsive trades than you might expect.

Some clients do step into volatility though, as you would expect from the more experienced traders who see it as an opportunity. The vast majority tend to wait, digest, and look for confirmation before acting.

[00:02:27] Jeremy: And I’m assuming that in a moment like this, timing as far as outcomes are concerned, means everything.

[00:02:34] Bongani: Yes, that is generally the accepted term. However, in this specific case, timing is more about sequencing not speed. The better outcomes usually come from investors who take a moment to see how the story evolves before reacting, because sometimes markets can often overshoot on the first move. Those who wait for direction rather than the drama tend to make more considered decisions.

You act too fast and your emotion can get in the way. You act too late and the markets already priced it in. The sweet spot is responding once the dust has settled.

[00:03:06] Jeremy: So Tinus, talking about drama despite intense geopolitical tension, equity markets, I think you’ll agree, have been relatively resilient, even hitting highs in some cases with gains concentrated though in a handful of sectors. So, here’s my question, if only a few sectors are driving returns, are we underestimating how fragile this rally actually is?

[00:03:27] Tinus: I think it’s fascinating to be in a world where we’ve got a war in the Middle East, we still have a war in the Ukraine on the go, we have got changing politics coming out of America by the minute or by the tweet, and it is interesting that the equity market is so resilient and robust. Having said that and looking at how concentrated it is, it does feel like it’s fragile, and part of that fragility you have seen in some big market moves over the last month, in the past six weeks, and so yeah, there is a bit of a fragility in the move.

It’s been very hard for the market to call whether this is a rally that will keep on going and it’s probably too soon to tell. The market is very excited whenever there’s any inkling of the Strait of Hormuz opening again. And, at the moment, the market is news-driven.

[00:04:17] Jeremy: And that’s the conundrum, then it’s the problem. We often talk about flight to safety in theory, so gold, dollars, bonds, but in practice, some investors don’t always follow the script. So, I’m interested to know what you’ve observed. Are investors following the textbook crisis path or are they writing their own playbook?

And is it driven by conviction or, as Bongani alluded to earlier, the speed of information?

[00:04:42] Tinus: The playbook has definitely changed, and the playbook we’ve seen is gold rally and essentially a dollar weakness maybe for the last 18 months or 12 to 18 months. That has played out outside of this loss – the crisis in the Middle East – and the playbook has maybe moved away from just purely looking at a single asset class as your safe haven towards clients looking at diversification. And we see clients instead of maybe going into a single asset class, going into ETFs or diversified plays, to be able to to weather the storm, and looking at various indices etc, to do that instead of just buying, as you say, gold or just trying to park in dollars.

Specifically between gold, dollars and bonds, the correlations have broken down, some of the narrative that used to be gospel is not gospel anymore. And so clients have definitely moved away from just blindly following the old about what to invest in when there’s risk. And the playbook has become more diversification across multi-jurisdiction, multi-index, multi-asset class.

And that’s been made much simpler through some of the products available now.

[00:05:54] Jeremy: So Tinus, if the playbook has changed, it’s all now about philosophy and mindset and I wonder then if investors are trying to trade the busy news cycle rather than investing through it. Does that behaviour actually add value over time, I wonder?

[00:06:11] Tinus: Picking up on what Bongani said earlier, we definitely have a spread of clients that we see that some of them are really familiar with both instruments and the market and are very comfortable to trade the news and to take a view on how they think things will play out. But we also have a big base of clients that are using investment as a real long-term play, and news cycles are less relevant. So, we are seeing a bit of both.

We’ve seen so many research articles showing that ad hoc trading around news usually destroys value instead of creating value, for most of your novice traders, but we see some experienced traders that enjoy trading the news cycles.

[00:06:53] Jeremy: Bongani, I’m coming to you in just a moment, but Tinus looking at the concentration of stocks, as we outlined at the beginning of this conversation, which we are seeing both locally and globally, I guess we’ve got to ask whether investors are diversified enough? Are they leaning into that or trying to diversify away from it, and which approach is then proving to be more effective?

[00:07:15] Tinus: We on average see that platforms nowadays give you easy access, both local and foreign diversified through, as I mentioned earlier, products like ETFs. We on average see accounts being well diversified, geography as well as industry. So clients are using the tools to easily diversify.

You might actually now get into a space where clients are over diversified and buying ETFs that hold similar stocks across, or similar indices across, and you’re not necessarily getting incremental value.

So, diversification is very good. It creates a different tool to deal with obviously the shocks and the volatility that we’ve seen, but we almost have to be a little bit weary of being too diversified, and they’re not necessarily getting the equity risk premium that you will get from owning stocks.

[00:06:53] Jeremy: So Bongani, let me push a little bit on diversification for local investors. Offshore exposure is often seen as diversification, but obviously returns are heavily influenced by the rand. Strategically then, how are they navigating this dynamic? Are they investing offshore for assets or for currency?

[00:08:24] Bongani: It’s honestly a bit of both. We see some investors are very deliberate about their offshore exposure. They want access to the global companies, the sectors, and the growth themes that they offer, which simply aren’t available locally. For them the asset comes first and the currency is almost a secondary benefit. What we’re seeing more recently is growing awareness of this trade off.

Though investors are starting to understand that offshore returns aren’t just about picking the right shares or stocks and ETFs, currency can amplify your gains just as much as it can mute it. So as a result, we’re starting to see investors have more realistic expectations of what the market can do for them, both on the stocks level as well as from a currency level.

People are thinking more consciously about when they want to go offshore and how much they want to allocate to their offshore allowance, and whether they’re comfortable with the currency swings being a major driver of their returns in the short term.

[00:09:18] Jeremy: Gentlemen, we are going to get back to the conversation in just a moment, but before we continue, I just want to touch more on Clarity by Investec.

It is a secure, straightforward investing platform designed for those who prefer to do it themselves.

It gives you direct access to local and global markets, with seamless currency exchange and share trading built in.

There’s no advice layer and no complexity – just the tools you need to invest on your terms, backed by the infrastructure and regulatory standards of a global bank.

Clarity by Investec. Investing, your way. Visit nowclarity.com for more information.

[00:09:55] Jeremy: Tinus, back to you then. Which sectors are seeing the biggest increase in interest on Clarity right now? And is that being driven by fundamentals or, as we’ve discussed a little earlier, the narrative?

[00:10:08] Tinus: At the moment, interest is driven by the narrative and not necessarily by the fundamentals. We have seen lots of activity in oil and oil- related exposure, which is fully expected. And so, at the moment, it’s more driven by narrative, I think. Interesting.

Just to touch on local or foreign narrative – as of the budget speech, South Africans can now take out R2 million under the SDA. It creates a lot more opportunity for clients to invest or makes it much easier to invest internationally.

And so it’s easier to get exposure to the BP’s, the Shells, to play this narrative. So, we’ve definitely seen a pickup in that.

[00:10:46] Jeremy: Which means Tinus, increase in activity in areas like commodities, energy, and even global tech. Given this current uncertain environment, is that positioning sustained or do you think it’s just short term?

[00:10:59] Tinus: Well, there’s no crystal ball here, Jeremy. I know you’d love to get the stock tip, but I think it’s harder to talk about the sustained runs or rallies.

Commodities and energy, ultimately, we’ll find a way to normalise because it drives inflation, and if inflation gets too hot, ultimately activity comes out of the GDP and out of industry, and therefore, demand will fall.

So, I think around commodities and energy, there’s a self-correcting process, and the cycle will correct itself if it runs too hot.

Global tech is a slightly different narrative. We all read a lot about AI and the advancements, etc, and a big part of the global tech rally is actually around –perceived correctly or not – increasing in productivity that AI can bring to civilisation as a whole.

And so maybe depending on whether we think it’s really overvalued or not, we’ll have different driving forces because you obviously can still see the massive productivity gains if some of the prediction around how the technology plays out comes true. So, some of it, I think, may be more sustained, but commodities and energy will have some self-correcting process to it.

[00:12:12] Jeremy: So Bongani, back to you then. Beyond equities, what instruments are gaining traction and what does this reflect? What are you seeing?

[00:12:19] Bongani: So, we’re seeing a growing interest in cash-like instruments on some defensive income-style assets. This tells us that investors aren’t necessarily bending all risk, but they’re rather becoming a little bit more selective.

There’s a clear desire for them to earn something whilst they’re waiting, rather than being completely all in or sidelined at the same time. We’re seeing quite a few people branch out into alternative investments, particularly cryptocurrencies. For some investors, crypto is viewed as a long-term hedge or diversification play rather than your short-term trade.

Alongside that, there’s also been a noticeable trend, as Tinus actually mentioned, toward AI-related investments. And whilst neither of us have a crystal ball here, it’s gaining a lot of traction. A lot of clients are trying to get all their hands on top of AI-related products, whether it be directly through companies or global tech companies that are actually producing these AI bots or agents as you may want to call them.

What we can see again is that there is some form of a structural trend that people are starting to see whether that’s going to be a long-term decision or long-term perception that holds or a passing cycle, we’ll only be able to know in a couple of years, I suppose.

[00:13:31] Jeremy: Tinus, back to you, and correct me if I’m wrong, but one of the risks I imagine in volatile markets is increased activity without improved outcomes. What are the most common mistakes that you are seeing right now?

[00:13:44] Tinus: I think it’s part of your old trading strategy, trading style, trading philosophy, “plan the trade and trade the plan”, and in high news flow environments like we have at the moment, trader individuals do tend to overreact, change their plan without necessarily going through the thoughtful process on why they’re in the position. What’s the target price for this position, what’s the stop loss for this position, etc.

So yes, we do see trading frequency, it’s news-driven. You’re a hundred percent right, not necessarily for better outcome. And the mistakes we’re seeing, it’s not different to any other news cycle, and that’s really to move away from the plan, the reason that someone got into a position and rather just get worried about the current year’s flow.

[00:14:31] Jeremy: And Bongani, I’m assuming that you are seeing a meaningful increase in trading frequency during this period of heightened volatility?

[00:14:39] Bongani: We certainly seeing quite a decent increase in trade and frequency, but it’s not uniform across all users, one could say, as myself and Tinus have been discussing earlier, we do have some of the more experienced traders who actually feel a little bit more comfortable, making those kind of decisions across periods of volatility.

Whereas other individuals or investors or long-term holding investors would prefer to wait and see how the market plays out in their favour.

Obviously, there would still be a lot more monitoring from their side because as Tinus did mention earlier, there’s quite a bit of news-driven narrative out there that are making people make hasty decisions, one would say, so a lot of the people who are inexperienced or the novice traders or investors obviously panic as soon as they hear that something is tanking or something’s dropping, or there’s some ridiculous news coming out there that shifts a specific industry.

The problem again with them is that their initial reaction is to get out immediately, as opposed to, as Tinus said, maybe, possibly just wait it out, figure out whether or not this is the position you want to hold, what’s your price point, when you’re going to get out.

So we do see increased activity from both sides, from experienced individuals and from the novice traders. However, there is something I want to stress though in terms of patience, because the distinction is quite important for an individual who’s wanting to hold a position versus somebody who’s immediately trying to get out because of a news-driven narrative.

And I said this distinction is quite important because it suggests a level of discipline. Increased awareness doesn’t always translate into increased action. In many cases, restraint is a healthy response. So, investors who tend to navigate volatile periods best are often the ones who stay well informed.

They reassess their positions, and they only act when something genuinely no longer aligns with their longer-term view.

[00:16:27] Jeremy: Tinus, there is a growing narrative around higher for longer interest rates and persistent inflation, you’ve both alluded to that. Are your users positioning for that reality assertively right now or still investing as if conditions will normalise quickly? And again, part of it is the crystal ball debate, I guess.

[00:16:49] Tinus: Yeah, I think we’ve definitely seen clients move some of their portfolios a bit more conservatively as the war in the Middle East began. And as you’ve seen and alluded to, the market has bounced off the lows and rallied hard.

And so some of our clients have definitely felt like they’ve missed out on some of the rally. Some of it has been to go into cash-like products as Bongani alluded to earlier. So yeah, we have seen it.

Clients are definitely positioning for this idea of high interest rates as inflation come through. Gone into a bit more defensive ETFs that doesn’t necessarily just give you, and I’ll talk about the S&P 500, for instance, but maybe more consumer defensive ETFs.

So yeah, we’ve seen it and clients are positioning for it. Are they too early? Well, if the war’s over tomorrow, would that mean inflation will normalise sooner? Or this scare of inflation won’t come through as bad as everyone’s predicting it at the moment with the high energy prices. Again, that’s the crystal ball.

[00:17:47] Jeremy: So Tinus, lastly then, against that backdrop, how should a South African investor interpret global conflict risk in their local portfolio?

[00:17:56] Tinus: We are quite lucky to be at the South of Africa at the moment. It feels like, at least from a safety point of view, we’re well removed from it. But how do you look at your portfolio?

We have definitely seen it over the previous five years there was a massive flight into dollar assets and how clients invest internationally. But with the top 40 in the South African index doing so well last year, stellar returns, we have seen clients coming back to having a more local flavoured portfolio, making sure that that balance is right between local and offshore. And as I said earlier, good, diversified portfolio will weather the storm.

[00:18:36] Jeremy: That is where we are going to close off today’s episode of No Ordinary Wednesday. Tinus, Bongani, thank you so much for joining me.

A new episode of No Ordinary Wednesday drops every two weeks. To ensure that you don’t miss out, search for Investec Focus radio SA wherever you get your podcasts and hit the follow button.

Until next time, goodbye from me, Jeremy Maggs, and the entire Focus Radio team.

Disclaimer: Clarity by Investec is a service offering of Investec Bank Limited, an authorised financial services provider, and over the counter derivatives provider, a registered credit provider, NCRCP 9, and a member of the JSE Limited.

In recent times, DRDGOLD has been greatly assisted by a gold price that has been moving sharply in the right direction. Focusing on gold tailings is a tough business, as they have to process plenty of ore to extract any gold whatsoever. If yields drop, or if access to material becomes difficult, then DRDGOLD’s margins can come under significant pressure at lower gold prices.

Thankfully for the company, “lower gold prices” seem to be a thing of the past. In an operating update for the quarter ended March 2026, the quarter-on-quarter move in the average rand gold price was 13%. To be clear, “quarter-on-quarter” means we are comparing this quarter to the immediately preceding three months (i.e. to December 2025), not to the quarter ended March 2025 (which would be a year-on-year move).

A 13% jump in that price over just three months is juicy. And it would’ve been even juicier if gold sales had increased. Alas, there was actually a 6% decrease in gold sales despite a 6% increase in gold production. The announcement doesn’t go into detail on this unusual mismatch.

With higher production comes greater efficiencies. Cash operating costs per kilogram of gold decreased by 4%. This means that total cash operating costs increased by 5% vs. a revenue increase of 6%, leading to adjusted EBITDA jumping by 21% as they unlocked an increase in margin. Remember, even a small difference in growth rate between group revenue and expenses can do great things for the margin in a company like this.

Further good news can be found in the capital expenditure update, where there’s a 16% decrease in capex on a quarter-on-quarter basis. But it’s worth noting that capex has been at elevated levels over the past nine months, jumping from R1.2 billion to R2.3 billion on a year-on-year basis. They’ve been investing heavily in their key projects, a necessary step to secure production of gold. Capex has now peaked though, so the company will no doubt be relieved that the gold price supported them throughout the capex programme.

If you want to see what happens when the market washes away from you during a period of heightened capex, just look at names like Sappi (JSE: SAP) and Gemfields (JSE: GML).

To end off on DRDGOLD, the balance sheet looks fat and happy with cash of R2.3 billion (vs. R1.7 billion as at December 2025). Although they have debt facilities in place, the company is currently free of debt as they haven’t drawn down on them. This bodes well for dividends, with the share price closing 8.3% higher in response to this update.

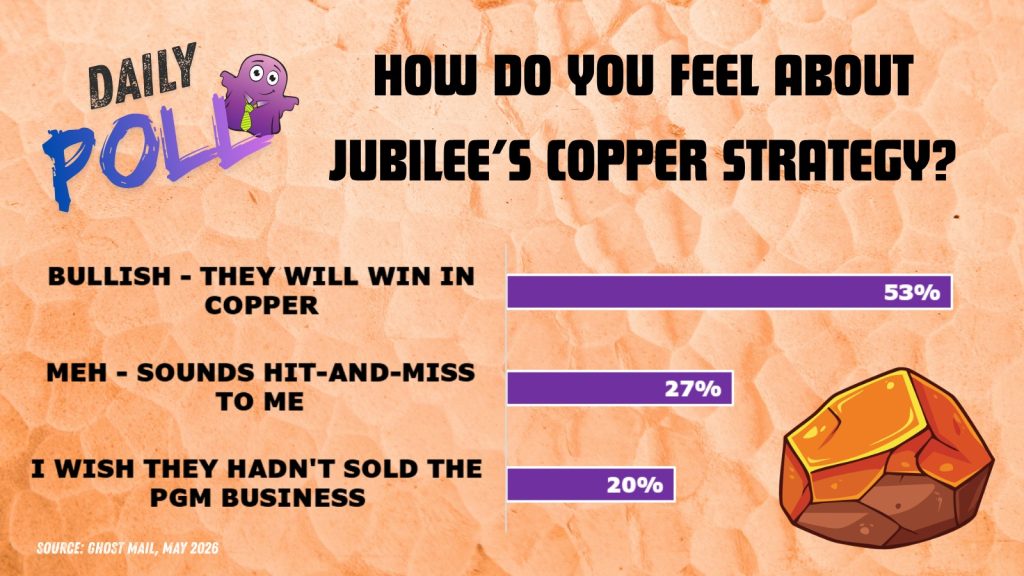

Production is up at Jubilee Metals, but guidance is a mixed bag (JSE: JBL)

Production guidance is “under review” based on recent developments

Jubilee Metals has released an operational and production update for the nine months to March 2026. With total saleable copper production for the period up by 28.7%, they are making progress on their strategy.

Production at Roan more than doubled, up 112.8% from the comparative period. Commissioning of the expanded Roan copper concentrate facility is near completion.

At the Molefe Mine, although there was a significant increase in ore mined and transported to the Sable Refinery, the announcement talks about interim numbers rather than nine-month numbers. I’m not sure if that’s just a typo.

Production at the Sable Refinery increased by 27.4% year-on-year. This is why the jump at Roan was watered down to a group increase of 28.7%.

Guidance for the year is an unusual situation. The company notes that it is currently “under review”, but they don’t make it clear whether it will be going up or down. The positive factor is the fast tracking of the expanded stripping programme at Molefe Mine, expected to be completed by July 2026. The negative factor is the delay in the commissioning and ramp-up of the expanded concentrate dewatering circuit at Roan, with targeted production expected to be reached in May.

The issue isn’t whether Jubilee Metals is increasing its copper production. The debate is around whether they are increasing it quickly enough!

This is despite a significant drop in average egg selling prices

People often talk about how food prices seem to head in one direction only. It certainly feels that way at the till for consumers, but the truth is that prices do sometimes go down.

In a trading statement dealing with the six months to March 2026, Quantum Foods noted that average egg selling prices fell by 9%. That’s good news for Eggs Benedict enthusiasts everywhere – like me!

Despite this, the company achieved HEPS growth of between 12% and 20%. The market would probably show some support for this if there was trade in the stock. Alas, liquidity is so thin that not a single share changed hands on the day.

As we’ve seen elsewhere in the poultry sector, the results were supported by important external factors like higher demand for poultry products in general, lower feed costs, and much less disruption from energy availability and avian influenza.

The egg business suffered a downturn in earnings as the price decrease more than offset the 4% increase in volumes. Thankfully, the feeds and broiler farming businesses registered an increase in earnings, while the layer farming business was stable. Earnings in the other African businesses are described as being significantly higher, with the exception of Mozambique.

It’s worth noting that head office costs increased in this period due to management incentivisation, so that’s something to look out for when the company releases detailed results on 22 May.

Things are going very well at Sibanye-Stillwater (JSE: SSW)

The latest quarterly update reflects incredible growth in earnings

With exposure to gold and PGMs as its primary commodities, Sibanye-Stillwater has enjoyed that rarest of rare things: an upswing in both commodity prices at the same time. At the right point in the cycle, these mining companies are basically a licence to print money.

In an operating update for the three months ended March 2026, Sibanye has delivered the incredibly happy news of a 371% spike in group adjusted EBITDA. Perhaps even more encouragingly, the positive contribution to earnings is across the group’s operations, rather than driven by just one area.

Prices have obviously played the major role here, with PGMs up 87% and gold up 49%. But you still need to get the stuff out of the ground, with a 2% increase in South African PGM production and stable local gold production. There was unfortunately a 5% decrease in production in the US PGM operations. Importantly, the US operation was profitable in this period, a huge swing from the losses seen a year ago.

In the recycling business, adjusted EBITDA jumped dramatically from under R200 million to nearly R1.6 billion. To put that in perspective, US PGM adjusted EBITDA was R777 million, or less than half of what they made from recycling. All of this pales in comparison to SA PGMs (R12.4 billion) and SA gold (R4.7 billion). It’s also worth touching on Century zinc, more than doubling year-on-year to R467 million.

The Keliber lithium project is an important strategic push by the business, with construction completed on schedule in this period. Negative adjusted EBITDA of R209 million is a feature of a development period – you have to spend money today in order to make money in future.

Trying to guess where these commodity prices will go is a risky game. There are myriad factors involved, ranging from jewellery demand in China (a key platinum driver) through to the more obvious stuff like catalytic converters and tariff risks. China is also a major factor in the lithium market, as are the supply and demand forces of AI-driven energy needs.

Sibanye can’t control external prices, but they can do their best to manage costs. Although all-in sustaining costs (AISC) per ounce was flat in the South African PGM business, it jumped by 15% in the South African gold business due to operating cost pressures and higher royalty taxes. The underground gold operations need to be managed carefully from a cost perspective.

The US PGM business needs to tighten up on costs, with AISC per ounce increasing by 14% year-on-year as production dipped. This is one of the hardest things about mining: when production falls, it’s a double-whammy as AISC inevitably increases and the margin per unit deteriorates.

With one quarter behind them, the company has left 2026 guidance unchanged. The share price closed 11.3% higher on the day.

Results of previous poll:

Nibbles:

Wesizwe Platinum (JSE: WEZ) is still trying to catch up on financial reporting and lift the suspension on the trading of its shares. They’ve released a trading statement dealing with the year ended December 2025, noting that HEPS swung from losses to profits – an increase of between 171% and 191%. The range is more useful than the percentage movement, with positive HEPS of between 8.64 cents and 11.08 cents. Results are due for release on 8 May.

Mantengu (JSE: MTU) has replaced the offtaker of its chrome. The legacy deal with RWE Supply & Trading seems to have had some difficult commercial terms around pricing, driving a negative impact on Mantengu’s numbers of R29 million in the previous interim period. The new deal with HMS Bergbau Africa (that sounds like the name of a ship!) has no such issue. Mantengu indicates that this commercial improvement should eliminate the recurrence of onerous terms, while delivering a route to market for Mantengu’s chrome.

ASP Isotopes (JSE: ISO) announced that subsidiary Quantum Leap Energy has further boosted its brains trust with the appointment of Dr. Peter Fiske to the strategic advisory board. Dr. Fiske comes with a long and impressive CV in the energy space in the US. It’s true that the company is being dressed up for its IPO, but it’s just as true that there is genuinely an incredible amount of talent in the organisation.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst.

Corporate management teams give a presentation and then we open the floor to an interactive Q&A session. I facilitate the Q&A alongside Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

In the 70th edition of Unlock the Stock, CA Sales Holdings returned to the platform to talk about the recent numbers and the strategic outlook for the business.

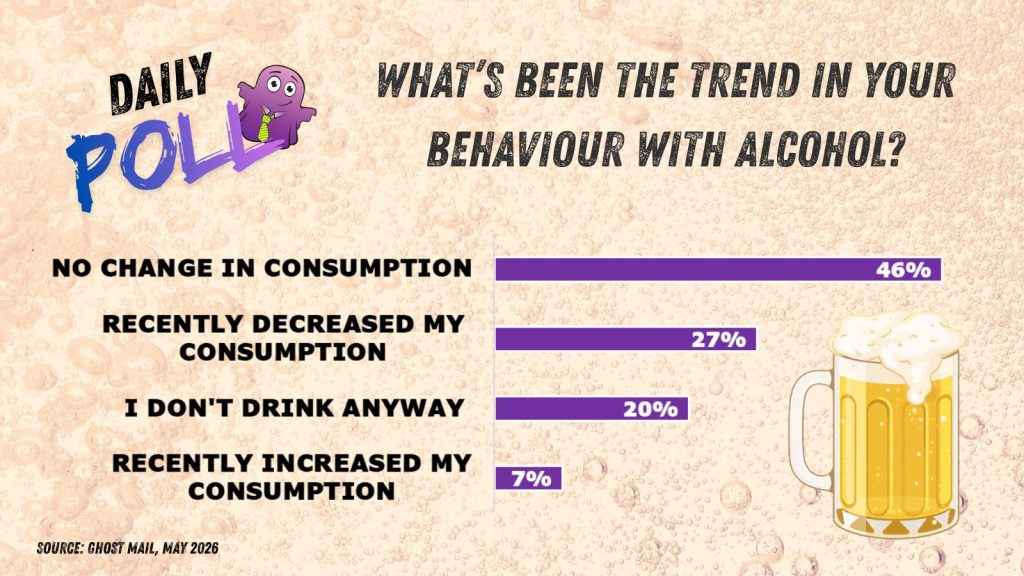

AB InBev’s beer volumes increased this quarter (JSE: ANH)

South America clearly hasn’t heard about the reduced consumption trend

Alcohol sales are a difficult thing to predict.

The recent narrative has been focused on the reduction in consumption by health-conscious adults, especially Gen Zs who seem to be drinking far less than prior generations. It’s not about cutting alcohol entirely – it’s about having three drinks instead of four. If everyone did that, consumption would drop by 25%!

I’m not exactly sure what has driven the latest uptick in beer volumes. It could be a low base effect. It could also just be a more stressful world, with people seeking out fun experiences to offset the constant barrage of negative news. Whatever the cause, AB InBev’s beer volumes increased by 1.2% in the latest quarter – and that’s a big surprise.

The market was caught off-guard by this news, with the share price up 8.3%.

But if we dig deeper, was this really because of alcohol consumption, or just the social pressure of wanting to drink something other than a soft drink? No-alcohol beer volumes were up 27%. I’m not a subscriber to the “all of the calories, none of the fun” camp, but each to their own.

There are also low calorie and even gluten free options these days. I won’t mention this to my dad – it’s not worth the trauma it will cause him.

Corona is still winning in the post-pandemic era, demonstrating that one of the best marketing tricks possible is for a global flu to be named after your product. Corona achieved 16% growth outside of its home market. Mexico, Corona’s home market, is still a very important source of growth for AB InBev. Colombia and Brazil reported record beer volumes, so South America doesn’t seem to be showing much interest in reducing their consumption. In stark contrast, it’s the “Beyond Beer” portfolio that was a meaningful contributor in the United States. Regional tastes make a big difference to performance!

Another important source of growth is the distribution capability. Their marketplace gross merchandise value jumped by 55% – and this is for sales of third-party products. Overall, the BEES marketplace was up 15%. This makes it a great driver of revenue and an important source of risk mitigation in terms of reliance on other ways to distribute product.

The increase in volumes, combined with price hikes, took revenue 5.8% higher in constant currency terms. It was up a delightful 12.0% as reported, with currency movements being highly favourable in this period.

Normalised EBITDA is a slightly less encouraging story, up by 5.3%. Normalised EBITDA margin contracted by 15 basis points to 35.6%.

By the time you reach the bottom of the income statement, you’ll find that constant currency earnings per share increased by 8.8%. There’s clearly some leverage in this thing below the EBITDA line.

There’s little doubt that the ESG consultants have been all over AB InBev, with terms like Balanced Choices and Beyond Beer. It sounds a lot like British American Tobacco (JSE: BTI). But what investors actually care about is the numbers – and with numbers like these, the share price will find support in the market.

And in case you’re wondering, South Africa achieved record high volumes, with Corona up in the mid-twenties. Premium beer brands are showing the strongest growth here, with Carling Black Label only achieving low single digit revenue growth.

What has been the recent trend in the consumption of alcohol by you and your peer group?

Kinetic Development Group is now the 51% holder of MC Mining (JSE: MCZ)

The second tranche of the subscription has closed

MC Mining has one potentially very good asset (the Makhado Project) and some scrappy stuff that is perhaps best described as being in damage control mode.

To make the Makhado Project a reality, they attracted Kinetic Development Group (KDG) as a major investor. This is a big deal and a strong show of faith in South Africa by a foreign investor.

With the latest tranche now completed, KDG has a 51% stake in MC Mining. A substantial $90 million has flowed into MC Mining over the course of the share subscription agreement.

MC Mining has also reminded the market that KDG brings plenty of operational and technical expertise to the table as well, being a leading global coal operator listed in Hong Kong. They have deep relationships in China, which will be helpful during the construction and commissioning phase.

KDG has appointed two directors to the board of MC Mining, so these aren’t just empty promises about contributing time and expertise in addition to the capital.

Thanks to the funding received from KDG, the Makhado Project is in advanced construction phase and is making progress towards commissioning and joint trial operations. They are targeting 800,000 tonnes per annum in hard coking coal and 700,000 tonnes per annum in thermal coal.

The share price closed 8.7% higher on the day. Although the market knew that the money was coming, there’s nothing quite like confirmation of money in the bank.

Results of previous poll:

Nibbles:

Director dealings:

The COO of Nedbank (JSE: NED) sold share awards worth R10.4 million. These relate to older schemes and the announcement doesn’t specify that the sale is for tax, so I assume that it isn’t.

Here’s some good news for shareholders in Aspen (JSE: APN): the company has received approval from the South African Health Products Regulatory Authority (SAHPRA) to release the first commercial batches of human insulin manufactured for sale in South Africa. The facility in Gqeberha is manufacturing this insulin. Aspen close 5.6% higher on the day.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.