Richemont has proposed a special dividend of CHF1.00 per ‘A’ share/10 ‘B’ shares. The dividend will be payable following the AGM scheduled to take place on September 6, 2023. In addition, the company has announced a new programme to buy back up to 10 million ‘A’ shares representing 1.7% of the issued share capital of the company. The shares will be held in treasury together with the 4 million ‘A’ shares currently held in treasury to hedge awards to executives and employees.

Mediclinic International’s shares will be suspended on JSE and NSX on May 25, 2023, following the company’s acquisition announced in August 2022. Manta Bidco, a joint venture owned by Remgro and MSC Mediterranean Shipping, acquired the remaining 55,44% stake in the company from minorities in a £2,05 billion transaction.

Purple Group has advised it intends to raise a maximum of R105 million from shareholders by way of a renounceable rights offer. A total of 129,629,630 will be offered at a subscription price of R0.81 per Rights Offer share. Shareholders holding shares equating to 27.12% have committed to follow their rights in terms of the offer and Sanlam Investment Holdings has agreed to underwrite the Offer. The funds will be used to fund the expansion needs of 70%-held Easy Equities which will be raising R150 million for its needs. The remaining R45 million will be funded by Easy Equities’ shareholders Sanlam which holds the remaining 30% stake.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Gemfields has repurchased 1,729,550 shares at a price of R3.45 per share which will be held as treasury shares. Following the repurchase, the total number of ordinary shares in issue is 1,218,586,612.

Calgro M3 has repurchased a further 5,198,000 shares for R14,78 million representing 3.71% of the issued ordinary share capital of the company. A further 18,89 million shares (7.03%) may be repurchased in terms of the General Authority granted.

Nedbank has cumulatively repurchased 15,784,216 shares representing 3.1% of the companies issued share capital. 9,595,526 shares have been delisted and cancelled with effect from Monday 8 May, 2023 while application has been made to the JSE for the delisting and cancelation of a further 4,178,925 shares.

Lewis has repurchased 1,765,939 shares, representing 3% of the company’s issued share capital. The shares were repurchased at an aggregate cost of R83,4 million between October 31, 2022 and May 11, 2023.

South32 has increased its share repurchase programme by c. $50 million in anticipation of a stronger outlook for commodity prices in the second half of its financial year. This will enable the company to return $158 million to shareholders before September 2023. This week the company repurchased a further 1,867,780 shares at an aggregate cost of A$7,55 million.

Glencore this week repurchased 14,700,000 shares for a total consideration of £63,87 million. The share repurchases form part of the second phase of the company’s existing buy-back programme.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 8 to 12 May 2023, a further 2,735,903 Prosus shares were repurchased for an aggregate €177,97 million and a further 573,864 Naspers shares for a total consideration of R1,81 billion.

Five companies issued profit warnings this week: KAP, Stefanutti Stocks, Dipula Income Fund, Telkom SA SOC and Coronation Fund Managers.

Five companies issued or withdrew a cautionary notice: Premier Fishing and Brands, Attacq, African Equity Empowerment Investments, Pembury Lifestyle and Chrometco.

Zydii, a Kenya-based digital training solutions provider, has received pre-seed funding from DOB Equity, Kua Ventures, Kaleo Ventures and NaiBAN. The funds will support the company’s growth plans by expanding its suite of solutions for upskilling the African workforce.

Morocco-based B2B e-commerce platform for fast moving consumer goods Chari, has secured a second round of investment from Plug and Play to help it scale its business. The investment amount was undisclosed.

M-KOPA, an asset financing platform providing access to life improving productive assets such as smartphones, solar home systems and electric motorbikes to underbanked individuals, who are able to pay for them via digital micropayments, has secured new funding. The capital injection includes US$55 million in equity and over $200 million in debt. The funding – purported to be one of the largest combined debt and equity raises in African tech, will enable M-KOPA to double the size of its customer base in existing markets, extend its financial services offerings and product sets.

Figorr, a Nigerian-based technology company that develops Internet of Things-powered solutions to support the last-mile delivery of perishable goods, has secured US$1,5 million in seed funding. The round was led by Atlantic Ventures with participation from Vested World, Jaza Rift and Katapult. The company provides real-time tracking, cold chain advisory services and data to stakeholders in various sectors such as pharmaceutical manufacturers and agricultural companies. The funds will be used for the roll out of a risk management platform that will provide data that will make it easier to insure perishable and temperature sensitive goods on the continent.

After a relatively strong year in 2021, mergers and acquisitions (M&A) activity dropped off in 2022, both in South Africa (SA) and around the world.

While we expect activity to remain muted in the near term, we expect a pickup towards the end of this calendar year as key drivers of activity fall into place.

Overall, the SA investment case outlook is beset with challenges: power outages, political uncertainty, and an increasing cost of living pressure for consumers. Against this backdrop, SA will struggle to deliver meaningful levels of growth, particularly as traditional European trading partners navigate recession and geo-political upheaval.

However, where investor uncertainty and operational challenges for management teams will continue to curtail M&A activity, we expect acquirers, or buyers, to take advantage of opportunities created by such turbulence.

As seen in recent years, multinationals tend to take a long-term view on South Africa and the sub-Saharan African region and, we believe, will continue to make material acquisitions in select sectors, acquiring quality earnings and operations at relatively attractive valuations.

Investors are recognising inching progress on structural reforms in the economy, supporting their longer-term investment decisions. Examples include Heineken’s acquisition of Distell, which recently received final regulatory clearance; Remgro and MSC’s acquisition of Mediclinic, which also just received approval from the Competition Tribunal, subject to various commitments; and the acquisition of EnviroServ by a SUEZ-led consortium.

This year should see a slightly more positive equity capital markets environment and increased equity issuance, which is supportive for M&A activity. EOH’s rights offer and the successful listing of Premier Foods in March 2023 is indicative of more positive sentiment in this regard.

In terms of private capital availability for M&A, financial sponsors and family offices continue to have large amounts of capital available for deployment. Globally, financial sponsor “dry powder” is almost three times what it was in 2015. Inevitably, this will translate into increased levels of M&A activity in SA and across Africa.

We see several trends driving M&A:

• Public to private deals – conditions remain strong for the trend of de-listings from the JSE to continue (down to 288 at the end of 2022, from 312 in 2019). We see this being driven by opportunistic buyers taking advantage of low trading multiples on the JSE, or existing shareholders taking the businesses out of the public domain with a view to making structural changes to unlock value over time.

• Consolidation – we will continue to see consolidation as a key driver of M&A. In periods of economic downturn and pressure on margins, large sector players take the opportunity to acquire market share from smaller, less resilient ones, or expand into adjacent sectors. Large corporates, which are also well-capitalised relative to pre-COVID-19 times, have recently refined their capital allocation strategies. They are now clearer on their “core” focus areas for investment and primed to execute on growth opportunities.

• M&A activity variation by sector:

We expect to see low levels of activity in consumer-facing sectors continuing through this year as management teams manage the price/volume balance to maintain margins. However, we believe that the major consumer groups in SA will spend time assessing options to unlock value for shareholders, which will support activity into 2024. RCL FOODS’ announced disposal of Vector Logistics in March 2023, as part of its broader managed separation process, is an example of a major consumer group delivering on an announced value creation strategy.

Other sectors, such as financial services, will continue to be active. Sanlam’s acquisition of the remaining 62% stake in BrightRock Insurance and acquisition of control of AfroCentric are recent examples of large players consolidating market share and leveraging their platforms. Sanlam and Allianz have also agreed to combine their current and future operations across Africa (ex-SA) to create the largest pan-African non-banking financial services entity on the continent.

In the resources sector, healthy balance sheet positions, enabled by attractive commodity prices paired with corporate diversification strategies, should be supportive of M&A-led growth opportunities. Thungela’s announcement in February 2023 of its acquisition of Ensham coal mine in Australia is an example of SA mining players with healthy balance sheet positions acquiring assets that offer geographical diversification opportunities.

ESG commitments and South Africa’s energy challenges are driving M&A activities in the energy sector, demonstrated by significant levels of investment into renewable and independent power generation opportunities. Seriti’s establishment of Seriti Green and its acquisition of 100% of Windlab Africa in December 2022, as well as Anglo American’s partnership with EDF Renewables – to form Envusa Energy – are just two examples of the high levels of long-term capital being allocated to the sector.

Healthcare in South Africa is seeing increased levels of deal-making as mid-tier healthcare players continue to emerge across the sector and raise capital for growth. IFC’s pending investment into Lenmed is a good example. Meanwhile, the larger players are driving their diversification strategies (Life Healthcare’s recent announced acquisitions of East Coast Radiology in February 2022 and TheraMed Nuclear in March 2023).

In the technology, media and telecommunications (TMT) sector, we see potential consolidation opportunities in South Africa, and fintech acquisition opportunities in the rest of Africa.

Investors will continue to take a cautious approach to M&A in Africa, and buyers will continue to look carefully at M&A options, requiring potential targets to have a proven track record of capturing consumer growth. Gaining a level of comfort in the regulatory and FX environment are also key criteria before investing. Outside of South Africa, Egypt, Nigeria and Kenya are attracting strong investor interest, and we see activity levels gradually increasing, with potential for a major jump in activity from the latter part of the year and into 2024.

Matthew Eb is a Senior Transactor and Itumeleng Molefe a Transactor for Corporate Finance | RMB.

This article first appeared in DealMakers, SA’s quarterly M&A publication

The team at Trive South Africa gets us closer to the energy companies that are moving markets – of both the fossil and renewable variety!

Local has not been that lekker when it comes to sources of energy, but whether you are on the fossil front or part of the go-green brigade, there is no denying that energy demand has been booming across the globe.

Big on Oil

After the resurgence of Crude Oil in 2022, it is no wonder that most investors have placed renewables on the back burner for now, despite central authorities’ best efforts to drive renewables. Even the world’s most famous investor, Warren Buffett, has been placing big bets on oil, with energy making up around 14% of his portfolio. The Oracle of Omaha stated that the world would depend on fossil fuels for years, which is quite interesting, as oil prices have fallen substantially from their 2022 highs.

Despite lower oil prices in 2023, the transition away from fossil fuels is anticipated to take longer than expected, as most companies needed to be more ambitious when setting goals to reduce their carbon emissions. Adverse weather conditions will also force more countries to rely more on fossil fuels in 2023, delaying the energy transition, per an EIU whitepaper.

Sasol Limited (JSE: SOL)

Locally, the diversified energy and chemicals company Sasol Limited has not only felt the brunt of the volatility in the oil market, but its greenhouse emissions are under scrutiny as well. The use of fossil fuels still seems high in the pecking order, despite Sasol’s plans to “Be Green” by 2050.

Recent lower oil prices could be a short-term positive for Sasol, as it determines the value of the energy company’s products. However, curbing emissions will need some heavy lifting from the company. Some have already called its net zero plans unrealistic, and the financial services group Old Mutual, a 3% stakeholder in Sasol, has also raised concerns.

The latest products and sales metrics for the nine months ended 31 March 2023 indicated higher production volumes at Secunda for Q3 FY23 than the previous quarter. Operational challenges at the Natref refinery negatively impacted run rates in Q3 FY23, while the Chemicals business showed overall demand and supply still below historical levels. The energy group expects that there will be more volatility across pricing and demand for the rest of 2023.

The chart below shows a double bottom formation, but the price action needs to close above R240.00 (black dotted) and then R255.81, a resistance level (solid redline). The price action could potentially see lower levels if the Crude Oil market sees oil prices move lower in the future.

Chevron Corporation (NYSE: CVX)

Chevron, the US multinational energy corporation, has been a favourite amongst billionaire investors over the last year as fossil fuel needs have been going strong for a while. Chevron’s dominance in one of the world’s most prolific oil fields, the Permian Basin, could see interest in Chevron for years to come.

Looking at the energy and chemicals corporation’s latest Q1 report card, sales and other operating revenues were 7% lower than the prior year’s first quarter, which recorded revenues of $52.3bn. The revenue decline was primarily driven by lower commodity prices, with crude oil prices down 12.37% year-to-date and a drop in total output, down 3% from a year ago to 2.98 million barrels of oil and gas per day.

Despite Chevron’s top line slide, its bottom line gave an upbeat performance as adjusted earnings were reportedly up 5% from a year ago. Driving the optimistic bottom line was the standout performance in Chevron’s refinery business. Margins were higher for Chevron’s refined petroleum products, leading to a five-fold increase in the unit’s income to $1.8bn.

The world’s number one investor, Warren Buffett, is rarely wrong when picking winning stocks. Is his recent 20% offload of Chevron stock a concern or precursor of things to come?

Diving into the chart below, we can see the share price jumped higher from the incline trendline (lower black dotted), which could potentially see a 12% increase if market believes that the fundamental value could be as high as $180.80 a share (green line).

The Renewable Chapter

The decarbonisation drive has been taking a back seat globally after the massive run in commodities of late. Still, with soaring demand and long-term incentives, renewables are not to be ignored.

Governments and industry role players are exploiting cleantech trends to achieve a net zero effect for the future. With the influx of renewable energy demand, the growth projections were dampened by rising costs, supply chain constraints, inflation, rising interest rates, and cross-border trade, which are some of the headwinds facing the industry globally.

The rush to find alternative sources of energy locally has seen renewable energy and alternative sources of energy pushed to the forefront as the fear of a grid collapse intensifies.

Renergen Limited (JSE: REN)

The local renewable energy front-runner, Renergen Limited, has also been making headway despite the current dismay of its shareholders. The local natural gas and helium producer boasts one of the world’s largest and richest helium reserves at the Virginia Gas Project (VGP); let that sink in.

The Global Helium Market was worth $7.9 billion in 2022. According to estimates, this market is projected to grow at a compounded annual growth rate (CAGR) of 7.2% and reach $12.8 billion by 2029. Renergen recently stated that they expect to secure additional equity capital to finalise the construction of the Virginia Gas Project, hinting to current shareholders that their present stake may experience dilution in the short term. The financials showed a 1.2% year-over-year decrease in revenue for the six-month period that ended on 31 August 2022. Cash outflows used in operating activities decreased by 13.6% year-over-year, marking a slight decrease in cash used in operations. Moreover, property, plant and equipment investment increased by 114.6% year-over-year to R226 million.

Despite the reinvestment and spending outlook on Phase 2, which could deliver substantial energy to the South African economy, the company is also developing hydrogen fuel cells. This bodes well for the decarbonisation drive and increasing revenue prospects for delivery trucks and the mining sector. Looking at Renergen’s chart, we can see the share price finding support at the R17.39 level (red line), which will be watched closely for another leg lower.

Brookfield Renewable Partners LP (NYSE: BEP)

Brookfield Renewable Partners has been steadily building its renewable energy portfolio, which includes wind, solar, energy transition and hydro, for some time now. While solar power and wind farms rake in all the attention, its hydro business might be one to watch.

As the world approaches decarbonisation, Brookfield Renewable Partners’ hydro segment provides the grid with steady emissions-free energy to roughly 6 million homes. Brookfield has 222 hydroelectric facilities, which produce around 8 gigawatts of power, and these assets contribute around 49% of the company’s cash flow.

The renewable energy conglomerate’s recent first-quarter earnings beat Wall Street’s expectations which saw the share price rise. Revenues were up 17% year-over-year, beating consensus by some margin, while losses per share improved to $0.09 in Q1 from $0.16 a year before. Funds from operations per unit (FFO) became a focal point as it beat consensus and indicated robust hydro generation across the portfolio, increased realised power pricing and contributions from growth. The Hydroelectric segment, which investors should watch, increased by 26%, while the wind segment decreased by 14%.

The share price could possibly see more upside if the $31.76 share resistance is crossed, which could potentially lead to a significant overhead resistance at $32.82. For the bear case, if the $31.76 resistance is not breached, the $29.48 support becomes a focal point.

Where to next?

Global macroeconomic factors will weigh heavily on the previously surging energy market during 2023, with global energy consumption only estimated to grow by 1.3%. Despite the best efforts of OPEC+ to cut production to try and stabilise falling oil prices, global recession fears continue to weigh on oil prices. According to the EIU, renewable energy consumption will surge by about 11%, with Asia leading the way, but investment will weaken due to various macroeconomic factors.

Sources: Bloomberg, Deloitte, S&P Global Commodity Insights, WallStreet Journal, Engineering News, Economist Intelligence, International Energy Agency (IEA), Energy Information Administration (EIA), Sasol Limited, Chevron Corporation, Renergen Limited, Brookfield Renewable Partners, Matthew DiLallo, Reuters, Koyfin, TradingView.

For more from Trive South Africa and to learn about the trading and investment platform, visit the website.

Is De Beers the canary in the luxury coal mine? (JSE: AGL)

The commentary on diamond sales is a helpful read-through into luxury demand

De Beers isn’t a big enough component of Anglo American to drive the share price by itself. For that reason, updates on diamond sales are very useful in giving us a sense of luxury demand and not necessarily useful for anything else.

Even the sales numbers themselves don’t mean much, as sales cycles aren’t directly comparable in absolute terms because of seasonality etc.

I skip straight to the management commentary. The last cycle included bullish commentary from management around demand in China. The latest cycle? Not so much. The CEO of De Beers has flagged a “slower pace of recovery in consumer demand from China than was widely anticipated.”

Although I wouldn’t put diamonds in the same league as other luxury goods because of the traditional association with weddings (thankfully nobody expects a Louis Vuitton engagement present), this is something that should be noted with luxury sector companies trading at such high levels.

Dipula grows its NAV by 7% (JSE: DIB)

The per-share numbers have been impacted by a share capital restructure

In June 2022, Dipula Income Fund achieved what the artist formally known as Fortress REIT could not: a restructure of its capital to collapse a dual share class structure into a single class. Through a scheme of arrangement, A shares were repurchased and more B shares were issued. This has a significant impact on the numbers per share, as Dipula specifically reported on the A shares and B shares in the prior period and now only has B shares.

So for the six months to February, it makes more sense to look at group level numbers.

In that period, Dipula grew net property income by a humble 1% and NAV by 7%. There are some fancy balance sheet swings in NAV linked to derivatives and the infamous “other” line that all investors fear in an set of financials, so I would focus on the increase in property value of 4.9% as a better indication of year-on-year improvement.

Although tenant retention has improved across the types of property, Office vacancies are up from 17.3% as at February 2022 to to 27.4% as at February 2023. The loan-to-value ratio sits at 36.9%, slightly higher than 36.7% a year prior.

There’s juicy HEPS growth at enX Group (JSE: ENX)

The industrials group has posted a positive set of numbers

Other than in the headlines related to the recent Takeover Regulation Panel investigations into activities in the company’s shares, you may not have heard much about enX. The company operates in the fleet, equipment and petrochemicals industries, so it sits at the heart of the South African economy. This perhaps makes it even more impressive that HEPS is up.

There are no more discontinued operations in this period, so we can just look at continuing operations. Revenue is 22% higher and HEPS has increased by 32%. As net finance charges came down year-on-year (which helps HEPS), just looking at those two numbers hides the fact that operating profit before tax was only 5% higher. This means that there was underlying margin pressure in the operations.

The group sounds happy with the balance sheet even after paying substantial special and ordinary dividends to shareholders, which led to a large increase in net debt since August 2022.

And as a final note on this company, here’s today’s reminder that no matter what crisis is going on out there, someone is making money:

NEPI Rockcastle gives a first quarter update (JSE: NRP)

Even on a like-for-like basis, net operating income has jumped sharply year-on-year

At a time when South African property funds are taking strain from load shedding, NEPI Rockcastle shareholders are enjoying exposure to Eastern Europe. In the first quarter of 2023, net operating income jumped by 27% year-on-year and 17% on a like-for-like basis (i.e. excluding acquisitions).

This has been driven by a strong performance in the malls. Tenant sales are up 25% year-on-year, with a 14% rise in footfall and most of the rest coming from a higher spend per visit.

Retail vacancies have fallen to 2.4%, with the management team highlighting that international retailers have taken an interest in the region based on growth being achieved in the retail sector.

The loan-to-value ratio looks comfortable at 34.7%, below the company’s “strategic threshold” of 35%.

And even without the pain of load shedding in that region, NEPI Rockcastle has cleverly raised “green” funding and is investing in solar PV projects at the malls.

With guidance of full-year growth of 11% in recurring distributable earnings per share, it’s hard to find fault with this performance. The share price has climbed 15% in the past year.

Ninety One sees HEPS drop by 15% (JSE: N91)

Asset management firms tend to be highly geared to equity market performance

How does an asset manager make money? Simply, they charge a combination of fixed fees (based on assets under management – AUM) and performance fees (also linked to AUM but only applicable when markets do well).

When markets perform poorly, there’s a double dose of pain. AUM drops and performance fees evaporate. When markets do well, the reverse happens and profits are great, although asset managers tend to reward staff more than shareholders even in those scenarios. It’s an industry-wide issue for investors.

The year ended March 2023 wasn’t a happy time for equity markets around the world. It’s therefore not surprising that Ninety One’s average AUM fell by 3% and total AUM fell by 10% year-on-year. Of concern is the net outflow number of £10.6 billion, as outflows represent a decision by clients to walk away from the products.

HEPS has fallen by 15% and the dividend per share is down by 10%, so the payout ratio increased.

Although market prices have improved thus far in 2023, the outlook statement is still cautious. It helps at least that Ninety One carries no debt, so shareholders are the beneficiaries of any profits, rather than bankers.

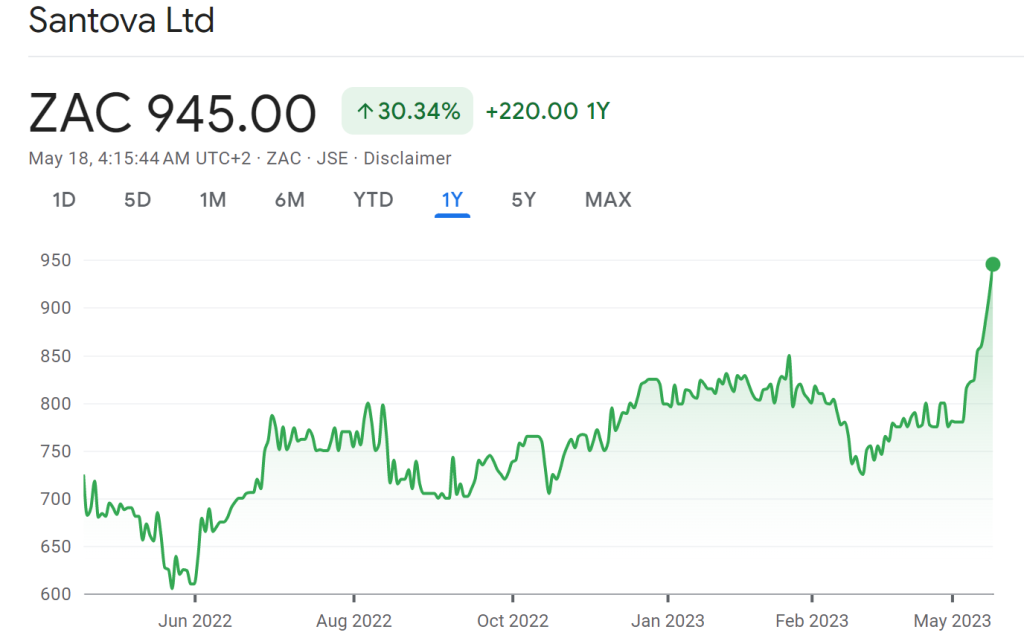

Santova adds another 4% to the share price (JSE: SNV)

Be very wary of sharp upward moves like we’ve seen at Santova recently

Santova is a solid company. As small caps on the JSE go, the company has done exceptionally well at punching above its weight and generating returns for shareholders. The share price is up more than 193% in 5 years!

Still, I have a rule about never chasing a chart that looks like this:

Big upward moves like that tend to pull back, although not always of course. If we knew what a price would always do, then we would all have yachts on Instagram.

Santova might be linked to the shipping industry, but not with yachts. The company falls into the broader supply chain industry, with freight forwarding and other services (and not just regarding ships). For the year ended February, that was a fun place to play, evidenced by a 22.1% increase in HEPS to 154.83 cents.

The net asset value (NAV) is R7.51 per share and the share price closed at R9.45. Although NAV is little more than a guideline in most sectors, I become a little nervous when companies trade at a significant premium to NAV unless we are talking about a manufacturing business with depreciated assets that are still operating. An exception is where a company generates return on equity far in excess of the cost of equity, which is the return required by shareholders.

Another important point is that although Twitter tends to get excited about the proportion of cash on Santova’s balance sheet and the quantum relative to the market cap, this is a working capital intensive business and they need a lot of cash to operate. The company is in a solid position, but don’t assume that all the cash on the balance sheet is sitting around waiting for a special dividend.

There isn’t even an ordinary dividend, with Santova electing to reinvest everything in the business instead. This says a lot about the growth prospects, which is why the valuation has run higher.

Telkom: a R13bn company with a R13bn impairment (JSE: TKG)

Telkom has shed over 43% of its value in the past 12 months

Value investing is a tough game. There are companies that are cheap for a reason, often due to market emotions or sheer apathy, creating opportunities. Then there are companies that are cheap because the underlying business units are rubbish, creating a value trap that is tough to explain to your friends.

“But what were you expecting?!? Everyone hates using Telkom!”

Common sense is often a better analytical tool than reading the numbers in detail. With a 15.6% drop in the share price in response to a trading update, Telkom shareholders won’t want to read these numbers.

For the year ended March, Telkom is going to recognise an impairment across the business of approximately R13 billion. After yesterday’s sell-off, that’s approximately equal to the group market cap!

Even if we strip out this non-cash charge and ignore the restructuring cost related to a 15% headcount reduction across the group, normalised HEPS fell by 60% to 80% this year.

Telkom is a technological dinosaur that is trying to migrate to new technologies in an economy that is making this incredibly difficult to achieve.

You know what happened to the dinosaurs, right?

Tsogo Sun Gaming flags a jump in HEPS (JSE: TSG)

In today’s accounting LOL, one of the drivers is “hedge ineffectiveness”

For the year ended March, Tsogo Sun Gaming welcomed many customers back to its properties for nights of gambling, drinking and generally doing things that nobody was allowed to do during the pandemic. It’s not surprising to see a solid uptick in HEPS vs. a base period that still had the impact of lockdowns.

With HEPS up by between 34% and 42%, the company has grown into the share price rather than grown the actual share price in the past year. You could always range-trade this share rather than go to any of the casinos:

The hotel management contract cancellation had a negative impact on HEPS, as the company expected. The funnier update (just because of how it reads) is a R57 million after tax benefit from “hedge ineffectiveness” – if a hedge isn’t going to work out as a hedge, it may as well work out as a trading profit!

Little Bites:

Director dealings:

A director of Ninety One (JSE: N91) has bought shares worth £19.3k.

A director of a subsidiary of Sappi (JSE: SAP) has bought shares worth just over R190k, an interesting play as you don’t often see dealings in Sappi and the cycle has turned against the company, driving a large sell-off in the shares.

A director of KAL Group (JSE: KAL) has bought shares worth R50k.

There isn’t much liquidity in tech microcap ISA Holdings (JSE: ISA), with a market cap of just over R210 million. In a further trading statement, the company guided HEPS for the year ended February of between 12.95 cents and 15.05 cents, an increase of between 23.3% and 43.3%. The shares trade (occasionally) at R1.25 per share at the moment.

Sygnia (JSE: SYG) seems to be intent on recycling executives. After outspoken founder and CEO Magda Wierzycka returned to the top job, we now have Niki Giles returning as Financial Director after serving in that role between 2015 and 2017 and subsequently leaving Sygnia in 2018.

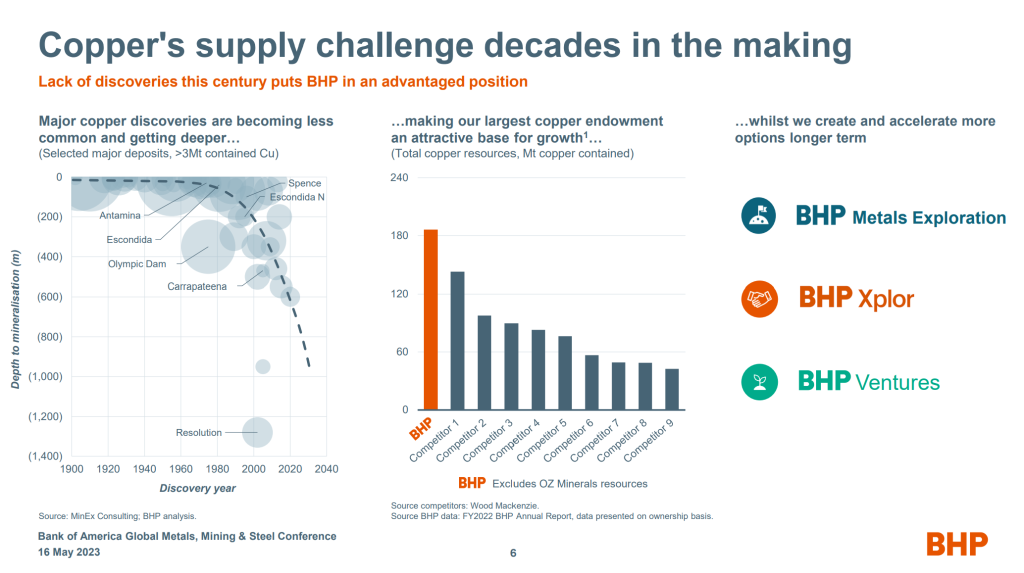

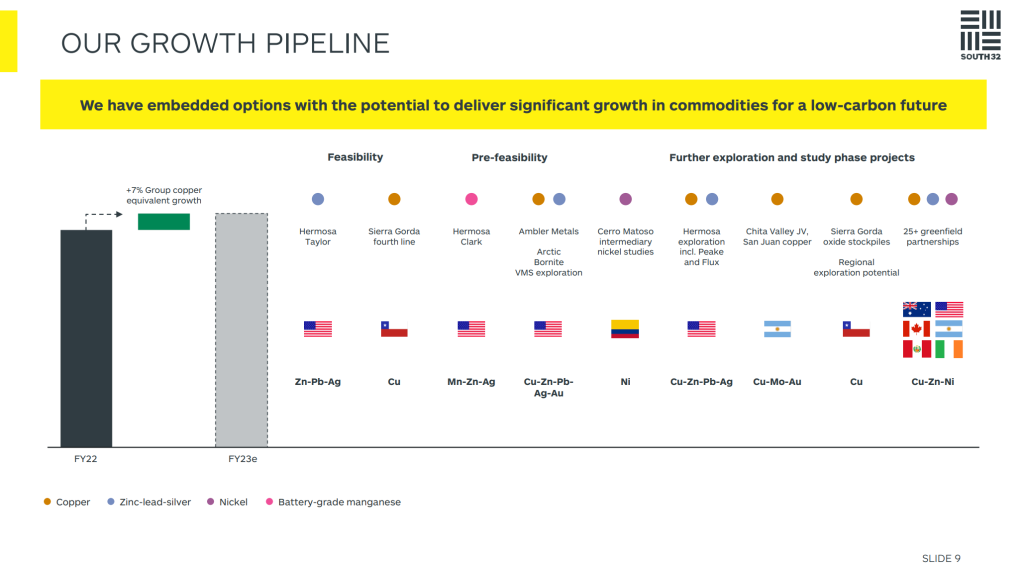

BHP (JSE: BHG) and South32 (JSE: S32) give strategic update presentations

There’s some interesting stuff in here to sink your teeth into

I enjoy it when companies make these types of presentations available. There’s almost always overlap with the most recent results presentation, but focusing on something other than the latest results means that you tend to notice new things.

Both BHP and South32 presented at the Bank of America Securities 2023 Global Metals, Mining and Steel Conference.

At BHP, the focus on copper in this presentation is clear. Here is just one example, showing how long supply and demand imbalances can take to develop:

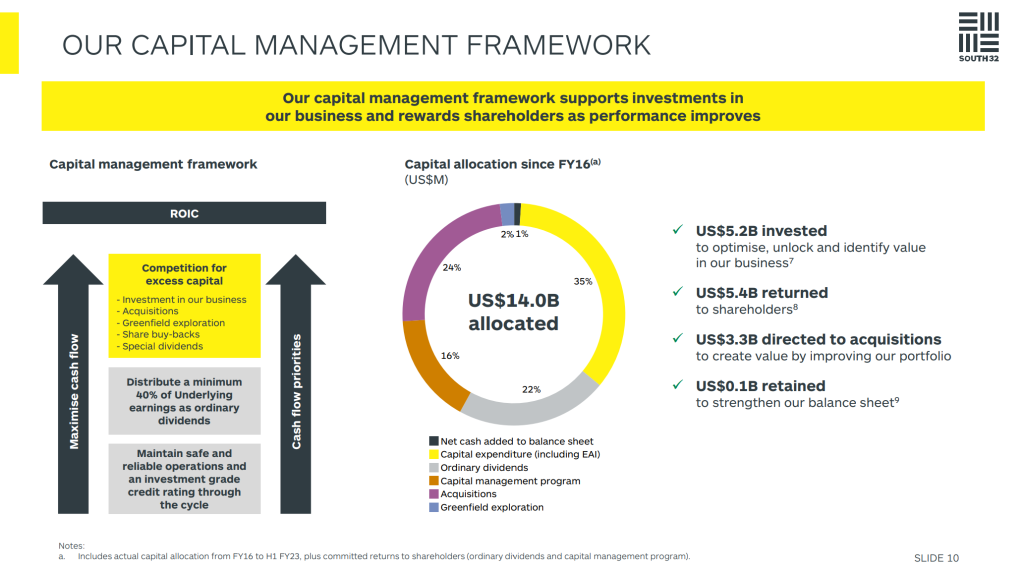

The South32 presentation is available here. This is a good example of the kind of slides that you’ll find in the deck:

I love the concept of “competition for excess capital” and especially the list of options given for excess capital. This is a lovely way to understand how share buybacks end up happening in companies outside of US tech companies – a company investing in its own shares is supposed to be a capital allocation decision. In US tech, it ends up being an anti-dilution mechanism to try and offset the effect of share-based compensation that is little more than a way to hide staff costs as non-cash expenses.

Thankfully, there’s none of that nonsense at South32.

In addition to the capital allocation learnings in the deck, there’s also some cool stuff on how mining projects are developed by these groups:

It’s all about taking projects from the “study phase” through to pre-feasibility, then feasibility and finally full operation. The trick lies in choosing which projects to focus on, an incredibly difficult task that is literally a case of throwing darts at a moving target as commodity dynamics change.

Welcome to the world of mining.

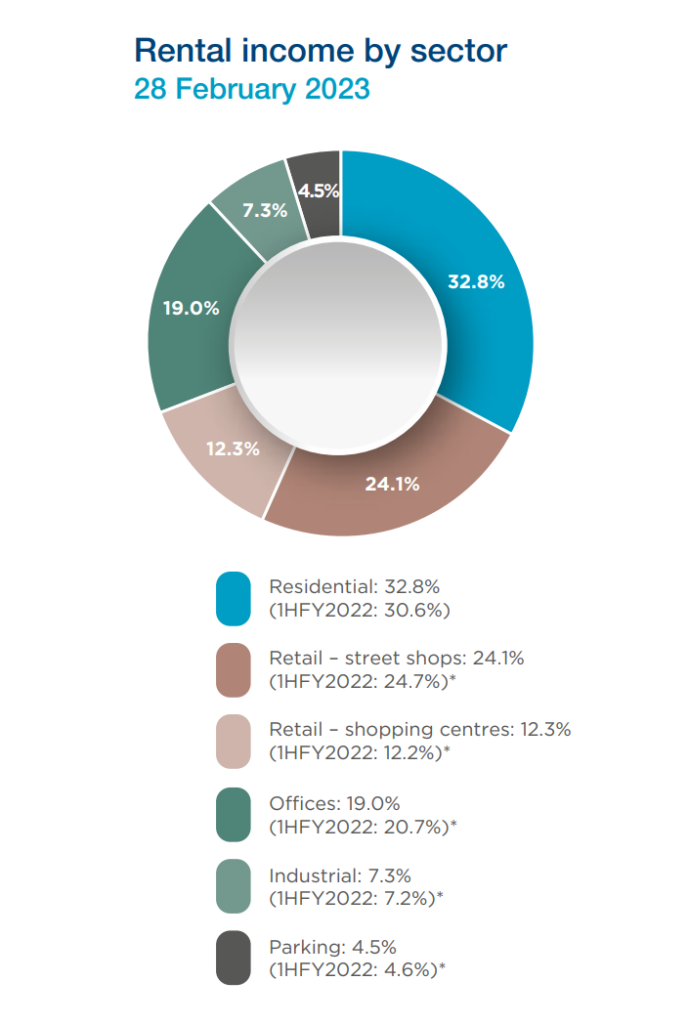

Octodec releases interim results (JSE: OCT)

Over the past year, the share price has gained over 20%

In the six months ended February, Octodec’s rental income grew by 3.2% and distributable income after tax was 10.7% higher. With the management team clearly feeling better about the world around them, the dividend per share is 20% higher.

The net asset value (NAV) per share is 3.9% higher at R24.0 per share. With the share price closing at R10.29 on Tuesday, the discount to NAV is a whopping 57%.

Although the fund has residential property as its highest source of income, the portfolio is more diversified than most people realise. Here’s a useful chart from the earnings update:

Purple Group announces a R105 million rights offer (JSE: PPE)

This will enable a R150 million capital raise in EasyEquities that Sanlam is also supporting

If ever you needed an example of the price driving the narrative, look no further than Purple.

When the price was clearly far too high and I was making myself unpopular on Twitter by pointing that out, everything was absolutely in love with the company. With the price having come down to earth with a bump, now the company gets given a hard time on Twitter.

If these emotions weren’t present in the market, there would never be opportunities to take advantage of them.

With a market cap of roughly R1.5 billion, a rights offer of R105 million is significant but by no means earth-shattering. This amount will enable Purple to follow its rights in a R150 million capital raise by EasyEquities, as Purple holds 70% in that company. Sanlam holds the other 30% and is supporting the raise.

In turn, EasyEquities will use the capital to accelerate expansion and move into international target regions including Kenya.

Pricing for the offer will only be announced later this week.

In the meantime, we know that four shareholders collectively holding 27.12% in Purple Group have committed to follow their rights in full. No commitment fees are payable for this.

All eyes will be on the pricing announcement on 18 May.

Reunert is a rare good news story in this environment (JSE: RLO)

This company is on the right side of load shedding, which helps greatly

In an update for the six months ended March 2023, Reunert delivered solid results in its segments.

The Electrical Engineering segment increased cable production in a period with no labour disruptions. As a double whammy of good news, margins also improved as supply chains eased in the aftermath of the pandemic.

In Applied Electronics, one of the drivers of performance was demand for renewable energy products and services as load shedding continued.

The Information and Communication Technology segment performed in line with expectations, which included high credit losses against the remaining lease and loan receivable book. The sale of this book funded the purchase of Etion Create.

Investors should note that a R44 million insurance payout in this period has helped operating profit. For reference, operating profit in the comparable period was R465 million, so that’s a material impact.

HEPS has increased by between 31.9% and 41.9%, Although the payout is part of the good news, there is clearly positive momentum in the operations as well.

Santam reflects on a promising quarter (JSE: SNT)

Despite tough conditions and changes to the group structure, it sounds good for Santam

For the three months ended March, Santam focused on bedding down its new operational restructure and improving the underwriting performance in the motor class of insurance. The property class was hit by claims related to power surges – thanks Eskom!

The Conventional Insurance segment achieved gross written premium growth of 6%. Despite best efforts, the underwriting result still came in below the target range of 5% to 10%.

Importantly, no adjustment was made to the contingent business interruption claims that did damage to the Santam brand during the pandemic.

Investment returns in this segment were volatile, but better than in the comparable year.

Santam doesn’t give any details on the performance of the Alternative Risk Transfer business, other than to give an overall positive commentary on it.

In the Sanlam Emerging Market partner business, Shriram in India achieved 23% growth in gross written premium, but net earned premium was in line with 2022 because of the lag between writing and earning the premiums. In India, most premiums are written annually in advance. The underwriting performance was weaker because of higher claims in the motor book due to inflationary impacts on repair costs and higher claim severity.

In Africa, the disposal of 10% in the SAN JV to Allianz is expected to close in the second half of 2023.

In other M&A news, the Competition Tribunal approved the acquisition of the MTN device insurance book. Santam is allocating R60 million to this initiative and believes that the underwriting profits will be sufficient to achieve the required return on capital. 400,000 policies will be added to the Santam licence.

After a volatile run, Santam is still up 4% year-to-date but down nearly 7% over 12 months.

Tharisa’s HEPS has moved higher (JSE: THA)

The share price has been stuck in a range since July 2022

PGM and chrome business Tharisa has released a trading statement for the six months ended March. It’s a bit of an odd one, as they give an earnings range with a tolerance of 10%. They also give a percentage change based on the earnings range but ignoring the “tolerance” – I don’t think I’ve seen this approach anywhere else in a trading statement.

If I interpret the tolerance correctly, HEPS could actually be between US 15.3 cents and 19.8 cents, which is a wide range vs. US 15.5 cents in the prior period. Without the tolerance, the guidance is for HEPS of between US 17 cents and 18 cents per share, which is growth of between 9.6% and 16.1%. I wish they wouldn’t make it harder to understand with the “tolerance” included in the guidance.

If you closely follow the markets, you’ll know that a trading statement is triggered by a 20% change in earnings. HEPS doesn’t trigger this but EPS does because of a once-off number related to the Karo Mining acquisition.

I would just focus on HEPS.

Little bites:

Director dealings:

A director of FirstRand (JSE: FSR) has bought shares worth R4.8 million.

A director of Calgro M3 (JSE: CGR) bought shares worth just under R115k and an associate of another director bought shares worth R134k. This means that three directors (including the CEO) recently bought shares.

Alphamin (JSE: APH) announced its Q1 numbers back in April. If you’re interested in digging deeper, the Q1 financial statements are now available at this link.

On 15 May, Calgro (JSE: CGR) managed to repurchase 3.71% of shares in issue for R14.8 million. It’s unusual for small caps to get meaningful buybacks done, hence the special mention.

Growthpoint (JSE: GRT) announced that both Fitch and Moody’s affirmed the company’s credit ratings and outlook.

The acquisition of Mediclinic (JSE: MEI) by a consortium of Remgro (JSE: REM) and Mediterranean Shipping Company has now received approval from the South African Reserve Bank. All regulatory approvals have been obtained and the UK court is expected to sanction the scheme on 24 May.

Efora Energy (JSE: EEL) is suspended from trading and has finally released financial statements for the year ended February 2021.

In a step that you won’t see very often, 4Sight Holdings (JSE: 4SI) has completed its redomicile to South Africa from Mauritius.

The circus at Pembury Lifestyle Group (JSE: PEM) continues. Two of the schools in Joburg have been instructed to close until the properties are rezoned. I have to include this screenshot purely because I’ve never seen such a ridiculous sentence on SENS in my life – it literally sounds like a recording of a child who had a busy day at school and needs to give ALL the details on the drive home. Highlights mark where it begins and ends:

These are messy numbers for shareholders to work with

Whenever a company releases adjusted numbers, you have to read very carefully to figure out exactly what those adjustments are. In the case of Altron, there are many in the market (like me) who thinks that there are some business-as-usual items in here that don’t justify adjustment.

For example, you can’t do work in the public sector and then expect the market to ignore bad debts in that space. If you work with government, there will be pain. Being surprised by that is like being shocked that a scorpion stung you.

If we look at continuing operations, revenue increased by 19% but EBITDA only grew by 2%. HEPS fell by 8% to 47 cents. You can now see why the company tries to convince the market that the adjustments are reasonable, as adjusted HEPS is miraculously 19% higher at 89 cents.

A language that we all speak is cash. Interestingly, the dividend has been declared based on adjusted HEPS rather than reported HEPS. That does go some way towards justifying the adjustments, although the board would’ve been well aware of that when proposing this dividend. I’m still skeptical of using adjusted HEPS here.

For the year ended February 2023, Calgro reported a juicy 45% increase in HEPS. This was driven right from the top, with a 15.4% increase in group revenue.

Metrics have moved in the right direction, with gross profit margin up by 220 basis points to 23.5% and the net asset value (NAV) per share up by 19.8% to R9.51. Calgro trades at a huge discount to NAV, with a share price of R2.96.

The group expects consistent delivery of the residential property development pipeline over the next year, which in turns means an expectation of consistent cash flows. In the memorial parks business, the group is still experimenting with the model but seems to be making progress in achieving product market fit.

Calgro M3 has been on Unlock the Stock a couple of times before and will return on 25 May to talk through these numbers and take your questions. Attendance is free and anyone is welcome, as we seek to open up the market to retail investors. Brought to you by A2X, you can register for the event here>>>

Dipula flags a drop in total distributable earnings (JSE: DIB)

The significant change in capital structure drives a major move in the dividend per share

In June 2022, Dipula Income Fund implemented a scheme of arrangement that saw all the A shares repurchased in exchange for the issue of 2.4 B shares per A share. In other words, there are now only B shares in issue vs. a mix of A shares and B shares as at February 2022.

So for the six months ended February 2023, it makes a lot more sense to look at the total distributable earnings in the company rather than the earnings per share, as the number of B shares in issue has changed drastically and there are no A shares left.

Distributable earnings have decreased by 6.92% to R256.6 million, which equates to almost 28.72 cents per B share. The interim dividend is nearly 25.85 cents per share and the share price closed at R3.90.

Ivan Saltzman hands over the reins at Dis-Chem (JSE: DCP)

Rui Morais is given the keys to a high performing castle

Ivan Saltzman co-founded Dis-Chem with his wife Lynette back in 1978. From a single store, they grew the business into South Africa’s largest retail pharmacy chain by market share. That’s quite a legacy to leave.

Although it sounds like Ivan won’t be able to resist spending time in the stores, he is now stepping down as CEO and handing over to CFO Rui Morais, who has been developed for this role for years now. Julia Pope takes over as CFO, having been in the finance team for six years. As succession planning goes, this is about as smooth as it gets.

The new team inherits a business that is still cooking. Excluding COVID vaccines, group revenue is up 9.0% and HEPS for the year ended February should be between 115.6 cents and 118 cents, an increase of between 16.5% and 19.0%. This puts the share price on a trailing Price/Earnings multiple of around 20.5x.

To achieve further alignment with the new team, the Saltzman family will sell a 3.75% stake in Dis-Chem to the executives and senior management team over time. No details are given of the structure to achieve this.

The announcement ends off with a clue that growth isn’t slowing down, with Dis-Chem acquiring a new distribution centre in Gauteng for R502 million. This will increase group warehouse space by 75%! The group indicates a “step change” in the pace of store rollout. Watch this one carefully, especially after a sell-off in the share price of 33% in the past year.

KAP’s share price is still getting klapped (JSE: KAP)

Another 3.4% drop takes the year-to-date move to -37%

The lift just keeps going down for KAP and there’s no sign of the basement level yet. This share price chart has been one way traffic this year:

The company has released an operational update for the ten months to 30 April 2023 and the dreaded words “load shedding” don’t take long to appear. This is causing havoc for KAP, driving issues like lower downstream demand at customers and higher wear and tear due to damaged equipment.

The macroeconomic environment is also putting pressure on the group, with higher raw material costs and of course higher finance as rates have increased.

Although the company has tried to navigate this environment, performance has come in below expectations. Headline earnings per share (HEPS) from continuing operations for the year ending June 2023 is expected to drop by at least 30% to a maximum of 52.1 cents. This puts the group on a trailing price/earnings multiple of 5.4x, which is cheapish but not bargain basement stuff.

Debt serviceability ratios are expected to remain within range, which means net debt to EBITDA of below 2.5x and interest cover of more than 3.5x.

If we look at divisional performance, PG Bison gained market share and even managed to increase prices, but the timing of the increase couldn’t save the operating margin for this period which fell year-on-year. Restonic suffered a drop in volumes and lower demand particularly in rural areas. Feltex (the automotive components business) had a much better time as new vehicle assembly volumes recovered.

Moving on to Safripol, usually the most important profit contributor to the group, we find a really tough result with lower margins and weaker domestic demand for polymers. Plant breakdowns as a result of load shedding were also a problem. Exports should help make up the demand gap from local challenges but they come at lower margins, so operating margin has dropped below the through-the-cycle target of 7% to 9%.

There are also margin pressures at Unitrans, with an operating margin below the prior period. This business is being restructured into a single operation with dedicated sector focus.

Finally, Optix (previously called DriveRisk) is a very small contributor that was acquired in December 2021. The weakening of the rand against the dollar had a major negative impact in the latest period.

Importantly, KAP is busy with renewable energy investments for Safripol and PG Bison, the largest energy users in the group and the most important divisions. The announcement doesn’t indicate the extent to which these projects can meet total energy needs.

Some sunshine at Pan African Resources (JSE: PAN)

The mining group is making significant progress on renewable energy opportunities

Eskom really has given ESG a boost, making renewable energy a business imperative if nothing else. PanAfrican Resources is investing heavily, with a significant project at Barberton Mines’ Fairview operation and a power purchase agreement with Sturdee for a 40MW solution available at any of the facilities.

Pan African was an early adopter of solar technology in the industry, as the first South African mining company to commission a utility scale, grid-tied solar PV project with the Evander Mines facility.

Across the existing projects and current feasibility studies, Pan African would be able to generate 28% of its power requirements once completed. That’s still going to take a while though.

A year to remember at Raubex (JSE: RBX)

You won’t see many local companies reporting record earnings at the moment

There are a couple of trends that Raubex is bucking. The first is the general mood in South Africa, with the company releasing record earnings for the year ended February 2023. The second is the usefulness of Australia, with a significant positive contribution to operating profit from a region that has claimed many South African corporate scalps.

Revenue is up 32.2%, HEPS is up by 32.1% and cash generated from operations jumped by an enormous 145%. The final dividend has jumped by almost 41% to 76 cents per share.

With a major contributor being the completion of the Beitbridge Border Post project, I would be careful extrapolating these numbers into the next year.

There are still large losses at Stefanutti Stocks (JSE: SSK)

But at least they are smaller than in the prior period

In a trading statement for the year ended February, Stefanutti Stocks has given guidance for total earnings and earnings from continuing operations, as there are important restructuring activities underway.

For continuing operations, the headline loss per share is expected to be between -37.30 cents and -20.72 cents, a significant improvement on -82.88 cents in the prior period but clearly still a loss.

For total operations, the headline loss per share range is -48.54 cents to -24.83 cents vs. a loss of -248.27 cents in the prior period.

The share price closed 7.6% lower at R1.10.

Vodacom reports on a major year in its history (JSE: VOD)

The R43.6bn acquisition of 55% in Vodafone Egypt was the biggest deal in Vodacom’s history

The Egypt deal was completed in December, so numbers for the year ended March are significantly impacted by the consolidation of this business into the group. For that reason (and in an effort to adjust for other distortions like currency movements), Vodacom reports several key metrics on a normalised basis.

This is helpful, because group revenue growth of 16% is a very different story to normalised revenue growth of 4.9%. Normalised EBITDA grew by 3.6%, so normalised EBITDA margin has deteriorated in line with the theme we are seeing in the telecoms industry at the moment.

This is a capital intensive business model, with Vodacom planning to spend between 13% and 14.5% of overall revenue on capital expenditure. Load shedding means that a great deal of “investment” goes into keeping the existing infrastructure alive rather than expanding it, with R4 billion spent on backup power solutions since 2020 and R300 million in the last financial year on diesel, security and maintenance. Net profit for the year is R18.1 billion, so this is less than a 2% impact on profit but is still very irritating, particularly when profit only grew by 2.1% year-on-year.

You may recall that Vodacom is in the process of completing a major fibre transaction with CIVH, which owns the Vumatel and Dark Fibre assets. ICASA approval was obtained in October and Competition Commission approval is still pending. To allow for the delay in this regulatory approval, Vodacom and Remgro (JSE: REM) announced an extension of the longstop date to 30 November 2023 and a few other revised terms to make allowance for the timeline.

Notably, Vodacom has moved to a payout policy that will see 75% of headline earnings paid out as a dividend. This is well down from the old policy, as the group looks to retain more capital for growth. This is why the full-year dividend of 670 cents per share is lower than 850 cents in the prior year, a 21.2% decrease despite a drop of “only” 6.4% in HEPS.

If you’re wondering why HEPS is down when profits are up, the higher number of shares in issue is the answer. This is due to the acquisition of the business in Egypt.

If we look a bit deeper, we find a predictably lethargic performance in Vodacom South Africa (EBITDA up 2.6% and capital expenditure just 0.2% higher) and a more exciting performance elsewhere, like Egypt posting EBITDA growth of 9.4% and the rest of Vodacom’s operating regions achieving 6.6% EBITDA growth. Safaricom was under pressure, with EBITDA down by 6.2% because of startup losses in Ethiopia that more than offset 4% growth in EBITDA in Kenya.

Net debt has increased from R35.2 billion to R48.3 billion. Of the R13.1 billion increase, the bulk (R10.7 billion) is related to the acquisition of Vodafone Egypt. Net debt to EBITDA has moved from 0.9x to 1.1x but if Egypt was consolidated for the full year, it would’ve actually dropped to 0.8x.

Vodacom is now trading on a trailing dividend yield of just under 6%. Considering that Vodacom’s share price is at a similar level to a decade ago, that dividend is the bulk of the return to shareholders – or the only return, depending when you bought! With this new payout ratio, Vodacom will have to convince shareholders that the reinvestment of more capital is a lucrative use of funds.

A year-to-date chart of arch-rivals Vodacom and MTN is fascinating when you consider the completely different major underlying exposures to Africa (East and North Africa at Vodacom and West Africa at MTN):

But the real fun is to draw it over 5 years, so you get the full effect of how wild MTN is in comparison to Vodacom:

Little Bites:

Director dealings:

The CEO of Calgro M3 (JSE: CGR) has bought shares worth R589k

There’s a change of leadership at British American Tobacco (JSE: BTI). Jack Bowles steps down as CEO immediately, with such a sudden change never being a good sign. He’s responsible for the A Better Tomorrow strategy, which I think helped keep the entire ESG consulting industry in business. Those consultants will be pleased to know that his successor, CFO Tadeu Marroco, wants to continue the progress made in distracting the market from the health issues of the core product range by marketing colourful “non-combustible” products instead.

City Lodge Hotels (JSE: CLH) has had a big month, with the share price turning higher and delivering a 14.4% return. At least some of that momentum must’ve been helped along by a company called HSS Investments, which now holds a stake of 5.0% in the company.

Attacq (JSE: ATT) is still busy negotiating legal agreements with the Government Employees Pension Fund regarding the 30% acquisition by the GEPF of Attacq Waterfall Investment Company.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Karooooo’s latest quarter, which makes it even clearer that management should be focusing on the core Cartrack business.

The ongoing bad luck at Quantum Foods, where the macroeconomic and load shedding issues have now been compounded by the horrors of avian influenza.

RFG Holdings as a good news story in a sea of pain on the JSE, with the business really performing well.

Sappi’s cyclical nature and ongoing debt reduction despite a sharp drop in profits.

MTN’s margin compression in South Africa and almost all the African subsidiaries, with market concerns over the balance sheet trajectory clear to see in the share price.

Southern Sun riding the wave of a post-COVID travel and tourism recovery, except in Sandton.

Richemont’s exceptional results in the core business this year, along with the strength of its direct-to-consumer strategy.

Transaction Capital’s latest capitulation in the share price off the back of results.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

With no South African assets anymore, this primary listing is headed for New York

Before you panic, AngloGold is not getting rid of its JSE and A2X listing. Even the listing in Ghana survives! The point is that the primary listing is moving to the New York Stock Exchange (NYSE), which means that the US regulations become the primary regulatory environment.

Get ready for quarterly results from the company!

It’s fascinating to note that the American Depository Receipt (ADR) programme in the US already accounts for two-thirds of daily liquidity in the stock, despite US investors holding only 35% of the share register. The pools of capital in the US are deeper than anything we can imagine in South Africa and AngloGold isn’t blind to that fact.

Of course, what the company is really hoping to achieve is a higher valuation multiple in line with international peers. That’s a nice way of saying that the company is trying to shed the South African image, which isn’t doing the multiple any favours even though there are no remaining assets here.

And in case you’re wondering, there’s also a change to domicile on the cards. The new listed structure will have its holding company in the UK, but “key corporate functions” will still be provided from Johannesburg.

The cost of this transaction is huge, with the announcement noting an expected cost of 5% of the market cap because of taxes payable in South Africa. That’s a nice payday for the fiscus, but AngloGold will then be out of the tax net forever.

The company also announced an update for the quarter ended March, with cash costs per ounce up 16% to $1,204/oz due to inflationary pressures. All-in sustaining cost (AISC) was up 15% to $1,619/oz. EBITDA fell from $438 million in Q1 2022 to $320 million in Q1 2023, a drop of 27%.

Guidance ranges for 2023 have been confirmed.

Ascendis puts Surgical Innovations into business rescue (JSE: ASC)

Legacy tax and creditor issues have been compounded by a new SARS assessment

When Ascendis Health released its interim results for the six months to December 2022, shareholders were advised of the dispute between Surgical Innovations and SARS regarding VAT for 2018 – 2020, with a total provision of R67 million raised in those results.

The company engaged with SARS on this amount but to no avail, with SARS requiring almost immediate repayment. Along with another legacy creditor, this has put the directors in a position where they needed to voluntarily commence business rescue proceedings.

The intention is for the business to continue while the disputes with SARS and the other non-operational creditor are resolved. The board of Surgical Innovations believes that there is a “high likelihood” that the company will exit this process as a solvent and commercially viable operations.

The announcement came out shortly before the close and the price moved 4.8% lower, but I wouldn’t see this as true price discovery on this matter as the bid-offer spread tends to be wide on small caps like this.

Eastern Platinum’s Q1 report is out (JSE: EPS)

The company is focused on the Zandfontein underground restart plan

In the first quarter of 2023, Eastern Platinum grew revenue by 26.7% year-on-year. The key driver was an increase in chrome sales on the open market, offset to some extent by pressure on PGM prices.

Mine operating income increased by 53.8% to $5.2 million. Net income attributable to equity holders was $1.3 million vs. $3.0 million in the comparable period, with forex losses as the major reason for the drop.

The balance sheet is where the attention needs to be, with a working capital deficit (current assets less current liabilities) of $35.2 million and short-term cash resources of only $3.8 million.

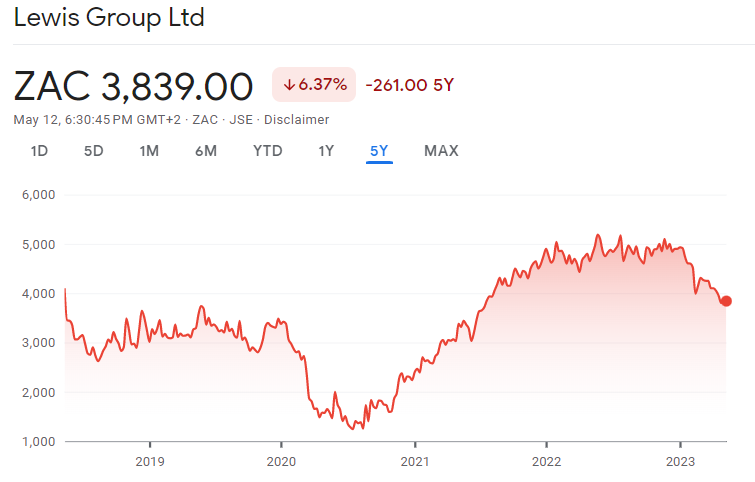

Lewis updates the market on its share buybacks (JSE: LEW)

These buybacks are core to the investment thesis

I wouldn’t usually give share buybacks this much airtime, but at Lewis the situation is a little different. The furniture industry in South Africa isn’t exactly a bastion of hope at the best of times, yet Lewis has managed to generate decent returns at times for shareholders because of the clever use of buybacks. Having said that, the share price has rolled over recently:

What you aren’t seeing on this chart is the all-important dividend yield that makes the total return look far better than the chart suggests. The key learning from Lewis isn’t related to cash dividends, but rather the use of share buybacks when a share is trading at a modest multiple.

This strategy has continued, with shareholders giving authority back in October 2022 for the company to repurchase up to 10% of shares in issue. Lewis has announced that 3% has been repurchased, leaving 7% to go.

The price volatility comes through here, with repurchases executed at prices between R38.00 and R50.00 per share. The average price is R47.23 per share and R83.7 million worth of cash has been invested in these buybacks,

With the current price at R38.39 and seemingly dropping, the company needs to get on the accelerator pedal with the remaining buybacks.

Richemont closes off its best-ever year (JSE: CFR)

The direct-to-consumer business now contributes nearly 75% of group sales

€20 billion is a big number. Although Richemont’s sales came in slightly short of that level, a 19% increase vs. the prior year was enough to make FY23 Richemont’s strongest ever year based on revenue. Operating profit also reached an all-time high of just over €5 billion and operating margin expanded from 22.4% to 25.2%.

Profit for the year from continuing operations was €3.9 billion, up 60% for the year. If you look a level lower on the income statement though, you’ll see some ugly numbers. The loss from discontinued operations was a huge non-charge of €3.4 billion on the transfer of YNAP net assets to being classified as held-for-sale. Non-cash or otherwise, the reality is that Richemont didn’t have a good time with this online initiative.

Still, the direct-to-consumer business has been a strategy that has paid dividends in other ways for Richemont. Sales in directly-operated stores contributed 68% of group sales. When combined with online sales, that number is close to three quarters of group sales.

If you look at the underlying business units, the Jewellery Maisons (like Cartier) increased sales by 16% at constant rates and achieved a 35% operating margin. A substantial 83% of revenue is generated through direct-to-consumer sales. Total sales in this segment were €13.4 billion.

The Specialist Watchmakers achieved 56% of sales through direct channels. Revenue grew by 8% at constant exchange rates and operating margin of 19% was achieved. This segment contributed €3.9 billion in revenue.

The Fashion & Accessories segment is the smallest with a revenue contribution of €2.7 billion, up 19% vs. the prior year. This business unit is profitable but not by much vs. the rest of the group, with an operating margin of around 3.5%.

There still isn’t much of an Asia Pacific growth story in these numbers, with sales up by 6%. The rebound in China etc. only came through in the final quarter of the year. This should be a significant driver of sales growth in the new financial year.

If you’re interested in the luxury sector, our report and podcast on LVMH (the global giant that is surprisingly different from Richemont) is fresh out the oven in Magic Markets Premium. Together with my partner Mohammed Nalla, we put out a report every week on a global stock and a subscription only costs R99/month. You can subscribe here>>>

Little Bites:

Director dealings:

Guess what? Des de Beer has bought more shares in Lighthouse Properties (JSE: LTE), this time worth R4.49 million.

The Chief Growth Officer of British American Tobacco (JSE: BTI) has bought shares worth £21.8k (note the currency).

Nedbank (JSE: NED) has repurchased 3.1% of its shares (based on the number in issue at the last AGM) at a total investment of R3.36 billion. The average price paid per share is R212.91 and the current share price is around R209.

While we are on buybacks, this is a reminder that Glencore (JSE: GLN) and South32 (JSE: S32) are both busy with share buyback programmes and are making daily announcements on the progress.

I’m not sure how they got this wrong, but Octodec (JSE: OCT) had to release a correction to its trading statement. The guidance for distributable income per share for the six months to February was given as between 81 and 99 cents per share. It should’ve been between 85 and 89 cents per share, which is thankfully within the originally disclosed range rather than outside of it. The percentage changes in the first trading statement are correct.

I’m never quite sure how much we can read into updates like these, but Vodacom (JSE: VOD) has constituted a standing investment committee. Such committee meetings were previously convened on an ad-hoc basis. This suggests that Vodacom is putting increased focus on how capital is allocated, which certainly makes sense to me.

A mandatory offer for enX Group is on the table (JSE: ENX)

Don’t get excited: there’s no premium here

If you followed the Takeover Regulation Panel’s investigation into various transactions involving enX, Extract Group, Zarclear Holdings and African Phoenix, then you’ll know that part of the settlement is that African Phoenix and its concert parties need to make a mandatory offer to all enX shareholders.

enX currently trades at R6.40 and the offer price is R6.41 per share, so there’s no real excitement here. Where this could be useful is for holders of large blocks of shares who would otherwise not be able to sell at the prevailing price due to liquidity constraints.

The concert parties hold 48.80% in the company and shareholders holding 19.6% have given an irrevocable undertaking not to accept the offer.

There’s a difference between concert parties for an offer and parties acting as a voting bloc. It’s likely that the concert parties will collectively move through a 50% holding, which would normally be relevant to the Competition Commission. I assume that the parties don’t have a formal voting agreement that would trigger a merger filing. I am sure that African Phoenix is pretty tired of regulators as it is!

enX also released a trading statement for the six months ended February 2023, reflecting an increase in HEPS from continuing operations of between 26% and 38%. Total HEPS is down between 51% and 55%.

Interestingly, revenue from continuing operations is up 20% and profit before tax is expected to be between 20% and 24% higher, so margins have expanded slightly.

There are bad signs at MTN (JSE: MTN)

I’m glad I sold at the start of this year

Telecoms companies don’t do well during load shedding. Battery backup power is incredibly expensive and consumer activity in general is subdued. Increased security costs don’t help either.

To compound MTN’s problems, the macroeconomic picture in key African subsidiaries is back to being messy. Due to difficulties in upstreaming cash, MTN Group is opting for scrip dividend alternatives from MTN Nigeria and potentially MTN Ghana as well. This increases the stake in those companies (as not all minority shareholders in those countries choose the scrip option) but does nothing to bring cash to where it is needed most: the mothership to reduce debt.

For now at least, there is also cash being upstreamed from subsidiaries. Whether or not it can continue remains to be seen.

Speaking of debt, group leverage of 0.3x is well with the limit of covenants. The holding company debt is what really counts, as MTN cannot move cash around in the group at the moment without major costs and problems. This has increased to 0.9x from 0.8x at the end of December. This is within target for now and the balance sheet looks alright, but you only need to look back a few years to see what can go wrong.

Moving to financial performance in Q1, I could only shake my head at MTN noting 90 days of load shedding during the quarter. In other words, there was load shedding basically every day vs. 14 days in Q1 2022. I assume that people making WhatsApp calls over fibre rather than voice calls on their network contributed to voice revenue falling by 16%, with overall service revenue up by 1.3%. An average prepaid subscriber uses 2.7GB per month and a contract subscriber uses 13.8GB per month.

South African EBITDA margin contracted by 370 basis points, so EBITDA fell by 6.5%. They hope for a recovery in the second half of the year based on improved network resilience during load shedding.

EBITDA pressure is being felt elsewhere as well, like Nigeria down 130 basis points, Southern and East Africa down 10 basis points and West and Central Africa down 170 basis points. EBITDA margin increased by 560 basis points in Middle East and North Africa but that’s by no means the most important region in the group.

In strategic news, the company is considering an exit of three operations in West Africa over the medium-term. These include the bustling economies of Guinea-Bissau, Guinea-Conakry and Liberia. They contribute just 0.7% to EBITDA, so I don’t think anyone will miss them.

It’s not obvious to me that things will improve anytime soon.

Octodec flags a significant jump in its dividend (JSE: OCT)

This REIT is unusual on our market, focusing on urban residential property

If you can imagine buy-to-let at scale, you’re on the right track when it comes to Octodec. The company has released a trading statement for the six months to February 2023 that reflects an increase of between 8% and 12% in distributable income per share.

With better operating conditions, the cash payout ratio has increased as the distribution is expected to be between 16% and 24% higher. This is an interim distribution of between 58 cents and 62 cents. For reference, the share price is trading at R9.82.

Money for jam at RFG Holdings (JSE: RFG)

There have been improvements across several food categories in the group

There are very few good news stories on the local market. Closing over 14% higher on Thursday, RFG Holdings flew the flag on an otherwise dark day. Of course, it’s the export business that did particularly well, with the local business growing thanks to inflation outpacing the drop in sales volumes as consumers tightened their belts. Literally.

The weakening of the rand contributed to a better international operating profit margin, so RFG is making a case for itself as a rand hedge that nobody talks about. International selling prices are also key, so it’s certainly not a pure-play view on the currency.

Locally, there were success stories in the Today acquisition (pies), fruit juice, dry foods and meat categories.

The HEPS increase of 35% to 40% is made even more impressive by the different reporting calendars, we are looking at a 26-week period vs. a 27-week period. In other words, this was achieved despite an extra trading week in the comparable period.

Sappi rallied 6.4%, but not because of these results (JSE: SAP)

On a day that was strong for rand hedges, Sappi reported a big drop in profits

Cyclical business are wild things and you’ll struggle to find a more cyclical business than Sappi. The market fell away from the company in the latest quarter, with “downstream inventory destocking” – a fancy way of saying that customers significantly slowed down on orders. This led to production curtailment and associated pressure on margins.

Just how badly can profit drop in these businesses, I hear you ask?

Year-on-year sales revenue fell by 22% this quarter and EBITDA crashed by 50%. HEPS fell by 67%. See? Badly.

The good news is that net debt was 32% lower at $1.225 billion, with $1 billion as the stated objective. I therefore find it rather strange that the group recently executed share repurchases of $23 million, representing 1.62% of shares in issue. I appreciate that the share price has lost a third of its value in the past year and that buybacks make sense when the price has come off, but reading this announcement makes me feel like reducing debt should be the only focus.

Trematon reports a double-digit drop in INAV (JSE: TMT)

If you read carefully, you’ll see the real reason for the drop

Trematon holds a fascinating portfolio of investments, ranging from Club Mykonos in Langebaan to Generation schools. With such a varied set of interests, the right measure to evaluate performance is intrinsic net asset value (INAV) per share, commonly used by investment holding companies.

As at February 2023, this measure has decreased by between 10% and 11% year-on-year. The INAV is between 418 cents and 422 cents. Importantly, 40 cents of the drop (i.e. most of it) is because of a capital distribution in December 2022.

In other words, the value of this Western Cape focused investment portfolio is largely flat year-on-year.

The share price is trading at R2.43 per share, a discount to INAV of around 42%.

Little Bites:

Director dealings:

Here’s arguably the most important one of the week: Sabvest (JSE: SBP) has bought R770k worth of shares in Transaction Capital (JSE: TCP) at an average price of around R7.70. In case you don’t know, Sabvest is the investment holding company of respected investor Chris Seabrooke who sits on the board. I would’ve liked to see a much larger purchase, though!

There’s a nice payday for a director of AfroCentric (JSE: ACT), whose associates have accepted the partial offer from Sanlam to the tune of nearly R142 million.

A director of DRDGOLD (JSE: DRD) has sold shares worth nearly R3.4 million.

Des de Beer seems to have found the loud pedal with his share purchases, buying R21.5 million worth of shares in (you guessed it) Lighthouse Properties (JSE: LTE).

A director of KAL Group (JSE: KAL) has bought shares worth R99k.

Newpark REIT (JSE: NRL) has a bid-offer spread the size of the moon, with bids at R4.50 and offers at R6.25. When you see the dividend, you’ll understand the offer price. For the year ended February 2023, the total dividend was 67.19 cents per share of which the final dividend was 42.19 cents per share. At the current market price of R4.50, this tiny property fund with a R450 million market cap is on a trailing yield of 14.9%!

Montauk Renewables (JSE: MKR) is one of those oddball listings on the JSE where the company doesn’t even bother writing a SENS announcement to accompany quarterly results. They simply provide the link to the filing in the US. I therefore won’t give this much airtime, other than to point out a loss before tax of $15.8 million vs. a loss of $1.4 million in the comparable quarter.

Kibo Energy (JSE: KBO) is holding an extraordinary general meeting to get authority to increase the authorised share capital of the company as part of a transaction to issue warrants and “reprofile” the institutional investor bridge loan facility. If you’re a shareholder here, I suggest you read carefully and make sure you understand what is being proposed by management..

Due to a conflict of interest as the auditor of both Grand Parade Investments (JSE: GPL) and Sun International (JSE: SUI), Deloitte and Grand Parade have mutually agreed to part ways. Moore Cape Town is the happy winner here, recommended as the new auditor of Grand Parade. Shareholders will be asked to approve this at the company AGM.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie