Alphamin had a strong 2025 despite security challenges (JSE: APH)

And the share price has rewarded those who took a punt

To say that Alphamin has been on a choppy journey would be an understatement. Check out this share price:

There’s clearly plenty of money that could’ve been made along the way, but it’s also possible to have bought the early peaks and been flat for the past few years. Also take note of the horrible dip in early 2025 in response to security fears in the DRC. The share price is up more than 2.2x since then!

This recovery has been driven by the only thing that investors want to see: tin coming out of the ground and producing cash. The security risks are never zero, which is why African mining businesses tend to trade at valuations that consider the risk. But as cash is banked and the balance sheet is shored up, investors breathe a collective sigh of relief – and pay more for the shares.

Alphamin has now released the results for the year and quarter ended December 2025. FY25 tin production was up 7% and sales volumes increased 4%. But thanks to a 13% jump in the average tin price achieved, EBITDA was up by a juicy 25%. Remember, this was despite the security issues in March/April that led to a suspension in operations. Shareholders will be more than happy with that!

Looking at Q4 vs. Q3 as a measure of momentum, tin production dipped 4% and sales were down 2%. The average tin price rose by 12% though (yes, quarter-on-quarter!) and so EBITDA increased by 13%. Production will always be volatile if you isolate each quarter, as mining isn’t exactly flipping burgers.

The encouraging element of this update is the momentum in the tin price and what this means for earnings, while recognising that FY25 was a strong year overall despite such challenges.

Alphamin’s cash balance improved from $30 million to $56 million over 12 months. Their next dividend decision will be made in April 2026. Naturally, the current trajectory of tin prices is bullish for cash payments to shareholders. They just need that trajectory to continue.

On the exploration side, recent drilling at Mpama South and Mpama North has delivered disappointing results. Although this doesn’t affect near-term cash flows, this is something investors will need to consider in terms of the longer-term value of the project and the valuation that it trades at.

Here’s another thing investors need to think about: CEO Maritz Smith has decided to retire after more than six years. The current CFO, Eoin O’Driscoll, will step up to the CEO role. JP van Staden, previously the CFO of the operating subsidiary in the DRC, will take the group CFO role. It’s always good to see internal succession like this.

Sibanye-Stillwater plots a way forward with lithium (JSE: SSW)

A staged approach is preferred for the Keliber project in Finland

Sibanye-Stillwater can certainly breathe a sigh or two of relief at the moment. The incredible PGM rally as a follow-on to the gold rally has delivered a share price return of a whopping 320% in the past year. And if you can believe it, the return over 5 years is just 12%! When people talk about cyclical companies, this is the kind of business they are referring to.

With the core business printing cash at the moment, Sibanye can afford to dedicate more time and attention to some of the other investments in the group, like the Keliber lithium project in Finland. These projects are all about careful planning, particularly in the context of market conditions.

The cold commissioning of the fully integrated project is on track for Q1 2026 with a total capital investment of around €783 million. But the real focus is on the plan for the ramp-up of the project and pathway to production, with a staged approach agreed between Sibanye and its partner in the project, Finnish Minerals Group.

This partner, owned by the State of Finland, intends to participate in further equity funding on a pro rata basis in terms of its existing stake of 20%. This is a strategically important project in the EU. Given the geopolitical environment at the moment, anything that improves European independence from other major regions will be given priority.

What does a staged approach really mean? Essentially, they are maintaining maximum flexibility and moving carefully through the pre-operational phase. This includes engaging with potential strategic off-takers as well. If you can imagine a game of hide-and-seek, this approach means checking each room carefully and plotting your move into the next one, rather than charging through the house to see what might happen behind the curtains.

Nibbles:

Director dealings:

An executive of Investec (JSE: INL | JSE: INP) sold shares worth R4.5 million.

A director of Dipula Properties (JSE: DIB) bought shares worth R167k.

Europa Metals (JSE: EUZ) will pay a return of capital to shareholders in February 2026 after shareholders approved the payment at a general meeting. The amount is 21.993 cents per share.

Numeral (JSE: XII) has confirmed that the 10:1 share consolidation will be completed by 2nd February. This is an important step to take the company out of impractical “penny stock” territory where there isn’t a practical bid-offer spread.

Priscilla Msimanga made the leap that so many dream of, yet few are willing to make: leaving a big corporate role and shifting into the grinding world of entrepreneurship. To add to the intrigue, she bought a Shell forecourt and stepped into specialist retail.

From managing staff to complying with petroleum regulations, the learning curve was steep. Drawing on her corporate experience, her love of sales and her passion for service, Priscilla rolled up her sleeves and did everything – from pumping fuel to serving food.

And yes, that means there’s a food truck to go with this great story!

On episode 7 of The Finance Ghost Plugged in with Capitec, Priscilla tells us more about her leap from corporate life to entrepreneurship.

Episode 7 covers:

Her corporate background and why she wanted to do something of her own

How she prepared before leaving corporate

Finding the right forecourt to buy

The retail strategy of a forecourt and adapting to local consumer tastes

Why hands-on involvement matters for success

An honest look at the short-term financial impact of leaving corporate and starting a business

The Finance Ghost plugged in with Capitec is made possible by the support of Capitec Business. All the entrepreneurs featured on this podcast are clients of Capitec. Capitec is an authorised Financial Services Provider, FSP number 46669.

Listen to the podcast here:

Read the transcript:

The Finance Ghost: Welcome to this episode of TheFinance Ghost plugged in with Capitec. What a wonderful podcast season we are having. We’ve spoken to some really interesting entrepreneurs doing all kinds of different things.

We’ve covered retail, we’ve covered restaurants, we’ve covered pharmacy. We’ve covered a whole bunch of things, and today we are doing something completely different.

What I’m particularly excited about with this podcast is that we will be speaking to someone who has done something that so many people dream of, and that is to leave their corporate job and go off and either start a business or acquire a business.

So many of the other people I’ve spoken to on this podcast season, they either started the business quite young or they’d been entrepreneurs for a very long time. Whereas for Priscilla Msimanga, the owner of Shell Boksburg Motors, this is actually quite new for you, which I think is great! A nice fresh journey into entrepreneurship, having left the typical corporate jobs and very senior roles.

So, Priscilla, thank you so much. Really excited to just get to know you and to talk about this. Because, as I say, I think what you’ve done is something that many people, when they’re sitting in traffic on the way to work, fantasise about doing. So, congratulations!

Priscilla Msimanga: Thank you! Good morning, Ghost, and good morning to your listeners. Thanks for having me.

The Finance Ghost: No, it’s great to have you. Let’s jump straight into that path that you have travelled, and then we’ll talk about the business that you own today.

So, let’s just get a backstory here. What was your career before you decided to get out of corporate and go into entrepreneurship?

Priscilla Msimanga: It was a weird sort of career, right? So, I studied business engineering, but I ended up in IT about 20 years ago – by chance, because I’m one of those people who like taking risks. So, I went into IT.

I got to move into SAB (South African Breweries) after being headhunted, and went into Head of IT (well, not Head of IT, but sort of Service Operations Manager, which is a Head of IT at a smaller scale) for a site, which was Egoli. That’s where my journey started, with IT, until three years ago when I decided I needed to pursue my love.

I’ve always been an entrepreneur at heart. I’ve always been that person who grew up in the dusty streets of Sebokeng, selling stuff. My mother never had a job. She made jobs by selling, and had a spaza shop, so that’s where the passion came from.

From a corporate perspective, I grew up in the ranks and became Head of IT for a multinational in Cape Town. Two multinationals, actually – by the time I left, I was a Head of BSS (Business Support Systems) for MiX Telematics, and before that, I worked for Philip Morris.

But MiX Telematics was more of a contract role, because I had started on the journey of, “I want to be an entrepreneur. I want to build a legacy, as opposed to being an employee.”

So, yeah, that’s kind of my journey. Loved corporate, loved IT, loved doing it. Loved the interaction with people – that was my passion. My last VP actually said to me, “You are more of a marketing person than an IT person.” I was like, “Yeah, maybe I am!”

So, yes, that’s how I started my journey. It wasn’t easy leaving corporate, because of the security around where your next salary is going to come from. I’ve grown quite a bit. I have a growth mindset. Studied quite a bit – you don’t have to pay for it, they actually pay for it. So, it was quite easy to do that.

It wasn’t a very easy decision to say, “I’m going into entrepreneurship,” but I was pushed more about building my own legacy and actually being an employer, as opposed to being an employee.

The Finance Ghost: Absolutely, I love that story. So, I always laugh – there’s this standard joke that goes along the lines of, “Instead of working 40 hours a week for someone else, I want to work 60 or 70 hours a week for myself!” Because entrepreneurs, of course, have gone through the long hours. They understand this. I’m sure that’s been your experience as well (although it doesn’t sound like your jobs were exactly 40 hours a week to start with). But I think there’s a good underlying point there around what it’s like to go from corporate into an entrepreneurial environment, and actually deal with that adjustment.

I love the reference there to taking risks, and that informal economy experience when you were growing up. It’s amazing how those experiences shape what people do later in life, it really is. And it comes through as you speak to entrepreneurs. They all have a relatively common thread that goes through their backstories around either their parents were hustlers, or they were, or it’s side gigs, or it’s holiday jobs, or it was something at high school. Something triggered an interest for them, and then it’s stayed with them.

And that comment you made about being more of a marketing person, I also really like that. Because if you work for yourself, you work in sales. Primarily, you work in sales. You’ve got to keep everything else going, all the operational stuff, but you’re a salesperson.

So, well done on making the leap. I think that’s fantastic. How did you actually make the final decision? Because, as you say, it’s not an easy thing to do, it’s not an easy decision to make, especially with large corporates.

It is quite a nice safety net, and like you say, lots of opportunities to grow, to study further. When you get to that level, you’re leaving behind quite a lot, and I think that’s what stops people from doing it.

So, what was the final decision for you? What made you say, “That’s it, I’m out of here. I’m leaving corporate”?

Priscilla Msimanga: Age. And moving to Gauteng. This was weird, how this came about, right? A friend of mine, while I was busy with a presentation for the ExCo, said to me, “There is a site in Leeu-Gamka.” Leeu-Gamka, of all places!

She kept on pestering me, and I was like, “Okay, let me just do this for them, let me get it out of the way,” because she had already acquired one. And two years later, then the process started, right?

And I’m still working. And I’m like, “Maybe let me pursue this,” and it started being interesting. I don’t know this, and I want to see what this has got for me. Because I always took risks, I was like, “I’m going to go for it.”

And that was the time when I made a decision, “In two or three years, I must be out of corporate.” I had to move to Gauteng in…2023? 2022, actually, and then I got to do the job with MiX in 2023.

But during that time, when I got into MiX, it was already set up. It was just getting a site and getting in there and starting the business, because I started in 2024. I was appointed in 2024 very early, around Feb. So, yeah, that’s how it started.

It was more of a push that, “You’ve got to go. Now it’s time.” Because I put it off, from the age of 27 until later in life. That I needed to go. So, until later in life, I’m like, “If I don’t do this now, I’ll probably never do it.” And then I just decided not to go for corporate anymore, and to pursue this full time.

The Finance Ghost: So, the one thing there that’s so interesting, Priscilla (and it’s, I think, also in my own experience, so true) is that kind of two- to three-year runway from when you decide, “Okay, it’s time to go.” It’s almost impossible to then do it straight away. You’ve still got to actually give yourself runway.

And two to three years is pretty common, actually. I think mine was even longer than that. I had this spreadsheet on my computer for a very long time, called ‘Escape Plan’.

And ‘Escape Plan’ was basically me making sure that whenever I added a monthly overhead, I used to put it on the Escape Plan and be like, “Look, is this an overhead where there’s no flex? Is this an overhead that can go away if it needs to? And then, what would I have to earn in order to escape?”

And people think people just wake up – they look at a successful entrepreneur, and they go like, “This guy or this lady just left corporate one day, and it worked.” It’s not actually how it works. You’ve got to plan for this thing, and you’ve got to adapt your life to it. You’ve got to get ready for it. Maybe we can chat about that just now.

But what I would like to understand is, you talk about these sites being ‘ready’, so this is the decision to go into fuel retail, these forecourts. As I said earlier, Shell Boksburg Motors – that’s you.

From Cape Town to Boksburg, that’s a reasonably unusual path (I think the other way around is more common, let’s be honest). So, from Cape Town to Boksburg you went, and you went and got this forecourt site.

How did this happen? How did the sites become available? What was the situation to be able to get one, to qualify? What was the backstory that got you to say, “Not only am I leaving corporate, I’m going to go and acquire a petrol station”? Which is a really interesting thing to do!

Priscilla Msimanga: So, to answer your first question, how did it happen? Moving to Joburg was an “I need to go back home”. Because Joburg is home. Boksburg, I already had a base because I held a house there, so it made more sense that I move back to my place.

So, the place that I applied for was not in Boksburg, it was somewhere in the Pretoria area. But there are a couple of sites that usually come up. When, during that process, the Boksburg site came up, I was like, “Okay, maybe I should try this one.”

It takes, literally, a year before everything is sorted, because it’s quite a process. It’s an advertisement on the site – I recommend that people check the fuel sites, different brands. They advertise petroleum sites on there. That’s what I did. I found a site, and I went and applied.

You’ve got to have a good idea of the area. You’ve got to create a business plan that shows the financials, the marketing. You’ve got to know at least a lot about the financial and the environmental sort of SWOT of that area.

I had to create that in preparation for this, because you go through three different interviews. The first one is pretty much around, “What is it that you know about the site?” You present your basic business plan – there’s a template, of course, but you’ve got to have your own so that it can feed into this.

It was luck that I actually lived in Boksburg before. So, I understood the area very well. I understood the LSM, which worked in my advantage. I understood the dynamics that they wanted in the place.

Then we went to the second interview, which is pretty much about the sales and the execs of Shell that will sit down and say, “What do you know about this place? What value are you bringing? What is it that you will change? What do the financials look like? Most importantly, do you have the money to buy it?”

So, the preparation we spoke about (of three years) was the money part, right? Because you’ve got to have at least 20% – depending on which bank you go for, 20% to 40% – of the actual capital. I needed to have that money. So, during that time, it was the savings, it was like, “Every penny counts, because this is what I want to do.” It’s the availability of that money – proving that you have it.

Then after that, it’s the actual work. After they say yes, it’s the licensing from a DMRE (Department of Mineral Resources and Energy) perspective. It takes about six months for that to happen, to have a final trading licence.

You’ve got to go into, “What’s my working capital? What does the site look like?” Now it’s real. It’s no longer pen and paper. It’s, “How do I make this work? How do I get the money to actually make it work?”

And I had to get the 20%, of course. I proved that. I had to go to all the banks – and Capitec (yay!) was amazing, they actually came out quicker than most of the banks – because they look at the risk, right?

“This is Priscilla, who comes from corporate, who’s an IT Head. What does she know about petroleum?” So, it presents a little bit of a, “Are we getting ourselves into a corner here? Will she do this? From computers to petrol – what is she doing?”

I think they took a leap of faith and appointed me. I went through a couple of sort of government financial institutions, which couldn’t come through in time. Some of the banks were a bit slower, but Capitec was much, much faster.

And this is where I am. And then the work starts. You pay the person, then you start working. You do not know anything about this business. But what I did, though, which was smart, was, between the Leeu-Gamka situation and when I took over, I took time to learn the business.

Being in a petrol station and just putting petrol is the least complex of all, but when you get into the business, there are so many things that you have to be aware of. There are so many things that you have to comply with.

There are a lot of requirements. From a business, from a South African perspective, from the licensing, from the food safety. There are so many nitty-gritties that I had to comply with.

But because I had already, for at least a year, been going to this other lady who helped me quite a lot in Pretoria. At least 180 hours, which I spent with her, just to understand the business.

Because the first one, I didn’t get, because I didn’t have the operational knowledge. And it was a challenge for me, like, “Go for the operational knowledge.” I had to go and learn, and it was quite interesting.

I’m like, “Sho. We just come in and pump petrol, and then you’re like, ‘I’m paying.’ And that’s it.” But there are quite a lot of things that happen behind the scenes.

So, yeah, that’s how the journey was, and how I got into a relationship with Capitec, as well.

The Finance Ghost: Yeah, very cool. I love that that’s come through. I was going to ask you what difference Capitec made in the process, and you’ve already answered the question, which is lovely.

And like you say, it’s such a big adjustment actually going into a business, right? You spoke earlier about how, if you’d stayed in corporate, maybe you would have been able to study further. I think you’ve learned much more by leaving corporate and actually spreading your wings and going out into a business like this.

Because that’s the biggest thing with entrepreneurship – you have to understand the entire business, and then you have to actually figure out how all of the different elements work. And this is where it’s so interesting.

So, especially with a business like that, I can imagine the risk and compliance stuff must be through the roof. Because, I mean, it’s as flammable as it gets. Let’s call a spade a spade – a forecourt is basically a great big bomb inside concrete. So, it comes with a ton of health and safety stuff.

And then you’ve got the store, which has to have the right strategy for the area. So, like you said, you’ve got to understand the local area. Because it’s a retailer, and like any retailer, if you don’t understand the average customer – a forecourt in a very rich area is going to sell something completely different to a forecourt in a lower-income area.

And you can see it when you look at the specials. If you go into a fancy area and you put petrol in your car, you’re going to go into the forecourt – they’re going to have freshly baked goods, it’s going to be Magnums on sale. It’s that kind of vibe.

When you go into a lower-income area, it’s pies, and it’s Score energy drinks. You’ve got to respond to the people in the area. That’s how retailers make money. So, there’s a lot to learn. I can imagine it’s been such an interesting business.

When you look back on it now, and as you continue to run this thing, what would you say was actually the biggest challenge in getting up the curve on understanding how the business works?

What was really, really difficult, and which pieces do you think were maybe a little bit easier?

Priscilla Msimanga: I think for me, the people part was the most challenging part. Forecourt, there is a best practice, so you probably can – if you’re from corporate, you’re used to standard operating procedures, you know that in terms of compliance, this is what I should do.

From the shop perspective, I had a little bit of knowledge around what LSMs are there and what it is that I need to sell. We used to sell things that are not relevant, and you look at the pricing and that, so you kind of have a strategy.

But human beings, you can’t have a strategy for. Because they are very different in nature. But I’ve always been very fascinated by the human mind, especially now that I’ve moved from managing professionals to now managing the forecourt staff. It’s very different, the different spaces.

So, for me, it was that. You’ll be surprised that, because this is a cents and rands business, theft is a huge thing. So, that was my challenge. How do I make the team be part of the business, if you get what I mean?

Most of the time, we employ people, but I wanted them to be part of the business and care about the business. Because if you do, then you get them to be loyal and know that “If I steal, then I would not be able to get a salary.” That understanding.

And also the customer service aspect of it, because I’ve always been very passionate about customer service. We don’t want you to come to the garage… The last thing I want is for you to be in the forecourt, trying to pour petrol, and it takes 10 minutes. I’m like, “What are we doing?”

So, I wanted people who are energetic. I wanted the spirit that I have – the passion of what I do, and the pride of what I do. I love owning a petrol station. I love being on that forecourt and gooi-ing petrol into that car.

The Finance Ghost: I was going to ask, if you are there pumping petrol sometimes! I can totally imagine you doing it.

Priscilla Msimanga: I am pumping petrol.

The Finance Ghost: There we go, I knew it!

Priscilla Msimanga: I’m being the cashier. I am everything, basically, most of the time. Of course, not all the time, because there are things that I need to do. But if the forecourt is full, I will say, “Give me my tag, I’m going to go on that forecourt and gooi.”

The Finance Ghost: Nice.

Priscilla Msimanga: Because we need those cars to move. And also, this is a business where you have to be highly involved. And the fact that I knew I didn’t know. It’s a very good position to be, when you say, “I’ve only learned this for the past 14 months.”

Compared to someone who’s been doing it for five years, they assume that they know. But I knew I didn’t know enough, so I had to learn. What I learned in the other spaces, now I had to practice, replicate.

And the only way to do that is to be involved. Be that cashier. Understand when a customer says, “Oh! You’re always out of Grand-Pa, what is wrong?” Then you know what to address.

Or when you are in a forecourt, and the person is upset because he said he wanted R100 and they gooi R200. So, you find ways of having a strategy on, “How do we satisfy a customer and, at the same time, not lose money?”

So, yes, I love being on that forecourt. I always say, “I’m from heels to boots.” Safety boots, because you’re wearing your safety boots on the forecourt. You have to be an example. I can’t come in wearing high heels on the forecourt. It will be an HSSE (Health, Safety, Security, and Environment) issue.

So, yes, I am on the forecourt all the time, very involved financially. Cash-ups, I do it. I check every little cent from banks. The merchants were another thing where I thought, “It’s easy.” Banks do not take two seconds to open a merchant account. It took, like, months. So, yeah.

The human element was the challenge, but I think I’m in a space where everyone understands what I expect. It’s been 14 months or so, and they understand what I’m at. They see it live, they see the passion. You can’t not have passion if the person who owns the place actually goes on the forecourt. Why do you say I can’t? So, it’s been quite a challenging part of this for me. The other parts are pretty much standard. I was able to comply.

And why I say it’s been something that I’m proud of is, this quarter, out of 583 stations, I’m number 15, and I haven’t even traded for two years. So, there’s something that we are doing right.

The Finance Ghost: Well done! And, yeah, I love the passion coming through there. It’s so obvious. That’s why I guessed that you were probably out there, as you say, gooi-ing petrol, because you just strike me as someone who gets involved. And I think that’s key here.

I was going to ask you if you have to actually be there all the time? Or can you trust a station manager to get it done? I guess when people own multiple forecourts, you can’t cut yourself into lots of pieces, so you have to get to the point where you have people you can trust.

But I guess, early days like this, you’ve got to understand how the entire business works. And that’s an interesting point. Because I’ve seen people in my life who have started businesses, and they start something where they either have very little idea of how it works – and that’s still okay, provided you’re willing to learn.

But sometimes they say, “Well, I don’t really know how this works, and I’m going to find someone who knows how it works, but I’m going to be the business owner.” It’s just…it’s a structural problem.

You need to understand your business inside out. You need to be able to do all the things it needs. You’re not going to do them forever – you’ve got to outsource, you’ve got to find staff, etcetera – but you’ve got to be able to jump in and be like, “I understand that job, this is how it’s going to work.” Especially for small businesses.

And that’s one of the big differences to corporate. In corporate, everyone is a cog in the wheel. You understand your world and how it fits in with everyone else, but that’s all you need to understand. Whereas when it’s your own business, you need to understand the whole thing, right? Inside out.

Priscilla Msimanga: Yeah, so I do have a site manager. Because part of my role is to scan the environment around me. To check the prices in other areas, to understand if I stand in the middle of a Makro, or any other warehouse, and go like, “What would I buy if I were my customer?”

And I would then do that buying and saying, “It’s Christmas, we have extra money from the bonuses. What would I want?” Instead of having Cadbury, I want to indulge and buy a Ferrero Rocher.” So, why not get Ferrero Rochers and test the market?

So, I do have someone that I now feel comfortable to leave when I’m not around. But it will be for a couple of hours, of course. He would be an operational person.

The other thing is the growth, right? So, the innovative part. I’m a Select store. Select store means I don’t have that big bakery. So, I don’t have hot food, but can I stay without hot food? Hell no. So, I needed to find a way to be creative around it.

If I can’t make my place bigger, I need to make a plan to sell hot food, and I did. I got the food truck. It was the first [laughing]. I have a little food truck…

The Finance Ghost: I love that! So cool [laughing]. That’s great!

Priscilla Msimanga: …and I’m selling hot food, and I’m selling what I think people would like for the market that I’m in. So, I have hot food now. When I got there, there was no gas. I’m like, “I have a gas stove, we have an electricity problem, so why not sell gas?”

Started the process of being compliant with the gas, because I didn’t have a licence, and I now sell gas. So, it’s those kinds of ideas. This is how you see it. When you scan your environment and say, “What do we need? Do we need gas? Yes, we need gas.”

The people who are selling gas close at 6pm or 8pm. I’m 24 hours. So, that market after 24 hours, that is why we are a convenience store. Your gas finishes at 8pm, you’re having a braai, so you come to me and buy the gas. So, yeah, that’s pretty much how it works.

The Finance Ghost: Yeah, it’s crazy interesting. The food truck is fascinating. Tell me about the menu. What can someone get when they’re hungry, there at Shell Boksburg Motors?

Priscilla Msimanga: We get from sandwiches to pap and steak, because my market is really people who are working in the area. I’m in between the car dealerships. Most of the people on lunch don’t have anything to eat. So, we have the best mogodu as well.

We have fancy foods like chicken and chips. We sell kota – I don’t know if you know what kota is? [laughing] It’s a little bunny chow.

The Finance Ghost: Yeah!

Priscilla Msimanga: So, we sell those and vetkoeks in the morning, to accommodate that market. We also have samosas. We are purely non-pork. If you eat pork, don’t come to us. Because my market is either people who are halal or people who are not eating pork.

We all need to test the market, I started selling pork, and no one bought. And I’m like, “Okay, so what is wrong?” Because I love pork! So, we then saw that it’s either a religious thing. So, then we stopped selling it, and we’re now getting traction. People are buying more.

We sell toasted sarmies, we have burgers and all that. So, yeah. But most of the high sellers are actually food – pap, rice and stew and all that. Mogodu is the high seller on Monday, because people have babbalas, so they want something like mogodu to take away the babbalas [laughing].

The Finance Ghost: Sort them out [laughing]. Ah, that’s great. I have small children, so now I just have ‘Are you achin’ for some bacon?’ in my head, courtesy of The Lion King. A gift that I’ve passed on to them.

But there’s a great story in there. Just because you are achin’ for the bacon doesn’t mean that your customers are. So, you’ve got to then adapt to the people who are actually coming to your store. If pork is not going to cut it, you take it out. You respond to what people want.

It does not help to sell premium croissants to a market that is actually looking for a babbalas cure on a Monday morning and cheap sources of maximum protein and carbs to keep them full. That’s the reality. So, that’s the cool thing with being in retail. It’s also the challenge with being in retail.

Let’s talk a little bit then – because I’ve always wondered about these forecourts. My understanding is that, when you sell a litre of fuel, basically, the amount of money you make per litre is just about fixed. It’s a very highly regulated space around pricing, etcetera.

So, you’ve actually really only got two ways of making more money, because you can’t just put the price of fuel up. You either have to sell more fuel, you’ve got to get more people coming, or you’ve got to get people to get out of their cars and walk into your shop, right?

I mean, that’s what this business comes down to. And I guess at the end of the day, getting people out of their cars is going to be stuff like service, how long it takes to get fuel. But then the shop, again, you need to give people a reason to come there. Like your food truck, etcetera, etcetera. It’s very clever.

So, is that essentially how the business works? Selling fuel is really only one part of it, and the shop is absolutely key to the economics of this thing?

Priscilla Msimanga: The fuel, as in 93 and 95, that’s the case. It’s highly regulated. You’ve got to sell it at the amount that the DMRE sets. Even with diesel. But there is a little bit of space to play around with diesel, because it’s not as regulated as the fuel.

So, you can go down or up, depending on your market. Because diesel is mostly for trucks, and you want to attract the trucks. So, you’ve got to be smart around how you price your diesel so that you still have the market come to you.

And for me, who has two competitors that are literally 900 metres away, I have to be very cognisant of how I price my diesel. It is also very regulated. They tell you how much you can go up by, but then the way that you would want to go down is dependent on you.

So, yes, it is regulated, and there is a margin that we do. There is a RAS (Regulatory Accounting System) model, and I don’t want to get into the technicalities (that I had to learn, by the way, when I got into this) on how much money or how much margin you make.

Then the shop, yeah. Ideally, we want to be able to pump more on the forecourt and also get people out of their cars to the truck or to the shop. Because I still sell pies, so if you don’t want my truck food, we still sell pies and other snacks and carbonated drinks and cigarettes.

So, basically, we are happy to give you the best service, and also, we are happy for you to say to my forecourt attendant, “Hey, can you get me a packet of ciggies when I pay?” And they can do that.

So, we have extended a value for your money kind of service, where you know that it’s a one-stop shop, kind of – not yet a one-stop shop, it will be one day – but you can get your cigarettes and pay at the same time, and this guy will do it for you in the quickest way possible.

Yeah, we do measure. I’m an efficiency kind of person at heart, so I do literally stand outside and see how long people wait, and if there’s no one servicing them, I’m like, “What is going on?” to the person in charge, or I will personally go and assist.

So, you want to get more people in the shop because the shop margins are a little bit different. Because we are a convenience store. We are not priced like Pick n Pay, because of the timing. We are 24 hours. You’ve got to pay two different shifts, as opposed to just one shift for the day.

So, yeah, what we used to do on Saturdays, we used to have boerewors rolls. That is the one that’s built into the truck. Boerewors roll – it smells nice, you see it with my little gas, so you get out of your car and park and buy the boerewors roll. So, those are the kinds of little things that we do.

Sometimes we then partner with some of our suppliers and get little ice creams and give them out on the forecourt so that people come back again.

But the service component is the most important. I want people that I would have tested. These people are passionate, they are proud, and they love serving people. And they like talking to people. People just want to be spoken to. It’s like a salon. When I go to do my hair, the last thing I do is my hair. It’s actually the conversation around what is happening around us.

So, I’ve had quite a few comments, people saying, “Thank you, just for talking to me.” And they are sure to come back. So, those are the kinds of things that my team and I are doing so that people would want to come back to us, as opposed to the other petrol stations.

The Finance Ghost: Boeries and ice creams. You’re definitely speaking my language. That sounds excellent. And the human touch, as you say. Just being friendly. I mean, it’s the basics, but this is what we crave.

We crave human connection – and ice cream, and boeries. And if you can get all three of those right, then you are golden. That’s how it works.

So, Priscilla, without giving away specifics (obviously this is private), but I’m just curious. What has the journey, high-level, been like for you, going from essentially a corporate salary in a big job into your own business? You had to borrow money for it. Would you say it’s been tough? Would you say it’s been in line with expectations? Again, no specifics here. Just high-level, for people thinking of doing this, what’s been your experience of it?

Priscilla Msimanga: So, if you are going into this business, you’ve got to be able to stop living the posh life. There’s no longer any going out and eating out. That has stopped, because your salary is the challenge for you.

You’re paying yourself little. Sometimes you don’t pay yourself at all, if it’s a bad month. So, you’ve got to be able to have a cushion on the side, or you’ve got to have some support, something. Or you have to downscale quite a bit, which I have done.

But for me, it’s a downscaling that you know, in five years, it will pay you back. You know what I mean? It’s just a temporary sort of inconvenience, but you have to be able to take it and be agile enough to adjust to your new reality now. I am not getting that salary that I was getting in corporate. I’m not going to get the 13th cheque. So, how do I balance my life to live the way that I’m living now?

If I were to give you an idea, my salary is not even half of what I used to get in corporate. But I love it. Because at the end of a year, when you look at your financials month-to-month, you’re like, “Okay, so it’s worth it.” At the end of a year, you will see the results, and you’re like, “In five years, I probably will pay myself a little bit better.”

But I think I would do it again. I don’t want to be promising people that you’ll get double your salary, because you won’t – you’ll bankrupt yourself. So, you’ve got to be smart around how you balance.

Because they do manage your expectations, the franchisors, to say, “You’re from corporate, you’re not going to get that salary. How do you balance your finances to still be able to maintain your life?”

Because you’ve got debts and whatever, right? So, you’ve got to package your life in such a way that you’re not going to struggle, but at the same time, you don’t pay yourself so much that you won’t even make a profit.

The Finance Ghost: Thank you. I think that’s a very honest and sobering viewpoint, and that’s why I asked the question. Because I always think people must just go into this with their eyes open.

It’s basically… There’s this quote that goes roughly along the lines of, “Living the life that others won’t, so that you can live the life that they can’t in years to come.” Take the hard stuff now, and it will pay off later.

I’ve always loved cars, and so I had some interesting stuff – nothing crazy at all, I was always careful, but I had some fun stuff. And then, when I finally decided, “It’s time to start getting out of corporate now. This is the opportunity in front of me, let’s do it.” I remember I downscaled all the way down to this leaking Fiat.

Basically, if it had rained, it would leak straight through the door, basically onto me. I was this ex-investment banker and CA in this leaking Fiat, but that’s what you’ve got to do. You’ve got to humble yourself down to that level. Because that tiny little overhead every month is going to make the difference if something goes wrong in the business, while your friend is paying off R15,000 a month on some fancy German car.

And that’s why entrepreneurs actually end up being much better at managing their money, because they don’t take on unnecessary overheads. They go into a cash mindset of, “Okay. Did I already make this money? All right, I’ll spend some of it. I’ll leave behind a buffer, spend some of it, but I had to make it already.”

They don’t go and throw debt at their personal lives. Whereas when you’re a salaried employee, you assume that money’s always going to be there, and then you’re very happy to layer on these big overheads.

And it’s dangerous, because corporates do retrench people. Things don’t always go to plan. And then you’re in serious trouble, because now you don’t have a plan B.

So, as much as it’s hard to go and do what you’ve done, you’re also in control of your own destiny, right? And that’s a nice way to wake up in the morning.

Priscilla Msimanga: Yes, I’ve been retrenched three times in my life.

The Finance Ghost: Wow! Yeah, you know that gig well.

Priscilla Msimanga: So, I know how that feels. I’m driving a 12-year-old car. Everyone asks me, “You’re still driving this thing?” I’m like, “Yes. Until it stops working, I will still drive it.” I’m not going to buy anything that will get me into a position where I struggle right now. If it moves, it moves. I get there!

The Finance Ghost: 100%. I love that. So, last question on this podcast. It’s been such a lovely look at just life leaving corporate. What advice would you give to someone who is maybe thinking about doing this in 2026 or beyond?

Or to someone who’s now maybe at that point, as we spoke about, where you kind of say, “Okay, two to three years from now.” That’s actually the safer runway. If you’re sitting here listening to this and you’re going, “Oh, 2026 is my year to leave corporate,” be careful. It takes longer than that.

So, what advice would you give to someone who’s in that situation? They’re in their corporate job, they’re dreaming of leaving to go and do this thing – what would your one piece of advice be?

Priscilla Msimanga: Stop being fearful. Just jump into it, and start planning today. Because, as you said, the day that you decide, it takes at least two years. So, it’s just a change of mindset. “I’m going to stop being afraid. I’m going to do this.” And now, you start defining the how. You start saving money. You start looking into where you want to go.

It was a collision with petroleum, but I loved it. I think it was meant to happen. I do think that our journeys are supposed to be ‘somewhere’, and you will be ‘somewhere’. But it collided with me, and I love it.

Sometimes people are born with a passion that they are underestimating, and then they die without actually pursuing it. So one day, in 2026, make a decision: “I’m an artistic person, I need to get in to open my art shop.” Start working towards that art shop!

There are a lot of banks that are actually – with a good business case, like Capitec – able to fund you if they see the logic. If they see that you have managed your money properly, and you have a contribution, they’ll be able to help.

I think a lot of people have this comment that, “I don’t have money, it’s a limitation.” Only because you are fearful. So, if you stop being fearful, then you look at possibilities. You can see that it is possible if you really, really want to do it. And that is where I was.

I would say, “Stop being fearful. Pursue what you love, and go for it.” Even if it doesn’t yield the result in two days. Because I was an impatient person. I think the one thing that this business has taught me is to be patient.

The waiting game. In four years, three years, whatever, it will be a different thing. Just hold on. And when they listen to this kind of podcast, they’ll be able to see that it can be done. If a dusty kid from Sebokeng can do this, anyone can, really.

Just go above the fear. And leave corporate. And I know I used to be one of the execs, and I’m like, “Oh, yeah, it’s prestigious,” but for whom? For me, now, I’m prestigious to me. I’m the one who makes decisions, and that’s different.

So, when you’re in corporate, you’re working for someone else who had the dream to do what they are doing, and they hire you to do it for them. So, in my opinion, I’m better off doing my dream than working for someone else’s dream. So, dream, go for your dream, and stop being fearful.

The Finance Ghost: I love that. Loads of great advice in there. It’s funny, so my thing is being able to fetch my kids from school without having to ask someone. That’s the biggest win for me. It’s not even about the money or whatever. It’s literally just the freedom.

The richest person you know is the person who has the most control over their time. That is my honest opinion on the world, really.

Priscilla, have you read The Alchemist before? Because if you haven’t, you should.

Priscilla Msimanga: Yes, I have read The Alchemist, funnily enough. It was like 14 years ago! [laughing] I still have it. I go back to it. So, yes, I have.

The Finance Ghost: You struck me as someone who should read it. And for anyone listening to this, there really are two types of people who read The Alchemist. There are those who read it and go, “I don’t understand the hype, what is this?” Then it just wasn’t for you, that’s fine. And then, if it is for you, it will really be for you.

So, I was one of those people where it was really for me. I took a lot from The Alchemist. I remember reading it on a flight between Joburg and Cape Town – a late-night, very tired, hardcore-financial-services-career flight, and I read The Alchemist.

And I remember” I basically read it, closed it, and that was the start. It ended up being much more than two to three years, but that was the start of me going, “Okay, I need to do something else long term.” So, yeah, it’s a lovely thing.

Priscilla Msimanga: There are just those books that never leave my shelf, and The Alchemist is one of them. Rich Dad Poor Dad is one of them. It’s just those that always remind me, “You know what? These people could do it. I can too.”

And there are people that have poured into me as well that would say, “You can do this,” and I’m like, “Okay, okay.” And so, yeah. But The Alchemist was one of them.

The Finance Ghost: It’s fantastic. So, there’s a dog in the background there that is calling you to go and run your business, so I’m going to let you go, Priscilla.

Priscilla Msimanga: [laughing]

The Finance Ghost: Thank you so much. We were done anyway, but it has been lovely. Thank you so much. We’ll take the dog’s hint here.

And just, good luck. Well done on everything you’re doing. It’s a very inspiring story, and I really wish you the best with it.

The World Economic Forum Annual Meeting is here and markets are paying attention. As leaders gather in Davos, the conversations will likely shape risk premiums, capital allocation and investor confidence in the months ahead. In episode one of our special Davos Debrief podcast series, host Jeremy Maggs is joined by Chris Holdsworth, Chief Investment Strategist at Investec, to cut through the noise and focus on what really matters for investors.

Please scroll down if you would prefer to read the transcript.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Also on Apple Podcasts and Spotify:

NOW Ep 117: WEF 2026 Preview

[00:00:00] Jeremy Maggs: It is World Economic Forum Week. Markets are open, capital is moving, and in Davos, the conversation this week will help shape where risk is priced and where opportunity emerges. This is No Ordinary Wednesday, Investec’s fortnightly podcast on the forces shaping business, markets and economies. Hello, I’m Jeremy Maggs, and this week it’s a special Davos debrief series.

I’m going to bring you insights from Investec leaders attending the 56th annual meeting in Switzerland. Now, today marks the start of WEF 2026, convening global leaders under the theme, “A Spirit of Dialogue”. But the backdrop is anything but calm. The Global Risks Report 2026 warns that geo-economic confrontation has become one of the most pressing near term threats to global stability.

At the same time, the Global Cooperation Barometer 2026 tells us that cooperation across geopolitics, technology, and trade is weakening precisely at a time when systemic risks are rising. So as Davos gets underway, what signals should markets be watching and which conversations rarely matter? To help us unpack the risks, the opportunities, and what this week could mean for markets and the global economy, I’m joined by Chris Holdsworth, Chief Investment Strategist at Investec. Chris, a warm welcome to No Ordinary Wednesday.

So let’s start with this then. The Global Risks Report 2026 ranks geo-economic confrontation as the top risk over the next two years. That’s ahead of even state-based armed conflict. Chris, how should investors then interpret that finding, particularly in relation to trade tensions, tariff tensions, or supply chain nationalisation?

[00:01:49] Chris Holdsworth: I think the essence of that report is that we’re seeing a shift away from cooperation to competition amongst major economies and tariffs are an example of that. And one of the key questions that we need to answer this week, and we hope to get some guidance, is around how persistent that is likely to be.

Is it the next two years, three years, five years? Is it a long term trend or is this something that is just cyclical for the short term? And if so, what are the other consequences that are likely to come about in addition to tariffs that we need to be concerned about? And I think we will get some hints in that regard and certainly something that we’ll provide an update on throughout the week as we get information, but for us, that’s pretty close to the top of the list of things that we are looking out for.

[00:02:28] Jeremy Maggs: So let me ask you a follow up to that. Does this shift in risk weighting from traditional geopolitical fears to geo-economic friction maybe change how we think about capital allocation and diversification?

[00:02:42] Chris Holdsworth: Yes, it’s a great question. I think the primary concern is around the extent to which the dollar continues to be a safe haven for international investors. There’s a shortage of safe haven assets across the globe, and if the dollar is not going to be the sort of safe haven that it was before, it means that we need to find other safe havens and we will be looking out for any information with regards to that potential issue.

[00:03:03] Jeremy Maggs: And Chris, are markets pricing this opportunity appropriately do you think? Or are investors underestimating the economic side of global risk?

[00:03:11] Chris Holdsworth: You know, it’s hard to say that markets are pricing in a lot of risk when the US stock market’s on a forward P/E of 23, which is pretty close to the top end of the range of what we’ve seen over the past 30 years. It does seem that the market’s pretty relaxed and we can understand why US GDP growth has been pretty good and earnings growth has been pretty good as well.

But there is a cloudy outlook, and I would suggest that there’s not a huge amount of risk currently priced in to US equities in particular. Elsewhere it’s a bit of a different story, but certainly in the US it seems like a lot of these risks are being put on the back burner for now.

[00:03:43] Jeremy Maggs: Alright, let me move on to this.

The Global Cooperation Barometer 2026 suggests cooperation is weakening even as risks intensify. So Chris Holdsworth, in your view then, are we in a world that is genuinely de-globalising or is the narrative more about reorganisation, maybe new partnerships, new corridors of capital and trade?

[00:04:07] Chris Holdsworth: Depending on the data sources, you look at. Trade over the past couple of years has been flat to up a little bit, but in effect, no sign of deglobalisation in the trade data just yet. Clearly there are threats to that. In summary, I think we are looking at an environment where the world is just a lot more complicated.

We can’t simply rely on past economic relationships between countries to continue going forward. And that just makes asset allocation a lot more complicated than it has been before. And in general, it makes investing a lot more difficult than it has been before. And again, we are going to be looking out for any information in that regard.

So we’ve put together a list of a couple of things and I’m sure we’ll talk about that shortly, and this will feature on that list too.

[00:04:47] Jeremy Maggs: So what then are the investment opportunities and risks in a more multipolar or contested economic order?

[00:04:55] Chris Holdsworth: Well, the first question is if the dollar’s not going be the safe haven that it was before, is there a substitute?

Is there something else that can offer the sort of protection for portfolios that dollar investments used to? And maybe it will be the dollar again in a couple of years, but maybe we need to try for something else. And I think that goes somewhere in expanding the recent, very strong performance in gold.

And there is a shortage of safe haven assets. And this is top of the list for investors across the globe, and again, top of the list for us this week in Davos.

[00:05:24] Jeremy Maggs: Now Chris, one of the central pillars of Davos 2026 is, as I understand it, unlocking new sources of growth, all well and good. Where do you see growth potential right now, both in developed economies and in emerging markets like those in Africa?

[00:05:41] Chris Holdsworth: Well, one underreported new development we think is that GDP growth in Africa this year is likely to outpace Asian GDP growth which doesn’t often happen. If you look over the last 30 years, it’s occurred on a handful of occasions. Now what’s more is that the IMF expects going forward, African GDP growth will be above Asian GDP growth for each of the next five years.

So we are on the cusp of a regime change and it means that the longstanding promise of faster African growth may well be delivered. And so if we are looking for new sources of growth, I think we should look probably not much further than the African continent.

[00:06:16] Jeremy Maggs: So are certain sectors like technology, energy transition, or even digital infrastructure maybe better positioned to capture this growth?

[00:06:26] Chris Holdsworth: Well, one of the problems is that there are very few ways to neatly access faster GDP growth in financial markets. So if you look for example, at listed entities in developed markets, typically Africa is a very small portion of their revenue. Even in South Africa, there’s only a handful of companies that are direct plays on Africa x SA growth and that makes it quite difficult. So we first need to see increased access for investors to the African continent, and that’s going to take a bit of time. That would be the initial stage of what could be a very long running theme, and it’s something that could be quite exciting and we hope to start to see some developments in that regard over the near term.

[00:07:03] Jeremy Maggs: Now, Chris, another key theme this week is deploying innovation responsibly. Now in a world where technological disruption can rapidly reshape industries and where risks from ungoverned tech rise over longer horizons, Chris, how should investors balance their innovation upside on the one hand with systemic risk exposure?

[00:07:25] Chris Holdsworth: That’s a very difficult question. I know there are a couple of talks this week on that, and so hopefully we’ll get some insights this week. I mean, one of the thoughts is that the development of AI in effect is going reduce barriers to entry, reduce moats, which means that higher quality companies, which have typically enjoyed barriers to entry and higher moats would be derated. And perhaps we’ve seen a bit of that over the past six months or so.

We are not going to get an answer to that question at the end of this week, I don’t think. Not a full answer, and we probably won’t get an answer to this question for the next couple of years, but hopefully we get some insight with regards to the problem that you’ve raised.

And if so, we’ll certainly report back in the follow-up sessions.

[00:08:02] Jeremy Maggs: Now Chris, the World Economic Forum Agenda, also emphasising building prosperity within so-called planetary boundaries. So for investors, looking beyond short-term returns, how do you think about resilience, whether for portfolios, for businesses or economies in the face of the risks highlighted in those two reports that we’ve mentioned?

[00:08:25] Chris Holdsworth: You know, this is a longstanding theme, the need to invest sustainably and responsibly. The theme is not particularly popular at the moment. It’s certainly less popular than it was a couple of years ago, but we do think that it’s going to come back into fashion over the next couple of years. And just like the AI theme, which is likely to play out over the next decade or so, we think that this theme is likely to play out over the next few years.

[00:08:47] Jeremy Maggs: Now as the week begins, what are the three signals or outcomes that you’ll be watching closely over the next couple of days that could shift market sentiment or reshape investment assumptions?

[00:09:00] Chris Holdsworth: Well, as a starting point, if you look back over time, there have been a number of World Economic Forums where there’s been market-moving commentary, particularly from central bankers with regards to the outlook for monetary policy. This time around the focus is more likely to be on geopolitics, but nonetheless, this is something that’s going to be pretty closely watched by investors across the globe, and everyone’s going to have their list of things that they’re looking out for.

In terms of our list, top of the list is to the point we mentioned earlier about the safe haven status of the dollar, and any information in that regard.

The second is around resource nationalism. This relatively new development that’s come about with regards to rare earths, but it also applies to other resources more broadly, and we’re looking out for any information in that regard.

And the third is questions around Central Bank independence, particularly in the US. Now that’s just the top of our list.

We’ve got to be open to the idea that there may well be other commentary coming through, that’s out of left field that are market-moving as well. So we might not get answers to our top three. Hopefully we do, but I think we will get some information out there, even if it’s not something that we are expecting at this point.

[00:10:03] Jeremy Maggs: Alright, I want to bring South Africa into the picture now. Team South Africa is in Davos, positioning this country as reforming, stabilising, ready for partnership. From an investment perspective, how material are these signals in a world, Chris, where capital has become, I think, far more risk selective?

[00:10:23] Chris Holdsworth: That’s absolutely critical there. There’s still a pretty widespread scepticism about the recovery story in SA, and it’s going to take more delivery to change views and talking to people is one thing, and talking about commitments is one thing, but at this point we need to see signs of delivery and you need to evidence that delivery and you need to make it public.

And this is a platform to do that.

[00:10:43] Jeremy Maggs: Now Chris, a recurring theme in the team South African narrative is that the country has moved from policy intent to implementation, particularly through Operation Vulindlela, energy reform and logistics modernisation. As a strategist, how do you then distinguish between reform rhetoric and reforms that can actually unlock capital?

[00:11:05] Chris Holdsworth: Now this is pretty important for us. A couple of years ago, we created our own SOE index to measure the performance of SOEs in South Africa. And the reason we did that is the realisation that SOEs at that point were a binding constraint on GDP growth in South Africa. And if you look at that index, it bottomed around 2023.

And since then there’s been a sizable recovery, and we can see that through electricity production as an example. We can also see it through the performance of container handling at the ports. So there’s signs that things are turning around. And what that means is SOEs are less of a binding constraint on growth, and that allows GDP growth to drift upwards.

We may even see it at 2% this year. And the more we see signs of delivery in that regard, the more we see signs of structural form actually leading to better results, the more likely we are to see a reduction in the risk premium in South Africa.

[00:11:55] Jeremy Maggs: Alright, Chris, a final question for you then, as investors wake up to this first day of Davos 2026, looking at a world, as we’ve discussed of elevated global risk, weaker cooperation, but also new growth corridors, is there one thing they should be watching this week when it comes to South Africa’s positioning in global portfolios?

[00:12:17] Chris Holdsworth: I think it’s the extent to which South Africa is relevant and desirable for foreign investors. And that’ll take a combination of things. It’ll take a combination of policy certainty, reform and signs of green shoots to convince foreigners to bother to look at SA. And there might still be some questions around foreign policy and the extent to which that affects the outlook for growth in SA, but I think the primary point is going to be trying to address investors scepticism about the recovery story in SA.

[00:12:45] Jeremy Maggs: And that’s where we are going to leave it. Chris Holdsworth, thank you for that big picture outlook and for helping us prepare for what promises to be a critical Davos week.

In episode two that drops on Wednesday the 21st of January, we’re going to explore technology, artificial intelligence, and the future of work with Investec’s Global Head of Digital and technology, Lyndon Subroyen.

Until then, thank you for listening.

Now remember to follow Investec Focus Radio SA wherever you get your podcasts. And if you like the channel, please take a moment to rate it and share it as this will help us reach more listeners. Until next time, goodbye from me, Jeremy Magsg and the entire Focus Radio team.

[00:13:29] Disclaimer: The views expressed are those of the contributors at the time of publication and do not necessarily represent the views of the firm and should not be taken as advice or recommendations. Investec Limited and subsidiaries authorised financial service providers, registered credit providers, and long-term insurer.

This comes after the share price lost roughly half its value in the past year

The Aveng share price has been a rather sad and sorry tale. They’ve been struggling with the Australian business McConnell Dowell (haven’t we heard that story many times before on the JSE?) and they went through a strategic process of figuring out how to separate it out from the group. After investors hoped for news of a value unlock, what they got instead was an update in December that Aveng would be hanging onto McConnell Dowell.

There’s also a potential sale of the South African business (Moolmans) on the cards. They recently appointed a new managing director in that business, which is an unusual step when you’re trying to sell something.

I don’t know what else has happened in the background, but it seems as though there’s unhappiness and disagreement in the system as the CEO has decided to part ways with the company. Scott Cummins will step down with effect from 30 January 2026 – that’s just one step short of an immediate change.

David Simpson will be appointed as the interim group CEO. Although the announcement gives lots of vague commentary about his previous roles, it neglects to indicate which companies he has led before.

The company has also begun the search for a permanent CEO. Interim appointments often become permanent after due process has been followed, but not always.

Results for the six months to December are expected around 24th February. That’s going to be rather interesting.

The share price fell 6% on the day of the announcement.

Ninety One’s share price is up by well over 50% in the past year. It closed 7% higher on Friday based on the assets under management (AUM) update. For a company like this, AUM is the lifeblood of revenue, as it is the basis upon which fees are earned. When AUM is heading in the right direction, the share price tends to do the same.

The AUM figure at 31 December 2025 of £159.8 billion is a meaty 22.7% higher than it was at 31 December 2024. The amplified impact on the share price is thanks to better sentiment towards the business and the positive impact on margins of achieving growth like this.

Recent momentum is also encouraging, as AUM is 5% higher than it was at the end of September 2025.

Shareholders will want to see more of this as Ninety One closes out their financial year in the next quarter.

Nibbles:

Director dealings:

Several executives at Life Healthcare (JSE: LHC) received share awards and took different courses of action. Encouragingly, it looks like the CEO hasn’t even sold the taxable portion, choosing instead to keep the full R3.3 million in shares. Two other directors sold only the taxable portion (the usual approach). Also, there were two senior execs who sold previously vested shares worth a total of roughly R10 million.

A senior exec at Investec (JSE: INL | JSE: INP) sold shares worth around R7.7 million.

Remgro (JSE: REM) has renewed the cautionary announcement related to a potential restructuring of the Mediclinic investment. You may recall that the intention here is for Remgro to take full ownership of Mediclinic Southern Africa, while the Swiss partners would then take full ownership of the Swiss business. Negotiations are still underway. It’s lovely to see an intention to increase exposure to South Africa rather than a desire to deploy more capital offshore!

After a long, painful and rather worrying process to get the deal done, Shuka Minerals (JSE: SKA) must be thrilled to announce that the acquisition of Leopard Exploration and Mining has now closed. This means they have 100% ownership of the Kabwe Zinc Mine. This is of course only the beginning – like all junior mining projects, it will be a capital hungry process.

Both are footnotes in a much older human habit: wanting something most when we’re told it’s off-limits.

Humans are curious creatures. Tell us something is forbidden and suddenly it’s the only thing we want to see. Hide information and we’ll dig for it. Try to erase something and we’ll screenshot it, repost it, remix it, and turn it into a meme before the PR company has finished drafting the apology statement.

Psychologists have a term for this tendency. The internet does too. And Barbra Streisand, somewhat unwillingly, gave it a name and a face.

A photo nobody cared about (until everybody did)

The year was 2003, and photographer Kenneth Adelman was flying over the Californian coastline in a helicopter. His goal wasn’t voyeurism. Adelman was working on the California Coastal Records Project, a nonprofit initiative designed to document coastal erosion. The series of photographs that he was taking were publicly available, free for non-commercial use, and frequently accessed by researchers and government bodies.

Among the more than 12,000 images that Adelman uploaded was one that happened to include Barbra Streisand’s Malibu mansion. At the time, almost no one noticed. But somehow, Streisand got wind of this and decided to sue.

Citing privacy concerns and legitimate fears around harassment and stalking, she filed a $50 million lawsuit against Adelman, arguing that the photograph exposed details of her residence and therefore endangered her safety. From her perspective, the move made sense. Remove the image, reduce the risk, regain control. It’s worth noting that at the time of the lawsuit the image in question had been downloaded only six times, and two of those downloads were by Streisand’s own legal team.

Streisand and her lawyers hoped that the photograph would quietly disappear and the world would be none the wiser. Instead, the lawsuit did something remarkable: it turned a mostly ignored aerial photograph into one of the most famous celebrity property images on the internet.

Within a month of the filing, the photo had been viewed more than 400,000 times. News outlets republished it. Blogs dissected it. People who had never heard a single Barbra Streisand song suddenly knew where she lived and what her house looked like from above. As if that wasn’t bad enough, Streisand also lost the case and was ordered to pay Adelman’s legal fees. The photo remains online to this day.

Years later, in her 2023 autobiography My Name Is Barbra, Streisand reflected on the episode with candour. Her issue, she explained, was never the photo itself – it was the attachment of her name to it. She believed she was standing up for a principle. In retrospect, she admitted, it was a mistake.

Why suppression so often backfires

The phenomenon now commonly known as the Streisand effect describes what happens when attempts to suppress, censor, or remove information end up amplifying it instead. In other words, the harder someone tries to make something disappear, the more attention it attracts.

This isn’t just an internet quirk. It’s a deeply human one. Attempts to control information have existed for as long as information itself. Books have been banned, artworks destroyed, speeches silenced. What’s changed since the advent of the internet is the speed and scale with which information can be accessed and shared. Online suppression doesn’t just fail quietly – it fails spectacularly.

Cease-and-desist letters are a common starting point. A polite but firm “please remove this content” lands in someone’s inbox. Sometimes it works. But often, especially when the request feels heavy-handed or unjustified, the result is the opposite. The letter gets shared, screenshots circulate, and in no time at all, the story becomes news.

Seeking an injunction to remove content can trigger the same effect. The legal action itself becomes a story, and the content you hoped to bury gets a second, louder life in headlines, think pieces, and social feeds.

When banning makes things more popular

One of the clearest demonstrations of the Streisand effect comes from an unlikely place: libraries. A study examining banned books in the United States found that titles on the banned list saw their circulation increased by an average of 12% compared to similar, non-banned books. It makes sense if you think about it – the act of banning signals scandal. If this book was dangerous, controversial, or forbidden, then it must be worth reading. It turns out the best thing an author can do to sell books in the US is to write something so controversial that it ends up on the banned list, but not so controversial that it alienates readers completely!

It’s not just the contents of forbidden books that get us salivating – we even go crazy for illegal numbers. This is what happened in 2007, when companies using Advanced Access Content System (AACS) encryption attempted to suppress a 128-bit numerical key that could be used to decrypt HD DVDs.

Not exactly a salacious or particularly interesting piece of information on its own, is it? The companies issued cease-and-desist letters demanding the key be removed from high-profile sites like Digg. What followed was internet folklore: the number spread everywhere. It appeared in forum signatures, chat rooms, blog posts, and comment sections. It was printed on T-shirts, tattooed onto bodies, and turned into songs on YouTube.

By the afternoon of Tuesday 1 May 2007, the number was still relatively contained. A Google search for the encryption key returned just over 9,000 results. By the following morning, that figure had exploded to nearly 300,000. By Friday of the same week, the BBC reported that almost 700,000 webpages were hosting the key. This was despite – or rather, because of – the fact that two weeks earlier the AACS Licensing Authority had sent Google a DMCA notice demanding that the search engine stop returning results for it.

A few years later, the same dynamic played out on a much larger, messier stage. In 2012, a UK high court ordered five major internet service providers to block access to The Pirate Bay, the Swedish file-sharing site that had long irritated copyright holders and governments alike. The ruling was meant to curb piracy by making the site harder to reach, effectively cutting it off at the source. Instead, it functioned as a global publicity campaign.

News outlets around the world reported on the ban, often explaining in detail what The Pirate Bay was and why authorities were so eager to shut it down. Curious users who had no idea that it was possible to (illegally) download films off the internet went looking for the site. Seasoned users shared workarounds, mirror links, and VPN tutorials with missionary zeal. Within days, traffic to the site had surged, increasing by more than 12 million visits.

Clearly, blocking access didn’t eliminate demand. In fact, we could argue that getting sued was the best marketing result that The Pirate Bay team ever achieved. The attempt to close the door simply taught millions of people where the door was and how to slip through it.

The people will not be denied access

The Streisand effect isn’t really about celebrities, pirates, or encryption keys. It’s about control, and our instinctive resistance to losing it. The moment someone tries to decide what we’re allowed to see, know, or talk about, curiosity turns into defiance. Information becomes more than data; it becomes a symbol. And accessing it feels like reclaiming agency.

In a reality where information moves faster than authority ever can, silence is no longer enforced – it’s negotiated. And more often than not, the loudest thing you can do online is try to make something go away. Barbra Streisand didn’t invent human curiosity, and the Swedish founders of The Pirate Bay didn’t perfect it. They simply revealed an uncomfortable truth of the digital age: attention is stubborn, curiosity is contagious, and once the internet smells secrecy, it cannot look away.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

In July 2025, Hyprop announced the sale of a 50% undivided share in Hyde Park Corner, along with the option to dispose of the remaining 50%. The proposed purchaser was a wholly owned subsidiary of Millennium Equity Partners.

In my opinion at least, Hyde Park Corner is one of the more interesting and unusual retail spaces in Joburg. Genuinely iconic and with great positioning, the centre includes a solid mix of upmarket offerings. Perhaps I’m just biased because there’s an impressive bookstore. Either way, I think it’s a solid property to own that was made even better by the recent opening of a Checkers FreshX store.

That positive view on the centre is just as well, as the deal to sell the share in the property has fallen through due to lack of fulfilment of conditions precedent. The announcement doesn’t specify which conditions weren’t met. This means that Hyprop shareholders will continue to have exposure to this mall in the absence of any other offers coming through.

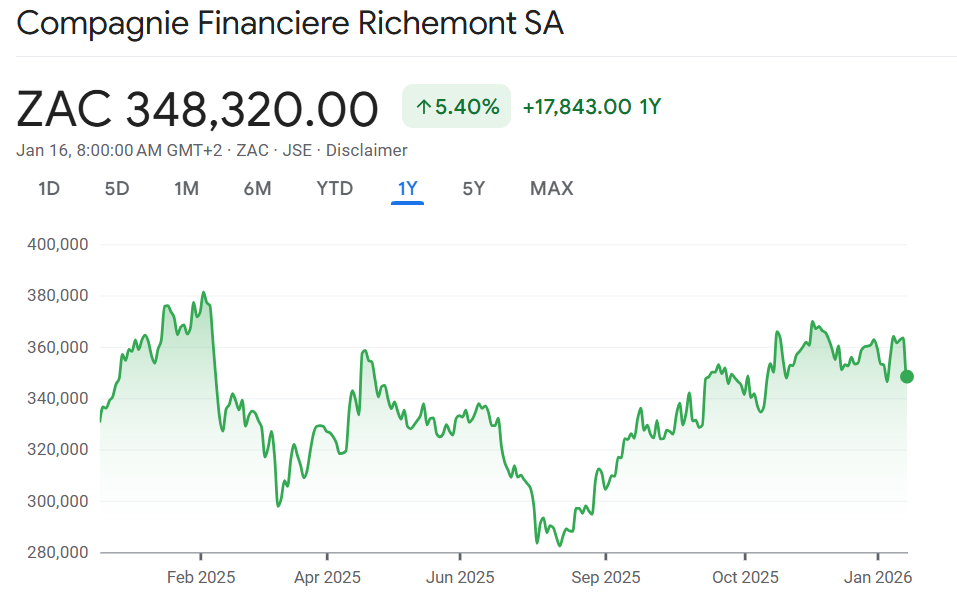

Currencies are having a huge effect on Richemont (JSE: CFR)

The dollar and yen are the worst offenders

Richemont released a sales update for the three months to December 2025, which is of course the all-important festive period. Sales were strong on a constant currency basis (up 11%), but this was diluted down to just 4% growth as reported in euros. Global geopolitical strain is having a serious effect on Richemont’s numbers.

Before we get to the currency effects, let’s deal with the momentum through the year. This quarter was slightly stronger than the nine-month results on a constant currency basis (11% Q3 vs. 10% YTD) and slightly lower as reported (4% Q3 vs. 5% YTD). This tells us that the the business itself is getting better, yet the geopolitical impacts are getting worse.