Long before racing circuits, luxury sedans, and million-dollar dealerships, there was one woman who quietly steered the Mercedes-Benz brand into the world’s imagination. Her name was Bertha Benz, and she was the first person to attempt a long-distance drive in a motorcar.

Bertha Ringer was born on 3 May 1849 in Pforzheim, in what was then the Grand Duchy of Baden. She was the third of nine children in a wealthy household. Her father, Karl Friedrich Ringer, made his fortune through carpentry and real estate speculation, while her much younger mother, Auguste, managed their bustling home.

As such, Bertha grew up surrounded by comfort and opportunity. She attended boarding school for a decade (an unusual privilege for girls at the time), where she developed a sharp mind and a keen curiosity about science and technology. Yet, like so many ambitious women of her time, her path was limited by law and custom. Universities were barred to her, and engineering was a closed door.

Still, Bertha was determined to be more than a housewife or a pretty society ornament. And while that determination was frowned upon at the time, it would later prove to be historic.

Enter Carl Benz

On a summer excursion in 1869, Bertha’s brother introduced her to a man named Carl Benz (his preferred spelling of Karl). He was five years older than her, penniless, and obsessed with machines. Bertha fell in love immediately. While Carl wasn’t smooth with words of love, he could talk endlessly about engines and mechanics. Where others saw a dreamer on the verge of failure, Bertha saw a man that she wanted to build things with.

In 1870, before they were married, Bertha invested part of her dowry into Carl’s struggling iron construction company. At that time, German law allowed an unmarried woman to make such decisions, but once married, she would lose that right. The investment kept Carl afloat and gave him room to pivot toward his true passion, which was building a “horseless carriage”.

When the two married in July 1872, they became more than husband and wife. They became co-inventors and business partners.

A dream in motion

The Benz’s early years were anything but easy. As their family grew, the couple lived under constant financial strain. In 1875, when Bertha was pregnant with their third child, debt collectors emptied their workshop overnight. Yet they persevered, and on New Year’s Eve in 1879, the breakthrough came when Carl and Bertha managed to get a two-stroke engine running. After years of tinkering, trial and humiliation, they were finally closer to realising Carl’s dream.

By December 1885, the first Patent-Motorwagen was complete – a three-wheeled contraption with a single-cylinder engine, spoked wheels, and a folding top. Carl secured a patent the following year for what would later be recognised as the world’s first automobile.

But there was a problem: nobody cared.

Carl Benz was an inventor, not a salesman, and his car looked fragile, noisy, and impractical. Wealthy Germans preferred their elegant carriages, pulled by reliable horses. Meanwhile, Gottlieb Daimler was emerging as a competitor with his own designs.

Carl was discouraged. Bertha, however, was not.

The forbidden journey

On 5 August 1888, 39-year-old Bertha quietly rolled the Model III Patent-Motorwagen out of their workshop in Mannheim. She set off at dawn without telling her husband, with only her two teenage sons, Richard and Eugen, to accompany her. Their destination was her mother’s home in Pforzheim, 106 kilometres away.

Officially, she was visiting family. Unofficially, she was staging the greatest marketing stunt of the century.

Up until that point, motorcars had only been tested in short loops, always close to workshops and with mechanics on hand. Bertha’s audacious idea was to prove the Motorwagen could handle a real journey through towns, over hills and across the countryside, and that it could be operated by anyone – even a woman (a big deal in those days).

Of course, the going wouldn’t be easy, but fortunately Bertha was a top class problem solver. Instead of a fuel tank, the Motorwagen had only a tiny carburettor with a 4.5-litre capacity. When it ran dry, Bertha stopped at a pharmacy in Wiesloch to purchase ligroin, a petroleum solvent. The apothecary that sold it to her unwittingly became the world’s first petrol station. When a fuel line clogged, Bertha unclogged it with her hat pin. When wiring needed insulation, she used her garter. A small-town blacksmith was enlisted to mend a broken chain, and when the wooden brakes wore thin, she persuaded a cobbler to nail on strips of leather, thereby creating the world’s first brake linings.

The car’s two gears weren’t enough for steep inclines. On hills, her sons had to get out and push. The engine’s cooling system demanded constant refills, so they collected water at every stop.

On top of all of that, the roads themselves were hostile. Designed for four-wheeled wagons, they rattled the Motorwagen’s narrow front wheel over stones and tufts of grass. With no road signs in place, Bertha navigated by memory and instinct. The trip was technically illegal, since she had no permit to test the vehicle, and incredibly dangerous.

And yet, after a full day’s journey, Bertha and her sons arrived safely in Pforzheim at dusk. She promptly sent her husband a telegram announcing their safe arrival. Days later, they drove the Motorwagen back to Mannheim, triumphant.

A turning point

The impact was immediate. Newspapers both local and international picked up the story, and crowds gathered wherever the Motorwagen appeared. Suddenly, people could imagine what this noisy, smelly machine might mean: a carriage that didn’t need horses, a vehicle that could carry families across distances, a new era of mobility.

Bertha’s field test also revealed a host of practical improvements. She had made detailed notes during her journey, and assessed that more gears, better brakes and more durable materials were required. Carl took Bertha’s suggestions seriously, and the car evolved. Most importantly, sales began.

Within a few years, Benz & Cie. was the world’s largest automobile company. By 1926, it merged with Daimler and Maybach to form Daimler-Benz, home of Mercedes-Benz. The global automotive industry owes much of its existence to Bertha and her daring drive.

Recognition at last

Carl Benz lived long enough to see the success of his invention. He died in 1929, during the Great Depression, just two years after the Daimler-Benz merger. In his memoirs, he credited his wife with saving not just his company, but his spirit:

“Only one person remained with me in the small ship of life when it seemed destined to sink. That was my wife. Bravely and resolutely she set the new sails of hope.”

Bertha herself lived to the ripe age of 95. On her birthday in 1944, she was named an Honorary Senator of the Technical University of Karlsruhe – the same university that had barred her from study as a young woman. She died just two days later, in her home in Ladenburg.

It took decades for the world to fully acknowledge her role. Carl was inducted into the Automotive Hall of Fame in 1974. Bertha followed only in 2016, 42 years later. But history has caught up. Today, the Bertha Benz Memorial Route traces her historic journey through Baden-Württemberg, celebrated by motorists retracing the path where the first long-distance drive once rattled over cobblestones.

Carl Benz may have built the car, but Bertha Benz put it on the map.

On that August morning in 1888, she did more than visit her mother. She proved that the automobile had a future. She marketed it, tested it and improved it, all in one audacious journey.

In honour of International Women’s Day in 2019, the Daimler company commissioned a truly excellent four-minute film dramatising portions of Bertha Benz’ 1888 journey. You can see it here:

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

The Bytes share price chart is an incredible way to be slightly down year-to-date (JSE: BYI)

Talk about a rollercoaster ride!

If someone told you that they were down 2.8% year-to-date in a stock, you probably wouldn’t expect to see something quite like this:

Those who managed to get in at the bottom have done nicely, although there was a scary dead cat bounce just after the precipitous drop. Trading is fun, but hard.

Underneath all this, we have Bytes Technologyas an example of a broken growth stock. It’s not really a broken company of course, but it’s certainly broken in terms of the growth expectations that the market used to have.

They are dealing with structural changes to their business that have led to words like “resilience” when describing the performance in the latest half-year trading update – not the kind of language that growth investors want to see.

The update notes that gross invoiced income for the six months is expected to be around £1.33 billion, which is ahead of £1.23 billion in the comparable period (not that the announcement bothers to give comparatives – you have to go digging). The problem is that despite this growth, gross profit is expected to be “not less than £82 million” (i.e. not less than what they managed last year) and operating profit is expected to be not less than £33 million. The prior year was £35.6 million, so there’s chance of a small dip in profits.

When a company needs to rebuild trust with the market, an announcement that just gives numbers without comparatives or a reminder of the guidance at the AGM isn’t good enough. Given the previous management scandal at Bytes and now the lack of growth under new management, they should be falling over themselves to make things easy for investors to understand, even when it’s a tough message to deliver.

Finbond swings into profits (JSE: FGL)

Yay for an early trading statement!

Finbond has released a trading statement for the period ended August 2025. Results are due to be released on 31 October, so they’ve done the right thing here and released a trading statement that gives investors plenty of advance warning.

It’s easier of course when you know that there’s a huge move in HEPS, but that’s exactly the point with a trading statement – the bigger the move, the earlier the trading statement should come out.

In this case, HEPS has increased by more than 100%, swinging from a loss of 2 cents per share to positive earnings of at least 0.5 cents per share.

Lighthouse adds the hypermarket at Espacio Mediterraneo to the deal (JSE: LTE)

Initially, it looked like the current, separate owner would be keeping it

Back in June this year, Lighthouse Properties announced the acquisition of Espacio Mediterraneo in Spain, adding to the portfolio in the Iberian Peninsula. The property has a large hypermarket in it (currently occupied by Carrefour) that was excluded from the deal due to its separate ownership.

Lighthouse has managed to persuade the owner to part with the hypermarket for €19.5 million, which is a net initial yield of 7% (excluding transaction costs). I can understand why owning the entire mall is much easier from a management perspective than having a separate owner of the hypermarket unit.

Despite the name, SA Corporate Real Estate holds various property types – even residential (JSE: SAC)

And the interim results tell a positive story

The property sector seems to be a pretty consistent source of growth at the moment. Most companies are growing their distribution at a rate above inflation, while some have achieved outstanding growth at much higher levels. The sector would’ve loved to see an interest rate cut this week, but alas it seems as though the SARB loves watching South Africans live life on hard mode.

In the meantime, the property sector (like all South Africans) must keep grinding away. SA Corporate Real Estate has a diverse property portfolio that managed like-for-like net property income growth of 4.9% in the six months to June 2025, along with a 7.5% increase in the distribution per share. This increase was partially due to the payout ratio being 92.5% vs. 90.0% in the comparable period, so just be aware of that – there’s only so far that a payout ratio can be pushed.

The loan-to-value ratio improved from 42.0% as at December 2024 to 40.3% by June, assisted by a significant asset disposal programme. Combined with a decrease in the weighted average cost of funding, this boosted earnings.

Perhaps the most unusual thing about SA Corporate Real Estate is the residential portfolio. Along with the types of properties that you’re used to seeing in listed funds, the company has what can only be described as buy-to-let at scale – and my head hurts just thinking about it, particularly as these are inner city properties in places like Joburg. While enjoying the rental income in the meantime, they are looking to sell over 3,000 units over the next three years. The sales thus far have been 60% above cost and 20% above book value, so they will hope for this trend to continue.

Here’s an interesting nugget from the results: “The redevelopment of Montana Crossing is now complete, with the introduction of Checkers Fresh X, Checkers Liquor and Petshop Science as anchor tenants replacing Pick n Pay. The Group anticipates a 30% uplift in the rental income of Montana Crossing for the 2026 financial year as a result.”

If you look at the property funds, you learn so much about retail. Whilst Pick n Pay (JSE: PIK) may shrink into a sustainable business, my view is that they will never regain the lost ground. Shoprite (JSE: SHP) is just sailing off into the sunset from a market share perspective.

Finishing off with SA Corporate Real Estate, the fund expects distributable income per share growth for the full year of between 4% and 5%. Thanks to the higher payout ratio, the distribution per share is expected to be between 7% and 8% higher.

Nibbles:

Director dealings:

Des de Beer bought more shares in Lighthouse Properties (JSE: LTE), this time to the value of R5.4 million.

The chairman of Sibanye-Stillwater (JSE: SSW) bought shares worth R174k and an executive director bought shares worth R1.9 million.

The chairman of KAP (JSE: KAP) bought shares in the company worth R50k.

Keen to learn more about Datatec (JSE: DTC)? The management team presented at the RMB Morgan Stanley Off Piste Conference this week and the company has made the presentation available here.

Here’s something worth keeping an eye on: Tiger Brands (JSE: TBS) has repurchased around 3% of its shares since the AGM in February 2025. That’s an investment of R1.5 billion in the company’s own shares at an average price per share of R278.61 (current price is R315.77). They can repurchase up to a total of 10% of the shares that were in issue at the date of the AGM. The benefit of repurchasing shares is that it boosts HEPS, as the pie is effectively being cut into fewer pieces to feed the remaining shareholders, hence each shareholder gets a bigger slice!

Remember Wikus Lategan from Calgro M3 (JSE: CGR)? Having resigned as CEO of Calgro M3 a while ago to pursue other opportunities, he’s now popped up as an independent non-executive director of Safari Investments (JSE: SAR). The announcement notes that Lategan is the co-founder of ION Holdings, a property investment firm. It will be interesting to see what he gets up to! Safari announced that corporate and commercial attorney Conrad Dormehl has also joined the board as an independent non-executive director, so the board has certainly been beefed up.

Vunani Limited (JSE: VUN) has released a bland cautionary, which means a cautionary announcement that is low on details (flavour). All we know is that a wholly owned subsidiary has entered into negotiations of some kind. We have no idea whether this is for an acquisition or disposal.

Shuka Minerals (JSE: SKA) has updated the market on a further delay to the funds due to be received from Gathoni Muchai Investments to facilitate the acquisition of Leopard Exploration and Mining Limited and the Kabwe Zinc Mine. It’s never good when weird things like payment delays start happening, particularly when they aren’t rectified timeously. The funder expects to resolve this problem by the end of September. Thankfully, the sellers of the assets remain supportive of the transaction.

Assura (JSE: AHR) has confirmed that the delisting of its shares from the JSE is expected to take place on 3 October, followed by the delisting in London on 6 October. This is because of the successful offer by Primary Health Properties (JSE: PHP) that achieved sufficient acceptances to allow the company to follow a squeeze-out process to mop up the remaining shares.

MTN Zakhele Futhi (JSE: MTNZF) released results for the six months to June 2025. They don’t really matter though, as the company is in the final stages of being wound up and the June NAV is now a very outdated number based on the distributions to shareholders. I’m purely mentioning it for completeness.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

In March, Metrofile released a cautionary advising that it was in discussions relating to the potential acquisition of the Company. This week the parties released a joint firm intention announcement in respect of Main Street 2093’s offer to acquire Metrofile (excluding the treasury shares) for a cash consideration of R3.25 per offer share for an aggregate R1,37 billion. Shareholders accounting for 52.81% of eligible shares have committed to supporting the deal. The Long Stop Date has been set at 15 April 2026.

Anglo American, through its 50.1%-owned subsidiary, Anglo American Sur S. A. (AAS), has entered into a joint mine plan with Codelco for their adjacent copper operations. The agreement is expected to unlock at least US$5 billion of value from Los Bronces and Andina copper mines in Chile. The joint mine plan has been developed to unlock an additional 2.7 million tonnes of copper production over a 21-year period once relevant permits are in place, currently expected in 2030. The 120,000 tonnes per year will be shared equally, with c.15% lower unit costs relative to the standalone operations and with minimal incremental capital expenditure. The transaction is expected to generate a pre-tax net present value uplift of at least $5 billion, to be shared equally between AAS and Codelco. Both parties will maintain the flexibility to develop separate standalone projects, including the advancement of underground resources, during the term of the joint mine plan.

In June 2025 Espacio Mediterràneo, a shopping mall in Cartagena in the province of Murcia, was acquired by Lighthouse Properties for €135,4 million, reinforcing its strategic positioning in Spain. At the time the hypermarket unit was under separate ownership and excluded from the transaction. Lighthouse has now entered into an agreement with Frey Mediterraneo to acquire the Hypermarket for €15,5 million reflecting a net initial yield of 7%.

As part of its ongoing strategic repositioning and restructuring programme Accelerate Property Fund has disposed of the commercial property 73 Hertzog Boulevard, situated in The Foreshore, Cape Town. The property has been sold to Amrichprop 2 Properties for an aggregate R68 million. The transaction is classified as a Category 2 transaction for Accelerate and as such does not require shareholder approval.

In a detailed cautionary announcement Ascendis Health notified shareholders that it had initiated a process regarding a potential delisting of the company from the JSE. Shareholders wishing to dispose of Ascendis shares will receive R0.97 per share in a conditional offer – to be accepted by shareholders holding not more than 20% of the shares in issue. In November 2023, CAN Capital IHC-led consortium offered shareholders R0.80 per share to take the Ascendis private but the transaction lapsed following an investigation by the TRP initiated due to complaints received.

OUTsurance has reached binding terms to dispose of 83% of the Group’s 14.4% interest in Entersekt. The transaction is expected to close by December 2025. The information was released in its AFS.

Visual International has received a non-binding offer from private investment and development company Serowe Industries for the acquisition of a minority stake of up to 34.9% in the company. The potential subscription of a minority stake is for an indicative subscription consideration of R60 million. The non-binding offer incorporates a request for exclusivity, of which 40 days has been granted. Visual will however issue shares for cash for R2 million by way of a bookbuild – details of which will be released separately and in which Serowe may participate.

Libstar has received non-binding expressions of interest from parties regarding the potential acquisition of all Libstar shares in issue. This follows the company’s announcement in March that the Board would assess potential strategies through which to deliver meaningful value unlock for stakeholders, alongside continued execution of Libstar’s ongoing operational and strategic initiatives.

In early September Shuka Minerals informed shareholders that the finalising of the acquisition of Leopard Exploration and Mining (LEM) and the Kabwe Zinc announced in July 2025, had been hindered due to the delay in the remittance of funds in the form of a loan from Gathoni Muchai Investments (GMI). The loan is necessary to satisfy the US$1,35 million balance of cash consideration due to the LEM vendors. GMI has confirmed that the matters are expected to be resolved by the end of September 2025 and have further confirmed their financial capacity to meet these obligations.

While the key scheme conditions for the acquisition by ASP Isotopes of Renergen have been fulfilled and the parties are optimistic that the remaining conditions can be met by 30 September as per the Circular, the decision has been taken to extend the fulfilment date to 28 November 2025.

In October 2024, Nampak announced that it would sell its 51.43% shareholding in Nampak Zimbabwe to TLS for a maximum consideration of US$25 million. This week shareholders were advised that the circumstances for TSL in motivating the transaction to their shareholders had changed and had, as a result with the agreement of Nampak, withdrawn from the proposed transaction. The plan to dispose of the stake in the Zimbabwean operation remained in place.

Unlisted Companies

African global telematics and fleet asset management business Ctrack has received a R406 million investment from Sanari Capital, through its 3S Growth Fund, (R250 million) and 27four Investment Managers (R156 million). The investment builds on Ctrack’s strategic acquisition of Inseego’s international telematics business in 2024.The transaction, which was supported with a follow-on investment by Convergence Partners, consolidated Ctrack’s global footprint and expanded its presence in key international markets. The new investment will further accelerate this global expansion and support innovation on Ctrack’s unified technology platform.

In a move to further increase its exposure to SA Corporate Real Estate (SAC), Castleview Property Fund acquired 125,252,618 SAC shares at an average purchase price of R2.80 per share for an aggregate consideration of R350,71 million. Following the conclusion of the latest transaction, Castleview holds a 21.13% stake in SAC.

OUTsurance is to pay a special dividend of 33.1 cents per ordinary share payable on October 20, 2025.

Fortress Real Estate Investments is offering shareholders the opportunity to elect to receive a dividend in specie of ordinary shares in NEPI Rockcastle (NRP) in respect of all or some of their Fortress B shares in lieu of the cash dividend. Fortress currently holds 108,292,699 NRP shares constituting 15.2% of the total issued shares capital of NRP. Publication of the results of the dividend in specie will be announced on 21 October 2025.

Naspers has finalised the dates in respect of the amendments to its existing share capital structure through the pro rata subdivision of the N ordinary shares and A ordinary shares. The subdivision will be effected in the ratio of five-for-one for reach respective class of issued shares. After the split there will be 7,5 million authorised A shares and 1,5 billion Ordinary shares. Naspers will suspend its repurchase programme temporarily from 25 September to 2 October 2025 with the subdivision effective and implemented on 6 October 2025.

Altvest Capital’s name change to Africa Bitcoin Corporation has been registered by CIPC and will trade under the new name from 23 September 2025.

Assura shares will be suspended on the JSE from 3 October 2025 and the company’s listing on the LSE and JSE will terminate on 3 and 23 October 2025 respectively.

The JSE has advised shareholders that Labat Africa has failed to submit its condensed financial statements withing the three-month period stipulated in the JSE’s Listing Requirements and risks the threat of suspension if these are not submitted on or before 30 September 2025.

This week the following companies announced the repurchase of shares:

Over the periods 12 March to 9 May and 23 July to 16 September 2025, Tiger Brands repurchased 5,420,969 shares representing a 3% stake in the issued share capital of the company. The shares were repurchased at an average price of R278.61 per share for an aggregate R1,51 billion, funded from available cash resources. The shares will be delisted and cancelled. The company may repurchase a further 6.994% (12,6 million shares) of its shares under the general authority granted at its AGM.

South32 continued with its US$200 million repurchase programme announced in August 2024. The shares will be repurchased over the period 12 September 2025 to 11 September 2026. This week 794,183 shares were repurchased for an aggregate cost of A$2,09 million.

Momentum repurchased a total of 44 million shares at an average price of R31.43 per share during the financial year to end June 2025 for an aggregate cost of R1,4 billion. 42 million shares were cancelled prior to year-end. The Board has approved a further R1 billion for the buyback programme subject to Prudential Authority approval.

Investec ltd commenced its share purchase and buy-back programme of up to R2,5 billion (£100 million). On 10 September 2025, Investec ltd purchased on the LSE, 163,676 Investec plc ordinary share at an average price of £5.8099 per share and 108,844 Investec plc shares on the JSE at an average price of R137.3015 per share. Over the same period Investec ltd repurchased 31,207 of its shares at an average price per share of R136.7294. The Investec ltd shares will be cancelled, and the Investec plc shares will be treated as if they were treasury shares in the consolidated annual financial statements of the Investec Group.

The purpose of Bytes Technology’s share repurchase programme, of up to a maximum aggregate consideration of £25 million, is to reduce Bytes’ share capital. This week 600,000 shares were repurchased at an average price per share of £4.11 for an aggregate £2,47 million.

Glencore plc’s current share buy-back programme plans to acquire shares of an aggregate value of up to US$1 billion. The shares will be repurchased on the LSE, BATS, Chi-X and Aquis exchanges and is expected to be completed in February 2026. This week 9,3 million shares were repurchased at an average price of £2.99 per share for an aggregate £27,77 million.

In May 2025 Tharisa plc announced it would undertake a repurchase programme of up to US$5 million. Shares have been trading at a significant discount, having been negatively impacted by the global commodity pricing environment, geo-political events and market volatility. Over the period 8 to 12 September 2025, the company repurchased 20,195 shares at an average price of R21.85 on the JSE and 242,308 shares at 92.51 pence per share on the LSE.

In May 2025, British American Tobacco plc extended its share buyback programme by a further £200 million, taking the total amount to be repurchased by 31 December 2025 to £1,1 billion. The extended programme is being funded using the net proceeds of the block trade of shares in ITC to institutional investors. This week the company repurchased a further 483,542 shares at an average price of £41.25 per share for an aggregate £19,94 million.

During the period 8 to 12 September 2025, Prosus repurchased a further 1,217,622 Prosus shares for an aggregate €65,6 million and Naspers, a further 98,011 Naspers shares for a total consideration of R570,23 million.

Two companies issued profit warnings this week: Oceana and Choppies Enterprises.

During the week four companies issued or withdrew a cautionary notice: Ascendis Health, Libstar, Metrofile and Vunani.

Nasan Energies Namibia has agreed with Vivo Energy Namibia to acquire 53 Engen and Shell-branded fuel service stations. In May 2024, Vivo Energy completed the purchase of Engen Limited from Petronas, which included the Engen Namibia business. However, as part of the regulatory process, the Nambian Competition Commission determined that Vivo Energy would have to sell a number of its service stations to uphold a fair and dynamic market. Following a thorough evaluation process that assessed both technical expertise and financial proposals, Nasan Energies was selected as the preferred bidder. The value of the deal was not disclosed and is subject to approval by the Namibian Competition Commission.

The Norwegian government’s investment fund for business development in developing countries Norfund, has announced an undisclosed debt investment in Mohinani Group to support the expansion of its rPET (recycled polyethylene terephthalate) initiatives in Ghana and Nigeria. The investment in the form of a loan aims to reduce waste, cut greenhouse gas emissions, and create jobs in two of West Africa’s largest economies. The Mohinani rPET facilities in Ghana and Nigeria, managed by Polytanks Ghana Limited and Sonnex Packaging Nigeria Limited, respectively, have the capacity to produce 15,000 tons of recycled PET resins each annually.

Metier, through its Capital Growth Fund III, has invested with Watu Group, a non-deposit taking microfinance institution focused on financing income-generating assets for underserved communities across sub-Saharan Africa. Founded in 2015, Watu has a strong presence in Kenya, Uganda, and Tanzania, and expanding operations in Rwanda, Sierra Leone, the Democratic Republic of Congo, Nigeria, and South Africa. Watu’s mission is to meaningfully improve employment and economic opportunity for individuals facing the greatest barriers to accessing financial services. Watu provides financing for income-generating assets, supporting access to mobility (2/3-wheeler ICE and electric vehicles) and connectivity (smartphones) assets for underserved and underbanked communities. The company employs over 2,800 people with more than 1.4 million active clients.

Amethis Fund III announced the acquisition of a minority stake in BH Holding, a Moroccan player in the packing and export of high-value fruits. BH Holding is a structured family-owned group with a key position in the sector, thanks to its full integration across the value chain – from production to export – and its distribution under both premium proprietary brands and private labels. The group primarily exports citrus fruits, cherry tomatoes, and red fruits to North America and Europe. It relies on modern agricultural practices and demonstrates a strong commitment to sustainability and technological innovation. Financial terms were not disclosed.

Adiwale Fund I acquired a minority stake in Codex SA, a Senegalese lifting services provider, for an undisclosed sum. Codex SA operates the largest fleet of mobile cranes in Senegal, with over 120 equipment, including cranes, forklifts, aerial platforms, and semi-trailers, and a 11,000 m² operational base located 35 km from Dakar. The company serves a diverse client base, particularly in the energy (oil & gas, wind, solar), industrial (refineries, chemical plants, etc.), and mining sectors. The capital will support the acquisition of new equipment to meet rising market demand and the mobilisation of resources to implement the company’s regional expansion programme.

In Egypt, Duaya, a digital transformation company in the healthcare sector, has acquired EXMGO, a provider of SaaS solutions for pharmacies and medical businesses, in a six-figure investment deal (value undisclosed). Founded in 2021, Duaya offers a platform that connects suppliers with pharmacies, clinics, hospitals, and labs. Following the deal, EXMGO was rebranded as Duaya Go, offering branded apps and websites for pharmacies to manage online sales, inventory, and payments.

Premier Credit Uganda, a subsidiary of The Platcorp Group, has secured a US$1,5 million investment from Enabling Qapital, a Swiss-based impact asset manager. The investment will enable Premier Credit Uganda to scale operations, innovate its services, and extend access to finance to underserved communities across Uganda.

The global food industry has experienced significant transformation in recent years, driven by evolving consumer preferences, technological advancements and economic factors. Mergers and acquisitions (M&A) have become pivotal strategies for companies seeking to enhance their market position, diversify product offerings and achieve economies of scale.

According to data from S&P Global, 50 transactions were announced in the food and beverage industry in the first quarter of 2025. This marks a 34% quarter-on-quarter decline in transaction volume, making it the lowest quarterly deal count since the second quarter of 2015.

Higher levels of activity appear to have continued into the second quarter of 2025, with notable transactions including Unilever’s £230m acquisition of Wild, Müller’s £100m takeover of Biotiful, and the merger of Greencore and Bakkavor. Despite this activity, Grant Thornton’s Head of Consumer Industries, Nicola Sartori notes that mounting economic uncertainty may impact dealmaking in the second half of the year due to increased global market volatility.

In developed markets, M&A trends in the food sector are being driven by a strong focus on health and wellness, cost efficiency and technology adoption. Consumers are placing more value on organic, sustainable and healthier food options, prompting companies to pursue acquisitions that align with these preferences. At the same time, rising inflation and supply chain disruptions are placing pressure on margins, encouraging companies to consolidate operations to reduce costs and improve profitability. Technology is also playing a growing role, with traditional food companies acquiring tech-savvy start-ups to enhance production processes, streamline supply chains and expand their online presence.

In African markets, M&A activity in the food sector is accelerating due to a different set of growth drivers. Population growth means an increasing demand for food products, while rapid urbanisation is changing consumer habits and driving interest in processed foods, prompting traditional companies to modernise and scale up through strategic mergers and acquisitions. In addition, Africa’s emerging markets present attractive opportunities for international investors seeking to enter or expand within the continent’s food sector.

Legal trends

The legal landscape surrounding M&A in the food industry is complex and varies across regions. However, several common trends have emerged and are reshaping the food industry’s legal landscape. One of the most significant is increased regulatory scrutiny. Competition authorities are taking a more active role in reviewing M&A transactions to prevent the creation of monopolies and to ensure fair competition. In the United States of America (USA), for example, the Federal Trade Commission (FTC) and the Department of Justice review M&A activity under antitrust laws. In South Africa, the Competition Commission plays a similar role. These regulatory authorities can block or require modifications to proposed mergers that threaten consumer choice or market integrity. For instance, the FTC recently blocked a proposed US$25bn merger between Kroger and Albertsons due to concerns over reduced competition and potential price hikes. Cross-border M&A deals face additional regulatory hurdles as authorities and enforcement agencies assess compliance with global standards, which can delay or derail deals.

Environmental, social and governance (ESG) considerations are also becoming more prominent in M&A decision-making. Although individual ESG elements have long featured in due diligence processes, there is growing pressure on acquirers to demonstrate broader alignment with sustainability and social responsibility goals. Acquiring a company with strong ESG credentials can enhance brand reputation and appeal to socially conscious consumers and investors.

Due diligence remains a central component of any M&A transaction. Legal due diligence typically involves reviewing contracts, employment and labour matters, intellectual property and regulatory compliance (including licences and land rights). This legal review is conducted in tandem with financial, tax and operational due diligence to identify potential risks that could influence negotiation strategies, risk allocation and purchase price adjustments. The insights gained during due diligence are key to shaping negotiation strategies, allocating risk, adjusting the purchase price (where necessary) and, ultimately, ensuring that the transaction delivers long-term value.

Key considerations

When assessing M&A opportunities in the food industry, businesses must take several factors into account. It is essential to assess whether the target company aligns with your strategic objectives, whether that means expanding your product line, gaining access to new markets, or acquiring technological capabilities. A comprehensive financial analysis will help determine the target’s profitability, debt levels and potential for sustainable growth. Planning for integration is equally important. Companies need a detailed approach to merging operations, harmonising supply chains, managing culture, and aligning systems across the combined business. Risk management should also be prioritised, with clear strategies in place to address potential risks, such as regulatory barriers, market volatility and operational disruptions.

While M&A activity in the food industry offers significant opportunities for growth and diversification, these transactions are not without legal and operational complexity. Success depends on a clear understanding of evolving market trends, strong legal and regulatory awareness, and thorough preparation throughout the deal process. By staying informed and taking a strategic, risk-aware approach, companies can navigate this evolving landscape with confidence and position themselves for long-term success.

Gopolang Kgaile is a Partner and Zinhle Gebashe an Associate | Webber Wentzel

This article first appeared in DealMakers, SA’s quarterly M&A publication.

For all the geological potential East Africa offers, the region’s junior miners remain caught in a familiar bind: promising assets, ambitious growth plans, but a stubborn lack of risk capital to bring projects to scale. Over the past three years, a handful of juniors with projects in Kenya, Tanzania and Ethiopia have tested the market, often relying on small equity placings, shareholder loans or piecemeal project-level deals to stay afloat. The result is a funding landscape that is still shallow and episodic, limiting the pace and scale of development.

Micro-raises and shareholder dependence

For most East African juniors, listings or dual listings on exchanges or their sub-markets is the most accessible route to capital. These are typically accompanied by small equity placements, often heavily reliant on existing shareholder support.

East Africa-focused Caracal Gold plc, for example, has leaned on this approach. Since 2023, the company has completed several modest equity raises, typically under £1 million each (RNS, April 2024). Proceeds have funded resource expansion and, more recently, restart plans following the suspension of production in early 2024. Yet Caracal’s market capitalisation hovers between £3-5 million (LSEG Market Data, 2025), underscoring the difficulty of scaling through micro-capital injections.

In Tanzania, Katoro Gold plc, an early-stage explorer in the Lake Victoria Goldfields, has walked a similar path. Its most recent £350,000 placing in Q2 2025 (AIM News, May 2025) follows a string of micro-placements stretching back to 2023, each just enough to fund incremental exploration and corporate overheads.

While these equity raises provide essential lifelines, they limit project advancement and keep most juniors in a cycle of dilution and underfunding.

Consolidation as an exit

By contrast, larger, cash-generative African producers are taking a different approach to East African gold. Perseus Mining’s A$260 million acquisition of OreCorp in 2023 gave it control of the 3Moz Nyanzaga project in Tanzania, now one of the most advanced gold developments in the region. Perseus gained a pipeline asset it could fund directly from internal cash reserves (ASX announcements, September 2023). Subsequent early works at Nyanzaga have been financed entirely from operating cashflow, avoiding external debt or equity dilution (Q3 FY25 Results, June 2025).

This is an advantage few juniors can hope to match. As such, acquisitions are another viable option for undercapitalised juniors with quality assets.

Project-level funding

Some juniors in the region are also exploring project-level financing structures tied to offtake or prepayment arrangements. For instance, Katoro Gold has publicly disclosed ongoing discussions with potential offtakers to fund its next phase of resource drilling (RNS, 12 June 2025). Similarly, Caracal Gold is evaluating offtake-backed financing structures to support Kilimapesa’s restart plans (RNS, 28 March 2025).

While East Africa has yet to see a large-scale streaming or royalty deal for a junior mining project, the concept is gaining traction in boardrooms as successful stories emerge from other parts of the continent, like the Pan African Resources’ $20 million gold prepayment facility for its Mintails project in South Africa (FY24 Results, August 2024) that has shown how offtake-linked structures can bridge the pre-production funding gap.

Hybrid approaches and creative structuring

Ultimately, juniors will need to employ innovative and hybridised models to bridge funding gaps. Shanta Gold, an East African producer, offers a useful case study. In 2023, the company raised approximately US$20 million via a convertible loan note to advance drilling and feasibility work across its portfolio, including the West Kenya project (RNS, June 2023). Shanta continues to leverage its DSE listing and free cashflows from its New Luika and Singida operations for funding flexibility (Q2 Operational Update, July 2025). While Shanta benefits from production scale that juniors lack, its use of blended capital structures points to the kind of creative solutions others may need to pursue.

Another example is East Africa Metals, which is pursuing a project-generator model. Instead of focusing on fully developing a single asset, the company has built a portfolio across Ethiopia and Tanzania, advancing projects like Harvest and Adyabo. This model involves identifying and acquiring promising mineral properties to initially explore, and then optioning or selling these projects to partners. This approach reduces balance sheet strain while keeping the project pipeline moving.

DFIs may also play a bigger role in bridging the capital gap. Institutions like the African Finance Corporation and Afreximbank have shown increasing appetite for resource-sector infrastructure and development-stage funding, albeit more commonly for larger-scale projects. Their evolving mandates may open new pathways for East Africa’s juniors, particularly as projects advance toward feasibility stage.

Crossing the chasm

East Africa sits atop world-class gold geology and global demand for critical minerals and precious metals remains strong. Yet without access to deeper pools of risk-tolerant capital, be it private, institutional or strategic, many of the region’s juniors risk staying stuck in exploration limbo.

Bridging East Africa’s junior mining funding gap will require more than incremental raises and patchwork financing. It will require a structural rethink: greater use of project-level and hybrid capital, stronger engagement with strategic partners, and a more active courting of global capital willing to invest in the region.

Noreen Kidunduhu is the Founding Principal | Noreen & Co and is an ILFA Alumni

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Choppies puts some concerns around Botswana to rest (JSE: CHP)

HEPS has moved in the right direction

Choppies released a trading statement for the year ended June 2025. Full results are due for release next Monday, so they’ve given investors only a few days of warning here. At least the results are in a different week to the trading statement, so there’s time for investors to digest it before the full results come out. It would still be good to see more daylight between the trading statement and the release of results.

The numbers are full of distortions related to the sale of the Zimbabwe business, forex impacts and other once-offs. There’s even a significant change to the effective tax rate due to losses in Namibia for which they haven’t raised deferred tax.

This is why profit after tax from total operations will drop by between 25% and 35%, while HEPS from total operations will increase by between 15% and 24%!

It’s encouraging that adjusted EBITDA from continuing operations was up by between 6% and 16%, as that’s about the closest we can get to a view on the core operations right now. Given all the concerns around the economy in Botswana at the moment, it’s good to see this. It will be important to wait for the full details before reaching any strong conclusions though.

At long last, Metrofile shareholders receive an offer (JSE: MFL)

And the market liked the price

Metrofile has been trading under cautionary for several months now. That doesn’t tell the whole story, as the market has been hearing about potential offers and take-privates for years now.

Finally, there’s an actual offer on the table from Mango Holding Corp (a Delaware company held by WndrCo LLC, James Simmons and his family) at R3.25 per share. We are talking about a stock with a 52-week low of R1.17 around February this year! To make it happen, the offeror has had to furnish a bank guarantee of almost R1.4 billion to show that they can afford the deal.

The deal takes the form of a scheme of arrangement, which means the acquirer wants to get their hands on all the shares in Metrofile. This also explains the premium of 99% to the 30-day VWAP to 25 March (the date before the first cautionary) and the premium of 25% to the 30-day VWAP to 16 September.

Unsurprisingly, this premium is enough to get strong support from a number of major shareholders who have given irrevocable undertakings to say yes to the Mango Holding dress. Holders of 52.81% of shares will support the offer, including MIC Investment (39.2%) and another name you’ll recognise: Sabvest (JSE: SBP) with a stake of 4.97%. The scheme will need 75% approval to be binding on all shareholders.

The circular will be distributed to shareholders in due course, including the independent expert opinion and the recommendation by the independent board. I think the extent of irrevocable undertakings already obtained tells you that the price is good.

Immense growth at Momentum (JSE: MTM)

The company has had a spectacular year

Momentum’s share price is up 19% in the past 12 months. Strong as that is, it doesn’t seem to tell the full story of a company that grew HEPS by 50% and the dividend per share by 40%.

But here’s the metric that it probably does reflect: diluted embedded value per share grew by 15%. I suspect that this anchored the share price performance in the same way that net asset value per share does it for banks.

It’s not surprising at all to see that one of the contributors to the positive result was a better underwriting result at Momentum Insure. This is in line with the narrative we’ve seen across the short-term insurance sector, although Momentum Insure’s normalised headline earnings more than doubled and thus put in a particularly great performance.

The largest segment is Momentum Corporate, which achieved 37% growth in normalised headline earnings. Momentum Retail is the second largest and posted growth of 22%. When your two largest segments are growing like that, it’s hard for the group results to go wrong. Notably, operating losses in India decreased significantly.

Interestingly, the present value of new business premiums (PVNBP) dipped 3% and the value of new business fell 20%. Momentum explains this as being partially due to a focus on quality rather than overall volumes, but they also acknowledge that the value of new business needs to be addressed.

In a group this size, there’s always something to work towards improving. But with return on equity up to 21.2% from 15.5% in the prior year, shareholders aren’t complaining.

Mustek’s earnings will be slightly up (JSE: MST)

Here’s another trading statement released too close to results

In case you haven’t noticed, I’m now making a point of highlighting companies that release trading statements at the last minute before releasing full results. Trading statements should be an early warning system for shareholders and the market at large, not merely a tick-box exercise just before the numbers come out.

Mustek is the latest culprit, releasing a trading statement for the year ended June 2025 on Wednesday, with full financials due to be released just two days later. That’s not good enough.

HEPS will move by between 0% and 10%, so that implies mid-single digit growth at the midpoint. A trading statement is triggered by a move of at least 20%, but not just in HEPS – the test is also applied to Earnings Per Share (EPS) which doesn’t make adjustments for large once-offs in the same way that HEPS does. This is why EPS is expected to be between 85% and 95% higher.

HEPS is the right measure of performance, so it was a period of modest growth for Mustek. But more importantly, it’s time that listed companies stopped treating trading statements as a joke. I find it hard to believe that clarity on such a huge increase in EPS (vs. the test of 20%) was achieved in the same week that a fully baked set of results will be presented to the market.

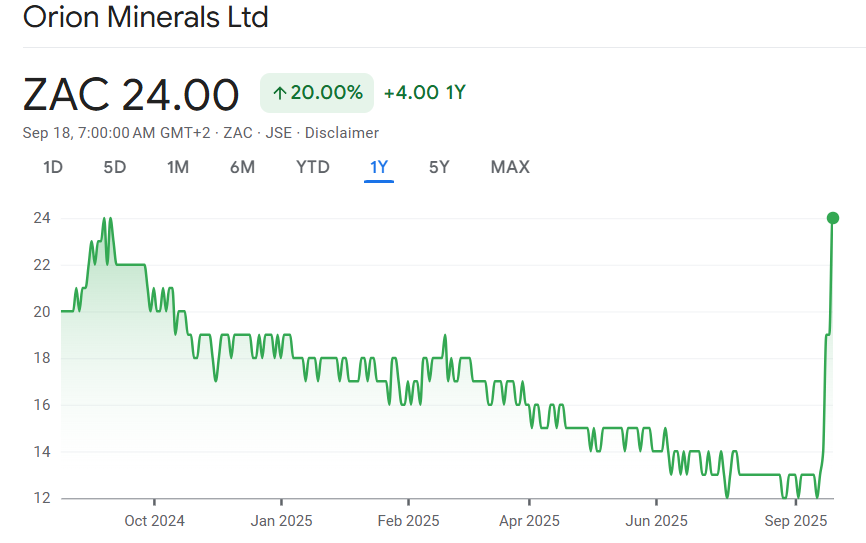

Orion Minerals’ share price shoots for the stars (JSE: ORN)

Nothing like a 26% jump in a single day!

Orion Minerals announced the news of a non-binding term sheet for a financing deal with a subsidiary of Glencore (JSE: GLN) and the market showed its appreciation, with a 26% increase in the share price. Worryingly, the share price is up 85% over 5 days. I get the argument around momentum traders and how they can amplify a move as they chase unusual volumes, but this is one of those classic cases where I hope the JSE will examine the trades before this announcement to make sure that there wasn’t any nonsense of someone trading based on a whisper they heard at a golf course. Sigh.

Back to the deal: provided that all goes well in the deal conditions, Orion has locked in financing of between $200 million and $250 million for the Prieska Copper Zinc Mine. They’ve also secured concentrate offtake as part of the deal.

The funding comes in two tranches. Tranche A is worth $40 million and will be used for the “Uppers” at Prieska. The remaining funding comes in Tranche B and will be used for the “Deeps” – descriptions that do what they say on the tin. As for the offtake, Glencore will take 100% of the bulk concentrates from the Uppers for 5 years, along with 100% of the copper concentrates and 100% of the zinc concentrates from the Deeps for 10 years.

Glencore still needs to complete a due diligence, so the funding isn’t guaranteed yet. These funding facilities will bear interest at “market rates” and will become cheaper once commercial production is declared. Glencore has some of the sharpest minds in the sector, so I have no doubt that they pushed Orion hard on the funding cost. The new management at Orion have done well here though, as the company desperately needed to show the market some meaningful progress in obtaining funding.

They hope to reach binding agreements over the next four to six weeks.

As share price charts go, you can add this to the “might inspire contemporary art” bucket:

Supermarket Income REIT managed only the slightest growth in the dividend (JSE: SRI)

The UK market isn’t a land of milk and honey right now

Most of what I read about the UK economy at the moment isn’t particularly encouraging. I’ve also heard reports from the ground on how difficult it is to grow businesses there. If I look at the results for Supermarket Income REIT, it once again looks like achieving meaningful growth in the UK market is difficult.

Net rental income may have been up 6% for the 12 months to June 2025, but EPRA earnings per share dipped by 2% and the dividend per share is up just 1%. The portfolio valuation increased by 1.9% on a like-for-like basis and the net asset value (NAV) per share was down 1% on an IFRS basis. The highlight is the improvement to the loan-to-value ratio, which decreased from 37% to 31%.

The company talks about the effect of cash drag on the earnings, as they recycled quite a bit of capital in this period. This, along with the effect of other initiatives (like the internalisation of the management company), creates the potential for more growth going forwards.

But here’s the problem: the FY26 target dividend is at least 6.18 pence per share. I’m afraid that’s only 1% higher than the FY25 dividend, which isn’t encouraging when the company is talking about how they are poised for growth.

An associate of a director of a subsidiary of eMedia Holdings (JSE: EMH | JSE: EMN) bought N ordinary shares worth R47k.

Castleview Property Fund (JSE: CVW) has further increased its stake in SA Corporate Real Estate (JSE: SAC). They now hold 21.1% of the shares in issue thanks to selling derivatives worth R95 million and then buying shares worth R351 million (a significant net investment).

Omnia (JSE: OMN) is presenting at the RMB Morgan Stanley Off Piste Conference this week. They’ve taken the opportunity to make their presentation available, giving a handy overview of the company and the outlook. They are aiming for a compound annual growth rate (CAGR) in earnings of 12% to 17% over the next 3 years. That’s a brave target!

Frontier Transport Holdings (JSE: FTH) announced that Ulandy Gribble will be the new CFO with effect from 1st October. This is an internal promotion, which is always good to see.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

Anglo American recently announced a blockbuster deal in the form of the proposed merger with Teck Resources to form Anglo Teck. They are trying very hard to convince everyone that this is a merger of equals, even though the numbers tell a different story. Anyway, copper sits at the heart of that strategy, with the latest news from Anglo American reflecting further progress in the underlying copper business.

Anglo American and Codelco have agreed to a joint mine plan for the adjacent copper operations (Los Bronces and Andina respectively) in Chile. This is expected to achieve additional copper production of 120,000 tonnes per year (shared equally), with 15% lower unit costs vs. standalone operations.

They believe that this unlocks a pre-tax net present value of at least $5 billion, shared equally between the firms. It’s important to note that Anglo’s stake in Los Bronces is in a 50.1%-held subsidiary, so Anglo shareholders are basically getting half of half of $5 billion in value uplift – in theory. These gains are all on paper at the moment.

If they get it right, the incremental production gain would take the combined production numbers into the top 5 copper mines globally. Currently, if you just add the mines together without the incremental gain, there’s a top 10 production base to work from.

It’s important to not fall into the trap of actually seeing this as a combined asset, as each company retains its separate ownership and can advance the underground resources as they see fit. This is really just a joint mine plan that hopefully goes well.

Attacq’s recent corporate activity has paid off in the form of much higher earnings (JSE: ATT)

You won’t often see these kind of growth numbers in a property fund

Attacq has released results for the year ended June 2025. Distributable income per share was up 25.6%. It’s possible in a period of heavy dealmaking to see an increase in overall distributable income of that amount (as funds can simply go out there and acquire earnings), but it’s very rare to see it on a per-share basis.

Powering this performance is growth in net operating income of 14.0% (a particularly impressive two-year stack as the prior year was 8.1%), along with the benefit of development activity at Waterfall City and the first full-year impact of deals at Waterfall City with the GEPF and the acquisition of the remaining 20% of Mall of Africa.

It’s easy at times to forget that Attacq has a substantial portfolio outside of Waterfall City. They are focused on dominating the precincts they are invested in, so you won’t find them owning random buildings in an incoherent strategy. Instead, they build out centres of excellence in various places, with Waterfall City as the precinct that they are best known for.

Looking deeper into the portfolio, we find a like-for-like valuation increase of 5%. The retail portfolio was the most impressive at 6.8%. It’s great to see the office portfolio (Attacq calls this the “collaboration hubs”) up 2.3% in value thanks to 6.1% net operating income growth. Its been a long, hard road for office property, as evidenced by this chart:

The fund is in great shape, which enables them to continue with the development strategy (including speculative logistics developments with lumpy effects on occupancy, as is also visible in the chart above).

Guidance for FY26 is for growth in distributable income per share of 7% to 10%, with an 80% dividend payout ratio. The FY25 payout ratio was 80.3%, so the distributable per share growth should be very close to distributable income per share growth.

Ethos Capital flags a significant uptick in NAV (JSE: EPE)

Optasia and the Brait exchangeable bonds have boosted the value

Ethos Capital has released a trading statement for the year ended June 2025. They do things the right way in terms of how they report performance, which means they use net asset value (NAV) per share instead of HEPS like some investment holding companies do. Full results are coming on 25 September, so they’ve also given shareholders more than a week of advance warning of what’s coming. That’s not amazing, but not too bad.

The good news for shareholders is that the net asset value per share is expected to be between R8.45 and R8.60, which means an increase of between 20% and 22% without adjusting for the Brait ordinary shares that were unbundled in July 2024. With that adjustment, the increase is between 28% and 31%.

The main driver of the increase is the value of Optasia (around 50% of group assets as at March 2025), along with positive valuation moves at Vertice, e4 and Primedia in the unlisted portfolio. In the listed space, the Brait exchangeable bonds also increased in value.

Hyprop’s dividend per share growth was just below the double-digit level (JSE: HYP)

And guidance for the coming year is higher

I’m still frustrated with how the Hyprop capital raise for the attempted acquisition of MAS (JSE: MSP) was handled. It probably says more about the cost of debt in South Africa than anything else, with institutional investors happy to throw money at property funds on the off-chance that they do a good deal, with reduction of debt as a palatable plan B. The cost of debt being so close to the cost of equity explains a lot about how hard it is to grow a business in South Africa.

For the year ended June 2025, Hyprop achieved very strong growth of 24% in distributable income in the Eastern European portfolio, along with 11% growth in South Africa. Distributable income was up 7.5%, but distributable income per share was up 2.3%. The per-share number is where you see the effect of the additional shares in issue.

Hyprop had enough flex in its payout ratio to make sure that the dividend per share tells a better story, up 9.9%. We will have to see what they do with the payout ratio in FY26, with guidance for distributable income per share growth of between 10% and 12%. This is on the assumption of interest costs remaining at current levels, so any decrease in global rates should help.

In the South African portfolio, Hyprop tenants enjoyed a 5.5% increase in turnover despite the economic pressure and growth trend in eCommerce (foot count was up just 0.1%). The reversion rate was positive at 4.3%.

In Eastern Europe, turnover growth was even better at 6.6% (in euros) despite a decline in foot count of 0.8%. Reversions were positive 9.1%.

Touching on debt reduction again for a moment, the group loan-to-value (LTV) ratio improved from 36.4% to 33.6%. The average cost of borrowings also reduced. This combination always does wonders for distributable income.

Table Bay Mall, which in my opinion Hyprop overpaid for, has a vacancy rate of 2.1%. That’s higher than Canal Walk (1.4% retail vacancy), Somerset Mall (0.6% vacancy) and CapeGate (0.9% vacancy) as Western Cape peers. The foot count at Table Bay Mall was just 5.6 million over 12 months, which is way off CapeGate at 10 million despite Table Bay Mall having only slightly less GLA. I know the area well and I don’t doubt the long-term growth, but it feels like they paid for all of it upfront.

Libstar might be headed for the exit (JSE: LBR)

And at a time when earnings are finally moving higher

Libstar has had a pretty rough journey as a listed company. That journey might be coming to an end, with the results announcement accompanied by a cautionary regarding non-binding expressions of interest received from parties who are looking at acquiring all the shares in Libstar. If that happens, it would obviously mean a delisting of Libstar. The discussions are at an early stage and there’s no guarantee of an offer coming through (or at what price), but that didn’t stop the market from taking the share price 14.5% higher.

Moving on to the results themselves, Libstar’s performance for the six months to June 2025 reflects a very helpful increase in revenue from continuing operations of 6.7%. This was accompanied by a 90 basis points increase in gross margin to 21.6%. Normalised operating profit came in 16.7% higher and normalised HEPS grew by 15.4%, so things are firmly on the up. This would’ve also supported the share price move.

As for all the normalisation adjustments, this includes what Libstar describes as “non-recurring, non-trading and non-cash items” – and hence a healthy dose of skepticism is a good idea. The great news is that normalised HEPS growth of 15.4% is actually much lower than HEPS growth (without adjustments) of 23.7%, so the normalisation adjustments are telling a more modest story. That’s a much better situation than the other way around.

Libstar only declares final dividends rather than interim dividends, so there’s no dividend at this time.

The outlook is one of a weak consumer market and a need for Libstar to focus on operational efficiencies in its business. They’ve been doing a pretty good job of that lately!

After the latest share price move, here’s what the chart looks like:

Premier Group achieved excellent earnings growth (JSE: PMR)

This is the kind of trading statement that the market loves seeing

Premier Group has released a trading statement for the six months ending 30 September 2025 – yes, they’ve done it before the end of the period! Great as that is, I don’t think the dates of the RMB Morgan Stanley Off Piste conference (17th and 18th September) are a coincidence. This trading statement at least gives management the ability to talk to conference attendees about just how well the business has done, without giving away non-public material price sensitive information.

Premier is achieving mid-single digit revenue growth and is on track to turn that into an increase in HEPS of between 20% and 30%. As leverage goes, that’s exceptional. It also explains why the share price closed 4.4% higher to take the 12-month increase to 57%.

RFG Holdings is battling tough sales conditions (JSE: RFG)

The market seemed to like the update anyway, presumably because of margins

RFG Holdings released a trading update for the 11 months to August. This is essentially a pre-close update by another name. The share price closed 7% higher in response, despite some clear challenges being faced by the business.

Revenue was up just 2.4% for the 11 months, which is even slower than the 3.5% growth in the interim period. A deceleration in revenue off a low base is concerning. Management has stated that they “remain committed” to achieving the operating profit margin target of 10%, although the announcement isn’t explicit on by when. The interim profit margin was 8.5%.

The deceleration in revenue is actually worse than it looks, with RFG noting that July and August showed particularly weak trading in South Africa. The regional segment (local sales) has been the only thing keeping RFG in the green, as the international segment has been experiencing a drop in revenue due to an oversupply of deciduous fruit products and now the uncertainty on tariffs as well.

For the 11 months, revenue in the regional segment was up 5.1% and the international segment was down 8.4%. This compares to interim growth of 7.6% and -17.2% respectively, so the international business actually clawed back lost ground in recent months while the regional segment slowed down even more.

It’s a tough business with exposure to numerous external factors, with the share price down 23% year-to-date and up 4.3% over 12 months.

Nibbles:

Director dealings:

A senior executive at Quilter (JSE: QLT) has sold shares worth around R5.7 million.

An independent non-executive director at STADIO (JSE: SDO) bought shares worth R40.6k.

Nampak (JSE: NPK) needs to find a new buyer for Nampak Zimbabwe. The disposal of its 51.43% stake in Nampak Zimbabwe for up to $25 million to TSL Limited has fallen through despite a successful due diligence and competition authority approval process. TSL has elected to withdraw from the deal for strategic reasons and Nampak has agreed to this. Nampak remains committed to an exit from this asset.

Visual International Holdings (JSE: VIS) announced that Serowe Industries has submitted a non-binding offer to acquire up to 34.9% of the issued shares in the company via a subscription for equity of R60 million. The 34.9% shareholding is just enough not to trigger a mandatory offer to all shareholders (35% is the threshold for that). Serowe has an exclusivity period of 40 business days for the due diligence. In that period, Visual can’t negotiate with anyone else regarding equity, other than for a R2 million bookbuild that will be executed during that period (and in which Serowe will be invited to participate). Visual’s current market cap is R44 million. The pre-money valuation implied in this process is R112 million, which you calculate as R60 million / 34.9% = R172 million post-money valuation. Take off the R60 million in new equity and you get to R112 million pre-money, or 2.5x the current market cap! It’s little wonder that the share price doubled on the day on exceptionally strong volumes (by Visual’s standards, as this is a highly illiquid stock).

MAS (JSE: MSP) – the company that dominated headlines for a few weeks as you may recall – has announced that four new independent non-executive directors have been appointed, along with a non-executive director (not of the independent variety) in the form of Martin Slabbert of Prime Kapital. Dewald Joubert, Nevenka Pergar, George Mucibabici and Yovav Carmi are the four independents who will join the board. Notably, the current independent chairman (Werner Alberts), lead independent non-executive director (Claudia Pendred) and chair of the audit and risk committee (Vasile Iuga) have all tendered their resignations with immediate effect. The replacement chairman hasn’t been announced yet and neither have the reconstituted committees. You won’t often see wholesale changes to a board like this, but then again you don’t usually see corporate activity like we saw at MAS.

If you wondered whether Truworths (JSE: TRU) CEO Michael Mark is finally headed for retirement, then the latest announcement of share awards at the company should put those worries / hopes (depending on your view) to rest. The performance shares are worth R16.5 million and the vesting profile is such that they all vest in year 3 (subject to performance conditions).

Southern Palladium (JSE: SDL) is presenting at the Resources Rising Stars Gold Coast Investor Conference this week. They’ve made the presentation available, with slides ranging from an overview of the PGM supply-demand expectations through to the optimised prefeasibility study at Bengwenyama. You’ll find the presentation here.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

With a background in law and economics, Obaratile (OB) Semenya’s approach to property includes exposure at practically every part of the value chain.

From developing high-end residential projects through Legaro Property Development to driving sales at his real estate agency, Natural Property, he’s mastered the full property journey.

And with extensive experience working closely with Balwin, OB also knows his way around the biggest developments around.

On episode 3 of The Finance Ghost Plugged in with Capitec, he talks about building the world he wants to see around him, all while ‘nerding out’ on the business and sector he loves most.

Episode 3 covers:

The risks and rewards of the property sector

Lessons from working across the full value chain

Insights from balancing development and real estate sales

Why passion for what you do often makes the rest fall into place

The Finance Ghost plugged in with Capitec is made possible by the support of Capitec Business. All the entrepreneurs featured on this podcast are clients of Capitec. Capitec is an authorised Financial Services Provider, FSP number 46669.

Listen to the podcast here:

Read the transcript:

Intro: From side hustles to success stories, this is The Finance Ghost plugged in with Capitec, where we explore what it really takes to build a business in South Africa. This podcast features Obaratile Semenya, a property entrepreneur with experience across the value chain from sales to development.

The Finance Ghost: Welcome to this episode of The Finance Ghost plugged in with Capitec. This is a wonderful podcast series in which I get to speak to some really interesting entrepreneurs. I get to dig into their backstory. I get to understand more about what they’ve built and why they are still building it. And of course, we get to learn along the way, which is something that I really enjoy because entrepreneurs are such inspiring and interesting people. And of course, my thanks to Capitec Business for making this possible.

And on this episode, I am grateful to be able to speak to OB Semenya. OB is a property entrepreneur. This man has got a lot of things going on. I’m not sure how he remembers which business to work on, on which day! The fact that he’s wearing a branded hoodie of one of the businesses tells me that maybe he just matches his outfit to what he’s working on that day. I guess we’ll find out shortly. OB, thank you so much for doing this podcast with me. You’ve got so much to share about the world of property, and I’m really looking forward to digging in with you.

Obaratile Semenya: It is an absolute honour. Thank you, Ghost, for the invitation. I appreciate it. I just hope that I can rise to the occasion for you.

The Finance Ghost: So spill the beans. Does that sweater that you’re wearing there, that hoodie, does that remind you what you need to work on today? It feels like you’re wearing your diary on your chest, basically.

Obaratile Semenya: Sort of! You’re not wrong. Today is very much a real estate day. There’s a sale that was closing this morning, so that’s the hoodie that we’re wearing today, but it will change late in the day meeting. So, yeah, not wrong.

The Finance Ghost: I love that. The life of an entrepreneur with a finger in many pies. And we’ll obviously dig into that, definitely.

But I think before we do, let’s just understand more about the backdrop of what got you into property, when this started for you, because it’s really interesting to understand the background of entrepreneurs and what gets them to the point they’ve gotten to today. I mean, in the last episode of this podcast series, which I would encourage listeners to go check out, I got to speak to Rabia Ghoor and she started swiitchbeauty when she was 14, dropped out of high school two years later, and 10 years after that she’s sitting with this wonderful eCommerce business.

So was property an early thing for you, OB? Was this something where even in school you were interested in it, or was it something that happened later? Because what’s fascinating with property is I find when I meet people who are property people, that really is what they are, right? Their whole career kind of sits in property because it’s such an interesting and specialist space. It’s not like, oh, you know, today I work in retail and then tomorrow I go and work in a different kind of client-facing business. People flit around other sectors a lot in their careers, but it feels like once you’re in the property stream, you’re in it. Has that been your experience?

Obaratile Semenya: So I think you’re not wrong. The more my journey into property develops, the more I find that to be a very common theme among people who if property is what they do, property is what they love, property is what they eat. Because of, I guess, the all-encompassing nature of the industry.

For me, actually, I wish I could say it’s the same, but it’s really not. I never even considered myself a property person per se. If I had to think about when my journey into property started, it started way before I was in school. My perspective even today about property mostly comes from my reality. I mean, I was born, geez, I don’t want to give myself away here, but I was born, what, 1990. So, I was born on the cusp of understanding the notion of property. The first home I can remember is one that I remember my dad buying in Kelvin with a CC, right. And him constantly reiterating to me how ridiculous it is that we live where we live. Because he’s a dad, right?

But my understanding of property has just been infused throughout my life as a discussion about, well, what does this country now look like? And I think that’s partly because of when I was born, but also because I come from a family of lawyers. So my property understanding actually comes from the law. And I only find myself being a property person later in my life, but it definitely is my passion.

The Finance Ghost: Yeah, that’s incredibly interesting. And obviously it talks to the history of South Africa and how property has been a really hard thing for a lot of people historically. And obviously we live in a very different country now and thank goodness for that. And as you say, born 1990 – that was right on the cusp of – I love the way you put it, where property starts to become a concept you can actually attach to. It’s actually such an incredible way to describe it really.

And interesting as well that you’ve come at it from a legal angle as opposed to more of a finance angle. I’ve got to say, some of the best people I worked with in my corporate finance career were attorneys by profession. Lawyers are very capable of great dealmaking, definitely. And it’s just interesting to see that, really.

So I think let’s get a lay of the land, of what it is that you’ve built, because if you need to, as I said, change your clothing based on which business it is that day, then there’s clearly a lot going on there. And I know from the discussions we had as the build up to the show, you do have your finger in very many pies in the property game and also at different points in the value chain, which makes this extra interesting.

We will obviously talk through some of the more detailed projects in the development space, etc. But I think just give us the sort of elevator pitch of OB the property entrepreneur. What do you have in the stable?