Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.

In the 62nd edition of Unlock the Stock, Redefine Properties joined us to talk about the recent numbers and the strategic outlook for the business. As usual, I co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

In our prior examinations of the South African fixed income universe, we detailed the structure and participant dynamics of the listed debt market. We established that this market is characterised by persistent illiquidity, driven by the dominance of institutional investors, such as life insurers and asset managers, who often adhere to conservative, “buy-to-hold” strategies. This environment, while offering predictable income streams and stable portfolio performance for some, restricts the ability of market participants to rapidly reallocate assets or respond effectively to evolving market conditions. The scarcity of buyers and sellers of the same instrument at the same time perpetuates this cycle.

However, the discourse on corporate debt must now pivot to address a far larger, yet less visible, segment of the market: Private Credit.

The global financial ecosystem is undergoing a profound transformation, marked by a significant migration of corporate debt from public, listed or syndicated markets toward bespoke, privately negotiated solutions. This evolving landscape, often termed private credit or direct lending, has swelled exponentially, with global assets under management (AUM) exceeding $2.5 trillion and projected to reach $3 trillion by 2028. South Africa, with its developed financial sector and large institutional investor base, is emerging as a critical participant in this sophisticated asset class not only for local investors, but on the global stage.

For financial market participants, grasping the drivers and dynamics of this shift, and its specific manifestation in the South African context, is paramount.

The Global Macro Shift: The Retreat from Public Credit

This global retreat from traditional public credit markets can be attributed to a convergence of factors on both the supply and demand sides of the equation. Traditional supply is impacted by regulatory hurdles and associated costs. Simultaneously, investors are now more sophisticated in their processes than ever before, and are less focused on whether an instrument is listed, something that was once a firm requirement.

Following the 2008 Global Financial Crisis (GFC), stringent regulatory requirements fundamentally altered the risk appetite and operational capacity of traditional commercial banks. Facing increased capital adequacy and liquidity constraints, banks began scaling back on lending, particularly to medium-sized or complex clients perceived as “risky”. This regulatory creep has created a substantial funding gap. Non-bank financial institutions (NBFIs) and specialist debt funds have stepped in to fill this gap, operating largely outside the rigorous capital perimeter of banking regulation. For instance, banks now struggle to provide term funding lasting longer than three years at competitive pricing, leaving room for fund managers to adopt a longer-term lending perspective. Basel III regulations, the most recent iteration of the core regulatory framework governing the capital reserves of these banks, is equally reinforcing these constraints.

Concurrently, institutional investors globally, including pension funds and asset managers, have driven immense demand for private credit. They are actively searching for asset classes that offer attractive risk-adjusted returns, diversification benefits, and enhanced yields compared to traditional debt instruments. Historically, private credit has demonstrated the potential to deliver superior returns, compensating investors for the asset class’s inherent illiquidity and perceived risk.

From the borrower’s perspective, private credit offers a superior user experience characterised by speed, flexibility, and confidentiality. Unlike standardised public debt instruments, private debt instruments can be customised with bespoke structures, flexible repayment schedules, and tailored covenant arrangements that align precisely with a borrower’s unique operational and financial requirements. In addition, transactions can often be executed faster, providing funding certainty more quickly than going through traditional bank credit committees or syndicated loan processes.

The True Scope of Private Credit in South Africa

In the South African financial context, the definition of private credit requires a nuanced understanding, extending beyond the common perception of merely funding high-risk, mid-market enterprises or providing smaller, high-yield investment opportunities.

Private credit, fundamentally, encompasses any instrument that is not publicly listed. This broad scope means it covers all forms of debt funding provided by non-bank lenders outside of the listed bond market.

It is important to remember that this asset class includes the debt raised by large, listed companies through private channels. The pool of entities requiring debt funding in the private market vastly surpasses the handful of major corporate issuers (around 25 entities annually, excluding government and SOEs) active in the local listed debt market. Given that there are nearly 300 listed companies in South Africa, most of which require some form of debt funding, the opportunity in the private credit space is significantly broader than in the listed space.

The South African Landscape

South Africa’s private credit market is influenced by the unique dynamics of its capital markets. The listed debt market is infamously characterised by illiquidity due to the dominance of institutional investors who typically hold assets until maturity. The resulting lack of a robust secondary market makes establishing reliable mark-to-market prices problematic.

Furthermore, the attractive yield and high liquidity offered by South African Government Bonds (SAGBs) often make corporate credit comparatively unattractive for conservative asset managers, discouraging diversification away from sovereign risk.

In this context, private credit provides essential capital to areas traditionally underserved, overlooked or deemed too complex by traditional banks. This includes addressing South Africa’s estimated R509 billion SME credit gap, supporting job creation across 19 distinct economic sectors. It also channels funding into development priorities like affordable housing, student accommodation, and infrastructure, offering both financial returns and measurable social impact. Major institutional investors, such as the Public Investment Corporation (PIC), are increasingly turning to private debt for its clear structure and reliable income, favouring it over illiquid equities and complex private equity deals across the continent.

Bridging the Transparency Gap: The Digital Ecosystem

A key structural limitation of global private credit markets, particularly relative to public markets, is their opacity, lack of price discovery, and illiquidity. As we have discussed previously with the Ghost Mail community, over reliance on mark-to-market pricing in illiquid markets can be deeply misleading as a single distressed trade can skew valuations far from a bond’s intrinsic worth (or fair value).

To address these challenges and enhance market efficiency, integrity, and transparency in South Africa’s fixed-income ecosystem, Intengo is employing technology to bridge the mechanics of private and listed credit.

A critical component of this emerging infrastructure is the ability to manage private and bespoke instruments seamlessly alongside more traditional public assets. Achieving operational and liquidity interoperability between these two segments would mark a major step forward, creating a more efficient, integrated, and resilient financial ecosystem.

Workflow Automation: The use of advanced workflow tools enables automation of crucial processes such as new fundraise creation for issuers, electronic fund allocation for selected investors; and integrated settlement orchestration. Automation reduces operational errors in both public and private debt issuance. However, continued reliance on manual processes, such as managing private transactions outside of the platform, increases the likelihood of errors. This further reinforces the value of a unified, automated workflow solution.

Multi-Asset Liquidity: Addressing the limited secondary trading volume requires a system that extends well beyond traditional listed bonds. Future advancements in the industry must establish a centralised venue for multilateral negotiation and trading of a range of assets, merging traditional listed instruments with dematerialised loans or notes, REPOs, and other structured products. This shift supports the goal of improving liquidity and execution capabilities for the entire market.

Intengo Market provides a digital ecosystem designed for debt issuers, investors, and intermediaries that is addressing these exact market challenges.

Crucially, Intengo enhances pricing transparency and discovery by integrating market intelligence and leveraging its unique data advantage. The platform collects anonymised auction bid-level data and secondary market trading data to build independent fair value curves. Unlike models based solely on listed data, Intengo’s approach incorporates the collective intelligence of the local institutional investor base to model credit spread curves that reflect true market consensus. This separates fundamental value from short-term market volatility, delivering rigorous, transparent analytics that bring private credit pricing closer to the efficiency of public markets.

Conclusion

The expansion of private credit is not a cyclical phenomenon, but a structural shift driven by an evolving and more sophisticated investor universe couple with a cost sensitive issuer base. While the inherent challenges of illiquidity, complexity, and valuation opacity remain central to the asset class, the South African market presents compelling opportunities for institutional investors who possess the local expertise to navigate its complexities. By leveraging technological platforms to enhance origination capabilities, data transparency and streamline transaction execution, the South African private credit market is poised to mature further, providing critical bespoke financing for growth while delivering potentially attractive risk-adjusted returns for sophisticated institutional investors.

Harmony Gold has completed the MAC Copper acquisition (JSE: HAR)

The R18.4 billion transaction is just one example of large mining houses chasing copper

Harmony Gold announced the MAC Copper acquisition back in May 2025. It always takes several months to get deals of this size across the line. The good news is that the wait is over, with Harmony implementing the deal with effect from 24 October. The total equity value was R18.4 billion ($1.01 billion), funding using cash reserves and a bridge facility (debt).

Harmony will focus on integrating MAC Copper into their group over the next three months. They will give a detailed update on operational performance and key development milestones when interim results are released in February/March 2026.

Metrofile has released the circular for the Mango Holding take-private (JSE: MFL)

The shareholder meeting will take place in November

After many years of deals waiting in the wings and not materialising, Metrofile shareholders finally have a take-private to consider in the form of a scheme of arrangement. A special purpose vehicle put together by Mango Holding acts as the offeror, with the plan being for the offeror to obtain a platform across Africa and the Middle East. If you work your way up the chain, you eventually land at WndrCo LLC as the largest individual shareholder, a technology investment firm focused on consumerisation of software. That makes sense. There are some other entrepreneurs and high net worth individuals involved who have experience in software as well.

For Metrofile shareholders, it’s much simpler than that: the scheme is a way to sell their shares at a premium of 95% to the 30-day VWAP up to 25 March, the day prior to the release of the cautionary. Before you get too excited about that premium, you need to see a multi-year chart of the share price:

As you can see, the price was extremely depressed when the offeror swooped earlier this year. The price of R3.25 per share is in line with where the shares traded in July 2023, except the offeror would be getting control of the company for this price!

A deal isn’t a deal until the conditions have been met, with the most important one at this stage being the shareholder approval. Irrevocable undertakings have been received from holders of 52.81% of shares in issue. That’s a very good start, but it doesn’t guarantee a successful outcome. They need 75% approval for the scheme.

The general meeting for the vote by shareholders is scheduled for 24 November.

Orion Minerals looks back on a watershed quarter (JSE: ORN)

The share price really tells the story

Junior mining companies are required to release quarterly activity reports to keep the market updated about the progress being made. Even if you know nothing about Orion Minerals, this chart will give you an idea of how important the latest quarter has been:

The biggest driver of this change in sentiment was the signing of a non-binding term sheet with a subsidiary of Glencore (JSE: GLN) for a financing package of $200 – $250 million. They’ve also made a key appointment of a project director and focused on further work at the underlying projects.

If you follow the company, you’ll also know that Orion has been busy with post-quarter capital raising activities. The planned raise was upsized a couple of times to the current level of roughly R99 million. Cash on hand at the end of the quarter was only around R6 million, so these capital raises are very necessary.

Quantum Foods is enjoying much better operating conditions (JSE: QFH)

HEPS shot up in FY25

Quantum Foods released a trading statement for the year ended September 2025. We knew that it was going to be a strong year, as interim HEPS was up by a rather spectacular 244%. Yes, this means that interim HEPS more than tripled!

The full-year move wasn’t nearly as impressive, but nobody is going to complain about a HEPS move of between 58% and 78%. It’s actually worth isolating the second half of the year to get a sense of the maintainable growth rate. In 2H’24, HEPS was 58.7 cents (you calculate this by substracting the comparable interim HEPS from the comparable full-year HEPS). In 2H’25, HEPS was between 52.6 cents and 68.6 cents. You can therefore see that the move in the second half of the year was very tame in comparison to the first half. At the midpoint of guidance (60.6 cents for 2H’25), it reflects growth of 3.2% for the second half.

Why is this the case? Well, it all makes sense when you look at how severely the previous period was hit by HPAI outbreaks (bird flu) and load shedding, particularly in the first half of FY24. This effect was less significant in the year-on-year growth for the second half of the year. Another reason why 2H’25 was softer is because egg prices in FY25 were 17% lower than in FY24. Despite a 79% jump in egg supply, the egg operations actually suffered a drop in profitability year-on-year because of the prices.

Thankfully, the weighted average cost of broiler feed was down 2% and layer feed was unchanged, thanks to a drop in price of soya meal that helped them offset the impact of expensive yellow maize. This is one of the reasons why the farming business was the star of the show on a year-on-year basis, with much higher layer flock numbers driving efficiencies and better cost recoveries. They talk about “much improved earnings” despite a small HPAI outbreak and other irritations like an administrative penalty related to a farm in the Eastern Cape. On the broiler side of the farming business, volumes were up and cost recoveries benefitted as a result.

In the feed business, total volumes were up 9% as volumes supplied to the external market and internally were boosted by the recovery in flocks across the country.

In the other African operations, Zambia and particularly Mozambique were difficult, with the latter impacted by civil unrest and outright theft of 16% of the birds in an incident in December 2024. Uganda thankfully has a far more positive story to tell, with earnings heading in the right direction.

Full results will be available on 28 November. The share price closed 13.6% higher on the day of results, but this was on very thin volumes and you can safely ignore that move. Interestingly, the share price is down 12.7% year-to-date and down 23.6% over 12 months.

Safari Investments isn’t wasting any time with its plan to go private (JSE: SAR)

The circular is out in the wild already

On 17 October, Safari Investments released a firm intention announcement regarding a plan to repurchase all the shares not held by Heriot REIT (JSE: HET) and its subsidiaries. In other words, this is Heriot taking Safari Investments private, but using Safari’s balance sheet. They are in a hurry to get it done, with the circular already released and the delisting date penciled in for 23 December.

Safari’s stock is highly illiquid and Heriot already owns 59.2% of the fund, so a delisting makes sense here. Another reason for the delisting is that Safari plans to undertake developments going forwards, so that makes things difficult for a REIT in terms of consistent dividends.

Irrevocable undertakings have been received from holders of 34.03% of the shares eligible to vote. This is an important point to understand. Heriot and its concert parties have 61.28% of the shares in issue, so only 38.72% of total shares in issue are eligible to vote. From that voting pool, 75% approval is required and they’ve locked in irrevocables from 34.03% (i.e. 34.03% of the 38.72%, not 34.03% of all shares in issue).

Incredibly, the fair value range of the shares is between R7.67 and R8.54, despite the net asset value (NAV) per share being R11.77 as at June 2025. In determining this fair value range, Moore acted as independent expert and used discounted cash flow and capitalisation of earnings. They took note of the much higher NAV per share and applied a market-related discount of 35.16% (based on observable JSE discounts) to arrive at the fair value.

In summary: the NAV of JSE-listed property funds is about as useful as those stapled condoms that once made headlines in South Africa. We know this already, but here it is in black and white. REITs are valued on yield and yield alone. It’s time that impairments to balance sheets were recognised to take this into account.

Nibbles:

Director dealings:

To give you an idea of what truly impressive balance sheets look like, Capitec (JSE: CPI) announced a couple of transactions by the founders. Michiel le Roux executed an option transaction with a put strike price of around R2,754 and a call strike of around R5,251 (the current spot price is R4,030). The expiry date is 1.29 years on average. The options relate to 350,000 shares, or a casual R1.4 billion in shares based on the call price! Separately, an associate of Piet Mouton pledged shares worth R2.3 billion for a loan facility. What do the kids say again? Aah yes, “there are levels to this game”.

A director of OUTsurance (JSE: OUT) bought shares worth over R3.25 million.

A non-executive director of Hammerson (JSE: HMN), bought shares in the company worth nearly R180k through the reinvestment of dividends.

The CEO of Spear REIT (JSE: SEA) bought shares in his family investment vehicles worth R98k.

The CEO of Vunani (JSE: VUN) bought shares worth R4k, adding to his recent purchases.

Canal+ has begun the squeeze-out process to acquire the remaining shares in MultiChoice (JSE: MCG). The MultiChoice listing is suspended from trading with effect from 27 October and will be terminated on 10 December (subject to final regulatory steps). For this reason, MultiChoice will not be releasing its interim results on 12 November 2025 as would otherwise have been the case.

With shareholders having given their support to the Natco Pharma offer, Adcock Ingram (JSE: AIP) has confirmed that the listing will be terminated with effect from 11 November. The scheme consideration of R75 per share will be paid to shareholders on 10 November.

Pan African Resources (JSE: PAN) has officially transitioned from the AIM to the London Stock Exchange Main Market. The company hasn’t issued any new shares in this regard. They’ve simple transferred the listing from the development board to the main board in a move that should help them attract larger institutional shareholders.

Barloworld (JSE: BAW) announced that Nopasika Lila is retiring as group finance director. According to the announcement, she leaves from 31 November 2025 – a date that doesn’t exist on the calendar! Ghostly dates aside, new finance director Relebohile Sehoole will be in that role with effect from 1 December 2025. At least that’s a date that you can find in your Outlook calendar. This is an internal promotion, which is always good to see.

Africa Bitcoin Corporation (JSE: BAC) announced that BDO has resigned as external auditor. This is because Forvis Mazars in South Africa has been appointed as auditor of the subsidiary Africa Bitcoin Strategies, which is en route to becoming a significant component of the group. BDO is looking to avoid a situation where they need to rely on an audit conducted by another firm on a large component of the group. The company hasn’t announced a new external auditor yet.

How a tropical island experiment, a writers’ strike, and a collapsing TV economy gave birth to modern day reality television.

The year was 2000. Pants were worn low, bean bags were everywhere, and you had to hit the number 6 three times on your Motorola Razr to type a letter “o”. Most people were just happy to have survived the Y2K bug. Little did we all know that our lives were about to be permanently altered – because this was the summer that Survivor premiered.

Before this moment, prime-time television was either rehearsed laughter in sitcoms, carefully plotted twists in dramas, or polished faces on talk shows. Then CBS sent sixteen strangers into an island wilderness and waited for a different kind of storytelling to unfold. Instead of a script, the world tuned in to the slow, combustible chemistry of humans under pressure.

It is tempting to tell the story of Survivor as a show that arrived fully formed and changed everything overnight. The truth is messier and more interesting. Reality television had been inching its way into American homes for years. Fox’s Cops and America’s Most Wanted had already blurred the line between reportage and entertainment while MTV’s The Real World (born of the early 1990s) had proved that unvarnished young lives could sustain narrative arcs across a season. But Survivor altered the gravitational pull of the medium. It turned unscripted spectacle into an engine that could fill schedules, attract advertisers, and redefine what networks thought viewers wanted. In short: it launched reality TV.

The market that found its formula

When the finale of the first season of Survivor aired, 51 million viewers tuned in. For context, that number belonged to an era when network television still measured cultural gravity in tens of millions of viewers per event; that year, it was a rating only eclipsed by the Super Bowl. The ratings translated into advertising gold, with CBS reportedly charging $600,000 per 30 second ad slot during the finale. The rest of the industry quickly sat up and took notice.

But Survivor didn’t just succeed because it was entertaining; it worked because it arrived at the exact moment the old model of television was collapsing under its own weight. By the late 1990s, scripted programming had become prohibitively expensive. Networks were paying millions per episode to retain stars, and writers’ guild negotiations had grown increasingly fraught. The 1988 Writers Guild strike (one of the longest in Hollywood history at the time) had already exposed how vulnerable networks were to production shutdowns. Executives began quietly searching for formats that could bypass unions altogether – shows without scripts, without actors, and without the constant threat of collective bargaining.

When Survivor arrived, it offered the perfect economic solution. It required no name-brand talent, no residuals, and no writers’ rooms full of salaried professionals. The drama was human and unscripted, the labour non-union, the costs minimal. Reality television was a new genre, sure, but it was also a business model born out of financial necessity. It allowed networks to fill airtime year-round without the overhead of scripted production, and audiences, exhausted by formulaic sitcoms, devoured the novelty.

No surprise, then, that the following years felt like a chain reaction. CBS doubled down on the success of Survivor by launching Big Brother and The Amazing Race, while Fox answered with American Idol. By the mid-2000s, every major network had a version of reality that suited its brand – ABC had The Bachelor and Extreme Makeover: Home Edition, NBC ran The Apprentice and The Biggest Loser; while MTV pivoted from music videos to household sagas with The Osbournes and Newlyweds. The medium matured not into a single shape but into many: competition, voyeurism, makeover, talent. In 2003 the Emmys created categories to acknowledge the impact. Reality TV had shifted from a curiosity into an industry.

How real is “real”?

From the start, the producers behind Survivor wanted to manufacture chaos. Their original plan for the show’s opening was to literally sink the ship that the contestants were on and have them swim to the island. When that proved logistically impossible (and more than a little dangerous), they settled for the next best thing: loading sixteen people onto a vessel, announcing that they had ten minutes to grab whatever they could carry, and sending them off in rafts toward an island. Things went wrong practically immediately: the waves were rougher than expected, contestants were vomiting everywhere, and what looked like a short distance required more than two hours of rowing to cover. The cameras kept rolling, capturing it all.

The island itself was more wilderness than set. There were no amenities, no real shelter, and, as it turned out, not even sleeping quarters for the crew. Cameramen, sound operators, and producers found themselves camping on the same beaches as their subjects, with their notebooks dissolving in the humidity and their nights interrupted by rats and snakes crawling over their legs. Both cast and crew lost weight, battled parasites, and suffered heat exhaustion. By the end of the 40-day shoot, many were physically wrecked and emotionally frayed.

This is what made Survivor so strangely compelling: its reality was constructed, but the suffering wasn’t. The conditions forced out real tears, real hunger, real desperation. A confession filmed in the middle of that chaos might have been edited for drama, but the emotion itself was authentic; the product of exhaustion and exposure as much as narrative design.

That’s the sleight of hand that defines reality television as a whole. The illusion of pure spontaneity is built on careful orchestration, but the emotions it captures are not false. The cameras didn’t create the breakdowns, but they did make sure the breakdowns were seen. What audiences respond to isn’t factual accuracy, but emotional truth – the visceral, uncomfortable immediacy of watching people pushed to their limits.

The people left to pick up the pieces

The consequences of manufactured authenticity are both personal and institutional. Contestants returning from seasons of Survivor are often in poor physical and emotional shape. Parasites, weight loss, and psychological strain are not rare. The first season of Survivor had “therapists” on set that contestants could request to talk to – but these therapists were on the CBS payroll, and therefore occupied a conflicted place between care and production priorities. After months of deprivation and public scrutiny, many former players described an unsettling sense of betrayal. They had been invited to participate in an experience that promised adventure and exposure, only to find themselves subject to manipulation in service of entertainment.

That ethical tension followed the shows into the culture at large. Reality television has normalised certain types of voyeurism, and it raised questions about consent in pressured circumstances and the responsibilities producers hold toward participants. Those questions have still not fully been answered, even as 57% of new TV programming today is classified as reality TV. Since 2000, at least 38 reality TV participants have died by suicide. The genre built its empire on access to the most vulnerable parts of human experience, but in doing so, it forced us to confront an uncomfortable truth: the line between storytelling and harm is far thinner than television ever let on.

What it left behind

You could argue that Survivor taught television to trade in intimacy. Audiences learned to care about ordinary people in extraordinary situations, to root for underdogs, to analyse social gameplay with the same intensity critics applied to scripted narratives. The genre diversified, hybridised, and metastasised into shows about talent, transformation, and competition. It reshaped summer programming and rebalanced industry economics in favour of formats that could be produced quickly and cheaply.

Two decades on, Survivor itself endures, its edges refined, its craftsmanship slicker, its players more strategic and media-savvy. The island is less of an accident and more of a calibrated laboratory (rumour has it the crew have actual quarters these days). Yet the fundamental equation remains the same: remove the comforts that prop up civilized behaviour, challenge people to meet one another in a confined social field, and let the human drama do the rest.

After all these years, the tribe still speaks. We listen – sometimes appalled, often delighted – and we keep coming back for more, not because we believe everything we see, but because, for a few hours a week, television gives us a mirror that is discomfitingly human. There’s just far more reality TV to choose from these days.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

4Sight Holdings is a small cap to watch (JSE: 4SI)

The share price has more than tripled over three years

As the name suggests, 4Sight is a future-focused company that manages to use just about every tech buzzword that you can possibly think of. Unlike most international tech companies that mention AI, 4Sight is more about profit growth than revenue at the moment. This makes it far more interesting than the tech furnaces that burn investor capital in the pursuit of revenue at all costs.

4Sight’s revenue was up just 6.8% for the six months to August, yet this was good enough for operating profit to increase by 35.7% and for HEPS to jump by 30.2%!

The group has four customer-focused segments and all of them are profitable. Services range from consulting through to reselling software for international partners. It’s a model that is clearly working.

Adcorp’s earnings are much higher, but watch out for those once-offs (JSE: ADR)

The prior period included some big non-recurring costs

Adcorp released a trading statement for the six months to August 2025 that reflects a huge jump in HEPS of between 83% and 92.9%. Before you get too excited about extrapolating that growth rate into the future, the company points out that the comparable period included once-off costs of R25.6 million. I went back and checked last year’s numbers: operating profit was R42.3 million and profit after tax was R29.4 million, so not having those costs in this period would explain a big part of the positive year-on-year move.

It’s not the sole reason for the uplift though. Adcorp’s announcement speaks to the benefits coming through from restructuring activities, a necessary step to address challenges around demand and the impact of a stronger rand.

The demand pressure is particularly clear in the Professional Services portfolio in South Africa. You can imagine the negative impact that AI is having on hiring at the moment, with the disruption caused by LinkedIn as another major challenge. Adcorp is seeing its best results in the Contingent Staffing and Staffing Solutions businesses, which makes perfect sense as AI can’t do those jobs and LinkedIn is far less relevant.

It’s much the same in Australia in terms of areas of relative strength, although the Professional Services business on that side of the pond seems to be doing better than in South Africa thanks to the focus on the technology and consulting sectors.

Although the share price closed 13% higher in response to this update, it was on lighter than average volumes.

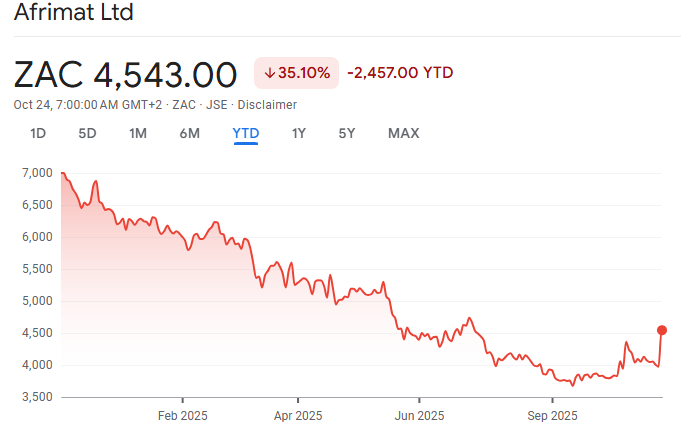

Yes, it turns out that Afrimat was indeed “primed for a big positive swing” as I wrote earlier this month (JSE: AFT)

Momentum is a powerful thing

Earlier this month, Afrimat released an encouraging trading statement that looked capable of changing the trajectory of the share price during a really tough year. In Ghost Bites at the time, I wrote that Afrimat looked promising for a positive swing and could rally back to the R50 level. After releasing full results on Thursday, the share price closed 14.4% higher at over R45. As I suspected, the market wants to close the gap on this one and see it go up.

But where does that leave us on a year-to-date basis?

As you can see, there’s a long way to go. Afrimat is still running way below the levels of profitability seen in the past few years, and not just because of the impact of the Lafarge integration.

The trick in this period was the second quarter momentum, where things got better in local iron ore sales and the ex-Lafarge cement factory. Markets absolutely love momentum, as share prices move in anticipation of future earnings. When the second quarter is better than the first quarter, the market focuses on the exit velocity for the period and buys accordingly.

For the six months, Afrimat’s revenue was up 29.9% and HEPS almost doubled, up 92.3% to 101.9 cents. For context, this is measured against a terribly weak base, as interim HEPS was 263.4 cents in 2023 before plummeting to 53 cents in 2024.

Part of the gap to historical earnings is that the cement business is still loss-making, despite revenue increasing by a whopping 118.8%. They truly did swing for the fences with the Lafarge deal and the jury is still out on whether it was the right call or not.

Iron ore export volumes need to be highlighted. Although they increased 13.5% year-on-year in the interim period, Afrimat has noted that the full-year volumes are likely to be flat based on expected pressure in the second half from maintenance activity on the Saldanha export line. There are also other major headaches in the local market, like the sad state of play in the ferrochrome industry and what this means for the Nkomati Anthracite Mine.

Afrimat’s share price has turned the corner for now at least. All eyes will be on the momentum in the ex-Lafarge assets in the second half of the year.

Do they ever sleep at ASP Isotopes? (JSE: ISO)

Subsidiary Quantum Leap Energy LLC has announced an acquisition

There are many listed companies that announce only one or two unusual things a year. ASP Isotopes certainly won’t be in that category, as the group is on an aggressive growth path that means plenty of capital raising and deal activity.

The latest such example is an acquisition by US subsidiary Quantum Leap Energy LLC. They are acquiring certain assets from a company called One30Seven, which focuses on decontamination solutions for water-soluble nuclear waste. There’s a lot of cutting-edge science involved here, with the overall goal being to increase the vertical integration of Quantum Leap Energy’s business in the nuclear fuel cycle through the development and commercialisation of the Creber machines that One30Seven is building.

The size of the prize is massive, as the Department of Energy in the US is on the hook for many billions of dollars to store nuclear waste. A solution that could process the waste rather than store it would obviously be of immense value.

As a further delightful little outcome, the initial isotope they are targeting is Cesium-137, which decays into stable Barium-137 – an isotope of increasing importance in quantum computing. It sounds to me like they have a few ways to make bucketloads of cash if this goes well.

The initial deal value is a cash payment of $150k and stock worth $2.85 million. When the first Creber Mini Unit is operational, they will pay a further $6 million. When a Creber Midi or Maxi Unit is done, there’s a payment of $11 million. These names keep reminding me of buying Chip ‘n Dip once a year when I go watch the Simola Hillclimb in Knysna!

The larger initial cost is the consulting agreement with inventor Brian Creber and his company B-Con Engineering Inc, with an estimated development cost of $4.5 million for the Creber Mini and $12.5 – $13 million for a Midi or Maxi Unit.

One30Seven was clever enough to lock in an ongoing royalty agreement, based on 6% of net revenues for 15 years per product. If this thing goes as planned, that’s the most lucrative part of the deal for them.

Liquidity in the stock is still limited on the JSE, but will hopefully improve over time.

Clicks has an outrageously good return on equity (JSE: CLS)

HEPS growth in the mid-teens doesn’t hurt either

Clicks enjoys one of the most demanding valuations on the JSE. That P/E multiple has been earned though, as the company boasts a defensive offering that is taking full advantage of the upward mobility of the average South African consumer in terms of having more disposable income available for health and beauty.

Clicks achieved a return on equity of 49.2% in the year ended August 2025. Yes, 49.2%! For context, that’s 3x higher than most South African legacy banks and with a more defensive underlying business than the banks. It’s little wonder that the market pays up for the story.

There’s also no shortage of growth, with group turnover up 5.3% in this period and trading margin up 60 basis points to 9.8%. Diluted HEPS rose by a delightful 14.1% and the dividend followed suit, up 14.2%.

The private label offering is a highlight, with growth in turnover of 10.7% in the in-house brands at Clicks. Another positive element to the result is the extent of store openings, with 55 net new stores and a total base of over 990 stores. Not every store has a pharmacy, as there are only 780 pharmacies in the store footprint. Pharmacy licensing is a complicated area and it contributes to the ability of smaller pharmacies to compete (if this interests you, be sure to listen to my podcast with Hugh Cunningham of The Local Choice Pharmacy in Harmelia).

When you see such an extensive store roll-out programme, you need to watch out for comparable or like-for-like sales to make sure that all the growth isn’t just coming from capex to increase the store footprint. Clicks managed comparable store turnover of 4.7% with volume growth of 2.1% and inflation of 2.6%, so that’s decent under the circumstances.

The Retail business continues to outperform the Distribution (wholesale) business, with turnover growth of 7% in the former vs. 5.1% in the latter. More importantly, Distribution suffered a decline in margin of 10 basis points, while Retail’s margin was up 70 basis points. The distribution business is key to Clicks’ strategy and needs to be there, but nothing beats the value of having the consumer relationship in the retailer.

In case you’re wondering about the OG of loyalty programmes in South Africa, Clicks ClubCard, they are up to 12.6 million active members who account for 82.6% of sales in Clicks.

As a final fun fact, one of the drivers of higher inventory in the group was demand for GLP-1 product, leading to buy-ins at the wholesaler. That’s an interesting read-through for Aspen (JSE: APN).

The group continues to work towards the medium-term target of 1,200 stores and will exceed 1,000 stores in the coming year. They also plan to get private label participation up to 35% of front shop sales, which will further boost margin. And yet, the share price is flat this year thanks to the extent to which this growth is already priced into the story:

Labat Africa has found a buyer for the cannabis assets (JSE: LAB)

They can now focus exclusively on technology

Labat Africa has been making huge strides recently thanks to the technology assets that were injected into the group. To create a pure-play technology company that might be of more interest to investors, they announced that they were looking at selling the cannabis assets.

After negotiations with several parties, the buyer has been announced. 64P Investments, an unrelated party, will be acquiring the assets for R23 million. This is well above the independent valuation of R15 million to R17 million. It’s much higher than the NAV of R5.3 million.

Here’s the funny thing though: these assets made a profit of R17.5 million in the last reporting period, so these earnings are clearly not maintainable as the independent valuation range suggests a P/E of less than 1x!

This is a Category 2 deal, so shareholders won’t be asked to vote on it.

Raubex’s earnings have dipped (JSE: RBX)

Australia is the problem

Raubex has released a trading update for the six months to August 2025. It’s not good news unfortunately, with an expected drop in HEPS of 10% to 20%.

The Roads and Earthworks division grew its operating profit, with SANRAL projects as the major driver of performance. They’ve won some impressive new tenders to keep things ticking over.

The Construction Materials division seems to be a mixed bag, with weather conditions in March and April affecting the performance in the first couple of months of the period. They have a wide variety of businesses in this space, with underlying drivers like the agriculture sector (positive in this period) and asphalt and aggregates (both off to a slow start that subsequently improved).

The Infrastructure division has been focusing on renewable energy projects and they’ve flagged a “substantial increase” in operating profit for this period, so investors will be pleased with that. The outlook for affordable housing projects is positive, with the company referencing the lower interest rates as a source of stimulus in this space. There are other major projects in process as well, like the parliament buildings in Cape Town and the Potsdam Wastewater Treatment Plant. They are clearly keen for more wastewater work, as they acquired a company called Hlumisa Engineering Services that specialises in this space.

The Materials Handling and Mining division is where some of the challenges are to be found. Their chrome operations were really rough in the second half of the prior year (a R351 million loss), so recovering from that to a break-even performance in this half is a great sequential story. Importantly, Kookfontein’s PGM plant has been commissioned and sales are expected to commence in the second half of the year, so hopefully the PGM market will remain favourable for them. Something else worth mentioning is that although Bauba is performing better than it was at the end of the previous financial year, Raubex is evaluating the long-term strategic direction of the business. When corporates talk like that, they are usually thinking of selling.

Australia is the problem child, with an operating loss this period thanks to a major underperforming project. They lost R210 million on a specific project that was terminated in September 2025. Although Raubex might be able to recover some of the losses, they’ve taken a nasty knock here. The rest of the Australian business is profitable and they’ve been busy with acquisitions and organic growth in that market.

Looking ahead, the secured order book has reached record levels and they are seeing positive momentum in infrastructure spend in South Africa. Things rarely go up in a straight line and Raubex is no different.

A big day for Sasol (JSE: SOL)

The share price closed 17% higher!

It’s hard to think of a better example of a stock that has driven a rollercoaster ride of emotions for so many investors, especially pandemic-era newbies who jumped on the Sasol train in 2020 / 2021. Just look at this share price chart:

When the Sasol price moves, it really moves. It closed 17% higher on Thursday based on the release of business performance metrics (like production volumes) for the three months to September.

The key highlight is that the destoning plant is delivering results, improving coal quality and driving better production at Secunda Operations. They also enjoyed better sales volumes in Fuels thanks to improved performance at Natref and Sasolburg.

It can’t all be good news, of course. Chemicals Africa volumes were in line with the prior period, but revenue was down due to weaker selling prices. The International Chemicals business has a more positive story to tell, with some pricing uplift seen in markets like Eurasia. This was good enough for the international business to achieve “significantly higher” revenue and EBITDA, with the latter supported by margin optimisation initiatives.

The story at Sasol remains one of driving margins in chemicals while doing the best they can in the fuels business and hoping that the oil price does the rest. The breakeven oil price for the quarter was in line with the market guidance of $55 – $60/bbl. Personally, I don’t have much faith in the oil price moving meaningfully higher over time, hence I don’t have a long position in Sasol.

Nibbles:

Director dealings:

The CEO of Vunani Limited (JSE: VUN) bought shares worth R10k.

A director of a major subsidiary of OUTsurance Group (JSE: OUT) bought shares for a minor child to the value of R7k.

Spear REIT (JSE: SEA) announced that the acquisition of Consani Industrial Park in Elsie’s River Industria has met all the conditions precedent. The registration of the property transfer is expected to take place in December 2025.

If you’re interested in Oasis Crescent Property Fund (JSE: OAS), a Shari’ah-compliant property fund that runs with no debt (something you won’t see anywhere else in the sector), then you may want to flick through their presentation showing the portfolio and the future plans.

Mantengu Mining (JSE: MTU) renewed the cautionary announcement related to the potential acquisition of Kilken Platinum. They are busy with the due diligence and assessing the price and regulatory requirements for the deal.

The offeror in the Barloworld (JSE: BAW) deal is up to a 67.3% holding in the company. If you combine this with the related and concert parties, it’s up to 90.6%.

Famous Brands is up, but on shaky ground (JSE: FBR)

The manufacturing segment saved this result– again

Famous Brands has had an extremely volatile share price in the past year. The company is way off the levels seen during the GNU exuberance, but has recently been moving higher after testing the 52-week low. For those who enjoy a bit of momentum trading, this chart might be interesting:

The business itself is doing better than the chart might otherwise suggest, although a deeper dive into the numbers will reveal where the risks are.

For the six months to August, revenue increased 5.6% and operating profit was up 5.8%. This means that Famous Brands achieved margin expansion despite that modest growth rate. HEPS increased by 8% and the dividend per share was also up 8%. It’s always good to see a higher growth rate in HEPS than in revenue, as it means that the company is using leverage successfully.

On the face of it, this looks like a resilient performance that investors should feel good about, particularly as the results for the year to February 2025 reflected pressure in almost every segment in the business. Have things actually turned around?

Let’s dig deeper to see where the improvement lies. Leading Brands (the typical takeaway outlets that the group is, well, famous for) grew like-for-like sales by 2.6% and system-wide sales by 6.0%, a significant acceleration vs. the previous financial year. Interestingly, only 27.8% of new restaurants were allocated to existing franchise partners, so there are lots of new investors who want to own a franchise. Unfortunately, this didn’t translate into any growth in operating profit, with an almost perfectly flat performance on a year-on-year basis.

Signature Brands remains a struggle. The trend of weak sales and a worsening operating margin continued in this period, with like-for-like sales down 0.6% and the operating loss margin moving from -6.7% to -7.0%. The company-owned PAUL restaurants haven’t even broken even yet. Personally, I think Famous Brands should just stick to selling burgers and pizzas.

In the SADC region, operating profit fell by 11.8% despite revenue growth of 2.7%. The AME region saw revenue fall 5.4%, with the operating loss only slightly better at -R19 million vs. -R22 million in the prior period. For context, the AME loss almost full offsets the operating profit of R24 million in SADC! UK Wimpy is just as bad, with operating profit of only R1 million. Why bother?

The supply chain side of the business has been a stronger recent performer, although I worry about how sustainable this is if the restaurants aren’t doing well. Has this continued?

Sure enough, manufacturing revenue increased 10.4% and operating profit was up 23.6%, with margins up from 9.3% to 10.4%. The logistics business runs at paper-thin margins, with revenue up 7.4% and operating profit down 14.8% as margins dipped to 1.1%. Finally, joining Wimpy UK in the why-bother bucket, we have Famous Brands’ retail business with an operating loss of R12 million from revenue of R171 million.

Customers are seeking better value all the time and Famous Brands operates in a very competitive space. Their group numbers look decent this period, but it’s more of the same in terms of relying on the manufacturing side to drive growth.

My view remains that the group is still too complicated and stretched too thin. Much like a pizza base, if you roll the dough too thin to try and cover too much ground, it breaks.

Quilter’s momentum in net flows continues (JSE: QLT)

They are already way ahead of the prior year – and only nine months in

Quilter is demonstrating the power of distribution. For financial services businesses to really make the big bucks, they need to be able to attract flows rather than just manage them. Quilter is doing an excellent job of that, with the third quarter in a row of net inflows in excess of £2 billion. Amazingly, third quarter flows were up 48% year-on-year and represent 7% of opening assets under management and administration (AuMA)!

This is why the third quarter year-to-date net inflow of £6.7 billion is already so far ahead of the full-year 2024 number of £5.2 billion. These are impressive numbers, with a positive story being told across the High Net Worth and especially Affluent channels.

From a profitability perspective, the business is becoming more productive over time (gross sales per adviser increased 10% year-on-year). This implies enhanced profitability at operational level. They don’t disclose profits for the quarter, but it’s hard not to believe that the full-year numbers will be strong based on these underlying metrics.

Salungano Group’s Keaton Mining has signed a coal supply agreement with Eskom (JSE: SLG)

As a reminder, the shares are still suspended from trading

Salungano Group recently released their financials for the year ended March 2024. No, you aren’t losing your mind – they are indeed very far behind. This is why the shares are currently suspended from trading.

Being suspended from trading isn’t the same as being prevented from doing business. It just means that the shares can’t change hands on the JSE in the normal way.

In the business itself, Salungano’s wholly-owned subsidiary Keaton Mining has signed a coal supply agreement with Eskom for the supply of coal from the Vanggatfontein Colliery. Deliveries will start on 1 November 2025 and run until the contracted quantity (6.5 million tons) has been delivered, which is estimated to take five years and two months.

Above all else, this obviously makes a big difference to the going concern assessment at Keaton Mining.

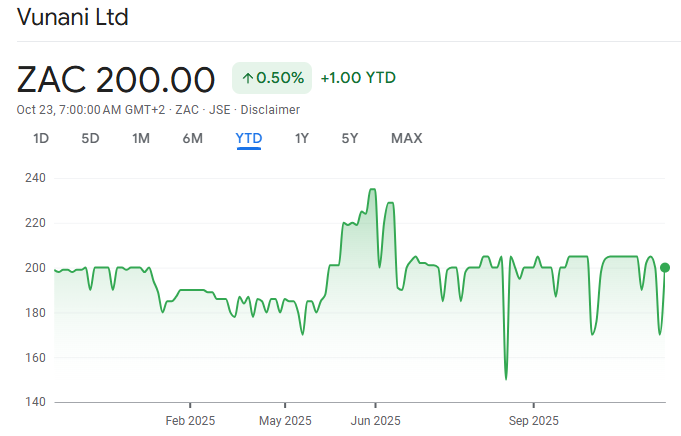

Vunani achieved revenue growth in every segment (JSE: VUN)

This addsto the positivityaround the recently announced Sentio merger

Vunani is having a year to remember. The group has been a tough story in recent years, with the share price still trading roughly 30% lower than three years ago. The stock is stuck in bid-offer spread hell right now, which is why the share price looks like this:

In the underlying business though, there are positive recent updates. Vunani will be merging with Sentio Capital Management to form a combined business with R60 billion in funds under management. Consolidation in that space makes sense, as margins are tight.

Even without the merger, Vunani’s business seems to be improving. The strong performance of the local market is good news for any fund management and securities broking business. Vunnai’s group revenue increased by 8.8% for the six months to August 2025, with each of the underlying segments achieving growth in revenue. The profit performance was a bit choppier, with two of the five segments still in loss-making positions.

By the time we reach HEPS, Vunani’s growth was a delightful 41.8%. They will certainly hope that this momentum can continue.

Nibbles:

Director dealings:

Jan Potgieter has sold more shares in Italtile (JSE: ITE), this time to the value of almost R2 million. I guess if he’s no longer going to be a director of the company, he would rather diversify his wealth. Makes sense to me.

The company secretary of AVI (JSE: AVI) sold an entire share award worth nearly R1.6 million.

Barloworld (JSE: BAW) announced that the PIC has disposed of all its shares in the company in terms of the offer by the consortium.

Marshall Monteagle (JSE: MMP) is selling the Nicol Garage property in Durban for R68.5 million. The purchaser is a private company that isn’t a related party. The property consists of a parking garage and multi-tenanted ground floor units with 129 small business tenants. The income at the property is R1.6 million per month. The net asset value is a whopping R132.7 million, so they are selling this way below book. The property made a loss of R9.4 million in the year ended March, which might explain why they are happy to let it go at this price.

In happy news for the overall functioning of the market, Insimbi Industrial Holdings (JSE: ISB) announced that the erroneous broker trades that we saw last week are being fixed by the broker. The announcement doesn’t clarify exactly how this fix is happening. This includes the CEO’s trades. This affected a number of companies, but I assume that Insimbi being corrected means that all of them are being corrected.

Hulamin (JSE: HLM) has noted that they are hosting an investor day on Thursday. Keep an eye out for the presentation!

aReit (JSE: APO) is still trying to get audited financials done. They’ve now submitted financials for the year ended December 2023 to the auditors who previously resigned because they ran out of patience. Those auditors are considering whether they will take aReit on as a client again or not. The financials for the year ended December 2024 are also ready. They would also need to get interims for the six months to June 2025 done before the suspension can be lifted!

AYO Technology (JSE: AYO) has received the compliance certificate from the TRP for the delisting offer. The delisting will be effecting from 28 October.

We all need somewhere to live, but that doesn’t mean that buying property should be the default decision. Most of all, it doesn’t mean that buying any property at any price is sensible. Data-led decision making is crucial when buying a home, especially in South Africa where house prices don’t automatically go up.

Hayley Ivins-Downes and the team at Lightstone Property are passionate about helping South Africans apply more science to the emotiv decision of buying a home. With incredible data on property across the country, Lightstone makes it easier to avoid turning a dream home into a nightmare.

On this podcast, Hayley unpacked topics like:

Relative property values across provinces and the trend over the years

Development activity and the types of properties being built

The effect of the interest rate cycle

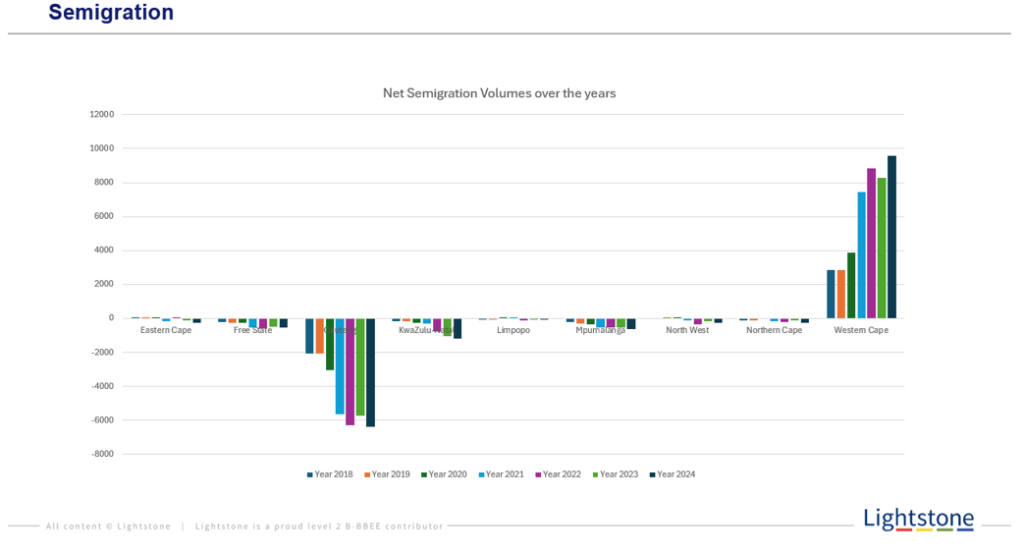

Semigration trends and the impact they have on values

How the average age of buyers has increased vs. ten years ago

The question on everyone’s lips in Cape Town: has the property trend reached a relative peak?

Property is one of the most important financial decisions you can make. If you do the research before you buy stocks, you should certainly do it before you buy property. You can learn more about Lightstone here.

Listen to the podcast here:

Transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. Thank you for being here with us. You’ve probably clicked on this because you have an interest in the property sector, and I think you will be well rewarded for that by getting some fantastic insights into the South African property market because today I have the great joy of speaking with Hayley Ivins-Downes. She is the Managing Executive of real estate at Lightstone Property.

Lightstone is fascinating because they have all the data, just all of it, basically – it’s brilliant! I’ve seen the reports, I’ve seen some of the stuff that you’re able to put out there, Hayley. I actually asked an agent for a Lightstone report, quite literally this week because I’m doing some planning around real estate for myself personally over the next few years. Data-led decision making hey – that’s something I’m passionate about, it’s something that you’re clearly passionate about.

So, Hayley, welcome to the show. Thank you for doing this. I’m very excited to dig in and get some fantastic insights from you.

Hayley Ivins-Downes: Great. Thanks, Ghost. It’s really great to be here and to be able to share some of our insights and knowledge and data from Lightstone. I think it’s really important for any homeowner / buyer / seller to make sure that they’ve got all the right information and making these decisions.

The Finance Ghost: Yeah, absolutely. And you’ve been with Lightstone for quite some time, so plenty of experience on this podcast, which I’m excited about.

So let’s maybe get a lay of the land, quite literally, actually, when it comes to Lightstone. I think people know the name, but I’m not sure that enough people know that they can ask for these reports from their agent. They can even go and buy the reports themselves. So let’s just get an understanding of what Lightstone actually is. What is the data set, how has it been built and why is it important?

Hayley Ivins-Downes: Lightstone is actually part of the Halls Group, coming out of Nelspruit and Mpumalanga area. We started in 2005, really just focused around offering information and valuations. We started by developing a residential property valuation model that the banks currently use in terms of granting of bonds. And so we use a lot of the deeds data. We’ve got all the history, all the transactions, and we obviously get a lot of insight out of that information.

We have over the years built up reports and specifically focusing on certain segments of the market – your banking, your insurance and your real estate. And for the man on the street, the home buyer, the homeowner, the home seller, we also have valuation reports which you can purchase with a credit card, pay as you go, which really makes it a lot easier than having to sign up.

Just as a matter of interest, when I was looking for a property, it was actually really quite important to ensure that you have all of this information. So sometimes it is not a bad thing to sign up for subscriptions because you have a month, because it does give you a lot of information on the area that you’re possibly going into and what is actually happening in that area on the property side.

So we’ve built up obviously a wealth of information over the years, and that just keeps us going and providing more information for really anybody in the property industry or sector.

The Finance Ghost: You’ve raised a really interesting point there, which is that the banks use this for valuations and a lot of people get caught out by this when they go and buy a house. So sometimes you have a buyer who just gets too hot for the deal and the seller and the agent manage to make it work. I mean, this is a negotiated transaction so if you don’t have your wits about you, then you will overpay for property.

And then you put in your offer to purchase and it’s subject to bond finance. And you’re assuming you’re going to get a 100% bond, and you might get a 100% bond – on the value that the bank thinks it’s worth! And if the bank thinks it’s worth R1.5 million and you’ve offered R1.7 million, you’re going to get a R1.5 million bond because the bank thinks you’re overpaying and so they don’t have enough asset cover on the bond. Is that accurate?

Hayley Ivins-Downes: Absolutely. I think that’s one of the benefits of having a Lightstone valuation report. This is really the valuation that the banks see as part of the process of granting the bond. They obviously assess their own credit information on the back-end, essentially on the buyer, but they use our valuation model and what our estimate is to help guide them as to whether they should be granting the bond and the amount that should be granted. So it’s really quite important to also have that knowledge before you buy the property, to understand what the bank may be seeing in terms of the process, in terms of the valuation estimate on the property you’re looking to purchase.

The Finance Ghost: A lot of people listening to this will be investors in shares on the market. This is just doing the valuation work, but for the property. You wouldn’t go and buy a share at any price – or you shouldn’t go and buy a share at any price – but people behave this way with property because I think it becomes such an emotive decision. You fall in love with a house or sometimes you live in a market where you end up in a situation where you’re squeezed on where you’re going to be next because rental stock is not always available. You can tell I live in Cape Town, it’s a very much a lived experience there – rental properties are not always available where you want them!

Or you want to try and lock in a specific house because your kids are starting school – there are a lot of reasons why people overpay for property and a lot of them are well-meaning reasons. These are not irrational reasons, but it can become a real issue down the line, not only from a bond perspective, but also just in terms of – you might really regret it in years to come. If you significantly overpay for a property, you can end up effectively underwater in that thing. At some point the shine comes off and you look at this and say, wow, how much financial damage have I done myself here? As opposed to just renting or even better, buying at the right price. So I guess that is where Lightstone is just so important.

Hayley Ivins-Downes: So important. I think it’s really – once you purchase a property and at the end of the day we do need to live somewhere – but also once you make that decision in terms of purchasing the property, just understand also in terms of the growth of the area, in terms of where the properties around you are actually growing in value, are you investing in the property in the right way? So if you’re going to be spending money, is it the right investment that you’re doing? Because at the end of the day, five years down the line, 10 years down the line, will you get some level of return on your property?

And I think we’ll discuss further down in the podcast, but you’ll see that in many areas, property is not the greatest investment from a short-term to medium-term at the moment. We really need to be astute and understand where we’re actually investing and what property we’re purchasing.

The Finance Ghost: Yeah, I will beat this drum all day. I absolutely agree with you. You’ve got to buy a property for the right reasons. The property you live in – there are a lot of good reasons to buy the place you’re going to live in for a long time, I’ve run a lot of the numbers myself, what annual growth you need to see in properties to make it make sense over a 7-to-10-year holding period.

Because that’s the other thing people say: “This is my forever home.” Forever is a really, really long time – people’s jobs change, their careers change, their spouses sometimes change, their kids move school, things happen and so if you overpay – and I think a big part of the problem is obviously just the costs on the way in and on the way out, transfer duty, etc. is so onerous that you can’t just – it’s almost like having a kid, you can’t put it back, you can’t go and buy a property and then 12 months later say, oh dear, I can’t own this thing anymore, let me get out of it. You’re going to take a massive, massive bath.

And the problem is it’s going to happen on an asset that is worth millions because it’s a very over-leveraged position. It’s like going and buying shares in a company, borrowing money from the bank and then not caring about the valuation. You would never do that. So why do people do it with property?

Hayley Ivins-Downes: No, exactly. Exactly! Anecdotally, just to share with everybody. We used to live in a suburb in Johannesburg and we purchased the property 10 years ago or 12 years ago and we paid a price…

The Finance Ghost: …oh, my condolences. I know where this story ends. It can’t be good.

Hayley Ivins-Downes: No, we sold it two years ago to move. We made a loss on that property.

The Finance Ghost: Yeah.

Hayley Ivins-Downes: We got less for that property than what we had paid!

The Finance Ghost: Sho, never mind inflation.

Hayley Ivins-Downes: No, never mind inflation. So I think it becomes really important just to keep your head up when you’re buying a property and not let the emotions run too much. Be aware of the area that you’re buying into because areas can decay and that also obviously affects your investment. So yes, all of these factors play a really important part.

The Finance Ghost: No, they really do. I mean, the last maybe anecdotal piece and then we can dig into some of the data that you’ve got at Lightstone about property – I think we’ve really landed the point around how important this is.

So I did my articles in a banking environment, which means I had access to staff rates on a home loan. And conventional wisdom, certainly from my parents’ generation, was always: don’t pay someone else’s bond! I mean, how many times have you heard that? Every time you pay rent, you’re paying off someone else’s bond? Pay off, just every payment is one more brick. You have heard all this before.

I naively in my articles was like, well, I have got access to this incredible bank rate, let me buy this little apartment in Joburg, and I came out okayish but definitely down versus if I had just rented. Without a doubt, I absolutely should have just rented. There is no reason on earth why I should have bought that property at the age I bought it when there was so much uncertainty over where my career would take me. There were no kids that needed a stable environment. It was an absolutely nonsensical decision with the benefit of hindsight.

I always encourage people: property can be the best decision you ever make and also the worst decision you ever make. It’s not like pressing the “buy” button because you feel like some shares in Sasol, you can get out of those pretty easily. It’s not the same in property.

Hayley Ivins-Downes: No, no. Do the numbers, before you make a decision.

The Finance Ghost: So let’s do some numbers because I think this is what we’re really here for is to understand what you’ve got in the data. I think one of the big South African talking points obviously of the past decade, has been the shift of wealth. You’ve talked about it now from Gauteng to effectively the Western Cape. I think that’s where most of it has gone. Another big talking point has been something like how vulnerable the Eastern Cape economy has actually been. And of course the beauty of property data is this is one of the ways you can just see it unemotively. Take out all the politics, take out people shouting at each other, property prices, willing buyers, willing sellers en masse dealing with having to take a view on somewhere in the ground. There’s no better measure than that.

Hayley Ivins-Downes: Yeah.

The Finance Ghost: So based on that, I’m very keen to see what stats and what trends you might have around that whole shifting-of-wealth-around-the-provinces point.

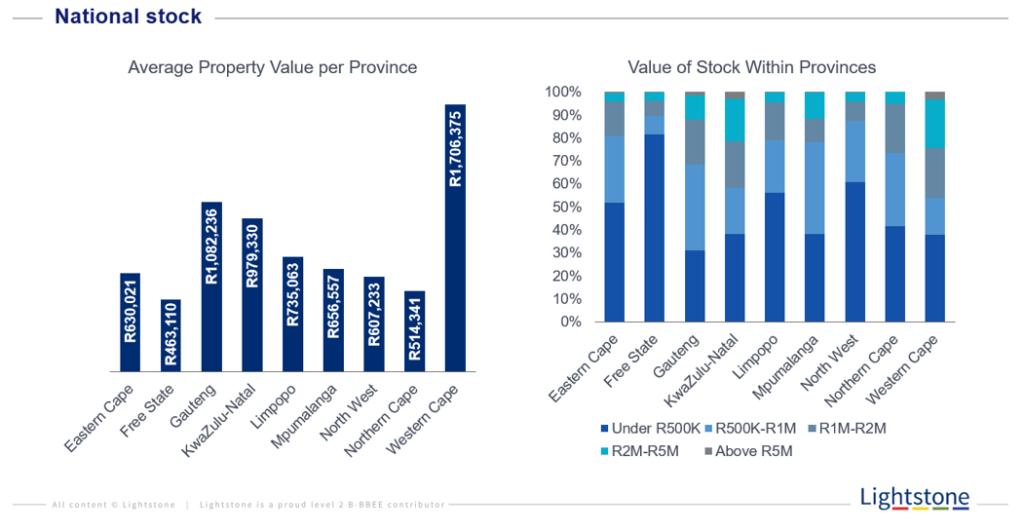

Hayley Ivins-Downes: Great. I think let’s start – probably good just to understand the total value that we’re talking around. If we had to look at the full property industry in South Africa, we’ve obviously divided that into residential and non-res, and your residential component basically makes up 85% of that. Total number of property stock: 8.55 million, just to give a view in terms of the legally owned property. And looking then at the value, total value of R13.5 trillion and of that, 54% in residential.

If we start now trying to understand what’s actually been happening in terms of the market and how it’s been shifting. So it’s been really interesting just to see specifically after Covid – but if I just do a little bit of a dig in terms of where the property market value has shifted, I actually managed to find an older version – 2015 – in terms of where we kind of showed the shift. In 2015, Gauteng was basically sitting with 38.4% of the value. Western Cape was sitting with 26.8% of the value. Third one, always coming in third is your KZN, and that was sitting at 12.3% of the value. And then I’ll get into Eastern Cape a little bit further on.

But if we just bear in mind the differences specifically between Gauteng and Western Cape. Up until now, what we’re saying now, 2025, basically Gauteng is now sitting at 36.9% of the value, so basically a drop of 2%. Western Cape has jumped up to 30% of the value so climbed 3.5% / 4% of value. And if you think about the value, that percentage of the R13 trillion, it’s a big number.

If we start looking at where the big difference started to happen, it was really post-Covid. So 2020, what we saw was interest rates dropped, an all-time low in 50 years, so it was really a big drive towards buying your property. It was certainly a buyer’s market – owning your own property as opposed to renting. And we saw this shift starting to happen and we saw 2020, I mean Gauteng was sitting at 38%, Western Cape had already started jumping up to 28% and then it just started increasing. We started to obviously see that shift – and we’ll get into more detail around semigration further on – but we’ve definitely seen the shift of value move definitely more down to the Western Cape.

Gauteng is still sitting at the top in terms of value, but Western Cape has certainly started catching up. Gauteng dropping.

The interesting component of KZN is it really is flat. There’s been hardly any movement. If we look 10 years ago it was 12.3%, it’s now 12.15%. So really tiny in terms of the shift.

The Finance Ghost: It really is Gauteng to Western Cape. I mean that’s what it’s done, right? It’s incredible.

Hayley Ivins-Downes: It is, definitely the biggest shift. And I think just linking into that, we obviously saw the shift of the ability to be able to work anywhere. So you didn’t need to go into the office. There was definitely a phase where that was happening. And so people used the opportunity to really move where they felt they wanted a better lifestyle or the fact that they could have better experiences. And obviously, the biggest view is Western Cape is running better from a municipal / provincial angle, so that’s also an interesting conversation on its own.

And then if we drop into the Eastern Cape, so the Eastern Cape economy has really been struggling. And I mean, if we go back 10 years, the value of Eastern Cape was sitting at 6.4% of the value. It really is now 6.29%. So it’s actually been declining in terms of what’s happening in the Eastern Cape. And it’s almost like a bit of the forgotten province and yet the potential there is huge.

Anecdotally, I was just on a hike on the Wild Coast, and I just think the potential for that area is so big, specifically from a tourism point of view to lift up that area. But we’ve definitely seen on the property side, that there’s been a bit of a slide on the value side of it. Even on the volume in terms of activity and transactions, also a bit of a drop. So, yeah, it’s definitely been the one that’s stood out as the drop that we’re seeing. It’s been interesting just to see the differences in the provinces.

The Finance Ghost: I mean, there’s a lot of interesting stuff to unpack there. In some ways, it’s actually not as big a shift as maybe some people might have expected to hear, because everything you get fed is obviously cost of living, cost of living, but of course, the cost of living comes through in a slightly tweaked metric, which is to compare the value proportion in a province to the volume of properties, because you get so much less for your money in the Western Cape.

Obviously I still have friends in Joburg and we’ll sometimes just laugh about – not laugh, but you just say, like, what is this house actually worth? And it’s this fantastic home in Joburg for a couple of million rand. And in Cape Town you are getting, if you are lucky, a complex – you know, you’re sharing walls with people for that sort of price. Joburg, you’re leaving behind a whole standalone story with a garden and a pool and a braai and three garages and the whole shebang. So it’s incredible.

I remember when I was in high school and I would get my parents to sometimes take a detour because I used to love going through the old areas of Joburg, certainly never grew up in them, like Westcliff, Houghton – just absolutely stunning. I looked the other day for fun at houses in Westcliff and what they’re worth now and I remember what they were changing hands for 15, 20 years ago. And it is just horrific! Look, people who owned Westcliff houses at that time, I don’t think that they care too much to be super honest about where the value went, they’ll be okay, but still no one wants to see their houses go down in value. That’s the reality. And it’s when you look at that top-tier property band that I think the Joburg / Western Cape difference becomes so stark. It’s amazing actually because I mean the stat is Western Cape is 30% of the value of South African property. But what percentage is it in terms of volumes?

Hayley Ivins-Downes: So volume wise, also quite interesting, it is 18% of the volumes compared to Johannesburg of 34%.

The Finance Ghost: Yeah. So that shows.

Hayley Ivins-Downes: It’s a big jump in volume compared to value.

The Finance Ghost: Massively. And that makes sense.

Hayley Ivins-Downes: That leads to it, it leans into what you’re saying. Yeah, we’ve seen the super luxury areas of Johannesburg take quite a knock in terms of property and what sellers are actually getting for their properties.

The Finance Ghost: Yeah, absolutely. And the other interesting thing in everything you were talking about there was, I think you made a comment that during the pandemic it was quite a buyer’s market because obviously you could get access to finance. So of course, the contrarian investor in me flicks it around and goes, well, that makes it a seller’s market! And the buyer’s market is when I can walk in because there’s no one else who can buy it. But because I bided my time and I can therefore get the debt and I’ve got the deposit – and that’s the way to think, you’ve got to almost think countercyclically if you want to make money in property. It’s just like buying stocks. Almost exactly like buying stocks. You’ve really got to think that stuff through, in a big way, actually!