Renew Capital has made its first investment in Mozambique. The impact investment firm is backing fintech startup, Roscas. The value of the investment was not disclosed.

The Fund for Export Development in Africa (FEDA), the impact investment subsidiary of Afreximbank, has invested in Bloom Africa Holdings Limited, a regional financial services platform operating across West Africa. The company has stakes in multiple financial institutions in Gambia, Sierra Leone and Liberia which operate as Bloom Bank Africa.

Sun International is to dispose of 43.3% of its 49.3% equity stake and 100% of its loan account in Tourist Company of Nigeria (t/a Federal Palace Hotel) to Nigerian Rutam Finance for an aggregate cash consideration of US$14,55 million. The remaining 6% equity interest held by Sun International will be sold in due course. The transaction is in accordance with the company’s stated intention and strategy to exit its investment in Nigeria.

Kenyan Insurtech Pula, has closed a US$20 million Series B led by BlueOrchard. Other investors include the IFC, the Bill & Melinda Gates Foundation, Hesabu Capital and existing investors.

Nigerian B2B e-commerce platform, OmniRetail, has announced the first investor for its newly launched Series A – Goodwell Investments, via its uMunthu II fund. The impact investment firm did not disclose the size of the investment.

Sahel Capital has approved a US$2,4 million working capital loan to Ghanian Licensed Buying Company, Kuapa Kokoo Limited. The loan will be provided by the Sahel Capital Social Enterprise Fund for Agriculture in Africa facility.

Inua Capital has invested in Uganda’s Forna Health Foods, the manufacturer of Aunt Porridge and Instapol. This is one of the first investments from Inua’s GLI impact fund. Forna Health Foods is a female-founded and female-led business that boasts a female workforce of about 65% and focuses on mothers and children as their core customers.

Over recent years, the successive hammer blows of the COVID-19 pandemic, high inflation and rapidly rising interest rates, the Russia/Ukraine war and other outlier events wreaked havoc with many companies’ M&A ambitions, with funds earmarked for M&A having to be diverted to strengthen balance sheets and other operating priorities.

However, with the pandemic and its initial effects now (hopefully) in the rear-view mirror and the African business landscape having largely acclimatised to the “new normal”, one may, over the next few years, see consolidation, as well-capitalised companies look to grow market share or vertically integrate by acquiring the less resilient to make up for lost ground.

THIS TIME MIGHT BE DIFFERENT

African M&A activity has not been all doom and gloom since the outbreak of the pandemic. On the contrary, the African M&A market experienced a record-breaking year in 2021, with total deal value exceeding circa US$64 billion.1 The surge likely resulted from the deployment, after the initial pandemic effects had passed, of funds previously allocated for M&A. Unfortunately, the African M&A market has been relatively subdued since then, amounting only to approximately $26 billion in 2022 and $10 billion in 2023.2

Nevertheless, 2024 might prove to be different (barring any significant new outlier events occurring). Unlike in 2022, the effects of the above outlier events have now largely been priced in. Interest rates and inflationary pressure appear to have stabilised. Well capitalised companies have also had a two-year window to re-evaluate their M&A action plans and build up their M&A war chests, while less resilient companies became more vulnerable to potential take-overs.

Furthermore, the political certainty gained following the conclusion of elections in several “powerhouse” countries this year could also help break the current holding pattern in M&A. While a modest recovery is expected by some in 2024,3 the M&A activity may surprise us and exceed expectations.

BENEFITS FOR AFRICA

Successful consolidations possess significant transformational power. The benefits of such consolidations are not only enjoyed by the firms in question, but also by other stakeholders and role players in the value chain. Examples of “flow-through” benefits enjoyed by such parties include, inter alia –

• Re-establishing competition Where a region or sector already has a dominant player, a consolidation between smaller players could potentially “even the playing field” by leveraging synergies and benefits of scale, resulting in cost- and selection benefits for consumers, as well as business opportunities for other service providers in the region or sector. By contrast, it may be more difficult for dominant players to participate in consolidation through M&A, given competition law restrictions.

• Cheaper financing options Generally, consolidated businesses – which have more assets to use as collateral – can access better financing terms, compared with their smaller peers. The transaction and borrowing costs saved in this regard could be “paid over” to shareholders in the form of dividends, or be utilised to further grow the business (which could, inter alia, lead to more employment opportunities).

• Diversification benefits Consolidations could enable the subject firm to be better diversified, whether from a product range, sectoral and/or geography perspective. This helps companies better mitigate risk and, in turn, become more resilient, resulting in greater certainty for all stakeholders in the value chain.

SECTOR FOCUS

Despite the somewhat sluggish African M&A activity over the 2022 and 2023 period, certain sectors, such as those outlined below, continued to enjoy positive transaction flow. These sectors could lead the potential consolidation surge.

• Healthcare The African healthcare sector’s resilience was apparent from the number of notable transactions during the period. Particularly robust were Pharmaceuticals and Life Sciences, along with Healthcare Services, which helped propel the sector’s dynamism. Noteworthy transactions included Mediclinic’s “take private” and Laprophan Laboratoires SA’s acquisition of SAHAM Pharma.

• Energy and infrastructure During this period, M&A became a strategic tool for companies looking to optimise resource utilisation and enhance operational efficiency in the energy and infrastructure sectors, aimed at bridging Africa’s infrastructure gap. Security of energy supply and the transitioning to “greener” energy sources continued to enjoy focus. Prominent transactions in these sectors included Harith General Partners’ investment in Mergence Investment Managers, BlackRock’s recently announced acquisition of Nigeria’s Adebayo Ogunlesi’s Global Infrastructure Partners, and ENGIE SA and Meridiam Infrastructure Finance’s acquisition of BTE Renewables.

• Banking and finance The African banking and financial services sectors were at the forefront of the M&A activity during the period. With the aim of fostering stability and enhancing competitiveness, numerous financial firms across the continent engaged in M&A transactions.

This trend not only resulted in larger, more resilient financial institutions, but also facilitated the integration of innovative technologies to meet the evolving needs of consumers. Notable transactions during the period included the Sanlam and Allianz joint venture, Apex Group’s acquisitions of Sanne, Maitland and the Efficient Group, the Rohatyn Group’s acquisition of Ethos Private Equity, and KCB Group’s acquisition of an 85% stake in Trust Merchant Bank.

LOOKING AHEAD

It is evident from African M&A activity during the period that international players are taking note (and capitalising) on many of these opportunities on the continent. Faster growth prospects, less competition and “cheaper” acquisition opportunities compared with those in their home markets may continue to drive international interest in African companies. In addition, potential game changing initiatives such as the African Continental Free Trade Area (AfCFTA) and related agreements and protocols are also expected to spur M&A on the continent, both from within and outside of Africa.4

Given the above, it appears that a potential consolidation surge may be on the horizon. As companies continue to navigate the African M&A landscape and the potential consolidation surge, it is essential for business leaders, policymakers and investors to stay abreast of the relevant trends and developments.

FOOTNOTES

Khaya Hlophe-Kunene and Johann Piek are Directors | PSG Capital

How to determine whether separate class meetings must be held to vote on a scheme of arrangement

The number of takeovers and resultant delistings of Johannesburg Stock Exchange (JSE)-listed companies has increased in recent years, and the scheme of arrangement (Scheme), in terms of section 114 of the Companies Act, No 71 of 2008 (the Act), remains the most commonly used mechanism to effect such transactions. In terms of s114 of the Act, the board of a company may propose to its shareholders an arrangement in terms of which, inter alia, the securities held by all or certain of the shareholders may be expropriated for consideration. The offer could be made by the company itself, or by a third-party offeror. Therefore, the Scheme would be proposed as an arrangement between the company and certain shareholders, in terms of which the company or a third-party offeror offers to acquire the relevant shares in issue (Target Shares). If the Scheme is approved at a general meeting by a special resolution of the shareholders entitled to vote thereon, and all applicable conditions to which the Scheme is subject are fulfilled, all of the Target Shares will, by operation of law, be acquired. This is the main benefit of a Scheme when compared with a “general offer” to the relevant shareholders: the Scheme binds all shareholders and not only those who support the Scheme. However, a potential complication arises when a Scheme is proposed to shareholders of a company who own different classes of shares. The question then arises whether separate class meetings ought to be held to consider and vote on the Scheme.

This issue arose for the first time under the new Act in the Sand Grove Opportunities Master Fund Ltd and others v Distell Group Holdings Ltd and others (2002) 2 All SA 855 (WCC) judgment, wherein the first respondent, Distell Group Holdings Ltd (Distell) proposed a Scheme to its shareholders in terms of which, inter alia, Distell would be acquired by a South African subsidiary of Heineken International BV (Heineken). Distell, a JSE-listed company at the time, had two classes of issued shares – ordinary shares and B shares. The B shares, owned by a subsidiary of Remgro Limited, were linked to certain of the ordinary shares held by such holder and enjoyed no economic rights, but afforded their holder certain additional voting rights at meetings of Distell. A combined meeting of Distell’s ordinary and B shareholders was held, which approved the Scheme with the requisite majority. The applicant, Sand Grove Opportunities Master Fund Ltd (Applicant), a hedge fund, was dissatisfied with this outcome and applied to the court for orders, inter alia, declaring that the meeting at which the special resolution was adopted was not properly constituted and, therefore, invalid and void, and that the special resolution adopted at the meeting was also invalid. The Applicant argued that the Scheme was required to be tabled for approval by the holders of each class of Distell’s shares at separate meetings in terms of s115(2)(a) of the Act – namely, one meeting for the holders of the ordinary shares, and a separate meeting for the holders of the B shares.

In making its determination, the court reminds us that in terms of s311(1) of the previous Companies Act, No 61 of 1973, a court could give direction on whether, separate, meetings had to be convened for different ‘classes’ of members or creditors. However, the court noted that under the current Act, the courts no longer play a role in determining, ahead of the voting, whether separate class meetings are required. Under the Act, this is the responsibility of the company which proposes the scheme to its shareholders, i.e. the independent board must consider and determine the manner in which s115(2) of the Act must be complied with. The court further observed that the Takeover Regulation Panel could also, in the exercise of its functions in terms of s119(2)(b)(ii) of the Act, direct the holding of appropriately constituted separate meetings.

In determining whether an offer should be put to shareholders in a single meeting or at separate class meetings, the court considered, inter alia, the principles established in English case law, especially the lease judgment in Sovereign Life Assurance Co v Dodd (1892) 2 QB 573, in which it was held that the test for calling separate meetings is based on the similarity or dissimilarity of the shareholders or creditors rights, and not on the similarity or dissimilarity of their interests. The court held that the manner of determining the question of whether a relevant dissimilarity of rights was involved would be to ask the questions of what was being offered to whom under the proposed Scheme and how different classes were being treated under the proposed Scheme, and to see whether the answer demonstrated that it was improbable that the classes could consult together at a combined meeting. Therefore, a difference in the rights of the shareholders may be a basis to require convening separate meetings, but only if the difference in treatment of the classes is such that it would make it unrealistic for the shareholders of the two classes to consult together. It was further noted that this is a value judgment which involves, amongst other things, the materiality of the differences in rights in comparison with the commonality of the rights under discussion.

The court also held that one must bear in mind the impracticalities and other disadvantages of dividing the total voting rights to be exercised into too many separate meetings – a principle that has long been recognised in the law in relation to schemes of arrangement. The court noted that it would not be advancing the general efficacy and efficiency of the Scheme procedure to adopt an interpretation of s114 of the Act that would bring about hair triggers for separate class meetings on the mere basis that the class rights were not identical. According to the court, it is unlikely that there was an intention by the legislature, in relation to s114 of the Act, to introduce a new approach abolishing the sound and well-established policy, or to import such obvious impracticalities. The court, therefore, held that a company concerned with convening a meeting in terms of s115(2) must conduct itself mindful of the same considerations mentioned above.

In conclusion, for now, the common law on class meetings lives on, and it is the responsibility of the independent board of a company, on a case-by-case basis, to consider and determine the most appropriate manner in which to comply with s115(2) of the Act. This is a question which will not always be easy to answer, and it is, of course, something which potentially could be reviewed by a court at the insistence of a dissenting shareholder, under an application in terms s115(3) of the Act.

Jesse Prinsloo is an Associate and Dane Kruger a Director in Corporate and Commercial | Cliffe Dekker Hofmeyr.

This article first appeared in DealMakers, SA’s quarterly M&A publication

The Global Accelerator offers 100% capital protection in dollars at maturity after five years, while giving exposure to global equity indices.

To explain how it all works, Japie Lubbe of Investec Structured Products joined me on this podcast and covered the following topics:

The design of the underlying equity basket

The use of “insurance” in an equity portfolio and how this can be understood in the context of more familiar concepts like car and home insurance

The upside of the Global Accelerator, both on an accelerated basis and a capped basis

The payoff of this product vs. buying an ETF that tracks a similar equity index, with specific reference to how dividends work

Building blocks of the Global Accelerator in terms of company structure and the various instruments used

Fees involved and how they compare to unit trusts

The liquidity available over the five-year period

How a debt instrument is used to provide capital protection and understanding the credit risk associated with this debt instrument.

Applications close 21 May 2024.

As always you must do your own research and speak to your financial advisor before investing in a product like this. You can find all the information you need on the Investec website at this link.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Anglo American has a slight uptick in diamond sales at De Beers (JSE: AGL)

But caution is still the flavour here

The debate around mined vs. lab grown diamonds continues, with De Beers (part of Anglo American) at least starting to show some improvement in sales after a dark period. The company can directly influence the level of supply in the market, which is exactly what it did to try and get prices to recover.

It seems to be working, with sales value for Cycle 3 of $445 million. That’s an improvement on Cycle 2 this year of $431 million, but remains lower than $542 million achieved in Cycle 3 of last year.

The economic landscape and slow pace of growth in China are also major contributing factors here. Although lab-grown diamonds don’t help, they are by no means the only challenge.

Insimbi had a tough time in the past year (JSE: ISB)

HEPS is down sharply

Insimbi Industrial Holdings released a trading statement in early February that indicated a drop in HEPS of at least 20% for the year ended 29 February 2024. That’s the minimum disclosure required by the JSE for a trading statement, so you always have to be careful when you see “at least 20%” – the wording “at least” can end up working very hard.

That’s the case here, with Insimbi expecting HEPS to be down by between 50% and 60% for the period. It will come in at between 11.02 cents and 13.78 cents.

The reasons? All the usual stuff, really. Apart from load shedding and higher interest rates, Insimbi is also exposed to the general state of our ports and transport infrastructure. A ban on exports of recycled metals is also listed among the negatives. Insimbi did what it could in terms of cost management, but couldn’t come out with an appealing earnings result. Still, it’s profitable and well capitalised and ready to step into the ring once more in the new financial year.

Orion takes an important step with the Okiep Copper Project (JSE: ORN)

There have been lots of complicated legal processes in the background

Back in 2021, Orion exercised a restructured option to directly acquire the mineral rights and various other assets related to the Okiep Copper Project, rather than shares in the entities themselves. The timing and manner of the transactions have been amended, with all parties other than the IDC having signed the addenda at this stage. The IDC is still dealing with internal approvals.

The remaining total consideration of R59.6 million remains unchanged, with the first phase settlement being R10.86 million in cash and R35.1 million in Orion shares, with disposal restrictions attached to those shares. The first settlement will take place when SARB approval is received.

Orion is aiming to conclude the Bankable Feasibility Study by June 2024, with the approval of the water use license outstanding before the project is fully permitted.

TeleMasters announces the structure of its B-BBEE deal for Catalytic Connections (JSE: TLM)

A good effort has been made here to minimise dilution for existing shareholders

People tend to forget that a B-BBEE deal isn’t as simple as previously disadvantaged individuals being empowered at the expense of those who have money. In a listed company, a costly B-BBEE deal hurts every single shareholder in that company of every colour. It’s a shift of value from one party to another, usually on economic terms that are highly in favour of the B-BBEE partner.

Sometimes, listed companies get it right to strike more of a balance, avoiding a scenario where the deal becomes extremely punitive to existing listed shareholders. TeleMasters is one such example, with the 30% deal in Catalytic Connections being structured intelligently to preserve the existing value for current shareholders. Future value creation is shared with the B-BBEE partner, in this case Sebenza Education and Empowerment Holdings, on a 70-30 basis.

As the announcement explains, this is achieved by Catalytic Connections creating preference shares equal to the current value of that company and issuing them to TeleMasters. This allows the B-BBEE party to subscribe for 30% of the shares in Catalytic Connections without taking on external debt. It’s a vastly superior structure to the usual externally leveraged deals that often end up underwater anyway.

Little Bites:

Director dealings:

Des de Beer elected to receive R42.7 million worth of shares in Lighthouse Properties (JSE: LTE) in lieu of a cash dividend as part of the scrip distribution option. Receiving scrip dividends has been core to his strategy in recent times of significantly increasing his stake in Lighthouse.

Motus (JSE: MTH) announced that Osman Arbee will be retiring as CEO of Motus with effect from 31 October 2024, having reached the retirement age of 65. He has been with the group for 20 years and has been CEO of Motus since 2017. Ockert Janse van Rensburg, currently the CFO of Motus, has been appointed as CEO with effect from 1 November 2024. He’s been in the CFO role since 2015 and served as CEO for six months while Arbee was ill, so there’s a strong succession story here.

From mining stocks to carbon capture, enabling companies and nuclear. There are so many investment opportunities stemming from South Africa’s energy transition. In episode 4 of Investec’s The Current, discover how you, as a private investor, can get some skin in the clean energy game. Iman Rappetti in conversation with Investec’s Barry Shamley, Zane Bezuidenhout, Boipelo Rabothata and Campbell Parry.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Afrimat has more good news for the market (JSE: AFT)

Alongside the Lafarge deal opportunities, the rest of the group is producing great results

Afrimat has released a trading statement for the year ended February 2024. HEPS is expected to increase by between 21% and 26%, coming in at between 553.6 cents and 576.5 cents. This is excellent news for shareholders, particularly after the other recent good news of the Lafarge deal closing.

On a share price of R63, Afrimat is trading on a Price/Earnings multiple of roughly 11.2x at the midpoint.

Detailed results are due on 15 May, so you’ll have to wait about a month to learn more about the drivers of these numbers.

Lighthouse is looking at selling more Hammerson shares (JSE: LTE | JSE: HMN)

Lighthouse would prefer to be prepared for direct property investment opportunities

Lighthouse Properties has already sold down quite a chunk of Hammerson shares, with Hammerson having won few friends among its strategic holders for the decisions it made around its dividend. Based on previous Category 2 announcements, Lighthouse has sold Hammerson shares representing 26.21% of Lighthouse’s market capitalisation. If they moved through the 30% mark over a 12 month period, it would trigger a Category 1 process.

Such a process is time-consuming, so Lighthouse is pre-empting this by going through the motions now and asking shareholders for approval for such a disposal. The shares in Hammerson wouldn’t be sold at a price lower than a 10% discount to the 5-day VWAP before the disposal.

Assuming the approval is obtained, this would give Lighthouse the flexibility to sell the Hammerson shares as required in response to opportunities to make yield-accretive direct property investments.

It’s more difficult to increase AUM without a significant distribution angle to the business

Whilst I’m the first to acknowledge that I’m no expert in this space, it does seem to me as though the PSG Konsults and Quilters of this world are finding it easier to increase AUM than the more pure-play asset managers like Coronation and Ninety One. It makes sense to me intuitively, as having a large sales force out there can only be positive for assets under management. Of course, that sales force comes at a substantial cost, so the distribution side of the business needs to be successful for there to be a net positive impact on the group.

Without a particularly strong distribution model, Ninety One’s AUM seems to be limping sideways. A year ago at the end of March 2023, it was £129.3 billion. At the end of December 2023, it was £124.2 billion. The latest number is for March 2024, coming in at £126 billion.

Key metrics head the right way at Purple Group (JSE: PPE)

The swing into profitability is for all the right reasons

When the trading statement came out that reflected a move into the green, the market didn’t really give much of an initial reaction. This changed with the release of detailed interim results, with the share price up nearly 17% for the day. This is because there’s a great story to tell, with Purple revenue up 29.3% and group expenses down 0.4%, leading to a positive earnings result.

Notably, the net asset value is 41.6 cents per share and interim HEPS was 0.78 cents, so the closing share price of 90 cents reflects a lofty valuation. If Purple can maintain this momentum and push through the inflection point for profitability (i.e. with most of the additional revenue dropping to the bottom line), the earnings multiple can unwind quite quickly.

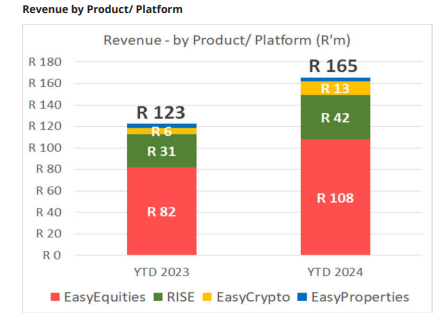

There are numerous metrics in the full report, including Easy Group (EasyEquities and associated businesses) growing revenue by 34.9% and active clients by 12.5%. This means they are making more per client, achieved through non-activity based revenue increasing by 62% to R95 million. The monthly account fees have made all the difference here. Compare this to activity-based revenue increasing by 10% to R71 million. For all the naysaying and complaining on social media at the time, the account fees have absolutely been the right decision. Easy’s bottom line swung from a loss of R16.5 million to profit of R11.8 million.

Perhaps most impressively, they achieved net retail inflows despite the operating environment.

This certainly isn’t the most beautiful chart I’ve ever seen, but it does show how the Easy Group actually makes money:

It’s also good to see that the earnings from GT247.com have become a lot more dependable, with profit for the period of R4.2 million for this period vs. R3.2 million in the comparable period.

Riskovitz Value Fund could invest up to $100 million in Trustco (JSE: TTO)

At this stage, the arrangement is light on details

Trustco has entered into an agreement with Riskowitz Value Fund that provides for a six-month window period for the latter to invest up to $100 million in hybrid capital (or other capital to be agreed on) in Trustco. Essentially, it sounds like Riskowitz is agreeing to keep the capital available for Trustco, with no fee payable by either party.

Riskowitz is already a shareholder in Trustco with a 23% stake. It has been a shareholder for over 10 years.

I found this line in the press release on the Trustco website, which wasn’t in the SENS announcement:

“The transactions allow Trustco and RVF to capitalise on the unreasonably low market valuation of Trustco, to create long-term value for all Trustco shareholders.”

To me, this makes it sound like Riskowitz may well be investing in a hybrid instrument so that Trustco can then execute share buybacks of ordinary shares at the depressed market price. I’m purely speculating on this.

Little Bites:

Director dealings:

As one would hope, a few directors and the company secretary of Fortress Real Estate Investments (JSE: FFB) elected to receive capitalisation shares in lieu of the cash dividend.

In today’s bear market, where traditional investment strategies fall short of expectations, dismissing alternative assets before properly evaluating their worth seems nonsensical.

No matter how you slice it, you simply can’t get true diversification from a collection of investments that all draw from the same diminishing pool of JSE equities and bonds. And the volatile performance of these over the last few years proves that.

These days, to meet an investor’s need for capital security and long-term growth, a balanced portfolio needs to contain a carefully curated mix of different asset classes that react in different ways to market movements. If all your investments behave the same, what’s to shield you from turbulent markets?

It’s easily achieved by incorporating an appropriate selection of both traditional investments and alternative investments. That way, risk exposure is better spread across the portfolio because the performance of the alternative assets is not linked to market sentiment.

Alternative isn’t a dirty word

Think of the word ‘alternative’ and what comes to mind? If it’s someone with vegan sandals and a goatee, that could explain the reluctance we see among some investors to take a serious look at alternative investments.

No judgement here about lifestyle choices. To each their own (though the jury is out on the edible footwear). However, there is a serious point to be made about the instinctive distrust of anything that falls outside the familiar. And, in the case of alternative investments, the bad rap they get simply for being less conventional and, frankly, misunderstood.

Not only does it do the alternative asset class a disservice to unfairly bundle everything that isn’t a listed equity or bond into one basket, but it also implies that anything with an ‘alternative’ tag is inherently sketchy and should be treated with distrust.

As is the nature of life, no two things are exactly the same. Alternative assets account for most of the options available in the market, outside of bonds and equities. With such an array of options to choose from, it stands to reason that some of these assets carry more risk than others. Due diligence is always key and the more intangible the assets – like hedge funds, crypto and other unique trading items – the greater the risk appetite required.

Our collective view of alternative assets definitely needs to be reassessed. After all, where do you think those former-JSE-listed assets go when retired from the stock exchange?

By their very nature, alternative assets offer investors a way to smooth their investment journeys because they aren’t prone to the same kind of extreme fluctuations as assets that are linked to the stock market.

At Fedgroup, we’re not championing alternatives merely for the sake of it and we’re not in the business of recommending assets in any class that can cost people their hard-earned savings. We consciously look at incorporating alternative assets that can provide the right return characteristics for investors, and an important factor to consider is the ability to deliver a smoother returns curve. So, you can believe it when we say we’re excited by the array of alternatives that meet our immoveable criteria for stability and security.

Getting the balance right

Incorporating alternatives and getting the mix of investments right gives you breathing room in your portfolio to explore interesting opportunities over the course of your investment journey, without sacrificing the returns of your entire portfolio.

So, which alternative assets have the potential to deliver these highly sought-after stable returns? Ventures in the sustainability sector are a good starting point. Especially those in renewable energy and agriculture, where investors have an opportunity to grow their own wealth while also making a positive contribution to our planet.

There’s also the broader benefit of helping to address key socio-economic factors such as job creation, food security, and energy production, which in turn have a positive impact on the ability of these assets to generate returns. People need to work and eat, and they need electricity. Investments into these sectors therefore will deliver a return as these sectors continue to grow.

A diverse mix of alternatives like these, along with traditional investments, can help investors to mitigate risk, by bringing balance to portfolios that have been sucker-punched by market sentiment and fluctuating market cycles.

Although more and more investors are getting the message, there are still too many whose portfolios exclude alternatives because they, or their financial advisors, remain blinkered to their potential.

At Fedgroup, we’ll keep banging the drum because, the way we see it, alternatives are fast becoming mainstream.

Fedgroup is a specialist financial services provider with a legacy of putting people before short-term profit. For over 30 years, we’ve delivered market-leading financial solutions that not only enhance value for our clients, but remain straightforward, transparent and easy to understand.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AH-Vest is profitable, although the share price suggests otherwise (JSE: AHL)

When last did you see something trading on a Price/Earnings multiple of 0.5x?

AH-Vest operates the All-Joy brand, which means it processes tomatoes and turns them into tasty things to put on your hotdogs or in your pastas. It’s a lot harder than it sounds, with issues like trying to manage the risks of import-heavy supply chains and supporting local farmers.

Although related party transactions do make this company trickier to understand than most people would like, the reality is that the share price is R0.02 and HEPS for the six months to December 2023 came in at R0.0259 – so this is on an annualised Price/Earnings multiple of below 0.5x. Another helpful data point is net asset value per share of 48.24 cents per share, which is over 24x higher than the share price.

Goodness knows this isn’t the most lucrative business model around. Revenue was up just 1.9% for the period and the gross profit margin deteriorated sharply from 36.6% to 32.4%, so there are challenges. The impact was largely offset by a 7.6% drop in operating expenses, driving a 35% increase in profit before tax.

The percentages sound interesting but the actual numbers are tiny here. Profit before tax increased from R2 million to R2.7 million. When you compare this to the trade receivables balance of R56.6 million, you can see that the working capital burden of this business model is concerning relative to profitability.

This seems to be a perfect example of a company on the JSE that is so tiny that very few in the market even read its SENS announcements, let alone buy it. It doesn’t help that the lowest offer in the market is R0.40, which is a lot closer to net asset value per share. The best bid is just R0.04.

Tomato spreads might be tasty, but bid-offer spreads like these are not.

Solid rental growth at Sirius Real Estate (JSE: SRE)

This is a good story to tell alongside recent acquisitions

Sirius Real Estate released a trading update for the year ended March 2024. The overall rent roll is up 8.2%, or 7.2% on a like-for-like basis. Sirius points out that this is the tenth consecutive year of like-for-like rent roll growth in excess of 5%. This is particularly impressive when you remember that this is in hard currency, as the portfolio is in Germany and the UK.

Inflation has come down in Germany in the past year, so growth in that market has been mainly achieved through a reduction in vacancies. This does good things for the portfolio valuations. The same is true for the UK, which is why like-for-like rent roll growth has been at similar levels across the two countries.

It sounds like there’s more pressure on valuation yields in the UK than Germany, so watch out for that. Despite the challenges, Sirius expects a positive movement at group level at year-end.

Sirius has been on the acquisition trail recently, having raised €165 million in the market for that purpose. €96 million has been invested in UK acquisitions and €55 million in acquisitions in Germany. The UK acquisitions were on a weighted average net initial yield of 8.9% and the German acquisitions on 9.3%.

The fund is also happy to recycle capital, which is so important in this sector. There were disposals of €51 million in the second half, all completed at or above book value. The disposal process has focused on mature properties in Germany, with Sirius taking the approach of acquiring underperforming properties and selling them once vacancies etc. have improved. This active approach is why the market is prepared to put a premium valuation on Sirius, even if that premium got way too high during the pandemic.

The weighted average cost of debt is 2.1% and there are no major maturities until June 2026. We do seem to be in a higher-for-longer environment though, with Sirius acknowledging the risk of higher future funding rates as debt is refinanced. For reference, last year’s refinancing activities were at rates around 4.25%, which is obviously well above the weighted average across the book.

Ever the optimists, Sirius also points out that the higher interest rates create opportunities for acquisitions due to pressure on property valuations!

Little Bites:

Barloworld (JSE: BAW) closed more than 10% higher after starting the day with the release of a cautionary announcement. It gives absolutely no information on the type of thing being considered or even which segment it relates to, but that didn’t stop speculators from hitting the “buy” button!

Trustco (JSE: TTO) has renewed the cautionary announcement related to various potential transactions, which are in the final stages of being submitted to the board for approval.

Holders of around 6.25% of shares in BHP Group (JSE: BHG) elected to participate in the dividend reinvestment plan. I’m surprised to see just how many BHP investors are clearly in this for cash dividends rather than capital growth.

Conversely, the result of the dividend capitalisation issue (a similar structure) at Fortress Real Estate (JSE: FFB) had a very different outcome, with holders of 33.79% of the FFB shares electing to receive more shares instead of a cash dividend.

As a further scrip-versus-cash data point, it looks like holders of around 35% of Lighthouse Properties (JSE: LTE) shares elected to receive shares in lieu of a cash dividend.

As a reminder of how enormous British American Tobacco (JSE: BTI) is, the company is casually busy with debt security repurchases of up to £1 billion as part of general management of the balance sheet.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Accelerate Property Fund taps the market (JSE: APF)

The company needs to raise R200 million via a rights offer

Accelerate Property Fund has a broken balance sheet. Fixing such a problem isn’t easy, unless there are properties that are easy to sell at market value. Even then, this inevitably means selling the best properties in a portfolio to reduce debt and being left with only that yucky stuff at the bottom of the dishwashing water.

Accelerate Property Fund got itself into this mess and shareholders will be asked to get it out. The company warned in December 2023 that a rights issue of up to R300 million may be needed. Although the end result isn’t quite as bad as that, a right issue of up to R200 million is still very far from ideal.

This is being done at a fat discount to what is already a highly discounted share price. The subscription price is a discount of 31.65% to the 30-day VWAP. Although excess allocations will not be allowed, this is a renounceable rights offer and so shareholders can try sell their letters of allocation in the market if they aren’t going to follow their rights.

Whatever you do, don’t allow your letters to expire worthless. Either follow your rights or sell the letters, or all you are doing is destroying value in your shareholding.

K2016336084 (South Africa) has fully underwritten the offer. Although this circular doesn’t say it, a previous announcement described this entity as the iGroup, which already holds a significant minority stake in Accelerate. Whether or not that name is still applicable isn’t obvious, but what is useful in the circular is a note that Urban Retail Property Investments is the sold shareholder in that entity.

The underwriter gets paid a delicious 5% fee of R10 million for this (plus a recoupment of costs of up to R300k), which just means more pain for other shareholders. Escaping a rotten balance sheet is always a very unpleasant exercise.

Purple Group released a trading statement for the six months ended January 2024 that tells a positive story. After reporting a headline loss per share of 0.84 cents in the prior period, Purple has swung solidly into the group with HEPS of between 0.74 cents and 0.82 cents.

Keep in mind that this is a stock trading at 70 cents per share, so this puts it on a rather daft Price/Earnings multiple. Of course, the market is smarter than that, so investors will wait for more information on the drivers of these earnings and other key metrics like cash conversion.

After a one-way journey for the share price since the peaks in early 2022, this is a welcome return to profitability. Full details are expected on Tuesday, 16th April.

Transaction Capital: life after WeBuyCars (JSE: TCP)

More leadership changes have been made

The Transaction Capital share price dropped to R3.36 in the aftermath of the WeBuyCars unbundling. This is where value investors will pay attention, as the “ugly duckling” that gets ignored by the markets is where savvy value investors can make money. It’s also where they can get severely humbled. Nobody said this game was easy.

With WeBuyCars now out of the picture and Transaction Capital having taken the opportunity to unlock some capital in the process to help repair the balance sheet, the group now has the charred remains of SA Taxi and the interesting prospects of Nutun to manage, along with some other bits and pieces.

To navigate the way forward, the board is being streamlined into three committees (down from six). Forgive me for not spending much time on non-executive director stuff, particularly since there were plenty of committees in place when I watched my Transaction Capital position blow up. Instead, I’ll focus on the executive changes, with the big one being that the Chief Investment Officer and Chief Financial Officer roles are being combined into a single executive position. Mark Herskovitz is stepping into that role, having been with the group since 2007 in various leadership roles. Sahil Samjowan is stepping down as CFO.

It’s also rather interesting to note that another Transaction Capital founder has been pulled off the proverbial golf course to come back and help fix things up. Roberto Rossi is being appointed as an executive director of TransCapital Investments.

The road ahead will be volatile, of that I’m confident.

York raises debt from an international lender (JSE: YRK)

Those biological asset movements must’ve been a key part of this negotiation

York Timbers is many things, but a cash cow hasn’t been one of them. Forestry is a complicated thing and movements in the valuation of the biological assets can look very different to the operational profits in a given year. York seems to have found a lender who understands that, with Nederlandse Financierings-Maatschappij Voor Ontwikkelingslanden N.V. (there’s a candidate for your next tongue twister) agreeing to lend R350 million to York as a new long-term facility.

This will refinance R146 million in debt from the Land and Agricultural Development Bank of South Africa and R75.7 million from Absa. They will also use R65.4 million to acquire Pine-Valley farms. The rest will be for general working capital and the Environmental and Social Action Plan.

The loan is for a nine-year period and must be paid off in instalments. Capital repayments only start after three years.

The rate is 3-month JIBAR plus a margin of 338 basis points per annum. This works out to 11.73% based on Friday’s JIBAR rate. The margin drops by 50 basis points once York achieves two consecutive years of net profit and a net debt to EBITDA ratio below 3x.

The debt has been structured to match the profile of York’s plantation reaching optimal rotation age, which is perhaps why York needed an international lender to get this right. This is very different to the standard loan and credit process.

Little Bites:

Director dealings:

It wasn’t the easiest thing to figure out, as Mpact (JSE: MPT) first announced the vesting of 2021 Bonus shares as well as shares under other schemes, and then a few days later announced the extent of share sales. As always, sales to cover tax don’t count as a sale for me, but excess sales do. From what I can see, almost all the executives and prescribed officers chose to sell all the shares that vested, rather than just a portion. On top of that, a director of the major subsidiary also sold R2 million worth of shares in an on-market trade.

The spouse of the CFO at Standard Bank (JSE: SBK) sold shares in the company worth R149k.

The stake held by Canal+ in MultiChoice (JSE: MCG) is now 40.01%, with the company mopping up liquidity in the market with recent purchases between R117 and almost R120 per share. Canal+ will keep doing this provided the price is below the mandatory offer price of R125 per share.

AH-Vest (JSE: AHL) has practically zero liquidity and a market cap of R2 million. No, that isn’t a typo. The share price is at 2 cents per share. For the six months to December 2023, HEPS will be 37% higher than the comparable period, coming in at 2.59 cents per share. This is one of those classic examples of a very odd situation in microcap land.

Visual International (JSE: VIS) replaced Moore Infinity with LDP Chartered Accountants as its auditors. This will save on audit costs going forward. LDP’s website suggests that they have nearly 140 staff, so it’s not the smallest place around even though I hadn’t heard of them before.

Salungano Group (JSE: SLG) announced a further delay to the publication of FY23 financial results due to the audit opinion not being finalised in time. To make it worse, no updated timeline has been given. The company also reminded shareholders that the business rescue process for Wescoal Mining is waiting for the postponed meeting in June 2024. The business rescue for Keaton Mining is under appeal, as the business rescue application was initially dismissed.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

| Insimbi | Orion | TeleMasters)")

")

")

")