")

Fee revenue is now 14% of earnings at Burstone (JSE: BTN)

The focus on building property fund platforms is clearly visible – but they need more growth

In the property sector, Burstone is following a business model that differentiates it from almost every other REIT you’ll find on the JSE. Instead of focusing on direct ownership of property, or indirect ownership via global partners, Burstone is building a fund management platform that makes use of that most wonderful concept that investment bankers love: Other People’s Money. Given Burstone’s prior links to Investec, it’s not surprising that they understand return on capital!

The benefit of this approach is that Burstone can earn property management fees in addition to a return on its own capital, which can juice up ROE (return on equity) over time. That’s the theory, at least. At this stage, Burstone has a gross asset value of R43 billion, of which R24 billion is third-party assets under management. Notably, 68% of the gross asset value is offshore.

In a pre-close update for the six months to September 2025, Burstone notes that the South African portfolio is good for like-for-like net operating income growth of 4% to 5%. On the investment income side, Europe is flat year-on-year while Australia is expected to grow “substantially” because of their asset management strategy in that market that has grown assets by 7%.

Speaking of asset management, fee revenue is now 14% of earnings, up from 8.5% in the comparable period. There’s been a lot of progress for Burstone in its international market in this regard, with plans still in place to build a similar South African platform. They are working with a “cornerstone institutional investor” in this space and final approvals are pending.

But here’s the catch: all of these efforts have only resulted in distributable earnings growth of 2% for the interim period, which is at the lower end of group guidance. They attribute this to slower capital deployment during the period as well as a major business failure in the South African industrial sector that has obviously affected their rental income. They can at least maintain the dividend payout ratio at 90%, so dividends per share will increase by 2%.

Digging deeper into the South African portfolio reveals like-for-like net operating income growth in the retail sector of between 8% and 10%, with the Zevenwacht Mall as a particular highlight. Importantly, the office portfolio is expected to grow by 3%, with negative reversions of -15% vs. -21.1% in the comparable period. The industrial portfolio was the unfortunate disappointment, with like-for-like net operating income down 5% thanks to the aforementioned business failure.

Burstone’s share price hasn’t exactly been a happy story, dropping 13% over the past 12 months. It’s tempting to suggest that the strength of the rand is a factor here, but the reality is that the rand has actually weakened against the euro over the past year and is only marginally better against the Australian dollar. We therefore have to assume that at a time when many of the local REITs are putting out strong growth numbers, the market isn’t particularly thrilled with the low growth at Burstone despite all the progress being made in building the platforms.

“Nature is no supermarket” at Gemfields – therein lies the risk and the opportunity (JSE: GML)

For the six months to June, the company swung into a loss

If you consider what has happened to the natural diamond market, then it’s sensible to question why the same can’t happen to rubies and emeralds. There are a few reasons why I think Gemfields is safer from disruption than De Beers.

Firstly, there’s no social pressure to buy rubies and emeralds. The problem for diamonds is that the major driver of purchases is engagements, which are happening later and later these days due to affordability. An alternative product that makes it easier to get engaged while respecting traditions and societal expectations can only be a winner.

Secondly, rubies and emeralds are valuable because of their imperfections, not despite them. The storytelling angle of these unique stones being created by nature falls over very quickly if you make them in a lab. For diamonds, clarity and perfection are highly valued – characteristics that are easier to achieve in a lab.

Of course, this doesn’t mean that Gemfields isn’t facing other risks. Aside from the usual stuff when you operate in Africa (like governments doing tax grabs and the ever-present risk of political violence), there are major supply and demand considerations in the underlying emerald and ruby markets. On top of this, the brilliant “nature isn’t a supermarket” quote in the CEO commentary is a reminder that the grade of rubies and emeralds is unpredictable, so the quality of what they get out the ground changes each period.

The six months to June 2025 puts these risks in the spotlight, with Montepuez Ruby Mining suffering a decrease in the production of premium rubies and Kagem Mining having halted its emerald mining operations at the end of 2024 to respond to oversupply in the market. Kagem only reopened two production points in May 2025.

As you might expect, the impact on revenue was hideous. Total auction revenue from rubies and emeralds approximately halved year-on-year, with some encouraging recent auction results for shareholders to hang their hats on.

When combined with the extensive recent capex programme, this is why the company desperately needed a $30 million rights issue in June 2025. They’ve also managed to sell Fabergé for $50 million in August, of which $44.7 million has already been received.

Things need to improve quickly, as the loss for the six months was $24.6 million. The recent cash injections into the business won’t last long at this rate. There’s all to play for in the second half, including the commissioning of the second processing plant in the rubies business.

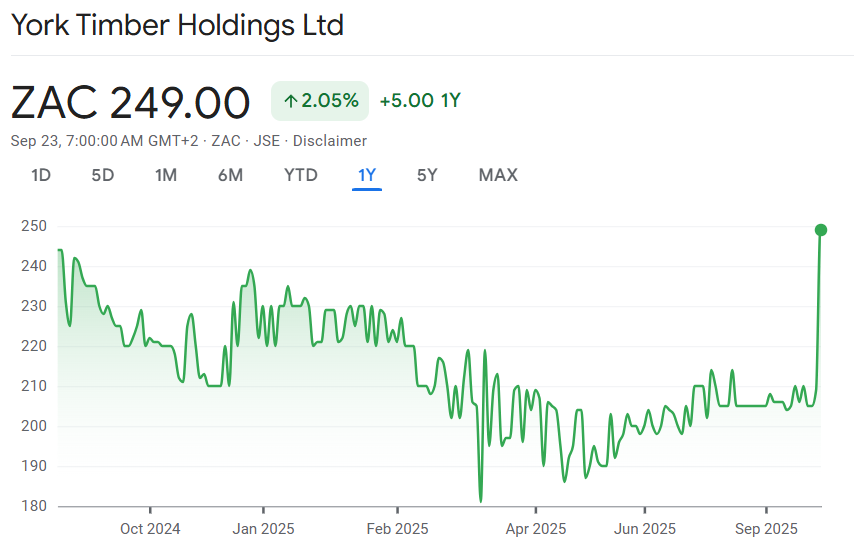

Traditional gaming assets (especially SunWest) drag Grand Parade lower (JSE: GPL)

As we’ve seen across the board, casino assets are struggling

The shine has really come off the casino industry in the post-COVID era. The pandemic forced people to find online sources of entertainment and many have never looked back, choosing alternatives like sports betting rather than going and sitting at the casino. That’s great news for the online operators and terrible for the owners of traditional casinos, which are large and expensive things to operate. With heavy fixed costs comes operating leverage, which means that a drop in revenue has an amplified impact on profits.

This is visible at Grand Parade Investments, where HEPS fell by 20% for the year ended June 2025 to 15.42 cents. They’ve decided not to pay a final dividend, so that’s also a bearish signal.

If you dig into the numbers, the main reason for the drop is a 15% decrease in Gaming revenue, with the investments in SunWest (primarily GrandWest – the biggest asset) down 20% and Sun Slots (almost as big) down 5%. To add to this, central costs were 17% higher, so the net impact on headline earnings from continuing operations was a drop of 25%.

Oddly, the Worcester casino has actually seen a far less severe year-on-year move, with revenue down 2.7% and EBITDA increasing from a very small base to R6.9 million. It’s a tiny asset vs. SunWest and Sun Slots, but it’s still interesting to see the resilience of revenue vs. SunWest where revenue fell by around 12%.

In terms of the outlook, the company is looking at Historical Horseracing, a segment that is apparently growing in the US by simulating horse races using actual past races. I truly cannot imagine a world in which people would rather bet on old horse races than on live sport, but I’m definitely not the target market for any of this stuff (sports betting included). My view is that the casino assets are in terminal decline, so I guess these companies need to look for growth wherever they can.

Mid-teens NAV per share growth at Remgro (JSE: REM)

Improvement at Heineken Beverages is an important part of the story

Remgro released results for the year ended June 2025. The company always tries to put the focus on HEPS for some reason, even though the market clearly cares more about the intrinsic net asset value (NAV) per share.

In case you needed any further evidence of this, HEPS was up by 38.4% in the past year and the NAV was up 16.5%. The share price is up 14.8%. Clearly, the valuation metric that matters is the discount to NAV, not the Price/Earnings multiple that uses HEPS. And yet, Remgro insists on HEPS being the hill that they will die on.

Of course, the trend in HEPS at the underlying portfolio companies is a major factor in their valuations, so the concepts are not completely divorced from each other. Remgro is enjoying positive momentum in Mediclinic, OUTsurance, Rainbow Chicken and RCL Foods, as well as Heineken Beverages which has been a massive headache since the Distell deal.

Mediclinic is no longer separately listed, so it’s worth digging a bit deeper into that story. One of the challenges being faced by the business is the difficult operating environment in Switzerland, where margins are being squeezed. Despite this, the management team has managed to achieve 5% growth in group revenue and 9% growth in adjusted EBITDA, so the Swiss challenges aren’t enough to offset the improvements made elsewhere.

Heineken Beverages also deserves further commentary, with a headline loss of R50 million in this period vs. a loss of R573 million in the prior period. There’s a big difference between positive momentum and a positive overall story. There are some significant non-cash costs in these numbers, without which the business would’ve recorded a profit of R90 million. Capevin has now also become a hangover of the Distell deal rather than a positive story, with a loss of R3 million vs. a profit of R79 million in the prior year. Aside from major changes to the underlying product distribution strategy, Capevin is suffering with a declining global spirits market.

Also on the negative side, TotalEnergies Marketing suffered a substantial negative stock revaluation. Energy businesses can be highly volatile things.

I think it’s worth highlighting that Dark Fibre Africa could only manage revenue growth of 1.5%. Vodacom (JSE: VOD) has fought so hard for the deal to combine its fibre business with that of Remgro, so hopefully growth will pick up in future thanks to that deal.

Another useful driver of earnings in this period was the much lower cost of corporate actions vs. the prior year. Remgro also reduced their finance costs through making changes to the balance sheet, specifically the redemption of preference shares.

Due to having excess cash on the balance sheet, Remgro has declared a special dividend of 200 cents per share. And no, I cannot for the life of me tell you why they’ve gone that route instead of more share buybacks when the shares are trading at a deep discount to the NAV per share.

Nibbles:

- Director dealings:

- A non-executive director of Momentum (JSE: MTM) bought shares worth R2.5 million.

- An associate of Des de Beer has bought another R218k worth of shares in Lighthouse Properties (JSE: LTE).

- ASP Isotopes (JSE: ISO) has confirmed that subsidiary Quantum Leap Energy recently became a controlling shareholder of Skyline Builders Group, which is listed on the Nasdaq with the ticker $SKBL. There were various steps in this dance, as there are two different classes of shares in Skyline. With all said and done, Quantum Leap Energy (and thus ASP Isotopes) has control of 79.14% of votes in Skyline. The CEO of ASP Isotopes has also invested in his personal capacity in Skyline. ASP plans to use Skyline as a platform to make acquisitions in the critical materials supply chain.

- Accelerate Property Fund (JSE: APF) will take every win they can at the moment, especially when the win takes the form of putting more cash on the balance sheet and reducing overall risk. The latest news is that the company has settled an insurance claim for business interruption insurance, which means they will receive R82.5 million. They might have gotten more if they fought it harder, but it’s not worth it to take that risk. This is a very helpful injection of cash, although nothing would help more than the Portside disposal circular going out and that deal closing!

- Rex Trueform (JSE: RTO) and African and Overseas Enterprises (JSE: AOO) aren’t the most liquid stocks around, so I’ll just give their trading statements a passing mention. They get bundled together as they are a group of companies. Rex Trueform expects HEPS for the year ended June 2025 to be up by more than 100%, coming in at 129 cents per share. African and Overseas Enterprises also expects a move of more than 100%, coming in at 110 cents per share. The reason they can both be so precise is that they’ve released the trading statements literally one business day before results are coming out. Again, trading statements just aren’t taken seriously enough by companies like these.

- Pan African Resources (JSE: PAN) has given the market an update on the planned move from the AIM to the London Main Market. It looks like this move will happen at the end of October. The importance of this corporate action is that it should increase Pan African Resources’ visibility in the UK market and make it viable for more institutional investors to hold the stock.

- Sebata Holdings (JSE: SEB) has updated on the market on the timing of the publication of results for the year ended March 2025. They expect to release results by 15 October.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE. Disclaimer.

")

")

")