Deon Lewis (co-founder of Futureneers) and James Rothmann (Projects Director and Tax Innovation Officer at Futureneers) joined The Finance Ghost to talk about the 12BA Renewable Energy Partnership and the opportunity it offers investors for a tax-enhanced investment in solar.

Listen to the show here:

On this podcast, we talked about topics including:

The background of Futureneers and the investment track record.

The return profile of the solar projects both with and without the tax benefits.

The way the tax works further down the line when there’s a potential sale of the project.

Whether this opportunity is relatively more attractive for potential investors who are in higher tax brackets.

The protections in place for investors.

For more information on Futureneers and to apply for this opportunity, you can follow this link.

As always, ensure that you do your own research and consult with your financial advisor. The Finance Ghost has no affiliation with Futureneers or involvement in the underlying investments and does not accept any responsibility for the financial returns. Futureneers is a registered Financial Services Provider (FSP 46996) and registered Section 12J Venture Capital Company.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

It doesn’t get more sideways than Adcock Ingram (JSE: AIP)

If you like small percentages, here’s one for you

Look, Adcock Ingram certainly isn’t going to set your hair on fire. For the six months ended December 2023, revenue was up 1%. Exciting, hey? Gross profit fell 2%, trading profit was down 1% and HEPS increased by 1%.

I actually can’t remember seeing a cluster of such small numbers! Normally, when revenue is so sideways, trading profit takes a dive. Not so in this case.

Once you get to segmental numbers, it does get more interesting at trading profit level. The biggest segment is Prescription, thanks to a 13% increase in trading profit despite flat revenue. Conversely, OTC saw profits drop 9% off flat revenue. Consumer maintained its margins, with both revenue and trading profit up 2%. The Hospital division is the smallest part of the group and saw profits fall 16% despite a 5% increase in revenue.

In a final nod to the sideways journey, the dividend of 125 cents per share is identical to the prior period.

Bidcorp just keeps marching on (JSE: BID)

Growth remains strong, although there’s a question mark around margins

Global food service giant Bidcorpis an excellent way to give your money a passport without leaving the JSE. The company only earns a fraction of its income from South Africa, with the largest markets being Europe and the UK. The food service industry is lucrative once a business reaches scale, as is the case at Bidcorp.

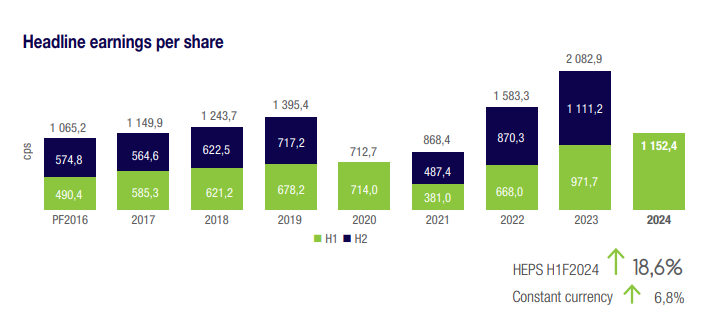

The pandemic obviously threw quite the spanner in the works. This chart is historically significant, showing how H2’20 earnings were literally non-existent:

The other thing to take from the chart is that earnings have grown beautifully if we look through the pandemic distortions. In the six months to December 2023, revenue was up 24% and trading profit increased by 20.8%. Now, this does mean some operating margin contraction, caused by operating expenses growing slightly faster than gross profit.

Still, 18.6% growth in HEPS and a 19.3% increase in the dividend per share isn’t anything to complain about.

If you look segmentally, the trading profit story does reveal a significant headache in the UK in particular. Revenue increased by 21.2% in that market and trading profit fell 15%. Gross margin pressure in that market is a direct result of the tough conditions being faced there in the hospitality sector. Again, the grass isn’t always greener!

The strategy going forward remains the same: organic growth plus the use of bolt-on acquisitions to expand either geographic reach or product range in existing markets.

What on earth is going on at Bytes? (JSE: BYI)

The share price fell 6% on very odd news of the CEO suddenly resigning

It’s never a good thing when an executive leaves out of the blue, especially the CEO. It’s even worse when a resignation comes through with immediate effect, as it suggests that something has gone badly wrong in the background. When the SENS announcement doesn’t give a good explanation for something like this (e.g. a health problem), speculation is rife.

So, the news of Bytes CEO Neil Murphy resigning with immediate effect (and with no explanation given) isn’t a happy thing, which is why the share price closed 6% lower. To add even more spice to this story, there have been trades in the company shares that he hadn’t disclosed to the company or the market.

As Alice cried, “Curiouser and curiouser!”

The jokes write themselves about the clarity of the situation, with Sam Mudd (MD of Phoenix Software and an executive director of the company) taking the role of interim CEO.

The only positive here is that trading for the year ending 29 February 2024 has been in line with expectations, with a trading update due in March.

Choppy results at Choppies (JSE: CHP)

The per-share numbers have been significantly impacted by the rights offer in June 2023

Retail group Choppieshas released a trading statement for the six months to December 2023. Earnings actually did rather well, with profit after tax from continuing operations up by between 36% and 46%. On a per-share basis, the picture looks very different, with HEPS expected to differ by between -3% and 7%.

This is because of the rights offer that was completed in June 2023 that resulted in more shares being in issue.

Glencore’s numbers are way down year-on-year (JSE: GLN)

This is another good example of mining cycles in action

At Glencore, revenue dropped by 15% in 2023 and adjusted EBITDA was down 50%. Funds from operations tanked by 67%. Clearly, the year-on-year story is typical of the hard correction we’ve seen in the commodity sector over the past 12 months.

Glencore is quick to remind the market that although the year-on-year picture might look awful, the group remains highly cash generative. This supports the deal to acquire a 77% stake in Teck’s Elk Valley Resources business for $6.93 billion in cash is in the process of regulatory approvals, with an expected closing date no later than Q3 2024.

The focus is on deleveraging the balance sheet towards a $5 billion net debt cap before a demerger into a fossil fuels and transition metals structure could be considered. Glencore expects the deleveraging to occur within 24 months from transaction close.

This is why there is no “top-up” distribution at this point, with Glencore hoping that such distributions will happen again in the future. It’s a vague comment from the company that is surrounded by reminders that the real focus is on deleveraging, so don’t hold your breath for a high payout ratio over the next couple of years.

Profitability has collapsed at Sibanye-Stillwater (JSE: SSW)

The share price is back below R20

The good news is that Sibanye achieved revised production guidance for the year ended December 2023 at all operations other than US PGM recycling, which was impacted by deliveries of used autocatalysts remaining depressed as used vehicles are taking longer to be replaced in an environment of higher interest rates.

That’s where the good news ends.

Other than gold, commodity prices plummeted in 2023. This has led to substantial impairments being recognised on various operations, including even the SA gold operations due to the Kloof 4 shaft closure and the deferral of the Burnstone project.

Those impairments can’t even be blamed for the precipitous drop in HEPS, which will be over 90% lower year-on-year at between 60 cents and 66 cents.

The share price has lost almost half its value in the past 12 months.

Spar’s local volumes are still under pressure (JSE: SPP)

And in a shock to nobody, the SAP issues continue

Sparhas released a trading update for the 26 weeks to 16 February, showing an increase in turnover of 9.3% for the period. This number needs to be unpacked though, as Spar has operations in several countries.

SPAR Southern Africa remains the most important part of the business. Core grocery and liquor turnover growth was only 6.1% vs. internal inflation of 7.5%, so volumes moved in the wrong direction. The grocery wholesale business was only up 5.1% thanks to ongoing systems issues in the KZN region after the business gave itself the kiss of death: a SAP implementation.

To this day, I cannot think of a single SAP implementation at a retailer that hasn’t caused severe disruptions.

SPAR2U, the rather obscure online offering, is now available at 403 sites. Sales increased by 450% but that’s vs. a tiny base.

The star of the local business is TOPS at SPAR, which increased sales by 12.7%. Pharmacy at Spar was also solid, up 11.6%. Conversely, building materials and construction business Build it could only manage 0.5%.

Moving abroad, BWG Group in Ireland and South West England grew turnover by 7.1% in EUR and thus 19.1% in ZAR, with the rand depreciation helping massively here. Ditto for SPAR Switzerland, where a decline in turnover of 5.7% in CHF translated into a 9.2% increase in ZAR.

In Poland, an ongoing headache that Spar wants to sell, turnover was down 2.9% in PLN terms and up 16.1% in ZAR.

The group is considering various debt structuring options, with an optimised debt structure dependent on the outcome of the disposal of the interests in Poland.

Interim results for the six months ending March will be released on 5 June.

Stor-Age’s key metrics moved in the right direction (JSE: SSS)

The company has released a trading update for the four months to January 2024

Growth at Stor-Age comes from three sources: new developments, higher occupancy in existing developments and pricing increases charged to customers for the storage space. The company is very good at pulling all three of those levers.

In the four months to January 2024, group occupancy in the owned portfolio increased 230 basis points to 90.1%. The South African portfolio was the star here, up 280 basis points to 92.1%. The UK was up 40 basis points to 83.0%. The joint venture portfolio is a lot smaller and runs at a significantly lower occupancy rate, but this is increasing quickly as the properties mature.

Importantly, the South African portfolio saw average rentals up by 9.4% and the UK portfolio achieved 4.8% growth in that key pricing metric.

And with respect to the third lever (new developments), there are currently four developments underway – two in South Africa and two in the UK. Stor-age is also expanding certain existing properties to respond to demand.

There’s actually a bonus lever of growth which is still in its infancy: managing properties on behalf of third parties. This is a great way to increase return on equity, as the group is earning income off assets that it didn’t pay to build.

Little Bites:

Director dealings:

Sean Riskowitz, acting through Protea Asset Management, has bought more shares in Finbond (JSE: FGL) worth R758k.

A non-executive director of British American Tobacco (JSE: BTI) has acquired shares in the company worth £99k.

Brimstone Investment Corporation (JSE: BRT) released a trading statement dealing with the year ended December 2023. It’s based on EPS growing by between 49% and 59%, which really isn’t a useful measure for Brimstone’s investment holding company structure. Let’s wait and see what the movement in net asset value (NAV) is when results are released on 6 March.

Due to the process with the Prudential Authority taking longer than expected, Conduit Capital (JSE: CND) and the acquirer of the Copper Sunset Trading subsidiary (a deal worth R55 million) have agreed to extend the fulfilment date once more to no later than 31 March 2024.

The application to liquidate Afristrat Investment Holdings (JSE: ATI) was dismissed in the High Court, with costs. This has been going on for a while now and the company has earned itself some breathing room with this judgment.

Primeserv (JSE: PMV) has repurchased 0.45% of shares in issue between 12 December 2023 and 19 February 2024 for a total amount of R667k.

Following the standout performance of their initial 12BA Renewable Energy Partnership, which effortlessly hit its R135 million target,Futureneers is rolling out the much-anticipated sequel: Renewable Energy Partnership II. This isn’t just about making waves in the investment world; it’s about creating a ripple effect of change across South Africa’s energy sector.

With Partnership I rallying an impressive R96 million in debt and equity from August to December 2023 and a staggering R39 million in equity during the last 4 weeks, the stage is set for an encore that promises not only remarkable financial returns but also significant societal impact.

Your Investment, Amplified

Renewable Energy Partnership II isn’t your everyday investment. It’s a gateway to leveraging your tax in a way that contributes directly to South Africa’s green energy transition. And here’s the kicker: with the tax year concluding on 29 February 2024, this Partnership offers an exclusive chance to benefit from a 125% tax deduction. Yes, it’s a limited offer, but the potential? Limitless.

This is about putting your money where your heart is, blending financial wisdom with a commitment to sustainable development. With just R20 million up for grabs, it’s an opportunity that demands swift action, potentially achieving an Internal Rate of Return (IRR) of 21% pre-tax, and making a tangible difference in our energy crisis.

Investment Highlights:

Exclusivity at Its Finest: With only R20 million available, this opportunity is as rare as it is impactful.

Unprecedented Tax Advantage: Secure your spot for the last chance at a 125% tax deduction for this tax year, exclusively through Futureneers.

Diverse Investor Appeal: Whether you’re an individual looking to maximize tax efficiency or a corporation aiming for impactful investment, this is for you.

Solid Returns: A projected pre-tax IRR of 21% (13% post-tax) marks this as a standout choice for serious investors.

Strategic Entry: A minimum investment of R500,000 with options for early exit provides both commitment and flexibility.

Make Your Move

As we approach the tax year deadline, the window for this unique investment narrows. It’s not just an opportunity for financial growth but a step towards contributing to a sustainable and energy-secure future for South Africa.

Position yourself at the forefront of change and investment excellence. Together, let’s turn the tide towards a greener, more prosperous tomorrow.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

You need to read the BHP numbers carefully (JSE: BHG)

For one things, there are massive impairments in the results

Mining giant BHP released results for the six months to December 2023 and the words “underlying profit” appear often. The key difference between underlying profit and attributable profit is the impairment of Western Australia Nickel ($2.5 billion) and a further charge related to the Samarco dam failure ($3.2 billion). This smashes attributable profit from $6.5 billion in the comparable period to just $0.9 billion in this period.

Although these are non-cash charges for now, the reality is that the Samarco provision is an estimated future outflow and the Western Australia Nickel impairment talks to capital allocation. I wouldn’t just ignore these as being inconsequential.

To get closer to the core mining results, we can look at revenue (up 6%) and underlying EBITDA (up 5%), with slightly contraction in underlying EBITDA margin from 53.5% to 53.3%.

Net operating cash flow is a much more exciting story, up 31% thanks to the increase in EBITDA and lower income tax and royalty tax payments as well, which aren’t captured in EBITDA.

Of net operating cash flow of $8.9 billion, BHP invested $5.1 billion in various capital projects and thus generated $3.8 billion in free cash flow. Some capital expenditure was also funded from debt, which is why net debt increased from $11.2 billion as at June 2023 to $12.6 billion as at December 2023.

This is still within BHP’s targeted range for net debt of $5 billion to $15 billion.

An interim dividend of $0.72 per share has been declared, which is a 56% payout ratio.

Although there’s lots of noise in the numbers around timing of projects and other things, it’s quite fun to compare Return on Capital Employed (ROCE) across the various business units. Copper came in at 10%, iron ore 85% and coal 15%. Thankfully for BHP shareholders, iron ore is the biggest part of the business.

Kumba cuts jobs along with the production outlook (JSE: KIO)

This is the inevitable outcome of failing infrastructure

Thanks to a period of strong cost savings (R1 billion) and a rebound in iron ore prices towards the end of the year, Kumba Iron Ore pulled off a decent set of numbers for the 2023 financial year. EBITDA margin actually increased from 50% to 53%, with attributable free cash flow coming in 43% higher. Return on capital employed increased from 76% to 82%.

It all sounds really good until you dig deeper, with the group having to cut back on production because Transnet simply cannot rail the stuff to port quickly and reliably enough. This didn’t do any good for unit costs at Sishen in particular, although cost initiatives helped unit costs at Kolomela move lower.

The logistics limitations have led to a lower expected production plan for 2024 to 2026, which means the workforce at the company is too bloated for expected production levels. To ensure they remain competitive, Kumba will need to reconfigure the business and this is expected to impact 490 jobs. A further 160 service providers and contractors are impacted.

It’s one thing when commodity prices lead to job losses, like in the PGM industry. It’s another thing altogether when government absolutely fails to support the private sector, forcing a more conservative approach that loses jobs rather than creates them.

As great as the HEPS increase of 26% is, Kumba needs to look ahead and ensure it is right-sized for conditions that may not be so favourable.

Record earnings at NEPI Rockcastle (JSE: NRP)

This is the highest distributable earnings per share (DEPS) result in the company’s history

Eastern Europe (with the obvious exception of Ukraine) has turned out to be a decent place to do business as a property company, particularly when you have NEPI Rockcastle’s portfolio and balance sheet. Smaller funds are struggling with funding costs, yet here we have NEPI as the big shot in the room with record DEPS for the year ended December 2023.

DEPS was up 9.3% year-on-year, which exceeded even recent expectations at the company. If you adjust for once-offs in the base related to litigation provisions, then recurring DEPS was up 17.1%. Net operating income was the driver of this result, up 21% year-on-year thanks to a 13% like-for-like increase and the rest from acquisitions. A high inflationary environment isn’t a problem when lease clauses have indexation clauses. Even better, new lettings achieved higher uplifts than indexation thanks to the way the properties have been managed.

Retailers clearly like the properties in the portfolio, with sales and footfall metrics moving in the right direction and the vacancy rate decreasing to 2.2%.

The balance sheet was further strengthened by a scrip dividend option (shareholders could receive more shares instead of cash dividends), with the loan-to-value ratio down to 32.2%.

DEPS for 2024 is expected to be 4% higher, with no expected change to the current payout ratio of 90%. This is a fairly modest growth outlook, particularly after such a strong year.

A not-very-super update at Super Group (JSE: SPG)

With a nasty correction in the share price of 10% for good measure

Super Group released a trading update for the six months to December that reflects a 16.2% decrease in HEPS despite an 11.9% increase in revenue. This is significant margin erosion, with EBITDA margin decreasing from 13.6% to 12.8%.

There were various challenges faced throughout the group, ranging from the Southern African Supply Chain business suffering from slow turnaround times at local ports through to the UK Dealerships business dealing with a drop in consumer demand and a substantial decrease in used vehicle trading margins. The German and UK Supply Chain businesses also had a tough time as higher interest rates worked through the system. It’s not always greener on the other side, you know.

The bright spots were the SG Fleet business in Australasia in particular, as well as the South African Dealerships business in a car sales environment that has already been through the pain of normalisation.

The balance sheet remains in decent shape, with net gearing of around 36.5%.

Looking ahead, the company expects conditions in the second half of the year to be broadly in line with the first half, with some room for improvement in the UK Dealerships operations.

Vukile had no problems raising capital (JSE: VKE)

As mentioned earlier this week, Vukile is taking advantage of positive investor sentiment

In the heydays of the property market on the JSE (around 2015 – 2016), property funds could raise literally billions of rands in the time it takes you to finish your breakfast. These accelerated bookbuilds were heavily oversubscribed and in most cases, the company didn’t even tell investors exactly what the capital would be used for.

When times are tougher, it’s a lot more difficult to raise capital at all. On the rare occasions where we see an equity raise, the REIT has to submit two blood samples and a lifelong history of the asset being acquired. In short: the equity raising trends on the JSE tell us a lot about where we are in the cycle.

Vukile is certainly one of the better local REITs, so it’s not a huge surprise that it is leading the way in taking us back to the glory years of capital raising. In an equity raise that was intended to be 5% of the market cap (around R750 million), Vukile was able to increase the size of the raise to R1 billion, placing the shares at only a 0.75% discount to the pre-launch share price (and a 4.85% discount to 10-day VWAP).

Most impressively, they could place the shares and raise the money for acquisitions that haven’t even been announced yet. For now, they are just building a war chest for future deals – and the market was quite happy to provide that blank cheque.

Keep an eye on this trend as a potential sign that the best days of the property sector recovery may be behind us. Sadly, Vukile’s share price is still down 28% over the past five years. It has approximately doubled over the past three years in a post-pandemic recovery.

WBHO moves in the right direction (JSE: WBO)

HEPS from continuing operations has increased by between 5% and 15%

Wilson Bayly Holmes-Ovcon, or WBHO as everyone knows the group, has seen its profits head in the right direction for the six months to December 2023. This has been driven by a strong order book in Africa and improvements in the UK as well. For the six month period, HEPS from continuing operations should be up by between 5% and 15%. Total HEPS should be up by between 35% and 45%.

Those of you who keep falling into potholes will be pleased to learn that the roads and earthworks division has increased revenue by at least 50%, so roads are being improved somewhere at least. Operating profit is up by at least 60%.

The building and civil engineering side has grown revenue by at least 15% and profits by at least 5%.

Despite the company complaining about procurement of new work in the UK being difficult, revenue is up by between 15% and 20% and operating profit is up by at least 40%.

The construction materials and property developments segment has performed in line with the prior period at operating profit level.

Share of profits from associates and joint ventures has decreased by at least 60% due to once-off effects of the refinancing of the Gigawatt Power Station in Mozambique.

Australia remains a headache, with the loss from discontinued operations down by at least 90% but many ongoing processes in that country in relation to the exit from that country.

Little Bites:

Director dealings:

An executive director of Richemont (JSE: CFR) has sold shares worth a substantial R22 million.

Kibo Energy (JSE: KBO) has sold nearly £21k worth of shares in Mast Energy Developments, with the proceeds used to reduce the debt with RiverFort Global Opportunities PCC. Selling down an investment to reduce debt isn’t a pretty picture.

Copper 360 (JSE: CPR) has released one of those announcements that only really makes sense to geologists and perhaps mining engineers. The rest of us have to rely on the flavour of the narrative in the commentary by the CEO. Long story short, the historically mined Tweefontein Mine had the highest grade mine in the entire copper district and there could be a new copper mine adjacent to this historically mined area. Magnetic drone surveys and surface sampling results are encouraging. They have three more copper “anomalies” to test, all of which are bigger than the first anomaly that has been tested.

In the unlikely event that you are a shareholder in Marshall Monteagle PLC (JSE: MMP), one of the more unusual local stocks, you’ll want to know that the circular for the disposal of property in California worth $26.5 million has been released to shareholders.

Zeder (JSE: ZED) has reminded shareholders that the SARB approval for the special distribution of 20 cents per share hasn’t been obtained yet. The timetable will need to be revised accordingly.

This is a big year for South Africa. Load shedding returned literally straight after the State of the Nation Address, creating a difficult foundation for the Budget Speech. The headlines are full of political activity in the build-up to elections. There’s a lot going on.

Tertius Troost is in the Tax Consulting team at Mazars, so this is a busy month to say the least. He took time away from a hectic February tax diary to share insights as a preview to the Budget Speech.

Why is this important? Well, as a South African, the Budget Speech directly impacts you in many different ways, ranging from direct changes to your taxes to the way in which your taxes are spent in the country. It’s critical to understand the key pressure points for our fiscus.

With the cosmic game of Jenga that global markets have been playing for the past three years, it’s reasonable to be rattled about investment instability.

Investors are finding it more difficult to spot attractive investment opportunities that will deliver secure, acceptable returns. Even the so-called equity ‘golden oldies’ no longer deliver consistently on investor expectations.

This prompts investors to question the overall viability of investments, but perhaps that line of questioning should be extended to investment strategies, and maybe even the way we assess investment options too. It’s probably time to rethink our existing investment perceptions and expectations and explore fresh ways to preserve capital, generate income and build wealth.

Traditional Thinking

Back in the day, portfolios were typically constructed by cherry-picking equities and bonds from the JSE and allocating them based on risk appetite, leaving investors to sit back and watch yields climb. Growth was the focus, and for the most part, stability lay simply in selecting a collection of traditional, albeit unimaginative, top performing assets, and ensuring they were stacked securely.

With little disruption to worry about, there was no compelling reason to look beyond the tried and trusted with few even thinking about alternative investment options. So, investors and their financial advisors continued to look forward to the annual portfolio review lunch, confident they’d be breaking out the good stuff.

But a new pattern had already started emerging by the time COVID-19 hit. It has since become undeniable and the corks have stopped popping. As conventional investment strategies failed to deliver the expected returns, the mutual backslapping quickly morphed into the Heimlich maneuver, and several critical shortcomings were revealed.

One, the misplaced belief that a Jenga tower built exclusively from the JSE’s top stocks and bonds could be an effective bulwark against market instability;

two, the reluctance to accept that a properly balanced portfolio should include a diversified range of investments beyond just the familiar; and,

three, the blinkers that resulted in many overlooking the potential of including alternative asset classes and fixed investments in balanced portfolios. Especially in rocky times.

Best of both worlds

Much like a real-life Jenga game, you need proper planning and a good mix of pieces in the right places. And much like with your investment portfolio, if you lean too heavily in any one direction, the slightest bump of the table will send the whole thing tumbling. It’s all about balance.

This approach has served Fedgroup well over the years by balancing innovation with a foundation of tried and tested financial wisdom to offer investors the best of both worlds.

With an unblemished track record of the performance of our fixed investments and a pioneering spirit, we’ve shown that it’s possible to constantly challenge industry norms for the benefit of investors. The result? Smooth investment journeys for investors and a consistent delivery on their financial security and growth objectives by incorporating innovative and competitive investment solutions into their portfolios.

How is this possible, you might ask?

Through a combination of fixed-term investments that could withstand a battering even when more traditional assets in investor portfolios might be reeling, providing a stable foundation, no matter the level of market volatility.

This approach to stability is rooted in the simple truth that, even the most aggressive investor, in the most bullish of markets, wants reassurance that a portion of their money is safe. And that’s truer still when the bears come out of hibernation, ready to deliver a COVID-sized klap.

This level of security is provided by fixed investments like our Secured Investment – and the more recently launched Fixed Endowment. They are perfectly positioned to offer investors certainty, from day one, of the exact returns they’ll receive at the end of the fixed term – making them great investment products regardless of whether you’re new to investing or an experienced, qualified investor.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Farewell to the good times at Anglo American Platinum (JSE: AMS)

The PG in PGMs should stand for Parental Guidance required to read these sector results

As you will also see in the Northam numbers further down, the PGM sector is doing what it does best at the moment: blikseming people. Anglo American Platinum (or Amplats) has reported 2023 numbers and they reflect a 26% decrease in the rand basket price and a 1% drop in refined PGM production. Sales volumes only increased 2% as they dug into the refined stockpile.

You don’t need too much experience in the market to know what that combination looks like for the financials.

Revenue is down 24%, adjusted EBITDA has fallen 67% and HEPS has tanked by 71%. Despite this, mining EBITDA margin was still a rather lucrative 35% – it’s just come down a lot from 57% last year.

The dividend has followed suit, down 81% to R21.30 per share.

Along with initiatives to save costs and reduce capex, the group is embarking on a section 189 process that could impact 3,700 jobs. A review of contractors and vendors could impact 620 service providers.

Aveng reports in Aussie dollars for the first time (JSE: AEG)

This tells us a lot about the focus going forward

Aveng has released results for the six months to 31 December 2023. This is the first time that the reporting currency has been changed from the South African rand to the Australian dollar. Importantly, you also need to look at continuing operations as this excludes Trident Steel in the prior period.

Revenue from continuing operations increased from A$1.1 billion to A$1.5 billion. That’s a 39% increase on the top line of the income statement, driving a 99% improvement in operating earnings i.e. earnings nearly doubled.

McConnell Dowell is the key business, achieving operating earnings of A$24.2 million vs. just A$1.9 million at Moolmans. McConnell Dowell repaid A$10 million of debt in this period and has a remaining balance of A$13 million that the company expects to settle by the end of June 2024.

Moolmans is currently an exclusively South African business, with the group hoping to diversify the exposure going forward.

Current Group CEO Sean Flanagan will retire in March 2024, with McConnell Dowell CEO Scott Cummins set to take the group’s top job. He certainly inherits a group that is in much better shape than before, with work in hand covering 100% of 2024 full year revenue and more than 60% of 2025 revenue. Of course, what really matters is how well the projects are delivered in terms of margins, which are usually very tight and have the potential to easily go into the negative if things aren’t managed properly.

For now at least, HEPS of A$8.8 cents (R1.06) for the interim period is a solid improvement. The share price closed 6% lower at R7.28.

4Sight more than doubles HEPS (JSE: 4SI)

Plus, there’s a dividend!

4Sight has been getting the JSE small cap enthusiasts excited and with good reason:

Has there ever been a more aptly named company, as you wish you had the foresight to see what would happen here?

The driver of the increase has been revenue growth of 34.9% in the year ended December 2023 that has powered a 70.6% increase in operating profit and a 127.8% jump in HEPS. Importantly, there’s now a dividend of 2.5 cents per share based on HEPS of 5.42 cents.

What does the company do? Well, the magic words “Artificial Intelligence” are involved and that always gets the crowd jumping, especially in South Africa where our exposure to the 4th Industrial Revolution is generally limited to the lights coming back on after load shedding.

Italtile: a casualty of this economy (JSE: ITE)

Much like at Cashbuild, there really isn’t much that they can do

Italtile is another great barometer for the state of our economy. Spoiler alert: the operating environment isn’t nearly as pretty as the fancy tiles.

System-wide turnover is down 2%, trading profit has fallen by 17% and HEPS has taken a 15% knock. The dividend has largely followed suit, down 16%.

The outlook doesn’t paint an appealing picture either, noting that consumers are likely to remain under pressure and that the business will find things difficult until interest rates decline and consumer confidence is restored.

One of the reasons why Italtile struggles is that there is a substantial manufacturing element to the business. When capacity utilisation moves in the wrong way due to weak demand, manufacturing businesses take a significant knock to their margins.

As another reminder of what we are dealing with in this economy, Italtile Retail (which focuses on higher income consumers) noted that the size of its market has declined over recent years, in line with “sustained emigration” – exactly what a business like this doesn’t need to see. It’s not much better in the mid-market either, with CTM’s sales and profits down mid-single digits. Yet, in the entry-level market, the TopT brand achieved low single-digit growth in sales and profits.

In summary, South African consumers who are coming through the income ranks at a lower level seem to be a source of growth. As for the rest of the income brackets, people are either emigrating or maintaining a flexible enough asset base that emigration is an option.

The PGM basket price hammered Northam Platinum (JSE: NPH)

In the latest news from the PGM jungle, HEPS at Northam has all but collapsed

The PGM sector has a reputation for hurting people. With a 42.3% decrease in the 4E basket price for the six months to December 2023, Northam Platinum is the latest casualty. Even a 10.4% increase in sales volumes does little to offset this pain.

It also doesn’t help when mining costs are subject to inflationary pressures, with a 6.7% increase in group unit cash cost per equivalent refined 4E oz despite the increase in production. When combined with what happened to PGM prices, the result is a 73.3% decrease in gross profit.

From there, it’s hard for the income statement to be anything other than hideous. And indeed, HEPS is expected to be between 87.5% and 97.5% lower.

The silver lining here must be the balance sheet, with net debt improving to R2.4 billion at the end of December. The rolling 12-month net debt to EBITDA ratio is 0.24x. Cash and cash equivalents were R11.8 billion and the company has access to undrawn facilities of R11.0 billion.

Included in earnings per share (not HEPS) is a R799.7 million loss on the disposal of Impala Platinum shares that were received as consideration for the disposal of Royal Bafokeng Platinum. You may recall that Northam Platinum was in a bidding war for Royal Bafokeng, before pulling out and letting Impala win that battle as PGM prices kept falling.

It’s concerning that based on the price achieved in this period, only the Booysendal mine actually made a profit. Zondereinde and Eland both lost money per ounce sold.

In an environment of depressed PGM prices, the group has trimmed back its capex plans, investing R2.4 billion in this period vs. R2.6 billion in the comparable period. R1.6 billion of that capex was expansionary spend.

Telkom manages a flat EBITDA performance (JSE: TKG)

At least Swiftnet is putting in decent numbers at just the right time

Telkom released a trading update for the third quarter that reflects revenue growth of 2% and stable group EBITDA. It’s not growing, but it’s not shrinking either. EBITDA margin contracted to 21.9%, impacted by BCX (EBITDA fell by 27%) and pressure on enterprise customers.

There were some highlights, like Telkom Consumer and Openserve growing operating earnings by 20.6% and 7.0% respectively. This was driven by metrics like Telkom Mobile subscribers growing by 6.4% (and data revenue up by 11.5%), as well as data revenue at Openserve increasing by 6.2% as the number of connected homes increased by 20.8%. Yes, it would be nice to see revenue at Openserve increasing at a rate in line with the number of connected homes. The bigger challenge at Openserve is the decline in total fixed voice revenue in the legacy side of the business, leading to overall revenue declining by 3.1%.

Swiftnet is thankfully doing well at the right time, as Telkom seems to be getting closer to a potential deal to dispose of the business. The bidder consortium is working towards meeting agreed milestones under the exclusivity arrangement. The company hopes to be able to make a more detailed announcement soon. Having said that, there’s still no guarantee at all that the parties will agree commercial terms or that a deal will go ahead. In the meantime, total revenue grew 4.7% at Swiftnet and EBITDA was up 11.3% as tower operating costs fell

Transpaco’s margin goes the wrong way (JSE: TPC)

And so did the share price

Transpaco has a market cap of under R1 billion, so it falls into that area of the JSE that is about as liquid as the dunes of Dubai. The share price fell 13.18% yesterday, which sounds spectacular at first blush, yet that can easily be the bid-offer spread when it comes to small caps.

It wouldn’t have helped that revenue for the six months to December 2023 fell by 4.5% and operating profit fell 12.3%. This is a classic case of operating leverage working against a manufacturing group. Operating margin contracted from 10.0% to 9.2%. HEPS was 5.6% lower at 299.1 cents and the dividend was 5.9% lower at 90.0 cents.

The usual suspects are blamed for the results (load shedding / the economy / interest rates), with the company commenting that share buybacks helped to cushion the blow. With HEPS falling by a significantly lower percentage than operating profit, you can see how having fewer shares in issue helped.

The Plastics division suffered most, with revenue down 10.1% vs. a 2.6% drop in the Paper and Board division.

Vukile taps the market for capital (JSE: VKE)

The group is looking at opportunities in both its markets of operation

Vukile has proven to be one of the better REITs of the post-pandemic era, so the company is doing exactly what it should be doing while sentiment is good: raising capital from investors. You always want to raise when you have the gold star on your forehead and you sit at the front of the class. Raising from the naughty corner ain’t easy.

The group has a portfolio in South Africa and Spain and is looking at a pipeline of opportunities in both markets. This is a cheeky capital raise, as the company is so confident of its abilities to raise the capital that details on the opportunities haven’t been given. Instead, the proceeds of the bookbuild will be used to temporarily reduce borrowings ahead of doing deals.

The extent of the raise? Approximately 5% of the company’s market cap, which implies over R750m in fresh capital.

Keep a close eye on what they do with the money. We really don’t have to dig very far back in the history books to a time when REITs raised billions in the time it takes you to drink your coffee, before deploying the money into overpriced properties.

Little Bites:

Director dealings:

An executive member of the board of Richemont (JSE: CFR) has shown us what real money looks like, with a disposal of shares worth R47 million.

Sean Riskowitz, acting through Protea Asset Management as usual, has bought another R754k worth of shares in Finbond (JSE: FGL).

The same director of Afine Investments (JSE: ANI) who executed an odd buy and sell trade the other day has now sold shares worth R48.5k, also at R5 per share.

Directors of Nictus (JSE: NCS) bought shares worth R15.6k in an off-market trade.

In a trading statement for the six months to March 2024 that isn’t nearly as useful as a trading statement usually is, Life Healthcare (JSE: LHC) noted that EPS will be at least 20% higher. This is thanks to the gain on disposal of Alliance Medical Group. Such a gain is excluded from HEPS and there are still weeks of trading left, so the group hasn’t commented on HEPS. In other words, as trading statements go, this is an anomaly that was required to meet JSE rules. It doesn’t tell us anything at all about core operating performance.

Copper 360 (JSE: CPR) has raised just under R100 million through the issue of shares for cash. It looks like there’s a buyback option linked to this raise to potentially limit dilution to existing shareholders. In total, the company has raised R374 million through various debt and equity issuances.

African Equity Empowerment Investments (JSE: AEE) announced that a fraud in November 2023 of $820k has led to the CEO of Premier Fishing and Brands being found guilty of negligence (not the theft itself). Efforts to recover the misappropriated funds are ongoing.

Watching a blockbuster film in a full cinema is arguably one of life’s finest experiences – and certainly one worth preserving. But will cinemas as we know them be able to keep up in the streaming race – or will they have to change their use case entirely?

The fourth quarter of 2023 was Netflix’s most explosive period for subscriber growth since Q1 2020. In case these dates are too vague for you, let me colour in the picture a little better: the last time Netflix saw numbers better than the ones they just released, a global pandemic had just forced the entire world indoors with nothing better to do than to watch TV. I stand to be corrected, but I think the only companies who had anywhere near the same levels of success as Netflix during the pandemic were those who were making either vaccines or video meeting platforms.

While Netflix has certainly been minting it lately (even their crackdown on password sharing, which many users criticised as draconian, has ultimately resulted in an uptick in new paying subscribers), the same can’t be said for the big screen. The cinema business has been haemorrhaging for a good long while now, with COVID-19 striking what many thought might be the deathblow. Fortunately, major movie houses have managed to hang on by their fingernails – but for how much longer will this continue?

As a self-proclaimed cinephile, the thought of a future without the opportunity to see a film on a big screen with a tub of overly-salted popcorn on my lap is too bleak to even entertain. What will it take to save our cinemas?

From silver screen to couch stream

It took a long while for humanity to progress from being able to create simple moving pictures to screening 2-hour-long blockbusters on IMAX screens. I won’t bore you with the full history – instead, I’d like to tell you about cinema’s golden age.

The 1930s and 40s represent the peak of cinema attendance. There are many reasons for this, but two stand out as major contributors. Firstly, this was the time when most films featured both colour and sound, thereby offering a vastly improved viewing experience to the silent black-and-white films that came before. And secondly, this was the time when cinema was considered the principal form of popular entertainment.

Going to the movies was so popular at the time that most people would attend the cinema as often as twice a week. As is always the case in business, demand drives supply, and in this case, the public’s demand for movies led to the building of ornate “supercinemas”, also known as picture palaces, in major cities and large towns. I’m not talking about the kind of in-mall cinemas that we’re used to seeing nowadays – these picture palaces were standalone buildings, large enough to fit multiple screening rooms, as well as cafés and ballrooms, all under one roof. Some of these supercinemas were large enough to accommodate up to 3,000 viewers in front of one screen.

Fast forward about 8 decades into the future, and North American box office revenues peaked in 2018 at $11.9 billion, followed by a slight decline to $11.4 billion in 2019, as reported by Comscore. Numbers have only continued to decline since then. In 2020, the onset of COVID-19 led to a drastic 80% drop in domestic box office earnings, plummeting to just $2.3 billion. Remarkably, $1.8 billion of that total was generated in the first three months of the year, before the pandemic fully disrupted normal life.

Keep in mind that the pandemic threw a wrench into both the making and showing of films, stashing away movies for extended periods while keeping audiences away from theatres. However, besides the direct disruptions caused by the pandemic, North America still faces the problem of having an excess of movie screens, which makes it difficult to get theatres to capacity. Moreover, the array of choices for streaming films at home has expanded, with new releases arriving much sooner than they did previously. Suddenly, staying home and streaming a movie on the couch is as appealing an option as a night out at the movies – and at a much lower cost.

There’s nothing like a full house

I absolutely love the feeling of being in a full cinema. For me, that’s where the magic of the movies always came from – that feeling of experiencing something as part of a crowd. Sure, you might feel something similar in a sports stadium or at a concert, but there’s just something about a group of people leaving reality behind for a couple of hours and stepping into an alternative world together that keeps me coming back for more.

I’ll never forget the experience I had while watching a horror film in a Cape Town cinema years ago, when a particularly nasty jump scare prompted a gentleman in the row in front of me to exclaim “djy!” at full volume. I remember the collective gasp in a full cinema during the screening of one of the latest Star Wars films, when fans of the franchise saw the Millennium Falcon on the big screen for the first time since 1983. And of course, there was no other way that I was going to see the atomic epic Oppenheimer than on the biggest, loudest IMAX screen I could find. Mankind’s biggest bomb just doesn’t resonate as well on a TV.

Usually when I write these articles, I try to find something that we can all learn from some clever business strategy or founder’s innovation. Today, I’m just writing to make a case for a business that I believe deserves to continue existing. And I’m not alone in this line of thinking either. When cinemas in North America closed their doors during the COVID-19 pandemic, award-winning director Christopher Nolan said “When this crisis passes, the need for collective human engagement, the need to live and love and laugh and cry together, will be more powerful than ever. We need what movies can offer us.”

Now, you might call him a bit biassed, based on his career choice. I prefer to think of him as simply a fellow film enthusiast.

“Pivot!”

So, I believe we can collectively agree that movie theatres are cool and that we’d like them to stick around for the foreseeable future. But to survive the next few decades, cinemas will have to pivot in new directions in order to differentiate themselves from their streaming competition. It’s not just about screening exciting films anymore – while Barbie and Oppenheimer have shown us that hype will still drive turnout in record numbers, a feast-and-famine income model is simply not a sustainable strategy.

Herewith my 2c: a collection of suggestions that may or may not save our cinemas, some of which are already being tried out there.

Pivot 1: Up the experience

If you’re asking an audience member to leave their home in order to see a film that they could just as easily view on their couch (in a few weeks’ time), then you need to make the experience of being out of the house worth their while. An average seat and standard snacks are easy to replicate at home. But change that to a plush reclining seat and gourmet snacks – potentially even alcoholic drinks and a menu of delicacies that can be served in-cinema – and the offering becomes that much more appealing.

Pivot 2: Bring back the classics

When the original Jurassic Park was showing audiences the magic of computer generated dinosaurs for the first time in 1993, I was less than a year old – not exactly the ideal movie-going age. I also completely missed my opportunity to see such classics as Jaws, the original Star Wars trilogy, Gladiator and The Matrix on the big screen – which is why I’d be willing to pay big bucks if that chance came around again. With the recent focus on reinventing older movie franchises like Indiana Jones, Jurassic Park and Top Gun, I believe movie theatres could benefit from offering a re-screening of the original films that inspired the new releases. This isn’t as far fetched an idea as it might seem if you consider that it was already done by the Avatar franchise, which re-screened the original Avatar movie (2009) in tandem with the release of Avatar 2: The Way of Water (2022).

Pivot 3: Rent out the screen

If you tilt your head and squint at it, a movie theatre is really just a potential venue-for-hire that includes a great sound system and a really big screen. Renting a theatre can make for a unique and memorable experience for events like birthdays, anniversaries, proposals, or even just a special date night. Businesses may rent out theatres for team-building events, product launches, or employee appreciation events. Schools or educational institutions may rent theatres for special screenings tied to their curriculum or to reward students for achievements. And lastly, with the rise of esports and gaming culture, some individuals or organisations may rent theatres for gaming tournaments or to host video game release parties.

Just bring back the audiences now

In the age of streaming dominance, the allure of the big screen seems to wane, yet the essence of the cinema experience remains irreplaceable. As we reminisce on the golden age of cinema and ponder its uncertain future, one thing becomes clear: the magic of movies lies not just in the narrative unfolding on screen, but in the collective engagement of a captivated audience.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

At Cognition, the balance sheet is what counts (JSE: CGN)

The gap between HEPS and NAV per share confirms it

After the sale of Private Property for a tremendous price, Cognition is now a group that is highly pregnant with cash. The group generated HEPS of just 2.48 cents for the six months to December 2023, yet the tangible NAV per share is 103.85 cents. That’s a huge difference, explained by R207 million worth of cash on the balance sheet vs. liabilities of just R28.2 million.

Cognition is currently in discussions with controlling shareholder Caxton & CTP Publishers and Printers (JSE: CAT), which may lead to an offer to delist Cognition.

The share price is currently trading at R1.05, which is already in line with the tangible NAV per share. It’s not obvious to me why Caxton would pay a significant premium to this price.

More insult and injury for Delta Property Fund (JSE: DLT)

It’s very debatable whether a fine a few years down the line actually punishes the right people

Delta Property Fund is another great local example of a company that turned into a financial disaster. The problems started with an announcement in 2020 dealing with problems in the financials. This would turn out to impact the 2018 and 2019 numbers as well.

The company initiated forensic investigations in 2020 that found a host of problems. To Delta’s credit, the JSE acknowledges that the company was transparent in dealing with the issues.

Still, there has to be some kind of punishment for not complying with IFRS, although share prices tend to dish out their own punishment when it comes to these things. The JSE has publicly censured Delta and imposed the maximum fine of R7.5 million, of which R5 million is suspended for a period of five years provided no other listings requirements are breached as they pertain to financial performance.

Far more importantly, the investigation into the individuals involved (rather than the company) is ongoing. It feels like that’s a much better way to punish the right people, rather than putting even more pressure on the company’s balance sheet and causing more damage to minority shareholders.

Transaction Capital releases the WeBuyCars unbundling circular (JSE: TCP)

Perhaps more importantly, there’s also a WeBuyCars management presentation to work through

In around April 2024 (and how I wish the Transaction Capital share price was just an April Fool’s Day joke), WeBuyCars will be separately listed on the JSE if all the conditions along the way are met. This is exciting stuff, particularly as our local universe of stocks tends to shrink a lot faster than it expands. WeBuyCars is that rare beast on the market: a pure-play view on a business model. They focus on doing one thing and doing it well.

It’s quite incredible to consider the history of WeBuyCars. It was started in 2001 and took another nine years until the first car supermarket was built in Pretoria with capacity for 100 vehicles. Fast forward to 2024 and they sold 14k vehicles just in January.

The company consistently reminds investors that Motus and CMH are not directly comparable, as WeBuyCars only sells used cars. There’s no noise from a rental business, or new car sales, or after-market parts. In fact, the strategy to expand the existing product offering is at this stage focused only on finance and insurance penetration, which means a higher value per customer. They are looking to make the value-added margin in addition to the gross margin on a sale. That’s a solid organic growth strategy, rather than a foray into something new or unrelated.

The group is looking to add at least 2,000 bays in FY25 to FY26, reaching regions of South Africa that aren’t currently serviced by sales outlets. They will need to be careful here that they don’t build supermarkets in areas that can’t support them.

Fascinatingly, they expect market share to grow from the existing 10% – 12% up to 23% by FY28. That’s a very bold chart to put in an investor deck! In theory, there’s no reason why they can’t achieve this.

FY23 was a wobbly in terms of the profit growth story. If you understand what happened to used vehicle prices over this period, then you’ll also understand why this chart (1) accelerated in FY21 and FY22 and (2) fell off in FY23:

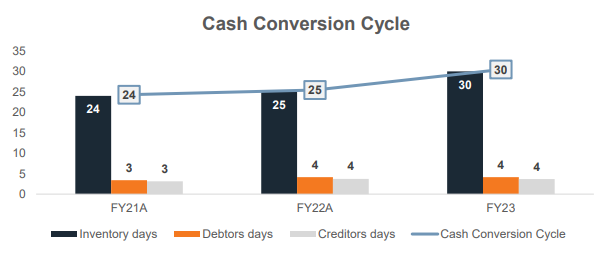

For me, where the economic reality does bite WeBuyCars is on the inventory days calculation. This is simply how many days worth of sales they have in inventory at any point in time. This has increased from 24 days to 30 days in the past two years, which is a material negative impact on working capital:

On the whole, in case it isn’t obvious, I’m bullish on WeBuyCars. This is exactly why I took exposure on Transaction Capital when they did the deal. Sadly, as you will no doubt be aware, the problems at SA Taxi blew up the Transaction Capital share price and I took that knock. At least the end result is direct exposure to WeBuyCars and some hope of an outcome for the “rump” of Transaction Capital, even if that might be a take-private of SA Taxi and Nutun. That is 100% speculation from my side, so please treat it as such. It just seems to make sense, as that rump will very much be the ugly duckling after the unbundling of this swan.

As a reminder, the structure of the unbundling and related capital raising activities will see Transaction Capital unlock between R900 million and R1.25 billion in cash. This will do wonders for the balance sheet. When you look through all the complex steps in the process, the equity value of WeBuyCars has been set at R7.5 billion.

The one hangover of this structure that I’m not a fan of is that Gomo (a finance and insurance business) will still be in Transaction Capital even though it services WeBuyCars in addition to SA Taxi. I’m sure everything is arms’ length and goodness knows a service provider doesn’t always need to be in the same group as the company it services, but it does mean there is still a legacy link to what is being left behind in Transaction Capital.

The WeBuyCars pre-listing statement is due for release on 12th March. That’s the day after my birthday and I’ll assume this is my gift from Transaction Capital.

Little Bites:

Director dealings:

The CFO of Nampak (JSE: NPK) has acquired shares worth R4 million.

In one of the strangest director dealings I’ve seen, a director of Afine Investments (JSE: ANI) bought shares worth R655k and then sold R606k worth of shares on the very same day at the same price per share. Then, a day later, he bought shares worth R1.85 million.

An associate of a director of Huge Group (JSE: HUG) has bought shares worth nearly R33k.

For those of you who like to keep track of the cost of debt for corporates, British American Tobacco (JSE: BTI) has priced notes due in 2031 at 5.834% and notes due in 2034 at 6.000%. The total issuance is a meaty $1.7 billion.

As indicated by the company earlier in the week, André van der Veen has officially replaced Peter Surgey as chairman of Nampak (JSE: NPK).

In a rather funny update that calls into question whether an investment strategy can also include a preference for similarity of names, an international investment house called Hosking Partners LLP has increased its interest in Hosken Consolidated Investments (JSE: HCI) to 5.05%.

Anglo American Platinum (JSE: AMS) announced that the Mototolo and Amandelbult mines are the first PGM mines to South Africa to complete an IRMA audit, achieving the IRMA 75 and IRMA 50 levels respectively. Whilst this doesn’t exactly do anything about the PGM prices, it does help with fussier buyers who track their supply chain and it helps keep Amplats on the right side of investors with an ESG slant to their mandates.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

A big jump in earnings at Aveng (JSE: AEG)

And a change in reporting currency

Aveng now earns 91% of its revenue from outside South Africa. To this end, the company is changing its reporting currency to the Australian dollar, reflecting the true economic situation of the group.

For the six months to 31 December 2023, Aveng’s revenue is expected to be 45% higher and earnings are up at both McConnell Dowell and Moolmans. Due to the disposal of Trident Steel in this period, HEPS from continuing operations is the right metric to focus on. It came in between 65.4% and 75.0% higher.

Local mining conditions hurt Barloworld (JSE: BAW)

The slowdown in South African mining is worrying

In the four months to 31 January 2024, Barloworld saw a 5% reduction in group revenue. The company has attributed this to lower demand in mining and consumer industries, with continued geopolitical conflicts not doing any favours.

With commodity prices having come under pressure and South African infrastructure doing a very poor job of supporting local mines, there was a slowdown in mining activity that saw Equipment southern Africa’s revenue decrease by 2%. After-sales activity was up, but at lower gross margins, leading to a dip in margin due to the mix effect. If there’s a silver lining here, it’s the decrease in levels of inventory. Also, the Bartrac joint venture in the DRC is showing an increase in attributable profits.

Equipment Eurasia has been supported by 20% revenue growth in Barloworld Mongolia, attributed to strong mining activity. The Russian business saw revenue drop by 26%, so that offset the overall story. At least both businesses achieved good operating margins.

In Consumer Industries, Ingrain’s revenue fell 5% due to lower demand in the alcoholic beverages, papermaking and converting sectors. Export sales fell due to competitive global pricing of starch. The impact of lower sales is that operating margins have fallen as well, as there are fixed costs. A restructure is underway to reduce fixed expenses.

More bad news in the nickel mining industry (JSE: BHP)

BHP is impairing Western Australia Nickel

BHP has announced two “exceptional items” for the financials for the six months to December 2023. This doesn’t mean exceptionally good, before you get excited.

The first is an impairment of the Western Australia Nickel operations of $3.5 billion pre-tax. Conditions in the nickel industry are really difficult at the moment (remember Glencore is also shutting an operation in this space) and BHP is reducing costs at the mine. The problem is the supply of nickel from Indonesia, which has significantly increased. This has lowered the nickel price at a time when mining costs are still under inflationary pressure.

There’s another impairment as well, but it has nothing to do with nickel. BHP is taking another pre-tax charge of $3.1 billion in relation to the Samarco dam failure, taking the total provision to $6.5 billion. This is based on an updated view of the costs after recent legal developments. Importantly, there is still significant uncertainty over what the final cost of this might be.

As usual, nothing is simple at Blue Label Telecoms (JSE: BLU)

You have to read the trading statement very carefully

Blue Label Telecoms has released a trading statement for the six months ended November 2023 and you have to be very sure of what you are looking at. For example, if you don’t take into account the huge negative move in the comparative period from the recapitalisation of Cell C, you would think that core HEPS is over 10x higher year-on-year. If you take out the current and prior period impacts of that recapitalisation, then HEPS is actually down 23%.

Then, it’s worth highlighting that the trouble in adjusted HEPS was from Comm Equipment Company (CEC), which saw headline earnings drop by R119 million. The rest of the group grew headline earnings by R19 million (10% growth). The problems at CEC are a drop in gross profit and substantial increases in expected credit losses, driven by a larger subscriber base and a deteriorating macroeconomic backdrop in South Africa.

There was a buzz around Blue Label Telecoms on Twitter/X in the latter part of 2023. The share price has rolled over since then, with the only real money being made on the rally from September to December. Over almost every time period, Blue Label investors have lost money.

The reward for foresight into 4Sight (JSE: 4SI)

The share price has approximately doubled just in 2024!

4Sight has a market cap of under R600 million. This is firmly small cap territory. It’s bigger than it was though, with an increase of a ridiculous 360% in the past 12 months! This year alone, the share price has roughly doubled. Welcome to Camp Small Cap and the rollercoaster ride.

To give support to this move, a trading statement for the year ended December 2023 reveals HEPS growth of 120.4% to 135.2%.

KAP’s earnings take a klap – again (JSE: KAP)

The good news (I guess) is the base period is better than everyone thought

Further to the trading statement in December that gave the bare minimum disclosure (a decrease in earnings of at least 20%), KAP has now issued a further trading statement that shows a drop in HEPS of between 25% and 36% vs. the comparable period as published.

This distinction is important, as the base period earnings are being restated to allow for Safripol recovering R183 million from a supplier that had overcharged the company. The good news is that the R183 million was recovered, thereby increasing HEPS for the base period by 2.8 cents. The bad news is that this makes the year-on-year decrease even worse: a range of -31% to -41%.

At least debt is lower than a year ago and a revolving credit facility of R3 billion has been raised to refinance upcoming debt maturities. With a HEPS range of 19.8 cents to 23.3 cents, the group is still profitable despite all the strain at Safripol.

MC Mining’s independent board does not approve of the takeover bid (JSE: MCZ)

Or, as per Aussie takeover law, a resounding DO NOT ACCEPT all in capital letters

Things always get very interesting when independent boards play hardball with a potential acquirer. It is their role to make a recommendation to shareholders regarding whether an offer is fair. MC Mining’s board isn’t impressed with the bid by Goldway Capital for A$0.16 per share, calling it opportunistic and lacking an appropriate premium for control of the company. Simply, they believe the offer should be higher.

The board also notes that the bidders would need to hold at least 82.19% of shares in issue based on acceptances in order for the bid to become unconditional. This is because holders of at least 50.1% of the shares not held by the joint bidders must accept the offer based on the conditions imposed by the bidder.

Lots of narrative at Nampak – but no numbers (JSE: NPK)

It seems like things are moving in the right direction

Nampak is a turnaround story that I really struggle to get excited about. The company faces an incredible array of headwinds, making it very difficult to achieve meaningful returns for investors.

An update for the three months to December 2023 gave the market some important nuggets of information, like the news that operating profit has improved and net debt levels are down. Importantly, the divestiture plan is proceeding in line with previous guidance.

The South African business is on the wrong end of consumer pressures, although this does vary depending where in the group you look. For example, a good crop in the fruit season helped with the canned fruit business. The plastic and paper businesses have a less encouraging story to tell.

As is usually the case, currency issues in Nigeria and Angola continue to cause problems. At least demand is higher in Angola for cans, which is more than Nigeria can say.

The labour costs across the group are still a problem. Discussions with unions are in progress to limit increases. Although the company doesn’t say so in this announcement, one can reliably assume that unsuccessful negotiations could lead to job losses.

Concerningly, it seems as though working capital seasonality had a negative impact on cash generated from operations. This is expected to normalise by the end of March and it’s important that it does. The group must reduce debt by R243 million by the end of March and is on track to do so, with R180 million already done from the proceeds on disposal of the Nampak Nigeria Metals property and the UK apartment.

Yes, an apartment in the UK. You read that correctly.

With the existing chairman stepping down at the AGM, the board resolved to appoint Andre van der Veen to the chairman role.

Another hiccup at Renergen (JSE: REN)

Compressors have let the company down

The good news at Renergen is that LNG deliveries have recommenced after the maintenance outage.

The bad news is that there are yet more issues in the helium side of the business (which is what people care about). This time, the blame is being put on primary mixed refrigerant compressors, supplied by a Swiss group and assembled in China. The new part is expected to be delivered after Chinese New Year celebrations. Although Renergen may have a claim from insurance or against the supplier for the problem, it does once more raise questions around when the helium production will start.

The market continues to wait, with the share price having halved in the past 12 months.

Is mining cyclical? Just ask South32 (JSE: S32)

The dividend has all but disappeared

My dad ensured that I received a healthy dose of Led Zeppelin in my teenage years. I’m glad that happened, because I love the band today. They have a song called Good Times Bad Times and it’s a good thing to keep in mind when investing in mining.

For the six months to December 2023, South32’s revenue fell by 15% and the ordinary dividend has collapsed by 92%. Do not, ever, buy mining houses based on trailing dividend yield. You will frequently get hurt. The forward dividend yield is the right metric.

The reason for the drop in dividend is that diluted HEPS has also been smashed, down from 12.6 US cents to 1.2 US cents.

The reason for the drop? Well, despite record aluminium production, commodity prices went in the wrong direction and metallurgical coal volumes were lower. The show must go on of course, so the company has announced a $2.16 billion investment in the Taylor zinc-lead-silver deposit in Arizona (no relation to Swift) despite the drop in earnings. Production is only expected in H2 of FY27, which is a good reminder of the length of the planning cycle in mining.

Return on Invested Capital (ROIC) has plummeted from 12% to 1.3% and South32 will certainly be hoping for some improvement in commodity prices. The company expects a 7% production uplift in the second half of the year and will be driving cost efficiencies in the business, but mining houses can only do so much if commodity prices remain depressed.

Little Bites:

Director dealings:

Sean Riskowitz, acting as usual through Protea Asset Management, has bought yet more shares in Finbond (JSE: FGL), this time worth R755k.

Philip Kotze, who is a representative of Clover Alloys, has agreed to step down from the Orion Minerals (JSE: ORN) board to avoid potential conflicts of interest that would arise from discussions around funding and other opportunities with multiple parties (including Clover).

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")

")