The story of how one forgotten wallet in 1949 led to the invention of the credit card – and the global debt crisis that followed.

When’s the last time you carried cash anywhere? Unless you’re regularly using public transport, it’s probably been a while, right?

If you want a good insight into humanity’s spending habits right now, all you have to do is go shopping for a new wallet. Now, notice how many of those new wallets on the shelf have simply done away with the little pocket that we used to keep coins in. If you’re lucky, you may still find a wallet that has a compartment for you to keep notes. Far more often, you’ll open a wallet and find only rows and rows of card slots inside.

I think that says a lot about our relationship with money. Like so many things in our lives, our currency has become digital – the texture of a coin or a crumpled paper note replaced by digital placeholders on our banking apps.

The best thing about digital money is that it never really runs out. When the cash in your wallet is used up, there’s literally nothing left in there for you to spend. On a banking app, however, you’re always two clicks away from accessing more – whether in the form of an overdraft, credit card or a microloan. In some instances, your bank may even use your spending data to pre-approve you for loans you never applied for (and then they’ll pepper you with messages and notifications telling you that this money is available to you).

In addition to our need for instant gratification, we’ve become accustomed to the idea of buying now and paying later. Could it be that the best thing about digital currency is also the worst thing about it?

The dawn of debt

Once upon a time back in 1949, a man named Frank McNamara received the bill after eating at a New York restaurant, and was horrified to realise that he had forgotten his wallet at home. Fortunately, his wife was able to come to his rescue, but this was a humiliating experience that Frank would struggle to forget. That seed of discomfort wedged itself into his brain until it grew into an idea.

“Why carry cash around at all?” Frank questioned. Why couldn’t every restaurant that he ate at send him the bill at the end of the month, and then he would pay them all together? Wouldn’t it be a much more pleasant experience for diners to sit down, enjoy themselves and then leave at the end of their meal without having to make a fuss about payment then and there?

Frank McNamara didn’t invent the idea of credit – that existed long before – but until the 1960s, it was never implemented on a significant scale.

The notion of credit traces its roots to ancient Mesopotamia, with evidence dating back at least 5,000 years. Inscriptions found on clay tablets from that era depict transactions between Mesopotamian traders and merchants from Harappa. They serve as some of the earliest documented instances of agreements to purchase goods immediately with a commitment to pay at a later time.

My guess is that for as long as we’ve been able to buy things, we’ve wanted to negotiate to buy things we couldn’t afford. What Frank and his partner Ralph Schneider did was to make it easy for everyday people to get used to the idea of paying for things without using cash. They invented the Diners Club.

In the beginning, Diners Club members would carry little cardboard cards around in their wallets as a show of faith – an IOU, if you will. In its first year of business, Diners Club had partnered with 28 restaurants and two hotels, all of which were prepared to accept monthly billing in respect of this select clientele. By 1960, the cardboard card was replaced by a more familiar-looking plastic version.

Before long, the Diners Club phenomenon shifted beyond the New York elite set, and everyone was showing their cards and getting their bills at home. This, of course, raised the attention of competitors in the field.

Swipe it like it’s hot

One of the first to jump on the credit track was American Express. To some degree, personal credit was a natural shift up the vertical: they already had a lucrative money order and travellers check business, which provided a safe replacement for travellers carrying large sums of cash. All they had to do now was to convince people to use a card for their everyday purchases instead of using money.

Here’s something from my research that truly astonished me. In 1958 – the same year that American Express launched their cards – California-based Bank of America dropped 60 000 paper BankAmericards with a pre-approved limit of $300 into mailboxes around the city of Fresno, California. Imagine 60 000 Americans waking up one morning to a letter in their mailboxes saying “Here’s $300. Go spend it and pay us back later.”

For context, in today’s money, that $300 equals more or less $3 000, or around R55 000.

As you can probably guess, giving unsolicited credit to random people without checking them for creditworthiness beforehand ended very badly, with that first attempt ending in delinquency rates of 20% and multiple instances of fraud. This didn’t stop more of these “drops” from happening though.

Suddenly, without any forewarning, credit appeared as if delivered from the heavens. As an American at that time, you could go to sleep with no cash in your wallet and wake up with $300 that you didn’t ask for in your mailbox. In the subsequent 12 years that it took to prohibit these kinds of mass card mailings, banks across America would inundate the country with 100 million unsolicited credit cards of various kinds.

Built on a bad foundation

In case you’re wondering whatever happened to the good old Diners Club, the simple answer is that they’re still around. In a classic case of second mover advantage, DCs innovative idea of allowing customers to pay with a card instead of cash was quickly snapped up, improved and rolled out by other businesses, making Diners Club a mostly irrelevant afterthought in the process. After all, who would choose a card that you could only use at restaurants when you could have a card that could swipe, well, everywhere?

To their credit (and probably to their own detriment), Diners Club stuck to their guns and held relatively fast to their original concept for as long as they could. In 2016, they finally caved and released a credit card. By that time, they had well and truly been overtaken by all those that came after them, to a degree that they will probably never catch up on. Had you heard of the Diners Club credit card before now? My point exactly.

The Diners Club business (in my opinion at least) may be fading into irrelevance. But the legacy of their idea has left an indelible mark on human history and behaviour.

I’m drawing on statistics from the United States on purpose here, because I think it’s worthwhile surveying the effect of the credit card in its country of origin. That doesn’t mean that we should assume that South Africans are in a much better position when it comes to credit card debt. We all know that we aren’t.

With statistics like these painting a dire picture, and warnings of a credit crunch sounded since April of this year, I can’t help but to think back to that morning in 1958, when residents of Fresno woke up to find those magical cards in their mailboxes. Did they have any way of knowing what a sticky trap waited on the other end of the swipe? Could they possibly have imagined the kind of world where we own nothing because we choose to owe everything?

I don’t know about you, but I think I need a new wallet. This time, I’m looking for one that has space for cash.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

The poultry industry isn’t for chickens (JSE: ARL)

I promise that’s my only pun about these results from Astral Foods

The chicken business is so tough that all of the listed companies in this space have “Foods” in their name rather than chicken, in the hope that perhaps you won’t notice what they do. Jokes aside, it’s often because of a desire to diversify beyond chicken, with RCL having made the biggest strides in that regard.

The focus here is on Astral Foods, which has released results for the year to September. It was a truly terrible period, with flat revenue and a complete collapse in profitability. Between load shedding and bird flu, this was a perfect storm.

Off the back of the first financial loss in the group’s 23-year history, the overdraft ended the period at R1 billion. A full R600 million was drawn over this period, with R398 million in capital expenditure focused on electricity and water services. In other words, the failings of government are hitting Astral squarely between the eyes.

The poultry game is so tough that a backlog in slaughtering can cause a serious problem for profits. Bluntly, a chicken that is past its ideal weight is now a financial liability that needs to still eat. This leads to older birds that are heavier than they should be. The chickens probably appreciate that, but shareholders don’t. When feed costs are 70% of the cost of raising a broiler and those prices increased 15.4% even before the load shedding-driven backlog, Astral never really stood a chance in this period.

The poultry division swung from an operating profit of R802 million to an operating loss of R1.38 billion. Bird flu was a R400 million hit, which really puts the estimated cost of load shedding (R1.6 billion) into perspective.

The feed division offered a modest silver lining, with revenue up 11.9% in response to higher selling prices. Volumes increased by 1.1%, not least of all thanks to the too-fat internal chickens. External sales volumes fell 10.9% as the pig and table egg sectors took strain. There really is nowhere to hide at the breakfast table. The feed division managed to increase operating profit by 21.5%, but much of the gain here was simply a loss in the poultry division.

There are a number of strategic initiatives underway to try and improve the situation and repair the balance sheet. The stark reality is that government needs to keep the lights on, otherwise South Africa’s staple protein is going to need to become more expensive.

Barloworld keeps grinding higher (JSE: BAW)

Key metrics have gone the right way

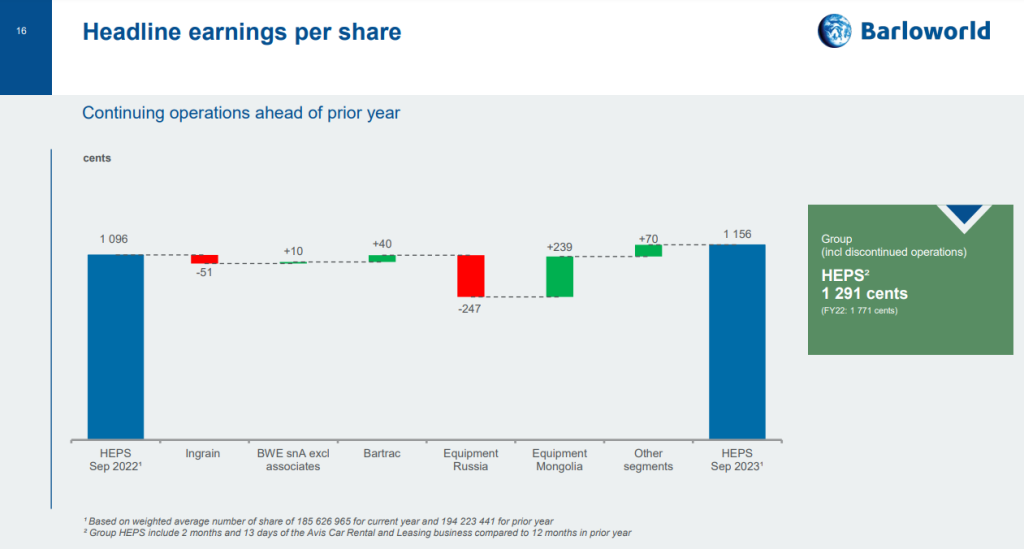

The highlights reel of this Barloworld result shows a group that is getting things right. Revenue is up 14% for the year ended September and EBITDA is up by 15%. Group net debt has come down drastically by 86% thanks to the unbundling of Zeda and a period of strong free cash flow generation.

It’s important to consider continuing vs. discontinued operations, as Barloworld unbundled Avis Car Rental and Leasing (now separately listed as Zeda) in December 2022 and sold the Supply Chain Solutions business in March 2023. The right thing to focus on is continuing operations.

If we look deeper, the largest segment is Equipment southern Africa and it grew revenue by 35%, so that’s rather helpful. Equipment Russia saw revenue decrease by 40% for obvious reasons. Equipment Mongolia was up 59%. Ingrain, the consumer industries business, grew revenue by 11%.

Operating profit tells a different story though. Equipment southern Africa was up 19%, so there’s some margin pressure there. Equipment Mongolia had beautiful operating leverage, with profit up 179%. Fascinatingly, Equipment Russia only saw profit fall by 15%, whereas Ingrain was down by 17% despite growing revenue!

The cost of money can never be ignored, with net finance costs up by 52%. Most of this is because of the increased cost of funding, though some of it is due to higher financing needs overall.

I love a good waterfall chart, so I’ll show the HEPS from continuing operations slide in all its glory. HEPS from continuing operations (the only one you should be looking at) increased by 5.5%, with the movements in Russia and Mongolia offsetting each other:

Brikor shows what an inflection point for profits looks like (JSE: BIK)

When the base period is break-even or close to it, modest revenue growth can cause fireworks

Brikor is currently under offer from Nikkel Trading, with the circular delayed because of a rather interesting turn of events that has seen the CEO of Brikor being unwilling to renew his irrevocable undertaking to not sell his shares.

Looking at the latest numbers, revenue for the six months to August has increased by 13.4%. That’s solid but not spectacular, until you see that revenue in the base period was only good enough for a break-even result. When you grow off that base, the impact on profit is huge.

EBITDA is more than 5x higher at R40.4 million vs. R7.3 million in the base period. Headline earnings per share moved from nil to 2.7 cents, with the share price currently at 17 cents. The tangible net asset value was 28.6% higher at 12.6 cents, so the current price is a significant premium to that metric.

The bricks segment achieved EBITDA of R17.1 million and the Coal segment was good for R9.8 million. In both cases, gross profit margin moved much higher than in the comparable period.

FirstRand reiterates guidance for the new financial year (JSE: FSR)

The financial services released a voluntary trading update

FirstRand has a June year-end. The guidance for results for the year ending June 2024 has been affirmed, but to be fair that guidance was given in September 2023 so there’s hardly been much time since then. The group is looking for earnings growth of real GDP plus CPI plus between 0% and 3%. ROE is expected to remain at the upper end of the targeted range of 18% to 22%, which is why FirstRand maintains a premium valuation vs. its peers.

The most interesting update is that the credit loss ratio is lower than initial guidance. It is not expected to even reach the midpoint of the through-the-cycle range, which shows how conservative the origination strategy has been. I must point out that a credit loss ratio can also be too low, leaving a bank exposed to losing market share. After all, the entire point of a bank is to lend out money.

Much of the current FirstRand performance is being achieved on the deposit side, with the bank continuing to execute a strategy of having a low funding cost relative to peers. This enables it to achieve a stronger net interest margin, particularly net of credit losses when being more selective about lending. Again, there are balancing arguments here.

FirstRand has cautioned the market that its interim results for the six months ending December won’t be in line with what the full-year results should look like, as there are importance once-offs in the interim base. Costs are also higher for this period, with expected normalisation in the second half.

Naspers and Prosus talk to “accelerated profitability” (JSE: NPN | JSE: PRX)

I think what they meant to say is “lower losses” in the portfolio beyond Tencent

Using the term “accelerated profitability” means that there is profitability to start with. Unless something drastic has changed since the last time I looked, the portfolio of businesses beyond Tencent is still firmly in cash burn stage. I accept that losses might have decreased year-on-year, but to describe this as accelerated profitability is a serious stretch.

After the exit of the OLX Auto business, the comparable numbers have been restated so that the group can report based on continuing and total operations.

If you look at HEPS from continuing operations, then Naspers jumped from 28 US cents to 282 – 284 US cents based on continuing operations. For total operations, HEPS showed a similar outcome by increasing from 24 US cents to 286 – 288 US cents.

At Prosus, which has more footnotes than anyone wants to deal with because of the effect of the cross-holding transaction, HEPS increased from 7 US cents to between 46 and 48 US cents.

A comment in the Prosus announcement should temper any enthusiasm about the portfolio. The company talks about how there were lower impairment losses of $0.5 billion in this period vs. $1.5 billion last year. This spike in profitability is because things are less bad, not because they are good.

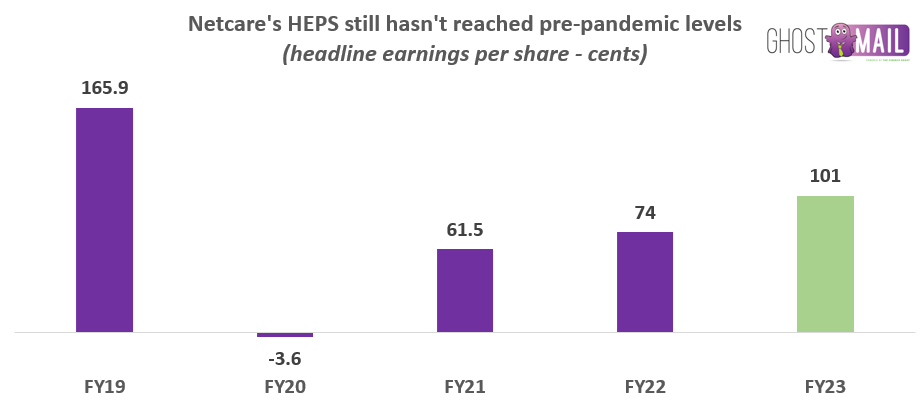

Netcare posts a significant year-on-year recovery (JSE: NTC)

There’s still a long way to go to pre-pandemic levels

Netcare has released numbers for the year ended September. The year-on-year numbers look super strong, with revenue up 9.5%, EBITDA up 14.5% and HEPS up 36.5%. The dividend per share is up 30%, so the cash has mostly followed the earnings.

Before you rush to buy Netcare in the hope that you’re buying a high growth stock, here’s a chart that includes pre-pandemic earnings:

There’s clearly some way to go. It’s also worth noting that return on invested capital (ROIC) has increased from 8.8% to 10.8%. In an environment where the prime rate is 11.75%, a return of 10.8% is far from exciting.

As I’ve shared in Ghost Mail before, I generally don’t see the appeal of hospital groups. They inevitably generate sub-par returns on capital.

I do always look in the detailed numbers for stats that give you an indication of the times that we live in. Maternity cases declined, which is a broader sector trend. The other very unfortunate trend is a sharp increase in mental health days. This is a focus area for Netcare because demand is so high, with mental health occupancy as the highest in the group.

The outlook for 2024 is revenue growth of between 7.5% and 9.5%, along with further EBITDA margin expansion and a higher ROIC.

The share price closed 6% higher on the day. It has lost nearly half its value over five years.

Omnia’s Chemicals business dished out the most pain (JSE: OMN)

The only bright spot in these numbers was the Mining business

For the six months to September, Omnia wrote a lot of pretty things about resilience while posting revenue down 14%. If we exclude the Zimbabwe operations due to hyperinflation, we find operating profit down 34% and adjusted HEPS down 28%. If we include Zimbabwe, HEPS fell by 4%.

The segmental piece tells the most important story. The Agriculture business saw revenue drop by 13% and operating profit fall by 47%, with slower purchases from two major customers. They expect a better performance in the second half of the year. Mining revenue decreased 6%, but operating profit increased by 26% thanks to the performance of the international business and cost benefits in the local business.

But the Chemicals segment is where the wheels really fell off, with revenue down 24% and operating profit collapsing by 95% to just R5 million off a revenue base of R1.09 billion. There’s a demand problem here which is cyclical, but there are also supply chain and manufacturing challenges that the company needs to overcome.

Omnia is still fighting with SARS over the tax assessments for 2014 to 2016. The process has reached the stage where the parties will go for Alternative Dispute Resolution.

PPC is focusing on southern Africa (JSE: PPC)

Will it be the right decision to concentrate on a low growth region?

PPC has released results for the six months to September. This is hot on the heels of the news of a disposal of CIMERWA in Rwanda, which the market liked when that deal was announced at a premium to the value at which the business was recognised in PPC’s books.

It may derisk things to turn a business into cash, but will it be the right long-term decision? After all, the decision to focus on southern Africa is a combination of PPC Zimbabwe (a good business in a volatile economy) and PPC South Africa (a business with excess capacity in a lame duck economy). We shouldn’t forget PPC Botswana as well, which gets lumped in with PPC South Africa for reporting purposes.

CEO Roland van Wijnen has done well during his tenure and this was his final strategic move, so I have no doubt it was well considered. His successor Matias Cardarelli won’t be taking many flights to East Africa, it seems.

The results from continuing operations are the ones to focus on, showing revenue up 20.9% and EBITDA up by a meaty 46.8%, as EBITDA margin moved 400 basis points higher. HEPS has moved strongly into the green at 26 cents vs. a loss of 5 cents in the comparable period.

The SA and Botswana businesses increased revenue by just 2%, hence my lame duck comment. Cement volumes fell 4.7%, mainly in the coastal regions (due to cheap imports) and in Botswana. At least EBITDA margins increased from 12.2% to 12.6%. PPC Zimbabwe grew revenue by 104% and saw EBITDA margins jump from 17.3% to 24.6%. A dividend of $4 million was paid and a further dividend of $7 million was declared in November.

Although the business in Rwanda is on its way out, it’s worth noting that revenue was up 14.5% but EBITDA margins decreased from 32.3% to 29.4%. Perhaps it’s the right time to sell, after all.

As a sign of how well PPC has done to repair the balance sheet, finance costs actually fell slightly year-on-year, despite the jump in interest rates. That’s a direct result of the reduction in gross debt.

Sirius taps the market for £145 million (JSE: SRE)

In an accelerated bookbuild structure, retail investors don’t get the chance to participate

Sirius had a busy day. The company released results for the six months to September and looked to raise £145 million on the market. In an accelerated bookbuild approach, the bookrunners get on the phone to institutional investors to offer them shares and find out how many they want. By “building the book” in this fashion, they basically keep going until the entire capital raise has been filled. If there is sufficient demand, the quantum of the raise can be increased.

The final pricing of the capital raise will depend on the level of institutional demand and at what price. Retail investors sit on the sidelines in this process. If the raise is at a discount (and it usually is), then there’s effectively dilution that cannot be avoided. We will have to wait for the results of the bookbuild to see what happened.

The intention behind the bookbuild was to raise money for potential acquisitions in the UK and Germany. The German assets are typically under-rented opportunities with a site value of €10-50 million. There is limited competition among buyers for these properties. In the UK, they also look for assets with asset management potential, usually with a site value range of £5-25 million. The group has identified eight properties that it wishes to acquire, of which four are in the Germany with a total value of €85 million and four are in the UK with a total value of £45 million. The bookbuild would also strengthen the balance sheet, taking the loan-to-value to below 35%, which is well below the group target of 40%.

Alongside the bookbuild, Sirius announced results for the six months to September. Funds from operations per share increased by 9.4%, with this metric seen by many property investors as being the most important one to focus on. Goodness knows that the dividend matters as well, up by 11.1%.

97% of group debt is at fixed interest rates for the next 2.5 years. The loan-to-value is 40.8%, which shows why the bookbuild is important for further acquisitions.

The net asset value per share is 102.65c. This is in euros, with a current conversion putting it at around R20.50. The current share price is R20.25, so hopefully the bookbuild was completed at or close to book value.

Smaller losses at Stefanutti Stocks (JSE: SSK)

But a loss is still a loss

Stefanutti Stocks released a trading statement for the six months to August. The split between continuing and total operations is important because the group is busy with a restructuring plan and related disposals. From continuing operations, the headline loss per share will be between -10.13 cents and -5.07 cents, which is at least a significant improvement vs. -25.33 cents in the comparable period.

For total operations, the headline loss per share is between -25.02 cents and -20.02 cents vs. -25.02 cents in the comparable period, so the discontinued operations are the problem. Disposals are expected to be concluded within the next 12 months.

Little Bites:

Director dealings:

A director of Investec Bank Limited, which is a major subsidiary of Investec (JSE: INL | JSE: INP), has sold shares worth R2.5 million.

The spouse of the CEO of WBHO (JSE: WBO) has sold shares worth nearly R1.7 million.

The Mouton family (through various vehicles) has bought shares in Curro (JSE: COH) worth a total of R1.6 million.

Two independent directors have resigned from the board of Spar (JSE: SPP) just 10 days before full-year results will be released.

Castleview Property Fund (JSE: CVW) announced that the expected dividend per share for the six months to September will be 10.676 cents per share. Interim results are expected to be released on 30 November. The current share price is R8.50.

Grand Parade Investments (JSE: GPL) has declared a cash dividend of 10 cents per share in respect of the year ended June 2023.

Sasol (JSE: SOL) shareholders voted in favour of the special resolution that would allow the company to issue shares to holders of convertible bonds who exercise their rights. This is dilutive for shareholders who don’t have these bonds i.e. most of them.

Salungano (JSE: SLG) renewed the cautionary announcement related to the voluntary business rescue process at subsidiary Wescoal Mining.

In case something went terribly wrong in your life and you are stuck with Go Life International (JSE: GLI) in your portfolio, then I guess you’ll want to know that results for the three months to May were released. The company doesn’t make any revenue. The operating loss is $43k and the net asset value per share is still negative. Good luck to you.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

More liquidity at Afine’s petrol pumps than in the stock (JSE: ANI)

This makes it difficult for the market to respond to earnings

Afine owns fuel filling stations with long term leases escalating at fixed rates. The company looks to add between one and two suitable properties per year.

Revenue for the six months ended August was 9.8% higher, while profit from operating activities increased by 2.7%. Despite this, distributable earnings fell 6.8%. The interim dividend is 20.60 cents per share, with the share price currently at R4.00 for reference.

There is very little liquidity in this stock, which probably explains why the share price is higher than the net asset value per share of R3.62.

The ongoing listing of AH-Vest remains a mystery (JSE: AHL)

The business is sub-scale and heading in the wrong direction

Being listed is expensive. Considering that AH-Vest has generated total profit of R3.5 million in the past two years, which is less than a modest restaurant should achieve, I really can’t understand why it remains listed.

The All-Joy brand (and a few others I’ve never heard of) would be a good fit in a food business that is currently light on sauces. They do have some resonance with customers, otherwise R211 million in revenue wouldn’t be possible. With gross profit margin down 310 basis points to 34.9% in the year ended June 2023, the company would probably benefit from some production scale as well.

Load shedding has obviously been a big problem here. The lesson is that you can’t respond to problems if you are up against some really big hitters in the same market. If you’re doing the corporate equivalent of taking a knife to a gun fight, there’s only one outcome.

With a market cap of just R16 million, it’s time for an industry player to come squeeze the last bit of sauce out of this one.

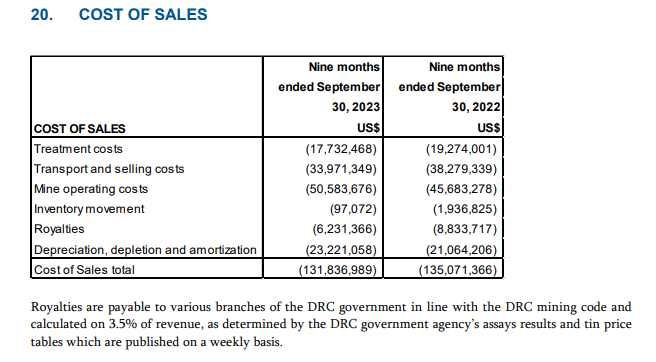

Alphamin released detailed third quarter and nine-month results, reflecting tin production in line with Q2 and EBITDA up 8.6% quarter-on-quarter. The average tin price received was 4% higher but all-in sustaining costs came in 5% higher, both of those being Q3 vs. Q2 numbers.

The company is very focused on the Mpama South project, where development is running in line with the updated two-year underground plan. They are looking to achieve the expanded production from FY24.

Of course, there’s never a dull moment when mining in emerging markets. A bridge on the primary export / import route in the DRC was damaged in September, driving longer transit times and delays in revenue receipts. Ongoing heavy rains in October and November caused the roads to deteriorate further. This is putting the balance sheet under strain, as revenue is being delayed further. The company raised an additional $10 million in senior debt finance and this facility was drawn down in November.

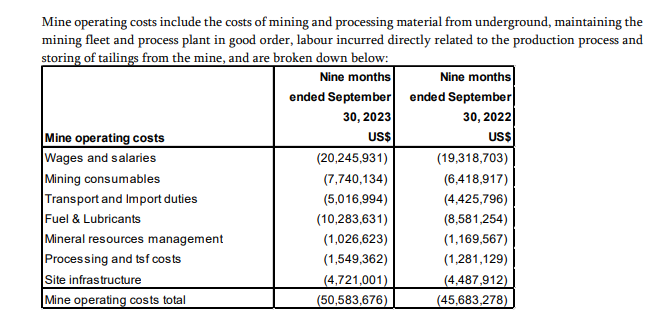

If you’ve ever wondered what the costs of running a mine tend to look like, wonder no more. Here’s the cost of sales breakdown at Alphamin:

Note the footnote regarding royalties. This is why mining is so important to governments in resource-rich countries.

As noted, that breakdown was of cost of sales. There are many other operating costs of course. Here’s what they look like:

Interesting, isn’t it? Now when mines talk about inflationary pressures on costs, you have a better idea of where the toughest areas might be.

Frontier Transport Holdings shows a big jump in HEPS (JSE: FTH)

This company owns Golden Arrow Bus Services and a few other transport businesses

The six months to September 2023 have been a much happier time for Frontier Transport Holdings. I would imagine that high levels of inflation are encouraging more consumers to use busses rather than taxis, although of course this isn’t always possible.

When full results come out next week, I’m sure we will get all the details. In the meantime, we know that HEPS is up by between 60% and 71%, coming in at a range of 57 cents to 61 cents for the interim period. The share price closed 4.3% higher at R5.89.

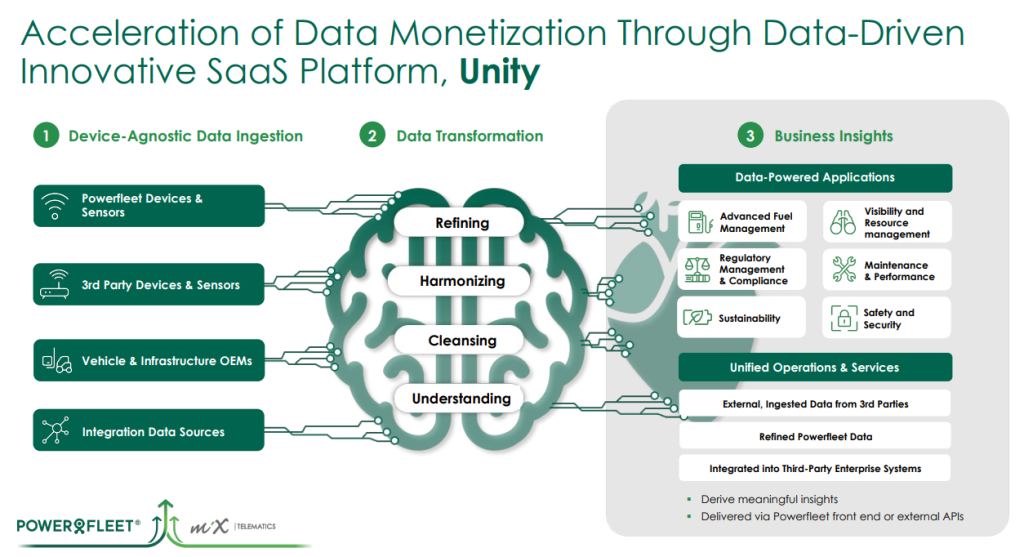

MiX Telematics presents the Powerfleet deal to the market (JSE: MIX)

Shareholders need to be convinced that this transaction is a great idea

Landmark mergers are difficult things to execute and investors know this, which is why corporate management teams have to put in the work to convince shareholders that a proposed merger is going to buck the trend and be successful. Sadly, most mergers end up being a disappointment.

The MiX Telematics – Powerfleet deal has one of the better deal rationales that I’ve seen before, namely being the achievement of scale. Two sub-scale players can genuinely create value by combining efforts and becoming stronger as a result.

I do however get nervous when I see companies talking about a Rule of 40 performance, which is a silly rule of thumb from venture capital land that talks to growth and usually adjusted EBITDA margin. I don’t know too many local investors who care much about the Rule of 40. Around here, we care about free cash flow.

For those of you who like tech and fancy slides, check this one out:

If you are a MiX shareholder, or you are just curious about this space, then you’ll find the presentation here.

MTN reduced its non-rand debt (JSE: MTN)

In this case, a tender offer has nothing to do with something you say to your romantic partner

The near-term stress for MTN is the same as it’s been for a while: the balance sheet. Forex is a nightmare for African businesses and the difficulties in repatriating cash from countries like Nigeria have given MTN many headaches. It’s also given MTN a rather ugly share price chart, with a 52-week high of R149 and a current price of under R94.

To try and improve the balance sheet, MTN is focused on reducing non-rand debt. In other words, US$-denominated debt. To this end, MTN invited noteholders of the $750 million 4.755% notes due November 2024 to tender them for an early redemption. Tenders of $353.1 million were received, so that’s an early reduction of debt.

Although the total level of holding company leverage is relatively unchanged at 1.5x after this early settlement, non-rand debt as a percentage of total debt is now down from 37% to 24%.

PPC has decided to sell the Rwandan business (JSE: PPC)

The group is focusing on its southern African markets

PPC has agreed to sell its entire shareholding in CIMERWA PLC in Rwanda to National Cement Holding Limited. This is a cash deal worth $42.5 million. PPC has held a 51% interest in the company since 2013, with the other 49% listed on the Rwanda Stock Exchange.

The purchaser is a private company that is part of the Devki group, one of the largest manufacturers of clinker and cement in East Africa. The buyer also has operations in Kenya and Uganda.

It’s not difficult to see how CIMERWA fits into the buyer’s strategy. For PPC, this allows the company to unlock a lot of cash and focus on the southern African markets.

It also helps that at March 2023, PPC’s accounts reflected a book value for this investment of $38.5 million. This is therefore a disposal above book value. This is a Category 2 transaction and hence shareholders won’t be asked to vote on it, but a 6.5% increase in the share price gives us a clue as to what the market’s opinion of the deal is.

Sanlam shows improved life insurance margins (JSE: SLM)

There’s also solid growth in volumes

Sanlam released an operational update for the nine months to September 2023 and all looks good, although the share price closing nearly 1% down on the day suggests that the growth has already been priced in.

As we already know from the recent Santam update, the short-term game is difficult at the moment. Margins have been below target because of significant loss events and related underpricing of risk, with strong investment return on insurance funds as the saving grace in that business.

The situation is thankfully very different in life insurance, with value of new life insurance business up 28% and margin improving to 2.90% from 2.46% in 2022. South Africa came in at 2.53% and emerging markets at 5.01%.

There’s more to Sanlam than just life insurance. There are credit and structuring businesses, as well as investment management businesses. The net result from financial services increased by 19%, with the credit and structuring business as the star with 28% growth.

This helped drive a group result that showed net operational earnings up by 35%. A major underlying driver was growth in new business volumes of 13%. The other difference between operational earnings and the financial services result is the investment return on the shareholder capital portfolio, which was much improved in this period thanks to market performance.

As a reminder, the Absa LISP transaction closed on 1 November 2023, adding R66 billion of assets under administration to the Glacier platform in the retail affluent category. Another major move was the Capital Legacy transaction, which closed in August with a cash outflow of R904 million. The group also bought the funding instrument in the B-BBEE vehicle from Standard Bank at a price of R2.4 billion. A special dividend from Santam of R1.2 billion helped pay some of these major amounts, but there’s still a sharp decrease in discretionary capital from R3.2 billion to R1.1 billion.

The other major corporate action was the Sanlam Allianz joint venture, which started operations in September. It will be reported in Sanlam’s accounts from 1 October.

Looking ahead, the group expects performance in the final quarter to result in the second half of the year being similar to the first half. The results are sensitive to movements in global investment market levels, so don’t expect great numbers out of Sanlam if broader markets don’t do well.

Little Bites:

Director dealings:

The chairman of WBHO (JSE: WBO) is “restructuring his retirement portfolio” with a sale of R12.5 million worth of shares.

An executive at Investec (JSE: INL | JSE: INP) sold shares worth £307k.

There’s another purchase of Lighthouse Properties (JSE: LTE) shares by a trust linked to Mark Olivier. Perhaps Des de Beer is on holiday. Either way, the purchase is worth over R5.7 million.

A prescribed officer of ADvTECH (JSE: ADH) sold shares worth R2.4 million.

An associate of the company secretary of Stor-Age (JSE: SSS) has bought shares worth around R620k.

The company secretary of Growthpoint (JSE: GRT) has sold shares worth R273k. Although these relate to scheme options vested, the announcement doesn’t make it explicit that this is only the taxable portion, so I’m assuming it’s a full sale.

An associate of a director of Wesizwe Platinum (JSE: WEZ) is still selling shares, this time to the value of around R210k.

An associate of Christo Wiese bought shares in Collins Property Group (JSE: CPP) worth R220k.

Value Capital Partners is an institutional investor that has director representation on its portfolio companies, like Altron (JSE: AEL). Any further purchases of shares are therefore classified as purchases by an associate of directors. Although the messaging is similar, the quantum isn’t a fair comparison to other director dealings as this is an institutional shareholder. Hopefully you’ll agree with my view when I point out that the latest purchase of shares is to the value of R23.9 million.

Brikor (JSE: BIK) is currently under offer. This doesn’t change the requirement for the company to announce earnings updates. In a trading update, HEPS for the six months ended August has been indicated at between 2.4 cents and 2.9 cents. The prior period was break-even, so the percentage increase isn’t meaningful.

I think that shareholders at Ethos Capital Partners (JSE: EPE) are a little bit gatvol of the discount in the share price, voting down a resolution related to a general authority to issue shares for cash.

In case you missed it on the news, climate protestors disrupted the Sasol (JSE: SOL) AGM to the point where it has to be reconvened. The Chairman invited the protestors to meetings with representatives of the board, which they declined. In other important news, CEO Fleetwood Grobler’s replacement has been announced as Simon Baloyi, who will move into the role on 1 April 2024. Grobler will stick around in an advisory role until 31 December 2024. This is an internal promotion, as Baloyi is currently Executive Vice President, Energy Operations and Technology. Incredibly, Grobler is celebrating 40 years with the company in various roles and Baloyi has been there since 2002!

If you are interested in learning more about Jubilee Metals (JSE: JBL), then you’ll be pleased to learn that there’s a brand new corporate presentation available on the website. You’ll find it here.

As a reminder of the ongoing dilution that comes with being an investor in a junior mining company, Orion Minerals (JSE: ORN) issued $2.27 million worth of shares to an option holder who acquired those options as part of the capital raise earlier this year.

CAFCA Limited (JSE: CAC) is the company that you can be more than slightly forgiven for never having heard of. It is completely illiquid and couldn’t be more obscure. Nonetheless, I like to include everything on SENS, so the update here is that a dividend of 7.90 US cents has been declared as part of the release of financial results. The results are in Zimbabwean dollars, so there are some very large numbers as that currency is worth so little.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I recapped five important stories on the local market:

NEPI Rockcastle is seen as one of the better REITs on the local market and a recent update shows why.

MultiChoice is in for a long journey with Showmax, at a time when the rest of the business is facing substantial other challenges.

Santam is focused on repricing risk, which means upward pressure on short-term insurance premiums across the industry.

Shoprite is doing an exceptional job of growing volumes, with further market share gains that look especially impressive when compared to a competitor like Woolworths.

Richemont saw sales drop in the Americas region and margins are under pressure across the board, so is the online side of the business proving to be a distraction?

The first exchange-traded fund (ETF) was launched 30 years ago in the US, the beginning of an industry that has grown exponentially to now holding nearly US$10 billion in assets under management.

In honour of this milestone, Satrix’s Chief Investment Officer (CIO), Kingsley Williams has done some future-gazing to see what might be next for this innovation in investing that has fundamentally impacted the landscape.

By 2030, what will the ETF landscape look like?

BlackRock forecasts the global exchange-traded fund (ETF) industry will grow to $25 trillion by then. Kingsley Williams, CIO at Satrix*, says ETF’s growth potential in South Africa is immense. Currently, index funds and ETFs account for over 50% of equity assets under management (AUM) in the US, almost 25% of assets in Europe, and 15% within equity and listed property categories in South Africa. That leaves ample growth opportunity, as other regions around the world catch up to the US.

Williams added that ETFs are an efficient way to harness investment themes, which are being shaped by five megatrends that are dominating economies and financial markets globally. These trends will continue into 2030 and beyond, shaping the investment landscape and providing opportunities for investors to harness these structural shifts.

Five global megatrends shaping the investment world of tomorrow:

Shifting economic power:

The International Monetary Fund forecasts that China and India will generate about half of all global economic growth in 2023. Power is moving from West to East, and ETF products are evolving to offer exposure to the East, including the Satrix MSCI China ETF and Satrix MSCI India ETF. Further evidence of this economic shift is how the BRICS nations (Brazil, Russia, India, China and South Africa), which represent the largest developing economies, have surpassed the G7 as the largest industrialised nations (US, UK, Germany, France, Japan, Italy and Canada) in terms of share of global GDP based on Purchasing Power Parity.

Shifting demographics and ageing populations:

In 1963, the fertility rate was 5.3 births per woman. By 2050, the UN forecasts this will fall to 2.1. Conversely, the global life expectancy in 1950 was 46.5 years; by 2050, this should be 77.3. Increased longevity and declining birth rates mean many countries have ageing populations, prompting seismic shifts to cater to older individuals. As populations age and technology enables further medical advances, this creates a virtuous circle as increased spending goes towards healthcare. Satrix launched the Satrix Healthcare Innovation ETF as a thematic strategy to enable investors to gain exposure to this megatrend within their portfolios.

Technological innovation and breakthrough:

A 2021 McKinsey paper suggests there will be more tech innovation in this decade than there was in the previous 100 years. Tech underpins multiple megatrends, and the Satrix Nasdaq 100 ETF is a great expression of capturing blue-chip game-changing companies in this space.

Rapid urbanisation:

The UN is expecting Africa’s population to double by 2050. People will migrate en masse to urban areas, creating mega cities worldwide. Satrix has Smart City Infrastructure and Global Infrastructure ETFs to address the titanic task of creating these cities, sustainably.

Climate change and resource scarcity:

By 2030, humans will need to have halved our greenhouse gas emissions to stop the most devastating effects of global warming from transpiring. We are running out of time, according to the Intergovernmental Panel on Climate Change. To help tackle this longstanding megatrend, Satrix has two ETFs which focus on climate transition while maximising exposure to highly rated ESG companies across the globe.

Trends shaping the South African ETF landscape of 2030

PwC predicts global ETF AUM will experience a 17% compound annual growth rate across the next five years. It pins this on recent record inflows, and a plethora of innovative new players and products. Williams expects robust growth locally, prompted primarily by institutional adoption and offshore interest.

He adds, “ETFs have been accessed primarily by the direct market locally. Now, we’re seeing adoption in intermediated spaces. In 2030, this trend is likely to continue, alongside offshore growth. As ETFs are traded more via Linked Investment Service Providers (LISPs) and other intermediated platforms, we’ll see increased activity that will naturally deepen the capital market process, lowering spreads and creating an ecosystem that attracts even more institutional players.

“Over the next decade, we’ll continue to see consolidation, with more refinement. Relative to income earned it’s costly to set up a low-margin business, so ETFs are likely to stay limited to the big players.”

Here, Williams gives further predictions for the local ETF landscape in 2030:

Institutional adoption:

There’s an upsurge in other African countries of institutional investors using ETFs to gain exposure in their portfolios. We’ll see this continue in South Africa as well. Swift uptake of interest-bearing asset classes: There’s a rapid roll-out of new asset classes that historically haven’t been available in ETF form, such as bonds, commodities and even crypto. Now, globally, there’s a surge of flows going to interest-bearing asset classes. This means more market transparency when it comes to pricing, and further democratisation as these asset classes become increasingly accessible.

Active management:

Globally, in the fixed interest space, there’s a proliferation of actively managed ETFs. For several consecutive quarters now, we’ve seen funds flow into this space worldwide. South Africa traditionally lags a little, but as uptake snowballs globally, we’re likely to see local adoption of actively managed ETFs as well.

ESG:

ETFs allow people to express their investment views and choose what they want to be exposed to. This includes ESG and sustainability-focused funds, like the Satrix MSCI World ESG and Satrix MSCI Emerging Markets ESG ETFs. Going into 2030, sustainable investment will remain a focus worldwide.

Traditionally, ETFs were synonymous with indexing and equity. Now, they’re being seen as a tool that benefits all players, across the asset class spectrum. There’s an increasing array of assets and investment strategies wrapped into the ETF vehicle, which makes them building blocks that give investors an almost infinite array of choices. This – plus their flexibility, low fees and dependability – is catapulting them into a new chapter of hyper-growth that’s likely to continue for the next decade and beyond.

*Satrix is a division of Sanlam Investment Management, an authorised financial services provider.

CIS disclosure

Satrix Investments (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). The information above does not constitute financial advice in terms of FAIS. Consult your financial adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

AH-Vest gets the squeeze (JSE: AHL)

It’s anything but All Joy at this small food manufacturer

With a market cap of just R16 million, it’s hard to imagine why AH-Vest is even listed. The best market bid is 1 cent a share, with the offer at 35 cents. It’s a total waste of time and is surely a take-out target for one of the major food groups, especially as All-Joy is a decent brand.

Load shedding really hurt the results for the year ended June 2023, with significant lost sales due to lost production volumes. Retailers don’t like it when suppliers can’t meet demand, so that might be a problem going forward as well. A further issue is increased input costs and supply chain pressures.

The combined impact is that HEPS is down by 33.2% from 2.02 cents per share to 1.35 cents per share.

Burstone releases its first set of results under that name (JSE: BTN)

The fund was previously called the Investec Property Fund

Burstone Group has released results for the six months to September 2023, with this year having been all about the internalisation of the management company and the rebranding of the group. Sadly, none of those things do anything about the cost of debt, with distributable income per share down by 5% as this REIT struggles along with most of the others in this environment.

The South African portfolio achieved 2.0% growth in like-for-like net property income. The European portfolio was good for 7.9% growth. The underlying portfolios are moving in the right direction, but the bankers are getting the incremental benefit.

For the full year, previous guidance has been maintained. This means distributable income per share growth of between 0% and 2%. That would be a strong second half that requires growth of 5% to 9%. This won’t be easy when the loan-to-value ratio is 43%.

It’s also worth noting that Sam Leon, the ex-CEO (back when it was called Investec Property Fund), has retired as a non-executive director of the company.

A change of year-end means there’s a seasonal skew in the numbers

In order to align with the year-end of its controlling shareholder Castleview Property Fund (JSE: CVW), Emira has changed its year-end from June to March. This means that the interim period to September 2023 has to be compared to the six months ended December 2022. In other words, the festive season is in the base period but not this one. Clearly, that limits comparability.

There are other elements that hurt comparability, like the substantial disposal of Enyuka.

I’ll therefore just focus on the latest numbers in isolation. The loan-to-value ratio is 41.2%, so that’s under control but definitely a happier place for bankers than shareholders. The net asset value is R17.03 and the current share price is R8.65, so that’s a bigger discount than you’ll usually see. The interim dividend is 61.74 cents, which is a yield of 7.1% just for the first six months!

For reference, that’s a pretty similar yield to what my residential landlord earns from me in 12 months. Again, if you really want to own property, there are “buy-to-let” opportunities right there on the JSE. They are called high yielding REITs.

Gold Fields gives an operational update (JSE: GFI)

Incoming CEO Mike Fraser will be in his comfortable chair on 1 January 2024

The quarter ended September has seen a 9% decrease in year-on-year group attributable gold-equivalent production at Gold Fields. That’s a mouthful. It’s also a mouthful that went the wrong way, particularly in Ghana.

With lower gold sales and inflationary increases in costs, group all-in cost increased by 27% year-on-year. All-in sustaining cost is 30% higher. It’s not hard to see why an increasing gold price is so important to these mines.

Net debt to EBITDA came in at 0.48x, a bit higher than 0.42x at the end of June.

The Salares Nortes project is 97% complete vs. 94% at the end of June. The group invested $111 million in this quarter alone. First gold is expected in December 2023, so that’s a nice Christmas present that sure beats coal under the tree!

In other corporate activity, the group is working with the government in Ghana to obtain approval for the proposed joint venture in that country with AngloGold Ashanti.

Investec looks back on a period filled with corporate activity (JSE: INP | JSE: INL)

Nobody can accuse the management team of sitting on their hands

Investec has released results for the six months to September and they reflect some major strategic actions.

The merger of Investec Wealth & Investment UK with the Rathbones Group is a smart transaction that delivers scale in that market, with that shareholding being equity accounted going forward. Investec sold its property management companies to Burstone Group for a rather eyewatering sum, so that was helpful to shareholders.

In the prior year (which is relevant for comparability), Investec distributed a 15% shareholding in Ninety One to shareholders and restructured The Bud Group to facilitate an orderly exit.

To help investors understand what the group now looks like, adjusted numbers have been presented that show what the six months would’ve looked like had the Rathbones and Burstone transactions taken place at the beginning of the period. On that basis, adjusted operating profit would be up 11.2% in GBP and HEPS would be up 15.3%.

Looking deeper, there was growth in both net interest income (up by double digits) and non-interest revenue. The cost to income ratio improved, as operating costs were up 12.3% in constant currency. The credit loss ratio of 32 basis points is well up on 16 basis points in the base period and towards the upper end of the through-the-cycle range of 25 to 35 basis points. The bank notes that rather than an overall deterioration in the credit book, there have been specific client stresses.

Return on equity improved from 12.9% to 14.6%. Please remember that this is as reported in GBP, so that’s a hard currency return.

The dividend is up 14.8% and around R6.8 billion has been invested in share repurchases since that programme was announced, so significant value is finding its way to shareholders. This is good stuff overall!

I don’t really see the appeal of investing in hospitals (JSE: LHC)

Life Healthcare isn’t the only reason why, but it’s one of them

It’s very easy to think about a hospital and go “yes, that place is frighteningly expensive and highly necessary and must be a great investment” – except, it isn’t. Over five years, Life Healthcare is down 30% and I would remind you that there was a pandemic in the middle of that period!

If you followed the hospital groups during the pandemic, you’ll know that COVID actually wasn’t helpful to them. The only cases running around were COVID, so the high margin voluntary stuff just wasn’t happening. Still, I can’t see the excitement even if we ignore the impact of the pandemic.

For the year ended September, Life grew revenue from continuing operations by 10.3% and normalised EBITDA by 4.4%. The dividend is 10% higher. At least things are moving in the right direction, but in a high interest rate environment I don’t see these as returns that warrant single stock exposure to the group. Remember, any company needs to look good relative to the broad market index, otherwise you should just diversify and own the index. It’s not just about whether they go up.

Normalised EBITDA margin fell from 17.4% to 16.9%, with the company attributing this to a variety of factors ranging from mix effect in revenue through to cost pressures. Margins are expected to remain flat in the 2024 financial year.

Group HEPS is down 16.9% because of the vast costs associated with the disposal of Alliance Medical Group. Adjusting for those in normalised EPS gives you growth of 11.4%. This means that dividend growth of 10% reflects a lower payout ratio.

The Alliance Medical Group transaction is expected to close in the second quarter of the 2024 financial year. The circular was recently released to shareholders, with the vote scheduled for 8 December. With all said and done, there should be £360 million on the table for a special distribution to shareholders.

Rocking out with proper growth at NEPI Rockcastle (JSE: NRP)

This is generally seen as one of the best REITs on the local market

NEPI Rockcastle has given an update for the nine months to September. At first blush, they show growth in net operating income of a very high 23%. There are three acquisitions skewing that higher though, with the like-for-like growth coming in at 14%. Of course, this is still really good!

It’s interesting to note that higher footfall (+6%) and a rise in average spend per visit (also +6%) were equal contributors to like-for-like growth in tenant sales. Against that backdrop, it’s not surprising that there is strong demand for space in these malls, with the vacancy rate down to 2.2%.

Importantly, there is absolute no debt maturing in 2023. The balance sheet was also boosted by a 74% take-up rate on the scrip dividend, bringing the loan-to-value ratio to 32.9%. That’s below the company’s strategic threshold of 35%.

Earnings guidance for the full year has been affirmed at 12% expected growth in distributable earnings per share.

Safari’s distributable earnings have dropped (JSE: SAR)

The main reason is a once-off insurance event in the comparable period

For the six months to September, Safari Investments (a REIT, in case you weren’t sure) reported growth in operating profit of 8.15%, helped by strong occupancy levels. Net asset value (NAV) per share increased by 6.42% to R9.45 per share, with the share price currently at R5.50 and reflecting a substantial discount to NAV.

Despite this, the distribution per share fell by 9.09% to 30 cents per share. This is because the base period included a substantial non-recurring insurance payout that was received by the company. It also doesn’t help that finance costs went up, as this reflects below operating profit.

The group maintains a 100% payout ratio, so the interim dividend is also 30 cents per share.

Southern Sun’s numbers need a careful read (JSE: SSU)

And the good news is that earnings guidance has been increased further

Southern Sun released a further trading statement for the six months to September, which means numbers previously provided to the market have been updated.

The base period included a large separation payment of R313 million post-tax. This number is included in HEPS, but excluded from adjusted HEPS as it is clearly once-off in nature. I would therefore focus on adjusted HEPS, otherwise it looks like the business is going backwards and that isn’t the case.

The base period still had a pretty serious COVID hangover in it, so the year-on-year growth rate looks ridiculous. I would simply focus on the earnings range for adjusted HEPS, which has moved higher. The original trading statement reflected expected adjusted HEPS of 14.5 to 17.4 cents. The updated range is 17.0 to 19.0 cents.

Trellidor: strong enough to keep even the bankers out (JSE: TRL)

For now, at least– but there is much to be done

Trellidor has had some really bad luck, with a labour ruling against the business that absolutely hammered it financially. When you combine this with the prevailing economic climate and all the supply chain issues during and after the pandemic, it’s a recipe for disaster.

When a company breaches lending covenants, it is now at the mercy of the bankers. The funny thing is that the bankers are somewhat at the mercy of management, as they lose their debt investments if the business goes under. In practice, a breach of covenants is basically an opportunity for the banks to fire a warning shot and put pressure on the company. They don’t just pull the rug at the first sign of a covenant breach.

This positive approach seems the be what has happened at Trellidor, with the banks having assessed the FY23 numbers and condoned the breaches, with no additional covenants or conditions imposed. This suggests that the banks are very comfortable with the turnaround plan.

One of the interesting points in the plan is that a significant contract related to roller shutters in the UK is being fulfilled, with an obvious benefit to revenue.

The group is actively looking at ways to improve the balance sheet. The dreaded words “rights offer” haven’t been used at this stage. Instead, the group is looking at a sale and leaseback transaction to free up some capital.

Based on this encouraging development, the debt will be reclassified back to non-current in nature, as it isn’t due within the next 12 months.

I must remind you that the banks are interested in protecting their debt investment and earning the yield. They might be happy, but that doesn’t mean that shareholders will have a good time.

Little Bites:

Director dealings:

The CEO of Shoprite (JSE: SHP) has sold shares as part of an “annual rebalancing of his investment portfolio” – and that rebalancing was a cool R30 million in value.

A director of a major subsidiary of Super Group (JSE: SPG) received a share award worth nearly R3 million and sold every one of those shares on the market.

The recently appointed CEO of AECI (JSE: AFE) has bought shares worth nearly R220k.

The CFO of Spear REIT (JSE: SEA) has bought shares worth R70.6k.

Hilariously, a director of Sable Exploration and Mining (JSE: SXM) bought 5 shares at 13 cents each. Yes, that really is a total trade of 65 cents. If you don’t laugh, you’ll cry.

Afine Investments (JSE: ANI) released a trading statement dealing with the six months ended August. Although HEPS will be within 20 of the prior period, earnings per share will be 24.55% down vs. the comparable period.

Quilter (JSE: QLT) has finalised the odd-lot offer, managing to repurchase nearly 15.8 million of its own shares in the process. That’s a meaty repurchase worth around R315 million. For reference, the market cap is nearly R29 billion. This is a big company.

If you are a shareholder in Premier Group (JSE: PMR), you may want to take a cursory look at the circular released by the company in relation to a new long-term incentive plan.

Globe Trade Centre (JSE: GTC) literally has no liquidity on the JSE whatsoever. In the very unlikely event that you are a shareholder, then you should know that the company is no longer pursuing the acquisition of Ultima Capital. I guess you should also know that the results for the nine months to September have been released, showing rentals up by 7% but a loss after tax of EUR 6 million.

The recent World Cup win by the boys in green and gold brought much needed relief, albeit for a fraction of time, from the daily bombardment of negative news that has become a way of life for South Africans. But like all good things, this hype has faded, and our attention is once again focused on making the best of, let’s face it, a very difficult setting.

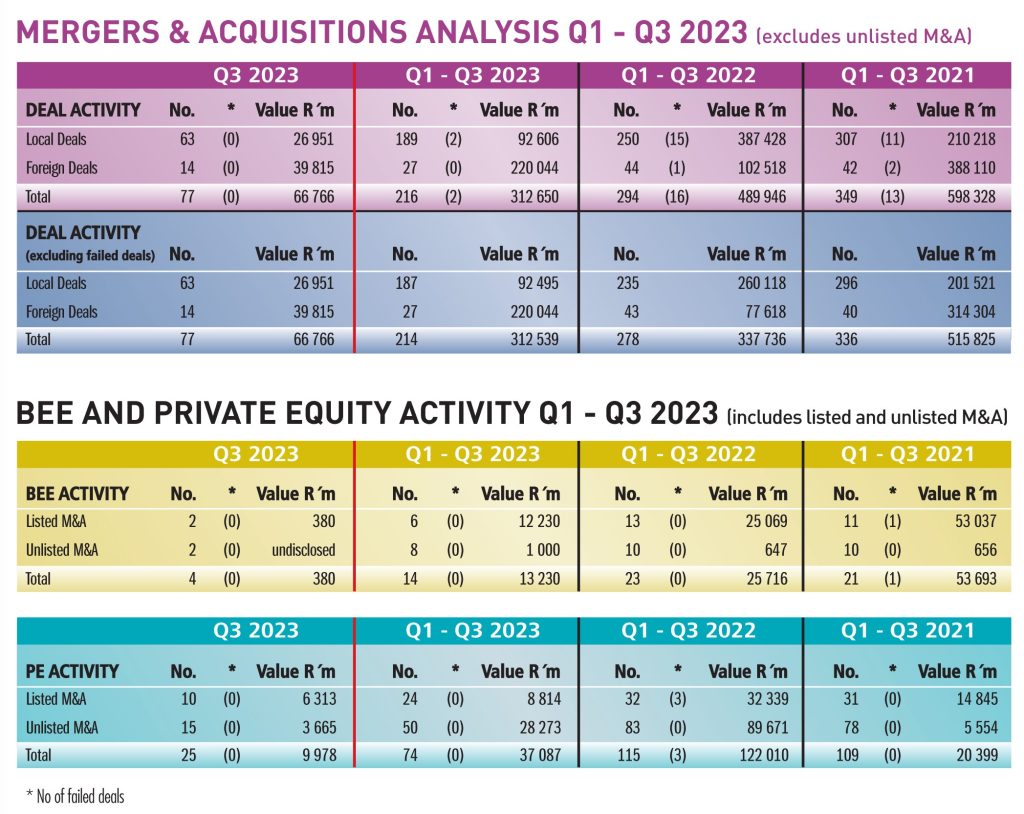

M&A activity is, by its very nature, resilient in tough times – rather, it is the type of deals completed that changes. Nevertheless, the industry has come under pressure. For the period from January to end-September 2023, deal activity declined 26% year-on-year, and almost 40% when compared with deal activity in 2021. Private Equity, an important driver in the dealmaking space, also declined – down 36% on the previous year.

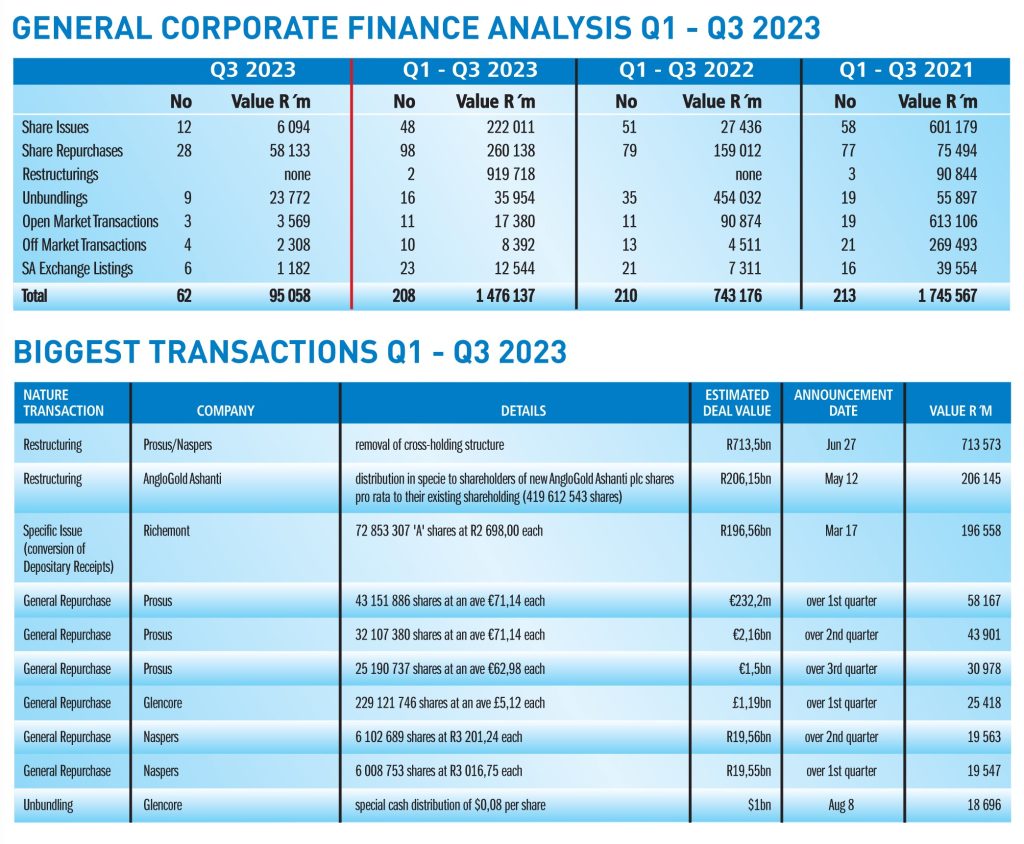

Share issues and repurchases continue to characterise the general corporate finance activity in 2023, with R222 billion raised from the issue of shares and R260 billion the value of shares repurchased. The repurchase programmes of Prosus, Naspers and Glencore account for most of this value, while the aggregate value of Richemont’s issue of A shares (conversion of depositary receipts) reported in Q1 was R196,56 billion.

A worrying trend is the exit of companies from Africa’s largest stock exchange, the JSE. Over the past six years (excluding 2023), an average of 25 companies have delisted each year. For the year to end-September, 19 companies have delisted, with a further five set to do so within the coming months. New listings have all but dried up. Private equity has been identified as one reason for the loss of listings, providing financing in softly regulated private markets. In 2017, the JSE welcomed 21 new listings; in the year to September 2023, this figure had dropped to three. Secondary listings on A2X continue to increase, with 18 recorded for the period under review.

It is becoming increasingly clear that South Africa’s approach to foreign affairs will play an important role in determining investment and growth outcomes for the country. While investor interest is present, with a good supply of deals in the pipeline, the challenge is getting them across the line. Investor sentiment – weighted down by the macroeconomic environment, geo-political influences, and the impending local elections – is adopting a wait and see attitude.

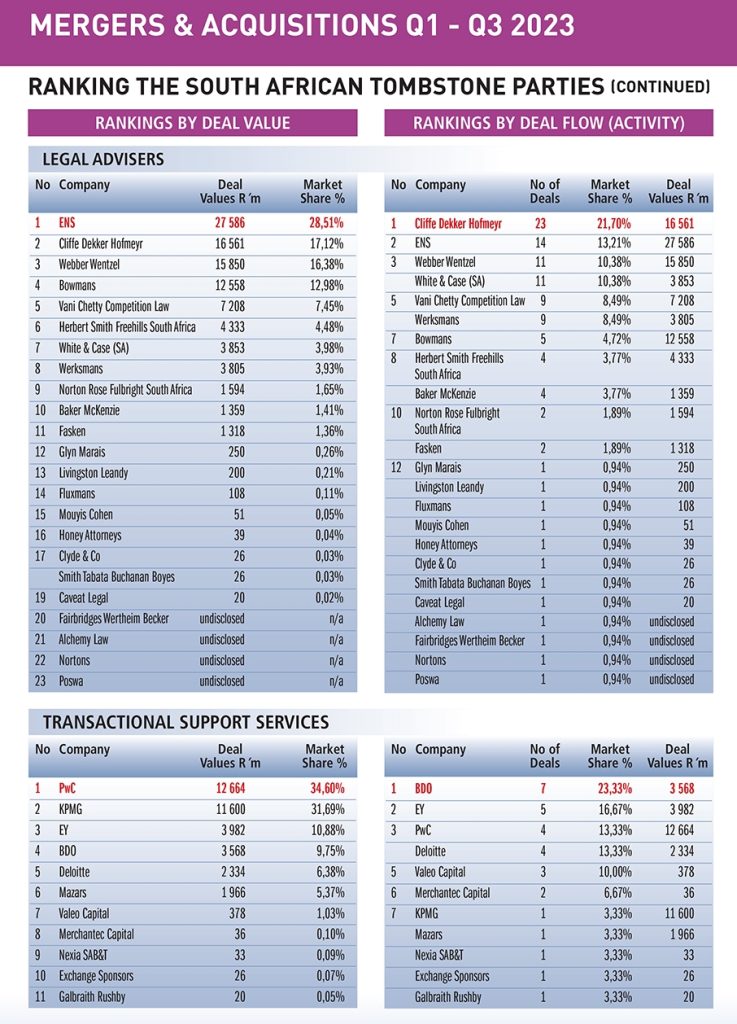

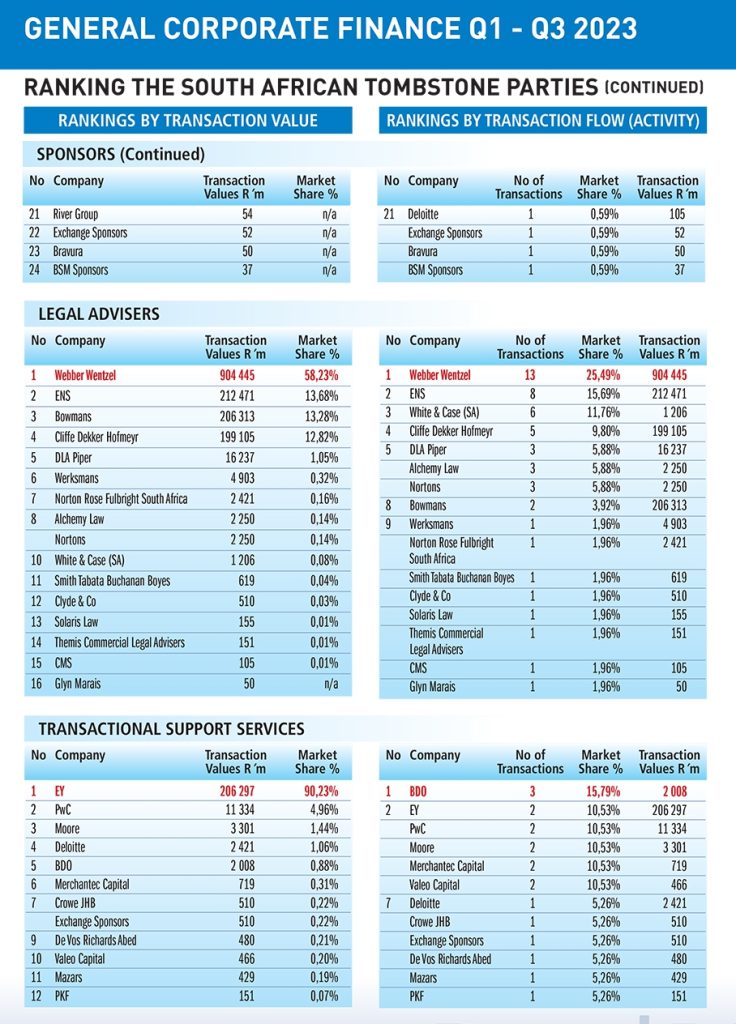

DealMakers Q1-Q3 League Table – M&A activity by the top South African advisory firms (in relation to exchange-listed companies).

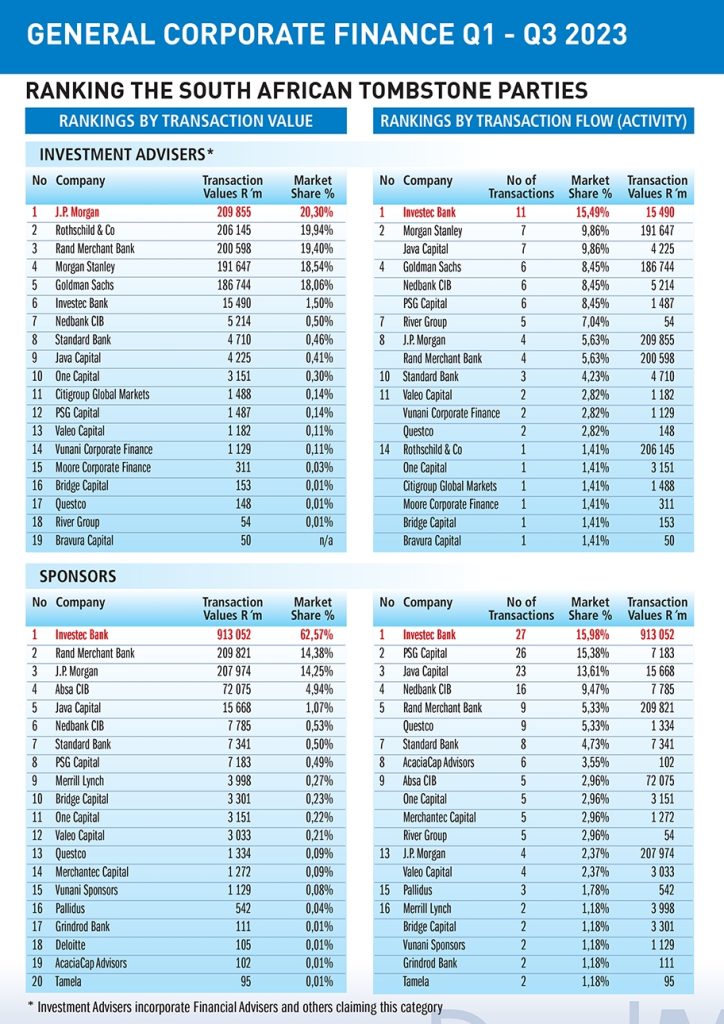

DealMakers Q1-Q3 League Table – General Corporate Finance activity by the top South African advisory firms (in relation to exchange-listed companies).

Having failed to persuade Teck Resources’ minority shareholders earlier this year, to merge the Teck operations with that of Glencore’s, Glencore has reached an agreement with Teck to acquire a 77% stake in its steelmaking coal business Elk Valley Resources (EVR) for US$5,93 billion in cash, on a cash free debt free basis. Nippon Steel Corporation will hold a 20% stake in EVR and POSCO the remaining 3% – both of whom have existing relationships with Glencore. The company remains committed to the demerge of the combined businesses, believing that a standalone company containing its combined coal and carbon steel materials business, including its stake in EVR, would attract strong investor demand given its yield potential.

Absa’s Mauritius subsidiary has reached an agreement to acquire the domestic Wealth and Personal and Business Banking business of The Hongkong and Shanghai Banking Corporation (HSBC) in Mauritius. Financial details were undisclosed.

Deneb Investments is to dispose of the property situated at 34 Kinghall Avenue, Epping in Cape Town to Gerber Advisory Specialists for R64,35 million. The property is not considered core to Deneb’s strategy.

Unlisted Companies

Pineapple, the local digital insurance provider, has announced the conclusion of a R400 million funding round. The round was led by new investors, Futuregrowth, Talent10 and Mineworkers Investment Company while the business received additional investment support from existing investors including Old Mutal ESD, Lireas Holdings, ASISA ESD Fund and E4E Africa. Pineapple’s technology allows it to service customers at 20% of the cost of traditional insurance providers.

Local proptech startup Neighbourgood has acquired Cape-based traveltech startup Local Knowledge in a move expected to transform the travel and hospitality experience. The deal will combine Neighbourgood’s 1000-plus living and working spaces with the Local Knowledge’s ability to provide the next-gen with unforgettable travel experiences via its technology.

Convergence Partners has increased its stake in African broadband infrastructure company CSquared through the acquisition of the stake held by Google. In addition, the pan-African impact investment management firm took part in CSquared’s US$25 million equity capital raise.

ASX-listed Vanadium Resources (VR8) has increased its interest in Steelpoortdrift by 4.59% to 86.49% through the completion of a transaction with Math-Pin, its BEE party. The acquisition is payable via a combination of R2,930 in cash and 8,092,810 share options to acquire VR8 shares, which will on exercise, represent 1.48% of the issued share capital of VR8.

Private Equity fund managers 1K Africa and Ascension Capital, have announced an investment in South Africa’s payment profile hosting credit bureau, Consumer Profile Bureau (CPB). The undisclosed investment will be used to help CPB scale its market position and services including its unique technology for tracing, credit verification and debtor profiling.

UK global sports media business LiveScore Group has increased its stake in Wonderlabz, a Cape-based software development and talent hub, from 25% to 100%.

UK headquartered online trading services provider ATFX, has acquired Khwezi Financial Services, a South Africa over-the-counter derivative provider. Financial details were undisclosed.

Liquid Intelligent Technology has received R900 million in funding from the IFC and Rand Merchant Bank to be used to scale affordable broadband access in the Eastern Cape Fibre Project.

This week was all about share repurchases and profit warnings.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 6 – 10 November 2023, a further 4,351,713 Prosus shares were repurchased for an aggregate €124,7 million and a further 326,470 Naspers shares for a total consideration of R1,04 billion.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of US$1,2 billion by February 2024. This week the company repurchased a further 10,010,000 shares for a total consideration of £43,88 million.

Super Group has concluded an intra-group repurchase of 5,309,812 shares at a price of R34.51 per Super Group share for an aggregate R183,24 million. The shares will be delisted.

Quilter plc has repurchased 15,798,423 shares in terms of its odd-lot offer. A total of 15,798,423 shares were acquired – 291,711 shares at 88.10 pence and 15,506,712 shares at R20,08 per share.

Five companies issued profit warnings this week: Quantum Foods, Dipula Income Fund, Trematon Capital Investments, Capital Appreciation, Afine Investments and AH-Vest.

Cognition was the only company this week to issue a cautionary notice. The company is in discussions with its holding company, Caxton and CTP Publishers and Printers which, it says may result in an offer by Caxton to acquire those shares in Cognition not already held. Will this be another delisting from the JSE?

Nigerian B2B marketplace for auto dealers, Shekel Mobility, has raised over US$7 million in a debt and equity seed round. Ventures Platform, MaC Venture Capital, Y Combinator, Rebel Fund, Unpopular Ventures, Maiora Capital, PageOne Lab, Phoenix Investment Club, Heirloom VC, Pioneer Ventures and other angel investors provided the US$3,2 million equity funding with the remaining US$4 million in debt financed by Zedvance, VFD Microfinance Bank, Zenith Bank, Fluna and others. This is the second time the mobility fintech has raised funds this year – in January the team announced a US$1,95 million oversubscribed pre-seed round led by Ventures Platform. Other investors included Y Combinator, Voltron Capital, Zedcrest and some angel investors.

RMB has provided N$500 million in new debt funding and has refinanced a N$100 million loan for Oryx Properties to help fund the acquisition of Dunes Mall in Walvis Bay, Namibia. The property fund announced the acquisition in May and undertook a ‘rights offer’ to part fund the N$620 million purchase price among other things. The rights offer was 82.4% taken-up, raising N$312,9 million.

The Namibia Infrastructure Development and Investment Fund (NIDIF), managed by Eos Capital, has acquired a minority stake in the Namibian business of Lightstruck, a fibre infrastructure company specialising in open access last-mile fibre networks. Financial details were undisclosed.

Lapaire, an African eyecare business headquartered in Abidjan, Côte d’Ivoire and operating 54 optical shops across seven African countries, has raised an undisclosed sum from Beyond Capital Ventures. The investment forms part of Lapaire’s Series B investment round. The Series B funding will aid the company’s plans to launch in five new markets including the DRC, Ghana, Guinea, Nigeria and Tanzania.

Pan-African tech company, CSquared Link Holdings (Mauritius), announced an equity capital raise from both new and existing investors. The US$25 million in funding came from Convergence Partners Digital Infrastructure Fund (CPDIF), the International Finance Corporation (IFC) and the International Development Association’s (IDA) Private Sector Window Blended Finance Facility. It was also announced that CPDIF had acquired Google LLC’s stake in CSquared.

PZ Cussons Nigeria has notified shareholders that the offer by majority shareholder PZ Cussons (Holdings) to acquire the remaining 26.73% held by minorities for ₦21 per share announced in September, has been increased to ₦23 per share.

Union Bank of Nigeria plc disclosed that the offer price to minorities had been increased from ₦7 per unit to ₦7.70 per unit. Titan Trust Bank acquired a majority stake in December 2021 and offered to buy out the remaining 6.59% stake from minorities through a mandatory offer in October 2022. The Bank is currently finalising the process of obtaining approval to delist from the NGX.

African Export and Import Bank (AFREXIM) has signed a debt funding package with Oando plc comprising a US$500 million senior secured reserved based lending facility and a US$300 million receivables backed term loan facility. The deal was signed at the Intra-Africa Trade Fair in Cairo, Egypt.

UAE-based Sky One has acquired a substantial stake in Libyan airliner Fly Oya. Financial terms were not disclosed.

ASX-listed 88 Energy has, through a newly formed subsidiary Eighty Eight Energy (Namibia), signed a three stage farm-in agreement with Monitor Oil and Gas Exploration (Namibia), a wholly-owned subsidiary of Monitor Exploration, to earn up to a 45% non-operated working interest in onshore Petroleum Exploration Licence 93 (PEL 93) located in Namibia’s Owambo Basin. The farm-in agreement schedule consists of three stages. Stage one: [20% working interest] the payment of US$3,7 million in consideration for past costs and the first US$3 million of the 2024 work programme. Stage two: [17.5% working interest] payment of US$7,5 million of the first well gross cost. Stage 3: [7.5% working interest] option to fund the first US$7,5million of the second well gross cost.

Holcim has announced the sale of its businesses in Uganda and Tanzania. In Uganda, Hima Cement has been sold to Sarrai Group for an enterprise value of US$120 million. In Tanzania, the 65% stake in Mbeya Cement Company has been sold to Amsons Group for an undisclosed sum.

Moroccan transport and logistics startup, CloudFret, has raised €2 million (US$2,1 million) from AfriMobility and Azur Innovation Fund. Operational in Morocco since 2021, the company expanded to Marseille and now looks to expand further with the introduction of an innovative solution geared towards optimising empty truck returns, with a focus on the intra-European market.

Akhdar has announced a six-figure investment from Value Maker Studios (VMS). The Egyptian edtech is an Arabic language platform that provides audiobook summaries. The funding will be used to expand its existing presence in Saudi Arabia.

SPE Capital and Proparco have sold Amanys Pharma to Laprophan for an undisclosed amount. The pair acquired the company in 2020 (known at the time as Saham Pharma) and this sale marks the second exit for SPE AIF.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months