Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Renergen finally becoming a helium producer.

The Foschini Group releasing impressive numbers over the festive season.

Truworths giving the market a positive surprise with its growth.

Clicks showing solid retail growth, with question marks over the wholesale performance.

Lewis demonstrating that lower income consumers are clearly under pressure, with strong credit sales and a drop in cash sales.

Astral Foods reminding the market that poultry is perhaps the toughest industry around.

ArcelorMittal showing a resilient performance (by its standards) in tough operating conditions.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

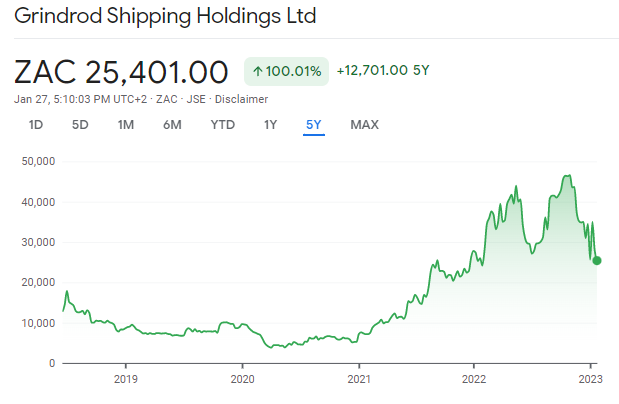

The company is working closely with Taylor Maritime Investments

After the recent corporate action, Taylor Maritime Investments is the proud owner of 83.23% of the shares in Grindrod Shipping. The company is still listed, so the shareholders who stayed behind will now participate in a journey of (hopefully) value creation as the companies explore synergies.

The companies are looking for efficiencies across insurance, commercial management, technical management and corporate activities. There is also a plan to reduce debt on Taylor’s balance sheet, which would give the company more firepower to support Grindrod Shipping.

There’s already a deal in place to sell a vessel to free up some cash, though the announcement doesn’t give an indication of the selling price.

This is a highly cyclical industry, as evidenced by the share price chart:

Industrials REIT is enjoying rental uplifts, but vacancies are down

In a quarterly update, the company gives a mature view on things

Industrials REIT – a fine example of a company that “does what it says on the tin” – is still enjoying an environment that is favourable for industrial properties. High demand and limited supply means that incredible uplifts in rent can be achieved when leases are renewed.

How much? Try a 31% average uplift on for size! It’s even better for new lettings rather than renewals, with an average uplift of 36%.

Of course, these growth rates are not applied mid-lease, so the entire portfolio certainly isn’t growing at these levels. Like-for-like rents were up 5% for the portfolio over the past 12 months.

Despite the company highlighting strong demand, occupancy actually fell by 0.4% this quarter. That’s not as small a move as you think, as the percentage is measured based on the entire portfolio.

To help with occupancy, the company has its own leasing platform in the UK that has boasted a 15.4% increase in visitors year-on-year. There is obviously a dedicated sales team as well. An efficient leasing strategy helps keep costs down, with 73% of leases contracted through Industrial REIT’s short-form digital “smart leases” (as the company likes to call them).

Although the company notes that the trading environment may become more difficult this year, they also believe that attractive acquisition opportunities may become available. That makes sense, as the best deals are to be found when things get tough. At that stage, companies with strong balance sheets can pounce. The company is sitting on its cash for now, with no new deals during the quarter.

In some cases, the opportunity exists to take an active asset management approach. Simply, this means buying a fixer-upper. A recent project near Edinburgh is expected to achieve a yield on cost of 17.7%. Bearing in mind that this is measured in GBP, that’s a proper yield!

Is Lewis a good barometer for consumer health?

If so, we are going to be in trouble soon

Over the past week or so, we’ve had a flurry of updates from clothing and homeware retailers. These are semi-durable goods, which means they aren’t as necessary as the bread in your shopping basket but they are also a much easier purchasing decision than a new car or TV.

With Lewis, we take a big step into the world of durable goods. To feel confident about these major purchases, consumers need to believe that everything is going to be alright. Whether they buy on cash or credit, there’s still a significant difference in the psychology behind these decisions vs. clothing or especially food.

In the nine months to December, Lewis could only increase sales by 2.0%. Inflation, higher interest rates, growing unemployment and load shedding are all major factors here, with same-store sales barely inching upwards by 0.4%.

If you dig deeper, you’ll find the really scary statistics: credit sales over the nine-month period increased by 16.8% while cash sales declined by 13.5%. That’s a worrying outlook for South African consumers. Credit sales contributed 58.3% of total sales, well up from 50.9% in the comparable period.

If that’s not enough to concern you, the trend over the period might just do it. In the three months to December, sales fell by 1.1%. Credit sales were 17.3% higher and cash sales were whacked by 20.7%, with a net sales result that is in the red.

Once other income is taken into account, total revenue was up 2.8% over the nine-month period.

The silver lining is that collection rates are strong, so those credit sales are working out for the time being. Collection rates came in at 82.7% this quarter, up from 79.7% in the comparable quarter. The trend is going in the right direction in this metric, as the nine-month collection rate is 82.0%.

Whilst it certainly helps to see collection rates improving as credit sales increase, it’s also important to remember that the collection rate is more of a lagging indicator. What really matters is whether collection rates will stay strong this year. With consumers clearly under pressure, that’s the risk that the market didn’t like, with Lewis dropping 2.3% on a trading day that was generally poor for retailers on the JSE.

The other risk lies in what could be happening to profitability, as the announcement only dealt with sales. With rampant inflation, that sales growth number doesn’t sound high enough to avoid margin compression.

Little Bites:

Director dealings:

The CFO of Naspers has sold shares through an option scheme worth R92.4m. That’s not a typo.

The CEO of Sirius Real Estate has bought shares in a self-invested pension (a structure you find in the UK) to the value of £21k.

A prescribed officer of Alexander Forbes has sold shares worth nearly R84k.

If you are wondering what’s going on at Steinhoff, the agenda for the AGM will be published on 2 February and a circular with full details of the balance sheet restructuring will be published on the same date.

The meeting to approve the scheme of arrangement at Alviva was approved by a strong majority of shareholders, with around 94% voting in favour of the deal that will see Alviva taken private.

In a sign of the times, there were two updates on SENS regarding business rescue processes. One was Rebosis, announcing an extension to the deadline to publish a business rescue plan (now 17 February 2023. The other was Basil Read, which noted that the company is currently operating steadily despite the obvious economic challenges.

AVI is treading water and maintaining flat earnings

But consumer pressures are a bigger problem than load shedding

For the six months ended December, AVI suffered the significant impact of load shedding in its manufacturing operations. Keeping the lights on in a retail store is one thing, but managing an entire manufacturing back-end is something else entirely.

Alternative power solutions added R22 million to operating costs. Although that isn’t a catastrophe for a R25 billion market cap company, it’s still painful. It may be a red herring though, as the bigger problems are in consumer spending.

Volumes are under pressure in some categories, as cutting luxuries from the grocery basket is an easy way to save money. Group revenue increased by 7.2%, with pricing as the bulk of the story here. As is always the case in these types of businesses, category-level performance can vary drastically. For example, I&J fell 2.3% with lower catch rates and other issues, while the fashion brand portfolio grew by 17.4%.

An important update is that the consolidated gross margin increased slightly, a solid outcome in an environment where margin pressure is common. The mix effect will be a major contributor here.

Without I&J, operating profit would’ve been up 8.4%. Including that business, group operating profit could only manage growth of 1.7%.

Below that line, there’s still the pressure from net finance costs, which increased as borrowings and rates were both higher. Inflation leads to bigger balance sheets, which is why I was bullish on banks last year. They sit on the other side of this issue for operating companies.

Overall, headline earnings per share (HEPS) for the period are expected to be between 0% and 1% higher, coming in at between 316.9 cents and 320.1 cents. The share price fell more than 3% on this news, as AVI doesn’t trade at the cheapest multiples around.

MiX Telematics releases strong quarterly results

Shareholders can smile at record subscriber growth and significant margin expansion

For some reason, MiX Telematics doesn’t bother to write a proper SENS announcement to go out with the results. Instead, you have to go digging on the website for the quarterly update. Investor relations laziness aside, the results look good.

With record net quarterly subscriber additions of 44,600, the subscriber base is now over 959,000. Revenue increased by 14% on a constant currency basis and adjusted EBITDA increased from $6 million to $8.4 million for the quarter.

You probably noticed the dollar signs. This is because MiX Telematics is listed on the JSE and the New York Stock Exchange, with the company choosing to report in dollars.

With adjusted EBITDA margin of 22.2% vs. 17% in the prior quarter, there’s good news here for the company. The other good news is that free cash flow is positive again, after timing of investment in inventory worked its way through the system.

In the next quarter, the management team hopes to see further improvement in margins. Heck, they might even make enough money to afford someone who can write a decent summary of the result on SENS.

Shareholders look set to get something OUT

Core earnings at OUTsurance are looking strong

For the six months ended December, the listed group formerly known as Rand Merchant Investment Holdings has released results that are mainly attributable to the OUTsurance business. Having cleaned out almost everything else, the group recently changed its name to OUTsurance Group Limited.

The insurance operations are in Australia (under the Youi brand) and in South Africa under the OUTsurance brand that we all know. In both cases, the performance is good. The reasons vary.

In Australia, fewer natural peril claims have helped alongside premium growth and a more favourable investment environment. Indeed, the only recent disaster in Australia of any consequence was our cricket tour there, which is sadly an uninsurable event.

In South Africa, premium growth was strong and the claims experience was in line with historical levels, so there’s a return to normality.

There are a million distortions in the headline earnings per share (HEPS) number at group level, due to the extensive disposals of assets by the group. The important number is normalised earnings for the insurance businesses that are now the core of the group, which increased by over 20% for the six-month period.

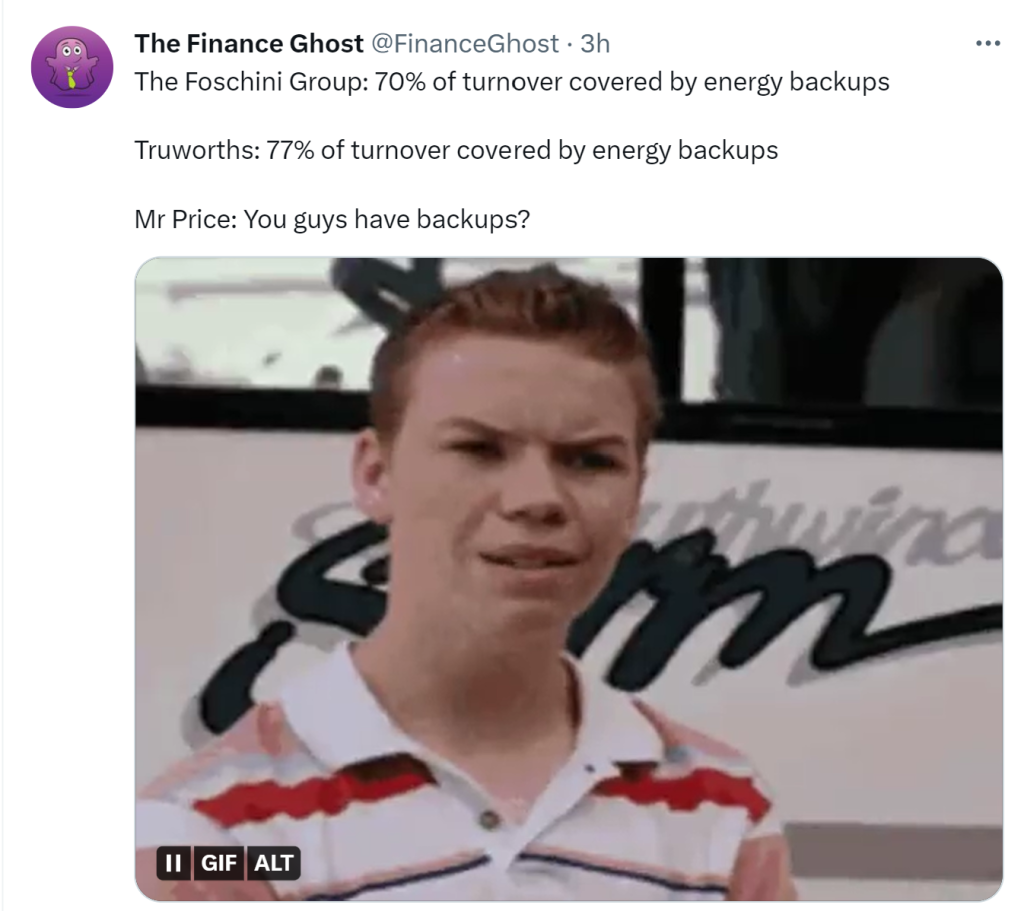

Even Truworths can figure out load shedding

The market doesn’t give Truworths much credit – will this update change that?

You know, it doesn’t seem that hard to think of a solution here. When the power is out, invest in energy backups so your customers aren’t shopping by smartphone torchlight.

Yes?

No?

It depends on which retailer we are talking about. Whilst Mr Price spent its time writing SENS announcements about how bad load shedding is, the likes of Truworths (and The Foschini Group and Woolworths) just got on with it.

With the Truworths numbers now in the wild, there are no excuses left for the shocking numbers from Mr Price. Truworths grew retail sales by 13.0% on a comparable basis for the 26 weeks to 1 January 2023. The growth was strong both locally (13.4%) and in the UK (12.3%).

Yes, there’s a timing impact here. The first part of the 26-week period was much butter than in the last 9 weeks that were hit by load shedding. I suspect that Mr Price would raise this point in its defence, as the Mr Price update only covered the Black Friday and festive season. Still, the gap in performance is so huge that timing alone cannot explain it.

Perhaps the extent of backup power has something to do with it? I’ll just defer to my Twitter here:

The numbers look good even as you dig deeper, with healthy growth across account (16.0%) and cash (9.9%) sales. Account sales contributed 51% of group sales. With inflation of 13.3%, I must highlight that volumes seem to have dipped slightly. Still, that’s decent in this environment.

In the UK where they have lots of electricity and not a lot of sunshine, retail sales at the Office segment were up by 12.3% in local currency. Online sales contributed 44% of total revenue, down from 47% in the comparable period. There was a nifty acceleration in that business, with sales up 15.1% in the last nine weeks of the period.

Trading space increased by 0.8% in Truworths Africa and was reduced by 3.8% in Office.

Headline earnings per share (HEPS) for the 26 weeks to 1 January 2023 are expected to be between 8% and 11% higher, coming in at 485 to 498 cents. Famous for trading on a modest multiple, the Truworths share price increased by over 4%.

Little Bites:

Director dealings:

An associate of the CEO of Spear REIT sold shares worth R309k and an associate of the CFO sold nearly R3.4m worth of shares – are interest rates starting to bite?

A director of Dipula Income Fund bought shares worth over R207k and an associate of a different director bought shares worth R1.44m.

A director of EOH has bought shares worth just under R100k.

Anglo American continues to make progress in having more efficient heavy machinery in its operations. You may recall the hydrogen mining truck that caused quite a buzz when it was launched. Now, we have an LNG dual-fuelled vessel, the first of ten such vessels that Anglo will use in its chartered fleet in 2023 and 2024. As part of the goal to achieve carbon neutrality by 2040, these vessels will cut CO2 emissions by 35% vs. conventional marine fuel vessels. The maiden voyage is a haul of iron ore from Kumba.

Here’s an unusual one for you: the CEO of AECI has accelerated his retirement by a few months, leaving to pursue other interests. A current independent non-executive director has been appointed as CEO while the group looks for a successor. This isn’t exactly a great handover, is it?

The ANSARADA DealMakers Annual Awards are just a few weeks away. The following are those transactions shortlisted for the Business Rescue Transaction of the Year 2022 and highlight the process as a tool to preserve value. The DealMakers Independent Panel have selected these transactions from the nominations submitted by the M&A industry advisers. They are in no particular order:

Ster-Kinekor

SA’s largest cinema chain with 65% of market share entered business rescue in January 2021 citing financial distress due to COVID-19 related restrictions and increased competition from streaming platforms. The consortium comprising UK-based asset manager Blantyre Capital and local private debt manager, Greenpoint Capital emerged as the successful bidder in the R250 million refinancing, restructure and sale of Ster-Kinekor’s assets. In November 2022 the company exited business rescue having continued operating throughout the process and without the loss of +-800 direct jobs.

The local advisers were: EY, Webber Wentzel, Baker McKenzie and Mike Pienaar Consulting.

Andalusite Resources

The country’s remaining independent andalusite producer exited the business rescue process in May 2022 having been placed under supervision in June 2019. A world class strategic asset, Andalusite Resources is one of three main suppliers of andalusite globally with a 23% market share. Eight expressions of interest were received with ARM (a subsidiary of Nikkel Trading 392) winning the bidding process which began in July 2019. The business and all 181 employees were successfully transferred to ARM, a South African entity, under the same terms and conditions.

The local advisers were: GCW Administrators and Werksmans.

Consolidated Infrastructure Group (CIG) and Consolidated Power Projects (CONCO)

The GIC and CONCO business operate in the infrastructure and construction sectors focused primarily on energy, electrification, building and oil and gas and as a result the business rescue of these groups were both large and complex due to multi-disciplinary operations involved. GIC was listed on the JSE when it entered business rescue. The successful operational restructuring implemented disposed of operationally stable, efficient and profitable going concerns resulting in the retention of jobs within those businesses and maximisation of net proceeds for all affected parties.

The local advisers were: Birkett Stewart McHendrie, Metis and Werksmans.

The winner will be announced at the ANSARADA DealMakers Annual Awards on 21 February, 2023 at the Sandton Convention Centre.

Astral shows us that chicken farming isn’t for chickens

The horrible numbers shouldn’t be a surprise to anyone who was paying attention

If you’re looking for a business with extraordinary operating leverage and very thin margins, then poultry is for you. Back in November, Astral warned the market that things would get ugly, with record high feed input costs and the terrible impact of load shedding on operations.

In the Feed division, costs came under pressure as the group navigated load shedding. To help manage its impact, capital expenditure will be required. The good news is that the Poultry division will require substantially higher internal feed volumes, which will positively impact this division’s financial performance.

This brings us neatly to the end of the good news.

We move on to the Poultry division, where feed input costs are causing havoc. Contributing around 70% of the cost of producing a live broiler, any significant movements in this cost have a substantial knock-on effect on margins. Load shedding is a huge problem here, with abnormal costs and production cutbacks of at least 12 million broilers for the interim period.

That’s a lot of chickens.

With a backlog in the slaughter programme, the chickens are quite literally older and heavier, which means they are consuming more feed before being slaughtered.

So in fact, that’s a lot of fat chickens.

If costs could be passed on to consumers, some of these issues could be mitigated. Sadly, consumers are under so much pressure that Astral is having to subsidise the increased cost of productions. Right now, Astral is making a loss on every chicken of at least R2/kg. This will lead to this division incurring “significant losses” for the interim period.

In summary, there are a lot of fat, loss-making chickens. This is a cluck up of note.

Most of the capital expenditure plans of R737 million have been put on hold, with some funds committed towards backup electricity generation to reduce the impact of load shedding.

For the six months to March 2023, headline earnings per share (HEPS) will drop by up to 90%, coming in at 142 cents or more. The comparable period saw HEPS of 1,420 cents.

Although the group balance sheet is healthy, the reality is that the monthly run-rate in the business sounds really bad. This period may have been profitable, but the next one won’t be unless something changes in Astral’s operating environment.

The market clearly thinks that things will get better, based on this five-year share price chart:

Quilter reports further net inflows

The company manages and administers just under £100 billion in assets

Quilter’s assets under management and administration increased by 3% in the three months ended December. Now coming in at £99.6 billion, net inflows of £159 million in the quarter represented around 1% of the growth.

This was lower than net inflows in the preceding quarter (£236 million) and vastly reduced from inflows of £950 million in the comparable quarter of the prior year.

Clearly, inflationary pressures are really hitting household savings, including in the UK.

Quilter’s own distribution channel is performing far better than the independent financial advisor channel, which makes sense when you have your own army of advisors out there selling your products. This is a major part of Quilter’s investment case.

2022 was a tough year for asset management. Quilter ended 2021 with £111.8 billion in assets under management and administration. A year later and at £99.6 billion, that’s nearly an 11% drop in 2022.

The market movements are outside of Quilter’s control but inflows are not, so investors will be pleased with net inflows, even if they dropped sharply for the year to £1,787 million from £3,967 million the year before.

The share price has lost nearly 40% in the past 12 months.

Little Bites:

Director dealings:

The chairperson of RFG Holdings has bought shares worth nearly R36k

An associate of a director of Dipula Income Fund bought shares worth over R42k

Eastern Platinum has announced that the contract to deliver PGM tailings concentrate to Impala Platinum has been extended on the existing terms until 21 December 2023. The relationship between the companies is important, with Eastern Platinum targeting a restart of the Zandfontein underground section in 2023 based on an off-take agreement with Implats.

Trencor released a trading statement that shows the company swinging into a loss for the year ended December 2022. The headline loss per share is expected to be between 0.7 and 1.3 cents vs. headline earnings per share of 3 cents in the prior year. This structure is a leftover on the JSE, so this isn’t as newsworthy as you may think. It is essentially a cash shell that will be wound up at a future point in time.

Profitability has been hammered as conditions turned against the company

For the year ended December 2022, ArcelorMittal’s headline earnings per share (HEPS) is expected to nosedive by between 60% and 65%, coming in at between R2.15 and R2.45 per share. To be fair, this still puts the company on a Price/Earnings multiple of under 2x!

Despite that low multiple, the share price fell 11.6% on this news.

There are various reasons for this, ranging from declines in steel prices through to the global energy crunch and the impact on the company’s operating costs. With destocking by local customers, demand also came under pressure. To make everything even worse, there was a shortage of road trucks for domestic and African overland deliveries in the final quarter of the year.

As the company points out, these results were actually much stronger than in previous times of crisis. Despite obvious operating challenges, there was still a profit on the table for shareholders.

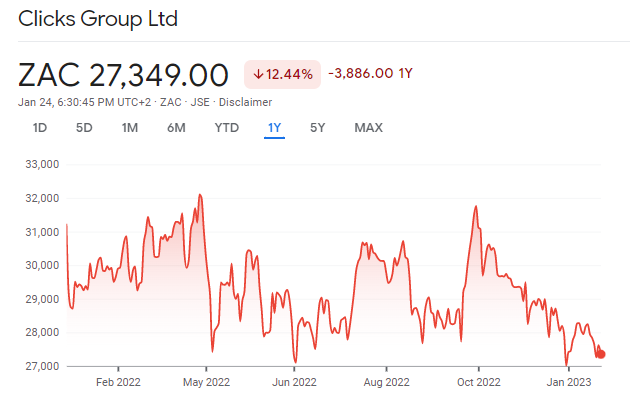

Clicks posts solid growth

The share price was flat, showing just how much is priced in

Clicks is famous in the local market for (1) exceptionally long queues at the dispensary and (2) a share price that trades at very high multiples. Investors have a soft spot for Clicks because of its defensive characteristics. The company is especially popular among global investors.

Still, the share price has been under pressure over the past year:

Credit where credit is due: the sales performance for the 20 weeks to 15 January 2023 is more than decent. Excluding vaccinations (which were huge in the base period), group turnover is up 7.8%.

Retail sales excluding vaccinations were up 12.2%, so the wholesale growth is significantly lower. Wholesale turnover in UPD fell by 0.6%, so it was turnover managed on behalf of bulk distribution clients that helped that side of the business.

Volumes were up, with like-for-like sales of 8.9% vs. selling price inflation of 6.8%.

Interim results are due in April. I’ll be interested to see why the wholesale side of the business is under pressure when things are clearly doing well on the retail side.

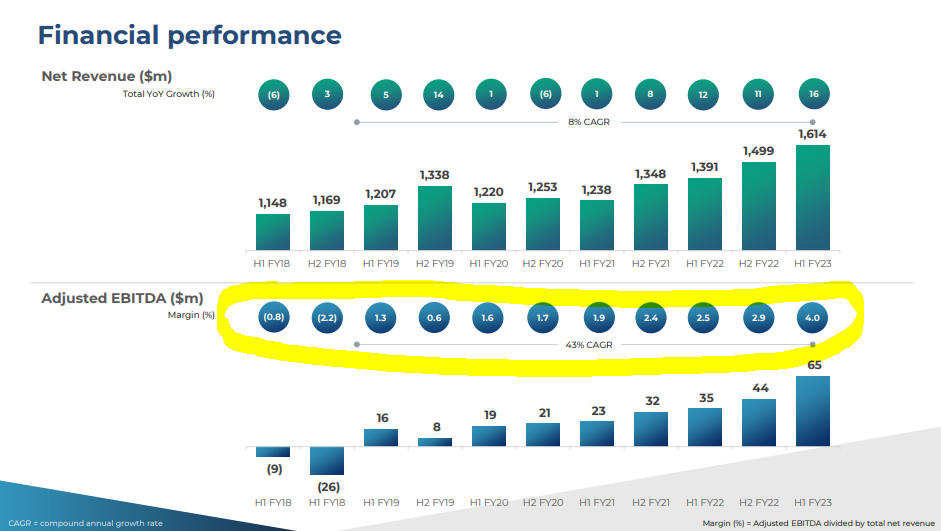

Datatec wants you to get to know Westcon International

The company has released a detailed investor presentation

The release of an investor presentation is always worth paying attention to. Generally, these are proper learning opportunities and the latest example from Datatec is no different.

For example, here’s an interesting chart showing how skinny the EBITDA margins are in the IT distribution game:

The yellow highlight is obviously my handiwork, drawing your attention to the EBITDA margin history. As you can see, there isn’t much room to make a mistake in this business!

Grindrod has alerted shareholders to a press release by the Port of Maputo that highlights a new handling record in 2022, having grown a whopping 20% compared to 2021. Volume handled was 26.7 million tons, up from 22.2 million tons in 2021.

The growth is attributed to infrastructure investment and the decision of the Government of Mozambique to establish a 24-hour border operation.

To depress you further about the trajectory of our infrastructure in South Africa vs. other countries, rail volumes for chrome and ferro-chrome jumped by 73% vs. the prior year. The press release notes that 26% of cargo is now carried by rail, with links into South Africa helping with this. It’s just a pity that other parts of our country aren’t working nearly as well as the Mozambique corridor.

Sasol jumps 4.7% after releasing a production update

The market also liked the news about renewable energy procurement

Eskom is doing a wonderful job of helping companies move towards meeting emissions targets. Not only does it make the ESG section of the report look better, but having alternative sources of power has become a business imperative thanks to the state of our national grid.

Sasol has announced three power purchase agreements, including 69MW of wind power for Sasolburg and 220MW of wind power for Secunda under two separate agreements. There’s a long way still to go, with Sasol aiming to procure 1,200MW of renewable energy by 2030.

Looking to the detailed numbers, external sales revenue for the half year was down 2% vs. the prior year.

Productivity in the mining business was lower in this period. The coal stockpile remains above the minimum level, helped by growth in external purchases. This is important to ensure continuous coal supply. Export sales fell by 25% in this part of the business, attributed to challenges at Transnet Freight Rail and the diversion of export coal to the stockpile.

In the Gas business, production fell by 2% due to reduced demand from Sasol itself and its external customer, attributed to load shedding and the impact it has on our industrial companies.

The Fuels business reported a 2% drop in production, hurt by various factors ranging from coal quality to rainfall incidents. Although Sasol hopes to achieved the original full year guidance, there are challenges in sourcing hydrofluoric acid and this is a risk to the numbers being achieved.

The Chemicals business experienced a 5% decrease in external sales volume and a 2% decrease in external sales revenue. The major pressure was in the Eurasia business, where volumes fell by 19% due to economic challenges in Europe and the war in Ukraine. The African and American businesses were positive.

Little Bites:

Director dealings:

The former CEO of Famous Brands has executed a collar structure over R12.28 million worth of shares, with a put strike price of R55.26 and a call strike price of R86.33. This is a way to protect the value of a stake within a certain range (the latest closing price is R61.96).

A director of CMH has acquired shares worth nearly R53k.

A director of Barloworld has acquired shares worth R77.5k

Reinet has released its net asset value per share update for the quarter ended December 2022. The net asset value per share is up 6.5% vs. September 2022 and the company has achieved a compound annual growth rate of 9.1% in euro terms since March 2009, including dividends paid.

Kore Potash has announced further drilling results form the DX extension in the Republic of Congo. Note that this is different to the Kola project that is usually in the headlines. The management team seems to be pleased with the results. If you want to learn about geology, you’re welcome to go read the complicated announcement!

In further junior mining news, Southern Palladium is pleased with the results of an internal scoping study for the Bengwenyama PGM project. It confirms that UG2 has the best development potential, with the company now believing that a mining rights application should be submitted earlier than first envisaged. The board has decided to initiate the Prefeasibility Study this quarter.

The following are those deals shortlisted for the Exxaro BEE Deal of the Year 2022. The DealMakers Independent Panel have selected these transactions from the nominations submitted by the M&A industry advisers. They are, in no particular order:

Old Mutual’s ‘Bula Tsela’ BEE transaction

During the Old Mutual separation process announced in 2018, the company undertook an empowerment commitment to increase its BEE ownership to 30% by June 2023. The disposal of a further 4.36% stake in 2022 in a three-legged process involving employee and community trusts and a retail offer, satisfied this commitment. The R2,8 billion deal involved complex funding options of notional vendor financing to the trusts and actual vendor funding to the retail scheme.

The local advisers to the deal were: Rand Merchant Bank, Tamela, Merrill Lynch, Bowmans, PwC and Deloitte.

Shoprite Checkers’ evergreen B-BBEE transaction

The announced R8,9 billion transaction in May 2022 was the first of its nature in the retail sector – the deal at Shoprite’s subsidiary boosted its B-BBEE ownership to 19.2% from 13.5%. The deal recognises its employees’ role in the success of the group by providing them with additional compensation over and above their salary. The evergreen B-BBEE Employee Benefit Trust will hold 40 million shares in the local subsidiary and employees will receive dividend entitlements but will not own the shares, so the transaction will not have an impact on the shares in issue in the listed holding company. Non-SA employees will also receive equivalent payment to that of its local employees.

The local advisers to the deal were: Rand Merchant Bank and Werksmans.

Seriti Resources’ acquisition of Windlab Africa

The acquisition by Seriti of a major stake in Windlab Australia’s South African and East African wind and solar-powered businesses, marked the transfer of strategically important renewable assets from foreign ownership into the hands of a black energy company. Windlab Africa has developed 230MW of projects currently operating and supplying the SA grid. The 54.2% stake in Windlab Africa for c.R892 million acquired via subsidiary Seriti Green, speaks to its goal of ensuring long term sustainability as a diversified energy producer. Seriti is currently Eskom’s largest black-controlled coal supplier.

The local advisers to the deal were: Standard Bank and White & Case.

Anglo American Platinum’s B-BBEE transaction

The company’s new employee share ownership plan valued at R1,8 billion, announced in September 2022, will issue to employees (SA and Zimbabwe) listed shares valued at R8,000 each year with each tranche vesting three years after allocation, and participation in the evergreen ownership of 2% of Rustenburg Platinum Mines (RPM). The RPM shares will be held into perpetuity on behalf of qualifying employees and shares will be fully funded by Amplats with employees receiving dividends as and when declared.

The local advisers to the deal were: Rand Merchant Bank, Merrill Lynch and Webber Wentzel.

The winner will be announced at the ANSARADA DealMakers Annual Awards on 21 February, 2023 at the Sandton Convention Centre.

It’s quite incredible how sentiment can change towards economies in the course of a few weeks or a few months. But that is precisely what has happened with respect to not only the US but also the EU economies in the past few months. Chris Gilmour elaborates.

Did Powell get it right?

It seems like yesterday that many observers were warning about US inflation getting out of hand and US Federal Reserve chair Jerome Powell perhaps having gone too far and precipitating a deep recession in the US. Others were saying he hadn’t gone far enough and that a return to the days of Paul Volcker and 20% plus interest rates was on the cards.

In any event, it appears as if Powell’s recipe for interest rate increases has been pitched just right.

Consensus is now for a mild recession in the US, beginning in March this year and only lasting a few months. Inflation and interest rates will probably begin easing towards year end.

Europe: not as bad as feared

Europe, where all sorts of nasties were being touted, most as a direct result of the Russo/Ukraine war, isn’t looking nearly as bad all of a sudden. Germany isn’t going into recession after all and its manufacturing base is able to soldier on, albeit that it has had to pay a lot more for its energy supplies. The European winter has turned out to be remarkably benign, with many European ski resorts literally having no snow other than artificial snow created by snow cannons.

Gas stores will easily last the entire winter.

Of course, next winter may well be very different, especially if Russia does indeed cut off all supplies to Europe by then. But for the meantime, tales of Europe’s demise appear to have been greatly exaggerated.

Even the UK, the “sick man of Europe” now that it’s hobbled by rolling industrial action, may just miss recording a technical recession in the last quarter of 2022 by the skin of its teeth. Figures from the Office for National Statistics (ONS) showed that the UK recorded a slight year on year uptick in GDP growth in November of 0.1%, compared with a consensus of 0.2% decline. In the three months to end September, GDP shrank by 0.3% and the bean-counters at the ONS have calculated that the UK’s GDP would need to have fallen by 0.5% in December in order to have two consecutive quarters of negative economic growth, the classical definition of recession.

What does this mean for stocks?

So with all this relatively less bad news in mind, why are global equity markets (especially in the US) performing so poorly?

The S&P 500 is down around 18% from its peak at the time of writing.

The answer probably lies in the combination of mistrust of the Fed (maybe Jerome Powell and his colleagues on the FOMC will keep on hiking beyond year-end) and the realisation that generally higher inflation and interest rates are here to stay for the time being.

That’s bad news for tech stocks, which have been the main drivers of the US market in recent years. One only has to look at the scale of layoffs currently taking place in Silicon Valley stocks to appreciate the real impact of the downturn on this segment of the market. A strong dollar doesn’t help either, but as rates begin to be perceived to be peaking in the US, the strength in the USD will likely falter.

But eventually investors and speculators alike will start buying tech stocks again once they perceive the rout to be over. In the meantime, attention is probably likely to be more focused on commodity-type stocks that will do well out of higher demand for basic metals and materials. All those cynics who said that the JSE was finished and that the only place to invest was offshore are now eating their words, as the JSE All Share hits news highs almost every trading day.

Every dog has its day and the JSE was a real dog for a long time. So enjoy the current boom while it lasts, because it never does.

This article reflects the independent views and opinions of Chris Gilmour, which are not necessarily the same as The Finance Ghost’s opinions on these stocks. For equity research on South African retail and other stocks, go to www.gilmour-research.co.za.

Sales are down, yet the share price barely moved in response

Eventually, battered and bruised, a share price stops getting a bloody nose every time numbers are released. It can sometimes be a buying opportunity, though there are no guarantees that things won’t deteriorate further.

Cashbuild is down 30% in the past year, so there is no shortage of pain among investors. The civil unrest was incredibly damaging to Cashbuild and the company took a long time to recover. By the time trading was largely restored, the economy had swung against Cashbuild. It really was a perfect storm.

For the second quarter of this financial year, revenue was down 5%. Like-for-like revenue fell 6% and new stores added 1%. Over the six-month period, revenue is down 4%. Despite this, the share price only closed 0.6% lower on the day, though I must point out that this was on a very good day for the JSE, so the effectively performance gap is higher than this would otherwise suggest.

Inflation seems to have moderated, with selling price inflation of just 4.5% for the quarter.

Much as I want to look for silver linings here, the reality is that growth deteriorated in Cashbuild South Africa, which contributes 81% of group revenue. It was down 3% in Q1 and then 5% in Q2. The P&L Hardware business is still under pressure, down 9% in Q2. That’s at least better than the 11% drop in Q1.

Cashbuild relies on home improvement and investment in construction. Load shedding does terrible things to consumer confidence, so I’m not sure that the revenue bleeding will stop just yet.

Renergen: more than just hot air

Finally, there is liquid helium

Nervous have been settled by the latest announcement from Renergen, with the exciting news that the helium module at the Virginia Gas Project is finally in operation. This means that South Africa is one of eight countries worldwide that produce helium.

A one-year share price chart shows how confidence started to dip towards the end of 2022 based on some difficult SENS announcements and then a fairly long period of silence from the company. A 9% rally on Monday helped claw back some of those losses!

South32 quarterly update

Overall, the production news is positive

Mining updates tend to be highly detailed and quite technical. If you’re looking for the finer details of the quarterly update, then I suggest reading the original SENS released by South32.

For the rest of us, all we really need to know is that copper production is up 12% for the first half of the 2023 financial year and aluminium production is up 15%. Australia Manganese achieved record production, posting an increase of 7%.

Importantly, operating unit costs for the first half of the year are expected to be in-line with or below guidance at the majority of group operations. This is a positive story overall.

The Foschini Group makes Mr Price look even worse

Load shedding or not, TFG is flying

If you’ve been reading your Ghost Bites this week, you’ll know that Mr Price released a horrible set of numbers that really calls into question whether the core business is resonating with consumers. My view is that Mr Price has been too focused on acquisitions, with the neglect of the core business now showing.

The latest update from The Foschini Group (TFG) confirms that view, with solid numbers despite facing all the same load shedding challenges that Mr Price had to deal with.

The key number is like-for-like growth in TFG Africa, which came in at 5.7% for the quarter. Even more impressively, like-for-like Homeware sales were up 3.4% for the quarter. Clothing was up 6.7%. With 70% of TFG’s local turnover supported by backup power solutions and a plan to take this to 100% over the next few months, TFG is spending less time apportioning blame and more time surviving the challenges.

The acquisition of Tapestry Home Brands skews the overall growth number in TFG Africa, which came in at 18.4%. Still, with nuggets in the announcement like record Black Friday and Cyber Monday sales, there was plenty for shareholders to smile about in this update. Online sales grew 43.3% and now contribute 3.9% of total TFG Africa retail turnover.

There are some issues for investors to worry about, like a 100bps drop in TFG Africa’s gross margin vs. the prior period. In the UK, TFG London could only manage a 2% increase in sales, though a less promotional environment (steady sales vs. a Black Friday focus) was supportive of margin. Online sales in the UK fell by 11.5%, now contributing 42% of total sales.

In Australia, turnover increased by 20.9%. Online fell 16.2%, now contributing 5.8% of total turnover in Australia.

Over nine months, group turnover is up 20.8%. We know that the Tapestry Home Brands acquisition is flattering this number, but there’s more than enough going on in the rest of the business to give this result a positive report card.

Speaking of acquisitions, TFG will acquire independent footwear retailer Street Fever. 114 Street Fever stores will be acquired and approximately 90 will be rebranded to Sneaker Factory. Others will be rebranded under other TFG brands as appropriate.

The trust related to the management team of Ninety One has bought shares worth around £246k

There were some mistakes in the Alviva circular related to the take-private offer being made by the consortium of investors. Certain shareholders are not eligible to vote on the deal due to conflicts of interest. The correct percentage of shareholders who cannot vote is 30.2%.

By 16th February, holders of at least 31.3% of Afrocentric shares need to have accepted the partial offer by Sanlam in order for the deal to stand any chance of going ahead. If the acceptance rate is lower than that percentage, Sanlam cannot elect to waive the minimum shares requirement.

Buffalo Coal Corp has received approval from the SARB for a loan from Ikwezi Mining, an affiliate of Belvedere Resources. The facility is for $30 million and it may be drawn in up to ten trances with interest accruing at a base lending rate prescribed by the SARB (currently 7.5%). Each facility is repayable within three years after drawdown.

Choppies Enterprises released a cautionary announcement regarding a potential acquisition of a fast moving consumer goods company in Botswana. There are no further details at this stage, as negotiations are underway.

In Trustco’s ongoing fights with the JSE, the latest issue is that Trustco is non-compliant due to missing a financial reporting deadline. The company anticipates releasing the reports by 31 January.

The Eskom Pension and Provident Fund has increased its stake in Hyprop. It’s nice to see the employees exposed to companies that Eskom is causing so much trouble for, like property funds.

This is one of the few property companies I hold in my portfolio

Attacq is a solid company in my view, despite the unnecessary renaming of types of properties. Shopping centres are “retail-experience hubs” and good ol’ offices are “collaboration hubs” – each to their own, I guess.

I’m invested in the numbers, not the names. Although load shedding is definitely a concern in this space as running backup power isn’t cheap, the good news is that turnover and footcount over the festive season both showed strong growth vs. the prior year.

Mall of Africa reported particularly great results, with turnover in November and December up 17.6% and 19.1% respectively. Footcount is also higher, up 10.8% and 15.5% for those two months. Those looking for clues about performance in different retail categories over the festive trading period will enjoy this paragraph from the Attacq announcement:

Vacancies at Lynnwood Bridge “collaboration hug” are down to 2.6% and there seems to be progress with leasing vacant space at Waterfall City. There does seem to be a general return to office environments, which is definitely good news for the property industry overall. The problems are still there in lower grade office properties or in areas that are hopelessly oversupplied, like Sandton.

Looking at the balance sheet, Attacq has successfully refinanced R1 billion of term loan facilities, taking the weighted average cost of debt on the facilities down by 64 basis points. The weighted average term to maturity on the refinanced facilities has increased from 1.5 years to 3.2 years.

It all looks pretty good to me, though I remain nervous about the impact of load shedding on profitability. The share price is up 22% over six months but has been range-trading since early December.

Fortress loses REIT status

It’s debatable whether this will be a positive or negative outcome

For the first time on the JSE, a listed property company has officially lost REIT status. After several attempts to restructure the dual-share classes failed, there was no way for Fortress to meet the distribution requirements to retain REIT status.

So, what does this mean?

From 1st February, Fortress will lose REIT status. It will remain a listed property company with two classes of shares. The rights attached to the shares wont change. The only difference is that the tax burden now sits with the company, not with its shareholders.

This is bad news for exempt investors, like pension funds. By now, they should’ve gotten off the share register anyway. If they didn’t, then you can expect to see some painful selling. There will also be asset managers out there who are only allowed to hold REITs, so the loss of that status is a forced sell.

Keep a close eye on SENS updates. For example, Coronation has sold some shares and now holds 18.92% of the Fortress A shares, which is still a big number. Speculative traders will be watching Fortress closely, hoping to take advantage of a bit of chaos on the register.

Is there a silver lining here? Well, maintaining REIT status puts the company on a cash flow treadmill that forces most profits to be paid out as a distribution. With the loss of that status, Fortress has far more balance sheet flexibility. The question is whether they will take advantage of that.

Karooooo releases third quarter results

With record net subscriber additions, things are finally looking up

Covid caused a lot of disruptions for Cartrack, Karooooo’s major underlying business. The global expansion plan was hit by travel restrictions, especially in Asia. The excuses eventually wore thin and the share price fell as low as R320 in mid-2022. A significant recovery to R412 has been staged since then, with the stock incredibly range-bound between R400 and R450.

Lack of liquidity is part of the problem, with a significant bid-offer spread that makes it hard to take advantage of that range.

With third quarter results now available, investors have fresh information to work through. The key statistic is that net subscriber additions for the quarter were record-breaking, coming in at 78,593. The total subscriber base is now nearly 1.68 million, up 14% year-on-year.

Subscription revenue increased 16% as reported and 15% on a constant currency basis. Total revenue was up 29% as reported and 28% on a constant currency basis, so you can see the impact of Carzuka and Picup (with the latter renamed Karooooo Logistics) on the growth numbers, as they aren’t subscription businesses.

Karooooo Logistics is at least profitable, with adjusted EBITDA of R2.6 million. That’s not a typo – it’s a very small business.

Carzuka is still incinerating cash, with adjusted EBITDA of -R14.6 million. Losses in startups are nothing new. I’m just not convinced of a strategy of mixing a low margin dealership business with a high margin subscription business.

Speaking of cash, Karooooo generated record free cash flow for the nine months ended November of R434 million, up from R306 million the year prior.

Has Mr Price lost its relevance with customers?

Fashion is intensely difficult and competition has heated up in this market

I’m not sure if you’ve Cotton On yet, but there are a lot of very good clothing retailers in our market. The international players entered our market with a vengeance, forcing Woolworths to focus and almost putting Edcon out of its misery entirely. Mr Price faces an onslaught in this space. If I look at the positioning of the likes of The Foschini Group vs. Mr Price, I struggle to see how Mr Price is staying relevant with customers.

The share price is down well over 20% in the past year and has lost 36% in the past five years. This excludes dividends, of course.

Mr Price seems to be focused on acquisitions rather than its core business, having gone on a buying spree that included Yuppiechef, Power Fashion and most recently Studio 88. Based on my glances through the shop windows, Studio 88 seems to give Mr Price a fighting chance in a market that TFG is currently dominating.

Despite the trading update for the 13 weeks to 31 December 2022 proudly declaring this a record quarter for Mr Price in terms of sales growth, the market thankfully isn’t that stupid. The share price fell more than 7%, which makes sense if you bother to read past the first paragraph.

After such large acquisitions, of course it’s a record quarter. If you include the revenue you acquired, it’s not hard to look much bigger than you used to be. Sadly, if you exclude Studio 88, the growth rate is a paltry 1.2%. With selling price inflation of 6.2%, this means that volumes plummeted.

Here’s a metric that makes it look even worse: cash sales grew by just 0.6%.

We don’t have numbers yet for net profit, but you can rest assured that they will be poor. Gross margin was lower and load shedding drove significant backup power costs at store level. The stores are seeing the action, with online sales down 6.1% if you exclude Studio 88.

Instead of focusing on what is broken, the group just keeps expanding. Excluding Studio 88, weighted average trading space increased by 5.4%.

Are there any silver linings here? Well, Power Fashion and Yuppiechef both achieved double digit sales growth. This suggests that Mr Price is doing a decent job on acquisitions and a poor job in the core business.

Maybe the retailer should take a leaf out of Woolworths’ book and focus on fixing the value proposition instead of rolling out lots of new stores?

Director dealings:

The CEO of Spear REIT has bought shares worth R15.3k

An associate of a director of Huge Group has bought shares worth R15k

Reinet always reports the net asset value (NAV) of the underlying fund and then reports the NAV of the listed company that is invested in the fund. Though the percentage movements aren’t usually identical, the fund movement is a strong clue as to the movement in the company. From September to December 2022, the NAV increased by 6.5%, so that was a strong quarter.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")

")