")

Double-digit HEPS growth at KAL Group (JSE: KAL)

This looks like a strong outcome for shareholders

KAL Group has released a trading statement for the six months to March 2026. They’ve given some helpful underlying details around the drivers of performance, with HEPS expected to be up by between 10.5% and 14.5%.

Recurring HEPS, also an important metric, is up by between 13.1% and 17.1%. That’s a great set of numbers for investors, with the share price up 18.5% over the past 12 months.

To achieve this growth, KAL managed a 4.8% increase in retail revenue, a 7.4% increase in agri input revenue and a 6.7% increase in fuel volume sales.

My concern here would be the impact of the rapid increase in fuel prices on the fuel business in the second half of the year. A higher fuel price is worse for retail fuel businesses, not better. As I understand it, the retailer makes a similar amount per litre regardless of the fuel price, but consumption drops when prices skyrocket. It also means that consumers have less money to spend at the forecourt shop.

Still, on a modest Price/Earnings multiple and with a solid underlying business, they will hopefully weather the storm without too much pain for investors.

I’m curious – how do you plan to respond to higher fuel prices?

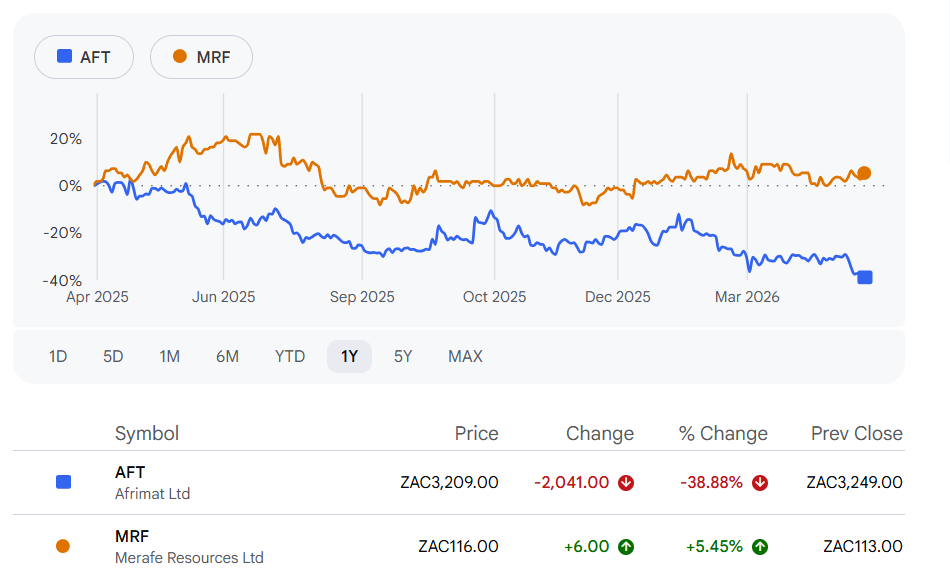

Metair has achieved some breathing room on the balance sheet (JSE: MTA)

But at what cost?

Metair always seems to be on the receiving end of bad luck. But for once, they’ve been thrown a bone by the universe in the form of a refinanced debt package for the “SA Obligor” group.

In simple terms, the reference to “SA Obligor” means the debt linked to Hesto Harnesses and the remaining South African subsidiaries. When banks start carving up groups and lending based on specific underlying assets, you know the risks are tricky to manage.

Despite plenty of concern about the underlying automotive manufacturing industry, as well as the difficulties in turning AutoZone around (remember that it was acquired out of business rescue), Standard Bank has approved a refinancing of the debt package. This extends the term of the full R3.3 billion to five years, with a structured repayment profile that is closely aligned with the group’s expected earnings growth and cash flows.

Importantly, this takes into account the capex in the year ending December 2026. A feature of Metair’s business is that they incur significant capex when an underlying customer introduces a major new vehicle model. This means that a structured debt package rather than a traditional amortising loan is required.

Another critical improvement to the package is that the cumulative EBITDA performance hurdle has been removed. The group has been operating under the extreme pressure of quarterly EBITDA targets, something that is very difficult for a business like Metair. This gives them more flexibility and reduces the risk of forced equity raises and asset disposals.

They aren’t quite done yet, with a working capital facility of R600 million that will be subject to review during the third quarter of this year. For now at least, they’ve got room to breathe on the term debt.

And the cost of debt, you ask? The SENS announcement doesn’t confirm this. They simply note that the reference rate has changed from JIBAR to ZARONIA (no surprise there). I suspect that this additional balance sheet flexibility has come at a cost.

If you’re keen to learn more about Metair, you can check out the recording of the very recent Unlock the Stock presentation and Q&A session here.

Pick n Pay moves into a s189 process at store level (JSE: PIK)

They are trying to address their cost base

Pick n Pay’s turnaround has faltered recently. Well, to be honest, I’ve always been bearish on it, but the last set of numbers confirmed my beliefs that it would be much harder than most people realise.

Having upset the market back in February with a trading update, Pick n Pay has now announced a s189 process aimed at resetting the store labour model. They are specifically targeting scheduling flexibility and benefits and allowances, particularly those that aren’t in line with peers. The objective isn’t to reduce head count, although I’m sure the changes to remuneration will lead to some attrition along the way.

It’s important for the sustainability of companies to make sure they are running efficiently. It’s also a reminder that bad strategies lead to poor outcomes for all stakeholders, including employees. Head office employees have already been through retrenchment and salary freeze processes. They now need to unlock savings at store level.

On The Money Show with Stephen Grootes on Monday evening, I discussed the Pick n Pay situation and the immense difficulties they face in a wildly competitive grocery market. Specifically, I talked about Pick n Pay’s “right to win” (or lack thereof). You’ll find the segment here (8 minutes long).

The share price is down 32% over 12 months. It’s fallen by a nasty 23% on a year-to-date basis.

Even Vodacom is a growth company these days (JSE: VOD)

With macroeconomics holding steady, HEPS has jumped sharply

Get ready for a potentially significant move in Vodacom on Tuesday. The company released a trading statement after market close on Monday and it tells quite the positive story.

For the year ended March 2026, Vodacom’s HEPS increased by between 20% and 25%. That’s a really impressive growth rate, particularly for the telco that has historically been seen as the “safe” choice vs. sector wild child MTN (JSE: MTN).

Vodacom has upped the risk in recent years in pursuit of growth, with deals like the major push into Egypt. If the macroeconomics can keep it together in East Africa and Egypt, then Vodacom can pull off growth rates that will attract some attention away from rivals.

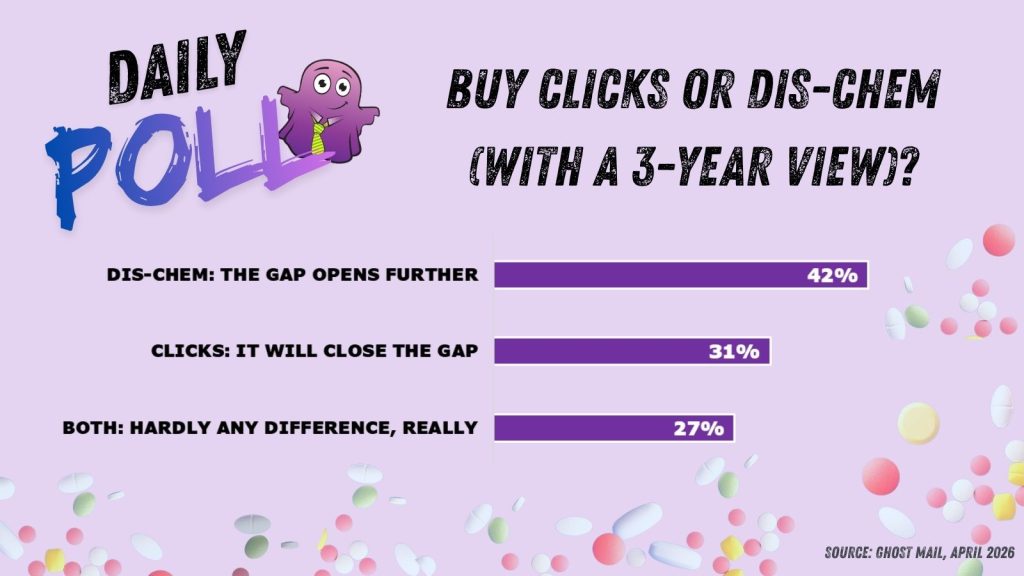

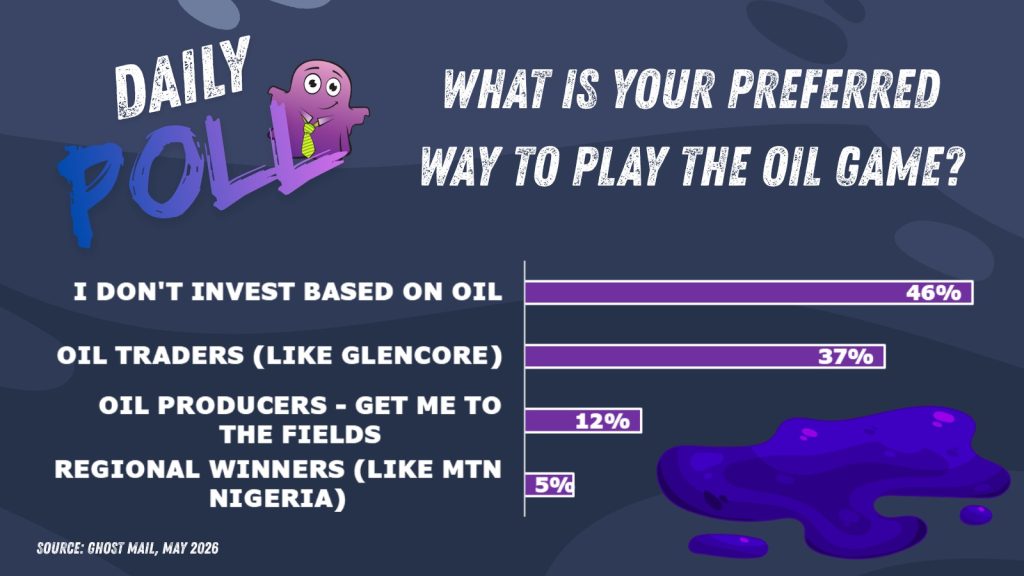

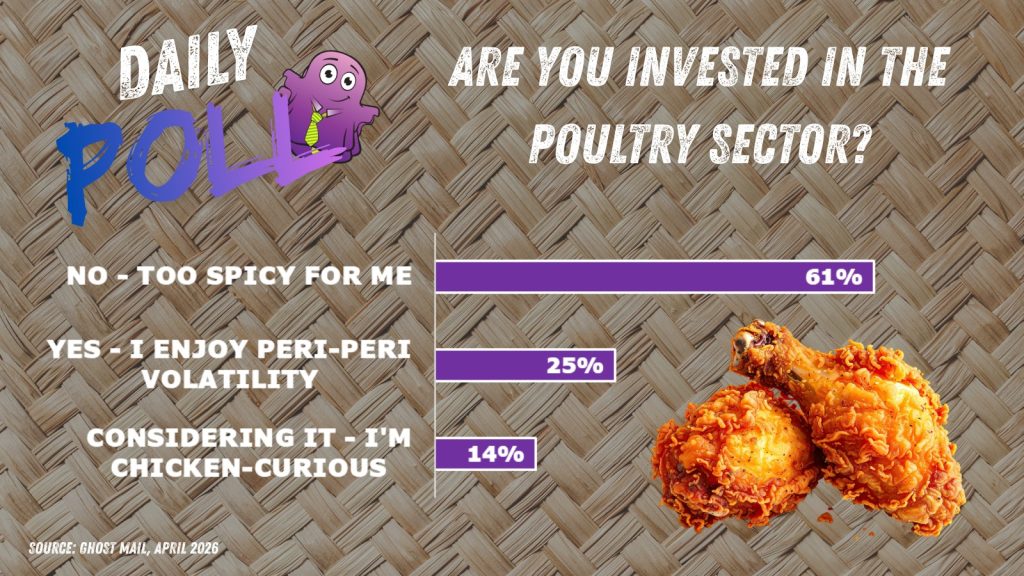

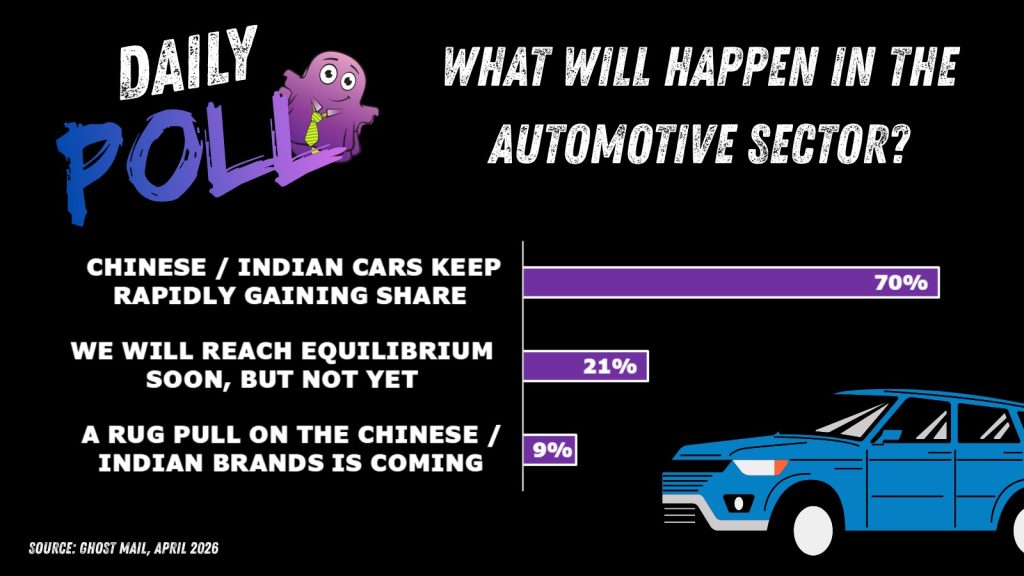

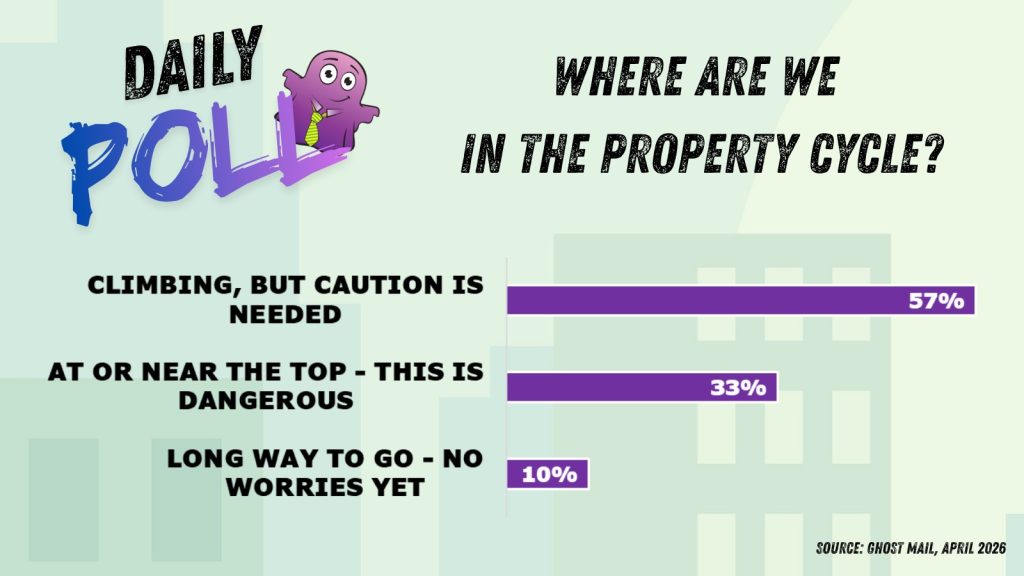

Results of previous poll:

Nibbles:

- Trematon (JSE: TMT) has released the circular dealing with the proposed disposal of Club Mykonos Langebaan. This is a related party deal that would get this resort off Trematon’s balance sheet. The company uses the circular to remind investors that the original investment thesis was to obtain a casino licence. It was subsequently disposed of in 2017 for a “significant return” – leaving them with the fixed property and limited ways to really move the dial for shareholders. Then again, the Trematon CEO and related parties seem to want to own the asset, so this is where the inherent conflict of interest becomes difficult. The independent board justifies the deal by noting that a sale to an unrelated third party would require an extensive due diligence and more onerous profit warranties. Whilst there is truth to this argument, shareholders should always be alert to situations where companies are transacting with executive managers. You can read the circular here.

- It’s technically still early days in the AttBid offer to RMB Holdings (JSE: RMH) shareholders, but there aren’t many acceptances at this point. Holders of only 0.4% of shares in issue have accepted the offer. Together with the current holdings of AttBid and Atterbury Property Fund (including some additional recent purchases), this would take the concert parties to a stake of 44.05%. The offer closes on 29 May, so there are still a few weeks to go. I’ve observed in other deals that most shareholders wait until the last minute to accept these things, preserving their optionality along the way.

- Nampak (JSE: NPK) has announced the appointment of Thiru Naicker as CFO with effect from 1 August 2026, replacing Glenn Fullerton. Thiru has held a number of senior executive roles in the FMCG space, with the most recent being as Senior Finance Director Supply Chain at PepsiCo South Africa. This sounds like strong operational appointment rather than a helicopter CFO. Given Nampak’s business model, that makes a lot of sense.

- A sad day at Sibanye-Stillwater (JSE: SSW) and a reminder of how dangerous the mining sector still is – during a route shaft inspection at the Kloof 8 shaft, an inspection platform detached and led to the fatal injury of two contractor employees. Shaft operation has been stopped while investigations take place.

- Numeral (JSE: XII) has renewed the cautionary announcement regarding the restatement of the financials for the year ended February 2025. At this stage, the restatements remain subject to completion of the audit and are in line with the information announced by the company on 22 April.

")

")

")

")