If you can’t beat them, join them. Or – in the case of many of the businesses that we’ve covered in Magic Markets Premium – make them join you.

The bolt-on acquisition strategy is a commonly employed approach by large firms seeking to expand their presence or market share within a specific industry. In most cases, this strategy involves the acquisition of a smaller firm that operates within the same industry – often one that was once considered a direct competitor.

The goal? To integrate the acquired firm’s resources, technology and expertise in order to gain a competitive advantage, all while neatly mopping up a competitor’s share of paying customers.

It’s a little bit like forming a coalition in government, except in most bolt-on cases, the merger actually benefits the consumer and makes their life more convenient.

Does that mean every bolt-on acquisition is a guaranteed success? Of course not. If it were that simple, we’d probably be living in a world where three mega-companies own every other business ever conceived. Bolt-ons can be beautiful, but they can also be a serious drag on their parent companies.

Let’s dive into two examples from opposite ends of the spectrum:

Salesforce: yes, you can pay too much for a good thing

Salesforce was born and raised in the heart of Silicon Valley, a region renowned for its dynamic and fast-paced environment. This has cultivated a culture where the pursuit of growth takes centre stage, often at the expense of other considerations. Like many of its contemporaries in the tech field, Salesforce is a bit of an expansion-junkie, relentlessly striving to own more of the playing field – and sometimes disregarding the potential consequences.

The “land grab” strategy employed by Salesforce in its aggressive quest to dominate market share introduces multiple risks for shareholders. The exorbitant costs associated with these bolt-on acquisitions and the subsequent pressure to demonstrate returns on investment can lead to potentially unfavourable outcomes when investors start to put the screws on management. Or even the bolts.

In our report, we highlighted that Salesforce currently finds itself navigating a slower growth environment, necessitating a shift in focus towards profitability. As the company adjusts its strategies to maintain sustainable growth, there is a need to recognise the importance of balancing expansion with financial prudence.

Will they be able to kick the bolt-on habit and get their heads back in the game? Only time (and the balance sheet) will tell on that one. It’s not that the deals have been bad, but rather that the pricing has simply been too rich.

Nuts and bolt-ons: they just go together at Home Depot

When bolt-ons work, they work well. Perhaps our favourite example of this comes from our recent report on Home Depot.

Home Depot’s claim of a 17% market share within a massive $950 billion total addressable market is a notable accomplishment. However, there is still significant room for further growth and expansion. Based on our research covering over 80 companies in Magic Markets Premium, we’ve noticed that the leading company in any given industry can usually command over 20% market share.

This indicates that there is ample space for Home Depot to increase its presence and capture a larger market share. And what would be a smart way for them to gain that extra 3%? You guessed it – bolt-ons.

Over the past decade, the company has completed a total of 13 acquisitions. That’s an average of more than one bolt-on acquisition per year. These acquisitions have served as a means for Home Depot to expand its reach, venture into new markets, and integrate complementary businesses to strengthen its overall market position, all without betting the farm on one given deal or losing focus on the core business.

This approach aligns with the company’s objective of proactive expansion, allowing it to leverage its existing infrastructure, supply chain, and customer loyalty to drive growth in new markets. The assimilation of these acquired companies also enables Home Depot to benefit from economies of scale, operational efficiencies, and increased bargaining power with suppliers.

By focusing on acquiring companies that not only make sense under its brand but also add value to its customer base, Home Depot is winning the bolt-on game.

With well over 80 research reports on global stocks available in the library, a subscription to Magic Markets Premium for just R99/month gives you access to an exceptional knowledge base that has been built since we launched in 2021. Consider it a bolt-on to your existing investment knowledge!

The painfor shareholders in Accelerate never seems to end

In March, Accelerate Property Fund released a trading statement dealing with the year ended March 2023. It suggested that the distribution would be at least 15% lower than the prior year, attributed to an increase in the number of shares in issue by 26.5%.

Rather shockingly, the company has now said that there is no distribution for the year. At all. This has nothing to do with the number of shares in issue and everything to do with a need to “strengthen its financial position and liquidity requirements” – in other words, they can’t afford to pay anything to shareholders.

Bell Equipment releases a great trading statement (JSE: BEL)

This is much happier news than the last update

The ink is barely dry on Bell Equipment’s last announcement that gave the market the surprising news of a resignation by the CEO. Leon Goosen will be leaving on a high note it seems, with incredibly strong HEPS growth in the six months ended June 2023.

HEPS will be at least 30% higher, which suggests a minimum of 273 cents for this interim period. On a share price of R15.30, you get to a pretty appealing valuation multiple if you annualise that number.

The increase has been attributed to stronger market conditions this year, so that’s also good news.

Some bites from Bytes in Ghost Bites (JSE: BYI)

There’s a brief update on recent trading from the AGM

Bytes Technology Group has had a cracking year. I’ve been very pleased to have it in my portfolio, up 53% this year alone.

This is a UK-based software, security and cloud services group that was unbundled by Altron. Ahead of the AGM on Wednesday afternoon, the company released a short update on recent trading conditions since the release of full year results on 23 May 2023.

The first four months of the new financial year have seen double digit growth in gross profit and adjusted operating profit, which is lovely. However, margins have come under pressure, with gross invoiced income growing at a significantly higher rate than gross profit. There have been high volume, lower gross margin software deals in this period.

So although the net picture looks good for shareholders, investors need to be mindful of the impact of potential margin pressures going forward. For now at least, double digit growth in earnings is rather delicious, although Bytes is trading on a fat multiple that reflects high growth expectations.

Bad news at Hulamin (JSE: HLM)

NUMSA has embarked on a strike

Perhaps the only saving grace for the South African economy is that we’ve seen relatively less labour action in recent years than I remember seeing a decade ago. Hulamin isn’t quite so lucky at the moment, with NUMSA deciding to embark on a strike.

The dispute relates to employee benefits, of course. Hulamin says that it is willing to engage on a complete agreement that is compliant with the law. This implies that NUMSA is only willing to discuss some parts of the agreement and not others.

Either way, this isn’t what any company needs right now.

Kibo Energy’s subsidiary locks in a joint venture (JSE: KBO)

Mast Energy Developments has agreed on a JV with a consortium of investors

Kibo Energy has announced that its UK-based subsidiary Mast Energy Developments (MED) has agreed a joint venture with a consortium led by institutional investors. Under the terms of the deal, MED will contribute low-carbon flexible gas generation peaker plants into the joint venture and the investors will put in £31 million in capital over time. The initial contribution is £5.9 million.

To be clear, there’s no cash contribution from MED, with the company holding 25.1% in the joint venture. Effectively, MED has sold off a 74.9% stake in its asset through contributing it to the joint venture. Interestingly, MED will have joint control of the board and full control of the operations. MED will be paid a fee under a five-year management services agreement.

The investors will receive 90% of profits until the investment has been recovered in full, at which point the dividends will revert to the percentage shareholdings.

It gets complicated, but the entire transaction also allows MED to repay £800k to Kibo Energy, leaving £432k owing to the listed group.

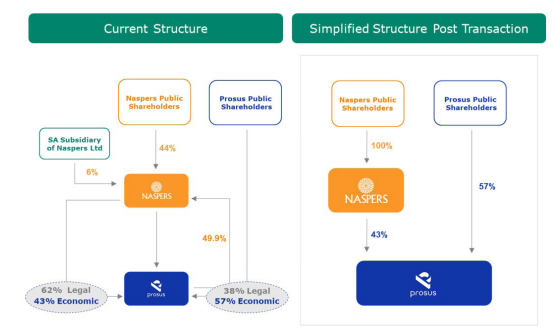

The circular for the unwinding of the cross-holding structure in the Naspers / Prosus group has been released. If you want to read it, you’ll find the whole thing here.

It’s a quantum leap forward for corporate structures. After all that time and money, they’ve arrived at the conclusion that the structure on the right is the correct one:

I know, right? Imagine a world in which Naspers shareholders hold Naspers, Prosus shareholders hold Prosus and Naspers has a big chunk of Prosus. Where is the fun in such a simple structure?

But the best is yet to come, dear JSE investors. I’ve never seen a company get away with not disclosing the costs of a circular, yet this is all that Prosus needed to disclose:

Not significant? What, as a percentage of the gigantic market cap? Come on.

Sasol is focused on air quality, not just earnings quality (JSE: SOL)

But not enough has been done

I’m certainly not going to pretend to be an expert in this space, or even a reasonably useful novice. Thankfully, the Sasol announcement about this issue is pretty clear.

Under the National Environmental Management: Air Quality Act 39 of 2004 (you need a breath of clean air just to be able to say that), Sasol needs atmospheric emission licences that are based on Minimum Emission Standards. There is the ability to apply for a facility or part of a facility to be regulated on an alternative emission load basis.

Sasol made this application for the boilers at the Secunda Operations and this application has been declined by the National Air Quality Officer. Sasol can (and will) appeal this to the Minister of Forestry, Fisheries and the Environment.

The group has spent over R7 billion over the past 5 years on emission reduction projects. This has led to 98% compliance with the Minimum Emission Standards. 98% is not 100%, as shareholders may now learn. Sulphur dioxide emissions from the boilers at the Secunda Operations are the major remaining challenge.

This isn’t something that can be fixed overnight and Sasol has an existing roadmap to try and achieve this. The regulator has clearly sent a message here. For investors, solutions come at a cost, so this isn’t good news for Sasol overall.

It’s probably good news for residents of Secunda and surrounding areas.

A smaller loss at Sebata – but still a loss (JSE: SEB)

The delayed results will be released this week

Sebata Holdings is late in the release of results for the year ended March 2023. Full results will be out this week, with a trading statement available to give shareholders an idea of what is coming.

The headline loss per share is between -13.98 cents and -14.98 cents, a very large improvement over -443.68 cents in the comparable period.

In case you’re wondering, the delay related to valuations that needed to be finalised for the current water and software B-BBEE deals.

Tharisa updates the market on quarterly production (JSE: THA)

Investors are as focused on the cash balance as they are on mining production

Tharisa’s share price has been getting properly whacked in recent weeks, driven by weakness in PGM prices. The 52-week low of R16.70 was hit on 10th July, a far cry from the 52-week high of R26 that we saw in December 2022.

Tharisa can’t control its share price and certainly can’t control commodity pricing. It can control its production and capital allocation though, which is why this quarterly update is important.

PGM output increased by 7.9% in Q3 vs. Q2, thanks to improved recoveries and a steady yield. In chrome, output fell by 6.4% despite a comment that grades, yield and recoveries were steady.

Pricing is where it all went wrong, with PGM prices down 16.6% in Q3 vs. Q2. Metallurgical grade chrome thankfully saw a 7.8% increase in price over the same period.

If we look at the nine months to June instead of just the third quarter, then year-on-year production is almost identical in chrome and is almost 15% lower in PGMs. Pricing for chrome is up by a very healthy 28%, with PGM pricing down nearly 22%. In those statistics, we can see why Tharisa is happy to have both commodities rather than just PGMs.

Importantly, cash on hand has increased from $205.8 million at the end of March 2023 to $242.6 million at the end of June. The net cash position is up from $101.1 million to $141.5 million over the same period. So with a market cap of roughly R5.6 billion, around R2.65 billion is in net cash.

The Karo project is on track, with a $135 million equity contribution by Tharisa over the course of the project. A recently concluded $130 million facility is undrawn as at the reporting period.

Tharisa seems to offer better PGM exposure than some of the alternatives in the market, though you can’t ignore the impact of PGM pricing on the share price.

At the end of June, Tharisa joined the Unlock the Stock platform (alongside property group Attacq) for a management presentation and Q&A. You can watch it here:

Little Bites:

Director dealings:

A director of Oceana (JSE: OCE) has sold shares worth R764.5k.

An associate of a director of Afrimat (JSE: AFT) has sold shares worth R234k.

A director of Growthpoint (JSE: GRT) has sold shares worth nearly R78k.

The scheme to delist Premier Fishing and Brands (JSE: PFB) has become unconditional and the delisting date has been set as 1 August 2023.

The COO of Fortress Real Estate Investments (JSE: FFA | JSE: FFB), Donnovan Pydigadu, has resigned. He will stick around until 31 December 2023 until moving on to new opportunities. He has been with the group for six years.

Delta Property Fund (JSE: DLT) has appointed Fikile Mhlontlo as CFO. His previous roles have included some tricky public sector posts like Denel and SAA, so he seems to bring experience in dealing with difficult financial circumstances.

If you’re in the audit industry, you may find it interesting that Telkom (JSE: TKG) has transitioned from joint auditors to a single auditor. The current auditors are PwC and SNG Grant Thornton, with Telkom selecting PwC as the sole auditor going forward. Shareholders will need to ratify this at the Telkom AGM.

Sable Exploration and Mining (JSE: SXM) could be the smallest company on the JSE, with a market cap of R2.5 million. It now has a full time financial director at least, with the part time director having resigned.

Choppies finally announces the Kamoso deal (JSE: CHP)

I just wish I understood it

At long last, we have a category 2 announcement for the Choppies – Kamoso deal. A category 2 transaction under JSE rules is a deal that is big enough to warrant a reasonable level of minimum disclosure, but not big enough to justify a shareholder vote.

Interestingly, in a category 2 under Botswana Stock Exchange rules, the audit committee needs to confirm that the terms of the transaction are fair to shareholders. Reading further, this also happens to be a related party transaction (as shareholders of the target include the CEO and another important figure at Choppies), which brings the need for a fairness opinion more in line with JSE rules. In this case, it looks like the opinion is prepared by the audit committee rather than an independent expert, although Grant Thornton did assist with the due diligence and valuation.

I must be honest with you: I don’t know what in the Gaberone is going on with these numbers. I read the announcement four times and I would welcome any corrections. Or an explanation. Anything, really.

High up in the announcement, it notes that Choppies will acquire 76% of Kamoso Group for two pula. Yes, just two Botswana pula. The shareholder loans of P28 million are also moving across. Fine, except a table further down in the announcement notes that the EBITDA of Kamoso is P66 million and the enterprise value is P340 million, so that’s an EV/EBITDA of 5.15x. A marketability discount of 15% has then been applied to the company. This suggests an equity value of P116 million that they are paying two pula for. Not two million pula, but two pula.

To add to my confusion, there is then P81 million of goodwill from this transaction. This implies that they paid a whole lot more than the net asset value, except they didn’t. Or they did. I give up.

The remaining 24% will continue to be held by the Botswana Development Corporation. Perhaps they understand the announcement.

The number that I do understand and will highlight is the net loss at Kamoso of 9 million pula. That EBITDA disappears rather quickly as you move further down the income statement.

The rationale for the deal is that Kamoso Group has a liquor licence, which solves a major problem for Choppies as the only major grocery retailer in Botswana without a liquor licence. Kamoso also has a hardware business, which is part of the Choppies strategy.

Seriously – if you understood the numbers, tell me. I’ll update this and credit you for making sense of it.

Conduit Capital finalises the disposal of CLAH (JSE: CND)

All conditions precedent have been fulfilled

In December 2022, embattled Conduit Capital announced the disposal of CLAH to Affinity for R20 million. It’s taken a long time to address all the outstanding conditions in the deal, which led to a couple of extensions for this deal.

All conditions have finally been met, with a disposal date of 3 July.

Another offshore deal for Invicta (JSE: IVT)

It’s been a busy period of deals for the group

Hot on the heels of the deal in Singapore that was recently announced, Invicta has given shareholders the news of another offshore transaction.

Within the Replacement Parts Auto – Agri business segment, Invicta has acquired 100% of the shares of Imexpart Limited (Imex) in the United Kingdom. This is a leading independent truck parts distributor, providing parts for a multitude of brands ranging from Volvo and Iveco trucks through to MAN coaches and buses. They also do parts for cars and vans, among other things.

The customers base is primarily in the UK and Ireland, which gives Invicta further geographical diversification in line with the group strategy. The benefit that Invicta brings to the table is a strong procurement capability, which can help improve gross margin at Imex. There are also Imex products that can be sold into other Invicta operations.

The effective date of the deal was 1 July and no financial information has been given, as this is too small a deal to be categorised and hence Invicta has made a voluntary announcement.

RMB Holdings is keeping its lawyers busy (JSE: RMH)

Beyond the Atterbury dispute, there’s also a fight underway under s164 with shareholders

We’ve reached a point on the JSE where a company cannot do a scheme of arrangement without attracting a group of opportunistic shareholders looking to apply s164 and get paid out fair value in the process. Now, if the share price is well below fair value, that’s a profitable strategy.

The law allows this, so it’s a clever use of s164. Companies hate it for obvious reasons, constantly lobbying for the rules to change. RMB Holdings has taken it a step forward, joining the Minister of Trade and Industry to the court action as the company looks to challenge the constitutionality of certain aspects of s164 of the Companies Act. The Minister will participate in the proceedings.

There were initially five dissenting shareholders to the special resolution back in July 2022. One withdrew the demand before the special dividend payment in October 2022, as a s164 action means you lose your entitlement to any dividends. Two have been settled now at 197.76 cents per share (with at least one of those entities linked to asset manager Chris Logan) and two have decided to go to court. The court action is by shareholders holding 13.27 million shares, so there’s a lot of money at stake here.

At some point, the courts will need to have a close look at how this section is being used in practice, with a common argument being that shareholders who buy after the initial announcement but before the meeting shouldn’t be allowed to use s164 as the behaviour is clearly opportunistic. I’m not sure if that timing applies to the shareholders in this court action, but all will no doubt become clear in months to come.

Either way, being the law firm on retainer from RMB Holdings is not a bad gig.

Little Bites:

Director dealings:

Encha Properties has sold 4.792 million shares in Vukile Property Fund (JSE: VKE), so it has made good progress with the intended sale of between 5.5 million and 6.0 million shares. The company is an associate of a director of Vukile and is the fund’s B-BBEE partner. The sale is being undertaken to deal with loan arrangements with Investec Bank.

If you’ve been wondering about the latest at Steinhoff (JSE: SNH), the next step is an extraordinary general meeting to vote on things like the dissolution of the company. The end is nigh.

In the very unlikely event that you are a Deutsche Konsum REIT (JSE: DKR) shareholder, the latest dividend is 247.61640 cents per share based on the exchange rate used in the calculation. It really does have the most epic bid-offer spread on the JSE, with bids at R0.03 and offers at R999.98. I truly have no idea why this thing is listed.

This episode of Ghost Stories is brought to you by Fedgroup, a diversified financial services group offering a range of financial products across investment, long-term insurance, lending, and fiduciary services. Fedgroup Financial Holdings (Pty) Limited is a licensed controlling company and entities within the Group are authorised financial services providers.

Established in 1990, Fedgroup has grown into a specialist financial services provider with over R10bn in assets under management and administration.

I was joined on this show by Grant Field, the Group CEO of Fedgroup since 2015, having worked for the group since 2002. We talked about a range of topics related to Fedgroup but we focused on impact investing and the unique product range that Fedgroup offers in this space.

Innovators in the impact investing space, Fedgroup has extensive experience and expertise in alternative investments, specifically within the renewable energy and smart agri sectors.

Combining this specialist expertise with their established licenses and offerings, Fedgroup has the capabilities to structure new investment offerings, such as their Specialist Endowment Portfolios, creating unparalleled value for retail and institutional investors.

As always, nothing you hear on this podcast should be interpreted as advice. This is for informational purposes only.

You can visit the Fedgroup website at this link to learn more.

A surprising resignation of the Bell Equipment CEO (JSE: BEL)

It’s never a good sign when a successor isn’t named, although there’s time to find one

Markets love certainty. By implication, markets hate uncertainty. With the Bell Equipment share price up by 23% in the past 12 months and almost 200% higher since the depths of the pandemic, CEO Leon Goosen was respected by the market. This share price performance came against the backdrop of a difficult relationship between the Bell family and a number of shareholders, related to a potential take-private of the company that never happened in the end.

Goosen has resigned from Bell to pursue another opportunity, whatever that may be. The saving grace here is that the effective date of the resignation is 31 December 2023, so there is time to find a successor. We just don’t know yet who the successor will be.

With Goosen having been on the board of directors since 2009, including roles as COO from 2014 to 2018 and then CEO until now, the successor will have big shoes to fill.

Invicta invests further in Singapore (JSE: IVT)

The group is acquiring a 50% stake in KMP Far East

Back in January 2022, Invicta acquired KMP with operations in the UK and USA. The group describes it as a “natural progression” to acquire a stake in KMP Far East, giving Invicta the KMP brand on a worldwide basis.

Importantly, Invicta is only acquiring 50% in KMP Far East. This allows existing shareholders and management to retain a large shareholding, which is important for incentivisation.

The business is focused on heavy-duty diesel engine parts for industrial and agricultural machinery in South-East Asia. The effective date of the deal was 1 April 2023, but the deal is too small to be categorised for JSE purposes and so this is a voluntary announcement.

Mondi buys a mill in Canada (JSE: MNP)

This is a $5 million deal with more investment to come

While Mondi is trying hard to sell Russian assets on one side of the world, the group is investing in Canada on the other side. Well, the “other side” is assuming you use the classic flat map of the world. In reality, Canada and Russia aren’t that far from one each other, with the Bering Strait separating Russia and Alaska by just 88kms. Canada borders Alaska.

Moving on from a geography lesson, Mondi is acquiring the Hinton Pulp Mill in Alberta, Canada from West Fraser Timber for $5 million. Mondi then plans to invest another €400 million in the asset (note the currency change), so the purchase price is barely a drop in the Bering Sea vs. that investment.

The goal is to produce and supply kraft paper into Mondi’s network of 10 paper bags plants in the region. At its core, this deal is all about securing the right site to improve the supply chain for sustainable packaging solutions across the Americas.

The RMBH – Atterbury issue heats up (JSE: RMH)

Like Dricus Du Plessis, but in a boardroom instead of the octagon

You have to focus here. RMB Holdings has an investment in Atterbury, but not enough to control the board. Atterbury owed R487 million to RMB bank (no longer related to RMB Holdings), for which RMB Holdings had provided a guarantee.

In an attempt to settle this amount, Atterbury was able to issue a share conversion notice to RMB bank to settle the loan with shares instead of cash. Instead, RMB demanded repayment under the guarantee from RMB Holdings, as the bank doesn’t want the shares in Atterbury.

RMB Holdings settled the debt under the guarantee through one of its subsidiaries and has now stepped into the shoes of the lender. In other words, after arbitration between the parties broke down, we now have a scenario where Atterbury owes RMB Holdings the money instead of RMB bank.

It goes a step further. Through the subsidiary that settled the debt, RMB Holdings has now demanded the amount of R487 million from Atterbury in cash.

It’s impossible to know for sure where this ends without seeing all the facility agreements, but the team at RMB Holdings knows a thing or two about investment banking.

Southern Palladium’s resource potential is clearer (JSE: SDL)

The total mineral resource (indicated and inferred) is 34% higher since drilling began

Southern Palladium has announced the first interim combined mineral resource update for the Merensky Reef and UG2 at the Bengwenyama Platinum Group Metal project.

The broader resource is larger than the figures presented in the 2022 IPO prospectus, thanks to the far east block of the UG2 resource rather than the Merensky Reef. Although there is a bigger opportunity, the initial drilling focuses on the defined UG2 payback area: the portion of the UG2 reef that can achieve capital payback of the project.

Junior mining is all about making the most of limited capital.

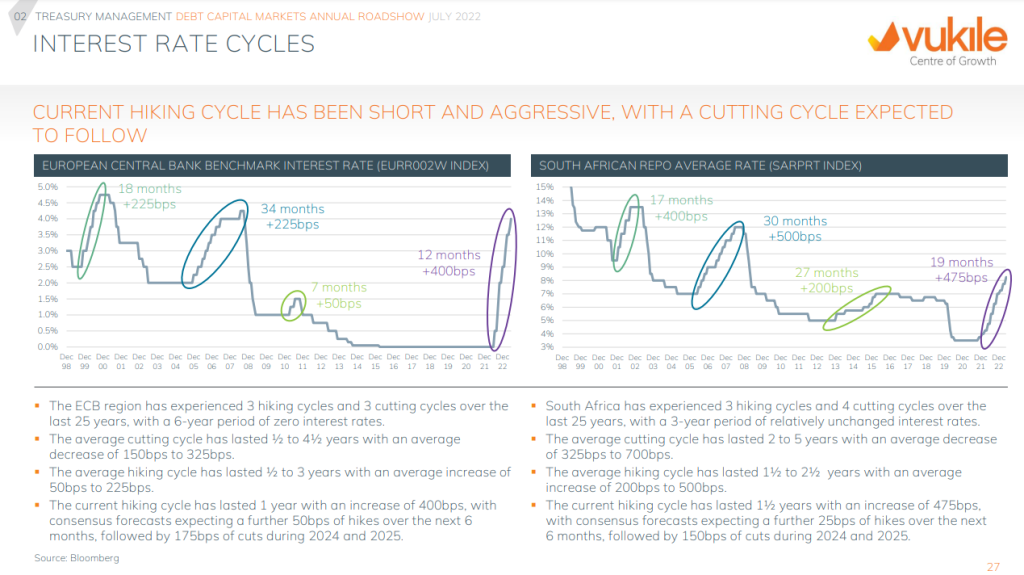

Vukile reminds us how severe the rate hikes have been (JSE: VKE)

There’s a lot of good stuff in the debt roadshow presentation

Vukile is busy with a debt capital markets roadshow. This is perfectly normal for a property fund, as there is always debt on the balance sheet and it regularly needs to be refinanced or optimised.

The full presentation is available here, including interesting slides like this one:

We often lose perspective on just how severe this hiking cycle has been, particularly in Europe off a base of zero rates. These Vukile charts do a very good job of reminding the markets what we have all lived through.

Little Bites:

Director dealings:

An associate of a director of Afrimat (JSE: AFT) has sold shares worth R2.38 million.

Written by Paul Counihan, Fedgroup Chief Wealth Officer, and Nomzamo Manqele, Fedgroup Financial Specialist.

Everyone wants to know what the future holds. We develop forecasting tools and models to make predictions, but even in this interconnected age with access to the best technology and smartest analysts, nobody saw the deluge of black-swan events of the past three years coming.

Global events of this magnitude can have a catastrophic impact on our investment portfolios. And for most investors, they already have.

While these events can create volatility and uncertainty in the market, understanding that turbulent markets are an expected response to global events can help us avoid making rash decisions and maintaining a disciplined investment approach that focuses on our long-term objectives.

Although markets reacted to a worldwide pandemic or global forces being pitted against each other exactly as expected, there has been a seismic shift in the underlying global economy.

We enjoyed a prolonged bull market, but we now find ourselves in what many expect to be an extended bear market. And that doesn’t bode well for those traditional assets that are linked to market sentiment. A decrease in the availability of equities on the JSE, coupled with the universal underperformance of traditional asset classes and a government pursuing its own goals, has seen South African investors move their money offshore en masse. But even that doesn’t work when the whole globe finds itself in a high interest rate cycle.

The problem with these events is that they can happen at any time, and you can never be sure how long their effects will last, throwing even the best laid plans off-kilter. And what do people do when faced with the unknown? They stick to what’s familiar, even when what is really required is some lateral thinking and common sense.

We’ve proven that we can’t predict the future, but we can learn from the past and plan accordingly. This is where the cardinal rule of investing comes into play. Diversification is less likely to let you down than those models that didn’t predict a global pandemic.

No longer a nice-to-have, true diversification offers investors a way to smooth out financial journeys by having assets with uncorrelated performance and risk factors rather than simply incorporating a limited range of similar assets, as many traditional investment vehicles do.

So, with most portfolios invested in the same collection of funds and their performance so highly correlated to the same events, how do we go about bolstering investment portfolios against the unpredictable and the uncertain?

The answer relies on us taking off our equity blinkers and re-evaluating what we consider to be viable investment options.

Commanding a mammoth share of the investment landscape, the alternative asset class represents a feasible option for investors with strained portfolios. And although they often play in an unregulated space, all alternative assets are not created equal and don’t come with the same risk profile. Sustainable assets, for example, have become more mainstream and address the needs of investors as well as some of our country’s key socioeconomic pain points.

Due to its growing prevalence and track record, alternative investments are becoming increasingly accessible to investors. And when packaged by a credible financial services provider with the requisite experience and track record in managing alternative assets, products that are built on the right, curated selection of underlying assets could change the investment landscape.

And those opportunities to invest in the real economy and contribute to alleviating some of our nation’s biggest concerns exist and are open to those who are willing to explore innovative ways to diversify their portfolios.

Astute investors are already investing in the commercial-scale installation of solar panels and in ventures that provide much-needed finance to farmers. Businesses operating in these sectors are more likely to stand the test of time and therefore inspire confidence in the stability of future investments.

The existing angst-inducing market conditions will undoubtedly also have an impact on the performance of investment portfolios for years to come. While we don’t have control over the decisions made by heads of state, we owe it to ourselves to interrogate our existing assumptions and explore new investment strategies that incorporate counter-cyclical assets offering greater stability to investment portfolios. We must consider allocating a responsible portion of investment funds towards alternative assets that have a proven track record of riding out and overperforming in bear markets.

We shouldn’t disregard entire asset classes based on psychological biases. Market cycles will inevitably continue to change for as long as people continue to invest.

The key is to build an investment portfolio that is robust and sustainable enough to withstand the volatility and turbulence that accompany these market cycles – investment portfolios that are geared for any eventuality.

Speak to your financial advisor about Fedgroup’s Impact Portfolio, a curated selection of alternative assets wrapped in an endowment structure to offer true diversification and greater peace of mind.

Mr Price (JSE: MRP) recently announced that South Africa’s energy crisis and associated load shedding wreaked havoc on its financial performance, resulting in a staggering revenue loss of approximately R1 billion for the full financial year ended on 1 April 2023.

The retailer’s core trading divisions suffered a severe blow in the financial year’s second half, particularly during the festive season when load shedding struck with unprecedented intensity, resulting in an annual loss of 318,000 trading hours.

Being a local value retailer, Mr Price had exercised caution when investing in backup power, as historical experiences with load shedding had been somewhat manageable. However, the dire situation took an alarming turn after September 2022, with power outages escalating to unparalleled levels, eclipsing the cumulative quantum of the previous 15 years.

South Africa’s heightened energy crisis and inadequate alternative energy sources resulted in an estimated loss of 318,000 trading hours, equivalent to roughly R1 billion in revenue.

With only 37% of Mr Price’s core business possessing backup power utilities by the end of September 2022, the heightened levels of rolling blackouts took a significant chunk out of the retailer’s top line, paving the path for implementing energy continuity plans. Indirectly, the repercussions of load shedding extended to customer behaviour, leading to diminished consumer confidence and a pressing need to reduce unsold stock levels, further curtailing the company’s top and bottom-line figures.

Despite load shedding ticking down throughout the winter period, much to the surprise of many local consumers, the power crisis is far from over. To combat this dire energy situation, Mr Price has implemented energy continuity roll-out plans and a substantial investment of R220 million in backup power systems.

Fundamental Analysis

Despite the adversity caused by loadshedding, Mr Price achieved a commendable revenue growth of 17% year-over-year, amounting to R32.85 billion for the financial year ending 1 April 2023. Notably, this figure includes the acquisition of a 70% stake in the Studio 88 Group in October 2022. Despite robust revenue growth amidst a period rife with extensive power disruptions, the effects of load shedding during the festive period resulted in a modest 5.4% year-over-year increase in the retailer’s annual EBITDA, coming in at R7.2 billion for the latest financial year. Furthermore, the group’s headline earnings per share (HEPS) figure declined by 6% year-over-year, reaching 1,205.70 cents, down from 1,282.10 cents for the prior year. Moreover, basic earnings per share (EPS) declined by 6.8% year-over-year, arriving at 1,210.70 cents, down from 1,298.60 cents.

Headline earnings per share (HEPS) increased from 1,100.10 cents for the 2018 fiscal year to 1,205.70 cents for the 2023 fiscal year, translating to a five-year compound annual growth rate of approximately 1.9%. Dividends per share (DPS) increased from 693.10 cents in 2018 to 759.60 cents in 2023, implying a five-year compound annual growth rate of 1.8%. Over the same time horizon, from 2018 to 2023, Mr Price has maintained the same dividend payout ratio of 63%, excluding the 2020 financial year, where it decreased its payout ratio to 29.7%. Despite retaining the same payout ratio, the group reported a 5.9% year-over-year dividend per share (DPS) decline from 2022 to 2023.

Notably, the retailer’s profitability and gearing ratios – return on net worth, return on average equity, return on capital employed and return on operating assets – all sit at their lowest levels when analysing the time horizon spanning from 2018 to 2023.

The group’s return on net worth currently sits at 23.9%, down from 27.8% in 2022, while its return on average equity sits at 24.8%, down from 29.2% in 2022. Moreover, the retailer’s return on capital employed comes in at 23.1% for the latest fiscal year, lower than the 27.3% reported in 2022. Return on operating assets comes in at 51% for the 2023 financial year, significantly down from the 74.6% reported for the 2022 fiscal year.

Over the same period, Mr Price reported their weakest current and quick ratios, with the former coming in at 1.6x for the 2023 financial year, significantly down from 3.1x reported in 2018 and 2.5x reported in 2022. The group posted a quick ratio of 0.6x for the latest financial year, significantly down from 2.2x in 2018 and 1.6x in 2022. Amidst South Africa’s dire energy situation, suppressed consumer sentiment, and rising interest rates curtailing customer spending, the retailer’s inventory turnover ratio comes in at 3.4x for the 2023 financial year, the lowest reading in over five years. Mr Price reported a total liabilities to total shareholder equity ratio of 1.1 for the 2023 fiscal year, significantly higher than the 2018 reading of 0.4 and the 2022 reading of 0.9. When looking at the six years spanning from 2018 to 2023, the 2023 reading of 1.1 is the highest across all six years, implying a significant reduction in solvency. The gradual weakening of the group’s current and quick ratios over the period spanning from 2018 to 2023 indicates an overall decrease in liquidity levels.

Delving into the group’s cash flow statements, net cash inflows from operating activities surged by an impressive 23.6% year-over-year, coming in at R5.94 billion for the financial year ending 1 April 2023, up from R4.81 billion in the prior fiscal year. Cash generated from operations increased by 9.7% year-over-year, coming in at R6.26 billion for the 2023 financial year.

Looking ahead, Mr Price anticipates continued challenges in the trading environment for the first six months of the 2024 fiscal year. While consumer price inflation (CPI) decreased slightly from 6.8% in April to 6.3% in May, the group emphasises that subsequent interest rate hikes have not significantly curbed inflation. As a result, consumers are shifting their spending toward non-discretionary items.

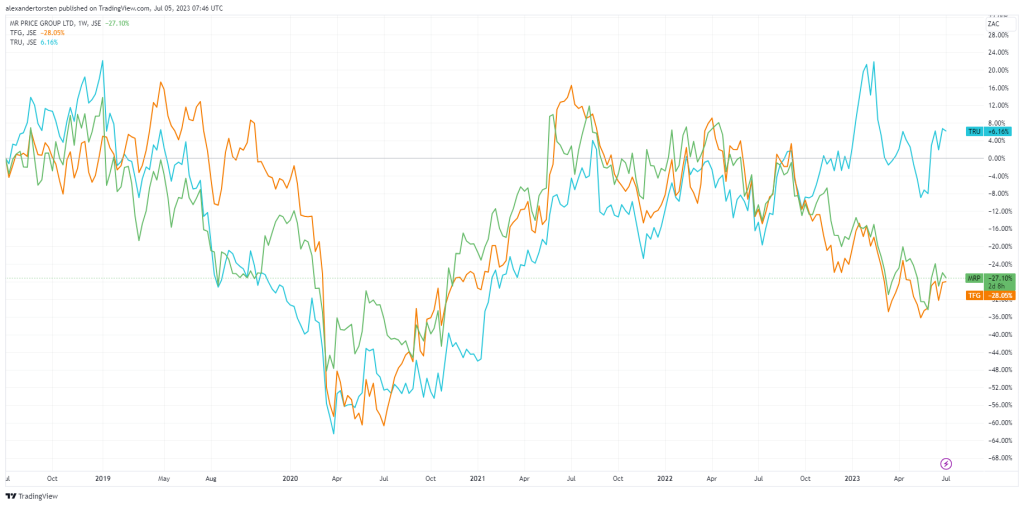

Comparative Analysis of Share Prices: Mr Price, Truworths, and The Foschini Group

Over the past five years, Mr Price (JSE: MRP) and The Foschini Group (JSE: TFG) have seen their share prices underperform relative to Truworths (JSE: TRU).

The price chart below displays the dismal five-year share price performance of Mr Price (green line) and The Foschini Group (orange line), returning -27% and -28% to shareholders, respectively. Over the same period, Truworths (blue line) has produced a measly 6% to shareholders.

Technical Analysis

Looking at the daily price chart of Mr Price, the price action has been under bearish pressure, trading lower in a descending channel since April 2022. Despite testing the primary support level at R124 per share (red line) towards the end of May 2023, the price action increased toward higher levels, testing the R149 per share (green line) resistance level in June but failing to break above that level.

The bulls will look for the share price to break above the R149 resistance level, a share level towards the R166 per share (horizontal black dotted line) resistance level, which could prevail as a level of interest for bullish investors and traders alike. The bears will look for the share price to decline toward the primary support level at R124 per share, which could be in play if negative sentiment persists or macroeconomic headwinds worsen.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Spear REIT released encouraging first quarter metrics overall, but the company certainly isn’t immune from the broader macroeconomic challenges despite being focused on the Western Cape.

Attacq has agreed terms with the Government Employees’ Pension Fund (GEPF) for the acquisition of a 30% stake in Attacq’s Waterfall portfolio.

AngloGold’s restructure into a NYSE-listed group doesn’t come cheap, with advisory fees of over R1.1 billion!

Brikor has decided to focus on its core brickmaking business, with TCQ Mining taking responsibility for the coal operations and giving Brikor a more stable return on them.

Mondi is a step closer to getting out of Russia, with the Gotek Group deal completed and the sale of Syktyvkar still needing to be achieved.

Sappi is discussing the future of the Stockstadt Mill with various stakeholders in Germany, as the company doesn’t believe that the facility can be sold as a going concern.

Telkom’s board has rejected the proposal from Afrifund, Axian and the PIC – the consortium led by ex-CEO Sipho Maseko.

RCL Foods has suffered a R234 million knock from a special levy by the South African Sugar Association, a direct result of Tongaat Hulett not paying its levies anymore.

Tania Habimana invited me to CNBC Africa for a detailed discussion on local retailers and whether I would buy any of them.

I thoroughly enjoy live TV interviews, not least of all because I get a kick from seeing the purple ghost logo on the screen on shows that I watched long before becoming a ghost. CNBC Africa is a great example of this, with a recent chat with excellent host Tania Habimana on local retailers.

It’s rough out there for South African consumers and we are seeing this come through in the numbers and the share price performance of the local retailers.

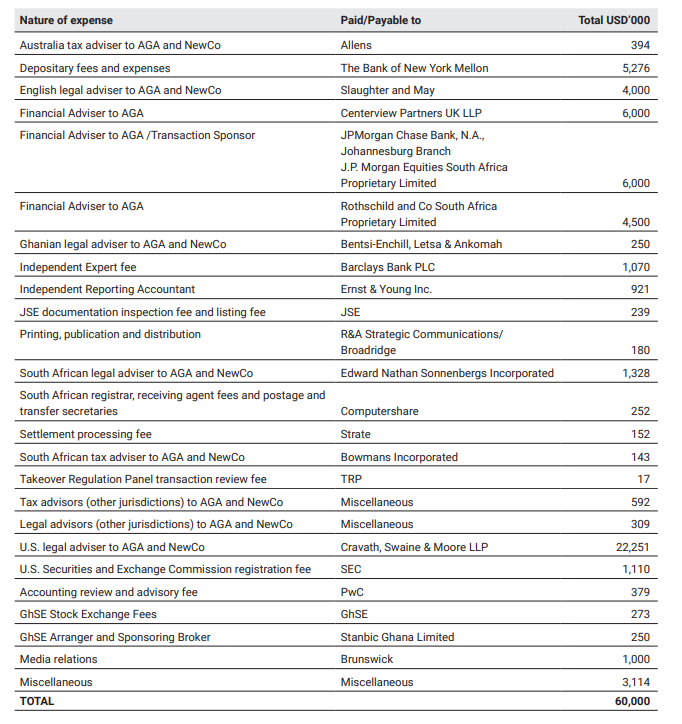

AngloGold’s corporate restructure costs $60 million (JSE: ANG)

Yes, that is well over R1 billion to restructure the group!

AngloGold Ashanti has a market cap of R160 billion. This makes it a meaty group that corporate advisors saw coming from a mile away, with costs of the intended restructure coming in at a truly spectacular $60 million. Here’s how that money gets spent:

This table comes from the pre-listing statement that has been released as the next major step in the corporate reorganisation. When all is said and done, AngloGold will have its primary listing on the NYSE and inward listings on the JSE and A2X, as well as a secondary listing on the Ghana Stock Exchange.

This entire gedoente is to convince the market that AngloGold is an international gold group rather than a South African company, which should hopefully drive a higher valuation multiple over time. It also gets the company a lot closer to North American investors, which isn’t a bad thing as that is the deepest pool of capital on the planet.

Choppies is still looking at Kamoso Group (JSE: CHP)

The cautionary announcement has been renewed once more

Botswana retail group Choppies has been figuring out a potential acquisition of the Kamoso Group for several months now, with the first cautionary announcement having been released in January 2023. The intended deal is an acquisition of a 76% controlling stake in the FMCG (fast-moving consumer goods) business.

Choppies has already received conditional approval from the Botswana Competition and Consumer Authority, even though there’s a long way to go in finalising the terms of any deal.

Eastern Platinum is being dragged to court (JSE: EPS)

The company is fighting with ABT Toda over a construction agreement

Eastern Platinum announced that its South African subsidiary, Barplats, is being taken to the High Court by ABT Toda, which is the intended nominee of Advanced Beneficiation Technologies (ABT) to hold its interest in a joint venture between Barplats and ABT.

That joint venture clearly hasn’t gone the way the parties intended. Barplats and ABT are in an arbitration process to deal with a dispute over the development and construction of a modular plant to process PGMs at the Crocodile River Mine. Various milestones needed to be met and weren’t, but that hasn’t stopped an escalation of this matter by ABT.

Shouting by Nedbank shareholders, but no substance (JSE: NED)

A strange habit has developed in the market around voting on remuneration policies

These days, you just aren’t a good corporate citizen unless you vote against remuneration policies at corporates. It almost doesn’t matter whether the policy is fair or not, as some players in the market just can’t bring themselves to vote in favour at any company.

Embarrassingly for those 25.24% of Nedbank shareholders at the AGM who voted against the remuneration policy, not a single one sent through questions or comments to Nedbank to engage on elements of the report. Not one.

If this isn’t the greatest example of the classic “Karen” complaining on Facebook about something ridiculous that can’t be backed up, then I don’t know what is.

Telkom’s board says no to Afrifund / Axian / the PIC (JSE: TKG)

The board thinks that the current Telkom strategy will create more value for shareholders

When a potential suitor comes to the table, the board needs to consider whether it will take the deal to shareholders. If they don’t, then there’s a chance that it goes hostile in the form of an offer directly to shareholders. This seldom happens because the deal risk (and costs) go through the roof.

The Afrifund consortium (consisting of ex-CEO Sipho Maseko, international partner Axian Telecoms and most recently the PIC) will now need to decide whether to sweeten the existing offer to the Telkom board or take it directly to shareholders. This is because the board has decided that the proposal isn’t in the best interests of shareholders, with the current Telkom strategy believed to be generating a better outcome for shareholders.

Here’s a chart of how the current strategy is performing:

Little Bites:

Director dealings:

A director of Dipula Income Fund (JSE: DIB) has bought shares worth R664k.

A director of Adcorp (JSE: ADR) bought shares worth R384k.

An associate of a director of Acsion (JSE: ACS) has bought shares worth R292k.

I usually ignore independent director appointments in Ghost Bites as they don’t really tell you much about the company. Occasionally, something catches my eye. The Foschini Group (JSE: TFG) has made two major appointments, with Jan Potgieter (ex-CEO of Italtile) and Nkululeko Sowazi (co-founder of Tiso Investment Holdings) both joining the board as independent non-executive directors.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")