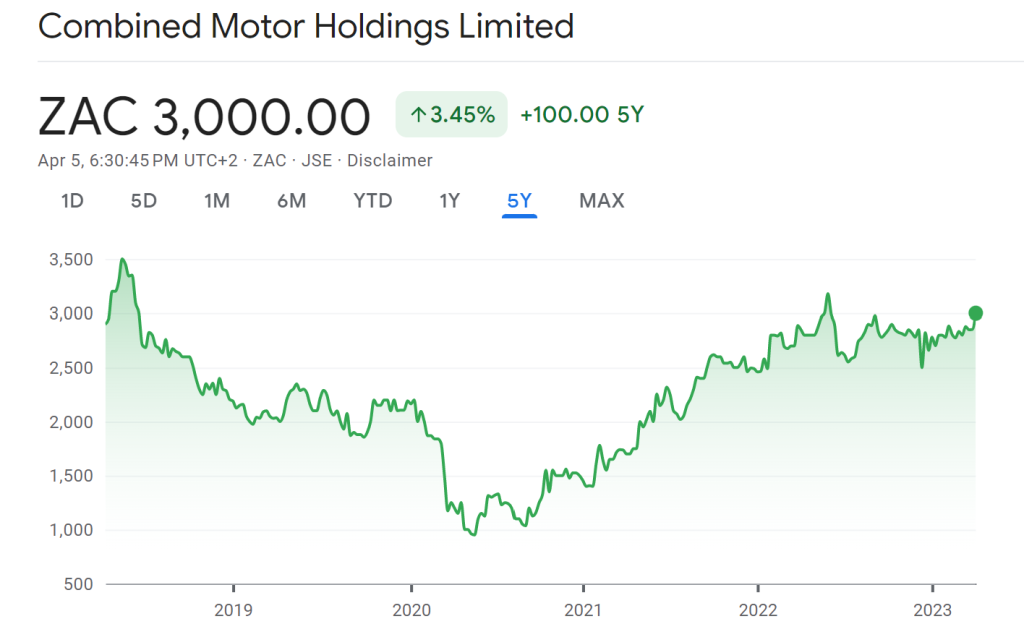

Combined Motor Holdings has another massive year (JSE: CMH)

I decided to go back to the annual report for the 2022 financial year to look for a chart that I remembered seeing previously. Here it is:

This sets the scene for the 2023 numbers, which I really didn’t expect to post much growth on top of the 2022 performance. I was absolutely wrong, with CMH expecting headline earnings per share (HEPS) of between 601.2 cents and 651.3 cents, a jump of between 20% and 30% vs. that ridiculous 2022 base.

Based on this, you might expect the share price to have reported massive growth over the last five years. Instead, here’s your chart:

All revved up and nowhere to go…the market has been skeptical of these high earnings continuing, with the company trading on a modest multiple and substantial dividend yield. The share price did close 4.9% higher after this trading statement, so there was some positive surprise in the market, but not much.

Copper 360 Limited is coming to the market (JSE: CPR)

I’m really hoping that the share code isn’t a sign of pain to come

Will shareholders need CPR? I hope not. It’s rare to see a new listing on the JSE and I wish Copper 360 Limited all the best with this.

Unless you’re an “invited investor”, you’ll have to wait to buy shares on the open market. Genuine IPOs are more unusual on the JSE than an honest politician, as our market just isn’t supportive of those deals. The company will raise around R152.5 million from investors.

To find out more about this pure-play copper opportunity, refer to the pre-listing statement here.

EOH catches another bid (JSE: EOH)

The release of detailed results added another 4% to the share price

EOH had given us a very good idea of what was coming in these numbers, with a recent update suggesting growth in operating profit and a far stronger platform going forward.

Detailed numbers have confirmed this, with operating profit for the six months ended January 2023 of R110 million. I misread the original announcement, as operating profit for FY22 was R100 million, not just for the comparable half-year. The comparable half-year profit was actually much higher, which shows how messy these numbers have been, as profits are actually lower year-on-year when looking at just the interim period.

The principle is unchanged, which is that EOH now has a profitable core business. Although this period doesn’t reflect the benefit of the rights issue in reducing debt, the next period will.

Europa Metals doesn’t waste any time (JSE: EUZ)

The drilling campaign at Toral has begun

With the twelve month joint venture budget with partner Denarius Metals now agreed, Europa Metals has moved quickly in getting the drilling programme underway.

This initial programme forms the bulk of the €1.8m budget agreed with Denarius. There are two rigs onsite and the company will update the market as results come in.

Industrials REIT is now a pure-play business (JSE: MLI)

But that benefit is most likely to accrue to Blackstone over time

A focused strategy doesn’t just make you a better business; it can make you a better acquisition target as well. Industrials REIT is proof of that, with a potentially huge offer on the table from Blackstone that sent the share up over 35% in recent days.

If the Blackstone offer goes ahead, the company would be buying a pure-play view on multi-let industrial property in the UK. This is the case after Industrials REIT announced the sale of the German care home joint venture for net proceeds of £15.6 million, which the company will use for further acquisitions in the UK.

It hasn’t been an easy journey, with a disposal programme to get to this point of more than £600 million over five years.

ISA Holdings plays its cards close to its chest (JSE: ISA)

The initial trading statement has the bare minimum details

Under JSE rules, a company needs to release a trading statement when it believes that earnings for a period will differ by more than 20% vs. the comparable period.

For the year ended February 2023, IT company ISA Holdings expects headline earnings per share (HEPS) to be at least 20% higher. As I said, this is literally the bare minimum disclosure. It could be 21% and it could be 50% – we just don’t know until a further update is released.

After all that, Northam Platinum walks away (JSE: NPH)

RIP to this year’s One Capital corporate finance budget

This is incredible, really. After a monumental fight at the regulators that must’ve cost an absolute fortune in professional fees, Northam Platinum has walked away from the Royal Bafokeng Platinum deal. This leaves Impala Platinum’s offer as the only one in the market.

Northam was able to do this because of the drop in prevailing PGM prices, with a sustained drop below a certain level being considered a material adverse change (MAC).

A MAC clause is there to protect the potential buyer of an asset. If a MAC occurs, the buyer has the option to walk away from the deal. Although it provides a convenient escape hatch, buyers don’t easily invoke these clauses unless they were looking for a way out.

In the case of Northam Platinum, they used the MAC clause to walk away. The biggest loser here is surely One Capital, with a history of charging eyewatering advisory fees to Northam. I hope they got decent retainers along the way, as that success fee has got to sting.

Texton sells Alrode Business Park (JSE: TEX)

The focus is on office assets – an interesting play in this environment

Texton is one of the stranger property companies on the local market. A rally of 16% was the market’s response to this latest update, but huge amounts of value have been lost over the years.

The latest news is the sale of Alrode Business Park for R50 million. That may not sound like much, but the market cap is around R770 million. With a book value of R55 million, capital has been recycled at fairly close to book value and the share price responded positively.

I’m not convinced by this rally, as the cash isn’t going to be paid to shareholders. Instead, it will be used to repay debt and “develop its SME strategy” – hmmm.

Little Bites:

Director dealings:

Value Capital Partners has bought R7.1m worth of shares in ADvTECH (JSE: ADH)

The Group CFO of MTN (JSE: MTN) has bought shares worth R4.4m.

A director of Lewis (JSE: LEW) has sold shares worth R695k.

Several NEPI Rockcastle (JSE: NEP) directors have made the scrip distribution election, as one would expect.

Novus Holdings (JSE: NVS) is busy selling a letting enterprise for R125 million. The due diligence deadline has been pushed out to mid-April and other conditions to June.

Conduit Capital’s (JSE: CND) sale of wholly-owned subsidiary Constantia Life and Health Assurance Company Limited has been delayed, with the fulfilment date for suspensive conditions pushed out to the end of April.

The CEO of Grand Parade Investments (JSE: GPL) has resigned from his position, having achieved the turnaround strategy that he set out to achieve. A replacement will be named in due course.

If you are a shareholder in Calgro M3 (JSE: CGR) then keep an eye out for the circular related to the introduction of an employee share incentive scheme.

At last, and not a moment too soon, a busy week for the companies on South Africa’s stock exchanges.

Exchange-Listed Companies

Investec plc and Rathbones Group plc have reached an agreement regarding an all-share combination of Investec Wealth & Investment (Investec W&I UK) and Rathbones to create a leading discretionary wealth manager in the UK. Under the terms of the combination, Rathbones will issue new shares in exchange for 100% of Investec W&I UK. On completion, Investec will own 41.25% of the economic interest in the enlarged Rathbones Group, with voting rights limited to 29.9%. The terms of the combination imply an equity value of c. £839 million for Investec W&I UK. The transaction includes Investec’s wealth and investment businesses in the UK and Channel Islands but excludes those in Switzerland and South Africa.

Absa proposes to implement a c. R11,16 billion deal which will distribute a 7% stake in the company to a Corporate Social Investment trust (4%) and a further 3% to its staff trust. The company says that the CSI scheme and the SA Staff scheme will enhance its B-BBEE credentials to at least 25%. The 62,6 million shares (7%) will be sourced from the existing 16 million shares currently held in the Absa Empowerment Trust, 12,7 million of which were obtained as part of the separation from Barclays in 2017 (currently held by Newshelf 1405) and 46,6 million new shares which will be sourced through a specific issue of shares for cash to Newshelf 1405.

Glencore has made an unsolicited proposal to the Board of Canadian miner Teck, which contemplates an all-share acquisition of Tech by the company followed by a demerger of the combined coal business. Glencore and Teck shareholders would own c. 76% and 24% of the merged entities, respectively. The Teck Board has rejected the proposal advising its shareholders to do the same.

Outsurance Holdings, an 89,7% owned subsidiary of Outsurance Group, is to acquire 50% of a stake held by former CEO and founder of Outsurance Holdings in Australian insurance operation Youi. He holds an equity stake of 5.3%. The stake will be acquired for A$36 million in cash.

Omnia, via its subsidiary MBE, has signed a conditional sale and purchase of shares agreement with Indonesian MNK which will see the companies combine their explosive businesses in a move to enhance opportunity for growth and expansion in the global mining market. The joint venture will combine BME’s technology and innovative products and systems with MNK’s local networks, experience and resource, creating a highly differentiated and integrated offering with an expanded suite of products and services for both surface and underground mines.

Blackstone and the Board of Industrials REIT have reached an agreement on key financial terms of a possible cash offer to the company’s minority shareholders. Under the terms of the final offer, shareholders would receive 168 pence per ordinary share in cash. The companies expect to make a firm intention announcement by 14 April, 2023.

Old Mutual Alternative Investments fund, Hybrid Equity, has invested R150 million into Enable Capital, a funder in national fibre network infrastructure in South Africa. The investment allows Enable Capital to find solutions for specific challenges faced by the subcontractors involved in the physical construction and deployment of local, regional and national fibre network infrastructure in the country.

Hammerson plc has completed the disposal of its 25% stake in Italie Deux, a shopping centre in Paris and 100% of Italik extension for a cash consideration of €164 million. This represents a 4% discount to the December 2022 book value and a net equivalent yield of 5%.

Industrials REIT has disposed of its interest in German care home joint venture for £15,6 million. The disposal marks the transition for the company into a 100% UK multi let industrial business. For the past five years, the company has been disposing of assets valued in aggregate at c.£600 million as part of its strategy to dispose of non MLI investments.

Texton Property Fund has disposed of Alrode Industrial Park to Benav Properties for R50 million. The disposal proceeds will be used to repay debt and further develop its SME strategy.

Sirius Real Estate has disposed of a mixed-use business park in Wuppertal, in North Rhine Westphalia, Germany for €8,8 million.

In a related party announcement Visual International is to acquire a 20% interest in Tuin Huis, a residential property development company, for a nominal sum. Tuin Huis has undertaken two trial Infill Housing Projects in the Durbanville area. Visual will be responsible for building and/or project managing all the development projects undertaken by Tuin Huis at cost.

In another related party transaction, Grindrod has disposed of a London residential property to the Grindrod family for £1,65 million (R35,56 million). The reason for the disposal – the company no longer has London-based operations following the spin-off of Grindrod Shipping.

Oceana has advised shareholders that the disposal of the Commercial Cold Storage business, announced in October 2022 is now unconditional. In addition shareholders were informed that Mokobela Shakati, a member of the purchasing consortium had been replaced by Ntiso Investment, sponsored by Mcebisi Jonas.

Unlisted Companies

Peach Payments, a local digital payment service provider enabling seamless, secure transactions for business and consumers in Africa, is to receive €29 million in Series A funding from Apis Growth Fund II. Peach Payments currently operates in South Africa, Kenya and Mauritius. The funds will be used to expand its product offering and reinforce its merchant value proposition. Other investors in Peach include Launch Africa, AG Venture and UW Ventures.

Orion Minerals has raised A$8,9 million via the placement of 593,499,999 shares at an issue price of A$0.015 (R0.18). The placement introduces Clover Alloys (SA) as a new cornerstone investor which will enable Orion to accelerate the development of both of its key base metal production hubs in the Northern Cape province.

Dipula Income Fund has reached a settlement with Breede Coalitions, following the shareholders notification to the company that it intended to exercise its Appraisal Rights. In March the company made an offer to repurchase all of the Dipula A shares for a consideration of 2.4 Dipula B shares for every Dipula A share held. In terms of section 164 of the Companies Act, shareholders of a scheme are afforded the right to demand that the company pay fair value for all DIA and DIB shares. In terms of the agreement reached, Dipula has paid an all-inclusive amount of R34 million for the 1,715,000 DIA shares and 2,000,000 DIB shares held by Breede Coalitions.

Ayo Technology Solutions has disclosed more information on its settlement with the Public Investment Corporation (PIC) following negative press around the scanty details of the agreement reached with the PIC. Ayo will repurchase 17,202,756 ordinary shares from the Government Employees Pension Fund (GEPF) for a total repurchase consideration of R619,42 million. The GEPF will retain a minimum stake of 25.01%.

NEPI Rockcastle will issue 28,830,268 new shares in terms of its scrip distribution alternative. The scrip dividend shares will be issued at R92.82 per share for an aggregate R2,68 billion. The total number of ordinary shares in the company following the issue will increase to 635,830,268.

Cashbuild has repurchased 89 164 shares in terms of its odd-lot offer to shareholders, representing 0.37% of the total issued share capital of the company for a total consideration of R17,59 million.

Shoprite is yet another blue-chip company to announce it will take a secondary listing on A2X. Currently the company’s stock trades on the JSE, the NSX and the LUSE. It will trade on A2X with effect from 11 April, 2023.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

South32 has increased its share repurchase programme by c. $50 million in anticipation of a stronger outlook for commodity prices in the second half of its financial year. This will enable the company to return $158 million to shareholders before September 2023. This week the company repurchased a further 1,287,351 shares at an aggregate cost of A$5,63 million.

Glencore this week repurchased 8,280,000 shares for a total consideration of £38,24 million. The share repurchases form part of the second phase of the company’s existing buy-back programme.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 27 to 31 March 2023, a further 3,883,762 Prosus shares were repurchased for an aggregate €272,23 million and a further 485,830 Naspers shares for a total consideration of R1,60 billion.

Two companies issued profit warnings this week: Advanced Health and Pick n Pay.

Five companies issued or withdrew cautionary notices: Tongaat Hulett, Conduit Capital, Primeserv, Finbond and Ayo Technology Solutions.

Africa has seen an increase in the number of stock markets and the level of market capitalisation over the last two decades, with improvements to market infrastructure across the continent.

Yet, with certain exceptions, liquidity levels remain a primary concern for investors on the continent, exacerbated by factors such as inefficient trading systems, high transaction costs slowing the velocity of trade, the lack of participation of retail investors on the markets, and long-term and large holdings of pension funds.

Against this background, efforts have been made to tackle the liquidity challenge. Most noteworthy is the launch of the African Exchanges Linkage Project (AELP) on 7 December 2022, an initiative which could, over time, boost liquidity by facilitating cross-border African investment, and attract more international investors if liquidity levels increase.

The AELP, a joint initiative of the African Development Bank and the African Securities Exchanges Association, launched an e-platform (The AELP Trading Link), which allows investors in different countries to buy shares on other exchanges through a common platform. The AELP Trading Link, which is hosted on Oracle Cloud Infrastructure, has been designed to integrate with exchange and stock broker trading systems, and is available in English, French and Arabic. It aggregates live market data from the exchanges and enables stock brokers to access information and see the market depth and liquidity of the foreign market of interest. The AELP Trading Link essentially enables seamless cross-border securities trading between seven African stock exchanges, which together represents 2,000 companies with roughly US$1.5 trillion market capitalisation.

The linkage project is not the first regional linkage initiative to boost liquidity in African Stock Markets. The Bourse Régionale des Valeurs Mobilières, which links the exchanges of eight West African nations, namely Benin, Burkina Faso, Côte d’Ivoire, Mali, Niger, Senegal and Togo, is the only exchange in the world shared by several countries, and has been most successful.

In its initial phase, seven stock exchanges in fourteen African countries will be linked by the AELP. The participating exchanges include the Bourse Régionale des Valeurs Mobilières, integrating the eight West African countries: the Casablanca Stock Exchange, The Egyptian Exchange, the Johannesburg Stock Exchange, the Nairobi Securities Exchange, The Nigerian Stock Exchange and the Stock Exchange of Mauritius.

Ultimately, the AELP is expected to, among other things, promote innovations in product creation that would support the diversification needs of investors in Africa and address the lack of depth in African capital markets. It is understood that once the necessary infrastructure has been created, institutional participation is also potentially contemplated, enabling institutions to settle trades directly.

The current framework for the linkage between the exchanges is “sponsored access”. This is based on the model where a registered stockbroker or “originating broker” in one participating securities exchange takes an order from a domestic client and sends a registered stockbroker on another exchange a request to execute the trade in that market. The executing or “sponsoring broker” is responsible for ensuring compliance to the rules, settlement and practice of the market where the security is bought or sold. Therefore, the sponsoring broker will clear and settle trades in the host market, using their local currency, in compliance with the host market’s rules and practices, and the regulatory bodies in all the participating markets are apprised of the progress.

The securities are to be held in the central securities depository where the security was traded, reducing cross-border movement of securities, and streamlining settlement and clearing to comply with only one market; that being the market where the trade is executed and the security is held.

While a project to link trading on seven of Africa’s largest and most liquid stock exchanges has the capacity to boost liquidity by encouraging cross-border African investment and attract more international investors, the AELP is still in its infantile stages and still faces roadblocks on a continent with disparate regulatory regimes and trading rules, and historical capital market challenges. Nevertheless, it is a step in the right direction.

Dimitri Cavvadas is a Partner and Obakeng Phatshwane an Associate | Fasken

This article first appeared in DealMakers AFRICA.

DealMakers AFRICA is the continent’s quarterly corporate finance publication. www.dealmakersafrica.com

As the ‘L’ in Leverage Buyout becomes more expensive, we can expect to see some downward pressure on private equity deal activity. In South Africa, leverage has not been used to the same extent as in more developed markets, but using debt is still a key component of securing returns attractive enough to pull the trigger on a transaction. And with interest rates now higher than before the COVID pandemic, many experts are warning that the receding tide of cheaper capital will reveal who has gone swimming naked with their portfolio companies.

Africa-focused private equity funds appear to have enjoyed a boom year in 2021. Figures from the African Private Equity and Venture Capital Association (AVCA) show that private capital fund managers in the region raised $4,4bn in final closes and another $2,3bn in interim closes last year.

This is a drop in the global financial ocean, but it does mark a fourfold increase on the capital raised during the depths of the pandemic in 2020.

The 2021 fundraising totals were boosted by some of the continent’s largest ever fund closes. Most notably, Development Partners International’s third fund closed on $900m in October, with another $250m in co-investment capital.

Scratch beneath the surface, however, and the picture looks less rosy. Much of the capital raised in 2021 simply represents “deferred investment” from 2020.

The total volumes raised by funds holding a final close in 2020 or 2021 – $5,5bn – were considerably less than the $6,7bn raised in the two years before the pandemic. Hope that the recovery would accelerate has been dented by the worsening global macroeconomic conditions in the first half of 2022. Today, Africa-focused fund managers face a major test in persuading capital allocators that the time to put their money to work on the continent is now.

Yet, with rising inflation in advanced economies prompting central bankers to raise interest rates, emerging markets have become less attractive as investment destinations. Higher returns available in the US and Europe mean that investors are less likely to take on the real and perceived risks of allocating to Africa focused vehicles.

This will particularly disadvantage managers unable to demonstrate a track record.

Currency volatility – a longstanding thorn in the side of efforts to boost investment in Africa – is likely to become more severe in the coming months, given that the Federal Reserve’s hawkish policies are strengthening the dollar.

Several of Africa’s largest markets have already seen their currencies depreciate against the dollar this year. For instance, according to the Bank of Ghana, the Ghanaian cedi depreciated by almost 20 percent against the dollar between January and July.

An AVCA survey published in March found that 23 percent of GPs “frequently” experience delays in raising capital in Africa because of currency risks. Another 41 percent view currency fluctuations as having a “significant negative impact” on returns.

Abi Mustapha-Maduakor, the chief executive of AVCA, insists that it is possible to learn from the current situation. She believes that increasing interest from venture capitalists in African start-ups won’t diminish. She asserts that “the fundamentals are still strong.” Even now, a portion of investors will probably want to invest more aggressively in Africa.

VC firms may be better placed to attract capital in the current environment than traditional private equity players that invest in brick-and-mortar businesses. MD of Endeavor South Africa, Alison Collier says that Fintechs and other tech start-ups have “attracted a lot of international private money because those businesses are looked at as international businesses. They started in Africa, but they can scale up globally.”

On the other hand, she bemoans the enduring wariness among institutional investors of committing to Africa-focused PE funds. “The perception of risk, in general, for Africa is higher than the reality,” she says.

Perhaps more surprisingly, even asset owners with impact mandates frequently have reservations about the continent when given the chance to invest in Africa and support the Sustainable Development Goals. According to a report released by the International Finance Corporation in July 2021, only a small portion of impact capital (31 percent) is allocated to African emerging markets funds.

Mobilising local capital

Institutional investors from outside the continent may be less likely to commit to Africa-focused funds until currency and other macroeconomic headwinds have eased. But what about pools of capital from within Africa itself?

African pension funds hold assets amounting to at least $350bn, a fi¬gure that has grown substantially in recent years. But these funds overwhelmingly allocate to government securities or, in markets such as South Africa, listed equities. Private equity and pension funds should be an ideal fit but, generally, there is a lack of understanding regarding the asset class among African pension funds.

Progress is being made to reform regulations to allow institutional investors to allocate more to alternative funds. In July last year, the South African government con¬firmed that the country’s pension funds would be able to increase their allocation to private equity to 15 percent of their assets from January 2023. Until now, allocations have been limited to 10 percent.

It is worth noting, however, that South African pension funds are not in danger of breaching the current limit. In fact, South African institutional investors allocate just 0.3 percent of their AUM to private equity, according to research published last year by development agency, FSD Africa.

Development finance institutions (DFIs) are commonly cited as playing a critical role in convincing institutional investors to back Africa-focused funds. Some of them say that we absolutely need a DFI to be part of a fund, because it gives comfort around the level of due diligence and ESG processes.

There is little doubt that DFIs will remain indispensable to private equity in Africa.

As private equity law doyen, John Bellew of Bowmans says, “DFIs have, for many years, provided the backbone for private equity managers looking to raise capital to deploy in Africa. We expect them to continue to support the industry, but to encourage managers to also raise capital from commercial LPs, especially in successor funds. A number of DFIs also have an appetite for co-investment, and we expect this also to continue.”

Michael Avery, is the editor of Catalyst

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

Anglo takes another step towards low carbon (JSE: AGL)

The goal is to reduce emissions in the steelmaking process

Anglo American has put together a deal with H2 Green Steel in Sweden that will see the Swedish company trial Anglo’s premium quality iron ore from Kumba in South Africa and Minas-Rio in Brazil as feedstock for a direct reduced iron production process.

If H2 gets this right, they will have created a plant in Sweden that would reduce CO2 emissions by up to 95% in the process vs. traditional steelmaking!

Investec and Rathbones to create the UK’s leading discretionary wealth manager (JSE: INL | JSE: INP)

The merged entity will have £100 billion in funds under management and administration

Investec is taking a major step in its UK business that will see Investec Wealth & Investment combined with Rathbones to create the biggest discretionary wealth manager in the UK.

The structure will see Rathbones acquire the business from Investec and issue shares to pay for it, which will take Investec to an economic interest in Rathbones of 41.25% and voting rights of 29.9%. The shares are locked up for two years and Investec can partially sell the stake in years three and four. Investec is also not allowed to acquire more shares in Rathbones or make an offer for five years.

The implied equity value for Investec’s business under this transaction is £839 million.

The companies believed that annual synergies from the transaction will be £60 million. There are many other strategic benefits to the deal, including a stronger client proposition and larger distribution power.

The Rathbones brand will be retained and the Investec Wealth & Investment brand will be phased out over time.

Murray & Roberts shareholders say yes to Bombela sale (JSE: MUR)

No surprises here – the balance sheet needs help and this is a quick win

Murray & Roberts needs to sort out its balance sheet. This means that non-core assets need to go, particularly those offering a low return on capital.

Building infrastructure is what the company should be doing, not owning it. Recognising that point, Murray & Roberts agreed to sell the Bombela Consortium (Gautrain) to Intertoll International Holdings. The net proceeds to Murray & Roberts would be R1.26 billion if shareholders said yes to the deal.

They did, in fact, say yes. I am not surprised at all that it received “overwhelming” support as Murrays really needs the capital. This will be used to reduce debt, which will now be R1.39 billion after the repayment. Around 10% of that debt balance is related to leases, which is a lot friendlier than owing the bank.

The annual interest cost will drop by R95 million.

As a quick update on the business, Murray & Roberts confirmed that the Mining platform represents R14.1 billion of the R16.1 billion order book, with the remainder in the Power, Industrial & Water platform. I’m old enough to remember when Murray & Roberts arranged a fancy investor day with presentations by each platform.

That was before the business (and share price) imploded:

Nampak buys some time (JSE: NPK)

And time is money, literally

As highlighted by its recent results update, Nampak is still in serious trouble. With its earnings being crushed by forex losses, the company isn’t making any progress in reducing its debt.

The latest news is positive in terms of keeping Nampak alive, though it sure does come at a cost. There was a facility of R1.35 billion partially due on 31 March 2023 which has had its maturity date extended to 30 June 2024. There are two different structures that make up that amount and both have been moved to that date.

What does this cost? Well, there’s a fee of 0.43% payable as an extension fee (R5.8 million) and the far more onerous term is that the original funding cost of 5.25% for the US Private Placement Noteholders (going back to 2013 when rates were much lower) has been ramped up to a fixed rate of 12.00%.

Even Jerome Powell would be taken aback by that hike!

On the revolving credit facility, rates are increasing by 86 basis points.

That’s not all, folks. The restructuring is subject to Nampak executing a rights offer that will be sufficient for a R350 million debt repayment by the end of September 2023. There will also need to be asset disposals of at least R250 million by the end of December 2023.

Finally, Nampak is required to finalise term sheets for the refinancing of long-term funding by 15 June 2023.

Nampak’s market cap is R650 million, so a rights offer of sufficient magnitude will be hugely dilutive for shareholders. This announcement came out after the close of play, so we don’t know yet what the market will think of this news.

Positive news for the NEPI Rockcastle balance sheet (JSE: NRP)

The scrip dividend was well supported and a “green” facility has been raised

Scrip dividends are useful cash retention tools, with companies offering to issue additional shares in lieu of a cash dividend. To entice shareholders to choose the shares rather than the cash, they frequently sweeten the deal by making the share issue more valuable than the cash dividend.

Property funds are particular fans of this strategy, as it helps them retain cash and reduce debt. This has worked for NEPI Rockcastle, where holders of nearly 85% of the shares in the company elected to receive a scrip distribution rather than a cash distribution.

Also, the company has secured five-year “green” portfolio financing of €200 million, which will be used to pay down the revolving credit facility that was utilised for recent acquisitions. This will restore the revolving credit facility to €620 million.

NEPI Rockcastle has now reduced its gearing below 35%.

Oceana completes the sale of Commercial Cold Storage (JSE: OCE)

The deal was implemented on 4 April 2023

Oceana has concluded the transaction to sell Commercial Cold Storage Group to a consortium of buyers that includes a large infrastructure fund and various other parties. These consortiums can sometimes change during the course of deal implementation, like in this case where an entity linked to Mcebisi Jonas has replaced the previously announced B-BBEE partner.

With all conditions precedent now fulfilled or waived, the R760 million deal is effective.

Little Bites:

Director dealings:

Value Capital Partners has bought another R35.6 million worth of shares in Sun International (JSE: SUI) and shares in Metair (JSE: MTA) worth nearly R34 million.

An associate of a director of Hudaco (JSE: HDC) has sold R25.4 million worth of shares as part of a diversification plan. The shares were originally related to a sale of businesses to Hudaco.

The CEO of Standard Bank (JSE: SBK) sold all the shares received under an employee share scheme (even the shares received after tax) and then sold another almost R10 million worth of shares for good measure.

I’m not sure what the plan is at Conduit Capital (JSE: CND), but there are two new directors on the board, one of whom is part of a private investment company in the US.

One needs to be careful with bland cautionaries. In these announcements, companies tell the market that something is going on that might be material, but there are no details. It’s rare to see two in one day, with Finbond (JSE: FGL) and Primeserv (JSE: PMV) both releasing such announcements. It’s inconceivable that the companies are talking to each other, so I think the timing is a coincidence.

Richemont’s (JSE: CFR) decision to simplify its listing structure was approved by shareholders, with the depository receipt programme in South Africa being abandoned in favour of Richemont’s A shares being listed on the JSE as an inward listing.

Shoprite (JSE: SHP) has become the latest company to list on A2X, an exchange that provides a secondary venue for trading of shares. This means that the JSE remains the primary regulator of the listing, but the shares can be traded in more than one place.

The chairman of AYO Technology (JSE: AYO) – Advocate Wallace Mgoqi – has sadly passed away. This isn’t a happy time for the board of AYO, with the settlement agreement with the PIC having dominated recent headlines.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In this sixteenth edition of Unlock the Stock, CA Sales Holdings returned to the platform to discuss a seriously impressive set of results. Still in its infancy as a separately listed company, CA Sales Holdings is making waves as a mid-cap group worth paying attention to. As ever, there was a management presentation and interacted Q&A session to enjoy.

Use the link below to enjoy this great event, co-hosted by yours truly, Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions:

Advanced Health needs to make SA profitable (JSE: AVL)

Losses have worsened in the South African business

Advanced Health’s business in Australia is profitable. It is also in the process of being sold for around R522 million.

This leaves the group with its South African business, a day hospital operation (see what I did there?) that could do with a few procedures itself. In the six months ended December, it lost R23.1 million vs. a loss of R21.9 million in the comparable period. Although the company attributes the negative trend to higher finance costs, the reality is that the business model is clearly not working.

There are various strategic initiatives highlighted in the earnings release to try and improve matters in the local business. Reducing group debt will help as well!

The Daily Maverick forces AYO’s hand (JSE: AYO)

Full marks to the publication for its role in the disclosure of these terms

When AYO Technology first released an announcement about the settlement with the Public Investment Corporation (PIC) and Government Employees Pension Fund (GEPF), they gave almost no details.

At the time, I wrote:

“There is now an “amicable” conclusion of a settlement agreement, but the terms are confidential. This is surprising, because AYO shareholders now have no idea what the settlement looks like and what the financial impact will be.”

Thanks to the existence of media houses like Daily Maverick who are investigative journalists rather than market commentators and analysts, AYO didn’t get away with this. Tim Cohen and Neesa Moodley published an article that was clearly painful enough for AYO that disclosure became necessary, with some pressure presumably applied by the regulators as well.

The Daily Maverick reports that a R4.3 billion investment was originally made at R43 per share for AYO shares. The company traded at R4.78 at close of play on Monday, so this hasn’t exactly been a lovely investment.

AYO will repurchase 17.2 million shares for a total amount of R619 million. That’s not too bad actually, implying a price per share of R36 that is vastly higher than where AYO is currently trading. After five years, the GEPF can sell another 5% of its stake at the higher of R20 per share or 90-day VWAP. Call me a skeptic if you must, but I would wager which of those two numbers will be higher.

The GEPF will retain a stake of 25.01% in the company. Lucky them.

The arbitrage was obvious at Cashbuild (JSE: CSB)

Theodd-lot offer ended up being more than twice the expected size

Fun fact about the market: it’s full of smart people who like making money. When there is the ability to buy an odd-lot of shares (fewer than 100) and have them bought from you a couple of weeks later at a tidy profit, many punters happily play the arbitrage and put some money in the bank. The profit per trader is obviously limited, as it can only be made on fewer than 100 shares per account, but it can add up to a lot for Cashbuild.

When the odd-lot offer circular was released, there were 40,493 shares that were held by investors who each had fewer than 100 shares. By the time the deal was concluded, Cashbuild repurchased 89,164 shares.

Goodness knows it won’t break the bank at Cashbuild, but the total value ended up being R17.6 million when it should’ve been less than half that amount. I hope their calculation on the cost savings took into account the arbitrage and the number of shareholders who would jump onto the register purely to be taken out at a premium.

There’s more good news at EOH (JSE: EOH)

The debt package with Standard Bank has been refinanced

There’s a definite shift in momentum at EOH, with the company emerging from a rights offer with a far better story than before. That doesn’t help those who held before the rights offer, but it might help those who bought afterwards.

In very encouraging news, the company has refinanced its debt package with Standard Bank and words like “normalised debt structure” are now being used. They have also “significantly lowered the cost of debt” for the group, which is more good news.

If you’re wondering what a sustainable debt structure looks like, here are the details:

R200 million 4-year amortising term loan (therefore capital and interest repaid over four years)

R250 million 3-year bullet term loan (interest paid for three years and the capital right at the end)

R250 million 4-year revolving credit facility (a bit like having an access bond)

R500 million general banking facility including working capital and ancillary banking facilities (essentially a huge overdraft)

Glencore tries to swoop in on Teck (JSE: GLN)

For now at least, the Canadian company has told Glencore where to go

Teck is one of Canada’s leading mining companies, with a focus on copper, zinc and steelmaking coal. The company is currently busy with a restructure of its operations and different classes of shares, which Glencore clearly saw as an opportunity.

Later this month, Teck shareholders will vote on a proposed spin-off of the steelmaking business and a sunset clause on the voting rights held by the super-voting Class A shares. This doesn’t leave Glencore with much time to win over the Teck board, with the initial Glencore proposal strongly rejected by Teck in this press release.

Glencore’s proposal is a merger of the companies, followed by a demerger to create two distinct groups. One would be the “dirty” business with coal and ferroalloys and the other would be the clean(er) business with transition metals like copper.

At the proposed ratio, Glencore shareholders would own 76% of the entities and Teck shareholders would own 24%.

Glencore reckons that synergies worth $4.25 billion and $5.25 billion would be achieved through this deal. This is estimated on a net present value basis.

If you want a wonderful example of corporate finance at the very top end of the market, here’s the letter sent by Teck to Glencore that politely tells them to get lost.

Hammerson sells at a discount to book value (JSE: HMN)

This won’t do much to improve sentiment

Hammerson has had some bad press recently, mainly because Resilient is upset that the company isn’t paying a dividend. In my view, that’s why listed companies shouldn’t own minority stakes in other listed companies. If you don’t have control or at least significant influence over the asset, you shouldn’t be earning a fee as a listed management team to own it.

Moving on, the latest news from Hammerson might not help matters. Although the company is making progress towards its asset disposal target to reduce debt, the latest sale is at a discount to book value – a 4% discount, to be exact. That’s a lot better than the discount that most property funds trade at, but it still calls into question the accuracy of the portfolio book value.

The latest sales are worth €164 million, taking the group closer to the target of €500 million worth of disposals by the end of 2023. Around €360 million worth of disposals have now been achieved. Headline LTV (a measure of gearing) improves to 36% as a result of this disposal.

A bonanza for shareholders in Industrials REIT (JSE: MLI)

Themother of all offers has landed from Blackstone

You won’t see a 37.5% rally in a share price very often, even when there’s a potential offer on the table. A premium in an offer is normal, but this is a particularly juicy one at Industrials REIT.

I’ve covered Sirius Real Estate (another industrials fund) in an update below, so it’s fun to plot the two on a chart:

Even with this mammoth offer for Industrials REIT, the share has lost value over the past year!

Blackstone may make an offer of 168 pence per share (yes, denominated in GBP), a premium of 40.6% to the one month volume-weighted average price (VWAP). If Blackstone pulls the trigger on the offer, the board of Industrials REIT will unsurprisingly recommend it to shareholders. A due diligence is underway as we speak, which will need to be finalised before an offer is made.

Investec amends the ManCo internalisation (JSE: IPF)

I guess that the institutional shareholders agreed with my sentiments here

I went back and read what I wrote about this Investec Property Fund ManCo deal when the news first broke. I talked about investors being fleeced of their capital and I stand by that view.

Institutions seemed to agree, putting pressure on the fund to temper its enthusiasm in paying a fortune to the ManCo. The deal isn’t much better for shareholders, but at least some of the purchase price has become an earn-out.

The fund starts off the announcement by noting strong support from investors for the strategic rationale of the deal, which isn’t the same as support for the price. Of the proposed price of R975 million, R125 million is now subject to an earn-out arrangement rather than being a guaranteed part of the price.

The measure for the earn-out is growth in assets under management, which feels like completely the wrong measure to me. All that is being encouraged here is capital raising activities, not great returns for shareholders.

There is also a note that Investec (the recipient of this wonderful amount of money) will contribute R45 million to the fund for management retention, IT systems and rebranding.

Shareholders controlling 36.2% of the voting rights in the company have agreed to vote in favour of the deal. The fund needs to achieve 50% approval for this deal to go through. Investec and its associates obviously have a conflict of interest here, so they can’t vote.

The circular should be released on 17 April or thereabouts.

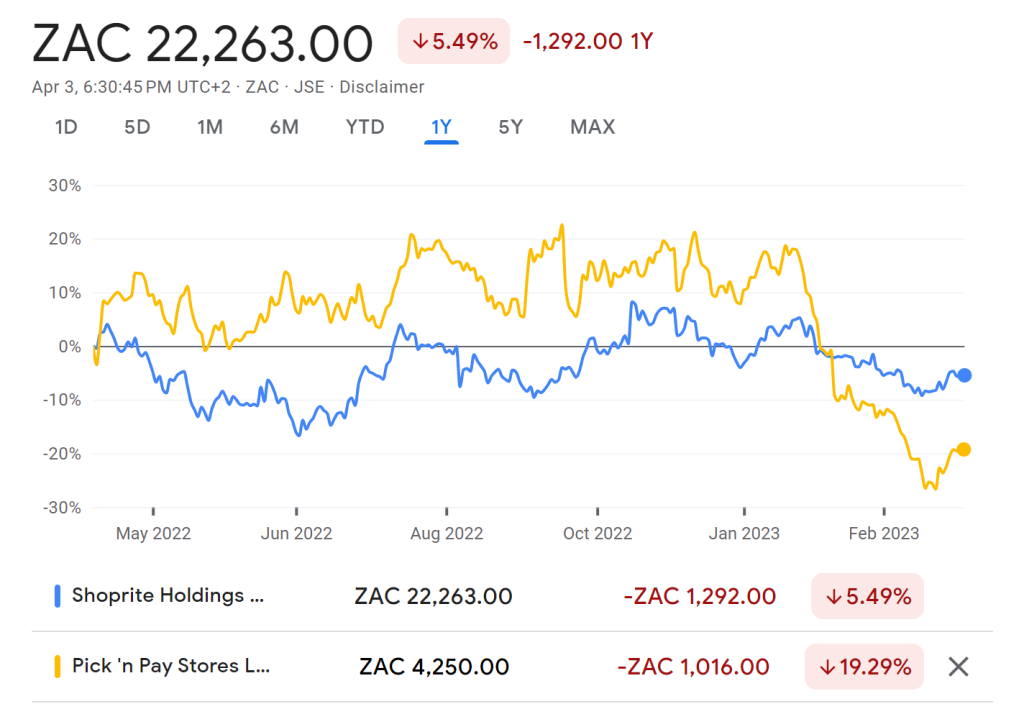

Pick n Pay will need the power of Star Wars Day (JSE: PIK)

May the 4th be with shareholders when these results come out

After the close on Monday, Pick n Pay released an earnings update for the 52 weeks ended 26 February 2023.

I don’t have much good news for you here, with diluted HEPS (excluding business interruption insurance and hyperinflation in Zimbabwe) down by between 12% and 18%. Ouch.

The cost of diesel generators has had a “significant influence” on these results, which I can certainly believe based on other retailers. As a mitigating factor, the retailer managed to hold gross margins constant in a really tough environment and they seem to be happy with trading expenses.

We will only know the full story when results are released on May 4th. We will at least know what the market thinks on Tuesday morning when trade opens after the market digested these numbers.

Although not directly comparable, Shoprite managed to grow its HEPS by 10.2% (excluding the discontinued operation in the DRC) for the 26 weeks to 1 January 2023. I would argue that the Shoprite result is made more impressive by the time period, as it included an even more concentrated period of load shedding.

I wouldn’t want to own either retailer in this environment, but I don’t expect the relative underperformance of Pick n Pay over the past year to reverse:

Sirius recycles more capital above book value (JSE: SRE)

Thelatest sale is a mixed-use property in Germany

Listed property funds usually trade at discounts to net asset value (NAV) per share. There are exceptions and I’m always worried when I see them, as investors get burnt more often than not by buying above NAV.

You wouldn’t buy a house in your area for 20% more than it’s worth, so why do it with a listed fund?

I wrote about Sirius Real Estate often during the pandemic, warning about buying at such an inflated valuation. The share price chart looks like a rather exciting mountain biking race, which isn’t what you want to see as an investor:

The company is focused on justifying its NAV to the market, as evidenced by the latest announcement regarding the sale of two properties. It’s one thing for the directors to tell us what a property is worth. It’s quite another for them to demonstrate it through sale.

The latest example is a mixed-use property in Germany that was acquired by Sirius in 2007. It has been sold for €8.8 million, a price that is 5.3% above book value.

Sirius has disposed of 6 properties in the past year at an aggregate premium of 25% to the net book value. In case you’re wondering about whether there was an outlier driving this outcome, each sale was at or above book value.

The proceeds were invested in three new sites in Germany, which are generating higher revenues than the properties disposed of.

It’s a good story, which is why the share price closed 4% higher. Can these sales be extrapolated to the rest of the portfolio? Perhaps that’s the biggest question of all.

Little Bites:

Director dealings:

Value Capital Partners has bought shares in ADvTECH (JSE: ADH) worth roughly R42.5 million. They have representation on the board, hence it comes through as director dealings.

I don’t usually report on employee share option trades, unless I spot something unusual. It’s common for executives to sell shares to cover the tax obligations on these share awards. In the case of Woolworths (JSE: WHL) CEO Roy Bagattini, he only sold enough shares to cover half the tax obligation, which means he paid half the tax from his own pocket (seems to be R6 million) and kept more shares than usual. That’s a director purchase in my books.

An associate of a director of Ascendis (JSE: ASC) has bought shares worth R176k.

Here’s a fun one for you: Grindrod (JSE: GND) no longer needs a property in London as the operations in the UK have been spun-off. The Grindrods (yes, you read that correctly) are buying the residential property from Grindrod for the tidy sum of R35.6 million. What does this get you in London? Two bedrooms. Yes, two of them. I’ll continue taking my chances in Cape Town, thanks. Jokes aside, the property was only on the balance sheet for R6.6 million, so there’s a juicy profit on disposal here!

ArcelorMittal (JSE: ACL) has appointed Siphamandla Mthethwa as the company’s new CFO. He is currently the CFO of Airports Company South Africa.

The chaos continues at Pembury Lifestyle Group (JSE: PEM) where a legal letter from the firm acting as company secretary set out various allegations against the company. This led to the resignation of three independent directors in March. The company has announced their replacements, also highlighting that the allegations by the company secretary have been announced on SENS as part of the company trying to clean up its act.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Absa announced a B-BBEE deal that I strongly feel is a missed opportunity, as no shares are being made available for investment by retail investors.

RCL Foods is selling vector logistics, a company that has been considered non-core for a while, to an emerging markets infrastructure fund linked to an investment house in Denmark.

Metair surely has the worst luck of any company on the JSE, with a horrible year capped off by the interim CEO being in an accident and the earnings roadshow being postponed.

York Timber needs to improve its operations and quickly, reporting poor numbers that make me question whether we might see another equity raise at some point in time.

Nampak now has a Chief Restructuring Officer and it looks as thought a rights offer will need to go ahead, although we still don’t know how big it will be.

EOH has been to hell and back, but the company may well have bottomed here based on the latest results.

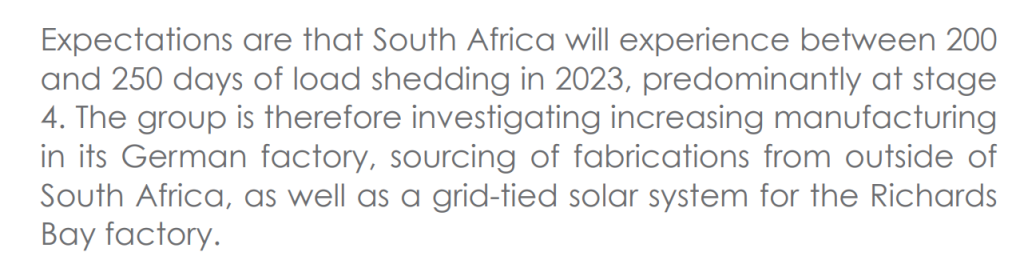

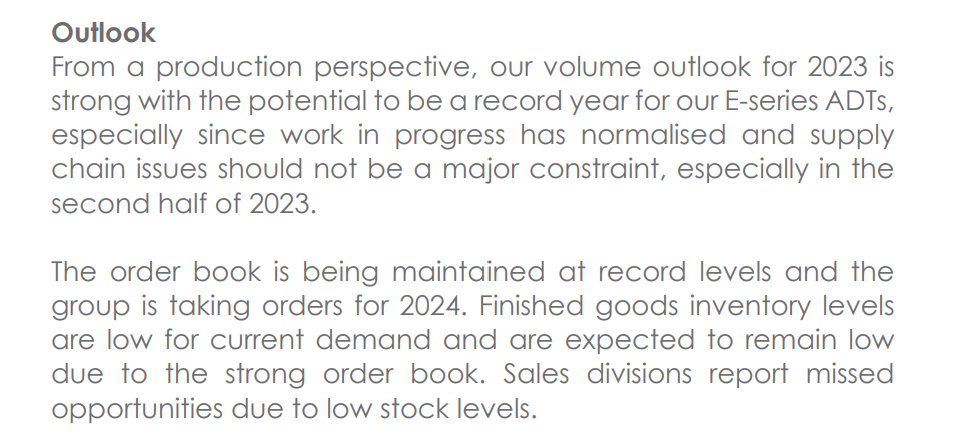

Bell Equipment has released excellent results and a strong outlook, along with a depressing paragraph in the earnings about the impact of load shedding on its local manufacturing strategy.

Barloworld is enjoying strong demand in the equipment businesses (outside of Russia), but is struggling with margins in the Consumer Industries segment.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

After Old Mutual’s recent deal, I was quite chuffed to see the headline on SENS about a new B-BBEE deal at Absa. The investable universe of listed B-BBEE structures is tiny and offers very little in the way of industry diversification.

Disappointingly, Absa isn’t improving the situation.

A 4% stake will land in the hands of a CSI trust and 3% is going to a staff trust. This is an R11.16 billion deal that Absa says will sustainably take its Black Ownership (as defined in the Codes) above 25%.

Interestingly, 82% of the scheme will be attributable to Black staff, which gives a sense of the underlying demographics in the group. There will essentially be a “kicker” for Black staff in the form of a larger allocation than for non-Black and foreign counterparts.

The CSI trust will focus on education and youth employability, both of which are critically important to the future of our country.

The funding structure includes a sizable portion of equity linked to existing shares held by Absa that were received from the Barclays separation, as well as preference share funding of R4.5 billion at 72% of prime and mezzanine funding of R1.7 billion at 90% of prime.

With only 55% of the value of the special purpose vehicle holding the shares funded by the senior and mezzanine preference shares, the level of gearing is reasonable from the outset. Long gone are the days of 100% geared structures using external bank funding, the only beneficiary of which was usually the bank providing funding that was in any event guaranteed by the corporate doing the B-BBEE deal.

There will be a substantial IFRS 2 charge linked to the equity portion of the structure, which will drop Absa’s headline earnings by over 3%.

Widening losses at Advanced Health (JSE: AVL)

The numbers are going the wrong way

Advanced Health is in the process of selling the PresMed Australia business, having received a resounding approval from shareholders for the deal.

The group needs to achieve a turnaround in its profitability, as a trading statement confirms that the headline loss per share for the year ended December 2022 will be 27% worse than the comparable period, coming in at -4.18 cents per share.

Importantly, this is a headline loss from continuing operations, so there is much work to be done.

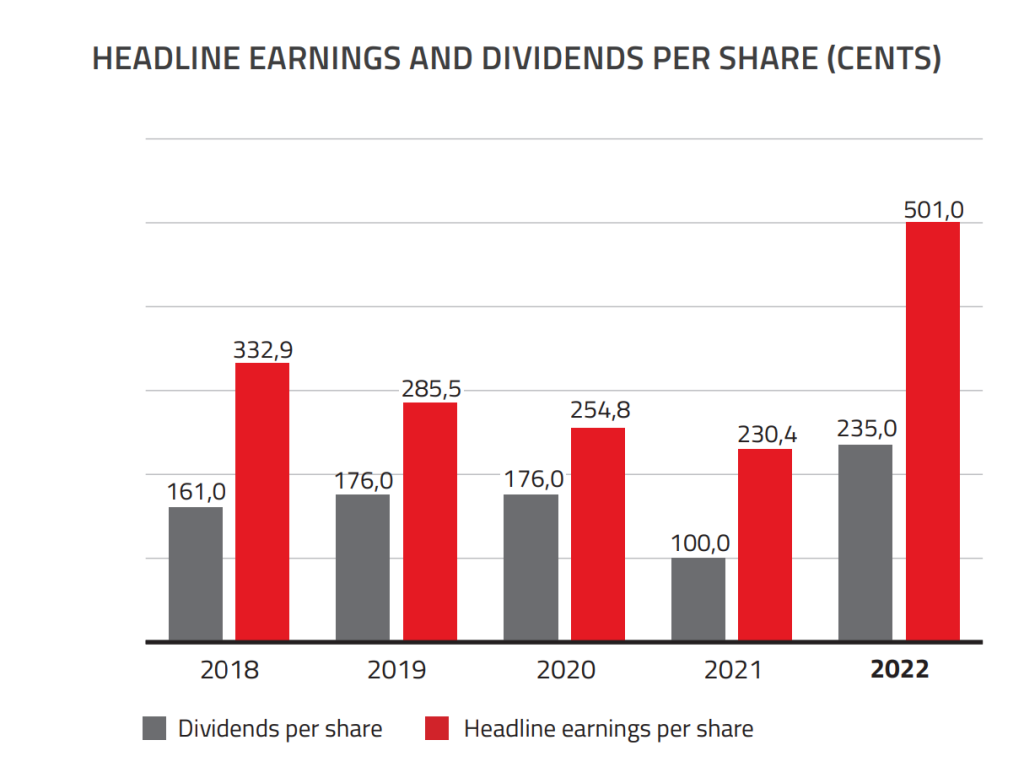

Bell signs off on a wonderful year (JSE: BEL)

The share price is up 170% over 3 years but is still at a modest multiple

If you can get the timing right in cyclical businesses, you can make serious money. You needed a crystal clear ball, not just a crystal ball back in 2020 in the height of Covid to know that the commodity sector (and related industries) would do well. If you had one of those (or just made a lucky guess), you would really be smiling in Bell Equipment.

In the year ended December 2022, revenue increased by 28% and HEPS was good for 61% growth. The dividend per share surpassed both those growth rates, up 80%. I wouldn’t describe Bell as a cash cow though, as HEPS was 473 cents and the dividend was 90 cents, so the payout ratio was only 19%.

The required investment in working capital is part of why Bell can’t pay huge dividends. Group inventory increased by 31% to support sales, which in absolute terms means R1.1 billion worth of shiny yellow equipment that inspires many toys at the local toy store. Full disclosure: yellow earthmoving equipment is Toddler Ghost’s absolute favourite thing in the world.

At a closing price of R17.25 per share, this puts the company on a trailing Price/Earnings multiple of just 3.65x. The dividend yield is appealing but not as high as some other JSE companies, trading at 5.2%.

There’s a paragraph linked to load shedding that really lays bare the impact of Eskom on our economy:

But to cheer you up a bit on this Monday, here’s the all-important paragraph from the outlook section:

This Bell might be ringing for a while still…

Caprec: revenue up, profits less convincing (JSE: CTA)

A long-term view is needed here on Capital Appreciation

Capital Appreciation offers products and services that are in fast-growing industries. That’s a good thing. Sometimes, this requires substantial investment to maintain a solid position in the market and to keep growing. That is hopefully only a bad thing when viewed through a short-term lens.

It’s been a wobbly of a year for Capital Appreciation, with the impairment of the GovChat loan scaring off some investors and leading to others increasing their positions in a time of market volatility. Perhaps more of this will happen when results are released in June.

In the meantime, the group has given an update on the year ended March to try and limit any surprises when detailed results come out.

In the Software division, there has been “exceptional revenue growth” but there has also been a significant increase in headcount and business development spend. This has led to some contracts being won that will only pay off in the next financial year, so there is a warning here about the impact on profits for the financial year that just ended.

There’s also a cautious update on the Payments business, which has experienced double-digit growing in terminal volumes but has seen a change in sales mix towards lower-priced terminals, which has a negative impact on profits.

The group has also reminded the market that the balance sheet has no debt and is in a strong position.

The management team has given the market ample warning here that revenue for FY23 will look good and profits will be under pressure. Despite this, there’s every chance of share price volatility when the results are eventually released.

The company recently joined us on Unlock the Stock, an incredibly useful resource for you to learn more about Capital Appreciation (and Afrimat from the same event):

Kore Potash needs to get its projects across the line (JSE: KP2)

The company needs to raise funds before the fourth quarter of 2023

Kore Potash has released its financial results for the year ended December 2022. The company’s focus is primarily on the Kola project in the Republic of Congo. You may recall that the Minister of Mines got grumpy with the company about lack of progress at the project, even leading to the address and release without charge of two senior employees.

A few visits to the Congo later and things seem to be ok on that front. That’s just as well, because the company doesn’t have sufficient working capital for the next 12 months and needs to get its project across the line. Net outflows for the year were $5.7 million and the cash balance is $5 million. You don’t need your calculator to help you see the problem here.

Thankfully, a lot of progress has been made on the project. The Engineering, Procurement and Construction (EPC) contract is being negotiated and this is a complicated piece of work. Remember, contracts can sink construction companies if they go wrong, so the counterparty (SEPCO Electric Power Construction Corporation) is taking its time to get it right. To try and reduce risk, Kore Potash has requested SEPCO’s parent company (PowerChina) to provide contract guarantees, including performance and retention bonds.

The good news is that the Summit Consortium has a lot of patience. The deal with Summit goes back to April 2021, with a plan for the consortium to provide funding for the project once the EPC is concluded. This has taken longer than expected, but Summit has confirmed that it is still very interested in the project and can provide the full construction funding within 6 weeks of the EPC being finalised.

The share price closed 5.9% lower on thin volumes, so I wouldn’t read too much into that.

This OUTsurance exec is getting something out (JSE: OUT)

OUTsurance is increasing its stake in the Aussie business

Australian corporate actions seem to be all the rage again on the JSE. It’s just a coincidence really, but it shows how many South African corporates have historically invested in the land of kangaroos and broken retail dreams.

Success has been rare, but OUTsurance seemed to get it right by starting Youi from scratch in 2008. It’s quite incredible that a business started in widowmaker Australia at the onset of the Global Financial Crisis has turned out to be a success.

So successful, in fact, that an OUTsurance executive with a 5.3% interest in the company (built up through share options during his time as CEO of the Aussie business) is selling half of that stake to the mother ship for A$36 million. OUTsurance also has a call option to buy the rest of the shares by 31 October 2023. The valuation methodology has been agreed but not the actual valuation, as earnings will vary between now and then.

OUTsurance already owns 89.8% of Youi before taking into account this stake. Full ownership surely isn’t far away.

Renergen recaps the quarter (JSE: REN)

Like in a bad relationship, the wells aren’t communicating

I learnt a new term from Renergen in this update. With the company talking about 5 successful wells within 100 metres of each other, the term is that they “aren’t communicating” i.e. aren’t connected, so each one is giving separate access to gas. This is important as the Reserve Report assumed 300 metres of distance between wells, so this suggests that more wells may be possible than initially thought.

As CEO Stefano Marani discussed on a recent podcast with me, Renergen is not exposed to load shedding. The power feed is directly from the main 132kV line. That’s a significant advantage in South Africa.

The LNG system achieved initial production in September 2022 and liquid helium (Lhe) production was achieved in January 2023. The modules for LNG and Lhe are now being integrated. Although not part of this quarter, the company noted that LNG delivery and gasification was commissioned for Ceramic Industries in October 2022 and Consol (now Ardagh Glass Bottling) in November 2022.

Of course, all eyes are on Phase 2 of Renergen’s story, which is the capital-hungry phase that will turn the company into a scale producer of helium. There are several operational milestones in this regard but the most relevant in my eyes is the debt raise with the United States Development Finance Corporation and Standard Bank. The combined debt is $750 million.

One of the risks here is completely outside of Renergen’s hands: the potential falling out of South Africa with the US government over relations with Russia. We are playing a risky political game as a country and the risk of this scuppering the debt raise isn’t zero.

The share price has come under great pressure as many retail investors learnt the hard way that junior mining requires loads of capital:

A critical time for Tongaat Hulett (JSE: TON)

There’s a lot happening between now and June

Tongaat Hulett is in business rescue and its shares are suspended from trading on the JSE because the company hasn’t released its financial statements for the year ended March. Until there is some certainty around the company’s ability to continue as a going concern, those financials can’t be released.

The post-commencement finance facility has been extended to 30 June 2023. This is the funding provided to the business rescue practitioners to enable the company to keep running while a plan is put together. Speaking of the business rescue plan, the release date has been extended to 31 May 2023. I don’t think I’ve ever seen a business rescue plan published in line with the originally communicated deadline.

Perhaps the most important news is that negotiations with existing stakeholders are expected to result in bids being received from equity partners by 26 May 2023.

In operational news, the impact of the floods in Mozambique has been estimated. Approximately 10% of the sugar cane estimated to be crushed by the Xinavane mill during the upcoming season has been lost. At Mafimbasse Estate, the impact is thankfully minimal.

Little Bites:

Director dealings:

The purchase of shares by Value Capital Partners tends to come through as director dealings because they usually have representation on the board. The latest example is a purchase of Sun International (JSE: SUI) shares worth over R65 million.

A prescribed officer of AngloGold Ashanti (JSE: ANG) sold shares worth A$920k (pay attention to the currency there).

An executive of Gold Fields (JSE: GFI) has sold shares worth R3.8 million.

Des de Beer has bought another R1.9 million worth of shares in Lighthouse Properties (JSE: LTE).

Three directors of Grand Parade Investments (JSE: GPL) accepted the mandatory offer by GMB (i.e. sold shares to GMB) worth a total of around R1.4 million.

Sabvest (JSE: SBP) bought another R1.275 million worth of shares in Transaction Capital (JSE: TCP) (this is a director dealing as Chris Seabrooke is on the board of Transaction Capital).

A non-executive director of BHP (JSE: BHG) has acquired shares worth over $58k.

An associate of a director of Astoria (JSE: ARA) bought shares worth R20.7k.

Lighthouse Properties (JSE: LTE) is offering another scrip distribution alternative to shareholders. This gives shareholders the option to receive shares in lieu of a cash dividend. The value for the scrip alternative is €0.01625 and the value for the cash distribution is €0.014625 per share. It’s been interesting to watch Des de Beer build his stake in the company through ongoing buying of shares and the scrip dividend as a kicker.

Gemfields (JSE : GML) gave such a detailed update in March that I had already covered the details in this edition of Ghost Bites. If you want to go digging for more gems in the numbers, be aware that the annual report has been released at this link.

Wesizwe Platinum (JSE: WEZ) released results for the year ended December 2022. There is no revenue yet, so there’s obviously no dividend. It’s all about cash burn, with administration expenses up by 66% to R62 million.

Telemasters (JSE: TLM) is an obscure listed company that holds a variety of networking and data centre businesses. Revenue fell by 5% in the six months ended December 2022. Expenses were also reduced, so there’s at least a tiny operating profit (and I mean tiny). There is still a headline loss per share of 1.02 cents though, an improvement from a loss of 1.68 cents in the comparable period. Weirdly, a dividend of 0.01 cents has been declared.

The circular for Ellies‘ (JSE: ELI) acquisition of Bundu Power will be distributed by 31 May 2023.

Delta Property Fund (JSE: DLT) has achieved shareholder approval for the disposal of Capital Towers in Pietermaritzburg. The price is R65.55 million and the sale is now unconditional.

Europa Metals (JSE: EUZ) released interim results for the six months ended December. The focus here is on the development of the Toral project, not the financial performance of Europa. The mining licence application is due for submission by 31 July 2023. The funding for the Toral project is coming from Canadian explorer and mine developer Denarius Metals Corp in exchange for a 51% stake in Toral project. In other words, investors need to be aware that Europa will not control that project over the long term.

In an unusual update, Sygnia (JSE: SYG) noted that the person earmarked to take the Financial Director role on 1 April can no longer do so for personal reasons. A new candidate will need to be found.

There’s a bit of musical chairs within the Heriot Properties (JSE: HET) stable in terms of where the investment in Safari Investments (JSE: SAR) is held. If you take the view of “Heriot and its concert parties” then there is no change here, as they hold 47.2% in the company before and after the latest deal.

The circular for Sekunjalo’s offer to shareholders of Premier Fishing and Brands (JSE: PFB) has been delayed and will only be distributed on 5th May 2023. Also linked to this group, there’s a delay in the circular for the unbundling of African Equity Empowerment Investment’s (JSE: AEE) stake in AYO Technology (JSE: AYO). That circular will be out on 4th May 2023.

Conduit Capital (JSE: CND) is currently suspended from trading and is in the process of finalising audits of group entities excluding Constantia Insurance Company. The board has also been a game of musical chairs in recent months, with several director changes.

In case you need a reminder of how tiny Visual International (JSE: VIS) is, the company has taken a 20% interest in a property company called Tuin Huis. Before you get excited, that company owns just two houses in Cape Town’s northern suburbs that will be developed as an “Infill Housing Project” – a fancy name for a sub-division, from what I can tell. The CEO of Visual is also a shareholder of Tuin Huis, but the deal is so small that an independent expert isn’t even needed.

London Finance & Investment Group (JSE: LNF), quite possibly the company on the JSE that gets spoken about the least in the market, released results for the six months ended December. The fair value of the portfolio increased by 8%, above the company’s benchmarks of the FTSE 100 (1.9%) and the FTSEurofirst 300 Index (5.7%). The dividend is steady year-on-year at 55 pence, with the rand amount obviously varying vs. last year because of the exchange rate. Liquidity in this stock is almost non-existent.

And finally, if you feel like reading something that will make all your problems feel better, look for the quarterly update by Afristrat Investment Holdings. I wish I could even find the company’s website to include as a link here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")