The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I looked at some of the more interesting stories in a busy few days of news.

Bell Equipment has released really strong results, but watch the cash.

Transaction Capital’s nightmares continue, with news of the departure of David Hurwitz and underlying earnings in a tough spot, sending the share price back below R6.

Capitec found some love in the market despite modest HEPS growth.

Caxton & CTP is a tale of two segments right now, with heavily discounted look-through exposure to Mpact making it interesting.

City Lodge’s occupancies are higher, but the market is looking for pricing power and that is lacking.

Sun International’s resorts and hotels segment boosted the group in the latest result, with gaming revenue also moving higher.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Bell Equipment: let’s talk about cash, baby (JSE: BEL)

Specifically, where did it go?

The Bell Equipment share price has had quite a year, posting a year-to-date increase of 23.7% according to Google Finance. The share price has shot straight up this month, which leaves it vulnerable to a correction and consolidation.

After the release of trading statements caused all the buzz, the release of detailed results didn’t add to the party. In face, the share price was slightly down on the day.

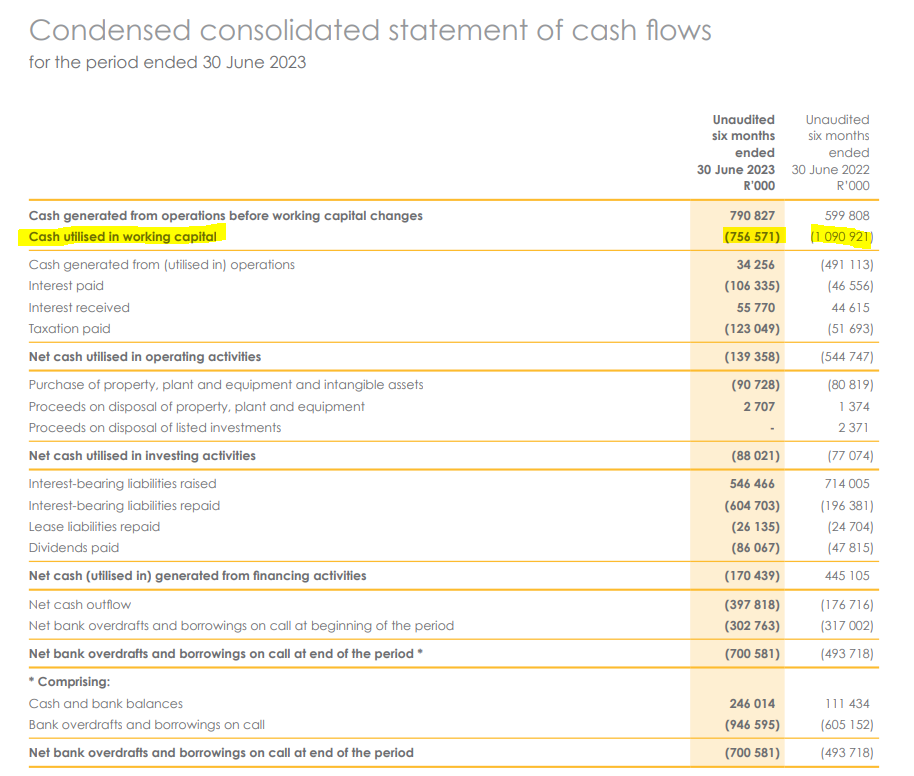

The metrics certainly look good, with revenue for the six months to June up by 42% and HEPS jumping 63%. Cash is important too, with that metric telling a very different story.

Despite profit from operating activities of R535.9 million, the cash outflow for the period was nearly R398 million. Last year, profit was R308 million and the cash outflow was R177 million, so this mismatch isn’t anything new.

The culprit is right at the top of the cash flow statement, with almost all the cash generated in this period being sucked into working capital. At least it’s better than last year:

The inventory balance has jumped from R4.75 billion to R5.88 billion. This is based on a planned increase in production volumes and shipping delays from South Africa. If you exclude inventory, Bell’s balance sheet isn’t exactly cash flush. It’s not in bad shape, but investors will keep a close eye on working capital.

There is no interim dividend once again, which makes sense in the context of the balance sheet.

City Lodge occupancies are ahead of 2019 levels (JSE: CLH)

But room rates haven’t recovered yet, so pricing power remains a concern

Group occupancy at City Lodge is up by a whopping 18 percentage points year-on-year, coming in at 56% for the year ended June 2023 vs. 38% in the prior year. Importantly, this is now slightly ahead of 55% in the FY19 result before the pandemic slaughtered the industry.

Although average room rates are up 12% vs. last year, they remain below pre-Covid levels. Pricing power to fill the hotels is in doubt here. What isn’t in doubt is the success of the food and beverage strategy, now contributing a significant 17% of total revenue (up from 15% last year). With load shedding as an ongoing reality for all of us, giving people a place to work and eat really isn’t a bad approach in this market, even if they don’t stay the night. The gross profit margin on food and beverages improved from 55% to 58% year-on-year.

As great as that is, it will be important to the investment case that room rates make a full recovery as well. The inflationary pressures in the cost base are substantial, with property costs up by 19%. The fixed cost base isn’t static.

Still, EBITDAR (the “R” isn’t a typo – this is industry standard in hospitality) increased by 83% and EBITDAR margin increased from 27.5% to 32.4%.

Thanks to a vastly improved balance sheet, a dividend of 8 cents per share has been declared. This is despite a significant capital investment programme in the new financial year with a clear focus on renewable energy solutions. They even need to put in place water solutions at some of the facilities, as supply can be erratic.

The good news for the new financial year is that occupancy has run at over 60% since the end of the financial year. The warm weather has only just begun, so hopefully a strong few months are ahead.

The share price hasn’t moved much based on these earnings. I think the market is keeping an eye on return on assets and the pricing power concerns I’ve highlighted.

Metrofile is swimming upstream (JSE: MFL)

If you love picking up coins in front of a steamroller, this one is for you

Metrofile isn’t exactly the most exciting company around. Image processing and document storage isn’t high on the list of “things I want to do when I grow up” for most people. The latest numbers won’t do anything to change that.

Excluding the acquisition of IronTree Internet Services, revenue has increased by 13%. Including that acquisition, revenue is up by 16%. That sounds pretty good, but wait until the bottom of the income statement. Before we move away from revenue, it’s important to note that gross box volumes intake was 6% and destructions and withdrawals were 9%, so closing box volumes fell by 3%.

Operating profit only increased by 6%, with margin mix as a concern because image processing is lower margin than other sources of revenue. There are obviously also inflationary pressures on costs. The company has invested in its go-to-market sales team, so more money is being put behind marketing to try and turn the tide on the drop in volumes.

Net debt increased by 11% and net finance costs were 18% higher because of the increase in prevailing interest rates. This is why HEPS could only limp 5% higher. The dividend for the year of 18 cents was consistent with the prior year, so the payout ratio dipped.

On a share price of R3, that’s a dividend yield of 6%. This means that the market is expecting the company to deliver meaningful growth in HEPS. Although this period wasn’t exactly a thrill ride, the company has highlighted important contracts in South Africa and the UAE that have been won.

The share price performance over 5 years is slightly in the red, so investors have had to be content with dividends over that period. The share price is down 14% this year.

Sun International confirms that we are still jolling (JSE: SUI)

South Africans know where the party is

Even load shedding couldn’t stop the Sun International party in the six months to June 2023, with income up 11.7% and adjusted EBITDA up by 5.6% thanks to diesel costs and a stronger contribution from resorts and hotels, which is a lower margin business (22% in this period) than gaming. Although margins are under pressure, this is a positive change in profits and that’s good going in this environment. Group adjusted EBITDA margin fell from 28.7% to 27.2%. Without load shedding, it would’ve fallen to 28.2% instead.

Adjusted headline earnings per share tells a better story, up 10.1%. When you consider the backdrop against which this result has been achieved, it looks pretty decent. The market certainly thought so, with the share price trading around 6% higher by lunchtime.

The major driver wasn’t gaming revenue, which contributes 78% of group income. It grew 6.6%, with casino income up 3.2% and Sun Slots slightly down year-on-year because of load shedding. SunBet generated record income, up 138.4% year-on-year. If you are willing to place much reliance on management’s calculation of adjusted EBITDA, then SunBet is up from R14 million to R90 million as income has moved significantly above break-even level. The company recognises that SunBet operates in a highly competitive industry and the hope is to differentiate through SunBet being part of the wider Sun International offering. They are aiming for 10% market share in online betting by 2026.

The real winner was resorts and hotels, up 26.9%. People are clearly hungry for experiences in a post-pandemic world and the weak rand really helps. Not only does it make us more appealing as a global destination, but it also means that locals who used to be able to afford an overseas holiday can now only afford to take a Sho’t Left. Average occupancy increased from 57% to 66.8%.

South African debt sits at R5.9 billion which is in line with December 2022 levels. Debt to adjusted EBITDA is at 1.8 times. Net interest jumped by 40.3% as the prevailing interest rates have increased substantially. With debt to adjusted EBITDA below the target of 2.0 times, a dividend based on 75% of adjusted HEPS has been declared. This is an interim dividend of 148 cents.

The outlook for the remainder of this year is bullish, which would also have been a contributor to the positive share price response.

Hurwitz didn’t survive the Transaction Capital mess (JSE: TCP)

Jonathan Jawno is back in the hot seat to try and fix this nightmare

I must say, I was skeptical about David Hurwitz managing to survive the SA Taxi debacle with his group CEO role still intact. We now have the answer, as he will step down effectively from 31 December 2023 and will remain available in 2024 to ensure a smooth handover. It sounds like 2024 will be gardening leave for him, so life could be worse.

The Transaction Capital garden isn’t looking so good and the share price performance on Tuesday morning is likely to be ugly. Aside from the catastrophe at SA Taxi, WeBuyCars expects earnings to be approximately 20% lower year-on-year, with a notable decision not to open any new branches in the second half of the 2023 financial year. Nutun’s earnings are growing more slowly than previously communicated. At a time when the group desperately needed the other divisions to do well or even outperform, it just hasn’t played out that way.

This brings us neatly to SA Taxi, with that segment renamed Mobalyz in an effort to get us to forget about how bad things are. There have been significant restructuring activities, moving towards a more variable cost model to help the group weather the storm. This results in savings of R500 million per year. Credit is being tightened and operations are being simplified, with the auto refurbishment and repair facilities potentially being sold. The business really has fallen apart, with short-term tactics to improve cash flow that definitely reduce the strategic moat over the long-term.

Aside from Jonathan Jawno who is spearheading the SA Taxi restructure, Chris Seabrooke is now chairing a Mobalyz Debt Sustainability Committee as Sabvest has a significant stake in Transaction Capital. It really is a case of all hands on deck.

Get ready for the share price to Mobalyz itself, firmly in the wrong direction again.

Transpaco agrees to a big repurchase at a discount (JSE: TPC)

This actually shows you how hard it is to sell a large stake in a local small- or mid-cap

Manufacturers Investment Company (Pty) Ltd is a private company that holds a meaningful stake in Transpaco. As liquidity in this stock is low, it’s just about impossible to sell a stake this size without bombing the share price of the company is the process. Welcome to life in local small- and mid-cap companies.

Transpaco is wise to the opportunity to provide exit liquidity to this shareholder in a form of a specific repurchase. Of course, this is at a discount to the current share price, so it’s a win for the remaining shareholders.

The stake represents 3.67% of shares outstanding and the cash consideration for the repurchase is R30.6 million. The price is R27.83, which is a 10.10% discount to the 30-day VWAP calculated based on Friday 1 September. The current share price is R33.76 but this is where a VWAP is so important, as illiquid stocks can move by large percentages on thin volumes. A VWAP takes that into account (as this is a volume-weighted calculation).

A circular will be sent to Transpaco shareholders to approve the proposed buyback.

Little Bites:

Director dealings:

Des de Beer has bought another R17 million worth of shares in Lighthouse Properties (JSE: LTE).

A director of AngloGold Ashanti (JSE: ANG) purchased American Depository Receipts worth $33k.

The Blue Label Telecoms (JSE: BLU) story continues to divide the market. A director of a subsidiary selling shares worth R97k doesn’t do any favours for sentiment.

We don’t know what transaction Clientele Limited (JSE: CLI) is contemplating, but we know that negotiations are still alive and well because a further cautionary announcement has been issued.

There’s still no sign of financials at Salungano (JSE: SLG), as the audit process cannot be completed until the refinancing process has been concluded. One of the conditions of the refinancing process is the appointment of a Chief Restructuring Officer, which tells you how things are going. No timing has been given in the announcement for the release of financial results. The shares remain suspended from trading.

Imtiaz Patel is stepping down from the board of MultiChoice (JSE: MCG), where he currently serves as Chair. Elias Masilela will take on that role, having already been on the board as an independent director for a while. Importantly, Patel will continue consulting to the group until 2028, with specific involvement in ShowMax and SuperSport. Although institutional knowledge is important in any organisation and Patel has plenty of that, this does also raise some questions around succession planning and the depth of talent in the group.

Advanced Health (JSE: AVL) announced that all conditions for the clean-out dividend of 20 cents per share and scheme of arrangement at 80 cents per share have been met.

Tsogo Sun (JSE: TSG) repurchased shares to the value of nearly R1.8 million in the odd-lot offer.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Capitec finds bidders with a trading statement (JSE: CPI)

It’s a voluntary update, so don’t expect any “at least 20%” news here

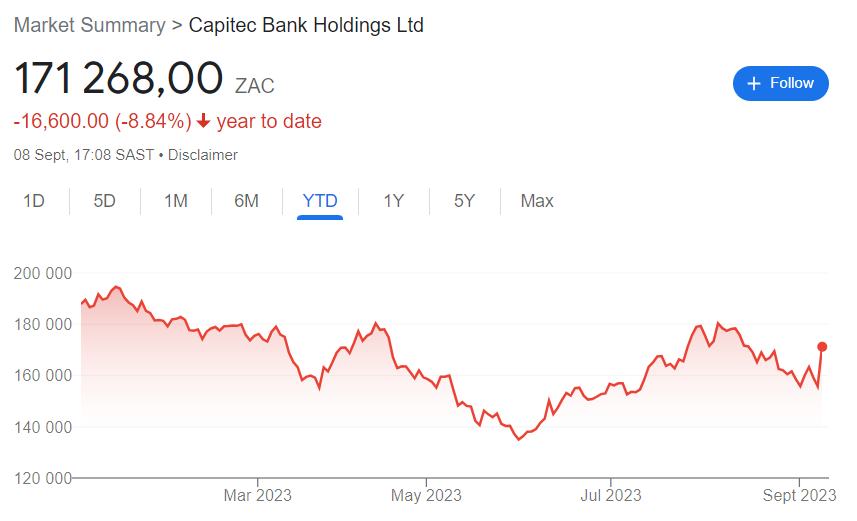

There’s nothing stopping companies from giving the market more updates than the minimum required under JSE rules. Even though Capitec is a long way off the threshold that triggers a trading statement (a 20% move in earnings), the company released a voluntary update based on earnings for the six months to August.

Group HEPS will be between 8% and 10% higher year-on-year, which the market seemed to love as the share price closed nearly 10% higher.

It hasn’t exactly been a happy year for the share price, with the gain on Friday helping to regain some of the recent lost ground:

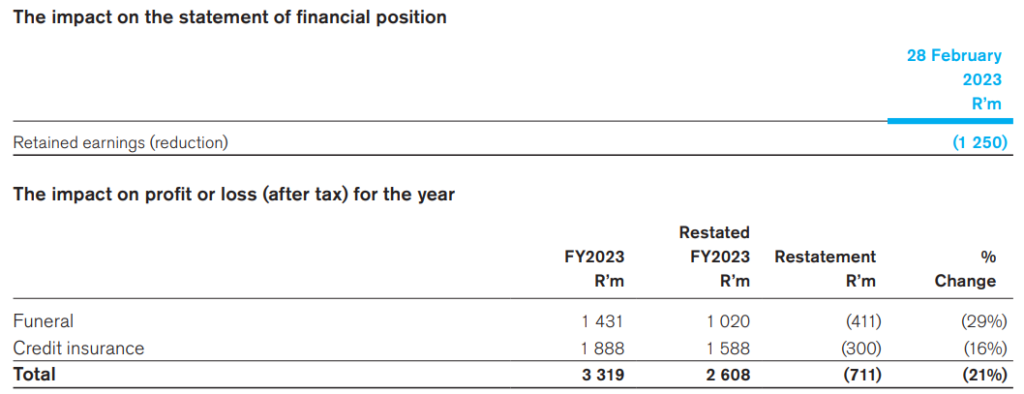

Due to the funeral and credit insurance businesses within Capitec, the group hasn’t escaped the introduction of IFRS 17 Insurance Contracts. This is the new standard that has caused major swings in earnings at the likes of Sanlam. There’s an entire report on the impact of this standard on Capitec (you can find it here) with this table showing how significant the difference is on restated full-year numbers:

Aside from the link to the IFRS 17 report and the guided HEPS growth range, the announcement is pretty light on financial details. There’s some commentary about consumers under pressure and credit granting criteria being tightened in response. Both transaction fee income and funeral insurance performed well according to the company.

Full details are expected to be released on 28 September.

Caxton is trading at roughly half of its NAV (JSE: CAT)

And the annual growth in the NAV doesn’t look too bad either

Caxton & CTP Publishers and Printers (or Caxton for our collective sanity) published record results for the year ended June 2023. HEPS grew by 20.2%, although I’m not sure that’s the ideal metric when assessing the valuation here.

The core business comes through on the income statement, with revenue up by 16.6% thanks to pricing and volume increases in the packaging business. The split is 49% publishing and printing, 51% packaging and stationery. The second half of the year wasn’t quite as exciting as the first half as demand softened and margins came under pressure and competition intensified. The packaging business is definitely the major growth driver at the moment.

Caxton is sitting on expensive stock and this will impact margins as it works through the system, although there’s already been a write-down on some stock items in this period.

Staff costs grew by 6.9% and other operating expenses grew 7.7%. That’s well below revenue growth.

Notably, operating profit of R810.8 million includes a net R84.6 million related to the insurance claim related to the KZN floods. Another important once-off is the R78.9 million profit on disposal of Cognition Holdings.

Cash is always king, with cash from operating activities of R523.2 million, which is a 21.7% increase over the prior year. In terms of capital allocation, the group made acquisitions of R144.6 million, of which the Amcor bag-in-box bladder business was the largest at R102 million. A dividend of R197.1 million was paid during the year and share repurchases were R25 million.

The outlook for the upcoming year isn’t as rosy as one might hope, as Caxton’s media publishing and printing business is highly exposed to local retailers. Certain parts of the packaging business are similarly exposed, although they also have exposure to more defensive sectors like alcohol, quick-service restaurants and cigarettes.

The reason why HEPS probably isn’t the best valuation metric here is because of assets of R9.2 billion, a whopping R1.4 billion is attributable to investments. Within that, R1.37 billion is in listed shares, which is mainly the investment in Mpact. The Mpact share price was down at R25.5 at the end of June, now up to over R30. The right place to see this benefit is the NAV per share rather than in HEPS.

Here’s an interesting media-related snippet that I thought was worth including here:

As another interesting strategic tidbit, the acquisition of Maskew Miller Learning by Novus Holdings (a competitor to Caxton) means that those textbook volumes have been lost. This was Caxton’s biggest textbook customer and the lost of volumes will mainly be felt in the new financial year.

What makes this especially interesting is that the metrics have been added to existing debt

Although banks and lenders will try hard to turn everything into a marketing opportunity about how altruistic they are, the reality is that most ESG-related decisions are a direct result of financial and regulatory pressures. In an effort to improve ESG scores, lenders look for opportunities to lend against sustainability-linked metrics that encourage the borrower to “do the right thing” in exchange for a better funding rate.

I always find it interesting when “the right thing” should be a core part of the business anyway. Curro is a perfect example, with one of the metrics being targets linked to bachelor’s degree pass rates. You would think that this is a key metric for Curro regardless, but if they can get lenders to reward them for it, then why not? Other metrics include employee diversity and water usage.

The thing I found most interesting about this news is that the metrics are an overlay to existing debt facilities with Standard Bank, FirstRand, Sanlam Specialised Finance, Investec and Absa. Standard Bank acted as the Sustainability Coordinator and PSG Capital as the Transaction Advisor, getting all these lenders across the line.

The debt value is R3.3 billion, so shaving some of the funding costs off this principal amount will be helpful. The announcement doesn’t indicate exactly what the targets are or what the potential saving might be.

Hammerson partially extended its debt maturities (JSE: HMN)

At this point in the cycle, that comes at a price

Hammerson recently announced a £100 million bond tap issuance, which means new debt raised under an existing bond programme. These are 7.25% coupon bonds maturing in 2028. The coupon drives the pricing of the yield, which is the actual cost of the debt to Hammerson. They were priced at a yield of 9.1%, which means they were issued at a discount to face value because a 7.25% return isn’t sufficient in this environment.

In a distinct but related transaction, Hammerson announced a tender offer for its £350 million 3.5% coupon bonds maturing in 2025 and its £300 million 6.0% coupon bonds maturing in 2026. If you look at the various transactions here, Hammerson effectively raised £100 million due in 2028 and used it to repay some of the short-dated debt through the holders of that debt “tendering” their debt back to Hammerson.

Hammerson accepted tenders for £11.7 million of the 2025 bonds and £88.4 million of the 2026 bonds at repurchase yields of 7.7% and 8.1% respectively. Remember, they issued debt at 9.1% to achieve this. The cost of shifting £100 million worth of maturities from 2025 and 2026 to 2028 is an annualised net interest cost of £3 million per year.

This debt cycle isn’t friendly to property companies, especially in the UK where rate hikes have been severe.

Little Bites:

Director dealings:

The spouse of a director of a major subsidiary of Northam Platinum (JSE: NPH) has executed a big sale of sales, coming in at R19.4 million.

In case you’re wondering whether it pays to be CEO of a listed company, the answer is that yes it does. This isn’t quite the standard director dealing as it relates directly to a vested share scheme, but it’s still worth highlighting that Truworths (JSE: TRU) CEO Michael Mark has sold shares worth R19.4 million. It’s interesting to note that the shares were awarded in 2009 and only vested in 2023.

The disposal of the Vyeboom Fruit Farm by Crookes Brothers Limited (JSE: CKS) was approved by shareholders at the general meeting with a 92.63% approval rate.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In the 24th edition of Unlock the Stock, we welcomed Curro Holdings for the first time to talk to investors about the recent performance and the way forward.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

I promise that this isn’t designed to depress you. It is, however, designed to make you think. Sometimes, we have to think about things that are sub-ideal.

There was a time in this world when a single income household with 2.4 children could enjoy a perfectly adequate middle-class lifestyle. The kids were in decent schools and if they showed real academic ability, further studies were possible. There was enough money for a family holiday now and then. You get the idea.

Today, there are many dual-income households with crazy working hours, a threat to “rather chop it off” than have a third child and so much stress that mental health has been thrust to the forefront of our existence.

What the hell happened?

Whatever the reasons, people are getting tired of making more people

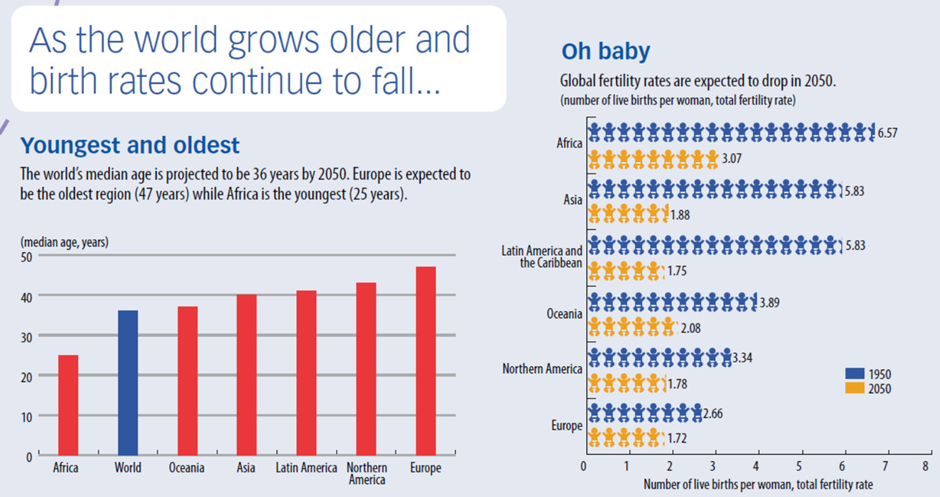

The United Nations reckons that on 15 November 2022, the world population reached 8 billion people. No, I’m not sure how they can be so precise, but anyway. It took 12 years to get from 7 billion to 8 billion. That same organisation reckons it will take 15 years to get from 8 billion to 9 billion, which means the rate of population growth is slowing significantly.

I wonder why that might be the case? Could it have anything to do with the ridiculous costs of having children and struggling to enjoy a similar standard of living to those a few generations earlier? I found this fascinating chart on the IMF website:

There’s obviously a really great humanitarian story underneath all of this, which is that mortality rates have plummeted as we’ve gotten far more advanced at keeping babies alive in even difficult circumstances. That’s a very good thing and it means that mothers don’t need to have more kids than they actually want, just to make allowance for terrible things that can happen. I just don’t think it fully explains the drop in birth rates and what people go through to have kids these days.

How did we get to this stage?

In 1950, the same IMF article that had the above chart tells me that the world had 2.5 billion people. From everything I’ve read and been told by older family members with a naughty look in their eyes, the sixties was a time of boosting the global population, usually at rock concerts. Either way, there are now more than three times the number of people on the planet and that’s in the space of seven decades, which means many people have seen that increase in their lifetimes.

It’s not like we have more space all of a sudden, so this explains why real estate costs have become ridiculous and very few people can have the typical suburban home that their parents enjoyed. Climate change is at the forefront of many conversations, perhaps because the same planet is now trying to support far more humans than ever before.

Despite Elon Musk’s opinion on the matter and certainly his practical approach to solving it, there are probably just too many humans.

What does this have to do with retirement, or lack thereof?

Assuming you went to university and that you plan to retire at 65, you’ve basically got 40 years to earn enough money to fully sustain yourself for 20 years (or more) after retirement.

Welcome to adulting.

During those 40 years, you’re probably going to have kids. That’s going to do things to your expenses that you never believed possible. Statistics aren’t really on your side in terms of divorce rates either, so that’s another potential financial nightmare. This is before we’ve even considered healthcare challenges, or the desperate need to manage your mental health through lifestyle upgrades and experiences, or your cat ripping up your brand-new rug.

You’re in a fight over a finite set of resources on the planet, with an increasing number of humans who need them.

40 years, you say? To make enough money for the next 20 or more? That’s a big ask, especially when it seems like humanity is hell-bent on using Artificial Intelligence to drive even more people into unemployment.

It’s all in the maths

To make this equation work, the retirement industry and many personal finance influencers focus on getting you to drink less coffee, thereby saving more of your income (before fees of course) in your early years and ensuring that you have a bang average 85 years on this world. This is because you’ll have very little spare money in the best years of your life, all so that you can afford Wimpy every Wednesday when you’re too old to remember what proper food tastes like anyway.

If we all knew precisely when we would die, it would be a lot easier to just work out exactly how much money we need and spend all the rest before our kids do. This is unfortunately not possible, even for the most dedicated Diamond members on Vitality.

I believe there’s another way, but you’ll have to buckle up and get ready for a wild ride to get it right.

Retirement is for salaried employees, not entrepreneurs

The biggest problem with the concept of retirement is that it assumes that at the age of 60 or perhaps 65, you suddenly become a useless amoeba who can’t add value to anything or anyone beyond falling asleep at the appropriate time after family lunches. This simply isn’t true.

If you can extend your ability to earn an income, then the maths starts to look very different indeed. Instead of hoping to live off passive income, you’re supplementing it with an active income. If you really get it right, then you’ll be living off the active income entirely for quite some time past the age of 60.

How do you do this? Well, a corporate is going to force you to retire at some point, so you then have to hope that you have a skillset that lends itself to some kind of consulting role. That’s really not easy to get right. I have some bad news for you on how useful many corporate skills are in the world outside of air-conditioned offices with full solar power backup.

When I made the decision to leap from corporate life into the very uncertain world of entrepreneurship, one of the things I imagined is how great it would be one day to perhaps have a business that can earn an income without me being involved all the time. That’s a semi-retirement that literally delivers the best of all worlds, with ongoing income and perhaps most importantly, a sense of purpose and something to keep my brain alive into hopefully much older years.

The lesson here? Learn continuously, keep your skillset relevant and be alert to opportunities to build income away from your salary. Perhaps most importantly, make sure your career is built around something you genuinely enjoy and can see yourself doing for many years. I can tell you for sure that these things are a lot more fun than cutting your coffee intake.

If all else fails, perhaps I’ll just run for president somewhere. Isn’t that what all the octogenarians are doing these days to stay active?

The excitement is building for the 2023 Rugby World Cup (RWC). Kickoff is 8 September in France and, as reigning champions, our nation’s hopes rest on the shoulders of the Springbok squad of 33 for another win. With strategies, tactics and game plans in the news, now is a good time to take a lead from rugby coaching staff in your investment journey.

Siyabulela Nomoyi, Satrix’s* quantitative portfolio manager, says, “We know that winning a rugby world cup relies on a number of factors coming together – the right coaches, right plan, right team, right mindset etc. And growing wealth actually has quite a few similarities.”

He said that investing through exchange-traded funds (ETFs) is an excellent way to start an investment journey. They are low cost, very accessible and easy to manage.

Nomoyi says some of the winning aspects of a good RWC campaign could be applied in the world of investing. Here are some rugby roles that you can take on in your own winning strategy:

The Head Coach: Strategy Is Everything Remember how the Springboks executed “The Move” in the 2019 Rugby World Cup final? That strategy took them to victory. Just as rugby teams dissect their opponents and forge plans to increase chances of a win, your investments need a clear game plan. To successfully build wealth through investing, you should look at crafting a roadmap that aligns with your long-term goals and risk appetite, much like the Springboks’ tactical masterpiece. This can be done in conjunction with a financial adviser or by doing careful research and using the wealth of online information to help you build the right plan.

The Selector: Diversity Is Key Look at the Springbok squad for the 2023 World Cup – a medley of players who all bring something special to the squad. The fast, the strong, the accurate, the leader. Similarly, diversification in investing is a key play. By spreading your investments across various sectors and asset classes, such as local and global equities, bonds and cash, you create a cushion against market fluctuations. This approach reduces the impact of a single loss and could amp up your overall portfolio performance.

The Tactician: The Right Tools Should Be In Place The Springboks have constantly come up with new configurations for their bench to keep the on-field momentum going. Last World Cup they ditched the traditional five-three split between forwards and backs for six-two. Now they have been experimenting with seven-one. Just like these tactics keep the Springboks forward momentum consistent, low-cost index funds do the same for your investments. They trim down fees that could otherwise eat into your returns over time, keeping your investment’s efficacy intact.

The Whole 15: Balancing Risk and Safety Ever notice how the Springboks choose the right moments to take risks on the rugby field? Your investment journey will thrive on the same balance. Like a rugby team balancing defensive plays and daring attacks, a well-rounded investment portfolio combines both high- and low-risk investments. Index funds, like dependable teammates, replicate established market trends, offering you a sturdy strategy.

The Captain: Weathering Market Storms The Springboks’ resilience after their tough loss in their first game of the 2019 tournament – a tough lesson but they bounced back and won. Similarly, when investment markets are turbulent, maintaining your strategy matters. Resisting the urge to make impulsive changes during market downturns will make sure you don’t lock in any losses and you will still be in the market when it starts to perform better again. Staying the course can lead to long-term gains, just like the Springboks’ triumphant comeback.

The Analyst: Learning From Wins and Losses In rugby, every game, whether it ends in cheers or tears, holds a nugget of wisdom. It’s the same with investments. Each outcome, good or bad, can teach you valuable lessons. So, as you tune into the Rugby World Cup, consider how the strategies employed by different teams could guide your investment journey.

As Nomoyi points out, “Much like a well-executed rugby game plan, investing strategically can lead to substantial victories in the financial arena.” So, embrace these rugby-infused tactics and watch as your investment game transforms into a winning streak.

*Satrix, a division of Sanlam Investment Management

Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. Satrix Managers is a registered Manager in terms of the Collective Investment Schemes Control Act, 2002.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Bell Equipment rings even louder (JSE: BEL)

An updated trading statement confirms an even bigger jump in earnings

Trading statements are funny things. They can be very conservative at times, especially when the language is an increase of “at least” and then a round number, like 20% of 30%. A much tighter trading statement would give a range, removing the chance of a major upside surprise after that.

In the initial trading statement for the six months to June, Bell indicated an increase in HEPS of at least 30%. The updated trading statement is far more exciting than that, with HEPS up by between 61% and 67%.

This implies a range of between 338 cents and 348 cents a share. As I keep saying, this year has been all about industrial companies rather than the retailers, an important lesson about inflationary conditions and the kinds of companies that do well during such a period.

A mandatory offer for Brikor is imminent (JSE: BIK)

Nikkel Trading is on the verge of breaching the 35% ownership threshold

Nikkel Trading currently has a 34.23% stake in Brikor. Nikkel has advised Brikor that it is in the process of acquiring more shares in the company, which will take it above the 35% ownership threshold. This triggers a mandatory offer to remaining shareholders.

The price for the acquisition is expected to be 17 cents a share, so this suggests that the mandatory offer would also be at this level. The share price jumped to 16 cents a share in response.

In a separate announcement, the company noted that the circular regarding the contract mining and coal purchase agreement should be sent out by 30 September.

British American Tobacco exits Russia and Belarus (JSE: BTI)

The price hasn’t been disclosed

Back in March 2022 when all hell literally broke loose in Ukraine, British American Tobacco announced that its ownership of assets in Russia and Belarus wasn’t sustainable. That’s right kids, a tobacco company with a conscience. Perhaps more importantly, international laws were to blame for this decision.

The buyer of the Russian and Belarusian businesses is a consortium led by the management team in Russia. The businesses will thereafter be known as the ITMS Group. Employees in the business will apparently enjoy their current employment terms for at least two years after completion of the deal.

British American Tobacco hasn’t disclosed the selling price for the businesses. This isn’t exactly an immaterial region, accounting for 2.7% of group revenue and 2.5% of group operating profit in the last financial year. The only other financial information we have is that the company remains confident of delivering the full year guidance that was given during the interim reporting cycle back in July.

Delta Property continues to fight for survival (JSE: DLT)

When debt was on a month-to-month basis, you know it was bad

Right at the top of the list of highlights for Delta Property Fund for the six months ended August, we find the news that month-to-month debt facilities with Nedbank and Investec were refinanced for 12 months and 24 months respectively. That surely takes a bit of the edge off at Delta, with the company working hard to steady the ship. The facilities come to R3.1 billion in total.

Other good news includes the conclusion of a revolving credit facility of R37.5 million with Nedbank and a 50 basis points reduction in the cost of debt with that bank.

The improved debt outlook wasn’t just driven by good rental collections. Delta has signed agreements to sell 5 assets in the next six months for a total of R123.8 million, with agreements in place to sell another R1.5 billion worth of properties within the next year.

There are two major problems that Delta is trying to navigate. The first goes to the very core of the business, which is that the portfolio is primarily B-grade office space with government as the tenant. Negotiating with our government really isn’t fun and they historically aren’t great payers, although that seems to have improved greatly in this interim period. The other problem is the environment of high interest rates, which puts the balance sheet on a knife-edge even after these improvements.

There are various other initiatives underway to try and unlock capital to repay debt. When results for this interim period are released, investors and punters alike will be fully focused on what the debt ratios look like.

Merafe deepens the JV relationship with Glencore (JSE: MRF | JSE: GLN)

Another PGM production plant will be included in the joint venture

Back in 2022, Merafe and Glencore agreed that a new PGM production plant at the Kroondal Mine would be contributed to the joint venture between the parties. This has proven to be a profitable decision and the parties are now looking to replicate that success with another production plant.

This time, it will be located at the Thorncliffe Mine, based on the eastern chrome mine operations. This project comes with a capital expenditure bill attributable to Merafe of R117 million.

This deal is so small in Glencore’s world that the company didn’t bother to announce it.

Sanlam: focus on the cash earnings, not HEPS (JSE: SLM)

IFRS complexities are doing what they do best: making financials harder to understand

IFRS 17 Insurance Contracts has become effective. It seems to be as useful to investors as the new leases standard was when that became effective. The latter caused havoc for retailers in particular, with the former obviously impacting insurers like Sanlam.

With headlines everywhere crowing about HEPS growth of 118% for Sanlam in the six months to June 2023, I’m just not sure that this is the metric to be focusing on. By Sanlam’s own admission in its results, the focus is actually on Return on Group Equity Value (RoGEV) and dividend growth.

This is incredibly complicated stuff and I certainly don’t claim to be an insurance expert (far from it). What I do know is that HEPS growth of 118% suggests an absolute blowout result, yet adjusted RoGEV (Sanlam’s favourite measure from what I can see) is 7.9% vs. the hurdle rate of 7.5%. That’s a good result for sure, but perhaps not extraordinary. Here’s what the calculation looks like:

As another useful metric, cash net results from financial services increased by 30%. Yes, it’s more complicated than that, but there’s a helluva big gap between the cash earnings growth of 30% and HEPS growth of 118%.

Transaction Capital buys itself some time on the WeBuyCars deal (JSE: TCP)

The put-call structure has been extended

Before the Transaction Capital share price blew up in a puff of oil smoke out of the back of a poorly maintained taxi, the deal with WeBuyCars had been executed in textbook fashion. Transaction Capital had built a strong relationship with the founders and they did a staggered transaction that allowed the founders to share knowledge while sticking around for the ride.

The huge problems at SA Taxi take nothing away from the quality of the WeBuyCars deal. There are always those in the market who are skeptical, but as a devout petrolhead I can tell you that WeBuyCars changed the game in this industry and put a real liquidity floor in place for consumers. Suddenly, a car could always be sold. That wasn’t the case previously, allowing dealers to make ridiculous lowball offers to desperate sellers.

The SA Taxi and share price issues have impacted Transaction Capital’s deal strategy, with various put-call options in place and the potential to settle 30% of the purchase price through the issuance of Transaction Capital shares. That was a whole lot more appealing to the company when the share price wasn’t in the toilet.

Under a revised structure, the good news is that Transaction Capital retains the ability to settle the remaining options based on 70% cash, 30% equity, or 100% cash if that is more appropriate at the time. The period of time for the structure has been extended, with various tranches between November 2023 and March 2029. The end result is that Transaction Capital can still end up owning just about 100% of WeBuyCars if all the options are exercised. There is no change to the price/earnings multiple range of 9.5x to 10.5x. used in the calculations for the put and call options.

There is one other significant change, which is that the metrics in the options will be calculated based on two-year averages. This includes volume-weighted average share price and the underlying earnings for the calculation.

Most of all, this outcome shows that Transaction Capital still has a good relationship with the WeBuyCars founders. Doing good deals can help you when you need it most.

Trellidor: just how much higher will earnings be? (JSE: TRL)

Here’s the classic “at least 20%” trading statement in action

Trellidor is finalising its earnings for the year ended June 2023. The comparative period (i.e. the 2022 financial year) was a revolting time for the company, with HEPS of just 0.4 cents. For context, 2021 saw HEPS of 40.8 cents and 2020 was 13.8 cents.

This context is so important, as it means that the latest trading statement with bland guidance that earnings will be “at least 20% higher” is just a tick-box exercise for the JSE Listings Requirements. The earnings should be multiple times higher than in 2022, nevermind just 20%.

The stock isn’t very liquid and is currently at R2.20, which also tells you that 2022 was just a freak year that must never be repeated. The question is just how significant the recovery in 2023 can be.

Little Bites:

Director dealings:

Des de Beer is at it again, buying another R1.86 million worth of shares in Lighthouse Properties (JSE: LTE).

An associate of a director of Nedbank (JSE: NED) has bought shares worth R380k.

The CEO of Sirius Real Estate (JSE: SRE) bought shares worth around R170k.

For a laugh, Moody’s has upgraded the credit outlook for Eskom from stable to positive. Now, before you get ready to hit your screen against the wall, this is purely a credit analysis and most importantly, the outlook is based on the current rating, which is so deep in junk that you can barely see it at the bottom of the dustbin. Basically, Eskom is right near the bottom of the dustbin and isn’t expected to fall between the cracks anymore, thanks to taxpayers (you and me) footing the bill via government.

And in other news from the public sector cess pool, the CFO of Sanral (Inge Mulder) is now on a temporary leave of absence pending internal processes. I suspect that this story is only just warming up.

British American Tobacco plc has announced the disposal of its Russian and Belarusian businesses to a consortium led by members of the Russian management team for an undisclosed sum. The company announced in March 2022 that the ownership of these businesses was no longer sustainable in the current environment. Post completion, the businesses will be known as the ITMS Group.

The sale of assets held by Rebosis, currently under business rescue, continues with the announced sale of a portfolio of 10 properties to Hemipac Investments for R650 million.

Oando plc has reached an agreement with Eni to acquire 100% of the shares in Nigerian Agip Oil Company. The transaction increases Oando’s current participating interests in OMLs 60 to 63 from 20% to 40%.

In March this year Brikor advised shareholders that Nikkel Trading 392 intended to acquire from major shareholders a 67.7% stake in Brikor in two tranches at 17 cents per share. The first tranche, representing a 34.1% stake, was acquired at the time of the announcement. The second tranche (33.6% stake) was conditional on several suspensive conditions, including regulatory approval from the Competition Authorities, the JSE and the TRP. Brikor has now advised that it will acquire the second tranche which will trigger a mandatory offer to minorities.

Unlisted Companies

Cipla Medpro South Africa is to acquire Actor Pharma in a deal valued at R900 million, according to a filing by its Indian holding company. The deal is a strategic move by the South African subsidiary to strengthen its position in the over-the-counter segment of the market, unlock future growth opportunities and leverage cost synergies in the SA market.

Real estate private equity platform Kasada, has acquired the former Radisson Blu Hotel & Residence situated in the Cape Town city center for an undisclosed sum. Kasada has a presence in eight African countries with a portfolio of 19 hotels.

Lighthouse Properties plc has issued 51,913,215 new Lighthouse shares in terms of its scrip dividend election at R5.39 per share, resulting in a capitalisation of the distributable retained profits in the company of R118 million.

Santam has advised that it is in a position to distribute R2 billion of the gross proceeds received from the sale in 2022 of its 10% interest in the SAN JV to Allianz Europe BV. Shareholders will receive a special dividend from income reserves of R17.80 per share.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 28 August and 1 September 2023, a further 1,012,749 Prosus shares were repurchased for an aggregate €64,99 million and a further 250,654 Naspers shares for a total consideration of R796,4 million.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 10,550,000 shares for a total consideration of £45,28 million.

South32 continued with its programme of repurchasing shares in the open market. This week a further 832,004 shares were acquired at an aggregate cost of A$2,88 million.

Two companies issued profit warnings this week: Pan African Resources and The Foschini Group.

Five companies issued or withdrew a cautionary notice: Trematon Capital Investments, Ellies, Afristrat Investment, enX and Brikor.

Beltone Venture Capital has acquired a 20% stake in Egypt’s digital home and décor brand, ariika. The Series A investment will accelerate the brand’s expansion to Saudi Arabia.

BIO and EDFI AgriFI are co-investing €6 million in gebana Faso to enhance integrated and sustainable food supply chains in the region. gebana Faso is a subsidiary of the gebana Group and specialises in processing and exporting Fair Trade and Organic cashew nuts and dried mangoes from Burkina Faso.

PZ Cussons Nigeria has announced that PZ Cussons Holdings wants to buy out the other existing shareholders at ₦21 per share via a Scheme of Arrangement. The deal is subject to board, shareholder and regulatory approval. PZ Cussons has been present in Nigeria since 1899 and the move is aimed at strengthening and simplifying the Nigerian operations.

Btrust has acquired Nigeria’s Qala, which has been rebranded as Btrust Builders Programme.

Galileo Resources has entered into a joint venture agreement with Cooperlemon Consultancy in respect of the exploration for copper at large scale exploration license 28001-HQ-LEL situated in Northwest Zambia. A series of earn-in and exploration expenditure will see Galileo take a 65% stake in the joint venture.

Global Investments Holding Ltd has acquired a 30% stake in Eastern Company, a tobacco producer in Egypt. The sale will reduce the Holding Company for Chemical Industries’ stake from 50.9% to 20.9% and is part of the Egyptian government’s ongoing programme of privatising state-owned assets. The deal was valued at US$625 million.

Uganda’s Asaak has entered the Latin American market through the acquisition of FlexClub Mexico. The fintech did not disclose the value of the deal.

Nigeria’s Itana has raised US$2 million to push forward its plans to establish a digital free zone. The funding was provided by LocalGlobe, Amplo, Pronomos Capital and Future Africa.

AfricInvest has invested US$40 million in The British University in Egypt. This is one of the largest foreign direct investments in the education sector in the North African country. The funds will go towards the university’s expansion and transformation plans.

Renew Capital Angels has invested an undisclosed amount in Kenyan fintech FlexPay.

Kenyan crypto payments startup, Kotani Pay has closed a US$2 million pre-seed round led by P1 Ventures. Other investors include DCG/Luno and Flori Ventures.

Lagos-based fintech, Anchor, has secured US$2,4 million in a seed round led by Goat Capital. Other investors include FoundersX, Rebel Fund, Pioneer Fund, Y Combinator, Byld Ventures and Future Africa. Since launching in August 2022, the embedded finance fintech has processed more than $550 million in annualised total transaction volumes and achieved a 30% month-on-month growth in revenue.

Sehatech, an Egyptian health insurtech, has raised US$850,000 from A15 and Beltone Venture Capital. The funds will be used to grow the staff contingent and to invest in product development.

Moroccan edtech Smartprof has raised an undisclosed amount of funding from Digital Africa’s Fuze. Part of the funding will be used to help the company accelerate its expansion into West Africa.

To strengthen its ESG agenda, Safaricom, has announced a new multi-billion Sustainability Linked Loan with four banks – Standard Chartered Bank, Stanbic Bank, ABSA Bank and KCB. This is the largest ESG linked loan facility in East Africa and the first Kenya Shilling denominated sustainability linked loan in the market. The loan is valued at KES15 billion, which can be increased to KES20 billion by accordion.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")