African Rainbow Minerals released a trading statement for the six months to December 2025. This was triggered by the move in earnings per share, which jumped by between 65% and 75% thanks to the profit on disposal of Sakura and a gain on remeasurement of the 50% in Nkomati Mine.

But what the market really cares about is HEPS, which increased by between 5% and 15% (not enough to trigger a trading statement). That suggests 10% at the mid-point, or just enough to be considered double-digit growth.

African Rainbow Minerals has various underlying interests, with PGMs as the highlight in this period. Investors will have to wait for 6th March to see how underlying operations performed.

Altron gives more details on a strong performance (JSE: AEL)

They are focusing on annuity opportunities that have higher margins

Altron believes that the year ending February 2026 marks the end of its “Accelerated Growth” strategy. They are now in “Transformative Growth” mode. These concepts always smell strongly of Eau de Management Consultant, but they are important for getting internal alignment in organisations that are going through change. Managing large groups of people who have different incentives isn’t easy.

Altron’s efforts are paying off though. Earlier this month, they released a trading statement that flagged growth in HEPS from continuing operations of more than 30%. In a voluntary operational update, they’ve given more details on how they got there.

It’s worth noting that HEPS from continuing operations for the first half of the year was up 22%, so they came into the second half with great momentum.

It’s also good to note that the discontinued operation is Altron Nexus, which was sold on 1 August 2025.

Double-digit EBITDA growth certainly helps, as does the low-to-mid-teens growth rate in operating profit (if you exclude the change in Netstar’s depreciation policy that distorts comparability).

The Platforms segment is doing the heavy lifting, with 45% of group revenue and around 90% of EBITDA and operating profit. This is clearly where you’ll find the best margins and a number of annuitised revenue streams.

Within Platforms, Netstar’s growth (mid-to-high teens EBITDA, and high-teens operating profit excluding the depreciation change) has been driven mainly by the South African business, as Australia’s recovery has been slower than anticipated. Altron FinTech is also in Platforms, achieving improving margins and high-twenties operating profit growth. Altron HealthTech, the third pillar in Platforms, achieved high-teens operating profit growth.

In IT Services, they struggled with a drop in revenue. The segment also clearly runs at a much lower margin. Altron Digital seems to be the biggest headache, but at least it was profitable in December 2025 and January 2026 after cost-cutting measures. Altron Security achieved double-digit revenue growth and operating profit growth in line with the interim performance. Altron Document Solutions achieved more than 30% growth in operating profit for the year, so that’s an example of where turnaround strategies can work.

Overall, annuity-based income is up to 65% of total revenue (both segments have this type of income). This gives great visibility on cash flow and helps with the valuation as well.

Double-digit growth in net operating income at NEPI Rockcastle (JSE: NRP)

They’ve hit the top end of revised guidance

NEPI Rockcastle released results for the year ended December 2025. Distributable earnings increased 6.7% and net operating income was up 11.2%. Tenant turnover across the Central and Eastern European portfolio increased by 3.6% on a like-for-like basis, while retail occupancies were up at 98.8%.

As you can see, there’s a good story to tell here – at least if you own dominant shopping centres in the region.

On a per-share basis, the growth isn’t quite as exciting. Distributable earnings per share increased by 3.1% for the year. When you keep issuing new shares, this is what happens.

Another important metric is like-for-like net operating income growth, which excludes acquisitions completed in 2024. Growth of 4.4% on this basis gives you a good idea of why distributable earnings per share growth was in the low single digits.

The fund welcomes Marek Noetzel as the new CEO on 1 April 2026. He takes the reins of an iconic property fund with a loan-to-value ratio of just 32.8%, below the 35% strategic threshold. That sounds to me like a good opportunity to hit the ground running.

Octodec will offload Killarney Mall for almost R400 million (JSE: OCT)

This is only slightly below the book value

Hot on the heels of a general operating update that dealt with Octodec’s portfolio and many of the unique challenges that they need to manage on a daily basis, the company has now announced that they have a buyer for Killarney Mall. With a relatively high vacancy rate, the new owner (AJPH Property) will have some work to do.

For Octodec shareholders, this means an exit from this asset at a price of R397.5 million. It remains subject to adjustments for working capital. This price is only slightly below the valuation of R407.6 million that was performed with an effective date of 31 August 2025.

Selling at a premium to book is obviously preferred, but companies need to sometimes get out and move on to new assets. It looks like Octodec is making a sensible decision here, with the proceeds being used to reduce debt and deploy into future projects.

RCL has given tighter guidance for a tough year (JSE: RCL)

As previously noted by the company, the pressure is in sugar

At the start of this month, RCL released a trading statement for the six months to December 2025. It noted an unpleasant drop in HEPS from total operations of at least 25% (or a decrease of at least 27.4 cents).

Most of this move (at least 21.8 cents) was thanks to the troubles in the sugar industry, with the stronger rand and ineffective sugar tariffs placing the local industry under even more strain. An additional issue for the year-on-year HEPS comparability is that there was a partial recovery of the sugar levy in the prior period. In more positive news, the initial trading statement noted that Groceries and Baking were expected to report improved underlying profitability.

We now have a further trading statement that gives a tighter range. HEPS from total operations is now expected to drop by between 29.2% and 32.1%.

Kudos to the company for keeping investors informed – an initial trading statement and subsequent further trading statement shows commitment to the market. It’s just a pity that the numbers have gone the wrong way.

Redefine’s pre-close update is full of nuggets (JSE: RDF)

Perhaps the most interesting is that large retail centres are doing well

Redefine Properties released a pre-close update dealing with the six months to February 2026. There’s a bullish narrative overall, with the company believing that they are in the strongest position they’ve been in during the post-pandemic period. Property fundamentals are showing positive signs and the balance sheet is in good shape, so they can take advantage of the opportunities out there.

But what do the numbers say? Well, in South Africa, negative rental reversions of -6.3% are worse than -5.2% in FY25. Renewal success rates are up though, so perhaps they are being slightly less strict on price in order to get the leases across the line.

The weighted average lease escalation of 6.4% is well above inflation in South Africa, although one must remember that property funds don’t deal with the CPI basket. They face municipal charges, as well as security, energy and other costs that tend to run above CPI.

Speaking of energy, Redefine’s solar projects generated 13.1% of the total energy demand in this period. They’ve invested heavily across the retail, office and industrial portfolios.

In the retail portfolio, Redefine notes that large-format centres have recovered. Turnover growth is now in line with convenience centres. Positive reversions in the retail portfolio of 2.4% were ahead of 1.0% in FY25. This is probably the bright spot in the update.

The office portfolio is where things got nasty. Reversions were -16.8%, even worse than -12.9% in FY25. This can be very lumpy though, with Redefine expecting it to moderate to -11% by the end of the year. Interestingly, of the 95 renewals in the period, 28 had negative reversions and 53 had positive reversions. The large tenants have the best bargaining power, as you might expect.

The industrial portfolio achieved positive renewals of 3.7%, up from 0.8% in FY25. This has been a solidly performing property asset class in South Africa.

In Poland (the EPP portfolio), like-for-like footfall increased by 0.8% and like-for-like turnover was up just 0.5%. Retail occupancies were steady at 98.2%, while office fell from 84.2% to 82.9%. At least rental reversions were up to 1.9% vs. 0.4% in FY25. In the ELI portfolio in Poland, which has the logistics assets, rental reversions were 1.8% – significantly lower than 6.9% in FY25.

They are looking to dispose of a number of assets in Poland as part of a broader plan to simplify the joint ventures in that country. They are also looking to build a strong self-storage platform in the country, taking advantage of trends like urbanisation and eCommerce.

Looking at the balance sheet, the group weighted average cost of debt has been maintained at 7.0%. There are various refinancing negotiations underway, with one of the primary goals being to address the maturity concentration risk in FY28. The loan-to-value (LTV) of 41.4% (calculated in line with the covenant of 50%) is in a healthy space. The see-through LTV of 47.2% is in line with what we’ve seen in recent years.

Overall, for FY26, they think that the upper end of the 4% – 6% guidance for growth in distributable income per share is in play.

Super Group pulled off an exceptional interim period (JSE: SPG)

Leaning into Chinese and Indian cars has worked

If you’re going to panic, panic quickly. This is some of the best advice you can ever be given. Instead of clinging to a sinking ship, get yourself onto something else as quickly as possible.

Super Group is proof of this, with the share price closing 5.4% higher thanks to the group achieving great interim numbers. Revenue was up 7% and operating profit increased by 8.7% as margins improved. By the time you reach HEPS from continuing operations, you find a fantastic outcome of 28% growth.

Cash generated from operations increased by 39.4%, so these results aren’t just pretty on paper. They are pretty in the bank account as well.

To understand the numbers, we need to dig into the segments.

The Supply Chain segment grew revenue by 6.3% and operating profit by 14.9%. This is the largest segment in the group, with operating profit of R695 million. The highlight within the segment was surely Ader in Spain, with revenue growth of 17.2% and EBITDA up by a rather ridiculous 225.6%. This is what can happen in low margin businesses when revenue heads in the right direction. Another useful outcome in this segment is that the cross-border transport business achievied a 90% reduction in trading losses.

Fleet Africa grew revenue by 15.3%, but operating profit could only manage a 4.2% increase due to pressure on margins from lower rental volumes. Operating profit was R156 million in this period.

Dealerships SA certainly deserves a mention, with the company leaning into Chinese and Indian brands for growth. 29.7% of new vehicle sales volumes are attributable to these brands, as Super Group’s volumes in this space more than doubled year-on-year. The profile of cars on our roads is changing dramatically. Operating profit improved from R193 million to R209 million, an excellent change in trajectory.

Dealerships UK managed to achieve a decent performance in Ford, while also taking advantage of the new Chinese brands. Operating profit growth jumped by 50.4% to R62 million thanks to the initiatives in this space. But I must point out that operating profit is at roughly half the levels we saw in interim 2024.

The discontinued operations still have some tough areas, like UK automotive logistics that is exposed to the broader automotive manufacturing environment in the UK and Europe (which is in enormous trouble). They are also looking to sell the UK KIA dealerships, having shut Hyundai and Suzuki. I’m old enough to remember when the new South Korean brands (KIA and Hyundai) were the disruptors rather than the disruptees.

Kudos to the group – they changed what needed to be changed. There’s a lesson in here for all of us about the importance of not ignoring disruption.

Give me your views on where the automotive sector is headed:

Nibbles:

Director dealings:

An associate of a director of Dis-Chem (JSE:DCP) bought shares worth R1.45 million.

A director of a major subsidiary of Stefanutti Stocks (JSE: SSU) bought shares worth nearly R45k.

Incoming CEO Magen Naidoo has bought another R9.6k worth of shares in Mantengu (JSE: MTU).

The Competition Commission has given Transpaco (JSE: TPC) a bloody nose. The regulator has prohibited the acquisition of Premier Plastics, a deal that was announced on 6 November 2025. Premier produces retail plastic carrier bags, so there’s immense overlap with Transpaco’s existing business. This is why the regulator wasn’t so keen on this R128 million transaction. Transpaco is considering its options based on the commission’s decision.

Reunert (JSE: RLO) announced that incoming CEO Anthonie de Beer will be appointed as an executive director from 1 March 2026.

Marshall Monteagle (JSE: MMP) concluded a rights offer back in November 2025 for $10.7 million. The raise was significantly oversubscribed, leaving many unfufilled excess applications. The company then used its general authority to issue shares, in order to give those applicants the opportunity to apply for new shares. This has led to an additional issue of shares worth $2 million.

Numeral(JSE: XII) is trying to raise R100 million (a large number). With only a partial underwrite of roughly R32 million, they are looking to close a huge gap. I’m not surprised to see that the closing date for this offer has been extended all the way out to 31 August 2026. This isn’t the kind of thing you see when people are queueing up to invest.

Blu Label (JSE: BLU) announced that Lindsay Ralphs, who previously served as the CEO of Bidvest (JSE: BVT), will be appointed as independent director and chairman designate with effect from 24 February 2026.

In case you were holding your breath, which I’m sure you weren’t, Trustco (JSE: TTO) has renewed the cautionary announcement regarding the potential delisting from the JSE. This is based on their ongoing assessment of the Simplified Listings Requirements.

Profits and cash flows look better at Aveng (JSE: AEG)

The order book has softened though

In construction, due to the immense pain that a bad contract can inflict, it’s possible to see profits improve substantially despite a drop in revenue. In fact, revenue can be a poor predictor of profitability, which is why I completely avoid investing in this sector.

We see this come through in Aveng’s results for the six months to December 2025. They reflect a drop in revenue from R16.6 billion to R14.2 billion, yet operating earnings swung beautifully from a loss of R356 million to profit of R107 million.

Even though infrastructure markets have softened in Australia and New Zealand, gross margin improved from 2.7% to 5.6% as the quality and implementation of projects improved. There’s also the substantial impact of the Jurong Region Line (J108) project in Southeast Asia and the Kidston Pumped Storage Hypro project in Australia, with combined losses of A$20.2 million in this period vs. A$76.7 million in the prior period.

Like I said – revenue is a poor predictor of profitability!

Aveng has recognised the forecast costs to complete those projects in this period, but the associated cash flows will be in the second half of FY26 and in FY27. It’s worth noting that cash on hand improved from R3.1 billion to R3.4 billion in this period.

Headline earnings came in at R4 million. That might not sound like much, but the comparable period was a loss of R399 million. At least they are back in the green, albeit only just.

There are other difficult contracts in the group as well, like the Tshipi project. Aveng is negotiating commercial settlements with various clients, with David Simpson appointed as the interim group CEO to focus on commercial resolution and delivery of underperforming projects. At the Moolmans business, Pieter van Greunen has been appointed as managing director, with the resolution of the Tshipi contract as one of the key focus areas.

The group heads into the second half of the financial year with work in hand of R38.6 billion, up from R37.5 billion in the first half. But it seems like success depends as much on resolving the legacy projects as it does on the new stuff.

And as a reminder, after a lot of work went into figuring out what to do with McConnell Dowell, Aveng has decided to keep that that business for now.

Clientèle’s numbers are complicated (JSE: CLI)

But they do seem to be heading in the right direction

Clientèle has released a trading statement for the six months to December 2025. Based on the JSE rules, the release of such an announcement immediately tells you that the numbers differ by at least 20% vs. the prior period. In this case, the percentage move is a lot bigger!

But we need to deal with some issues that are impacting the comparability of numbers.

One of the major distortions in the numbers is the bargain purchase gain of over R400 million related to the acquisition of 1Life. This is excluded from HEPS, which gives me a good opportunity to remind you that HEPS is the number that the market uses to actually judge performance.

Here comes another distortion that does impact HEPS though: a change to the application of IFRS 17 that led to a restatement of the interim results for the six months to December 2024. That may sound like a long time ago, but remember that this impacts the base period of comparison for the six months to December 2025.

But perhaps the biggest distortion of all is that Emerald Life has been consolidated for the first time in the latest numbers. This has resulted in HEPS increasing by between 92% and 112% vs. the previously reported numbers, a sizable jump that is essentially a doubling of HEPS at the midpoint of that range. After the base period was restated for IFRS 17, the expected increase in HEPS is between 43% and 63%.

There are a lot of adjustments to consider here, but the direction of travel is up.

Gemfields flags decent pricing for fine-quality rubies (JSE: GML)

But the lower-quality stuff is under pressure

Gemfields announced the results of a mixed-quality rough ruby auction held from 9th to 20th February. This is the auction that was deferred from December 2025. The auctions are always difficult to use to establish a trend, as the quality of the stones varies from one auction to the next.

In this case, they achieved auction revenue of $53 million, having sold 90% of the lots offered for sale and 88% of the carats offered for sale. The average price was $279 per carat.

Although fine-quality rubies attracted decent prices, management has indicated that other qualities were more “muted” due to the uptick in product on the market from illegal mining networks, along with weaker demand from China. The products may be beautiful, but it’s still a tough space to operate in.

Notably, this is the first auction that includes material from MRM’s second processing plant.

If we look at previous auctions over the past few years, the price per carat at this auction is the lowest that we’ve seen. Although Gemfields notes that this is because lower quality rubies weren’t offered at those auctions, the reality is that pressure on the average price per carat can’t be good news for shareholders. I doubt it’s much cheaper to extract a lower quality ruby vs. a high quality ruby, so the price per carat is still relevant to profitability.

Mr Price is ready to close the NKD deal (JSE: MRP)

Based on the lack of share price recovery, the market still doesn’t like it

A chart of the Mr Price share price makes it depressingly easy to see exactly when they announced the NKD acquisition. You’re looking for the precipitous drop in late 2025 that looks like someone threw the share price off the side of a cliff:

You may also note that the share price hasn’t really staged a recovery yet. Some efforts earlier this year to address the anger in the market stemmed the bleeding, at least, but there’s little doubt that the market is still angry about the deal.

Mr Price has gone ahead with the deal anyway, with the latest update being that all regulatory conditions have now been fulfilled. The deal is therefore subject only to the money actually changing hands. They are targeting a scheduled closing date of 31 March 2026.

In yet another effort to try to get the market on the same page as management here, there is an investor presentation scheduled for 17 March. I’m not sure how they will try to tell a better story that time around, but perhaps some pleasantly surprising nuggets will be shared.

Nedbank secures an important regulatory win in the NCBA deal (JSE: NED)

They have received an exemption from making a mandatory offer

In January this year, Nedbank announced an intention to acquire a 66% stake in NCBA Group, a major financial services operation in East Africa. Nedbank is well behind its peers when it comes to the African growth story, so this feels a bit like a game of catch-up.

To pay for the deal, Nedbank is using 20% cash and 80% new shares in Nedbank. The deal is worth a substantial R13.9 billion, so it’s not surprising that they can’t do a transaction of that size purely in cash.

An important component of the deal is that the remaining 34% of shares in NCBA will continue to trade on the Nairobi Securities Exchange. This makes the deal a manageable size for Nedbank, while giving them control via the 66% stake. Companies like to buy control, but not necessarily 100% of the earnings.

But in the event of needing to do a mandatory offer, Nedbank was prepared to switch the structure to an offer for 100% of the shares. This tells me that they want either 66% or 100%, but preferably nothing inbetween.

They don’t need to follow this route though, as the takeover law regulator in Kenya has provided the exemption from the mandatory offer, so 66% it shall be.

Another element to the transaction is that this is a pro-rata offer to shareholders, which also allows for excess applications for those who want to sell more than 66% of their shares to Nedbank (to make up for others who may not want to sell). Nedbank has received irrevocable undertakings to accept the offer from holders of 77.54% of NCBA shares in issue.

Octodec affirms guidance – but this portfolio sounds like hard work to manage (JSE: OCT)

Inner-city properties come with a host of challenges

Octodec might begin with a bullish narrative in its pre-close update for the interim period, but it quickly becomes clear that managing their property portfolio is anything but easy.

In an update that covers the five months from 1 September 2025 to 31 January 2026, the Johannesburg residential portfolio is one of the more obvious challenges. Octodec highlights the pressure on landlords to provide alternative solutions to failing council service delivery and infrastructure. Tenant affordability is another challenge. Nothing about this sounds particularly encouraging for rental yields.

On the plus side, at least the retail portfolio around Lilian Ngoyi Street has improved after the damage from the gas explosion was finally fixed. The Joburg CBD really is an example of how to play the property game on hard mode.

The overall retail shopping centre portfolio had a vacancy rate of just 0.2% as at the end of January 2026, which is better than the 0.5% reported for August 2025. The ugly duckling is Killarney Mall, currently held for sale with a vacancy rate of 17.7% at the end of January (in line with August). The launch of a Regus shared-office space at Killarney is expected to improve footfall.

The collection rate is largely okay, although they do highlight that one of their tenants is in business rescue.

Despite the portfolio being a tricky thing to manage, Octodec has plenty of experience in this space and the risks are well diversified. This has enabled them to raise debt at reasonable rates, with refinancing of maturing debt on improved commercial terms also being possible.

It also make a big difference that the loan-to-value ratio is on the right side of 40%, with disposals of nine non-core properties during the five months (for a total of R81.2 million at a 3.7% premium to book value) helping to achieve this outcome. Unutilised facilities increased from R675 million to R1 billion, so they have decent headroom on the balance sheet.

The goal is to get to 35% in the long term, achieved through further disposals of smaller properties in the portfolio. They also need to fund various capex projects of course, including the ongoing Gezina City project.

The weighted average cost of debt is down to 8.8% at the end of January 2026, an improvement from 9.1% in August 2025. This is thanks to the refinancing activity, as well as the lower overall interest rates.

Guidance for the year ending August 2026 has been affirmed, with expected growth in the distribution per share of between 0% and 4%. That’s not much, but at least it’s in the green.

Earnings fall at Sasol, but at least free cash flow is up (JSE: SOL)

Growth remains hard to come by

Sasol’s share price is up 62% in the past year. But for the six months to December, HEPS has fallen by 34%. Markets can be confusing things, especially for the likes of Sasol where the valuation is low and the the share price performance will depend on just how much bad news actually materialises.

With flat turnover (despite a 3% increase in volumes), Sasol’s adjusted EBITDA fell by 12%. Production volumes at Secunda Operations were up 10% and this no doubt informed some of the share price action, but the macro environment is still working against Sasol. The average rand price of oil fell 17%. Even the price of chemicals (in US dollar per ton) dropped, with the rand strength against the dollar putting further pressure on the translation of the international chemical results.

Capital expenditure fell by 43% to R8.5 billion, so free cash flow generation actually improved dramatically thanks to this. Free cash flow for the period was R0.8 billion vs. -R1.3 billion in the comparable period.

On a market cap of R89 billion though, R0.8 billion in free cash flow isn’t exactly an exciting yield (even if you annualise it).

Here’s the real kicker though: this is actually the first positive interim free cash flow for four years. When you’re used to dry bread, a piece of toast with butter can feel gourmet. I just wish that the butter was coming from improved cash flow from operations, rather than a drop in capex.

With net debt to adjusted EBITDA of 1.6x, the balance sheet is in reasonable shape. EBITDA can change quickly though, so this ratio is always at risk. Debt was brought down from R103.3 billion to R93.5 billion, so that’s an encouraging sign.

In terms of updated guidance, the dip in capex is expected to stick. They reckon that capex for the year will be R2 billion lower than previous guidance of R24 billion – R26 billion. Alas, the International Chemicals adjusted EBITDA is revised lower to between $375 million and $450 million, well off the previous level of $450 million to $550 million. This is a decrease in adjusted EBITDA margin, to between 8% and 10% vs. previous guidance of 10% to 13%.

Will they ever recover from the catastrophic SAP implementation?

SPAR is such a good example of how the success of your local franchisee can be a terrible indication of the health of the franchisor. We’ve all shopped at a SPAR that we know and love, with a great deli and a product assortment that makes it unique in the local community. Yet for all the effort that goes into making that happen by the franchisee, we have a scenario where the holding company performance looks like something revolting that got cleaned out of a grimy corner of the storeroom.

Part of the problem is that the franchisees aren’t required to buy everything from the franchisor. In other words, SPAR as a wholesaler must compete with other suppliers to the stores. You would imagine that this is a no-brainer, as SPAR is surely the most efficient and obvious supplier to the stores. After all, they send one truck from the distribution centre that has everything on it.

Right? Well…

What happens when the distribution centre implements a new system in a way that is disastrous even by oh-no-this-retailer-is-going-with-SAP standards? And what happens when they do it in their traditionally-strongest regional market?

Also, what happens if that same company runs around in Europe dealing with problems elsewhere, instead of focusing on the home market?

Here’s what happens:

I actually have a small speculative position here, based on a thesis around believing that it would be difficult to fully destroy a brand that is part of the fabric of community retail in South Africa. I’m now wondering about whether it is so difficult after all.

CEO Angelo Swartz has decided to throw in the towel. He’s only 43 years old based on the SPAR website, yet this turnaround managed to burn him (and his family) out. That tells you something about how bad it actually is.

Reeza Isaacs is taking the top job, hopefully bringing some stability to the story. Megan Pydigadu moves from COO to CFO to replace Isaacs. And based on the latest trading update at the company, they have a lot of work to do.

For the 18 weeks to 30 January 2026, SPAR’s wholesale turnover from continuing operations was up just 2.1%. To make it even worse, their gross margin fell, which means they could only achieve this number through highly promotional activity to drive sales.

SPAR Southern Africa? Growth of just 0.9% – a shocker. Within that, Grocery & Liquor was just 0.8% (exceptionally poor), Build it fell 2.4% (also poor, but a tricky business) and SPAR Health was up 23.0%. Perhaps all the accountants looking at these numbers were at least buying their headache tablets internally.

In Ireland, growth was 3.1% in local currency and 6.1% in rand. This helps bring the group number up to the 2.1% noted above. Yay.

With internal selling price inflation of 2.6% in Grocery & Liquor, they suffered a negative move in volumes despite all the promotional activity. Although they try and make things sound better by referring to 2.3% overall growth in November to January (i.e. excluding a soft October that dragged them down to 0.8%), even the “better” number is actually very weak.

Another example of clutching at straws is to describe the high-income segment as showing a “modest recovery” with like-for-like growth of 1.6%. Modest, indeed. Compare this to Checkers and Woolworths Food, and you’ll quickly see just how bad SPAR is.

Retailer loyalty is the way they measure the extent to which franchisees procure from the wholesaler. Loyalty in KZN is at just 71.5% vs. 84% for the rest of South Africa, reflecting the immense hangover of the SAP implementation that left retailers stranded for stock. There’s even litigation around this, with claims related to the SAP implementation and how it affected the claimant. The initial claim was R5 million and the litigation “significantly exceeds” that amount. Other than the claimant and one other retailer, all KZN retailers have reached settlements with SPAR.

You can’t just stop a SAP process along the way. To get the full benefits, they need to finish the project. They talk about a risk-mitigated revised plan to finish the project.

My long-standing joke remains undefeated: Ernie Els is the only truly successful SAP implementation story.

The group has reiterated that they want to hire a Managing Director for the Grocery & Liquor business in South Africa. I’ll say it again: adding layers of management to the structure is not the answer.

And are they at least done with selling businesses in Europe? Not quite, with AWG in South-West England needing to be sold. I’m going to pull this pearler from the announcement, as it genuinely tells you everything you need to know about SPAR:

“Further, the Group does not anticipate needing to make a cash injection to effect the disposal.”

They are so accustomed to having to pay people to drag their rubbish away that they now need to specifically indicate to the market whether that will be happening again.

They talk about a transaction structure that has been “substantially agreed” for the AWG disposal. Let’s hope they can get it done quickly.

Somehow, against this backdrop, SPAR believes that they might be able to do share repurchases in the next financial year. Getting the authority from shareholders vs. actually being in a financial position to pull the trigger on share repurchases are two different things.

Overall, the company is now a steaming pile of you-know-what. I would’ve loved to buy the dip here, but I think it would be a safer bet to stick to the type that I’ll find in the chips aisle.

But what do you think? Do you believe they can restore SPAR to its former glory?

Nibbles:

Director dealings:

Despite all the positivity around Dis-Chem (JSE: DCP) (or perhaps because of it?), an associate of director Stanley Goetsch sold shares worth R11.2 million.

An associate of a director of 4Sight Holdings (JSE: 4SI) bought shares worth R724k.

Another day, another SENS announcement from ASP Isotopes (JSE: ISO) regarding US subsidiary Quantum Leap Energy. Except in this case, the update actually relates to a South African subsidiary of Quantum Leap Energy! Group structure aside, it relates to an agreement with the South African Nuclear Energy Corporation (Necsa) to collaborate, develop and produce High Assay Low Enriched Uranium (HALEU). This services contract builds on the previously announced memorandum of understanding between the parties. Necsa will provide facilities and infrastructure in Pelindaba, while Quantum Leap Energy will provide proprietary enrichment technology. The world’s energy needs are going through the roof right now thanks to AI data centre infrastructure and general industrial electrification, so ASP Isotopes and its subsidiaries are fully focused on addressing that opportunity.

Telemasters(JSE: TLM) released a trading statement for the six months to December 2025. They have flagged a increase of 94% in HEPS, taking it from 0.35 cents to 0.68 cents. Note: I said 0.68 cents, not R0.68. So although the share price is under R2, it’s still trading on an enormous Price/Earnings (P/E) multiple.

Louis Raubenheimer, son of Raubex (JSE: RBX) founder Koos Raubenheimer, has been appointed to the board of that company as an independent non-executive director. He has plenty of prior experience with the company, having held various roles from 1992 until 2022. His most recent role was running the Roads and Earthworks Division.

The talk in investment markets is that the AI “bubble” may soon burst. Nico Katzke, Head of Portfolio Solutions at Satrix, disagrees with these predictions, though he does caution investors about potential risks.

“In market terms, a bubble means irrational pricing,” he says. “It occurs when hype eclipses reason. Prices then reflect investors’ urgency to buy, as they fear they’ll miss out. This hype pushes prices even higher, reinforcing positive sentiment in a self-perpetuating loop.”

In other words, bubbles occur when asset prices far exceed their sustainable value. This happened with tulip prices in the 1600s (“tulip mania”) and tech stocks in the early 2000s (“dot-com” bubble). Some analysts believe it’s happening to artificial intelligence (AI) shares now.

Katzke is not convinced by that analysis. He points to the 2000 dot-com crash as a lesson from the past that informs the current market. “In the early 2000s, there were naysayers who wrote the obituary for a tech industry that – at the time – looked like it had died before it had even matured,” he says. “A few analysts were saying, ‘We told you so. This was all hype, all bubble, no substance.’ But hindsight shows us that the market was not irrational in valuing highly the companies that would ultimately benefit from widespread internet adoption.”

Instead, the dot-com crash was simply a case of not all tech companies becoming winners. There’s a lesson there for today’s AI companies and today’s investors.

“Markets tend to be remarkably resilient and efficient over time,” says Katze. “The dot-com crash simply preceded an era of enormous stock market growth – particularly in companies that succeeded in the Internet age. Were there failures? Of course. But after the stock market correction, many analysts pointed to the irrational behaviour of companies that were overly enthusiastic about building the internet’s infrastructure, including laying the same fragile undersea fibre-optic cables that have enabled our current era of global connectivity. In hindsight, we’ve come to rely on that infrastructure. And the technology is still here. After all, you’re likely reading this on the internet.”

The long-term market rebound that followed the dot-com bubble of the 2000s highlighted the importance of staying calm and avoiding panic selling. Stock markets truly are the only marketplace where customers flee when there’s a sale. Building long-term exposure to equity markets and remaining invested has been shown to deliver long-term value.

Katzke recommends adopting a cautious but open-minded approach to the current AI bull run. “Will there be pain from AI? More than likely. Some companies may disappoint. Others will fail entirely. Are valuations stretched today? I would incline to agree, but at the same time, I would point out that traditional accounting measures aren’t great at measuring the value of technology companies,” he says. “Even though markets will likely remain volatile for some time to come, investors should not forego long-term investment discipline due to short-term uncertainty.”

Like AI, other assets – such as cryptocurrencies, commodities and resource stocks today – also face “bubble” warnings. “It’s not helpful to label everything a bubble,” says Katzke. “All that does is create fear among investors, who then view those industries or stocks as being irrationally priced. This fear affects behaviour, and investors remain on the sidelines without a sober consideration of the long-term risk/reward trade-offs in investing in an asset class.”

Instead, he suggests taking a pragmatic, long-term view of the market. “AI stocks may look expensive today, based on fundamentals, but how relevant are those fundamentals?” he concludes. “Many of these companies are building the infrastructure for tomorrow’s AI-powered world. I would argue that building exposure to companies developing the infrastructure that will power future AI integration is still a sound investment. Here we like the larger, well-diversified technology indices such as the Nasdaq 100 as opposed to smaller, more niche and predominantly software exposed indices.”

Satrix consists of the following authorised Financial Services Providers: Satrix Managers (RF) (Pty) Ltd and Satrix Investments (Pty) Ltd. The information does not constitute financial advice. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Flat EBITDA at Anglo American and a nasty drop in HEPS (JSE: AGL)

Operating cash flow is a highlight, though

Anglo American released results for the year ended December 2025. It didn’t take them long in the announcement to mention copper and the Teck deal, although they didn’t actually refer to it as a “merger of equals” in the opening line!

With a major regulatory approval achieved at the end of 2025, they are making good progress in the Teck deal. Once completed, investors will have more than 70% exposure to copper in the enlarged Anglo group.

They could do with a boost, as underlying group EBITDA had a flat year in 2025, coming in at $6.4 billion vs. $6.3 billion in the prior year. This is despite $1.8 billion in run-rate cost savings that were delivered on schedule by the end of 2025. The “run-rate” reference means that the $1.8 billion may not be fully captured in the 2025 financials.

EBITDA margins were strong in the businesses that Anglo plans to keep, like copper at 49% and premium iron ore at 43%.

But despite this, group HEPS actually fell sharply from $0.72 to $0.39 per share.

The highlight was cash conversion in continuing operations of 107%, as they reduced working capital and unlocked cash to help reduce debt. Along with the proceeds of the sale of shares in Valterra Platinum (JSE: VAL), this reduced net debt from $10.6 billion to $8.6 billion.

De Beers remains an ugly story, with an impairment of $2.3 billion to the value of that asset. It will be a brave soul indeed who acquires De Beers and takes a risk on mined diamonds.

The sale of the nickel business is going through regulatory approvals, while the steelmaking coal business still has an uncertain future (while Anglo searches for a buyer).

Record free cash flow at AngloGold Ashanti (JSE: ANG)

The 2025 dividend is the highest in the company’s history

Are you bored of the record numbers coming through in the gold sector? Or are you invested in this sector and every additional update just feels like another pat on the back?

As you know by now, the gold price did really well in the past year and the gold mining houses have been printing cash. AngloGold has added its name to that celebratory list with the release of results for the year ended December 2025.

Free cash flow tripled to a record $2.9 billion. This magnificent outcome was thanks to strong cost control (total cash costs per ounce increased by 7%, mainly due to higher royalty payments) and a 16% boost in production to complement the higher gold prices.

Total dividends for the year were $1.8 billion, a new record. This represents 62% of free cash flow, which is higher than the typical payout of 50% of free cash flow. But this also shows you that management is retaining plenty of firepower, with capital expenditure having increased by 32% in 2025. Notably, sustaining capital expenditure was up 22%, while non-sustaining (or expansionary) capital expenditure increased by 62%.

They haven’t just been sitting back and enjoying the gold cycle. AngloGold has been busy with acquisitions and disposals, having invested heavily in areas like Nevada in the United States. They’ve let go of non-core assets in riskier markets like Côte d’Ivoire and Brazil.

Production guidance for 2026 is 2.8 million to 3.17 million ounces vs. the 2025 number of 3.1 million ounces. They also expect an 11% increase in the cash cost per ounce, with approximately half of the increase from royalty payments and the other half from inflation.

Dis-Chem accelerates to double-digit revenue growth (JSE: DCP)

They are focused on data and partnerships

Dis-Chem released a trading statement for the 24 weeks from 1 September 2025 to 16 February 2026. The market liked it, with the share price closing 3.9% higher on the day.

This is because Dis-Chem achieved group revenue growth of 10.1% in this 24-week period. To give that more context, the six months to August saw them achieve group revenue growth of 8.7%. An acceleration in growth is always welcomed by the market, with the second half of the year clearly going even better than the first half.

Retail revenue growth was 9.5% in this period vs. 8.3% in the interim period. An increase in the growth rate of 120 basis points is meaningful. Like-for-like revenue growth was 5.7% and volume growth was 5.0%, so there is minimal price inflation in these numbers.

If you dig deeper, the efforts of the “X, bigly labs” team at Dis-Chem seem to be paying off (despite having the most ridiculous name in history that sounds like a Musk-Trump concoction). With better data and a refreshed loyalty programme that was launched approximately 7 weeks into this period, they saw retail revenue in the 17-week period increase by 10.4%. This is encouraging exit velocity that shareholders will like.

The profits are what count though. Achieving better sales is great, but the rewards programme comes at a cost in the form of savings passed on to shoppers. Dis-Chem notes that customers enjoyed R410 million in savings over the 17 weeks. I will be interested to see what the impact on gross margin looks like, with the potential upside surprise being that supplier-funded deals often help to reduce the impact on the retail margins of these programmes.

For now though, Dis-Chem is happy to bank the market share gains. For the 12 weeks to 25 January 2026 (a period measured by NielsenIQ), they achieved volume growth of 8% vs. the market at 1.3%, taking market share across all categories up by 80 basis points.

They are also doing particularly well in areas like GLP-1 drugs, with pharmacy revenue up 13.7% for the 17 weeks under the new rewards programme. Aspen (JSE: APN) shareholders will certainly be interested in this level of GLP-1 adoption.

In the Wholesale business, revenue was up 15.7% in the 24-week period vs. 11.1% in the interim period to August. Sales to own retail stores were up 16.2% vs. 10.9% in the August period. The Local Choice pharmacies increased from 230 stores to 281 stores. Wherever you look, there’s an encouraging acceleration in the business.

This is a seriously impressive performance. A gap has now opened up between the Dis-Chem and Clicks (JSE: CLS) share prices:

Are we witnessing a rerating of Dis-Chem that will stick this time, relative to Clicks at least? Have your say in the poll below:

enX will sell the remaining 75% interest in West African International (JSE: ENX)

Trichem is exercising its option to own the entire thing

Back in March 2025, enX announced that Trichem would subscribe for a 25% stake in West African International (WAI). Trichem then had the option to sell their 25% stake back to enX (a put option), or to acquire the remaining 75% interest in WAI (a call option).

Trichem is clearly happy with the asset, having injected R107 million for the initial 25%. They’ve decided to go with the call option rather than the put option, which means they will acquire the remaining 75% in WAI from enX.

It’s a much bigger deal than you might think, as it triggers a s112 situation for enX. This is because the 75% stake represents the majority of the remaining assets in enX. This puts us into the territory of the Companies Act that is regulated by the Takeover Regulation Panel, hence the exercise of the option by Trichem is actually classified as a Firm Intention Announcement.

It gets even more interesting from a regulatory perspective. As this is just a subsequent tranche of a previously announced transaction, the categorisation calculation that took place at the time of the original deal stills stands. So although it is a s112 from a Companies Act perspective, it’s only a Category 2 under the JSE Listings Requirements.

But they need a circular anyway, not just a terms announcement, as the s112 needs a shareholder vote. They also need to include a fair and reasonable opinion from an independent expert.

It all sounds like useful inspiration for a tricky question in the JSE Sponsor exams!

The call option will be practically implemented as a subscription for shares by Trichem, followed by a share repurchase from enX. The pricing for the subscription was previously set at between R286 million and R407 million, with the calculation based on the underlying net asset value and profit after tax.

Based on the receipt of cash for this tranche, along with the release of cash held in escrow after the first subscription, enX plans to return the majority of the resultant net cash to shareholders. The circular will hopefully give a better indication of what that number might look like.

Local gold and PGM at Sibanye-Stillwater more than doubled EBITDA in 2025 (JSE: SSW)

The day really was darkest before the dawn

Sibanye-Stillwater’s results show you what can happen when you give yourself a chance to get lucky. After many self-help initiatives during the PGM downturn, the business was positioned for an upswing. And boy, did that upswing arrive in 2025.

The results reflect a 14% increase in revenue in 2025. That was good enough to drive a wonderful jump in HEPS of 281%. Talk about a year to remember!

It was also heavily weighted towards the second half, with normalised earnings coming in 377% higher in the second half vs. the first half of the year. The second half contributed 83% of full-year normalised earnings. If they can maintain that momentum, 2026 will be even better.

The balance sheet is in much better shape these days thanks to the improved profits, with net debt to adjusted EBITDA of 0.59x at 31 December 2025.

If we dig a bit deeper, we find that the South African PGM operations generated EBITDA of R16.7 billion, while South African gold generated R12.5 billion. In both cases, those operations more than doubled EBITDA vs. the 2024 levels.

The numbers are excellent elsewhere as well. The US PGM business swung from a loss in 2024 to positive EBITDA of R4.4 billion in 2025. The recycling business generated R4 billion in 2025 vs. just R0.6 billion in 2024. In fact, only the nickel business was in the red in 2025.

It wasn’t all good news in the gold business. The geotechnical issues at Kloof represent just one of the group’s headaches. But when the commodity prices behave like this, it can make up for a lot of other problems.

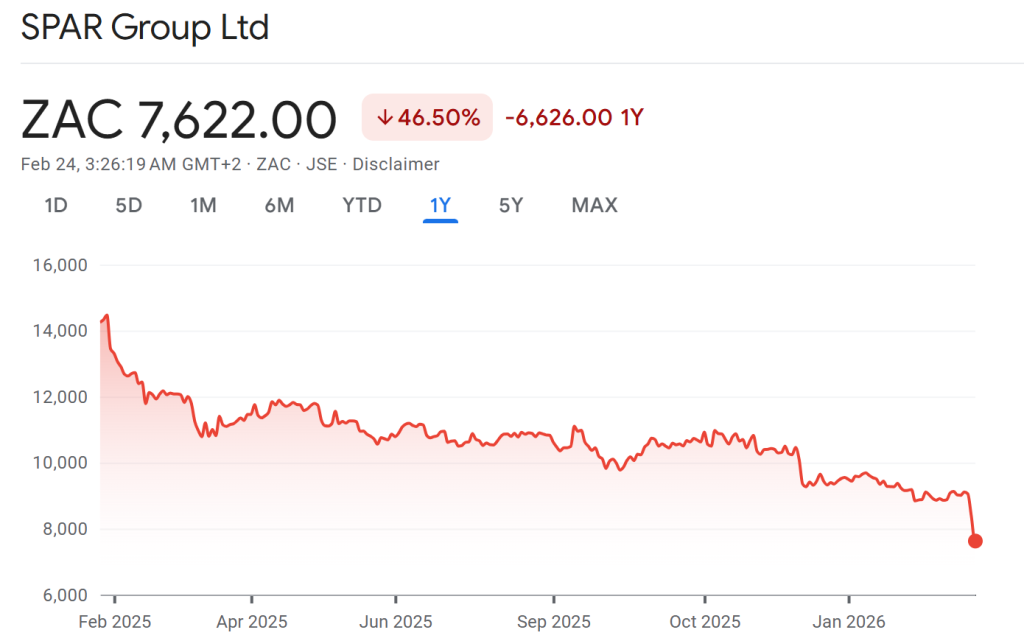

Spar needs a new CEO (JSE: SPP)

Things seem to be going from bad to worse

Spar closed 7% lower on Friday after giving the market a negative surprise around leadership. Angelo Swartz has resigned as CEO, having been with the group for 19 years. He was only in the top job since October 2023, so that’s not a terribly long innings by CEO standards.

The group isn’t exactly on a firm footing right now, hence why the market punished the share price for this turn of events. It helps a bit that Reeza Isaacs, the current CFO, will be stepping into the CEO role. This at least shows some internal continuity.

Megan Pydigadu, currently the COO, steps into the CFO role. The experience she gained in the turnaround of iOCO (JSE: IOC), which was of course still called EOH at the time of the turnaround, will no doubt be useful at Spar.

A further leadership change is the creation of a Managing Director position for Groceries and Liquor in Southern Africa. I don’t like this at all, as it suggests that top management will be straying further from the core business and will be focusing their attention elsewhere.

Above all, I sincerely hope that Spar isn’t cooking up another offshore acquisition. If you think the market response to Mr Price (JSE: MRP) announcing the NKD deal was bad, just wait until you see what would happen if Spar does something ridiculous. The only thing they should be doing is focusing on their core business – and it should be getting maximum attention from the top execs.

There’s a trading update call scheduled for Monday morning, so investors will no doubt have some pointed questions about this development.

Nibbles:

Director dealings:

The CFO of Calgro M3 (JSE: CGR) bought shares worth R203k.

An associate of a director of Visual International (JSE: VIS) sold shares worth R124k.

Magen Naidoo has bought another R7.6k of shares in Mantengu (JSE: MTU). You’ll find an important update on the leadership of the company further down in the Nibbles.

AfroCentric (JSE: ACT) announced the disposal of Active Health back in December 2025. It’s a Category 1 transaction, so they need to get a circular out. The JSE has granted an extension until 24 April 2026 to distribute the circular.

Northam Platinum (JSE: NPH) announced that the revolving credit facility has been increased from R11.3 billion to R13.3 billion. It matures in August 2027, giving them useful flexibility on the balance sheet. They also have a general banking facility of R1 billion, so the total available banking facility is now R14.3 billion. The plan is to push further into renewable energy projects that are owned and built by the company, rather than relying only on power purchase agreements with independent power producers. By 2030, Northam expects to source 70% of group energy needs from renewable sources.

Boxer (JSE: BOX) announced that James Formby is stepping down as chair with effect from 28 February 2026. The interesting element to this story is that Sean Summers, the CEO of Pick n Pay (JSE: PIK), will be taking the role of non-independent, non-executive chair. Formby will remain on the board, just not as the chair. And in case you’re wondering, Charlotte Maponya will continue as lead independent director of Boxer. If Summer’s appointment confuses you, just remember that Pick n Pay still holds a controlling stake in Boxer.

Mantengu (JSE: MTU) announced that CEO Mike Miller has resigned with effect from 28 February 2026. Those who followed the story last year may be aware that I was on the receiving end of a number of completely unsubstantiated allegations by Miller. I hope he finds peace in whatever he does next. And most of all, for the sake of the employees at Mantengu, I hope that incoming CEO (and current CFO) Magen Naidoo can improve things at the company, as recent performance has been very concerning. The jury is still out on whether any of the share price manipulation allegations have merit, as there were a number of parties accused of being involved. Will we ever really find out? Honestly, who knows – it’s one of the most bizarre stories I have ever seen on the market. And in case you’re wondering, Langton Mpofu has been appointed as the CFO to replace Naidoo. Mpofu has been with Mantengu since 2024, so there’s at least some continuity there.

Goodness knows what the reason for the delay is, but the special dividend declared by Caxton and CTP Publishers and Printers (JSE: CAT) has not received approval from the South African Reserve Bank (SARB). For this reason, the company has chosen to withdraw the declaration of the dividend and rather declare an interim dividend of the same value as the intended special dividend. Interim dividends don’t need approval by the SARB. I would love to have been a fly on the wall for some of the discussions that would’ve taken place in the background here!

Shareholders of 4Sight Holdings (JSE: 4SI) approved the repurchase of shares from Silver Knight Trustees at 55 cents per share. The value of the repurchase is R10 million. That might not sound like much, but the market cap of the company is R390 million. Perhaps more importantly, the current share price is significantly higher at 71 cents.

I generally ignore independent director changes that don’t have other interesting elements to them, but a change in the chairperson of the board is always worth mentioning. Insimbi Industrial Holdings (JSE: ISB) noted that Robert Dickerson will retire as chair, with Nelson Mwale taking that role with effect from 28 February 2026. There are changes to board committees as well.

Trustco (JSE: TTO) has decided to terminate the American Depository Receipt (ADR) programme that trades in the over-the-counter (OTC) market in the US. Holders will have until 26 March 2027 to swap their ADRs for underlying ordinary shares, which would then need to be held on the Namibian or South African register. Is this a precursor to the promised full-fat listing in the US, instead of the skim milk version on the OTC market?

As artificial intelligence begins reshaping the labour market, the real risk may lie in the turbulent gap between jobs lost and jobs created. The uncomfortable question is whether our economic safety nets are built for disruption at this speed and scale.

Somewhere around the start of last year, I began to feel anxious about artificial intelligence. Not in a Terminator-style, the-robots-are-coming kind of way, although Anthropic co-founder Dario Amodei’s prediction that AI models will one day build and control their own robots did make me feel a bit… queasy.

No, my anxiety comes from a much more practical place. I’m anxious because I struggle to understand what happens when we have more people than we have jobs for.

When I read AI-related thoughtpieces online, there is a lot of talk about the smaller workforce of the future, with parallels drawn to those shrinking birthrates that are currently alarming statisticians worldwide. It makes sense in the (very) long run: a smaller global population would equal a smaller human workforce, and the gaps left by people could be filled in by AI.

Seems like a neat solution, right?

But what I don’t quite understand is what happens now, in the year 2026, when our world population stands at 8.3 billion and the global workforce is at 3.7 billion. The clever people at McKinsey are constantly running models to try figure this out, with their latest research suggesting that between 400 million and 800 million individuals could be displaced by AI-ification in the next 4 years.

The awkward middle of automation

Of course, this isn’t the first time in human history that invention has led to job loss. We could look back at the Industrial Revolution, for example, or more recently, at the invention and widespread adoption of the personal computer.

In the US alone, about 3.5 million jobswere lost to the adoption of the computer and the internet in the 1980s and 90s. For context, the US population at the time was around 250 million, and 63% of Americans – around 160 million people – were employed. So, roughly 2.2% of American jobs were lost to new technology in the 90s.

A somewhat stark comparison to the roughly 15% of jobs that McKinsey predicts will be felled by AI, isn’t it?

But on the flipside of that coin, an estimated 19 million US jobs have been created since the 90s as a direct result of computer technology. Here we are just a few decades after the big disruption and about 10% of the civilian labour force is in an occupation that’s a direct result of the introduction of the computer.

History therefore teaches us that the computer and internet did indeed create more jobs. And how many jobs AI will create is certainly one question. But perhaps a more important question is: who will these new jobs be for?

History is far murkier on whether those who are displaced are the ones who get to claim those shiny new jobs. And with what we are currently observing in AI, this feels very different to someone learning to point and click a mouse.

The new roles that AI is expected to generate – things like prompt engineers, data annotators, AI auditors, model trainers, and robotics technicians – tend to sit on the more technical end of the skills spectrum. They reward digital fluency, adaptability, and in many cases, formal training. If you held a position as a delivery driver, a call centre agent, a retail cashier, or a bank teller – all roles that are earmarked for AI replacement – then the distance between your current skill set and the jobs being forecast is not necessarily a short one.

Entry-level white collar roles are at serious risk, as are junior professional roles that require training from senior staff.

Reskilling sounds good in theory, but in practice it can be a slow and expensive process. It also assumes people have the time, stability, and financial buffer to retrain themselves while their income is under pressure – and we are talking about a generation that can barely even afford to have children, let alone build up a balance sheet to withstand a crisis.

Labour markets do not rebalance overnight. Even if AI ultimately creates more jobs than it destroys (an outcome that is predicted, but not guaranteed), there may well be long and uncomfortable gaps in between. In those gaps, we could see mid-career workers struggle to pivot, while younger workers flood into new sectors faster than older ones can adapt.

The transition period, in other words, is where most of the real human pain tends to sit. In considering how to address this pain, we can refer to a writer named Paine. Nominative determinism never lets us down.

The original “disruption dividend”

Once upon a time (in 1795, to be precise) a political thinker named Thomas Paine published a pamphlet titled Agrarian Justice. Paine wrote his pamphlet because he was bothered by the rise of private land ownership. While he accepted that enclosing land was a logical step in the development of agriculture, he worried about what was being lost in the process: rivers, fields and orchards that had once functioned as shared sources of food were now disappearing behind fences and property lines.

In his writing, he shared his belief that those who benefited from private land ownership had some obligation to compensate the wider public, from whom the ability to sustain themselves – to hunt, fish, gather or farm on open land – had effectively been taken.

Paine didn’t stop at theory. He sketched out a concrete funding model where landowners would be taxed once per generation to support those who owned no land at all. Even in the late eighteenth century, the architecture is recognisable: not charity, exactly, but an attempt to design a system-level response to the economic dislocations created by structural change.

I heard echoes of this story when I first read the news that OpenAI’s Sam Altman was funding a basic income experiment in the US. From 2020 to 2023, Altman’s OpenResearch distributed $1,000 a month to 1,000 low-income participants in Illinois and Texas, while a control group of 2,000 people received $50 monthly. All participants were earning at or below 300% of the federal poverty line, with average annual household incomes under $29,000 (or around $2,400 per month).

The findings were intriguing. At the risk of straying from the main thread of this article, I encourage you to explore OpenResearch’s full report here. What fascinates me is the parallel between these two stories, even though they are separated by two centuries.

In 1795, Thomas Paine argued that people should be compensated as they lost the ability to sustain themselves from the land. In 2021, Sam Altman wondered whether people might one day need compensation as they lose the ability to sustain themselves through their labour. Paine didn’t try to block private land ownership, because he understood that, while it was disruptive to the status quo, it was necessary in order for agriculture (and by extension, humanity) to progress.

Similarly, Altman seems to be acknowledging that artificial intelligence will bring inevitable disruption, and that this disruption is necessary in order for our species to advance to the next phase. Like Paine, he appears to be wondering whether those who “own the land” should be responsible for addressing the gap left by their inventions.

Who actually pays for AI disruption?

Each major technological leap expands what the economy can produce, and unsettles how people earn a living along the way. Artificial intelligence appears to be following that same script, only faster. The real tension is not the long-term outcome, but the messy transition period in the middle, where labour markets tend to wobble before they rebalance.

That is why the basic income conversation keeps resurfacing. Not because it is politically easy (it is not), and not because it is proven at scale (it is not that either). An unconditional universal basic income, in its pure form, has never been successfully implemented at national level. What we have instead are pilots, partial schemes (like the ones implemented during the Covid-19 pandemic) and local experiments. And while these are all useful signals, they are far from settled policy.

Of course, even if the basic income model could be made to work inside one country, a more complicated problem sits just beneath the surface. Back in 1795, the world was a whole lot less connected. Thomas Paine was writing about taxing land within national borders to support that nation’s citizens.

Today’s AI economy does not respect those boundaries.

The companies building the most powerful systems are concentrated in the United States, but the labour disruption that those systems will trigger is spreading globally. If the “owners of the land” – the AI creators – are only taxed or regulated in their home markets, the resulting support mechanisms will also remain largely domestic.

That creates an obvious imbalance. The productivity gains may cluster in the US, where the technology is developed, while labour market disruption ripples outward into economies with far less fiscal room to cushion the blow. The geography of AI profits vs. AI pain is not set to line up.

So how does the world deal with that mismatch?

One idea occasionally raised in policy circles is some form of cross-border adjustment in the form of tariffs, usage levies or access fees on advanced AI tools deployed in foreign markets. For example, if you are a South African business preparing to replace a South African employee with technology that makes profit for an American business, the government could make you pay more for that choice through tariffs. In theory, this could help recycle a portion of AI-driven value back into the regions absorbing the labour shock, as companies will weigh up the cost of AI tokens vs. the cost of a warm body in the office.

In practice, it would be technically complex, politically sensitive and highly contested in global trade forums. But solutions seem thin on the ground right now.

The deeper we move into an AI-shaped economy, the clearer it becomes that this is not just a domestic labour story, but a global one. Technological disruption rarely waits for policy to catch up. It compounds first, and the surrounding systems adjust later.

The open question is whether we start designing those adjustments while the shift is still gathering speed, or only after the imbalances have already taken hold. Society as we know it today may depend on the answer to that question.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Blu Label Unlimited’s results are still impacted by once-offs (JSE: BLU)

But they have taken a big step towards “clean” numbers

Blu Label’s economic relationship with (now separately listed) Cell C (JSE: CCD) has no doubt inspired many a sadistic FinAcc IV examiner. With a reputation for arguably the most confusing set of financials in the local listed market, the hope is that the separation of Cell C will help create more understandable numbers going forward.

But we aren’t quite there yet. Cell C only listed at the end of 2025, so Blu Label’s numbers for the six months to November 2025 are still full of complexities. There also happens to be an impairment of R6 billion on The Prepaid Company’s investment in Cell C, partially offset by a gain on remeasurement.

Thankfully, the trading statement gives us some numbers that are actually useful. If you strip out everything related to the restructuring of Cell C, you arrive at revenue for Blu Label of R5 billion, EBITDA of R535 million and net profit after tax of R389 million. Core headline earnings of R398 million translates to 44.19 cents per share in earnings.

Notably, Cell C will be equity accounted by the group, as Blu Label has retained a non-controlling 49.47% interest. Equity accounting is much simpler than consolidation accounting, as any tired and weary accounting student will tell you.

But here’s something else to chew on: core HEPS is down by between 10% and 14% year-on-year. Even if you use the simpler numbers, it doesn’t look like the business had a great year.

Those who bought this story in 2023/2024 did extremely well, with high returns in a short period of time. But those who bought the hype in the run-up to the Cell C listing have been smashed. I haven’t participated at all, as I only buy things that I think I understand.

The markets are hard enough without backing yourself to win a game of musical chairs:

City Lodge’s results would be so much better without the forex movements (JSE: CLH)

At least the dividend is up strongly

My City Lodge position is currently up 16%. That’s certainly not bad, although recent weakness in the share price has taken some of the shine off the returns.

Group occupancy rates for the six months to December 2025 tell a positive story, increasing by 420 basis points to 61.6%. This is the highest occupancy rate since pre-Covid. Combined with an average room rate growth of 4%, revenue was up by 12%. It’s also worth highlighting that rooms revenue increased 10%, while food and beverage revenue was up 17%.

Food and beverage revenue is now 20.5% of total revenue, an exceptional example of management’s strategic execution in recent years.

With total costs up 9% (a solid outcome in the context of higher occupancies), adjusted EBITDAR was up by 16%. And no, the R on the end isn’t a typo – EBITDAR is the industry standard in hospitality.

Adjusted EBITDAR margin was 130 basis points higher at 32.5%. In terms of cash returns, their cash generated from operations increased by 39%. That’s another encouraging metric for the underlying performance.

It all sounds great so far, right? Well… there’s a catch.

Sadly, HEPS actually fell by 0.5% thanks to forex movements. The stronger rand gave them an unrealised loss on forex of R24.7 million vs. a gain of R10.9 million in the prior period – a nasty year-on-year swing. This mainly relates to an intercompany rand-denominated loan in Mozambique.

The group reports adjusted HEPS growth of 33% in an effort to convince investors to focus on that number. It helps that the dividend also increased by 33%, as there’s nothing quite like cash returns to help focus the minds of investors.

The HEPS performance was assisted by share repurchases in the past year, as City Lodge has repurchased 6% of shares in issue at an average price of R4.00 per share. The current share price is R4.75.

Despite this promising underlying narrative and a number of refurbishment projects underway to take advantage of improving local conditions, January occupancy levels were irritatingly weak. They fell by 200 basis points to 42%. Total revenue was up 4% year-on-year, but that’s not great. February was even worse, with occupancy down 400 basis points to 56%. At least they’ve managed to achieve better average room rates and food and beverage revenue in February, with total revenue up 5% despite the drop in occupancy.

The second half of February is showing some momentum. They are hoping it continues.

At least I wasn’t hallucinating the slow start to the year. I couldn’t understand how things were taking so long to get going. Based on this update, people clearly took their time to get out of bed in 2026. I still can’t really figure out why.

Equites Property Fund affirms guidance and highlights appealing metrics (JSE: EQU)

Their portfolio has locked in above-inflation returns

Equites Property Fund has released a pre-close update dealing with the year ending February 2026. With a low portfolio vacancy rate of 0.3% and weighted average lease escalations of 6.2% in the portfolio, key metrics look good. Guidance for growth in distribution per share of 5% to 7% is unchanged for FY26.

As Equites quite correctly points out, their weighted average lease escalations are more than double the current SARB inflation target. With a weighted average lease expiry in the portfolio of 14.1 years, they are poised to significantly beat inflation for a long time. And thanks to triple-net leases that put cost exposure on the tenants rather than the landlord, the fund feels good about turning revenue growth into distributable profits.

The loan-to-value is expected to be 34.2% at the end of the period, down from 36.0% at the end of FY25. The balance sheet is therefore in good shape.

The loan-to-value ratio will come down further when more of the UK disposals are concluded. Some properties in the UK are being held while rent reviews are finalised, as this improves the chances of a successful exit. They do still have development plans in Equites Newlands Group Limited (ENGL), the platform in the UK that Equites owns alongside Newlands Property Development LLP.

But the real focus is on South Africa, where logistics space demand has remained strong. The R21 corridor is particularly appealing to Equites, with a joint venture in place with Tridevco to maximise their chances of capturing this demand. Overall, sector vacancies are just 2%.

A good example of a typical project is a development for Tiger Brands (in partnership with Tridevco), with a yield of 9% on a development cost of R1 billion. They are in advanced stages of negotiating further development leases with an expected capital investment value of R1 billion over the next 12 to 18 months.

In case you’re wondering about how this development yield compares to the cost of funding, Equites has a cost of debt of 8.2%. They’ve had some encouraging recent bond issuances and debt refinancings, so that helps to keep their cost of debt on the right side of their development yield.

Although construction cost inflation helps the value of existing properties, it can also make it difficult to achieve an attractive yield on new builds. Equites noted that the Construction Input Price Index (CIPI) showed average inflation for the year of just 1.5%, well below the 5-year and 10-year averages of 8% and 6% respectively. It picked up towards the end of the year though, so that is something that Equites will need to carefully manage.

There is limited exposure to renewals in the next 24 months. Although you might think that is a good thing, it can actually be a drag on earnings if we are in an environment of positive reversions. It looks like the FY27 renewals could achieve a significant positive reversion of 17%, while FY28 is far less appealing with an expected negative reversion of -9%. The logistics funds have lumpy leases vs. retail funds.

And for the renewable energy enthusiasts, you’ll find it interesting that the sector is generating 16% of total energy demand from solar (according to Nedbank CIB Market Research). It helps that distribution centres have huge roofs! This is an obvious area of investment by logistics property funds, particularly with so much pressure on electricity tariffs.

I’m curious to get your views on the property sector. Which asset class do you like the most?

Gold Fields joins the earnings party in the sector (JSE: GFI)

As you know by now, the gold miners have been printing cash

Gold Fields has now added its name to the list of gold mining houses that made a fortune in 2025. For the year ended December 2025, they achieved a jump in attributable profit from approximately $1.25 billion to $3.6 billion. The move in headline earnings was a slightly less thrilling increase from $1.2 billion to $2.6 billion.

On a per-share basis, this means that HEPS more than doubled from 133 US cents to 288 US cents. The base dividend per share for the year was R25.50, up from R10.00 in the prior year. In addition to this, they have declared a special dividend of R4.50 per share.

This kind of dividend growth is made possible by adjusted free cash flow jumping from $0.6 billion to nearly $3 billion.

One of the highlights is that all-in sustaining costs only increased from $1,629/oz to $1,645/oz. In a period where the gold price moved higher, that’s obviously a huge boost to profits.

The jump in earnings helped them reduce net debt from $2.1 billion to $1.4 billion. The entire sector is deleveraging at the moment, with bumper profits being used to repay lenders.

Although there’s obviously more variance in performance once you dig down into the individual mines, the group results are clearly good news for shareholders. The Gold Fields share price is up 134% in the past year – well behind Pan African Resources (JSE: PAN) as my lucky pick that managed to increase by 311%!

Jubilee Metals is on track for 2026 copper production guidance (JSE: JBL)

This is despite the rainfall in Zambia

Mining is a tough game. There are many external risks, with the weather being just one of them. If there’s enough rainfall, then extracting metals from the ground becomes difficult – and sometimes, impossible.

In an update covering the six months to December 2025, the Jubilee Metals narrative is one of strong production despite the expected rainfall.

The Roan Operations hit their targeted production level of a feed rate of 30,000 tonnes per month. Copper production was up 172.8% for the first half of the year vs. the comparable period in the prior year.