Sasol delivered a mixed set of results for the first six months of the 2023 financial year, supported by oil and refining tailwinds offset by lower volumes and higher feedstock costs.

No loss of life since October 2021

~550MW renewable energy power purchase agreements conclude in South Africa

R18 billion spend with black-owned suppliers

Invested R780 million in socio-economic and skills development

Venture Capital Fund launched supporting low carbon strategy

Earnings before interest and tax (EBIT) of R24,2 billion

Core headline earnings per share up 9% to R24,55

Interim dividend of R7,00 per share declared

The impact from the global weaker economic growth, disrupted supply chains, depressed chemical prices and the resultant higher input costs impacted the Chemicals business negatively. Performance of our South African value chain was muted given the scheduled total East factory shutdown at Secunda and operational variability experienced, mainly due to lower productivity and coal quality in our Mining operations, contributing to lower volumes for the six months. The safety of our people and stability of our operations is a key priority. The company will continue to focus efforts on improving business performance to maximise profitability for the full year.

“We navigated several challenges during the period, including safety and operational stoppages at our Mining operations, power supply interruptions which also impacted our suppliers and customers, weaker global economic growth, disrupted supply chains and higher feedstock and energy costs. The last two factors had a particularly severe impact on the profitability of the Chemicals Eurasia and Chemicals America segments,”

said Fleetwood Grobler, President and Chief Executive Officer, Sasol Limited.

Earnings before interest and tax (EBIT) of R24,2 billion remained in line with the prior period, mainly due to a strong pricing environment which was offset by lower volumes and increasing input cost pressures, with declining demand for chemicals globally. Earnings benefitted from gains of R5,1 billion on the valuation of financial instruments and derivative contracts offset by remeasurement items of R6,4 billion.

Remeasurement items include impairments of our Secunda liquid fuels refinery cash generating unit (CGU) (R8,1 billion), South African Wax CGU (R0,9 billion) and China Essential Care Chemicals CGU (R0,9 billion) and a reversal of impairment of our Tetramerization CGU (R3,6 billion) in the United States of America, as well as a profit on partial disposal of an interest in the Area A5-A offshore exploration license in Mozambique (R266 million) and the realisation of foreign currency translation reserves following the liquidation of subsidiaries (R251 million).

“I am excited about the progress we have made towards achieving our 30% greenhouse gas emission reduction target. We have concluded power purchase agreements (PPAs) for the purchase of a significant quantity of renewable energy in South Africa totalling approximately 550 MW. In Mozambique, our gas drilling campaign is progressing ahead of plan, providing us with increased feedstock flexibility up to 2030. Our Sasol ecoFT business is also making good progress, and we have entered into several studies to determine the feasibility of producing sustainable aviation fuel (SAF) from green hydrogen and sustainable carbon sources,” concluded Grobler.

Note: this article was sponsored and written by Sasol

Adcock Ingram has delivered a masterclass here, with great earnings and dividend growth off relatively modest top-line growth.

It’s funny how just one product can cause major swings, with Panado demand normalising and volumes down by 5.4% in the Consumer business as a result. Thanks to average selling price increases of 9.8% though, turnover was higher and trading profit grew by 7.1% as costs were well managed.

In the OTC business, turnover was up 15.3% with volume growth in brands like Allergex. Although gross margin was under pressure from production costs and the weaker currency, trading profit still increased by 8.5%.

The largest segment is Prescription, which increased turnover by 9.4%. Combined with a higher gross margin, the net impact was a substantial 37.4% jump in trading profit.

The disappointing segment was Hospital, which saw turnover decline by 2.2%. Still, with gross margin going in the right direction, trading profit improved by 10%.

As you can see, the trading profit performance was impressive across the board and Adcock Ingram really did a great job here in tricky conditions. With the Single Exit Price increase of just 3.28% this year, cost control will be critical in this industry. The company has warned that gross margin compression is almost unavoidable.

The interim dividend is 20% higher at 125 cents per share and the share price was trading at just under R53.00 in afternoon trade.

Assemble, Avengers! (JSE: AEG)

A 13.4% rally was the reward for punters

I’m old enough to remember when Aveng was trading at one cent per share. Literally. In the heat of the pandemic when the Fed was making it really easy for everyone by letting money fall out of the sky into the economy, the Aveng fans called themselves the Avengers.

It’s worth remembering where Aveng came from:

Buy and hold, they said. It will be fun, they said.

You can’t see it on the chart, but the share price is down 28% over the past year. This is despite Tuesday’s rally. In case you’re wondering what happened to the “one cent” share price, there was a huge share consolidation during the pandemic.

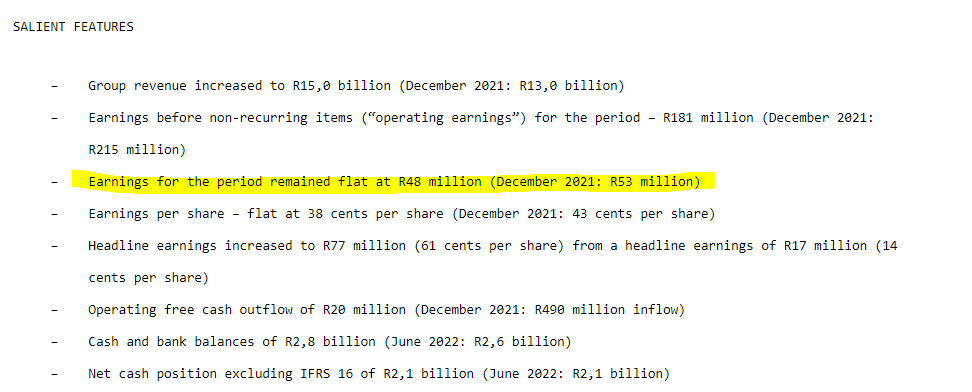

Moving on to results for the six months to December, someone really needs to help Aveng with what “flat” means. When earnings drop from R53 million to R48 million (-9.5%) that’s not “flat”:

Corporate nonsense aside, the business is clearly more profitable and has cash in the bank. The metric they don’t include in the summary is “normalised earnings” which dropped from R82 million to R44 million. So…is it more profitable?

I think the market focused on the debt. R125 million was repaid in the period. There’s another R353 million of “legacy debt” that will be dealt with by the proceeds of the Trident Steel disposal. The trade finance facility will also be settled.

The focus going forward is on McConnell Dowell in Australia and Moolmans in South Africa.

BHP on the wrong end of iron ore and copper prices (JSE: BHG)

Attributable operating profit is down 32%

Managing a mining giant isn’t easy. There isn’t much you can do about commodity prices, so you have to focus on controlling production, expenses and capital allocation.

Despite commodity prices moving against BHP in the six months ended December and revenue dropping by 16%, the company still achieved an EBITDA margin of 54%. Margins were under pressure though, as EBITDA was down 28% year-on-year.

After $3 billion found its way into capital expenditure, there was $3.5 billion in free cash flow for shareholders to enjoy.

Net debt is at $6.9 billion, which is towards the bottom of the target range of $5 billion to $15 billion. An interim dividend of $0.90 per share has been declared, equivalent to a 69% payout ratio.

BHP tells a cautionary tale for the second half of the year, noting a volatile operating environment and a global slowdown in the wake of anti-inflationary policies (i.e. higher interest rates). Much of the commodity demand depends on China.

KAP Industrial Holdings reports a drop in HEPS (JSE: KAP)

Safripol and Restonic had a particularly tough time

KAP Industrial Holdings is a well-diversified business. The downside is that one of the businesses is usually having a tough time, so the company trades in a frustrating price range that now sees it near the 52-week low of R3.68. The price closed at R3.75 after releasing results, down 3.85% on the day.

Revenue increased by 12% in the six months to December. This doesn’t help when operating profit falls by 8%, driven by a 26% decline in Safripol based on lower volumes and pressure in Restonic as well. If you read further down the report, you’ll realise that profitability took a knock across almost the entire business, with revenue up and operating profit either flat or slightly down in several divisions.

With finance costs up sharply, the impact was amplified at HEPS level, down 17% year-on-year.

The cash story is the worst one of all, with cash flow from operations down by 96% due to a R2.2 billion temporary absorption of working capital. Investors will be hoping that “temporary” is the operative word there.

The company describes the near-term outlook as “challenging and uncertain” – but they are confident in the group. Still, there’s no obvious reason why the group’s operating environment should materially improve in the second half of the year, as the macroeconomic pressures aren’t disappearing.

Kumba reports a 46% drop in HEPS (JSE: KIO)

This is despite average realised FOB export prices 13% above the benchmark

Demand for Kumba’s high-grade iron ore helped the company achieve an average price of $113 per wet metric tonne, which is 13% above benchmark prices. With production lower across the group and export sales down by 9%, that wasn’t enough to save this result.

Unit costs increased sharply, driven by inflation and lower production. EBITDA margin fell from 63% to 50%, a situation that would’ve been worse without Kumba’s cost saving efforts.

Free cash flow was 66% lower at R10.4 billion. Total dividends for the year fell by 61% to R40.

With a closing price of R540, this puts Kumba on a trailing dividend yield of roughly 7.4%.

Motus earnings are up, but watch the balance sheet (JSE: MTH)

There’s a lot more debt in the system now

In the six months ended December, Motus achieved revenue growth of 14% and EBITDA growth of 25%. Although operating profit was 22% higher, attributable profit only increased by 9%.

The difference lies in the interest costs (which more than doubled), with Motus having taken on far more debt as part of making strategic acquisitions. Net debt to equity has increased from 30% to 75% and net debt to EBITDA is up from 0.9x to 1.6x. More debt was also required for higher levels of working capital. Of the bank funding (rather than floorplan funding), only 9% is at fixed rates and the rest is floating.

Whilst growth in HEPS of 13% is nothing to get upset about, metrics like free cash flow (down from R2.9 billion to just R425 million) spooked investors. The dividend was up only 9% and investors don’t want to see a dividend growing at a slower percentage than revenue, as it means that the top-line story isn’t being enjoyed by shareholders.

In terms of market share, Motus holds 20.5% share of the retail new car market in South Africa, which contributes 65% to revenue and 78% to operating profit. The company doesn’t disclose the share in the UK and Australia but notes that it maintained market share in those countries.

Growing organically is the “cheap” but difficult way to do it. Motus uses acquisitions to grow faster, with two deals in this period. One was for Motor Parts Direct in the UK, a substantial deal for Motus. The other was a bolt-on acquisition of three Mercedes Benz passenger dealerships and one commercial vehicle dealership.

With the share price down 3%, the market must have a concern or two about this balance sheet. I know that I do.

NEPI Rockcastle: record operating income (JSE: NRP)

Management is bullish about the momentum continuing

Despite the challenging economic background and the obvious problems in Eastern Europe related to Ukraine, NEPI Rockcastle enjoyed resilient consumers in Central and Eastern Europe (CEE) who spent more per visit to the malls. With record net operating income in the year ended December 2022, the management team expects growth to continue.

The company highlights that regional malls play a huge role in CEE, which is different to the high street culture in Western Europe. That sounds rather similar to South Africa!

With a loan-to-value ratio of 35.7%, the NEPI Rockcastle balance sheet is in very good shape.

Distributable earnings per share for the year was 52.15 euro cents, which was 51.5% higher than in 2021. An adjustment is needed for a once-off item, which would see a recurring view on earnings reflecting 20% growth. That’s still impressive.

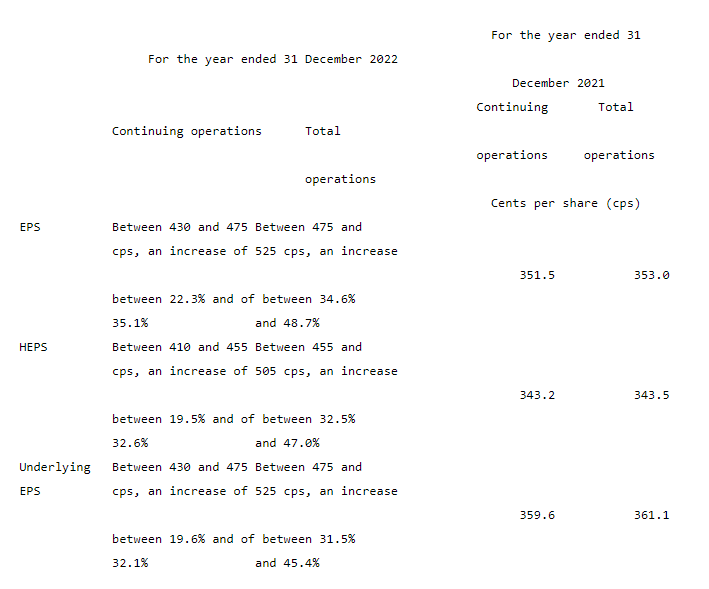

Sasol was a mixed bag in this interim period (JSE: SOL)

Local supply chain challenges dampened the earnings party

Here’s a little reminder of how crazy things got in the pandemic for Sasol vs. where they are now:

This chart hides the recent momentum, which has been poor to say the least. Sasol has lost 15.7% in the past six months as local operational issues have plagued the company.

We now have results for the six months ended December, a period during which oil prices helped but chemical prices didn’t. Pressure on input costs hit the chemicals side of the business and lower coal quality in the mining business contributed to lower volumes.

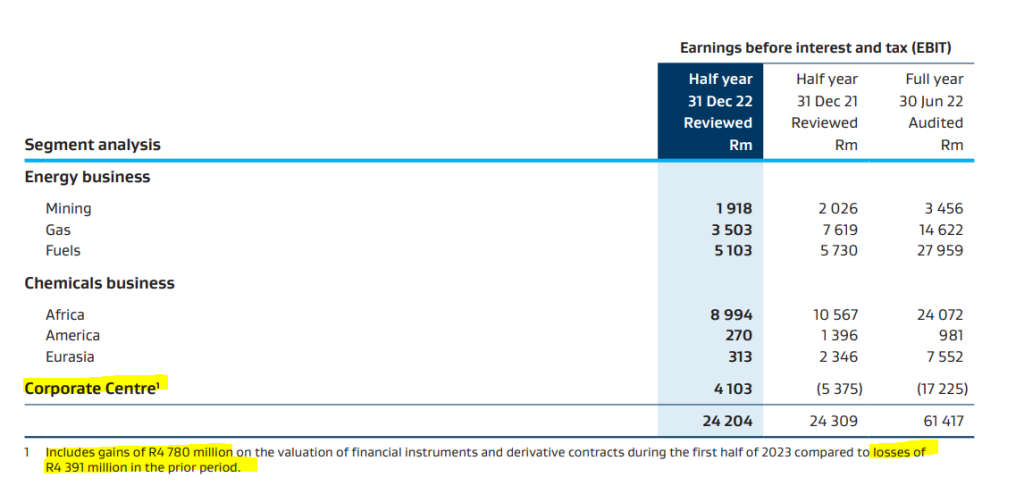

This resulted in a flat EBIT performance of R24.2 billion. There were valuation gains on financial instruments of R5.1 billion, more than offset by impairments with Secunda liquid fuels refinery as the main culprit (R8.1 billion).

You have to read really carefully when lookin at Sasol’s numbers, with the hedging at the corporate centre making a huge difference:

The mixed result means that earnings per share was down 3.1% year-on-year, but headline earnings per share (which excludes impairments) more than doubled to R30.90. The group reported core HEPS growth of 9%, coming in at R24.55.

The interim dividend is R7.00 per share, so you don’t get a particularly exciting payout ratio here. Sasol is a hungry animal in terms of capital expenditure and you can see this impact on the cash that eventually finds its way to shareholders. If you read the detailed results, you’ll see that Sasol might end up spending more than guidance on capex this year due to inflationary pressures.

The market was clearly expecting more here, with Sasol down nearly 4% by lunchtime.

Open market bids for Salungano (JSE: SLG)

RBFT Investments wants to increase its stake

RBFT Investments holds an 18.1% stake in Salungano Group and wants to make that bigger. The intent is to eventually acquire all the shares and delist the company. For now, the company wants to acquire up to 60 million shares at R1.40 per share and will be doing so on the open market.

This is an exempt partial offer, not a general offer. If you hold Salungano shares and want the price, you just need to offer the shares on the screen accordingly.

Sibanye wants New Century Resources (JSE: SSW)

Sibanye already holds 19.9% and has made an offer for the rest

Sibanye-Stillwater (which everyone just calls Sibanye) already owns 19.9% in New Century Resources, making it the largest shareholder in the company. New Century is an Australian base metal producer and a top-15 global zinc producer, operating a tailings operation in Queensland.

Sibanye wants to own all of it, which is in line with the company’s “circular economy” strategy that includes a goal to be a global leader in tailings retreatment and recycling.

If all New Century Resources shareholders accept the offer, then Sibanye will need to cough up US$83 million for the deal.

The offer price is A$1.10 per share, a whopping 42% higher than the prior day’s closing price.

Sibanye also released a trading statement and production update for the year ended December, reflecting a drop in HEPS of between 46% and 51%. This reflects the gold sector labour issues in South Africa and the severe weather event at Stillwater. The gold strike had a massive impact, with production down by 50% in that part of the business.

The share price fell 5.5% on the day to close at R39.24. For reference, the 52-week low is R39.24.

Super Group keeps doing well (JSE: SPG)

Another 2% gain takes the year-to-date performance to nearly 23%

For the six months ended December, Super Group’s revenue increased by 34.6% and EBITDA was up 24.2%. This means that margins came under pressure, but it also means that earnings grew considerably.

As we head further down the income statement, it gets exciting again with HEPS up by 30.1%.

The company certainly took advantage of favourable conditions, ranging from strong supply chain demand in South Africa in the transport business and higher revenues per load in Europe through to an increase in new car sales thanks to improved vehicle availability in South Africa and the UK. From an accounting perspective, LeasePlan in Australia was consolidated for the full six months.

Management sounds bullish after this result!

Texton: the market price doesn’t lie (JSE: TEX)

The fund trades at less than a third of NAV

After the initial news broke of the interim dividend becoming only a distant memory, Texton has now released detailed numbers.

The fund is following a rather unusual strategy, with a direct property portfolio valued at R2.2 billion and indirect investments valued at R538.5 million. Essentially, capital has been recycled from the direct portfolio into the indirect portfolio, which is how Texton has gained exposure to the US market.

Although distributable earnings grew by 5.24%, HEPS fell by 28.9% and there is no dividend per share for this period vs. 10 cents in the comparable period. The net asset value (NAV) per share increased by 2.7% to 609.51 cents. The share price trading at just R2 tells the story, less than a third of the NAV per share.

I guess this is what happens when you take shareholder capital and invest it in funds like the Blackstone Real Estate Income Trust instead. I still don’t see a single logical reason why Texton is pursuing this strategy instead of returning capital to shareholders.

The loan to value ratio is at least healthy, coming in at 26.9%.

Tiger Brands is roaring, for now at least (JSE: TBS)

For how much longer can consumers keep this up?

For the four months to January, Tiger Brands managed to increase revenue by a whopping 17%. Here’s the real kicker though: 18% is due to price increases and volumes fell by 1%.

The volume performance obviously varies significantly at category level. Snacks & Treats did well for example, whereas the Baby division reported lower volumes and a drop in market share.

Load shedding cost pressures are still coming for consumers, with costs of R27 million for generators in this period. Tiger Brands hasn’t “yet” recovered this in price, which suggests that food inflation isn’t going anywhere. Each day of stage 6 load shedding costs Tiger Brands R1.5 million in incremental costs.

To prepare for stages 6 – 8 (something most of us are living in denial of), Tiger Brands needs to invest a further R120 million in additional generating capacity. To make it worse, the bulk of this investment would be on diesel and water storage capacity to mitigate the impact of load shedding on the municipal water supply.

The inflation outlook is low double digits in the second half of the financial year. Of course, this depends on Eskom not getting even worse.

For the six months to March, Tiger Brands expects solid operating income growth. I’m once again surprised by the company’s ability to keep growing earnings in this inflationary environment.

At what point will consumers simply break? Or will the pain keep going elsewhere, like into discretionary retailers?

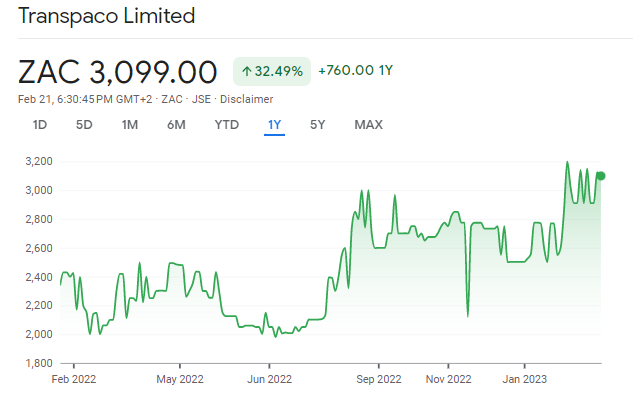

Transpaco reports a major jump in HEPS (JSE: TPC)

The dividend isn’t far behind, up more than 41%

Transpaco isn’t the most liquid stock around, so the share price chart includes those typical horizontal periods where not much happens in the share price:

Still, the 32% gain over the past year has been backed up by earnings. For the six months to December, HEPS increased by 45% to 316.7 cents and the dividend increased by over 41% to 85 cents per share. This was achieved off revenue growth of 19.8%, so this is a perfect example of operating leverage (a percentage change in revenue leading to a higher percentage change in profits because of fixed costs in the structure).

Operating margin expanded from 9.0% to 10.0%. Those aren’t the biggest margins around, but at least they are heading in the right direction.

To add to the happy news, the gearing position (level of debt) improved.

Little Bites:

Director dealings:

Two directors of Spar (JSE: SPP) sold shares worth a total of R1.27m that vested under a conditional share plan, but the announcement doesn’t specify whether this was just the portion to cover taxes.

An associate of a director of Newpark REIT (JSE: NRL) has acquired shares worth R21k.

An associate of a director of Tradehold (JSE: TDH) has acquired shares worth R13k.

Steinhoff (JSE: SNH) has agreed to settle litigation in Europe for EUR202 million. The share price dropped another 3% to 31 cents, which means it is now only 31 cents too expensive.

Shareholders of Premier Fishing and Brands (JSE:PFB) have approved the acquisition of an additional equity stake in Talhado Fishing Enterprises.

The publication of the Rebosis Property Fund (JSE: REB) business plan has been postponed for the fifth time. It is now expected by 3rd March.

Before I delve into production numbers at Anglo American Platinum (Amplats), I have to point out the relationship between the PGM prices and the USD/ZAR cross. The dollar basket price per PGM ounce fell by 8% and the rand basket price increased by 2%. Our currency depreciation obviously lends a helping hand to the Amplats business.

Despite this, production issues and lower volumes meant a 24% decrease in revenue. Those fixed costs sadly don’t disappear just because production is lower, so adjusted EBITDA fell by 32% and EBITDA margin decreased from 65% to 57%.

Headline earnings per share fell by 38% and net cash fell by 43%. With that combination, it’s perhaps not surprising that the dividend fell by 62%.

The share price only fell by 2% as these results were well telegraphed to the market ahead of time.

CA Sales Holdings jumped 7.5%

This FMCG group released exciting numbers

In a trading statement covering the year ended December 2022, CA Sales Holdings indicated that HEPS would be up between 29% and 34%. That’s a juicy growth rate by any standards, with an expected HEPS range of 76.89 cents to 79.87 cents.

After the share price closed 7.5% higher at R7.05, this is still only a Price/Earnings multiple of around 9x at the midpoint of guidance.

City Lodge is profitable again

But HEPS looks a little light vs. the share price

In case you’ve been living under a rock, the tourists are back and the good times are flowing. City Lodge is thrilled to see the end of COVID, with numbers that are back in the green.

If we exclude the once-off settlement for business interruption insurance, then City Lodge achieved HEPS for the interim period of between 12.6 cents and 14.5 cents. That’s a vast improvement from the loss-making comparable period that was ruined by the pandemic.

Still, with a share price of R4.81, that doesn’t seem like a particularly great outcome. Even if we double this period, a simplification of note when you consider an ongoing month-on-month recovery (mitigated to some extent by recognising that the summer holidays must be the best time for this business), then it’s on an annualised Price/Earnings multiple of 17.8x.

Hmmm….that’s rather a lot, isn’t it?

The share price closed 2.8% lower after this announcement.

A positive Mpact

A 6.5% rally rewarded shareholders on Monday

For the year ended December, revenue from continuing operations was up 7%. The underlying operations did even better than this, as the base period included the major distribution agreement that Mpact terminated. Without that impact, revenue would’ve been up by 15% and volumes by 6%, so the benefit of higher pricing is clearly visible.

The volume growth was all in the Paper business, as the Plastics business saw flat volumes year-on-year across most of that division.

The joys of operating leverage are being felt here, with earnings before interest and tax (EBIT) up by 23% year-on-year. The “I” in “EBIT” is a bit painful though, with net finance costs of R180 million in 2022 vs. R140 million the year prior, driven by increased average net debt and higher interest rates.

Due to capital expenditure and increased working capital, net debt increased from R1.756 billion to R2.327 billion.

Looking ahead, Mpact will be investing R1.2 billion in its Mkhondo Paper Mill in response to growth in demand from the South African export fruit sector. Mpact hasn’t been shy to invest in its operations in general, including in major solar projects.

In case you’re wondering about discontinued operations, the Versapak business is held for sale. The company reported 20% growth in revenue and a strong improvement in profitability from net earnings of R2 million to R65 million. This is encouraging for potential offers that Mpact might receive.

I would really love to tell you what the HEPS increase will be. Sadly, the formatting of the SENS announcement was a complete disaster, so I’ll just include it here for you to decide for yourself:

Either way, earnings are up strongly and the market liked that, even if nobody was quite sure how to read this.

Murray & Roberts says bye-bye to Bombela

Strong shareholder support was achieved

This is a short update for Murray & Roberts, but one that is too important to be buried in the Little Bites. The company desperately needs to make progress on fixing its balance sheet, with the disposal of Bombela Concession Company firmly part of that strategy.

At the general meeting of shareholders to vote on the deal, it received overwhelming support, with 99.988% of votes cast in favour of the transaction.

Clearly, this deal is moving forward.

No dividend at Texton

There’s an abundance of caution here

If you invest in a property fund, it’s usually because you want to earn a dividend. Sorry for you if Texton was your fund of choice, because the old dividend of 10 cents per share is but a distant memory. For the six months to December, there is no interim dividend at all.

This is despite an increase in distributable earnings of 5.2%.

The board wants to “conserve cash” and “manage its balance sheet liquidity through the current interest rate environment” – so time will tell how this plays out.

WBHO updates its earnings guidance

There is a strong year-on-year improvement in profitability

Construction group WBHO has finished its work on the accounting impact of the Australian tax position on the 2021 numbers.

Based on this calculation, HEPS from continuing operations is expected to be between 800 cents and 828 cents for 2022 vs. 591 cents in the comparable period, an increase of between 35% and 40%.

Little Bites:

Director dealings:

A director of a subsidiary of Tharisa has sold shares worth R221.5k

A prescribed officer of Barloworld has bought shares worth R142k.

An associate of a director of Huge Group has bought shares worth R58.2k.

If you are an Alviva shareholder, keep an eye on your trading account on 6th March. That’s when the cash from the implementation of the Alviva delisting should be yours for the taking.

Spear REIT repurchased 2.83% of shares in issue between July 2022 and February 2023, at an average price of R7.62 per share. The current share price is R7.13, so ongoing buybacks will hopefully continue to bring the average repurchase price down.

The City of Johannesburg Valuation Appeal Board has upheld the municipal valuation proposed by the city for Sandton City, so the rates bill for Liberty Two Degrees is higher than they would like. With a provision needing to be recognised for arrear rates and interest, the impact on the year ended December 2022 is 2 cents per share. On a closing share price of R4.45, that’s not a huge impact on the yield.

Jasco Electronics Holdings increased 9% despite reporting a headline loss from continuing operations of between -6.3 cents and -6.5 cents. For those looking for silver linings, at least the order book is a lot healthier.

In the latest episode of Ghost Stories, Renergen CEO Stefano Marani took a break from a busy capital raising schedule to have an in-depth conversation with The Finance Ghost. After the first half of the show focused on the background to the project and the importance of helium to the global economy, the second half looked at the capital raising strategy.

Topics covered in the show include:

Stefano’s background in investment banking in the pre-GFC days, with the events of 2008/2009 leading to a career shift and the eventual investment in what would become Renergen.

The future-proof nature of helium, including several examples of industrial and technological applications for which there is no known substitute.

The importance of government support over the lifetime of this project.

South Africa’s geographical and geopolitical positioning, both of which are helpful to Renergen.

The logistical challenges around transportation of liquid helium.

Renergen’s plan to self-power its operations, making it grid agnostic in a country that we know doesn’t have enough electricity.

The Cryo-Vacc and the helium tokens – what happened to these headline grabbers?

The group structure and the way this drives the capital raising strategy with asset-specific funding partners.

An overview of Phase 1 vs. Phase 2 of the project.

The use of accelerated bookbuilds and why they are a necessity in South Africa vs. rights offers.

The capital raising strategy going forward, including the pursuit of a full listing on a US exchange rather than an OTC listing.

The likelihood of achieving meaningful liquidity in the US vs. what a company like Karooooo has experienced on the Nasdaq.

And on a fun note – the positive social impact of Renergen’s sponsorship of local rally racing.

Helium is the second most abundant element in the universe, but on earth it is relatively rare. It’s a colourless, odourless, tasteless, non-toxic gas that is lighter than air. Helium is found in natural gas deposits, and it is produced by radioactive decay. For many years, helium was used primarily for balloons and other recreational purposes. However, in recent years, its importance in modern technology has grown significantly.

The primary use of helium today is in cryogenics, or “extremely cold temperatures”. It is the only element that remains liquid at near absolute zero temperatures, making it an essential coolant for many scientific and industrial applications, but also the only propellant for rockets making it integral to space exploration and launching satellites. It has the same purpose in a rocket as the gas in your deodorant can: to push the important contents out at high speed. Back on earth though, it is used in magnetic resonance imaging (MRI) scanners, superconducting magnets, and particle accelerators.

Being inert, it has many industrial uses such as in welding, manufacture of semiconductors, manufacture of fibre optic cables, in laboratory equipment and many more. The world became acutely aware of the global semiconductor shortage after COVID, and this gave rise to increasing geopolitical tension over Taiwan’s sheer dominance in their manufacture. What few realise is that one of the primary reasons for the shortage of semiconductors was the critical short supply of helium over the period, which is now creating a significant opportunity for helium producers given the US’s approval of the recent stimulus package to construct semiconductor factories in the US, thus creating significantly more demand for this gas.

As technology advances, the uses of helium will only continue to increase. Its unique properties make it an essential part of modern life, and its importance will only grow in the years to come.

New technologies such as quantum computing and fusion (endless clean energy) are only possible with vast quantities of helium, in much the same way that most modern nuclear reactors have a helium cycle to transfer the heat from the reactor to the steam boiler to eliminate the risk of contamination in the event of a malfunction.

Most of the elements on the period table have a substitute of one kind or another, and in this regard helium is truly unique. It exhibits properties not shared with other gases, and as a result if the world were to run out of helium, most of our modern technology we enjoy would disappear along with it. This presents an interesting challenge however, as its most famous property is that it is lighter than air. If you release it, such as letting a balloon fly away for example, the helium escapes earth’s gravity and leaves the planet. This is not true of any other commodity we use. With sufficient money and resources, everything can be recycled, but not helium making it the world’s truly only diminishing resource.

Many ask if it can be made in a laboratory, and the short answer is yes. The full answer is that man-made helium costs around US$14 million per kilogram and is missing a neutron; in over 70 years the planet has only stockpiled 26 kilograms of this stuff. It’s called Helium-3, an exceedingly rare isotope of helium that when it comes near a radioactive source changes to normal helium and alerts you to the presence of the radioactivity. Clearly, guessing its purpose isn’t very difficult. It has been discovered on the surface of the moon in parts per million, and the Chinese government has now begun making plans to mine it on the moon and bring it back to earth.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Zeda’s first update as a listed company was excellent.

Emira Property Fund showcases a year-on-year recovery in its portfolio.

Attacq is selling 30% of Waterfall City to the GEPF as a great price for listed shareholders.

Italtile and Cashbuild are struggling with consumer confidence and affordability for home improvement projects.

Pan African Resources, AngloGold, Gold Fields and DRDGOLD gave a flurry of gold mining updates that didn’t tell a great story for the sector.

Absa is a red bank with green numbers that look highly impressive.

Discovery didn’t impress anyone with its attempt at adjusted earnings – interest rates are too important to just ignore.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Very few people use “Absa” and “high performance” in the same sentence, yet the post-Barclays reality for the bank has been something to behold. Released from the shackles, the bank may be red but the results have been green.

For the year ended December 2022, headline earnings per share (HEPS) is expected to increase by between 10% and 15%. There are major macroeconomic headaches in Ghana, without which normalised HEPS would’ve been up by more than 20%. This gives a good indication of how the rest of the group is performing, as the exposure to sovereign bonds in Ghana is an isolated (and annoying) issue.

Revenue increased by mid-teens in 2022, with non-interest revenue (NIR) growth as a major contributor. This is always terrific news for a bank, as it drives Return on Equity (ROE). When ROE is higher, the bank trades at a better Price/Book multiple. In other words, shareholders make money.

Pre-provision profit growth is expected in the mid-20s (which is brilliant) and the cost-to-income ratio is dropping to the low 50s. The bank is becoming more efficient relative to its revenue.

Critically, the credit loss ratio is expected to be similar to the interim level of 91 basis points, excluding charges related to the Ghana sovereign bonds.

ROE is expected to be slightly below 17% including Ghana, or 18% without it. Either way, that’s well in excess of the cost of equity, so Absa is doing all the right things for shareholders. With the dividend payout ratio going up as well, this is an excellent performance even with the pain in Ghana.

Aveng drops after a trading statement

Normalised earnings have decreased sharply

For the six months ended December, Aveng managed to increase group revenue by 16%. McConnell Dowell in Australia was a helpful contributor here with revenue growth of 22%. In South Africa, Moolmans is experiencing a drop in revenue based on project timing vs. the prior period. Revenue at Trident Steel (the business being sold) is up 58%.

The pipeline (measured by “work in hand”) has increased by 64% since 30 June 2022.

Despite the efforts of the Australian business, group operating earnings are expected to be lower by 13% to 17%. Without any normalisation adjustments, headline earnings per share (HEPS) is expected to increase dramatically from 14 cents to between 59 cents and 64 cents. The problem is that once normalisation adjustments are included, the earnings aren’t nearly as rosy.

Normalised earnings are expected to be 44% to 52% lower in this period.

Detailed results are due on 21 February, so investors won’t have to wait long to get the details.

Barloworld: heavy on the narrative

Light on the numbers

Hot on the heels of Zeda’s excellent update the previous day, Barloworld has updated the market on trading conditions for the four months ended January 2023. Remember, Zeda (the mobility business – car rental etc.) was unbundled by Barloworld at the end of 2022.

In Barloworld’s update, there’s a LOT of commentary and not much in the way of numbers, so we need to read carefully and figure out what the most important points are.

In the Equipment southern Africa business (and yes, they use a small “s”), demand from the mining sector has driven solid revenue numbers in both machine sales and aftersales parts. They make more profit on the latter, so a shift in mix towards machine sales has resulted in a slightly lower operating margin. With a strong order book for the rest of the year, there has been investment in working capital. You can expect to see that impact on the balance sheet.

Notably, things are looking up in the DRC, where the Bartrac joint venture is posting profits and is expected to continue to do so.

In Equipment Eurasia, Mongolia is doing well and Russia is performing ahead of expectations. The Russian results are obviously down from the prior period (which happened to be a record), but Barloworld is trying to find a way to operate responsibly. Remember, with our political affiliation to BRICS, this isn’t the situation that faced US companies who were forced to pull out of Russia almost overnight. In Mongolia, the business was positively impacted by the opening of borders in China, allowing products and commodities to flow freely.

Overall, Mongolia is expected to be up year-on-year on all metrics and Russia is less of a drag than expected.

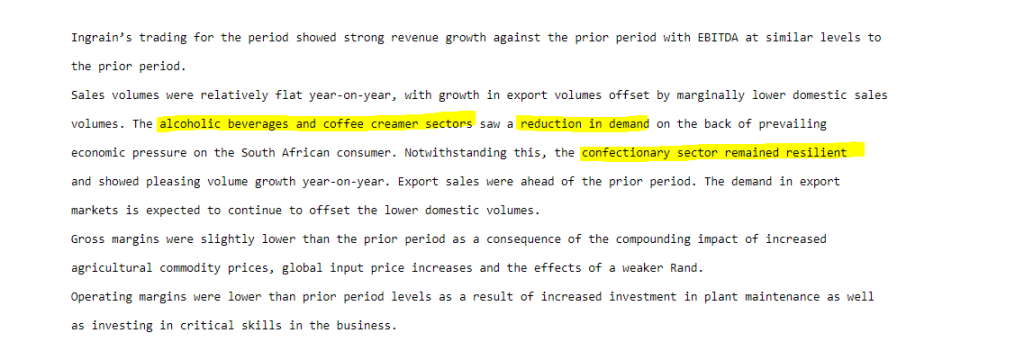

The Ingrain business (which you may recall was acquired from Tongaat Hulett) achieved “strong” revenue growth and “EBITDA at similar levels” to the prior period, which means margins contracted. Here’s a fun excerpt telling us that things are so bad in South Africa that we don’t even bother with the alcohol and coffee anymore, we just head straight for the chocolates drawer:

Barloworld is very good at balance sheet management. For me, they were the stand-out performer in the pandemic in terms of managing a crisis and coming out even stronger. I’m not surprised that the group is happy with the state of the balance sheet.

Look out for a pre-close update closer to the end of March.

Blue Label Telecoms is still hard to understand

Even accountants struggle with this one

Blue Label Telecoms is one of the trickiest companies on the JSE to get your head around. They are masters of doing highly complicated deals that usually end up disappointing shareholders. A share price that is down 58% over five years is proof of that.

In complexity though, one finds opportunity. Over three years, the share price has more than doubled. This is a highly volatile stock, which is why traders like it. There isn’t much excitement for traders in focusing on a company that trades in a tight range and goes up 7% every year.

The latest update is perfectly on brand for Blue Label Telecoms, because hardly anyone understands it. The share price dropped 5% in frustration, with group earnings down spectacularly. Even core headline earnings per share was down between 92% and 96%.

There were huge losses recognised on the Cell C investment, including the impact of the restructuring of the business. If we casually ignore that, then HEPS would be up 14%.

Blue Label is trading at the same levels as during the aftermath Global Financial Crisis. For those of you who are too young to remember, that was in 2008/2009. Whilst I can understand why traders try hard to get on the right side of these spectacular upswings, this management team’s track record with capital allocation is truly horrible. I wouldn’t have a long-term investment here.

Dis-Chem reports uninspiring retail sales numbers

On a like-for-like basis, consumer pressures are showing

With a drop in the share price of around 2.3% after releasing this announcement, the market has spoken. Dis-Chem trades on a high earnings multiple and that makes it vulnerable to any slowdown in performance.

For approximately the 5 months to the end of January, the group achieved revenue growth excluding COVID-related products (like vaccines) of 8.7%. That sounds ok, but like-for-like revenue growth in the retail side of the business was only 4.4% and that isn’t ok. An important difference between those numbers is the acquisition of Baby Boom, which was rebranded to Dis-Chem Baby City.

The company highlights vitamin C and zinc sales in the base period as a factor in the slower retail sales growth. They wouldn’t strip those out as being purely COVID-related, as as these products were accelerated by COVID but not entirely reliant on it. This is part of why growth is lower. Still, it seems incredible that those two products can have such an impact at group level.

Dis-Chem doesn’t suffer as much from load shedding as retailers with cold chains, but the diesel expense was still 54% higher at R36 million over this period.

The wholesale business is doing well, with external customer revenue up by 18.7% and overall wholesale revenue up by 8.6%. The Local Choice (TLC) franchise stores achieved revenue growth of 21% and there are now 165 of these stores.

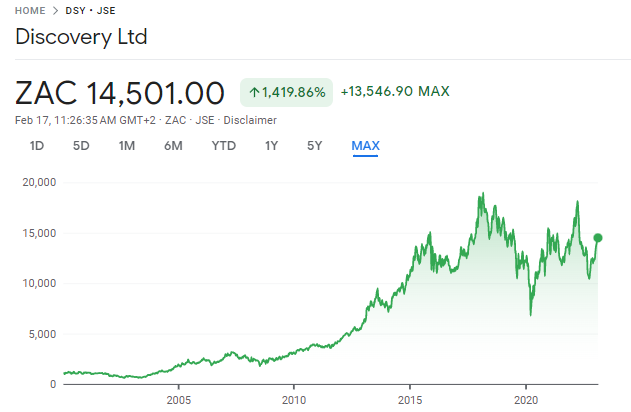

Discovery pretends that interest rates don’t exist

“Normalised” earnings look great, at least

If you bought shares in Discovery in October 2015 and ignored your broking account for 7.5 years, what would your gain on your Discovery shares be?

Zilch. Nada. Nothing.

The dividends don’t cut it, I’m afraid. After Discovery won huge market share and became a household name in South Africa, the returns stagnated and things got a lot harder. Check out this share price chart:

If this investment was on Vitality, it would be Blue Status. There wouldn’t even be a discounted smoothie.

With headline earnings for the six months ended December expected to decline by between 7% and 12%, it doesn’t seem to be improving. There’s always something causing an issue. But on a “normalised” basis, the growth is magically between 27% and 32%.

POW! Straight to Diamond Status you go, thanks to a few adjustments. The market is smarter than that, with a small positive share price move based on this announcement.

The normalisation is driven by adjustments for the effects of interest rate changes. These apparently have no impact on the operations, yet they can swing a drop in headline earnings into an increase of potentially over 30%.

No impact indeed. I think we can all agree that interest rates can’t just be ignored.

Looking through the noise, what do investors need to know?

There isn’t a huge amount of detail in this trading statement, but we do know that Discovery Bank is performing in line with the plan. The group aims to bomb 10% of normalised operating profit on new initiatives, with the numbers running close to this level. As for whether investors will ever see a return on Discovery Bank, the jury is still out.

The other important news (and a contributor to negative earnings in this period) is that the lifting of zero-COVID lockdowns in China has led to waves of infections. Ping An Health Insurance has taken a conservative approach to provisions here, although claims have been limited thus far. The investment returns in China also took a knock in this period, though lifting of lockdowns should help with that as Chinese equity markets have rallied considerably.

Steinhoff: ugly, but fair

Sadly, life just isn’t fair

The agreement that Steinhoff is trying to implement with its creditors is a hideous outcome for shareholders. It remains beyond me why anyone is buying shares in Steinhoff at the moment. Nevertheless, it is still trading at 35 cents per share.

Although there really isn’t much left for shareholders in this structure, the reality is that the situation is “fair” to shareholders in the financial sense. EY was engaged to provide a fairness opinion and has made various assumptions in the process, mainly around the lack of meaningful restructuring alternatives for Steinhoff.

On that basis, the proposed restructuring has been found to be fair. If you’re curious, you can read the opinion here.

Little Bites:

Director dealings:

The directors of Jubilee Metals certainly bought the dip this week. The CEO put R535k behind the company, the independent chairperson bought R646k worth of shares and the ex-chairperson was good for R408k. With the share price under serious pressure in recent days, the market liked this.

Jonathan Ackerman has taken early retirement as an executive director of Pick n Pay, marking another step that the family has taken away from the retailer. Having said that, he will stay on the board in a non-executive role.

In a trading statement released on Wednesday, African Rainbow Minerals highlighted that headline earnings should be between 34% and 44% higher, with the manganese and coal operations as the major drivers here.

There were several asset impairments that led to a much lower increase in earnings per share (between 8% and 16%). This is a good example of one of the major differences between HEPS and EPS, as impairments are excluded from the former.

Not much fire at Brimstone

HEPS is down between 72% and 82%

Brimstone is an investment holding company, so I would’ve thought that net asset value per share would be a useful measure of performance. Nevertheless, the Brimstone trading statement focuses on earnings per share and reflects a drop in HEPS of between 72% and 82%. That’s not pretty.

There are several reasons for this, ranging from lower profitability at Sea Harvest through to higher finance costs. Detailed results are due on 7 March.

The Equites – Shoprite relationship continues

Good business is about partnerships, like this one

When it comes to being a strong tenant, it’s hard to fault Shoprite. The group is growing beautifully and has immense financial muscle. Equites Property Fund specialises in logistics properties and has a funding profile that suits this strategy, where Shoprite investors are looking for a different risk-return opportunity vs. a property fund.

The Equites-Shoprite relationship is interesting, as the parties seem to be able to do a variety of different types of deals. In the latest example, Equites is going to acquire an existing logistics campus from Shoprite for R560 million. There’s another R78.2 million changing hands for undeveloped land and costs already incurred by Shoprite as part of the development plan.

Over and above the R78.2 million, Equites expects to invest R344 million in extending the facilities.

These are long-term plays, with a 20-year lease with Shoprite and three additional 10-year lease renewal periods. The initial rental yield is 7.75% and the rental will escalate at 5% per annum. The initial yield is where I feel a little uneasy, as that seems to be on the low side in this environment.

Equites’ loan-to-value ratio will increase by 230 basis points due to this deal, which will be funded through a combination of undrawn debt facilities and capital recycled from property disposals.

Grindrod Shipping: which way will it go?

Supply – demand dynamics have swung sharply

In Textainer’s recent quarterly update, we saw a drop in fleet utilisation rates. 2022 was a record year for the container company and so the year-on-year story needs to be interpreted in that context. Still, demand for containers has cooled off.

With a quarterly update from Grindrod Shipping now available to us as well, we can see the same trend coming through. Revenue in the 4th quarter was only $81.4 million vs. $460.5 million for the full year, so that’s a big slowdown in the final quarter.

Gross profit is even worse, coming in at $23 million for the quarter. Over the preceding three quarters, total gross profit of $143.8 million had been generated. You don’t need to get the calculator out to figure that negative momentum out for yourself.

The company actually reported a loss in the fourth quarter of $4.6 million. Adjusted net income was $10.6 million though, with various non-recurring charges taken out. I would still be careful of putting too much importance on the adjusted number.

Instead, I would focus on this paragraph from the announcement:

When a cyclical business starts talking about reducing debt, having more flexible liquidity and optimising operations, you know that the good times are coming to an end.

So, would you go long or short this share price chart?

South32 looks forward to better margins

The first half of the year wasn’t a happy time

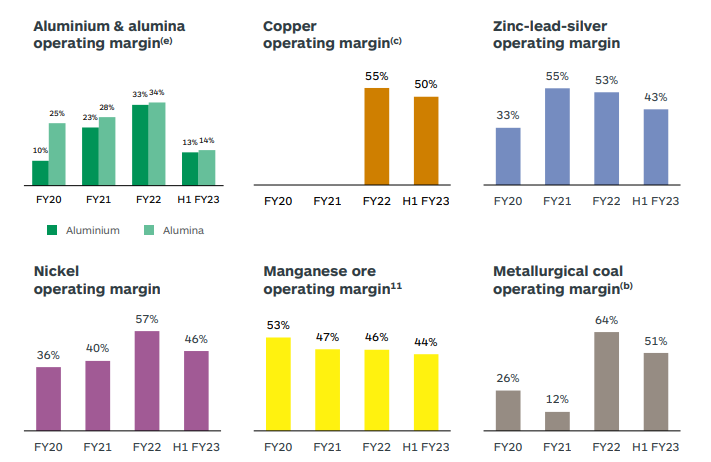

South32 has a very interesting commodity mix, which includes aluminium, copper, nickel, zinc-lead-silver, manganese ore and metallurgical coal. There are over 25 exploration prospects, so the group has plenty of options out there. The projects are also found in several continents, so South32 is a diversified resources play.

Metallurgical coal contributed 30% of EBITDA in the first half of the year. The next largest contributors were manganese ore (17%) and nickel and copper, both 13%. Margins have come under pressure across the various commodities, as shown by this excellent slide from the investor presentation:

The group highlights the reopening of China as underpinning a commodity price rebound to start the second half of the year. Operating margins are highly sensitive to the commodity prices of course, with South32 doing everything possible to manage what it can control (e.g. operating costs).

Full year guidance is unchanged and the company is still aiming to deliver production growth of 6% for the full year. This will help drive lower unit costs, which should improve margins.

For the first half of the year though, the margin pressure is biting. Revenue is down 8% and the ordinary dividend is down by a whopping 44% as HEPS has decreased by the same percentage.

Despite this, the share price is up 16% in the past year. Like Glencore, it’s been a solid performer through the pandemic.

Zeda is off to a cracking start as a listed company

Performance in the quarter ended December was strong

There are two really important things that you want to see as an investor: an increase in revenue and an expansion (or at least maintenance) of the EBITDA margin.

Zeda has achieved both these things in its inaugural quarter as a listed company, having been unbundled by Barloworld back in November. Revenue is up 24% and EBITDA is up 23%, so that’s really strong growth with EBITDA margin protected at around 38%, a juicy number in an of itself.

Zeda is primarily a car rental and fleet business and the holiday season is obviously critical for that model. Interestingly, this result was achieved despite an average utilisation rate for the quarter of only 70%. This was negatively impacted by the delivery of vehicles that Zeda had ordered ages ago, which is further evidence that supply chains have loosened up (refer to the Grindrod Shipping update).

An important element of the strategy is the mix between discretionary business (like travel) and contracted services (like insurance and monthly subscriptions), with the latter contributing 55% of revenue.

The optionality in this business lies in the opportunity to improve the utilisation rate, as revenue of the car rental business is ahead of pre-pandemic levels despite billed days only running at 68% of 2019 levels. They are targeting utilisation of 73% to 75% for the full year, which would deliver solid results.

The leasing business is a great revenue underpin for this group and is stable, with focus on the corporate business and value-added products.

On the used car side, both retail and wholesale sales recorded growth and margins were stable despite the supply of vehicles improving. Surprisingly, demand was strong in an environment of higher interest rates, inflation, fuel hikes and load shedding.

I haven’t included this under director dealings because I didn’t want to confuse you. Back in 2021, a director of Harmony Gold (at the time) casually sold R5.9 million worth of shares and didn’t get permission because of an “administrative oversight” – I have no idea what penalties or similar would be applicable in this case, but I hope something applies. If it doesn’t, then what is the point of even having these rules?

AECI has appointed Holger Riemensperger as the group CEO. As you probably guessed from his name, Riemensperger is an international appointment who comes to the group with extensive experience across many regions.

The terminated 2022 deal between Murray & Roberts (M&R) and Italian group Webuild for the R445 million disposal by M&R of Clough Australia, is back on. Creditors have followed the recommendations of the administrators and voted in favour of the deal bringing an end Clough’s voluntary administration process.

Sanlam’s partial offer to shareholders for the acquisition of up to a 43.9% stake in Afrocentric Investment has been exceeded with acceptances representing 46.4% being received. Sanlam made the offer in October 2022 at R6.00 per share.

Acsion has acquired an unoccupied industrial property in Pilea, Greece for a cash consideration of €9,24 million. The property was previously owned by a Greek company in liquidation, Philkerman-Jonson.

Equites Property Fund has acquired from Shoprite the logistics campus in Canelands, KwaZulu-Natal. The acquisition cost of the existing campus is R560 million with a further R78,25 million payable for undeveloped land and costs already incurred by Shoprite in respect of the Development Lease Agreement.

Metrofile has acquired an additional 15% stake in E-File Masters, the legal entity for Metrofile Middle East which is headquartered in the UAE. The additional stake, the value of which was undisclosed, increased Metrofile’s shareholding to 95%.

In a proposed transaction, Attacq will dispose of a 30% stake in Attacq Waterfall Investment Company (AWIC) to the Government Employees Pension Fund (GEPF) for an estimated cash consideration of R2,5 billion. In addition, the GEPF will inject a further R300 million into AWIC as a shareholder loan. Should the transaction be implemented, Attacq will retain control of AWIC and continue to provide asset management and administration services to AWIC at market-related fees.

Spear REIT has disposed of the property known as the Liberty Life Building in Century City, Cape Town to Capitec for R400 million. The sale provides Spear with rebalancing opportunities and an investment bias towards industrial warehousing, logistics and retail assets within the Western Cape.

Unlisted Companies

Moshe Capital, a black-women-owned firm, is to take a 20% stake in Pragma Holdings, an engineering services company to local and international companies across various sectors from mining to retail.

Engen and Vivo Energy are to combine their respective African businesses to create one of the continent’s largest energy distribution companies. The combined group will have over 3,900 service stations and more than two billion litres of storage capacity across 27 African countries. Petronas will sell its 74% shareholding in Engen to Vivo Energy at completion while Phembani will remain invested as a 21% shareholder in Engen’s SA business.

EOH’s rights offer which closed on 10 February, 2023 was oversubscribed, raising R500 million as first announced in November 2022. All 384,615,384 shares were issued at R1.30 per share. In addition, Lebashe Investment Group subscribed for 76,923,076 shares raising a further R100 million.

Alternative trading platform ZARX has had its license cancelled by the Financial Sector Conduct Authority. The Public Investment Corporation holds a 24.14% stake in the exchange. ZARX’s license was suspended in August 2021 due to liquidity and capital adequacy noncompliance.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Argent Industrial repurchased 51,429 shares representing 0.09% of the issued share capital of the company for an aggregate value of R787,19 million.

Hudaco Industries repurchased 1,562,860 shares at an average price of R151,05 per share for a total value of R236,1m. The shares will be delisted and cancelled.

Textainer announced it has repurchased 1,543,267 shares at an average price of US$29.29 per share during the fourth quarter of 2022.

Glencore this week repurchased 22,600,000 shares for a total consideration of £132,59 million. The share repurchases form part of the second phase of the company’s existing buy-back programme which is expected to be completed this month.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 6 to 10 February 2023, a further 3,087,207 Prosus shares were repurchased for an aggregate €228,2 million and a further 520,956 Naspers shares for a total consideration of R1,77 billion.

Nine companies issued profit warnings this week: Pan African Resources, Curro, PSV, Anglo American Platinum, Santam, Gold Fields, Cashbuild, AngloGold Ashanti and Brimstone Investment.

Four companies issued or withdrew cautionary notices. The companies were: Premier Fishing and Brands, Attacq, African Equity Empowerment Investments and Life Healthcare.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")