The following are those deals shortlisted for the Exxaro BEE Deal of the Year 2022. The DealMakers Independent Panel have selected these transactions from the nominations submitted by the M&A industry advisers. They are, in no particular order:

Old Mutual’s ‘Bula Tsela’ BEE transaction

During the Old Mutual separation process announced in 2018, the company undertook an empowerment commitment to increase its BEE ownership to 30% by June 2023. The disposal of a further 4.36% stake in 2022 in a three-legged process involving employee and community trusts and a retail offer, satisfied this commitment. The R2,8 billion deal involved complex funding options of notional vendor financing to the trusts and actual vendor funding to the retail scheme.

The local advisers to the deal were: Rand Merchant Bank, Tamela, Merrill Lynch, Bowmans, PwC and Deloitte.

Shoprite Checkers’ evergreen B-BBEE transaction

The announced R8,9 billion transaction in May 2022 was the first of its nature in the retail sector – the deal at Shoprite’s subsidiary boosted its B-BBEE ownership to 19.2% from 13.5%. The deal recognises its employees’ role in the success of the group by providing them with additional compensation over and above their salary. The evergreen B-BBEE Employee Benefit Trust will hold 40 million shares in the local subsidiary and employees will receive dividend entitlements but will not own the shares, so the transaction will not have an impact on the shares in issue in the listed holding company. Non-SA employees will also receive equivalent payment to that of its local employees.

The local advisers to the deal were: Rand Merchant Bank and Werksmans.

Seriti Resources’ acquisition of Windlab Africa

The acquisition by Seriti of a major stake in Windlab Australia’s South African and East African wind and solar-powered businesses, marked the transfer of strategically important renewable assets from foreign ownership into the hands of a black energy company. Windlab Africa has developed 230MW of projects currently operating and supplying the SA grid. The 54.2% stake in Windlab Africa for c.R892 million acquired via subsidiary Seriti Green, speaks to its goal of ensuring long term sustainability as a diversified energy producer. Seriti is currently Eskom’s largest black-controlled coal supplier.

The local advisers to the deal were: Standard Bank and White & Case.

Anglo American Platinum’s B-BBEE transaction

The company’s new employee share ownership plan valued at R1,8 billion, announced in September 2022, will issue to employees (SA and Zimbabwe) listed shares valued at R8,000 each year with each tranche vesting three years after allocation, and participation in the evergreen ownership of 2% of Rustenburg Platinum Mines (RPM). The RPM shares will be held into perpetuity on behalf of qualifying employees and shares will be fully funded by Amplats with employees receiving dividends as and when declared.

The local advisers to the deal were: Rand Merchant Bank, Merrill Lynch and Webber Wentzel.

The winner will be announced at the ANSARADA DealMakers Annual Awards on 21 February, 2023 at the Sandton Convention Centre.

It’s quite incredible how sentiment can change towards economies in the course of a few weeks or a few months. But that is precisely what has happened with respect to not only the US but also the EU economies in the past few months. Chris Gilmour elaborates.

Did Powell get it right?

It seems like yesterday that many observers were warning about US inflation getting out of hand and US Federal Reserve chair Jerome Powell perhaps having gone too far and precipitating a deep recession in the US. Others were saying he hadn’t gone far enough and that a return to the days of Paul Volcker and 20% plus interest rates was on the cards.

In any event, it appears as if Powell’s recipe for interest rate increases has been pitched just right.

Consensus is now for a mild recession in the US, beginning in March this year and only lasting a few months. Inflation and interest rates will probably begin easing towards year end.

Europe: not as bad as feared

Europe, where all sorts of nasties were being touted, most as a direct result of the Russo/Ukraine war, isn’t looking nearly as bad all of a sudden. Germany isn’t going into recession after all and its manufacturing base is able to soldier on, albeit that it has had to pay a lot more for its energy supplies. The European winter has turned out to be remarkably benign, with many European ski resorts literally having no snow other than artificial snow created by snow cannons.

Gas stores will easily last the entire winter.

Of course, next winter may well be very different, especially if Russia does indeed cut off all supplies to Europe by then. But for the meantime, tales of Europe’s demise appear to have been greatly exaggerated.

Even the UK, the “sick man of Europe” now that it’s hobbled by rolling industrial action, may just miss recording a technical recession in the last quarter of 2022 by the skin of its teeth. Figures from the Office for National Statistics (ONS) showed that the UK recorded a slight year on year uptick in GDP growth in November of 0.1%, compared with a consensus of 0.2% decline. In the three months to end September, GDP shrank by 0.3% and the bean-counters at the ONS have calculated that the UK’s GDP would need to have fallen by 0.5% in December in order to have two consecutive quarters of negative economic growth, the classical definition of recession.

What does this mean for stocks?

So with all this relatively less bad news in mind, why are global equity markets (especially in the US) performing so poorly?

The S&P 500 is down around 18% from its peak at the time of writing.

The answer probably lies in the combination of mistrust of the Fed (maybe Jerome Powell and his colleagues on the FOMC will keep on hiking beyond year-end) and the realisation that generally higher inflation and interest rates are here to stay for the time being.

That’s bad news for tech stocks, which have been the main drivers of the US market in recent years. One only has to look at the scale of layoffs currently taking place in Silicon Valley stocks to appreciate the real impact of the downturn on this segment of the market. A strong dollar doesn’t help either, but as rates begin to be perceived to be peaking in the US, the strength in the USD will likely falter.

But eventually investors and speculators alike will start buying tech stocks again once they perceive the rout to be over. In the meantime, attention is probably likely to be more focused on commodity-type stocks that will do well out of higher demand for basic metals and materials. All those cynics who said that the JSE was finished and that the only place to invest was offshore are now eating their words, as the JSE All Share hits news highs almost every trading day.

Every dog has its day and the JSE was a real dog for a long time. So enjoy the current boom while it lasts, because it never does.

This article reflects the independent views and opinions of Chris Gilmour, which are not necessarily the same as The Finance Ghost’s opinions on these stocks. For equity research on South African retail and other stocks, go to www.gilmour-research.co.za.

Sales are down, yet the share price barely moved in response

Eventually, battered and bruised, a share price stops getting a bloody nose every time numbers are released. It can sometimes be a buying opportunity, though there are no guarantees that things won’t deteriorate further.

Cashbuild is down 30% in the past year, so there is no shortage of pain among investors. The civil unrest was incredibly damaging to Cashbuild and the company took a long time to recover. By the time trading was largely restored, the economy had swung against Cashbuild. It really was a perfect storm.

For the second quarter of this financial year, revenue was down 5%. Like-for-like revenue fell 6% and new stores added 1%. Over the six-month period, revenue is down 4%. Despite this, the share price only closed 0.6% lower on the day, though I must point out that this was on a very good day for the JSE, so the effectively performance gap is higher than this would otherwise suggest.

Inflation seems to have moderated, with selling price inflation of just 4.5% for the quarter.

Much as I want to look for silver linings here, the reality is that growth deteriorated in Cashbuild South Africa, which contributes 81% of group revenue. It was down 3% in Q1 and then 5% in Q2. The P&L Hardware business is still under pressure, down 9% in Q2. That’s at least better than the 11% drop in Q1.

Cashbuild relies on home improvement and investment in construction. Load shedding does terrible things to consumer confidence, so I’m not sure that the revenue bleeding will stop just yet.

Renergen: more than just hot air

Finally, there is liquid helium

Nervous have been settled by the latest announcement from Renergen, with the exciting news that the helium module at the Virginia Gas Project is finally in operation. This means that South Africa is one of eight countries worldwide that produce helium.

A one-year share price chart shows how confidence started to dip towards the end of 2022 based on some difficult SENS announcements and then a fairly long period of silence from the company. A 9% rally on Monday helped claw back some of those losses!

South32 quarterly update

Overall, the production news is positive

Mining updates tend to be highly detailed and quite technical. If you’re looking for the finer details of the quarterly update, then I suggest reading the original SENS released by South32.

For the rest of us, all we really need to know is that copper production is up 12% for the first half of the 2023 financial year and aluminium production is up 15%. Australia Manganese achieved record production, posting an increase of 7%.

Importantly, operating unit costs for the first half of the year are expected to be in-line with or below guidance at the majority of group operations. This is a positive story overall.

The Foschini Group makes Mr Price look even worse

Load shedding or not, TFG is flying

If you’ve been reading your Ghost Bites this week, you’ll know that Mr Price released a horrible set of numbers that really calls into question whether the core business is resonating with consumers. My view is that Mr Price has been too focused on acquisitions, with the neglect of the core business now showing.

The latest update from The Foschini Group (TFG) confirms that view, with solid numbers despite facing all the same load shedding challenges that Mr Price had to deal with.

The key number is like-for-like growth in TFG Africa, which came in at 5.7% for the quarter. Even more impressively, like-for-like Homeware sales were up 3.4% for the quarter. Clothing was up 6.7%. With 70% of TFG’s local turnover supported by backup power solutions and a plan to take this to 100% over the next few months, TFG is spending less time apportioning blame and more time surviving the challenges.

The acquisition of Tapestry Home Brands skews the overall growth number in TFG Africa, which came in at 18.4%. Still, with nuggets in the announcement like record Black Friday and Cyber Monday sales, there was plenty for shareholders to smile about in this update. Online sales grew 43.3% and now contribute 3.9% of total TFG Africa retail turnover.

There are some issues for investors to worry about, like a 100bps drop in TFG Africa’s gross margin vs. the prior period. In the UK, TFG London could only manage a 2% increase in sales, though a less promotional environment (steady sales vs. a Black Friday focus) was supportive of margin. Online sales in the UK fell by 11.5%, now contributing 42% of total sales.

In Australia, turnover increased by 20.9%. Online fell 16.2%, now contributing 5.8% of total turnover in Australia.

Over nine months, group turnover is up 20.8%. We know that the Tapestry Home Brands acquisition is flattering this number, but there’s more than enough going on in the rest of the business to give this result a positive report card.

Speaking of acquisitions, TFG will acquire independent footwear retailer Street Fever. 114 Street Fever stores will be acquired and approximately 90 will be rebranded to Sneaker Factory. Others will be rebranded under other TFG brands as appropriate.

The trust related to the management team of Ninety One has bought shares worth around £246k

There were some mistakes in the Alviva circular related to the take-private offer being made by the consortium of investors. Certain shareholders are not eligible to vote on the deal due to conflicts of interest. The correct percentage of shareholders who cannot vote is 30.2%.

By 16th February, holders of at least 31.3% of Afrocentric shares need to have accepted the partial offer by Sanlam in order for the deal to stand any chance of going ahead. If the acceptance rate is lower than that percentage, Sanlam cannot elect to waive the minimum shares requirement.

Buffalo Coal Corp has received approval from the SARB for a loan from Ikwezi Mining, an affiliate of Belvedere Resources. The facility is for $30 million and it may be drawn in up to ten trances with interest accruing at a base lending rate prescribed by the SARB (currently 7.5%). Each facility is repayable within three years after drawdown.

Choppies Enterprises released a cautionary announcement regarding a potential acquisition of a fast moving consumer goods company in Botswana. There are no further details at this stage, as negotiations are underway.

In Trustco’s ongoing fights with the JSE, the latest issue is that Trustco is non-compliant due to missing a financial reporting deadline. The company anticipates releasing the reports by 31 January.

The Eskom Pension and Provident Fund has increased its stake in Hyprop. It’s nice to see the employees exposed to companies that Eskom is causing so much trouble for, like property funds.

This is one of the few property companies I hold in my portfolio

Attacq is a solid company in my view, despite the unnecessary renaming of types of properties. Shopping centres are “retail-experience hubs” and good ol’ offices are “collaboration hubs” – each to their own, I guess.

I’m invested in the numbers, not the names. Although load shedding is definitely a concern in this space as running backup power isn’t cheap, the good news is that turnover and footcount over the festive season both showed strong growth vs. the prior year.

Mall of Africa reported particularly great results, with turnover in November and December up 17.6% and 19.1% respectively. Footcount is also higher, up 10.8% and 15.5% for those two months. Those looking for clues about performance in different retail categories over the festive trading period will enjoy this paragraph from the Attacq announcement:

Vacancies at Lynnwood Bridge “collaboration hug” are down to 2.6% and there seems to be progress with leasing vacant space at Waterfall City. There does seem to be a general return to office environments, which is definitely good news for the property industry overall. The problems are still there in lower grade office properties or in areas that are hopelessly oversupplied, like Sandton.

Looking at the balance sheet, Attacq has successfully refinanced R1 billion of term loan facilities, taking the weighted average cost of debt on the facilities down by 64 basis points. The weighted average term to maturity on the refinanced facilities has increased from 1.5 years to 3.2 years.

It all looks pretty good to me, though I remain nervous about the impact of load shedding on profitability. The share price is up 22% over six months but has been range-trading since early December.

Fortress loses REIT status

It’s debatable whether this will be a positive or negative outcome

For the first time on the JSE, a listed property company has officially lost REIT status. After several attempts to restructure the dual-share classes failed, there was no way for Fortress to meet the distribution requirements to retain REIT status.

So, what does this mean?

From 1st February, Fortress will lose REIT status. It will remain a listed property company with two classes of shares. The rights attached to the shares wont change. The only difference is that the tax burden now sits with the company, not with its shareholders.

This is bad news for exempt investors, like pension funds. By now, they should’ve gotten off the share register anyway. If they didn’t, then you can expect to see some painful selling. There will also be asset managers out there who are only allowed to hold REITs, so the loss of that status is a forced sell.

Keep a close eye on SENS updates. For example, Coronation has sold some shares and now holds 18.92% of the Fortress A shares, which is still a big number. Speculative traders will be watching Fortress closely, hoping to take advantage of a bit of chaos on the register.

Is there a silver lining here? Well, maintaining REIT status puts the company on a cash flow treadmill that forces most profits to be paid out as a distribution. With the loss of that status, Fortress has far more balance sheet flexibility. The question is whether they will take advantage of that.

Karooooo releases third quarter results

With record net subscriber additions, things are finally looking up

Covid caused a lot of disruptions for Cartrack, Karooooo’s major underlying business. The global expansion plan was hit by travel restrictions, especially in Asia. The excuses eventually wore thin and the share price fell as low as R320 in mid-2022. A significant recovery to R412 has been staged since then, with the stock incredibly range-bound between R400 and R450.

Lack of liquidity is part of the problem, with a significant bid-offer spread that makes it hard to take advantage of that range.

With third quarter results now available, investors have fresh information to work through. The key statistic is that net subscriber additions for the quarter were record-breaking, coming in at 78,593. The total subscriber base is now nearly 1.68 million, up 14% year-on-year.

Subscription revenue increased 16% as reported and 15% on a constant currency basis. Total revenue was up 29% as reported and 28% on a constant currency basis, so you can see the impact of Carzuka and Picup (with the latter renamed Karooooo Logistics) on the growth numbers, as they aren’t subscription businesses.

Karooooo Logistics is at least profitable, with adjusted EBITDA of R2.6 million. That’s not a typo – it’s a very small business.

Carzuka is still incinerating cash, with adjusted EBITDA of -R14.6 million. Losses in startups are nothing new. I’m just not convinced of a strategy of mixing a low margin dealership business with a high margin subscription business.

Speaking of cash, Karooooo generated record free cash flow for the nine months ended November of R434 million, up from R306 million the year prior.

Has Mr Price lost its relevance with customers?

Fashion is intensely difficult and competition has heated up in this market

I’m not sure if you’ve Cotton On yet, but there are a lot of very good clothing retailers in our market. The international players entered our market with a vengeance, forcing Woolworths to focus and almost putting Edcon out of its misery entirely. Mr Price faces an onslaught in this space. If I look at the positioning of the likes of The Foschini Group vs. Mr Price, I struggle to see how Mr Price is staying relevant with customers.

The share price is down well over 20% in the past year and has lost 36% in the past five years. This excludes dividends, of course.

Mr Price seems to be focused on acquisitions rather than its core business, having gone on a buying spree that included Yuppiechef, Power Fashion and most recently Studio 88. Based on my glances through the shop windows, Studio 88 seems to give Mr Price a fighting chance in a market that TFG is currently dominating.

Despite the trading update for the 13 weeks to 31 December 2022 proudly declaring this a record quarter for Mr Price in terms of sales growth, the market thankfully isn’t that stupid. The share price fell more than 7%, which makes sense if you bother to read past the first paragraph.

After such large acquisitions, of course it’s a record quarter. If you include the revenue you acquired, it’s not hard to look much bigger than you used to be. Sadly, if you exclude Studio 88, the growth rate is a paltry 1.2%. With selling price inflation of 6.2%, this means that volumes plummeted.

Here’s a metric that makes it look even worse: cash sales grew by just 0.6%.

We don’t have numbers yet for net profit, but you can rest assured that they will be poor. Gross margin was lower and load shedding drove significant backup power costs at store level. The stores are seeing the action, with online sales down 6.1% if you exclude Studio 88.

Instead of focusing on what is broken, the group just keeps expanding. Excluding Studio 88, weighted average trading space increased by 5.4%.

Are there any silver linings here? Well, Power Fashion and Yuppiechef both achieved double digit sales growth. This suggests that Mr Price is doing a decent job on acquisitions and a poor job in the core business.

Maybe the retailer should take a leaf out of Woolworths’ book and focus on fixing the value proposition instead of rolling out lots of new stores?

Director dealings:

The CEO of Spear REIT has bought shares worth R15.3k

An associate of a director of Huge Group has bought shares worth R15k

Reinet always reports the net asset value (NAV) of the underlying fund and then reports the NAV of the listed company that is invested in the fund. Though the percentage movements aren’t usually identical, the fund movement is a strong clue as to the movement in the company. From September to December 2022, the NAV increased by 6.5%, so that was a strong quarter.

The time to reflect on a forgettable year in global markets is fast running out – in fact, some might say it has passed already. We want to take the last opportunity available to look back and ask: “What worked, what didn’t, and what have we learned?”

Looking back

It should come as no surprise that few global indexes were spared pain in 2022, with sharp corrections and heightened volatility being the norm. The VIX Volatility index, frequently referred to as the global “fear gauge” (essentially aggregating insurance premiums for equity market corrections, known as implied volatility), had a median value only eclipsed in 2009 and the Covid-pandemic-hit 2020 over the past few decades, while the US Dollar strength index (DXY) reached its highest level in September – buoyed by both fear and FOMO (fear of missing out), as capital flowed into the world’s reserve currency on the back of geopolitical tensions and a US Federal Reserve (Fed) raising yields aggressively.

In a year where geopolitical tensions spilled over into armed conflict directly challenging Western democratic ideals and causing severe energy market disruptions, and with environmental and pandemic issues intensely debated among world leaders, it seems odd to say that the tail that firmly wagged the dog last year was inflation.

Many would argue that it should never have been a surprise following more than a decade of historically accommodative monetary policies, but the sheer scale of price rises and coordinated central bank reactions shook markets. The preeminent global tech play, the Nasdaq-100 index, receded by 32.4%, the S&P 500 was down 18.1%, the Nikkei was down 18.5%, the Australian (-7.32%), French (12.2%), Korean (-28.6%) and Taiwanese (-26.9%) market indexes all closed down sharply; and the MSCI Emerging Markets (-20%), China (-21.8%), Growth (-29.1%) and Momentum (-17.4%) indexes all fell precipitously (returns calculated in US dollars, assuming gross dividends reinvested).

Even traditional safe-haven assets were not spared, with the Global Aggregate Bond index down 16%, and gold being flat for the year (-0.2%) and, somewhat surprisingly, even losing its shine since Russia invaded Ukraine (down 11% since its March peak).

Why the pain?

But why would unexpectedly high inflation levels be a catalyst for such a severe coordinated asset market sell-off?

This may seem counter-intuitive considering that higher inflation should, all things equal, raise the nominal value of the companies selling those same goods and services. But such a simple heuristic ignores the key temporal element for how assets are priced: current valuations discount future earnings and cash flow. This means that higher inflation expectations and commensurate interest rate hikes in the future, imply that tomorrow’s earnings are valued lower in today’s terms (being discounted at a steeper rate).

But just how steeply did discount rates rise?

Consider the fact that as we entered 2022, the federal funds rate in the US, a key anchor for developed market interest rates, was a mere 0.25%. By the end of the year, it had reached 4.5%. This prompted most other central banks, the South African Reserve Bank included, to follow suit and aggressively raise rates to slow consumer spending and inflation.

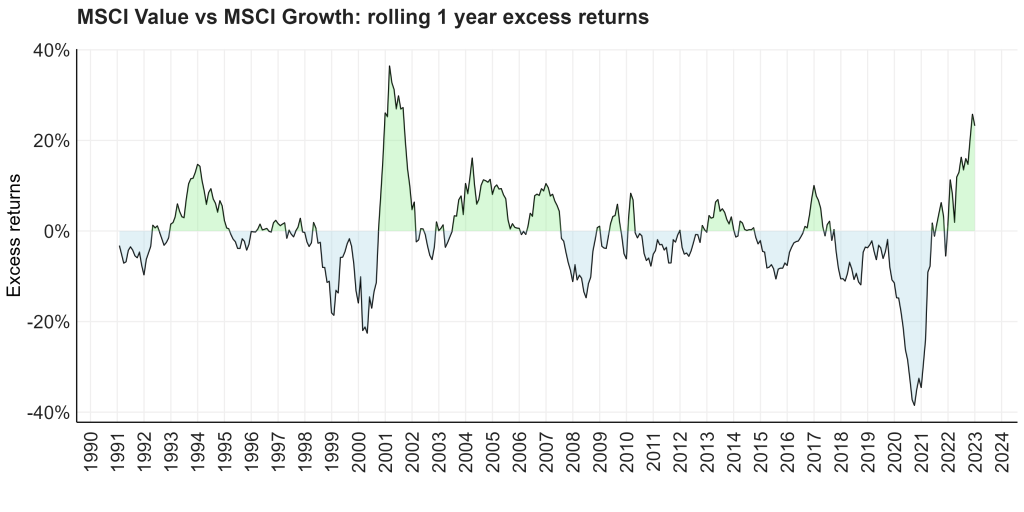

To understand which market indexes were most affected and why, consider the classic dichotomy of Growth vs Value shares. Growth companies or industries tend to have loftier valuations because of higher future earnings potential. This follows for the same reason some pay eyewatering premiums for houses in a sought-after estate ‒ hoping a high price today might look cheap tomorrow. Value companies tend to have more muted (some might even say grounded) earnings expectations, and are often associated with larger, more established and slower-growth blue-chip companies. An investment in Coca-Cola won’t double in value in a year; Apple or Amazon just might.

Understanding this distinction helps understand why pain occurred so acutely in equity markets in 2022. The MSCI All Country World index (ACWI) (comprising of nearly 3 000 global companies) is an often-used proxy for global equity market performance. The index composition has, over time, begun reflecting a decade-long preference for growth companies that coincided with low global rates and low inflation (technology and IT consumer services companies still dominate the index despite significant losses in 2022, comprising more than a quarter of the index today). Low interest rates since 2010 simply meant lower future earnings discount rates, meaning companies with higher growth potential were valued more favourably; low inflation meant less urgency to materialise these expectations. Even the traditionally industrial-heavy S&P 500 index has effectively become a tech-heavy growth proxy today. In truth, why back the tortoise (Coca-Cola) when you can bet on the hare (the next Apple or Amazon)?

This all came undone spectacularly in the perfect storm that was 2022. As global inflation spiked, the Fed kicked off a historically aggressive cycle of coordinated global tightening causing future discount rates to soar. Higher expected future inflation created a renewed sense of urgency to deliver on lofty earnings promises; heavily indebted growth companies, hoping to leverage their potential in a low-rate environment, faced real solvency risks; and higher discount rates made previously attractive valuations seem excessive. All in the space of a year.

By contrast, Value strategies and industries performed strongly. As at the end of 2022, the MSCI Value to MSCI Growth index spread reached its highest level since the dotcom crash in the early 2000s, following a decade of underperforming Value strategies.

Source: MSCI. Calculation Satrix

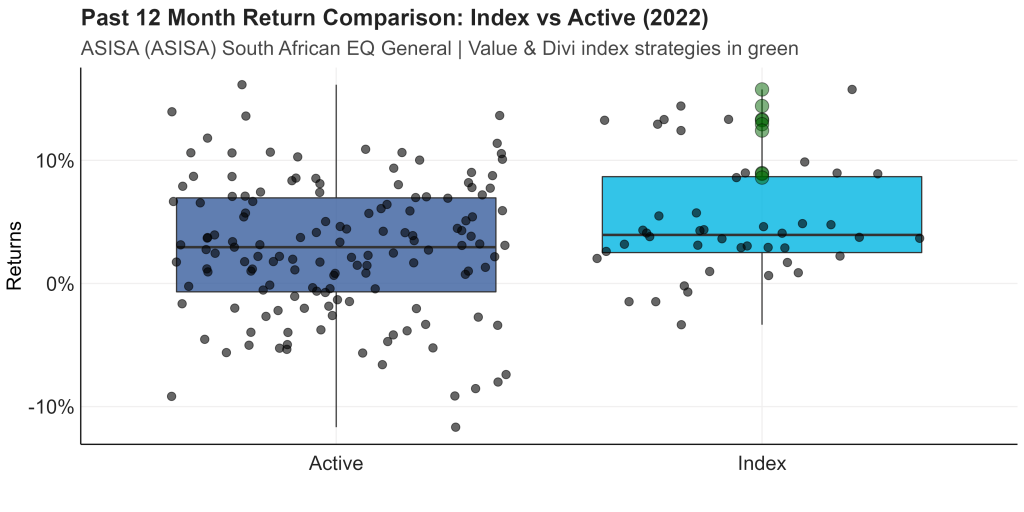

Locally, we’ve seen the same. Value managers broadly outperformed their active peers, while in the rules-based indexation segment we saw Value-oriented ETF and index funds comfortably outshine other retail strategies (highlighted in green)

Source: Morningstar. Calculation Satrix. Box plot indicates the top and bottom quartile of performers, with the black middle inner line the median performance.

What have we learned?

Investors should take at least two important lessons from 2022.

First, the importance of healthy diversification across both asset classes and investment styles. While the MSCI ACWI holds 3 000 companies, it is less diversified than you might think. It has become surprisingly susceptible to changing investor risk appetite, which caused a coordinated sell-off in growth strategies. The same applies to other large, trusted global indexes like the S&P 500, Nikkei and FTSE 100, which have become Growth-oriented strategies. Investors would be wise to consider adding more diversified sources of return to their portfolios, not simply more sources.

Second, 2022 was particularly challenging for local balanced fund managers. Regulatory changes allowed multi-managers to increase their funds’ offshore exposure (Regulation 28 changes allowed up to 45% offshore exposure). In response, many chose to down-weight local equity market exposure (with the FTSE/JSE All Share index closing down a mere 2.8% in US dollars) to move assets offshore. Managers who made use of rand hedges would have also been doubly hurt, as the weaker rand (down just over 6% to the dollar) would have offset some of the offshore losses. This isn’t a one-off though. Our research shows that over the last 20 years a fully hedged 60/40 equity and bond portfolio (with 70% local and 30% offshore exposure) underperformed the unhedged alternative 72% of the time on a rolling one-year basis, while having a higher realised volatility 61.4% of the time (which is somewhat surprising given the rand’s volatility). The lesson learnt is that increasing offshore exposure at all cost is not necessarily wise, while hedging currency exposure does not necessarily increase portfolio efficiency.

What happens next?

A tantalising question looking ahead is whether Value will continue to dominate Growth strategies in 2023 ‒ momentum is arguably less interesting, as it can be considered somewhat of a chameleon style; strong performance in Value means you now hold more Value counters today. Even if one does not follow a strict style approach to investing, the distinction remains key for understanding which indexes will likely perform.

Analysts broadly agree that the Fed was overzealous in their tightening efforts in 2022, much the same way that they were overly accommodating in 2020. With historically high corporate and sovereign debt levels and inflation forecasts having begun receding towards the end of 2022, it will be increasingly unpalatable for the Fed to remain as intent on tightening this year. This might be good news for current bond holders, as instruments purchased at higher yields will increase in value should prevailing rates decline towards year’s end.

For equity markets, the key question is whether investors will again be drawn to Growth sectors should yields decline and risk assets become more attractive. Certainly, lower yields and lower inflation would begin to nudge this behaviour, although likely not as much as before given the Fed having showed a strong willingness to act should inflation resurface. In fact, for a strong Growth rebound to happen this year with similar fervour as in the distant pre-Covid past, the stars would have to align on several fronts, not least of which include a soft landing (markedly lower global inflation outlook without significant GDP contraction), and an accommodating Fed (who might be less eager to bring back the punch bowl prematurely as they did in 2020).

Lest we forget, stranger things have happened in the recent past, although one might be tempted to conclude that Value-oriented sectors and industries might be more likely to continue performing strongly in the year to come. This should bode well for our local equity indexes, as well as emerging market indexes like India and China.

While these points will remain debatable over the coming year, what is certain and timeless is the importance of ensuring one’s portfolio is properly diversified across different sources of return and risk. Investors will be well advised to enquire as to the appropriate index or multi-asset solutions that provide said diversification, and not simply hope that the number of instruments in a portfolio ensures real diversification is achieved.

Satrix consists of the following authorised FSPs: Satrix, a division of Sanlam Investment Management (Pty) Ltd, Satrix Managers (RF) (Pty) Ltd and Satrix Investments (Pty) Ltd in terms of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Nampak’s efforts to avoid a painful rights offer.

Steinhoff offloading a portion of its stake in Pepco.

Richemont’s recent share price momentum and the look-through to China.

BHP looking to China as a stabilising force for commodities in 2023.

Woolworths reporting solid growth over the festive trading period, with the strategy clearly working.

Mr Price reporting the opposite to Woolworths, with weak trading that knocked the share price 7% lower.

Spar trying to clean up its governance reputation with shareholders.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

The following are those deals shortlisted for the Private Equity Deal of the Year 2022. The DealMakers Independent Panel have selected these transactions from the nominations submitted by the M&A industry advisers. They are, in no particular order:

Exit by Rockwood Private Equity of EnviroServ to SUEZ SA, Royal Bafokeng Holdings and African Infrastructure Investment Managers

The waste treatment and disposal company with facilities across South Africa, Mozambique and Uganda was acquired in October by a consortium comprising SUEZ SA (51%), Royal Bafokeng Holdings (24.5%) and African Infrastructure Investment Managers (24.5%) in an exit led by Rockwood Private Equity. The transaction, one of the largest SA private equity exits in 2022, provides a strategic platform for its new shareholders and enables French utility Suez, to strengthen its position on the African continent while providing expertise and knowledge to the local waste management landscape.

Advisers to the deal were: Standard Bank, Rand Merchant Bank, Quercus Corporate Finance, Bowmans and Roodt.

Exit by Actis and Mainstream Renewable Power Africa of Lekela Power

The US$1,5 billion deal announced in July 2022 with the acquisition of Lekela Power’s assets in South Africa, Egypt and Senegal by Infinity Group and Africa Finance Corporation, represents Africa’s biggest Renewable Energy M&A deal with a combined installed generation capacity of 1.0GW and including a 1.8GW pipeline of greenfield projects. The platform was established in 2015 as part of a joint venture between Actis (60%) and Mainstream (40%). The planned exit reflects the successful culmination of the partnership which has seen Lekela become the continent’s largest pure-play renewable Independent Power Producer.

Advisers to the deal were: Citigroup Global Markets, Absa CIB, Cantor Fitzgerald, Webber Wentzel, Clifford Chance and Norton Rose Fulbright.

Exit by RMB Ventures Six and management of Studio 88 to Mr Price

The exit by RMB Ventures and current management of a 70% stake in Studio 88 for a total transaction value of R3,3 billion, marks for RMB Ventures, the end of a 9-year journey with the company. One which has seen exceptional growth, most of which has been organic growth funded by internally generated cashflows. For Mr Price, the acquisition represents an opportunity to expand into the aspirational value segment of the market.

Advisers to the deal were: Rand Merchant Bank, Investec Bank, Bowmans, Deloitte and Renmere Advisory.

The winner will be announced at the ANSARADA DealMakers Annual Awards on 21 February, 2023 at the Sandton Convention Centre.

DealMakers is South Africa’s M&A quarterly publication

If detailed reporting makes you happy, this quarterly update is for you

BHP’s quarterly reports are enough to get the heart racing of any Excel enthusiast, with literally pages upon pages of detailed production disclosures.

For the rest of us who just want a vague idea of what’s going on, the key point is that production guidance for the 2023 financial year remains unchanged. There are some good bits (like record production at Western Australia Iron Ore) and some disappointing bits (Escondida copper in Chile and BHP Mitsubishi Alliance both trending to the low end of their ranges).

In some operations, unit cost guidance has been increased due to wet weather and inflationary pressures. Remember, high rainfall isn’t good news for miners, with coal mining in Queensland having been affected by this.

Here’s perhaps the most important comment of all, which I’ve decided to include in full:

Kore Potash quarterly review

If you ever fancied working in the Republic of Congo, perhaps read this first

Other than arguments with the Minister of Mines in the Republic of Congo (which included the arrest without charge of two senior employees of the company in that country), Kore Potash’s focus has been on securing the financing required for the Kola Potash Project in that country.

The SEPCO Electric Power Construction Corporation is negotiating contractual terms with Kore Potash for the Engineering, Procurement and Construction (EPC) proposal. Once this is in place, a financial proposal is expected from the Summit Consortium.

The company has $5 million in cash after investing nearly $1.1 million in exploration this quarter.

There’s never a dull moment when doing business in Africa, especially in the mining industry and especially in a country like the Republic of Congo.

Spar tries to take some of the heat off the share price

The market liked it, with a 3.9% rally

If you’ve been following the Spar updates, you’ll know that the management team is leaving amid allegations of poor corporate governance and even fictitious and fraudulent loans.

Spar has moved to reassure the market, with three important points raised:

Allegations of discrimination against retailers were investigated by a law firm (one that I’ve never heard of) and the allegations were unfounded. Spar is in a mediation process with the retailers that lodged claims.

In an example of a professional services firm that I have heard of, PricewaterhouseCoopers notified Spar of a loan that is a reportable irregularity. Upon further investigations, it was found to be a an “isolated matter” that occurred five years ago with a total value of R11 million.

Among the significant changes to the board, the retirement of Brett Botten as CEO is “pursuant to his request to the board for an early retirement”.

Look, I would also retire early instead of dealing with this kind of pain. The announcement of a new Group CEO will be made in due course.

Is this enough to give investors confidence in the company once more? I suspect that many will wait to find out who the new CEO is before taking a longer term position.

Woolworths is continuing to deliver its turnaround

But watch out for load shedding costs and pressure on gross margin

It’s been a huge year for Woolworths, with share price growth of 27.5%. For longer term holders, the picture looks less like fancy Belgian yoghurt and more like old polony, with total growth of around 4% over five years.

Markets are all about timing. Don’t let anyone tell you otherwise.

The reason that Woolworths has done well in the past year is that the management team is doing the right things. They are reducing trading space, taking Woolworths back to its roots and reducing exposure to Australia, a country where we shouldn’t play cricket or try and own retail businesses. Country Road seems to be an exception. David Jones certainly wasn’t.

For the 26 weeks ended 25 December 2022, group turnover is up by a whopping 16.3% in constant currency terms and 18.5% as reported. There were substantial lockdowns in the base period in Australia, so this isn’t a fair indication of group performance.

A better comparison is to use the last 6 weeks of the period, in which sales increased by 8.8%. Woolworths sounds happy with Black Friday and festive season trade.

As we are seeing in many retailers, consumers have returned to bricks-and-mortar stores and online shopping has slowed down. Without a doubt, some of the changed behaviour will stick and most retailers have reported online sales that are still way ahead of pre-pandemic levels. Woolworths has highlighted the return to stores in Australia in particular, though the base effect of hectic lockdowns would be highly relevant here.

Online sales at group level now contribute 10.9% of total turnover vs. 13.7% in the prior period.

Looking deeper, Fashion Beauty Home sales in South Africa were up 11.2% and accelerated to 12% in the final six weeks. Price movement was 10.8%, so inflation helps here alongside some volume growth. Space was reduced by 2.2%, so trading density (sales per square metre) has definitely improved. Online sales in this segment grew 4.5% and contribute 4.2% of South African sales.

Food is where much of the pressure has been thanks to competitors taking a bite out of Woolworths’ customer base, especially as they trade down in search of value. This has forced Woolworths to become more competitive on price, evidenced by price movement of 6.8% vs. food inflation of 8.4%. Sales were up 5.4% on a comparable store basis, which suggests a drop in volumes. As trading space is increasing, total growth was higher at 7.6%. Online sales grew by 22.7%, now contributing 3.6% of local sales as Woolworths Dash gets some traction in the market.

The Woolworths Financial Services book is 17.2% larger, suggesting that Woolworths has been more willing to give credit. With an annualised impairment rate of 5.5% vs. 4.0% in the prior period, that willingness does come at a cost.

In Australia, Country Road Group is the business that Woolworths is holding on to and sales grew by 25.5%. Again, the base effect skews this. In the last six weeks of the period, growth was 8.5% despite trading space decreasing by 5.5%. Online sales contributed 26.1% to total sales vs. 33.8% in the comparable period.

Woolworths has agreed to sell its stake in David Jones and that deal should be completed by the end of March. With sales performance in those six weeks of just 2.3%, shareholders won’t be sad to see this one go.

The expected increase in HEPS for the 26 weeks ended 25 December 2022 is between 70% and 80%, coming in at between 285.9 cents and 302.8 cents.

The market celebrated these numbers with a jump in the share price of nearly 4.8%.

Little Bites:

Director dealings:

An associate of a director of Afrimat has sold shares in the company worth R3.85 million.

On the 1st of February, history will be made on the JSE when Fortress REIT Limited will no longer be a REIT. The name change is coming. The biggest question is what other changes are coming, particularly to the shareholder register? Personally, I’m not sure that losing REIT status is the end of the world here, but time will tell.

Shareholders have voted in favour of Aveng’s proposed sale of Trident Steel, which isn’t a surprise based on the pricing achieved.

Trematon owns 50% in a property in Woodstock that is being sold to a coffee shop for R16.25 million. As tiny as this deal is, it’s a small related party transaction and that means an independent expert needs to be appointed to opine on the fairness of the deal.

Hopefully they can afford to fix the sign outside the Claremont office now

While walking back from the cricket at Newlands over the weekend, I couldn’t help but laugh at the Coronation sign that appeared to be suffering from partial load shedding. With “oro” out of service, it shone “Conation” brightly to thousands of people leaving the cricket. Cue the bear market jokes.

The irritating disclosure by the company continues, with updates on assets under management still not giving any comparatives. This means I have to go digging through the SENS archives.

Here’s the recent trend:

31 Dec 2022: R602bn

30 Sep 2022: R574bn

30 Jun 2022: R580bn

31 Mar 2022: R625bn

31 Dec 2021: R662bn

With AUM still a lot lower than it was a year ago (not least of all because of broader market prices), perhaps the sign will have to be patient to be fixed?

The booze cruise

We have an update on how much money Capevin and Gordon’s Gin makes for Distell

Due to the length of time it is taking to implement Distell’s transaction with Heineken International, the company was required under law to issue a revised prospectus. This is only exciting if you were one of the lawyers earning a fee to draft the thing.

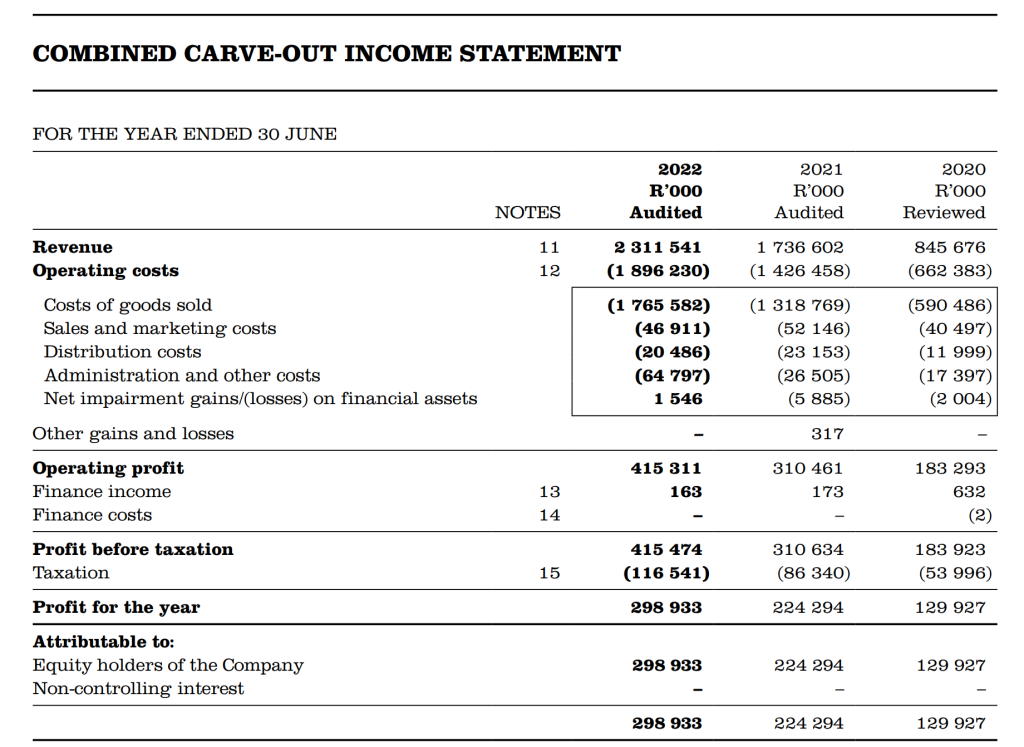

The far more interesting document is the carved out historical financial information of Capevin and Gordon’s Gin, which the company has issued to give shareholders an updated view on the business.

I’ve included a screenshot of the income statement below. I think the movement between 2020 and 2022 is truly breathtaking. With a year-end of June, this is presumably because of Covid restrictions on alcohol.

Perhaps the most interesting thing is that profit before tax margin decreased from 21.7% in 2020 to below 18% in the subsequent years. I am very surprised that a much smaller version of the operation is more efficient!

Nampak: meeting adjourned

Shareholders gave this proposed adjournment unanimous support

As reported in Ghost Bites earlier in the week, Nampak is in discussions with “a number of stakeholders” regarding the way forward. We don’t know yet who the parties are, but we can speculate.

To give those discussions more time to come to fruition, the company proposed an adjournment of the meeting that would’ve seen shareholders vote on the resolutions for a proposed rights offer. The fact that 100% of shareholders in attendance at the meeting gave approval for the adjournment tells us that the rights offer is a truly horrible outcome that everyone would prefer to avoid.

The meeting has been adjourned until 8th March, so Nampak has a few weeks to try and work and miracle.

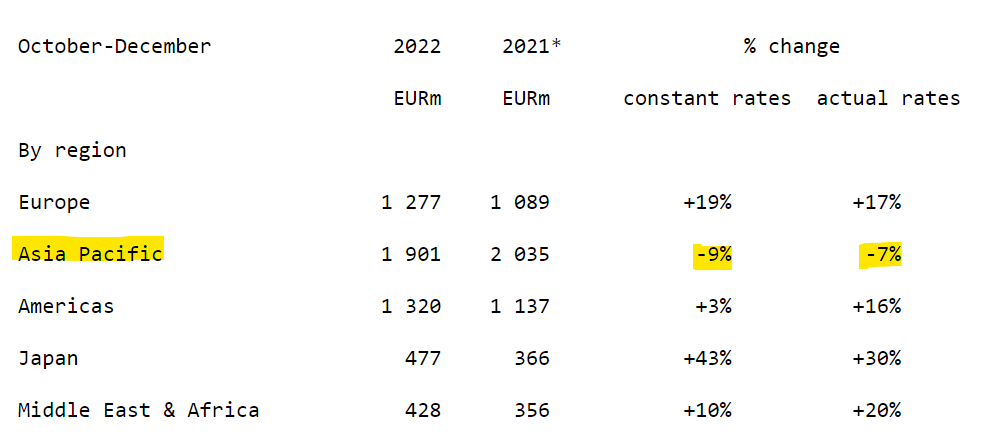

Richemont needs the reopening of China to stick

The company’s most important region has been going backwards

Richemont has reported sales growth of 8% for the quarter ended December 2022 and 18% for the nine months ended December. It would’ve been so much better had the Chinese economy been open for business.

Even in ultra luxury goods, it makes a big difference when an economy is locked down. The proof is very clearly in the numbers:

I also found it interesting to note the performance of the underlying product categories. The Jewellery Maisons (yes, this is the official term used by Richemont, dripping with caviar and 1st world problems) grew by 8% in constant currency and the Specialist Watchmakers (surely a missed opportunity to call them Timepiece Maisons?) fell by 5%.

Messy online business YOOX NET-A-PORTER (this name definitely doesn’t work alongside “Maisons”) posted a 6% drop in sales. It is now presented as a discontinued operation as Richemont is selling a controlling stake.

Steinhoff offloads some of its Pepco stake

Don’t get excited – plebs like us couldn’t get any

With Pepco (Steinhoff’s European discount retail business) having released solid results recently, Steinhoff took advantage by selling off some of its stake to institutional investors. Unless you’re in the little black book of banks like Goldman Sachs or J.P. Morgan, it’s unlikely that you were called about these shares.

This is a “private placement” which means VIP section only. The goal is for the bankers to make a few phone calls, place large blocks of shares and take a juicy fee along the way.

Pricing was finalised through the process and it happened very quickly, with the results of the offer announced just one hour after the initial announcement. I can almost guarantee that calls had already been made overnight. Steinhoff offloaded a 6.6% stake in Pepco and raised EUR315 million in the process. This reduces Steinhoff’s stake in the company to 72.3%.

Steinhoff must have liked the pricing that came through, as the original plan was to sell a 6% stake. An upsized offer means that investors were putting proper numbers down on the table. The banks definitely did their jobs here.

To be clear, the cash will flow from the investors into Steinhoff, not into Pepco. Steinhoff will use that money to help reduce debt. This is distinct from the previously announced plan to restructure the debt and leave shareholders with very little.

Little Bites:

Director dealings:

The Group Risk Officer of Investec sold shares worth R10.8 million and a person who I would guess is his wife sold shares worth R8.6 million.

There are significant changes to the board at Novus, including the (expected) retirement of the CEO. Further announcements of replacements will be made in due course.

The final payment to shareholders by Etion will take place on 6th February and the delisting will be effective from the morning of 7th February.

EOHsays there is “significant interest” in its rights offer– but it is fully underwritten anyway!

A rights offer of R500 million by EOH isn’t fresh news. In fact, shareholders approved it back in December, with the circular due to be released on 23 January.

This was inevitable. I’ve been writing about it since I walked away from this punt at over R7 per share. EOH closed at R3.32 on Tuesday, so I’m very glad I did. It took too long to sell the underlying businesses, the prices weren’t high enough and the interest burden in the background was simply too large.

The good news is that EOH has managed to achieve a fully underwritten rights offer through a combination of boutique asset managers and investors. This doesn’t come for free, with underwriting fees of either 1.5% or 2% due to the underwriters (depending on which one you look at).

In a pre-close update for the six months ending January, the group paints a bleak picture of operating conditions in South Africa. Still, EOH believes that things will be better this year, with revenue and EBITDA for the five months ended December looking promising.

Debt at the end of July 2022 of R1.3 billion has been reduced to R1.2 billion, but it doesn’t help when interest rates have gone up and the financing cost has remained the same. This is why I felt that a rights offer was inevitable, as there is just way too much debt here. For reference, EOH’s market cap is less than half the current debt level!

Assuming the rights issue goes ahead without any problems, Standard Bank has agreed to refinance the debt in a way that EOH believes will be sustainable.

I guess that time will tell. I struggle to find anything to get excited about with EOH.

Kibo looks to synthetic oil

If they get it right, this is a new revenue stream and potentially a less risky project

Kibo Energy owns 65% of Sustineri Energy, a business that hopes to produce electricity from syngas. I’m no engineer, but “produce electricity” is a statement that I can get behind right now.

There’s an interesting change of plan here, which the company is calling an “optimisation improvement decision” – a term that made full use of the corporate thesaurus.

By focusing on producing synthetic oil instead of electricity in phase 1, Kibo believes that the project can be de-risked and made more attractive to funders. They are currently busy with a comprehensive integration study that will look at financial viability among other factors, so we don’t even know yet if this will work.

Honestly, if this gets us closer to generating electricity from waste, then I’m all for it.

Ninety One’s AUM is flat for the quarter

It’s not easy managing money in a rough market

In the asset management industry, fees are earned based on assets under management (AUM). They take the form of fixed fees and performance fees, which means that asset management firms are highly exposed to broader asset values in the market.

This would be called a “high beta” industry, as the share prices are strongly correlated with the broader market index.

With that bit of finance nerdiness out of the way, I can report that Ninety One’s AUM as at the end of December was £132.4 billion, down approximately 6.5% year-on-year. Importantly, it’s very similar to the number reported at the end of September, so AUM was flat over the quarter.

There are only two drivers of AUM: (1) asset values in the underlying portfolio and (2) net client flows. The Ninety One quarterly update doesn’t give an indication of the drivers of the AUM movement over the period, but it’s worth keeping this in mind.

Property values don’t always go up during inflation

It’s all about the market yields vs. rental levels

Property is often put forward as a great inflation hedge. The theory is that rentals should increase, thereby protecting investors.

Here’s what they don’t tell you: property values often go down during periods of inflation, as the yield demanded by investors also goes up. Value has an inverse relationship with yield, so a higher yield = a lower value on the property.

If the net operating income increases by enough to offset this issue, then it is true that investors will receive a higher dividend and will see the value of capital protected, as the rental growth can offset the yield pressure.

If net operating income doesn’t increase sufficiently, because of say economic challenges during inflation that make it hard to demand endlessly higher rentals, then the inflation hedge thesis takes a knock.

Schroder European Real Estate Investment Trust is a perfect example, with the property portfolio valuation as at 31 December taking a knock over the quarter of 3.3%. The company attributes this to “25 basis points of outward yield movement,” which in English means that yields are higher (now at 6.6% on the portfolio) and hence values are down.

100% of the portfolio leases are subject to indexation, which (once again) in English means that rentals will increase with inflation. The company believes that this will mitigate further value declines.

The latest loan-to-value for Schroder is 32% based on gross asset value and 22% net of cash.

Wholesale changes at Spar

After a disastrous few months, the management team is out

The governance at Spar has a smell that would embarrass the fish section after Stage 6 load shedding on a boiling hot summer’s day. Change is finally upon us, with big news at board level.

Graham O’Conner is retiring at the AGM and will not make himself available for re-election. That’s the right choice, as I somehow doubt that the vote would’ve gone in his favour based on current investor sentiment.

CEO Brett Botten is also on his way out after less than two years in the job.

There are also changes in independent directors, including the appointment of Pedro da Silva. If that name sounds familiar, it’s because he ran Pick n Pay South Africa for a short time. Dr Shirley Zinn has also joined the board, bringing loads of experience from other listed boards. Dr Phumla Mnganga is stepping down as an independent director after 17 years.

Little Bites:

Director dealings:

An entity related to Adv JD Wiese (Christo Wiese’s son) has acquired preference shares in Invicta to the value of R2.98 million

Delta Property Fund just can’t catch a break. After announcing the sale of a property in Kimberly in December for R22.1 million, the deal has fallen through as the purchaser couldn’t put the money together. Back to the drawing board they go.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")