In this special episode of Ghost Stories, there’s no sponsor. There is no company partnering with me to bring a message to market under normal conditions.

Instead, we find a CEO who was willing to engage with me on very short notice after comments I made in Ghost Mail. Given the circumstances around Transaction Capital at the moment, I jumped at the opportunity.

With David Hurwitz in the hot seat, we talked about:

In layman’s terms, what does SA Taxi do and what are the conditions under which the business performs?

What did Transaction Capital mean about the issues in SA Taxi being “structural” and is this really an accurate view on the industry?

A discussion on how the banks play in this space and why Transaction Capital is different.

Whether there is likely to ever be a viable alternative to the taxi sector and how government could play a role in the industry.

The funding model for SA Taxi and how that balance sheet works, including a discussion on the contamination / cross-default risks and the duration of debt.

SANTACO’s position in this crisis and how they are thinking about the relationship.

Bluntly – is SA Taxi going to be OK and to what extent did the management team see this coming?

An overview of the Nutun business and how it will grow.

How can investors be confident that an SA Taxi-style nightmare isn’t brewing at WeBuyCars?

A discussion on the margins at WeBuyCars in cheaper vehicles vs. more expensive vehicles.

An overview of GoMo and how quickly this business can be built up.

I haven’t edited even a single “um” out of this podcast, so this is the conversation precisely as I had it with David.

As anyone who regularly follows me will know, I hold a long position in Transaction Capital at the time of release of this podcast. Please note that you must do your own research before deciding to enter or exit a position in Transaction Capital, or any other company for that matter!

I hope that this podcast will enhance your understanding of what has happened at Transaction Capital and what could happen in future.

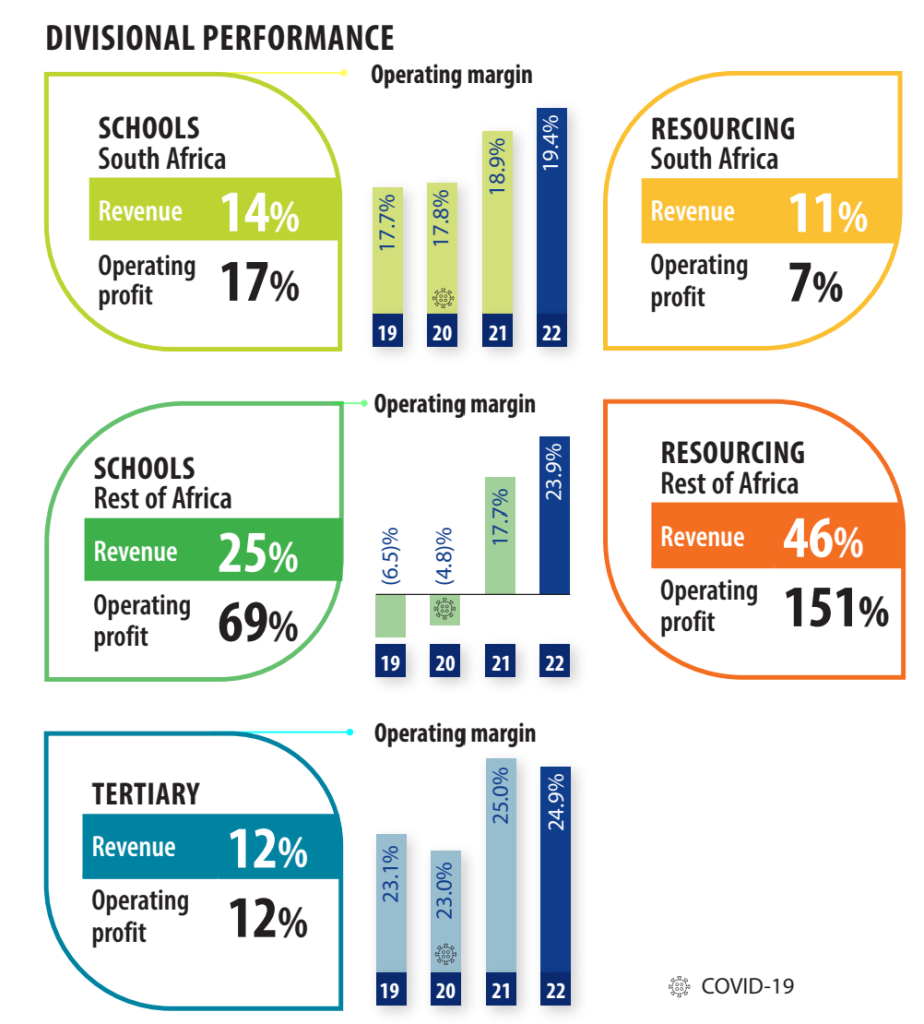

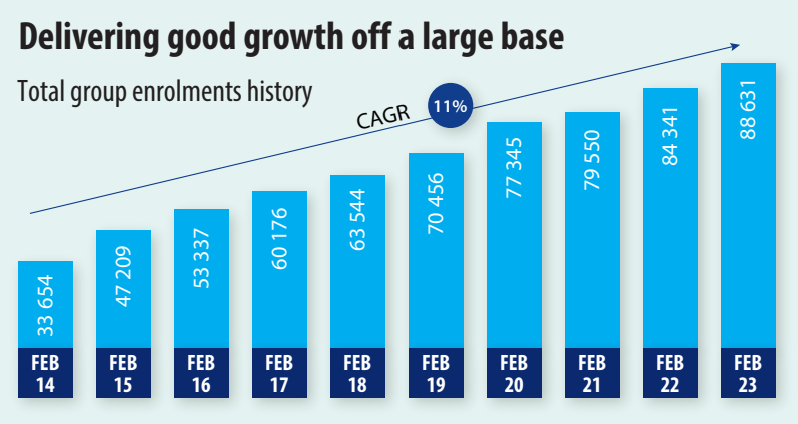

ADvTECH has mastered confusing infographics (JSE: ADH)

I just hope that the kids at the schools get better explanations than this

Credit where credit is due: even with hours to think about how to do it, I doubt I could come up with something more confusing than what ADvTECH has put forward here:

An infographic is supposed to give you a quick understanding of the numbers, not leave you with more questions than answers. After staring at this fruit salad of numbers for a while, you can eventually see what they are trying to do. But yikes, it doesn’t need to be that hard.

To be fair to the company, I’ll include a chart that certaintly speaks my language as a shareholder:

In the year ended December, ADvTECH grew revenue by 18% and operating profit by 20%. HEPS increased by 20% and so did the full year dividend, coming in at 60 cents per share.

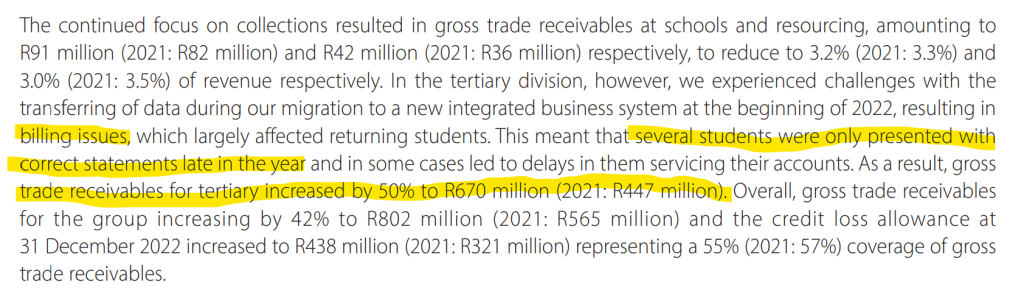

But before we move off this company, I have to point out this exceptionally dicey paragraph buried in the earnings announcement:

It’s great to recognise revenue, but it’s more important to collect it. The group says that the billing system issues have been resolved. I certainly hope so.

But supply chain backlogs are still hurting the business in Latin America

Ahead of results in May, Datatec has released a trading update for the year ended February. This is different to a trading statement that is triggered when earnings will differ by more than 20% vs. the comparable period. This is a voluntary update, something that companies do to keep the market appraised of performance and foster good relationships with investors.

Excluding Analysys Mason which was sold in September 2022, group revenue is expected to increase by 13% for the period. The largest business, Westcon International, grew revenue by 18%. Logicalis International was 10% higher and Logicalis Latin America (significantly smaller than the other divisions) was down 6% as supply chain issues continued for the region.

The good news is that the Latin American business had a better second half to the year, so the momentum into the new financial year is promising.

Fairvest wants to focus on retail (JSE: FTA)

The sale of Indluplace is a major portfolio tilt and will significantly reduce debt

Fairvest released a pre-close presentation that says “coming of age” on the cover page. In this case, this is corporate-speak for “we only want retail assets” – a major shift from the current portfolio exposure.

This is a process rather than something that can be achieved immediately, although the sale of Indluplace is certainly going to help. The expected proceeds of just over R650 million will be used to reduce debt, driving a 500 basis points reduction in the loan-to-value ratio.

There is also R422.8 million coming from properties that have been sold but not yet transferred. Most of them are office properties, as one would expect based on the stated strategy. A couple of them were sold well below book value, with the entire “sold” portfolio coming in at 0.8% below book value.

With 37 assets in the office portfolio, there’s a long way to go. Tenant retention has worsened and so has the vacancy rate. Things just aren’t getting better for this sector.

The emerald market is normalising (JSE: GML)

Still, the pricing achieved at Gemfields’ latest auction has been attractive

Total auction revenues of $21.2 million were achieved at emerald auctions during March, with Gemfields selling 86% of the lots offered for sale. The average price of $7.12 per carat is the third highest price per carat achieved over 21 auctions, so pricing is still looking strong.

Having said that, the management team has warned in the release of results that 2023 will be a year of normalisation and they have reinforced that view in this announcement, highlighting that the market has “normalised appreciably following the exuberance” in 2022.

To give an indication of how volatile pricing is, the prices over the past five auctions varied from $4.01 to $9.37 per carat.

Murray & Roberts gets rid of A$7 million in debt (JSE: MUR)

It’s incredible how listed groups can own such scrappy assets

Thanks to materiality, an accounting concept that determines the level of disclosure required, you have to really dig into financial statements to find all the assets that a listed company owns. It’s only when a corporate needs to clean up its act and its balance sheet that the insects come crawling out of the woodwork.

One such insect even sounds like one, with Insig Technologies being sold by Murray & Roberts for the king’s ransom of A$1. Yes, less than a loaf of bread. Aside from the worthless equity, the important point is that the purchaser is assuming A$7 million worth of liabilities. In other words, Murray & Roberts is making the debt and this business someone else’s problem.

Insig is a Perth-based technology company that made a loss of A$1.7 million for the year to February 2023. It has a net asset value of A$2.9 million. The company needs further investment and Murrays barely has enough money to afford coffee at the staff canteen, so this transaction makes sense.

The buyer is AVID, a name that astonishingly also sounds like a certain little green insect if you pronounce that “A” with all your might.

You can now play in the Premier league (JSE: BAT and JSE: PMR)

Premier Group is now listed on the JSE and Brait has received the proceeds

Brait has announced that in light of food group Premier trading on the JSE since 24th March, it has received gross proceeds of R3.6 billion, which could reduce to R3.5 billion depending on the outcome of the overallotment option of R100 million.

The funds will be used to settle Brait’s R2.1 billion revolving credit facility, with the rest going to working capital and investment needs going forward. That seems like a lot of money left over…

Importantly, Titan (Christo Wiese’s company) holds 31% of Premier, South African institutional investors hold 21%, Brait will remain the largest holder at 47% and Premier’s management team will have 1%. Brait is subject to a 360 day lock-up arrangement but is entitled to unbundle its shareholding in Premier within that period.

There’s no much volume in Premier and I don’t expect that to change until the Brait unbundling, which could still be several months away.

A busy day for Remgro-related corporate actions (JSE: REM)

There are timing updates on the Distell (JSE: DGH) and Mediclinic (JSE: MEI) transactions

With Remgro’s discount to NAV at a higher level than normal, there’s been much talk in the market about how (and if) that would close. There were two updates on the market on Monday that are relevant to Remgro, even though neither of them specifically reference the company.

I’ll deal with Distell first, with the transaction with Heineken set to be implemented in April – May of this year. Some punters in the market are excited about Remgro’s positioning here, which will see it take on AB InBev through the enlarged Heineken – Distell vehicle. Importantly for the discount in the Remgro share price, Distell won’t be listed anymore in a few weeks from now.

Mediclinic is comfortably the largest exposure inside Remgro and there is further progress on the take-private deal here. As you may recall, Remgro and MSC Mediterranean Shipping Company are jointly bidding to take the group private. The Competition Tribunal has now approved the acquisition, with only outstanding regulatory approval being the SARB. Once that is in place, a UK Court will need to sanction the scheme, a milestone that is expected to be reached in mid-May.

Will a greater mix of unlisted vs. listed exposure in the Remgro portfolio help close the discount, or at least get it back to historical levels?

This is a useful reminder of how specialised mining debt can be

Tharisa is a co-producer of platinum group metals (PGMs) and chrome and is listed on the JSE and in London. It has also raised a bond on the Victoria Falls Stock Exchange, which you’ve likely never heard of before.

To add to that capital mix, the company has also put together a $130 million debt facility with Absa and Société Générale. This is a 42-month facility with a term loan of $80 million and a revolving facility of $50 million, secured by commodity offtake agreements.

The last part is also the most interesting part, as it is a reminder that mining debt raises are specialised in nature. The banks look to the commodities themselves as security.

This is a significant capital raise, as the net cash position at the end of December was $101.1 million.

Thungela continues its slide (JSE: TGA)

The share price has lost a quarter of its value this year

Thungela has declared a final dividend of R40 per share. Let’s put that in perspective. At the start of the year, it was trading above R257 per share. It’s now below R192.

This is an excellent lesson in why chasing hot commodity stocks is a fool’s errand. The dividend doesn’t help you if the share price falls sharply.

The full year dividend was R100, but that doesn’t help you much if you bought at the start of this year.

HEPS for the year increased by 97%, coming in at R130.82 per share. The dividend payout ratio was thus 76.4%.

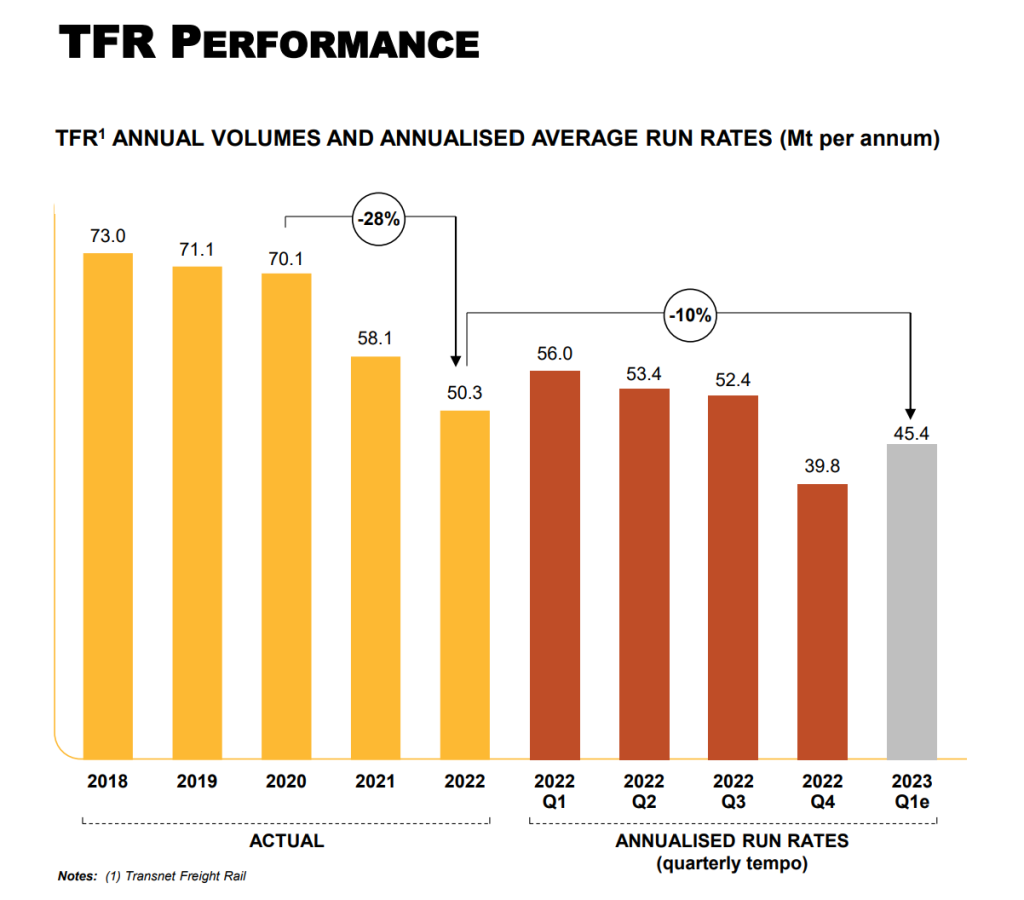

With net cash of R14.7 billion on the balance sheet, there’s no shortage of money here, with R5.6 billion earmarked for the final dividend. But instead of returning the remaining excess to shareholders, the group is on the acquisition trail in an effort to diversify away from South Africa (and specifically Transnet). This is going to lead to debt being raised, which is precisely why investors have gotten cold feet rather than coal feet.

The group has given guidance for 2023 that has been negatively impacted by Transnet Freight Rail. Our infrastructure is so bad that Thungela won’t give guidance for 2024.

Here’s the chart from the results presentation that tells the story of Transnet Freight Rail, which in 2022 recorded its lowest railed volume since 1996:

Vukile bucks the property trend (JSE: VKE)

It’s rare to see property companies raising equity at a discount to NAV

After the heady days of 2015 – 2016, property companies have found life a lot more difficult. With share prices trading at discounts to net asset value, the market screams for buybacks rather than capital raises. Most funds resort to recycling capital by selling assets for attractive prices (or not, in some cases) and reinvesting the capital in other opportunities. With a requirement to pay almost all profits out as a distribution, this can leave REITs in a very tight position where it is tough to grow.

Vukile has clearly had enough, announcing an accelerated bookbuild targeting an equity raise of R500 million. In such a raise, you need to be in the little black book of the advisor (in this case Java) to get a phone call offering you the shares. The offer isn’t open to the general public.

The capital raise announcement was made alongside the release of a pre-close presentation giving details of the performance in South Africa and Spain.

The presentation included the all-important news that vacancies have dropped in South Africa to the lowest point since the company listed in 2004, and the reversionary cycle has turned positive, which means new leases are finally being concluded at higher rentals than the expired lease being replaced.

The news from the South African portfolio almost seems impossibly good, including this comment: “As figures are now comfortably ahead of pre-COVID levels we will no longer be referencing that period.” That’s quite something, referring to both sales and footfall.

Clearly, the lower-income economy is bustling despite what the unemployment rate is telling us. The informal economy is alive and well and those profits get spent at the local mall. Vukile is looking to invest further in this portfolio, acquiring the Pan Africa Shopping Centre in Alexandra for R421 million (phase 1) and R254 million (phase 2), as well as BT Ngebs City in Mthatha for R400 million. Both deals are at an initial yield of 9.25%.

The performance also looks pretty good in Spain, with almost all retail categories ahead of pandemic levels.

Looking to the balance sheet, 88% of group interest-bearing debt is hedged and all FY23 expiries have already been repaid, refinanced or renegotiated. 63% of FY24 debt has also been dealt with in one of those three ways.

Vukile has reaffirmed guidance for FY23 of growth in funds from operations and the dividend of between 5% and 7%.

Woolworths clears a lot of headspace (JSE: WHL)

The nightmarish journey with David Jones is finally over

Woolworths has announced that legal completion of the David Jones sale has been concluded. The proceeds from the deal will be finalised by the end of June, as this is a completion accounts structure that sees the final price vary based on the working capital on the balance sheet at completion date.

Perhaps as a reminder of the pain in case they are ever tempted to do another acquisition like this again, Woolworths will retain ownership of the Bourke Street, Melbourne property asset. It will be leased to David Jones on market-related terms.

R1.6 billion has been returned to Woolworths from David Jones over the past 12 months. Far more importantly, R22 billion in liabilities will no longer be a headache for Woolworths with David Jones off the balance sheet, which will allow management to focus elsewhere.

The value destruction is over and a new broom is certainly sweeping clean at Woolworths. To get to know the current CEO, Roy Bagattini, you could listen to this recent episode of Ghost Stories.

Little Bites:

Director dealings:

Value Capital Partners is related to directors of Sun International (JSE: SUI), so this comes through as director dealings even though it is more comparable to institutional shareholder dealing. Nevertheless, Value Capital Partners has bought over R56 million worth of shares.

A director of a major subsidiary of Clientele (JSE: CLI) has sold shares worth R2.15 million to diversify exposure. That sound plausible, but keep an eye out for any further selling, as Clientele doesn’t often feature here.

A director of Richemont (JSE: CFR) has sold shares worth R2 million.

A director of Motus (JSE: MTH) has bought shares worth R950k.

Associates of directors of Astoria (JSE: ARA) have bought shares worth nearly R820k.

Pepkor (JSE: PPH) has had its credit rating and outlook (stable) reaffirmed by Moody’s. A focus on value products in this environment and its strong liquidity were highlighted as major contributors to this outcome.

In case you ever doubted whether property funds are really just capital structuring machines, Sirius Real Estate (JSE: SRE) has appointed a new CFO who brings many years of experience primarily in investment banking and corporate advisory roles. At property funds, it’s all about the balance sheet.

KAP Industrial Holdings (JSE: KAP) is changing its name to KAP Limited and will retain its existing ticker.

The sole director of GMB Investments (Gregory Mark Bortz – the name now makes sense) has been appointed to the board of Grand Parade Investments (JSE: GPL) along with another new director.

Sable Exploration and Mining (JSE: SXM) has announced that 9.8% of shareholders accepted the mandatory offer from PBNJ Trading and Consulting, leaving that company with a 59.9% stake in Sable.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Remgro reminds us that impressing most local financial commentators really isn’t difficult: just increase the cash dividend, regardless of other capital allocation opportunities.

Steinhoff shareholders are throwing the dice one last time, hoping for a better-than-zero outcome, one that was almost guaranteed under the proposed creditor settlement.

York Timber has seen earnings fall faster than the trees in the forest, proving once more than this company really struggles to reward shareholders consistently.

RFG Holdings seems to be coping under inflation, though the proof will be in the pies rather than the pudding.

CA Sales Holdings is posting really strong numbers in its life after PSG, making a strong case for itself as an attractive mid-cap on the local market.

Master Drilling is almost literally the shovel in the gold rush, benefitting from increased activity in the mining sector.

Bell Equipment is also on the right side of the mining story, with an exceptional rally in the past week as the market realised how cheap the traded multiple was.

Gemfields really is a gem, achieving results in 2022 that are just as beautiful as the emeralds, rubies and wildly overpriced eggs at Fabergé.

Astoria has a story to tell, boasting a portfolio mostly comprised of assets that you can’t get access to anywhere else.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

You’ve gotta love AYO Technology and the rest of the companies in the broader Sekunjalo stable. This is a listed company that was in a material dispute with the PIC and Government Employees Pension Fund (GEPF) over capital that had been invested in AYO.

There is now an “amicable” conclusion of a settlement agreement, but the terms are confidential. This is surprising, because AYO shareholders now have no idea what the settlement looks like and what the financial impact will be.

Nonetheless, the company lifted its cautionary announcement and noted that caution is no longer required to be exercised when dealing in its shares. I would be cautious here regardless of whether there’s an official cautionary announcement or not.

Eastern Platinum launches a major rights offer (JSE: EPS)

The number of shares in issue will double

Eastern Platinum is raising capital for a number of purposes, ranging from the restart of operations at the Crocodile River Mine through to completion of phase 3 of the Zandfontein Concentrator Plant. There are other projects that need capital, like Mareesburg and Spitzkop. Junior mining is expensive!

With a market cap of roughly R343 million, Eastern Platinum is small. It’s about to get considerably larger, is the company plans to raise just over R200 million in this process. With a rights offer ratio of 1:1 (i.e. the number of shares will double) and armed with that knowledge of the market cap vs. the size of the raise, you can immediately tell that the offer price is a significant discount to the current traded price.

The offer price is R1.4564 per share and Eastern Platinum closed at R2.50 on Friday.

A little gem (JSE: GML)

Gemfields achieved record revenue in 2022 against a backdrop of major stress in Mozambique

Gemfields owns and operates the Kagem emerald mine in Zambia, the Montepuez ruby mine in Mozambique and luxury brand Fabergé. The latter is famous for eggs that make your local Lindt selection seem very reasonably priced in comparison. Of revenue of $13.8 million at Fabergé in the past financial year, a whopping $2.2 million came from the sale of the Fabergé x Game of Thrones objet egg.

In the aftermath of the pandemic, the coloured gemstone market has experienced strong demand. The company makes it clear that 2023 may not be as juicy as 2022, particularly against an inflationary and possibly recessionary environment.

In 2022 at least, Gemfields made the most of conditions. Revenue shot up by more than 32% to $341 million and EBITDA came in at nearly $166 million, up 24.5%.

The mix is important here: Montepuez is the largest revenue contributor at $166.7 million, with Kagem up next at $148.6 million. Fabergé contributes $17.6 million and other revenue sources come to $8.2 million.

There is clearly some margin pressure in the system, with the group highlighting fuel costs at the Zambian emerald mine as one example of inflationary cost pressure. In Mozambique, the stress has been more political in nature, with the insurgency in northern Mozambique coming dangerously close to the mine. This risk in Mozambique come with costs as well, as security certainly isn’t free. Group EBITDA margin decreased from 52% to 49%. Kagem came in at 49% and Montepuez at 50%.

As there has been solid support from government in Mozambique when it comes to security, Gemfields seems to feel confident enough to invest further in that region with a second processing plant. The payback period is less than 18 months, which tells you everything about mining in Africa: maximum risk, maximum rewards.

And despite the fancy eggs (and other jewellery) at Fabergé, the luxury brand still isn’t profitable. 2022 saw its lowest ever cash draw from Gemfields (i.e. the least assistance the group has ever needed from its shareholder), so perhaps there is hope. A loss of $3.1 million was reported by that business, which should be viewed in the context of Gemfields group operating profit of $116.5 million.

Despite the big jump in profits, free cash flow was actually slightly down vs. 2021 at $84.4 million. Capital expenditure was a meaty $34 million (vs. $11.7 million), most of which was replacement capex. Shareholders will want to keep a close eye on this, especially as the group expects capital expenditure to increase in 2023.

With worries about 2023, I would personally trim a position in this stock (if I had one) based on this chart and the earnings guidance:

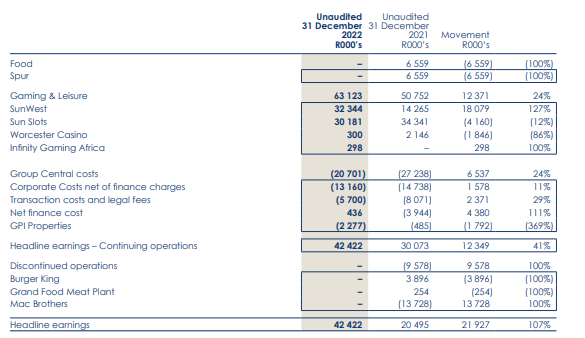

Grand Parade is simpler and better (JSE: GPL)

You just need to look at the right metrics

I really have no idea who writes the short-form announcement for Grand Parade, but I wouldn’t be proud of it if it was me. Inexplicably, it focuses on revenue as the first metric, which doesn’t make sense for a company that now derives its entire value from investments in gaming entities. Grand Parade is firmly an investment entity now, having gotten out of the foods business.

The key line is “profit from equity-accounted investments” at R63 million vs. the silly little revenue number of R3.8 million.

Anyway, moving on from the pointless short-form announcement, we find a really useful table in the results that shows exactly how much the group has changed in the past year:

This is a good lesson in creating cleaner, focused groups. Just take a look at how Mac Brothers was hammering profitability!

There is currently a mandatory offer on the table from GMB for R3.33 per share, a 27% premium to NAV. The last day to trade is 3 April and I’ll be interested to see what happens to the share price thereafter. I’m not sure it should be trading at a premium to NAV under normal circumstances.

Northam: a sharp rise in earnings but no dividend (JSE: NPH)

The group is at a “critical juncture” in its growth strategy

There aren’t many mining houses that managed to improve margins during 2022. With inflationary pressures on mining costs and commodity prices that in some cases went sideways, margins were squeezed for many mining groups.

Not so at Northam Platinum, where operating profit margin in the six months to December 2022 was 290 basis points higher at 45.1%. This means that a 44.9% increase in revenue drove a 55.0% increase in operating profit. At HEPS level, the jump was 67.3%. This is particularly impressive when you consider that the cash cost per equivalent refined ounce increased by 14%.

Of course, the major focus is on the offer to the shareholders of Royal Bafokeng Platinum. Based on the way in which the offer is structured, the split between cash and shares will change depending on whether Impala Platinum accepts the offer from Northam. This uncertainty is why the board has elected not to pay an interim dividend.

The Northam share price has lost nearly a third of its value in the last twelve months. It’s down 22% this year. The market isn’t a fan of risky acquisitions in this environment.

Little Bites:

Director dealings:

There’s some chunky buying underway at Sibanye Stillwater (JSE: SSW), with the CFO buying over R5.5 million worth of shares.

An associate of a director of Transaction Capital (JSE: TCP) has bought shares worth just over R1 million. This is a different director to those who have been doing the buying in the past week.

Directors of gold companies are cashing in on this latest rally, with the latest example being two directors of Harmony Gold (JSE: HAR) who sold shares worth nearly R5 million.

Des de Beer has bought another R640k worth of shares in Lighthouse Properties (JSE: LTE)

There’s yet more director buying at Invicta Holdings (JSE: IVT), with an associate of the CEO buying shares worth R320k.

Montauk Renewables (JSE: MKR) has announced an investment of $25 million in the development off a new gas-to-RNG facility in South Carolina, the group’s first investment in that state.

Accelerate Property Fund (JSE: APF) doesn’t have a great reputation for corporate governance. With the announcement of joint CEOs being appointed with effect from 1 April, we have yet another governance concern. From my perspective at least, a company appointing joint CEOs is a sign that they simply can’t make a decision and don’t trust either of them to fully do the job properly.

As a reminder of how dangerous mining still is, an employee at Harmony’s (JSE: HAR) Kusasalethu Mine near Carletonville lost his life. Sadly, this is still a fairly regular occurrence in this industry.

Telemasters Holdings (JSE: TLM) is one of the most obscure companies on the JSE, with a market cap of just R60 million. In a trading statement that is deserving of such an odd company (mainly because whoever wrote it didn’t bother to mention which period it covers), the headline loss per share will be 39.3% smaller than in the prior period. It’s still a loss, but a smaller one.

Brikor (JSE: BIK) has been party to several legal proceedings for which a settlement has been reached. The announcement doesn’t mention any cash changing hands, but a lot of legal action is being withdrawn by all parties. It seems they have all decided to just go away. Meanwhile, a company called Nikkel Trading 392 now owns 23% in the company.

If you are a shareholder in cash shell Trencor (JSE: TRE), be aware that the annual financial statements have been released.

Accelerate flags a drop in earnings per share (JSE: APF)

Despite this, the share price increased by 8%

When most companies execute a dividend reinvestment plan (the ability for shareholders to receive more shares in lieu of a cash dividend), there’s a reasonable take-up that doesn’t result in materially more shares being in issue.

Not so at Accelerate Property Fund, where the pricing of the reinvestment plan was such that 80% of company shareholders elected the reinvestment plan. We are dealing with some crazy numbers here, as this led to a huge increase in the number of shares in issue by 26.5%!

Of course, this has hit distributable income per share, as the number of shares is so much higher. In a trading statement for the year ending March 2023, Accelerate has flagged a drop in distributable earnings per share of at least 15%.

Ringing the Bell on better-than-expected earnings (JSE: BEL)

A further trading statement gave another boost to the Bell Equipment share price

After navigating a massively tricky period for Bell Equipment and its relationship with the Bell family, the management team has managed to deliver a really good set of numbers. Much like we saw with Master Drilling earlier this week, conditions have been favourable for suppliers to the mining industry.

For the year ended December 2022, Bell’s HEPS will be between 58% and 65% higher. This is considerably better than the guidance in the initial trading statement that envisaged an increase of between 40% and 43%.

This means that Bell’s HEPS will be between 465 cents and 485 cents. The share price closed at R15.80, implying a Price/Earnings multiple of around 3.3x at the mid-point of that range. The market is clearly putting a cyclical multiple on this business, so there’s an opportunity here if you think the cycle still has some way to go.

There’s a new Cell-C-EO in the hot seat (JSE: BLU)

Douglas Craigie Stevenson is gatvoland on his way

Blue Label Telecoms remains a risky play because the management team loves to take a punt at all kinds of things, not least of all Cell C. Just as things were starting to look more settled, the CEO of Cell C has upped and left.

Brett Copans has been appointed as the interim CEO of Cell C, having served as Chief Restructuring Officer at Cell C since April 2022. He has plenty of experience in investment banking, which tells you that Cell C is still more of a financial turnaround story than a telecoms play.

The Blue Label share price closed over 8% lower.

Equites locks in a decent IRR on two properties (JSE: EQU)

Importantly though, the sale was at a price below NAV

Equites has sold two distribution centres for an approximate total of R1 billion. There is an interesting shift in the portfolio here that is worth spending some time on.

Firstly, the focus at Equites is clearly on the weighted average lease expiry (WALE). These distribution centres had remaining lease terms of 5.4 years and 6.3 years, way below the UK portfolio WALE of 15.6 years. So, a benefit of this deal is that the WALE will increase.

Secondly, the money is coming home. Equites will reinvest the cash in the development pipeline in South Africa that has been pre-let with blue chip clients. The company is looking for yield and growth here, something that is harder to come by in the UK.

Equites did well on these distribution centres, realising an IRR of over 13% since acquiring them in 2018. Remember, that’s a hard currency return.

The concern in the market is around the price relative to the valuation in the books. The price is a 7.95% discount to the carrying value of the assets as at August 2022. Does this suggest that the rest of the book might also be due a downward revaluation?

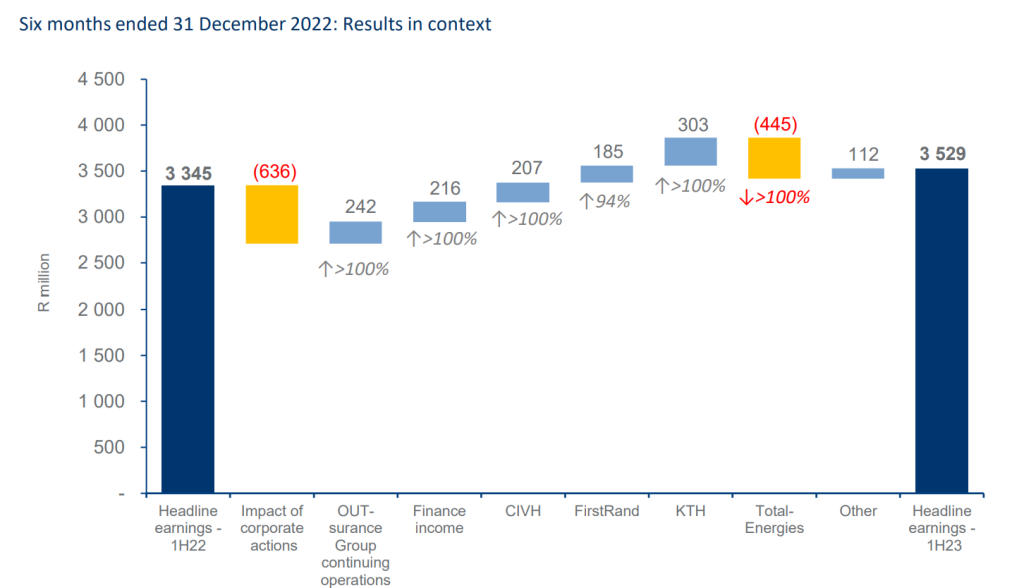

Remgro inches higher in this environment (JSE: REM)

I have serious questions about the capital allocation strategy though

We find ourselves in an environment where it’s better to be a banker than a shareholder, with only a handful of exceptions on the JSE where companies are showing returns that beat the cost of equity.

Remgro is an example of just how tough it is, with the intrinsic net asset value (INAV) up by 5% in the six months to December 2022. This is a director valuation of the portfolio and it equates to R223.86 per share. Remgro is trading at roughly R131 per share, a discount of around 41.5%. Remgro’s share price has fallen by 12.4% over 12 months, so the discount has increased rather than decreased.

With just 5% growth in the INAV, you would’ve been better off with your money in the bank over the past year even if the traded discount to NAV had remained consistent.

There were a number of positive stories in the underlying portfolio, most of which were offset by a huge negative swing at TotalEnergies. The contribution to headline earnings was R301 million in the base period, but this investment registered a loss of R144 million in this period. Although headline earnings isn’t the best metric to assess the performance of Remgro, this waterfall chart is really helpful in understanding how severe the impact of TotalEnergies was in this period:

One thing that Remgro has no shortage of is cash at the centre, with nearly R14 billion in cash of which R7.3 billion is invested in money market funds. I was informed on Twitter that the underlying corporate actions have something to do with the relative lack of buybacks, with only R274 million invested in buybacks in the six months to December. That’s barely a rounding error.

It looks even stranger in the context of the dividend, which has jumped 60% from 50 cents per share to 80 cents per share. Again, at such a big discount to NAV, surely the best use of cash is buybacks rather than cash dividends? The finance textbook would tell you that cash dividends should be zero here. Based on that, I think we can safely conclude that Remgro isn’t run purely with the minority shareholders or finance textbooks in mind.

The discount shouldn’t be a surprise, then.

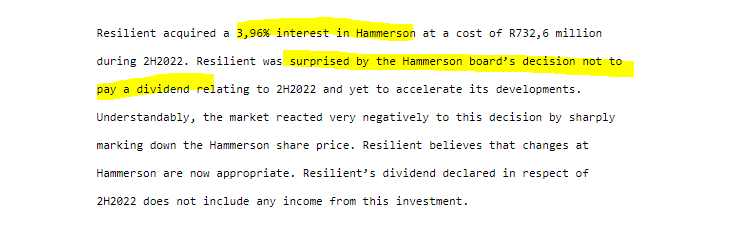

Like all property companies, Resilient is investing in solar (JSE: RES)

The dividend is higher year-on-year if you adjust for the Lighthouse shares

I like the way Resilient describes its strategy: investing in dominant retail centres with at least three anchor tenants and let predominantly to national retailers. If you skip to the prospects section of the latest announcement, you’ll find a note that Resilient plans to right-size department stores (i.e. make them smaller) and increase exposure to grocery retailers. This is a defensive strategy that says a lot about the economic climate.

Resilient has largely lived up to its name, with a dividend that would’ve been 3.8% higher were it not for the unbundling of the Lighthouse shares. But because Resilient no longer receives the dividends on those shares, the dividend declared by Resilient for 2022 is 3.2% lower than the preceding 12 months.

I also quite enjoyed this paragraph, which is a perfect example of why listed companies shouldn’t be running around making silly little portfolio investments in other companies:

Bluntly, companies shouldn’t be allocating capital where they have little or no influence. The last thing I need to do is pay a management team to be negatively surprised on my behalf!

Looking at the numbers, the South African property portfolio grew net property income by 6.0%, but earnings from France were lower than forecast. Despite this, the French portfolio enjoyed a positive revaluation.

At December 2022, Resilient produced 14.6% of its electricity consumption. This is expected to increase to 25% by December 2023.

With energy supply as such a difficult variable and uncertainty around the dividends that Resilient will receive from its listed investments, Resilient has deferred its distribution guidance. Again, what value is the management team adding to these listed investments that introduce even more uncertainty to an already tricky environment?

Schroder’s property valuations fell this quarter (JSE: SCD)

The NAV as at 31 December 2022 has been announced

Schroder Real Estate Investment Trust’s NAV fell by 3.4% between September and December 2022. This was driven almost entirely by a 3.3% decline in the value of the portfolio.

The gearing in the portfolio is manageable (18% net of cash and 30% gross of cash), so this is hopefully just a bump in the road.

An interim dividend of 1.85 euro cents per share has been declared.

Looking for a flood? Ask Sibanye-Stillwater (JSE: SSW)

The universe has a cruel sense of humour with this name

The obvious irony of the name is just incredible: Sibanye-Stillwater has a knack for being on the receiving end of flooding. After too much water caused havoc at the US PGM operations, the latest news is that the company has agreed to provide A$30 million in support to New Century Resources because of flooding in North Queensland.

With suspension of operations for 2 – 3 weeks, the ability of New Century to continue as a going concern has been called into question. Mining is no joke, particularly groups that are completely exposed to a single location.

In case you’ve forgotten, Sibanye is in the middle of a takeover bid for the company that the board of New Century had recommended to shareholders. It’s too late now to run away, as Sibanye already holds 87.64% of the company based on offer acceptances and on-market purchases. Based on this, I suspect that the remaining shareholders will be only too happy to take Sibanye’s offer.

Steinhoff: the choice between zero and probably zero (JSE: SNH)

Surprise! People choose to die later rather than die now

Is there any equity left in Steinhoff? Probably not. Is there a tiny chance that there will be some equity at a future point in time? Sure! There’s always a chance.

The proposed settlement with creditors that would’ve left equity holders with practically worthless unlisted shares was rejected by shareholders. I guess they agreed with my original assessment that such an unlisted stake would be utterly useless. Instead, the shareholders have chosen to give themselves a sliver of hope that perhaps there will be some equity left once the lenders have finished eating the Steinhoff carcass.

Personally, I still think it’s likely that Steinhoff is worthless. Despite this, speculators are buying this thing at around 31 cents per share. I wish them luck.

Little bites:

Director dealings:

The founders of Transaction Capital (JSE: TCP) (Jawno, Mendelowitz and Rossi) pumped another R17.6 million into shares with an average cost of R11.71, helping to drive a substantial rally in the stock of 15%.

A director and a prescribed officer of FirstRand (JSE: FSR) collectively bought shares worth R10.7 million.

An executive of Gold Fields (JSE: GFI) has sold shares worth R1.1 million, selling into the recent strength in the gold price.

An executive of Harmony Gold (JSE: HAR) has also decided that its time to take some money off the table, selling shares worth R717k.

The chairman of Sibanye-Stillwater (JSE: SSW) has bought shares worth R374k.

An entity owned by the Sassoon Children’s Trust – and hence linked to the founders of Sasfin (JSE: SFN) – has bought shares worth R159k. Based on the long-term performance of the company, those kids must’ve been really naughty to deserve that.

A director of Zeda (JSE: ZZD) has bought shares worth nearly R100k.

A director of KAL Group (previously Kaap Agri) has bought shares worth R79k.

The CEO of Super Group (JSE: SPG) has bought shares worth over R68k.

Trustco (JSE: TTO) had its trading suspension lifted by the JSE, as the company now complies with the financial reporting requirements. Nothing happened for hours, until a trade right at the close that took the price 34% higher. I’m not sure that much can be read into that.

Obscure small cap 4Sight Holdings (JSE: 4SI) released a trading statement dealing with the year ended December 2022. HEPS is expected to increase by between 30% and 40.8%.

Life Healthcare (JSE: LHC) has renewed the cautionary announcement linked to the group’s interest in AMG, the European business in the group. Life has received several unsolicited proposals for the asset and is engaging formally with the potential buyers. Of course, it’s possible that no deal will happen here. I must remind you that most M&A opportunities end up failing to go through.

Shareholders of Jasco Electronics (JSE: JSC) should’ve received the circular detailing the offer of 18 cents per share. If you hold shares in that company, make sure you’ve read it.

Rand Merchant Bank (FirstRand) has acquired a 25% shareholding in Remgro’s Ubiquity Energy platform, a strategic energy focused investment vehicle. Ubiquity is the holding company of Energy Exchange of Southern Africa (Energy Exchange). Energy Exchange is a NERSA licensed electricity trader, offering corporate customers an attractive, renewable, alternative source of electricity produced by independent power generators.

Equites Property Fund has sold two distribution centres in the UK to an investment fund managed by New York headquartered Clarion Partners Europe. The distribution centres, located in Peterborough were sold for a cash consideration of £51,81 million. The sale will release net cash proceeds of c. R1 billion, lower the loan-to-value ratio across its portfolio, increase the weighted average lease expiry of the portfolio and enhance the growth profile of distributable earnings per share over the long term.

Capital & Regional Plc has confirmed the sale of its interest in The Mall, Luton shopping centre to SDI (Luton) for £58 million.

Schroder European Real Estate Investment Trust has acquired, for €11m, a freehold industrial warehouse in Alkmaar, the Netherlands, reflecting a net initial yield of 5.6%. Commenting on the acquisition the company said “this was a rare opportunity to acquire a highly sustainable asset with a strong and visible income profile that enhances the Company’s sector weighting, average unexpired lease term and credit strength”.

Sibanye-Stillwater is to provide A$30 million in financial support to New Century Resources following the suspension of operation at the Century mine due to extreme weather impacting Northern Queensland. In February, Sibanye announced a takeover bid to acquire up to 100% of New Century’s share capital through an off-market transaction. The offer will close on 11 April 2023. As of 21 March, Sibanye’s interest in New Century has increased to 87.64%.

Richemont has advised it intends to terminate its South African depository receipt programme and to list ‘A’ shares on the JSE as a secondary listing, in addition to their listing on the SIX Swiss Exchange. If the depository receipt holders approve the termination of the programme and the company obtains the other relevant regulatory approvals, holders will receive one ‘A’ share in exchange for 10 depository receipts that they own. The secondary listing will take place on 19 April 2023.

Following the cancellation of the Premier listing in December and the announcement by Brait in March that it had been approached by investors supporting a listing of Premier, the company will list in the Food Products sector of the main board of the JSE today, 24 March 2023. Investors acquired 65 million shares in an IPO priced at R53,82 per share (excluding the 1,86 million overallotment shares) raising in total R3,6 billion and valuing the company at R6,9 billion (Brait will retain a 47% stake).

On February 6 2023 Cashbuild advised shareholders of its intention to repurchase the Odd-lot Holdings from the Odd-lot Holders. The offer price of 19728.75450 cents represents a 5% premium to the 30-day volume weighted average price of a Cashbuild Share at the close of business on Friday, 17 March 2023. Shares repurchased will be delisted with effect from the commencement of trading on or about Monday, 3 April 2023.

Afrimat’s sector classification on the JSE has been reclassified from the Basic Materials Construction and Materials sector to the General Mining sector with effect from 20 March 2023. The JSE lifted the suspension of trade in the shares of Trustco on 23 March 2023 following the Company’s publication of its audited consolidated results for the 12-month period ended 31 August 2022.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Calgro M3 has repurchased 6 million shares in the open market during the period 15 March to 20 March, 2023. The shares were repurchased at R2.50 per share for an aggregate value of R15 million.

South32 has increased its share repurchase programme by c. $50 million in anticipation of a stronger outlook for commodity prices in the second half of its financial year. This will enable the company to return $158 million to shareholders before September 2023. This week the company repurchased a further 2,627,923 shares at an aggregate cost of A$10,69 million.

Glencore this week repurchased 14,880,000 shares for a total consideration of £65,48 million. The share repurchases form part of the second phase of the company’s existing buy-back programme.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 13 to 17 March 2023, a further 4,453,715 Prosus shares were repurchased for an aggregate €289,18 million and a further 621,447 Naspers shares for a total consideration of R1,91 billion.

Three companies issued profit warnings this week: Transaction Capital, York Timber and Accelerate Property Fund.

Two companies issued or withdrew cautionary notices. The companies were: Choppies Enterprises and Life Healthcare.

Analysis by DealMakersAFRICA of the M&A data for 2022 (excluding South Africa and failed deals) shows 687 local deals were announced across the continent, valued at US$17,53 billion – almost 15% lower than 2021’s deal value.

The slowdown in activity witnessed in the second half of the year was the result of macroeconomic factors such as the war in Ukraine, inflationary pressures and rising interest rates, and while these are likely to keep activity subdued for now, impacting on market sentiment, valuations and the cost of debt financing, it is important to note that the numbers are nevertheless back to their pre-COVID levels. The caveat here, however, is that this is thanks to private capital investors, rather than a return to ‘normal’ pre-COVID conditions.

Private Equity activity continues to grow and, in 2022, it represented two-thirds of the deals announced, valued at $4,67 billion. A closer look at the regional numbers speaks to this rise in private equity and impact investing. The three most active regions – East, West and North Africa account for 97% of these deals announced, and 83% of all M&A activity for the period. In terms of total deals, West Africa continued to dominate, recording $3,29 billion by value, with Nigeria the centre of activity (135 deals). It was followed by East Africa, which recorded deal values in aggregate of $2,88 billion. Kenya was the most active of the East African countries, recording 123 deals of the 162 for the region.

Of the top 10 deals for 2022 by value, the largest was the acquisition in March by MSC Mediterranean Shipping Company of the African transport and logistics business of Balloré S.A. for €5,7 billion (US$6,32 billion). Given the global energy crises, brought to a head by the conflict between Russia and Ukraine, it is unsurprising that five of these deals are energy related.

The awards ceremony was held at Villa Rosa Kempinski on 14 March 2023 and recognised the work carried out by the advisers in the mergers and acquisition and general corporate finance space during 2022.

EAST AFRICA

The winner of the East Africa Deal of the Year was KCB Group’s acquisition of Trust Merchant Bank (TMB). The acquisition provides KCB with an opportunity to tap the immense trade opportunities that come with the DRC’s recent admission to the East Africa Community. Advisers to the winning transaction were Deloitte, Bowmans, Stein Scop and EY.

Amethis Retail’s exit of its investment in Naivas, Kenya’s largest retail chain, was named Private Equity Deal of the Year. The deal estimated to be worth US$151,97 million is c. three times the price paid by the minority shareholders just two years ago in 2020. The advisory firms to the deal were Rothchild & Co., Bowmans, Benoit Chambers, Kaplan & Stratton, PwC and EY.

The following awards were made on the night to the top financial and legal advisers to the East African mergers and acquisition industry:

Mergers & Acquisitions

Financial Adviser by deal value 1st Strand Hanson 2nd Ekta Partners 3rd Stanbic Bank Kenya

Financial Adviser by deal flow 1st tie Standard Bank Kenya and I&M Burbidge Capital 3rd tie Horizon Africa Capital and Ekta Partners

Legal Adviser by deal value 1st Goodwin Procter 2nd Bowmans 3rd Freshfields Bruckhaus Deringer

Financial Adviser by transaction value 1st tie NCBA Investment Bank and Lions Head Global Partners 3rd Verdant Capital

Financial Adviser by transaction flow 1st Verdant Capital 2nd tie Lions Head Global Partners, NCBA Investment Bank and I&M Burbidge Capital

Legal Adviser by transaction value 1st Kaplan & Stratton 2nd DLA Piper Africa | IKM Advocates 3rd tie Anjarwalla & Khanna and White & Case

Legal Adviser by transaction flow 1st Kaplan & Stratton 2nd DLA Piper Africa | IKM Advocates 3rd tie Anjarwalla & Khanna and Mboya Wangong’u & Waiyaki Advocates

WEST AFRICA

The winner of the West Africa Deal of the Year was Access for the formation of Access Pensions. The merger creates Nigeria’s fourth largest Pension Fund Administrator by assets under management, enabling it to leverage the synergies of the merged entities and a wider distribution network. Advisers to the winning transaction were Coronation Merchant Bank, Banwo & Ighodalo, Aluko Oyebode and Jackson Etti & Edu.

The winning Private Equity Deal of the Year for the West African region was Verod Capital’s investment in Medplus. Advisers to the transaction were Stanbic IBTC Capital, Templars, G Elias and Banwo & Ighodalo. The investment was funded by Verod’s Capital Growth Fund III, targeting mid-sized growth companies in Anglophone West Africa, with the primary focus on Nigeria and Ghana. The investment is part of its broader strategy to deepen access and affordability in the healthcare sector.

The following awards were made on the night to the top financial and legal advisers to the West African mergers and acquisition industry:

Mergers & Acquisitions

Financial Adviser by deal value 1st Scotiabank 2nd tie Canaccord Genuity, Durose Asset Management and Treadstone Resource Partners

Financial Adviser by deal flow 1st tie Scotiabank, Stanbic IBTC Capital, Coronation Merchant Bank and Enexus Finance

Legal Adviser by deal value 1st Udo Udoma & Belo-Osagie 2nd White & Case 3rd Olaniwun Ajayi

Legal Adviser by deal flow 1st G Elias 2nd Banwo & Ighodalo 3rd tie Asafo & Co and Aluko & Oyebode

General Corporate Finance

Financial Adviser by transaction value 1st Stanbic IBTC Capital 2nd UCML Capital 3rd Standard Chartered

Financial Adviser by transaction flow 1st United Capital 2nd tie Stanbic IBTC Capital and FSDH Capital

Legal Adviser by transaction value 1st Banwo & Ighodalo 2nd Udo Udoma & Belo-Osagie 3rd G Elias

Legal Adviser by transaction flow 1st G Elias 2nd Banwo & Ighodalo 3rd Udo Udoma & Belo-Osagie

The DealMakers AFRICA’s Special Recognition Award was awarded to the Sanlam Allianz joint venture. This is the second time the award has been made and seeks to acknowledge and showcase a deal or transaction, the characteristics of which are noteworthy and make a significant contribution to the region or industry. This award is not region specific. The joint venture reshapes the African insurance industry involving 27 countries and 12 overlapping countries, creating complexity in terms of valuations, due diligence and regulatory approvals. Advisers included financial, legal and transitional support teams across the continent.

During 2023, DealMakers AFRICA hopes to expand to provide league tables – not only for East and West Africa, but also North Africa. It is anticipated that the next DealMakers AFRICA Awards for 2023 will be held in March 2024 in West Africa.

The latest magazine can be accessed as a free-to-read publication at www.dealmakersdigital.co.za

Against the backdrop of economic stagnation and a predicted recession, a plethora of South African companies are hard at work, searching for innovative strategies to create value and liquidity for their shareholders.

One such strategy is an endeavour to pay its shareholders a donation instead of a dividend, to avoid the mandatory solvency and liquidity test enshrined in section 4 of the Companies Act No. 71 of 2008, as amended (Companies Act).

In terms of Section 46(1) of the Companies Act, a company must not make any proposed distribution unless (i) it reasonably appears that the company will satisfy the solvency and liquidity test immediately after completing the proposed distribution; and (ii) the board of the company, by resolution, has acknowledged that it has applied the solvency and liquidity test, as set out in section 4 of the Companies Act, and reasonably concluded that the company will satisfy the solvency and liquidity test immediately after completing the proposed distribution.

Section 4 of the Companies Act provides that a company satisfies the solvency and liquidity test at a particular time if, considering all reasonably foreseeable financial circumstances of the company at that time (i) the assets of the company, as fairly valued, equal or exceed the liabilities of the company, as fairly valued; and (ii) it appears that the company will be able to pay its debts as they become due in the ordinary course of business for a period of 12 months following that distribution. Accordingly, cash-strapped companies, aware that they may not pass the solvency and liquidity test, may perceive the payment of a donation to its shareholders as a strategy to evade the solvency and liquidity test. However, this strategy will not be permissible in our corporate law framework, as indicated below.

Companies should be mindful that a “distribution” as defined in section 1 of the Companies Act is far wider than the generally assumed concept of a payment by a company of a cash or in specie dividend to its shareholders, as contemplated in subsection (a)(i) of the definition. Boards, therefore, need to ensure that other qualifying transactions, such as a donation, are not overlooked for the purposes of compliance with section 46.

In terms of the Companies Act, the formulation of a “distribution” encompasses, in the first instance, a direct or indirect transfer by a company (paying company) of money or other property to or for the benefit of (i) one or more holders of any of the shares in the paying company or (ii) to the holder of a beneficial interest in shares of the paying company or (iii) in any other company in the same group of companies as the paying company (para (a) of the definition of distribution in the Companies Act). In Henochsberg on the Companies Act 71of 2008, P Delport et al. notes that an “indirect” transfer is a transaction of whatever nature if the substance is the transfer of company property or money to a shareholder without any consideration received by the company.

Donations as a distribution

A company makes a donation by paying money or parting with other assets in instances where the entity is not legally obliged to do so. A donation can also occur in instances where a company enters into a unilateral undertaking with only obligations and no rights; for example, a contract of donation. For the sake of brevity, all such donations are herein referred to as “gifts”.

In Commentary on the Companies Act, 2008, J Yeats et al. posits that gifts made by companies fall into two categories:

a) Category 1: this category refers to gifts that further, realise or are incidental or conducive to a business object (business gifts). Category 1 is extrapolated from Commissioner for Inland Revenue v Pick ‘n Pay Wholesalers (Pty) Ltd (1987(3)SA 453(A) 469), where Nicholas AJA referred to donations made with a ‘business object’; and b) Category 2: this category refers to gifts that are not made in pursuit of a business object and is a gratuitous transaction motivated by benevolence (pure gifts).

In the context of the definition of “distribution” in the Companies Act, it is clear that the making of both business gifts and pure gifts to shareholders would be considered a “distribution” for the purpose of the Companies Act, and the company would be required to comply with section 46 to provide such gifts to its shareholders.

In Commentary the Companies Act, 2008, J Yeats et al. raises the question of whether pure gifts to persons other than in their capacity as shareholders should be regulated by the Companies Act. Based on the above, it is clear that section 46 would not apply, because such gifts would not be “distributions”, as defined in the Companies Act.

They also note that directors would ordinarily have the power to make gifts in accordance with their general powers to operate a company (subject to any restrictions in a company’s memorandum of incorporation). The questions that are raised in such commentary are whether the exercise of such powers by the directors to make a gift is indeed unconditional, and why should the solvency and liquidity standing of the company not be taken into account by the directors before making any gifts? On the basis of insolvency legislation, it would stand to reason that a gift should only be made using the company’s net assets, but what about the liquidity test? The authors note that it would seem improbable that the legislative safeguards offered by the solvency and liquidity test for a “distribution” would not likewise be applicable to the provision of gifts by a company. Therefore, further clarification by legislation is necessary.

Tevin Ramalu is a Candidate Legal Practitioner and Leonard Bilchitz is an Executive in the Corporate-Commercial Department | ENSafrica

This article first appeared in DealMakers, SA’s quarterly M&A publication.

A 15.4% rally in a single day is always a pretty thing

Astoria is an investment holding company that is focused on growing its net asset value over time. The current management team of well-known investors took over in December 2020 and they have done a solid job of growing the NAV ever since. The overall gain in NAV under their watch is just under 130%.

Looking at recent performance, between December 2021 and December 2022 the NAV per share grew by nearly 42%.

Half the trick here is that Astoria’s portfolio includes a number of companies that you can’t get anywhere else. This helps reduce the discount to NAV, as investors hate pyramid structures that feature one listed company holding most of its exposure in other listed companies. This just creates layers of costs and discounting. For reference, see Naspers / Prosus.

For example, 43.2% of the NAV is related to Outdoor Investment Holdings, a niche retailer that has performed very nicely in South Africa. 14% of the NAV is in gaming business Goldrush (through RAC preference shares – admittedly a listed instrument), 11.9% is in Marine Diamond Operations, 10.6% is in Trans Hex and 6.5% sits in ISA Carstens, a tertiary education business.

To round off the portfolio, 6.3% is in Vehicle Care Group (a finance house in the used car industry) and 5.6% is in Leatt Corporation, a home-grown hero that trades over-the-counter in the US.

The NAV per share is R14.06 and the share price closed 15.4% higher at R8.25. That’s still a significant discount to NAV.

Bytes inside your Bites (JSE: BYI)

The company released a short and sweet trading update

Bytes Technology Group gave a light-touch update for the year ended February 2023 as a precursor to the release of detailed earnings.

Gross profit and adjusted operating profit will be approximately 20% higher year-on-year. Interestingly, headline earnings presumably isn’t up by 20% or more, as this would’ve triggered a formal trading statement. It would be a little weird if the company issues a trading statement subsequent to a trading update like this. Weird, but not impossible.

Cash conversion improved in the second half of the year. For the full year, cash conversion was 85% and the group had £73 million in cash. Take careful note of that currency.

CA Sales Holdings is a mid-cap worth watching (JSE: CAA)

How does HEPS growth of 31.2% grab you?

There are some companies on the JSE that are criminally overlooked. CA Sales Holdings is a new kid on the block that has registered share price growth of 29% in the past six months. With the release of results for the year ended December, we can clearly see that the performance supports the share price move.

This is a particularly interesting business that operates in the FMCG industry, helping its clients move goods through the retailers and into the hands of consumers. That sounds ridiculous, unless you have experience in this industry. Trust me, it’s not as easy as you think to navigate retail supply chains and store channels.

With revenue growth of 18.2%, the group’s leverage was on fine display with operating profit up by 32.4%. HEPS increased by 31.2% and the dividend increased by 30.4%, so the cash followed the earnings. That’s perhaps the most important thing to look for.

If you want to learn more about this interesting and clearly successful company, register for the upcoming Unlock the Stock event on 30 March. Management will be giving a presentation on the company and will then take your questions. Attendance is free but you must sign up here>>>

Calgro achieved a substantial share buyback (JSE: CGR)

Mopping up this many shares isn’t easy

Liquidity in Calgro’s stock has always been a challenge unfortunately, something that so many JSE-listed companies can relate to. For some reason, Calgro managed to get R15 million worth of share buybacks away between 15 March and 20 March 2023. The price paid was R2.50 and almost all the volume went through on 20 March, presumably after someone in the market with a meaty position saw the bids at that price.

This represents 4.28% of the company’s issued ordinary share capital and Calgro has authority to repurchase up to 20% of its shares. The share price has lost over a third of its value in the past year.

How bad is Nampak’s balance sheet? (JSE: NPK)

So bad that they need to announce the sale of some equipment

You can tell a lot about a company based on the news that it releases over SENS. At Nampak, the balance sheet is broken. This is why the company has excitedly announced a sale of equipment for cash. At this stage, shareholders will be thrilled to see any improvement to the debt.

Having shut down the crate manufacturing business, the corporate equivalent of a garage sale managed to attract a subsidiary of Mpact to swoop in and buy the equipment. This includes injection moulding and recycling equipment amongst other bits and bobs.

The price is R40 million, so this isn’t exactly a bucket of screws. The book value is only R4.5 million, a reminder that the book value of industrial businesses is largely useless as it is measured on an historical cost basis. Nampak will bank a profit of R35.5 million on this sale.

To put that amount in perspective, the group made a loss of R25.7 million in 2022. Perhaps it should become an equipment trading business?

The R40 million is payable over three months based on certain delivery milestones. Of course, Nampak will put that money straight into the interest-bearing debt that is busy choking the company.

Master Drilling confirms a juicy jump in earnings (JSE: MDI)

In the commodities rush, sell shovels (or drills)

Master Drilling has done very nicely since the lows of 2020. Up over 64% in three years, it is quite literally the shovel in the gold rush. As global commodity prices have supported increased investment in mining exploration, Master Drilling has been a beneficiary.

For the year ended December 2022, HEPS is expected to be between 229.50 cents and 248.60 cents. This is between 20.3% and 30.3% higher than the prior year. The company also mentions its USD earnings, which will be between 8.2% and 18.2% higher. Of course, the rand range looks better because the rand has lost ground over this time.

The share price closed 3.4% higher at R13.90. This is trailing Price/Earnings multiple of 5.8x at the midpoint of the earnings range.

Yes, OUTsurance shareholders get something out (JSE: OUT)

You need to read these numbers carefully

I’m not usually one for normalised numbers, but there’s little choice here. The base period for OUTsurance Group was literally a completely different business. It included Hastings, Discovery and Momentum Metropolitan when the listed company was called Rand Merchant Investment Holdings.

Those businesses are now out of the system, so investors can invest in an entity that is almost entirely comprised of OUTsurance’s insurance businesses. There’s still some legacy stuff in there as well, but it’s minor.

Normalised earnings from continuing operations jumped by 77.7%, driven by gross written premium growth of 17.4%. It’s certainly worth highlighting a strong performance in Australian business Youi, a rare example of South Africans getting it right in Australia.

Insurance is volatile of course, as that’s exactly why people have insurance in the first place. A lower claims ratio was a driver of performance in this period. Steps taken to offset inflationary impacts of claims include higher excesses on power surge and dip claims (thanks Eskom) and pro-active price increases in premiums.

Normalised ROE increased from 23.6% to 29.1%. This shows just how lucrative this industry is.

In major strategic news, the group is looking to expand to the Republic of Ireland. The business interests in Namibia were disposed of. Guinness beats Windhoek, I guess.

An interim dividend of 56.8 cents per share was declared and the share price closed at R33.83.

RFG Holdings seems to be coping with inflation (JSE: RFG)

The focus is on financial performance, not winning market share

This is a wonderful way to learn about price elasticity of demand, which is the way that volumes respond to a change in price. What a company should be doing is trying to find the optimal balance that generates maximum profits. In practice, companies sometimes absorb the pain in their margins just to grow or even maintain market share.

Not so at RFG Holdings, where revenue increased by 7.4% in the 21 weeks ended 26 February 2023 and price inflation was 14.7%. This means that volumes fell sharply, with group volumes down by 11%. The numbers don’t balance because of the Today acquisition which wouldn’t be included in like-for-like numbers.

In terms of market share, the company notes that the volume declines are largely in line with the market movements in those categories. In other words, consumers are buying less from everyone because of pricing pressures.

To make ourselves feel better, we seem to be eating pies. Lots of pies. RFG highlights the pie category as a winner in this period, with a turnaround in the Today business to sweeten the outcome, or perhaps to make it more savoury?

Like all of us, RFG is hoping for a reduction in load shedding. The diesel cost is currently R2 million per week.

Overall, the group seems to be coping with inflation, although packaging (cans and paper) and meat costs are continuing to cause pressure. Despite this, the share price has taken a dive of over 30% this year.

Transaction Capital shareholder movements (JSE: TCP)

The market is desperate for signals at the moment

After the capitulation of the Transaction Capital share price, the market is watching every bit of news very closely. Traders and general punters are looking for institutional investors and insiders buying the shares, as this is a sign that perhaps things will be ok.

For that reason, I’ve included these trades in the main section of Ghost Bites and repeated them in the director dealings section for those who refer back to Little Bites and might miss this news otherwise.

Coronation Asset Management has bought more shares, taking its stake from 14.41% to 16.57%. This is helpful, but the market doesn’t pay too much attention to asset managers making small changes.

Insiders give the real clue to what might be going on. There were two such examples on Wednesday, with a non-executive director (Diane Radley) buying nearly R1.2 million in shares and none other than Chris Seabrooke (through Sabvest Capital) mopping up R5.4 million shares.

Now, when Sabvest buys shares, the market pays attention. The purchase price was around R10.80 per share.

Transaction Capital closed 9.8% higher at R11.69. The rollercoaster continues.

Little Bites:

Director dealings:

There was an absolute banger of a director purchase of shares at Curro (JSE: COH), sending the share price 5.6% higher. Piet Mouton bought R19 million worth of shares.

As noted above, non-executive directors of Transaction Capital (JSE: TCP) bought shares worth R6.6 million, including Sabvest Capital (JSE: SBP – linked to Chris Seabrooke) buying R5.4 million.

Des de Beer is back at it, buying R386k worth of shares in Lighthouse Properties (JSE: LTE).

A director of Kaap Agri (JSE: KAL) bought shares worth R120k.

An associate of the CEO of Invicta Holdings (JSE: IVT) has bought shares worth R111k. There’s been quite a bit of insider buying at Invicta – something to take note of?

Although the results aren’t out on SENS yet, news reports suggested that the Steinhoff (JSE: SNH) shareholders rejected the restructuring plan. I maintain that the equity is worthless, yet it still changed hands at R0.30 on Wednesday. The end is surely nigh.

Perhaps I wasn’t blind on Tuesday when I couldn’t find the Rebosis (JSE: REA) business plan. They released a subsequent SENS announcement with the link and I can now see it right at the top of the page at this link.

It seems like there was an unexpected resignation at Metair (JSE: MTA), with CEO Riaz Haffejee stepping down with effect from 31 March. That doesn’t leave any time at all for a handover and he was only there for roughly two years. The current CFO, Sjoerd Douwenga, will take over as interim CEO. There has been an internal promotion to the interim CFO position.

There have been significant changes to the executive management team of Grindrod Shipping (JSE GSH), with the founder and CEO of Taylor Maritime also taking the role of CEO of Grindrod Shipping.

Mr Mvuleni Geoffrey Qhena, former CEO of the IDC, has joined the board of Telkom (JSE: TKG) as its Chairperson.

Europa Metals (JSE: EUZ) has announced that the initial budget for drilling has been agreed with its joint venture partner in the Toral Project in Spain. $1.8 million will be spent over a 12-month period.

Randgold & Exploration Company (JSE: RNG) issued a further trading statement that tightens the earnings range. The headline loss per share will be between 80.26% and 90.26% worse. This is to be expected in a junior mining company.

Choppies Enterprises (JSE: CHP) renewed its cautionary announcement regarding the potential acquisition of up to a 100% stake in a Botswana-based FMCG business.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")