Africa’s fintech evolution is a fascinating example of how a confluence of technological and customer behaviour trends can create not one, but several leapfrog moments.

The genesis of fintech’s success across the continent, especially payment providers such as Paystack, M-Pesa, Moniepoint, Mukuru, Momo Money and Flutterwave, is primarily due to the advances made in the telecommunications industry. As telecommunications providers built network infrastructure to support mobile phone access from Cairo to Cape Town, they unwittingly created the backbone that enabled feature phones and then smartphones to thrive across Africa.

It is the access created by these mobile technologies that has allowed consumers on the continent to connect to the global digital payments system, with PCs and laptops no longer a necessity. Before digital payments came into being, African consumers quickly adapted to new payment plans to go mobile, such as pay-as-you-go, which became available in South Africa in 1996.

In 2022, global consultancy McKinsey published a report called Fintech in Africa: The end of the beginning, where it stated:

“Our analysis shows that fintech players are delivering significant value to their customers. Their transactional solutions can be up to 80 percent cheaper and interest on savings up to three times higher than those provided by traditional players, while the cost of remittances may be up to six times cheaper.”

“Taken together with an influx of funding and increasingly supportive regulatory frameworks, these factors could signify that African fintech markets are at the beginning of a period of exponential growth if, as expected, they follow the trajectory of more mature markets such as Vietnam, Indonesia, and India.”

TELECOMS ARE BECOMING FINANCIAL SERVICE COMPANIES

Of further interest is the way in which, over the last decade, telecommunications companies have become financial service companies. Safaricom (owner of M-Pesa), MTN and Vodacom are examples of telecommunications companies that have leveraged their owned infrastructure to challenge, and often surpass, traditional banks to capture market share in the financial services sector, optimising opportunities for cross-selling.

Broadly speaking, African telecommunications providers have shown an appetite for calculated risk that their peers in Europe and North America would baulk at. Often, African providers are not just building telecommunications infrastructure at the greenfield stage, but other infrastructure taken for granted in older markets, such as roads, electricity and security, a role traditionally played by mining companies.

REGULATORY ENVIRONMENT AMONG KEY FINTECH CHALLENGES ACROSS AFRICA’S MARKETS

The fintech sector’s success across Africa’s markets does, however, run into its own challenges. According to McKinsey, the key challenges cited as stymying the continent’s fintech sector were scale and profitability, an uncertain regulatory environment, scarcity, and corporate governance.

Speaking to our clients operating across the continent, the regulatory challenge alone is one that poses significant delays and uncertainty for businesses.

Central banks and bodies that regulate the fintech sector play an outsized role in shaping national sector development. In fact, recent regulatory changes made by the Central Bank of Nigeria reportedly helped their fintech sector grow by approximately 70% in 2024.

Key to regulatory success is forming or leveraging existing relationships with regulators based on trust and mutual respect, which takes years to cultivate. Webber Wentzel partners with our clients to maintain and manage these relationships, working with specialist local firms and on-the-ground teams versed in the complexities of financial services and digital regulation.

On occasion, working with regulators also requires leveraging our legal expertise beyond the financial services sector, which is why it’s advantageous to partner with a full-service firm. While legal text can be interpreted in a limited number of ways, having the right personnel and expertise in the room is as much a success factor as legal knowledge, as noted by select clients.

INSURANCE – THE NEXT EXCITING MARKET

When speaking of fintech in Africa’s different markets, what is materially being referred to is Africa’s digital payments landscape. It has been the sector’s growth engine, with Africa accounting for around 70% of global mobile money payments in 2022.

But with payments reaching maturation, what’s the next frontier? According to some of our clients in the financial services sector, insurance is the next great fintech opportunity across the continent.

In 2022, the insurance penetration rate in East Africa’s various economies was dismally low: 2.14% in Kenya, and 0.62%, 0.74%, and 0.3% in Tanzania, Uganda, and Ethiopia respectively. The penetration rate of life insurance continent-wide was reportedly 1.6% in 2022, with South Africa accounting for 79% of total life insurance premiums in Africa.

Like the payments landscape, success will depend on having a nuanced understanding of local market conditions and consumer behaviour, in addition to conforming to the legal framework. For example, in Nigeria, a startup called WellaHealth has partnered with pharmacies to provide insurance products to pharmacy customers, knowing that most Nigerians will visit a pharmacy first, and self-treat before seeing a doctor.

As digital penetration continues to make inroads outside Africa’s largest markets, Africa’s fintech leaders will likely be joined by innovative newcomers in the next few years.

Liesl Olivier is a Senior Associate | Webber Wentzel

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

The bidding war worked out nicely for Assura shareholders (JSE: AHR)

The private equity bidders have upped their offer to compete with Primary Health Properties (JSE: PHP)

Assura is hot property. KKR and Stonepeak have been trying to seduce shareholders with a cash-based offer (as is always the case for private equity bidders), while fellow listed company Primary Health Properties has been using its listed status to try and persuade shareholders into a merger. Of course, the real winners in the situation of competitive tension are the shareholders of the target company.

After Primary Health’s initial offer was deemed to be inadequate to even be worth a look, it appeared as though KKR and Stonepeak were on their way to a successful deal. Primary Health then swooped back in with an upgraded offer that was interesting enough to force the Assura board to pay attention, calling a halt to the meeting to vote on the KKR and Stonepeak deal while they conducted due diligence on Primary Health.

KKR and Stonepeak have further sharpened their pencils, returning with what they have called a “best and final” offer that works out to 52.1 pence per Assura share.

The Assura directors must be getting whiplash at this point, as they’ve now swung their attention back to KKR and Stonepeak and called this a fair and reasonable offer that they intend to unanimously recommend to shareholders.

They’ve also commented that after doing due diligence on the Primary Health offer, they’ve decided that it “presents material risks” to Assura shareholders – of course it does, as it’s a merger rather than a cash deal. Assura couldn’t help but get in a dig at Primary Health’s portfolio, which they note as having higher exposure to public sector rather than private sector assets.

Primary Health released an announcement later in the day that “strongly disagrees” with the Assura assessment. They also indicated that government spending on healthcare is expected to be positive for the portfolio in years to come.

Cash is king. If someone puts a proper cash number on the table, that’s the deal that happens. This is how life works.

MultiChoice always seems to be in even more trouble than I thought (JSE: MCG)

They are losing linear subscribers locally and in Rest of Africa

Aah, MultiChoice – a company that boasts about 5.7% price increases in South Africa as “inflationary” and “disciplined” thanks to their strong cost control. This of course is while bleeding subscribers left and right, with 600k linear subscribers in South Africa having run for the hills. In Rest of Africa, the pricing increase was an average of 31% in local currency. While inflation in Africa is certainly much higher than what we are used to seeing in South Africa, the loss of around 600k linear subscribers elsewhere in the continent is an indication that perhaps their pricing strategy needs work. The total loss of 1.2 million subscribers is an 8% drop in the active subscriber base.

I don’t know what the incremental cost of adding a subscriber is, but it’s very hard to imagine that it wouldn’t be accretive to MultiChoice to be more affordable and attract more subscribers. The current strategy certainly isn’t working, with organic revenue growth of just 1% in the year ended March 2025.

They are still investing like crazy in Showmax, which of course they justify based on the loss of linear subscribers. This puts them squarely up against the likes of Netflix. Showmax subscribers increased 44% off a modest base, showing that there is some hope for that business. Still, group organic trading profit took a 9% knock thanks to the modest revenue growth being insufficient to offset the pressure of the investment in Showmax.

Once we move past “organic” numbers, we find a decline in revenue of 9% and a massive drop in trading profit of 49%. There was a free cash outflow of R0.5 billion in FY25 vs. an inflow of R0.6 billion.

The headline loss per share of 258 cents may be an improvement on the loss of 715 cents per share in the comparable year, but it’s still a substantial loss.

I can understand why MultiChoice needs to build a streaming offering. I just don’t agree with their approach to their linear business. In FY25, the South Africa linear business generated revenue of R33 billion and trading profit of R9.4 billion. By comparison, Showmax revenue was just R753 million and the trading loss was R4.9 billion – and that’s for the entire continent.

Again, this will hopefully become Canal+’s problem to manage. If it wasn’t for that transaction, it feels like MultiChoice would literally be running itself into the ground.

Naspers and Prosus earnings are through the roof (JSE: NPN | JSE: PRX)

I’m a very happy shareholder in the Bloisi era

I cannot overstate the importance of the management team in the companies that you invest in. In the previous era of Naspers and Prosus, I didn’t touch the shares as I had zero faith in the capital allocation strategy. In the Fabricio Bloisi era, it became obvious to me rather quickly that things were now different. I wrote about it at the time and indicated my decision to buy shares in the group (I chose Prosus). I’m so glad I did.

A trading statement for the year ended March 2025 reveals that core HEPS (which excludes gains on the sell down of Tencent) increased by 53.9% to 63.2% for Prosus, and 55.9% to 62.9% for Naspers. This is based on continuing operations, so it’s the best way to view the group. Including discontinued operations actually leads to slightly higher percentage growth rates.

Detailed financials are due for release on 23 June 2025.

Pan African Resources delivered in the second half (JSE: PAN)

The market gave me a gift in February and I took it with both hands

Back in February this year, Pan African Resources released an unfortunate set of interim numbers. The market hated them, mainly because Pan African went backwards at a time when the other gold miners were printing cash. The market dumped the shares, even though the company indicated that the second half should be much better for production and that a hedge on the gold price was due to expire at the end of February, giving them exposure to how strong the gold price had become.

That was good enough for me to say thank you to the market and buy the shares. Today, that position is 32% up. Not bad!

The second half has come through largely as promised, with record production at the company for a six-month period. Although they have fallen short of full-year guidance, coming in at 197,000oz vs. guided 205,000oz – 215,000oz, time has shown that the market overreacted.

Net debt is down 32% vs. the interim period and they expect to be debt-free during FY26 at current gold prices. This is helped by a production expectation for FY26 of between 275,000oz and 292,000oz, a jump of around 40% year-on-year thanks to things like the ramp-up at Evander being behind them now.

With the group approving a share buyback of up to R200 million, they are clearly feeling confident. With global geopolitics in such an inflationary position at the moment, I don’t blame them. I’ll be hanging onto my shares.

Nibbles:

Director dealings:

The director of Italtile (JSE: ITE) who needs to sell pledged shares this month has managed to offload another R31.3 million of them.

Associates of two directors of Ascendis (JSE: ASC) – including the CEO – bought shares worth R54k in aggregate.

Here’s another large forced sale of shares by a Discovery (JSE: DSY) director in relation to the maturity of a collar transaction. In this case, it’s Barry Swartzberg. He sold shares worth R74 million.

The CEO of RH Bophelo (JSE: RHB) bought shares worth R25k.

Here’s a surprise: the board of MTN Zakhele Futhi (JSE: MTNZF) has decided to fully unwind the scheme. This comes after a rally of 42% in the MTN share price this year. They announced the placement on Wednesday and a further announcement early on Thursday morning confirmed that they raised R3.0 billion in the process. They will now need to run through the settlement of the debt and the costs of unwind, with an announcement to come regarding the amount payable to investors.

African Rainbow Minerals (JSE: ARI) has hedged a significant portion of its stake in Harmony Gold (JSE: HAR). This takes the form of a collar hedge over 24% of the stake held in Harmony, or 2.84% of Harmony’s total shares. They’ve bought 18 million put options at a strike price of R234.85 and sold 18 million call options at a strike price of R562.40. Both options are exercisable in June 2030 (on average). Harmony’s current price is around R253, so they are mainly hedging against downside exposure here. They also talk about how this gives them access to funding in the future on efficient terms, so presumably they are thinking of using the hedged portion as collateral at some point.

With the mandatory offer circular out in the wild, Novus (JSE: NVS) is also able to acquire Mustek (JSE: MST) in the open market i.e. outside of the mandatory offer. They’ve acquired R26.4 million shares in this way, increasing their stake in Mustek from 35.07% to 38.60%.

Sappi (JSE: SAP) is trying to increase its visibility to North American investors. With around 70% of the current shareholder base being South African, they are looking to attract more international investors over time. To help achieve this, they are joining the OTCQX trading platform. There’s some pretty decent liquidity on there actually, with a number of companies choosing this route rather than a full-blown listing on e.g. the NASDAQ.

Speaking of visibility to US-based investors, AngloGold Ashanti (JSE: ANG) has been added on a preliminary basis to the Russell indices. There are a few of these indices, with AngloGold still waiting to see whether they are in the Russell 1,000 or Russell 2,000 (in addition to the Russell 3,000 and Russell Midcap) indices. This matters because of the large number of index-tracking funds that are driven by these indices. Those funds will now need to buy and maintain a holding in AngloGold.

FirstRand has received approval for the HSBC South Africa deal (JSE: FSR)

They are essentially giving HSBC an orderly exit from South Africa

Back in September 2024, FirstRand announced that they would be acquiring the clients, assets and liabilities as well as employees of HSBC’s branch in South Africa.

The group has now received regulatory approval for the deal. This is a boost to FirstRand’s corporate and investment banking business (RMB), as the clients are typically multinational organisations operating in South Africa (hence why it was so important to HSBC to achieve a smooth transition for those clients).

The transaction will be complete by the end of October 2025.

Another klap for KAP (JSE: KAP)

The share price closed 22% lower after a trading statement

KAP released an update for the 11 months of the financial year up until May 2025, so that’s essentially a pre-close update. The interim period was unpleasant for KAP, with the group having reported a 21% drop in HEPS at that stage. Things have only gotten worse, with the expectation being a drop in HEPS of at least 30% for the full year.

This is despite PG Bison getting the new MDF line in Mkhonda up and running properly by the end of the year, achieving full utilisation in the fourth quarter vs. only 60% in the first half of the year during ramp-up. Despite this, operating profit fell due to depreciation and other costs on the new line, along with depressed export prices. It’s never a good look when your shiny new facility is a drag on profitability!

At least Safripol went in the right direction, with both revenue and operating profit higher. The same can be said for Sleep Group. Blink, and you’ll miss the highlights package in these numbers – I’m afraid it’s only those two divisions.

Over at Unitrans, revenue and operating profit fell despite the restructuring activities at the end of 2024. They are now restructuring the petrochemical operations as well.

Feltex had a better second half than first half, but still faces significant challenges as production comes under pressure at lower vehicle manufacturers. Revenue and profit were down for the full year.

Optix revenue and operating profit fell, with performance well below KAP’s expectations.

Speaking of being below expectations, their debt reduction efforts are running behind schedule because of pressure on EBITDA.

These really are poor numbers. The share price closed 22% lower and I’m not surprised. Things just never seem to get better at KAP, with there always being something that ruins the story. With an imminent change in CEO, the market will be looking for decisive action that fixes a situation where KAP is trading 33% below where it was 5 years ago – in the throes of COVID!

Kore Potash has announced details of a funding plan for the Kola Project (JSE: KP2)

Although they aren’t explicit for some reason, I think this is the Summit Consortium

Companies sometimes do strange things when it comes to the wording of their announcements. Since forever, we’ve been hearing about how the Summit Consortium is the likely source of funding for Kore Potash’s Kola Project, but they’ve also made it clear that other parties may emerge. We now have details of a funding package, but there’s no mention of the Summit Consortium anywhere in the announcement. I’ve gotta tell you that online searches aren’t conclusive, so I think this is the Summit Consortium package coming through (Occam’s Razor and all that), but I can’t say for sure.

These are still non-binding term sheets, so anything could happen. All we know for sure is that a package of $2.2 billion is on the table, structured as a combination of senior secured project finance and royalty financing. The counterparty is OWI-RAMS, a Swiss investment platform part of the portfolio of Record Financial Group, a UK-based multi-asset investment company. OWI-RAMS invests in the food security value chain. You can’t eat potash, but you certainly can (and should) use it as plant fertiliser.

Interestingly, the funding needs to be structured in accordance with Shari’ah principles. I did a great podcast with Yusuf Wadee of Satrix last year on this topic, in case you want to learn more about these principles.

This structuring requirement is why they talk about a profit payment rather than an interest cost, coming in at between 6.8% and 9.3% per annum (depending on the outcome of the due diligence). This is on the senior facility, which represents around 70% of the total funding requirement. No payments are due for the first 49 – 50 months during the construction and ramp-up phase, with the capital amount then amortised over the subsequent 7 – 8 years. As you would expect, there are a number of financial covenants attached to this, including limitations on dividends unless specific interest cover ratios are in place.

The remaining 30% of the funding is a royalty arrangement, giving the financier a share of the gross revenues generated by the Kola Project over the life of mine. This is like selling shares in the company, except the shareholder has no exposure to the costs of production and just skims an amount off the top. While the senior debt is outstanding, the revenue-sharing is equal to 14% of gross revenue. Thereafter, the percentage is 16%.

Cleverly, Kore Potash includes a table of what it would look like for shareholders if they raised the royalty financing amount ($655 million) on the market instead of through this deal. Estimated dilution would be somewhere between 60% and 80%, depending on the pricing achieved. They do however acknowledge that the royalty rate of 14% to 16% is significantly higher than the typical market percentages.

I can’t help but wonder if we might see other potential sources of funding emerge, including strategic investors who might want to inject capital in order to reduce the requirement for the costly royalty-financing agreement.

The share price closed 2.3% lower on very strong volumes on the day, so the market wasn’t exactly thrilled with these terms.

Premier is a great example of when leverage works in your favour (JSE: PMR)

Margin expansion does wonders for an income statement

Premier’s share price is up 114% over 12 months. That’s been great news not just for Premier shareholders, but for punters in Brait as well.

Supporting this share price increase is revenue growth of 7% for the year ended March 2025, which was enough to drive EBITDA higher by 14.7%. HEPS increased by 26.8% to 943 cents, which means that the current share price of R136 is a pretty fully Price/Earnings multiple of 14.4x. I would argue that the re-rating has largely played out, which means that share price growth from here onwards will primarily be driven by earnings growth.

Thankfully, both underlying divisions grew revenue, with Millbake up 5.7% and Groceries and International up 13.3%. Interestingly, the margin story is the other way around, with Millbake’s EBITDA up 14.7% and Groceries and International only up 9.2%. The latter was impacted by some operational disruptions and the unrest in Mozambique.

The economics of baking businesses like Millbake mean that relatively modest revenue growth can drive significant earnings growth due to the inherent operating leverage (fixed costs) in the business model. The other side of that coin is that weak revenue growth is leveraged up into an ugly outcome.

The expectation for FY26 is only moderate revenue growth, with the group expecting to pass cost savings on maize input prices through to consumers. There will be other sources of inflation though, like Eskom tariff hikes and other South African infrastructure issues. With no shortage of investment in improving its business over time, Premier looks pretty well positioned for those challenges.

Southern Palladium is raising capital this week (JSE: SDL)

The differences between the rules of the Australian Stock Exchange and the JSE are stark here

Southern Palladium is looking to raise capital this week. We don’t know how much yet, as they haven’t made a detailed announcement. The reason we know that this is happening is because a trading halt has been put on the shares on the Australian Stock Exchange, pending a detailed announcement. On the JSE, there is no such trading halt.

This is a key difference in approach between the rules of the Australian Stock Exchange and the JSE, leading to some really awkward situations for companies. I’m led to believe that this is why Renergen didn’t take the route of a cautionary announcement for the ASP Isotopes deal, for example.

For Southern Palladium, the halt will be in place until the earlier of a detailed announcement regarding the outcome of the capital raise (which seems to be structured as a placement to specific investors), or the commencement of trade on 12th June.

The Australian approach seems very clunky vs. the JSE approach of cautionary announcements.

A great day for Telkom – and a great year! (JSE: TKG)

The share price closed nearly 8% higher based on results and a special dividend

Telkom released results for the year ended March. Although group revenue was only 3.3% higher, this was enough for adjusted EBITDA to jump by 25.1%, which means adjusted EBITDA margin was 470 basis points higher at 26.9%.

Thanks to the extent of free cash flow generated by this performance, net debt to group adjusted EBITDA decreased from 1.8x to 0.6x. Interest-bearing debt is R2.6 billion lower. And just to add some sprinkles on top, an ordinary dividend of 163 cents per share has been declared, along with a special dividend of 98 cents per share related to the cash proceeds of the Swiftnet disposal.

This is why the Telkom share price is now up 82% over 12 months, boosted by a day in which it closed nearly 8% higher in celebration of these numbers. This is further proof that investing isn’t about picking the best companies in the world – it’s about choosing the stocks that offer the best risk/reward trade-offs at a particular valuation.

One of the key underlying growth drivers is Telkom Mobile, which increased revenue by 10.2% and saw EBITDA margin expand to 20%. The results presentation noted that Telkom has enjoyed ten consecutive quarters of market-leading service revenue growth in this business.

Openserve’s fibre revenue was up 5.9%, but this wasn’t enough to put Openserve in the green overall, with total revenue down 1.3%. With 82% of revenue now from fibre-related services rather than the legacy voice business (up from 69% two years ago), the EBITDA margin is up to 32.4%.

BCX still has some way to go, with fibre-related revenue up 12.7% and cloud up 5.8%, but IT hardware sales down 23.7%. The improving mix of services saw an uptick in EBITDA margin from 9.0% in the first half of the year to 13.2% in the second half.

Telkom expects annual revenue growth in the mid-single digits and ongoing improvement in EBITDA margins, although it does seem as though the positive step-change in the group is now behind them. Well done to those who believed in this story and bought into it!

Nibbles:

Director dealings:

As part of the substantial capital raise by Lighthouse Properties (JSE: LTE) that took place earlier this week, Des de Beer subscribed for shares worth R40.5 million.

Despite the fact that Gerrie Fourie is due to retire as CEO of Capitec (JSE: CPI) in July 2025, he’s bought shares worth R6 million.

A director of PSG Financial Services (JSE: KST) and two directors of different underlying subsidiaries bought shares worth R1.3 million.

An independent non-executive director of STADIO (JSE: SDO) bought shares worth R360k.

A director of a subsidiary of Tharisa (JSE: THA) sold shares worth R265k.

I’m just mentioning this trade for completeness, rather than because you can read anything into it. As we’ve seen recently, founding directors of Discovery (JSE: DSY) have been selling shares as pat of the unwinding of collar hedge positions, as the share price has closed above the call option price. These sales aren’t on a voluntary basis. The latest such example is Adrian Gore, who sold shares worth R38 million.

Here’s another trade that you can’t read much into – as previously warned, a non-executive director of Italtile (JSE: ITE) sold pledged shares worth R120k.

Metair (JSE: MTA) has appointed a new CFO, having previously announced the resignation of outgoing CFO Anesh Jogia with effect from 1 April 2025. As the group is going through so much change at the moment, the CFO role is truly critical. Alastair Walker has been appointed to the role with effect from 1 July 2025. Encouragingly, this is an internal appointment, as he currently runs the treasury at Metair. His previous corporate finance exposure will come in handy at Metair as they look to evolve the group.

I don’t often comment on institutional investor movements on share registers, but this one is interesting enough to warrant a mention. With Nutun (JSE: NTU) trying desperately to stabilise and grow the business, 36ONE has increased its stake from 4.47% to 6.48%. That’s bullish.

Putting another feather in the cap of NEPI Rockcastle (JSE: NRP), they have been included in the FTSE EPRA NAREIT Global Emerging Index, an absolute mouthful that essentially gives them an inclusion in any ETFs that track the index. It also improves visibility among global investors, which can lead to a broader shareholder register over time.

Trustco (JSE: TTO) has renewed the cautionary announcement related to the potential delisting from the JSE, Namibian Stock Exchange and OTCQX market in the US, with the plan being to subsequently list on the Nasdaq. They are still working on the steps required for this transaction.

4Sight carried on where the interim period left off (JSE: 4SI)

And yet the market is largely ignoring this small cap

4Sight’s website might be drowning in a soup of tech buzzwords, but the underlying corporate story is becoming increasingly interesting to follow. They are doing some smart stuff, like the cleverly structured B-BBEE deal that was announced in May this year. I appreciate it when small caps behave like larger companies, as it shows that the foundations are there for growth.

And growth is certainly the order of the day, with a trading statement for the year ended February 2025 suggesting an increase of between 27.9% and 38.6% in HEPS. I had a look at the interims to August 2024 and HEPS was up by 35.5%, so they’ve basically carried on where they left off at the halfway mark.

Despite this, the market isn’t paying much attention to the stock, with no obvious direction over the past year apart from the choppy bid-offer spread. To be fair, the suggested HEPS range of 6.932 cents to 7.510 cents vs. the current share price of 70 cents puts it on a pretty full P/E by small cap standards. Still, this is worth keeping an eye on.

A great year for Alexander Forbes (JSE: AFH)

This supports the share price growth over the past 12 months

The Alexander Forbes share price has been volatile, but heading higher in recent times. The 12-month performance is a gain of 38% and the release of results for the year ended March 2025 explains why that has happened.

Normalised HEPS has increased by 23%, boosted by operating income growth of 13% thanks to a combination of organic growth and the benefit of acquisitions made in previous years. Operating expenses were up 11% including the impact of major accounting changes, or 6% if you look through a more business-focused lens on the operations. Profit from operations increased by 14% and cash from operations grew by 15%, so mid-teens growth is probably the correct summary of this performance.

Although the dividend was only 10% higher at 55 cents per share for the full year, there’s a special dividend of 10 cents per share as well to sweeten the deal. Companies use special dividends when they don’t want to create an expectation in the market that higher dividends have been baked in, so this isn’t as strong a signal of growth as would’ve been the case had the ordinary dividend increased in line with earnings. They indicate that part of the special dividend is the receipt of proceeds from successful litigation, but that doesn’t really explain why they were so conservative in the payout ratio for the ordinary dividend in this period.

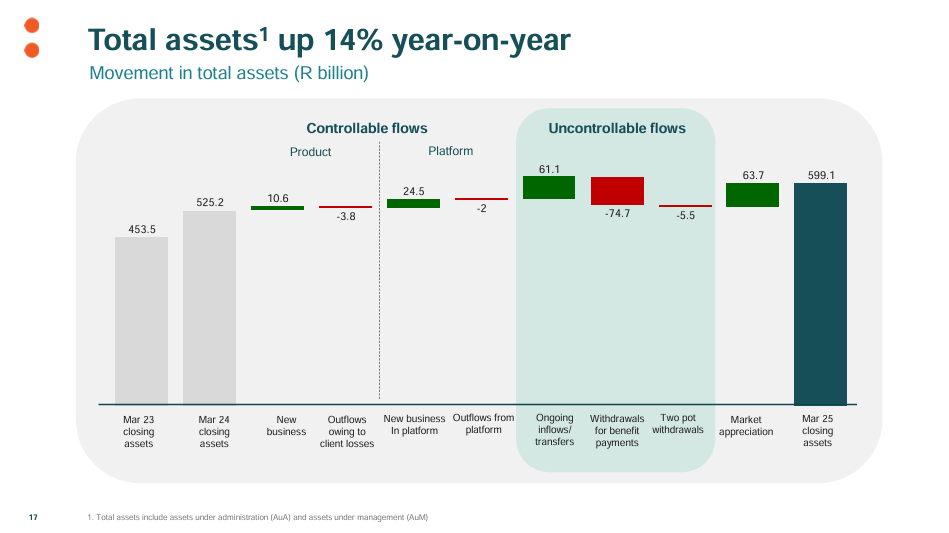

Other metrics that I think are worth highlighting include 4% growth in the number of active retirement members, as well as a 23% jump in umbrella assets under management. There’s also this pretty interesting chart in the analyst presentation that shows how they think about the different types of flows:

No profits at Aveng this year (JSE: AEG)

Construction companies are only as good as their worst projects

Aveng has flagged that they will report a headline loss per share for the year ending June 2025. Quite how bad it will be, we just don’t know yet. Either way, it’s a very ugly swing vs. HEPS of A$29.6 cents in the comparable period.

As is usually the case for construction companies, there are just a couple of projects letting the whole team down. Both of them are in McConnell Dowell, which Aveng is trying to figure out what to do with that business from a strategic perspective. If you’re looking to sell or separately list something, you want to do it when the going is good, not when there are losses.

Within McConnell Dowell, the New Zealand and Pacific Islands operations have grown their profits. The Australian side was break-even in the interim period and deteriorated in the second half, with the Kidston Pumped Hydro project costs running away from them. The weather has been a major factor here, leading to a delay in the work by a number of months. Whether or note they can recover any of these costs through commercial claims and negotiations with the client remains to be seen. Other than the Kidston project, the business is profitable. And finally, in Southeast Asia, the Jurong Region Line project is running in line with the revised project plan and cost.

Outside of the infrastructure segment noted above, Built Environs is profitable and growing. They are light on details for mining business Moolmans, which suggests that they might be having a trickier time there as well. Generally, when companies have a good news story to tell, they tell it.

Moolmans is also up for sale by the way, with negotiations in progress with interested parties. As you can see, there are a lot of moving parts for this group, with a likely outcome being a break up and eventual name change of whatever the listed entity is. At this stage, nothing is certain.

The Aveng share price has cratered this year, having lost half its value year-to-date.

Barloworld gets the green light from the Competition Commission (JSE: BAW)

Subject to conditions, as usual

Barloworld is currently under offer at R120 per share, as you are probably aware. The scheme of arrangement for this deal failed to garner sufficient support, so everything now depends on whether enough shareholders accept the offer to make it viable for the offerors. Recent results at Barloworld (and a sector peer like Bell Equipment) have made me inclined to think that more shareholders might be wiling to accept the offer than before. We will have to wait and see.

In the meantime, Barloworld has been busy getting regulatory approvals in place. The Competition Commission has approved the deal, subject to a 13.5% B-BBEE empowerment transaction being executed in Barloworld after the delisting. This is effectively to replace the empowerment that currently stems from the PIC being a shareholder, as the PIC has agreed to accept the offer.

The Competition Tribunal still needs to sign off on the deal. Although it does sometimes happen that the Tribunal disagrees with the Competition Commission’s recommendation, this is quite rare.

The offer to shareholders is open until 30 June 2025. We will know soon enough whether this thing is going ahead and I suspect that an updated view on the acceptance rate will be released in the next couple of weeks.

Lighthouse had no trouble raising R400 million in equity (JSE: LTE)

The property sector is hot once more

Property funds are popular things on the JSE. There are very deep pools of institutional capital out there, which means that high quality property funds tend to have no trouble in raising hundreds of millions of rands in the space of a morning. This is fine. The problems start when the middle-of-the-road and then low-grade funds start raising without any issues – at that point, we are in bubble territory. I see no evidence of that yet.

Lighthouse Properties is a good example of a solid local property fund, even though their investment story is centred firmly on Europe. On Monday morning, they announced that they wanted to raise R100 million through an accelerated bookbuild process, with the announcement reminding the market that the fund’s acquisitive activity has focused on Portugal and Spain.

Perhaps thanks to Carlos Alcaraz reminding everyone that the Spanish are a tenacious and talented bunch, the market responded positively and Lighthouse announced that the capital raise would up increased to R300 million. By the time the dust settled, they had actually raised R400 million at R8.20 per share – and the book was still oversubscribed at this level.

To give you a sense of pricing, the share price opened at R8.40 on the day, so this raise is at a slight discount to the prevailing market price.

Oceana hurt by fish oil prices (JSE: OCE)

There are just so many variables in this industry

Agriculture and mining are considered to be cyclical, risky businesses as they are so reliant on commodity prices that are completely outside of their control. When it comes to fishing businesses, you can then layer on the additional risks of variable catch rates and all the other challenges that the ocean is capable of dishing up. This is why you can get volatility in the Oceana share price like this:

The six months to March 2025 were rougher than the seas for Oceana. Although revenue increased by 2.9%, HEPS took a horrible knock of 43.9% and the dividend was much the same story, down 43.6%.

The main problem was global fish oil pricing, which fell based on the Peruvian anchovy resource coming back to the market. This hammered the American business from a year-on-year perspective (operating profit down 55.6%), with improved performance in South Africa (Lucky Star as the key segment, with operating profit up 35.9%) unable to offset the impact. Despite margins at Lucky Star improving, group gross profit margin fell from 34.1% to 27.8%.

To add insult to injury, the net interest expense jumped from R93 million to R144 million due to higher borrowing levels. When the operations had a tough time, it obviously only makes things worse if finance costs moved significantly higher. The pressure on the balance sheet came from strategic buying of inventory, ensuring consistent supply in an uncertain trade environment. One would hope that this will normalise in the second half of the year, as cash from operations was just R10 million in this period vs. R634 million in the comparable period.

The net impact of lower profits and higher debt is that net debt to EBITDA increased from 1.2x to 2.2x. Although the group is in compliance with all lender covenant requirements, I don’t think they can realistically run the balance sheet this hot for too long. To be fair, it looks like much of the inventory investment is to support the Lucky Star business, which is where they just can’t afford to miss out on any sales at the moment.

There’s little indication that the second half of the year will provide a significant improvement on the first half, as global fish oil prices are expected to remain under pressure. The US tariff environment is interesting, as it might assist Daybrook in that domestic market. Overall, they’ve done their best at Oceana to position the group for the best possible second half under the circumstances, with shareholders thanking their Lucky Star as usual.

A flat period at Omnia (JSE: OMN)

But not if you look at a share price chart

At first blush, Omnia’s results for the year ended March 2025 just look “boring” – revenue was up 3% and operating profit was essentially flat, while HEPS increased by 1%. This isn’t a story that will be passed down for generations.

And yet here is the share price chart over the past 12 months, with plenty of action:

Market sentiment is an incredible thing, leading to vast differences in the valuation of roughly the same underlying cash flows.

If we dig deeper into Omnia, Agriculture saw a dip in revenue of 2% and an increase in operating profit of 3%, so not much to report there. Mining was stronger, with revenue up 10% and operating profit up by a juicy 13%, with solid growth in some markets outside of South Africa as well. Sadly, Chemicals was a very different story, with a nasty swing into operating losses despite revenue increasing by 2%.

I honestly don’t have a clue how the global chemicals markets work, but perhaps I’m just feeling browbeaten from reading about “chemicals” in Sasol and now these numbers in Omnia.

In summary, the Chemicals segment was a nasty drag on earnings, bringing the group to a flat position overall despite the variance in segmental performance. This is a common situation in corporates. As a further overhang on the story, the fight with SARS still hasn’t been resolved, with Alternative Dispute Resolution proceedings hopefully being finalised soon.

It’s all about the margins at PPC (JSE: PPC)

Profits are what count

PPC has released results for the year ended March 2025. You won’t find the happy news on the revenue line, where group revenue decreased by 1.9%. But as you move down the income statement, you’ll find that HEPS more than doubled from 19 cents to 40 cents! For those who only trust cash earnings growth, you’ll be pleased to note that the ordinary dividend is up 28.5%.

What matters more to you – strong revenue growth and low profits, or muted revenue and great profits? If those are the only two options available, it’s clear that the latter is better. The holy grail is of course great revenue growth and better margins, but have you seen the state of South African infrastructure investment?

Cement volumes in the SA and Botswana segment fell 2.3%, but revenue was up 0.6% due to positive pricing moves. EBITDA jumped 31%, taking EBITDA margin 260 basis points higher to 11.0%. Most importantly, this segment is finally paying a dividend, after such a long period of being at the mercy of the banks.

In Zimbabwe, volumes were down 5.5% and revenue fell 6.7%. Despite this, EBITDA was up 26% and EBITDA margin was up a meaty 700 basis points to 27.2%. Zimbabwe has been a reliable payer of dividends (if you can believe that), up from $11 million to $13 million in this period.

The CEO talks about the Awaken the Giant strategy. Right now, they are certainly a lot more awake when it comes to profits. There is of course a practical limit to how far you can drive profit growth without revenue growth, so investors will want to see revenue increases coming through. PPC knows this, hence the decision to build a new integrated plant in the Western Cape. Although South Africa as a whole may have weak supply-demand dynamics for cement, there’s significant growth in the Western Cape and they see the opportunity there.

As a final note, finance costs were down 19.1% as debt levels dropped significantly. This is a wonderful turnaround story.

Insights from Santova’s latest presentation (JSE: SNV)

Although it deals with February year-end results, there’s much more to it

Santova recently announced the acquisition of Seabourne in the UK, giving the group deeper exposure to the eCommerce sector in Europe through a business that has been built to handle smaller, more frequent packages rather than bulkier items stored for a longer time. This is an interesting play by Santova and one that was followed up by extensive buying of shares by directors, which is always a positive sign.

The group has made the annual results presentation available to the market, with the nuance being that it includes plenty of strategic thinking in the context of the Seabourne deal. In other words, this is far more than just a normal numbers deck.

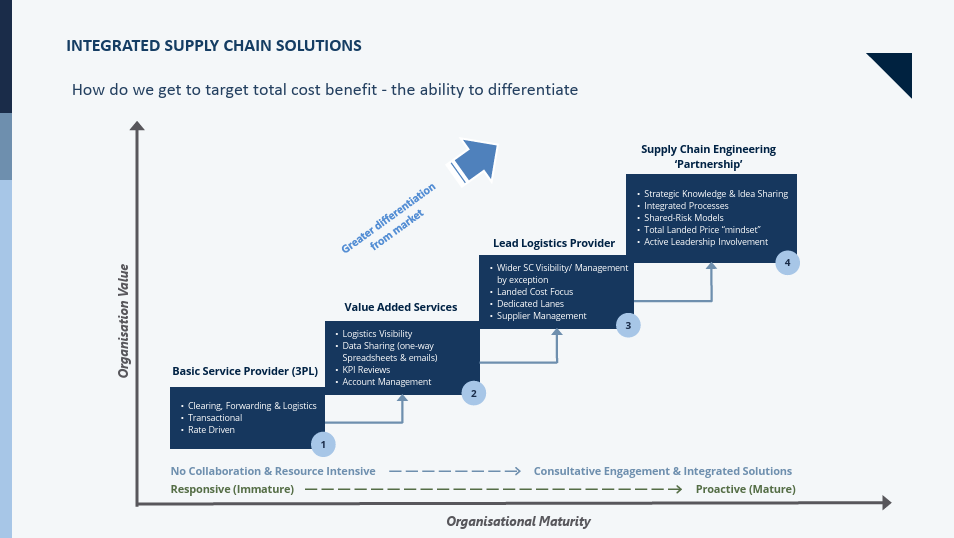

This struck me as a pretty useful slide, as it shows how companies in the logistics sector build a wider moat over time:

Unsurprisingly, the presentation is filled with references to how changeable global conditions are. It’s not just the trade war and associated risks that are relevant – it’s also the kind of wars fought with bullets and missiles that disrupt trade routes. Santova has a truly global business (only 17.1% of new client revenue came from Africa in this period), so they are exposed to the broader geopolitical environment.

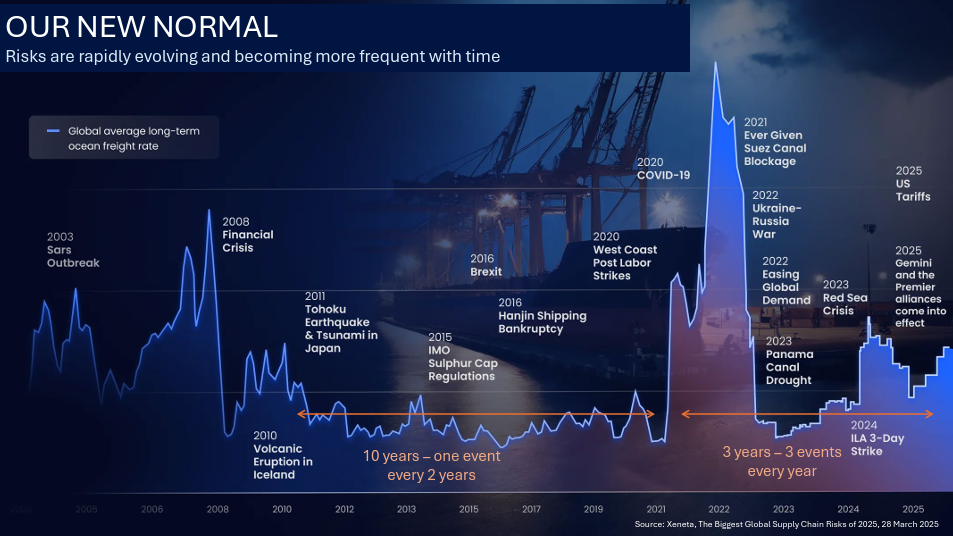

And of course this is before taking into account some of the other disruptions in the sector, shown in this pretty epic slide:

Despite this high-risk backdrop, there are strong growth opportunities. eCommerce is an incredible force at the moment, shifting demand for space from retail into industrial as more orders are fulfilled from warehouses rather than stores. This is changing the game in the sector, with Santova noting that the Netherlands is the “predominant gateway” to Europe. Interesting.

Another trend they reference is “friendshoring and nearshoring” as opposed to just onshoring, which means bringing supply chains into friendlier territories even if this comes at a greater cost. Supply chain security is a higher priority than just cost of production, so that points to a more inflationary environment overall.

The bear case for Santova is ironically also the bull case, with the question being whether Europe can go from being sluggish to exciting. A knock to US exceptionalism doesn’t necessarily mean that Europe will suddenly spring into life. Revenue and profits fell in the region in the latest financial year, with Santova making the brave decision to invest in Seabourne despite the risks. Another angle to the bear case is of course the US trade lane as well, as US government policy is firmly focused on encouraging domestic consumption at this time.

Santova’s share price has climbed nearly 28% in the past month. The market is enjoying the combination of the recently announced deal and the extensive director buying. I also thoroughly enjoyed how detailed the investor presentation is, as it really is helpful in understanding all the pros and cons of the sector at the moment.

Nibbles:

Director dealings:

A director of a major subsidiary of KAP (JSE: KAP) – PG Bison, to be exact – sold shares worth R6.5 million.

The CFO of Sirius Real Estate (JSE: SRE) and his immediate family members bought shares worth R585k.

An associate of the company secretary of Cashbuild (JSE: CSB) sold shares worth R59k.

Although there were some directors of Ninety One (JSE: NY1 | JSE: N91) who sold vested shares, there were also a few who kept the entire amount. And of course, there were those who sold only the taxable portion. I’m calling it a draw, with no obvious pattern in the behaviour.

This is just a reshuffling of chairs, so I haven’t included it in the director dealings section as I don’t want to create the wrong impression that this is a trade that should be interpreted as a signal. It’s just a reminder of the sheer extent of the wealth of the Christo Wiese family that they’ve moved around some Collins Property Group (JSE: CPP) shares between family entities with a total value of around R300 million.

Oasis Crescent Property Fund (JSE: OAS) announced that holders of 72.5% of units in the fund elected to receive a cash dividend, while holders of the remaining 27.5% opted to receive new units instead.

I’m glad to see that Mpact’s (JSE: MPT) shareholder impasse regarding non-executive director remuneration has been solved. There was an insane situation for a while where directors were appointed to the board of a subsidiary instead of the holding company as that was the only way for them to be paid. Perhaps the weirdness between Mpact and Caxton (JSE: CAT) is behind us.

The co-founder and honourary chairman of Mr Price (JSE: MRP), Stewart Cohen, will be retiring from the board in August this year. He co-founded the business in 1985, so it really has been an incredible journey. Cohen turns 80 this year and is ready to step away from formal duties, freeing up more time for for the Mr Price Foundation and other social projects. He will give strategic input to management in a non-remunerated advisory capacity.

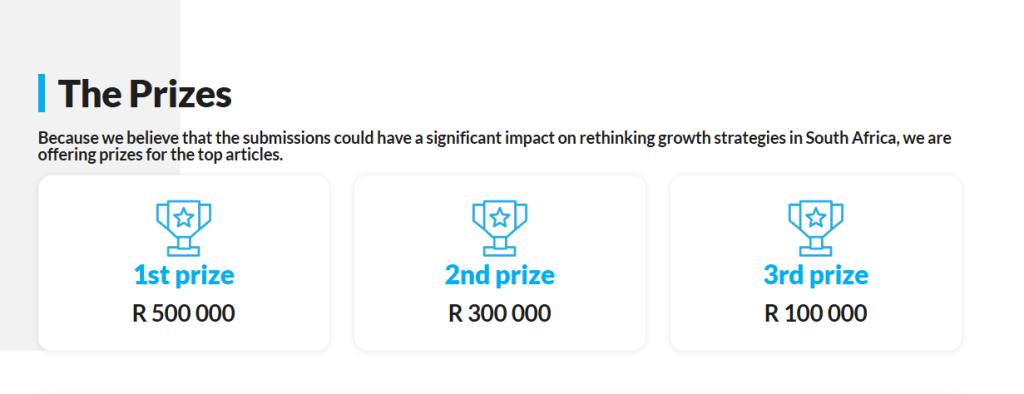

PSG Financial Services is the proud sponsor of the Think Big South Africa competition, in collaboration with Economic Research Southern Africa (ERSA). PSG wants to encourage South Africans to get involved in their country at the highest level, bringing forward policy ideas and constructive solutions to drive conversations and real change in our country.

The 2025 topic is How Capital Markets Enhance Economic Performance and Facilitate Job Creation. Papers are due for submission by 30 August 2025. In addition to the fantastic opportunity to drive change in our country, there’s an impressive first prize of R500,000 and there are several other cash prizes as well.

To discuss the importance of this competition and why PSG is so proud to be involved, PSG Financial Services CEO Francois Gouws joined me on this podcast.

You can find out more about the competition at this link.

Full transcript:

Intro: This episode of Ghost Stories features Francois Gouws, the CEO of PSG. PSG is the sponsor of the Think Big South Africa competition. This is an opportunity to make your voice heard, drive policy in South Africa, and earn some pretty impressive prize money along the way. The 2025 topic is the role of capital markets in enhancing economic growth and job creation in South Africa, and the first prize for this competition is a significant R500,000. We dig into the backstory of this competition and why PSG is so proud to be involved here.

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast with your host, The Finance Ghost. And I’m particularly excited for this one because we are doing something, I think, very different and very important for this country that we know and love.

My guest on this episode is Francois Gouws. He is the CEO of PSG Financial Services. And although there’s definitely a case to be made for talking about a share price chart that seems to be going to the top right of the page all the time – it really is a great business and I’ve written about it many times – that is actually not what we will be talking about today. Francois has another passion and so does the team at PSG around just driving South Africa forwards and rewarding the thinkers who can bring great ideas.

So, Francois, thank you so much for your time and interest in doing this. I’m really looking forward to this conversation. I think we’re going to learn some interesting stuff.

Francois Gouws: Thank you. Looking forward to it.

The Finance Ghost: So, I think as finance professionals especially, but just South Africans in general, we so often get bombarded with bad news, right? We really do in South Africa. But it does feel like there’s been a lot of good news lately as well, which is pretty exciting. I mean, load shedding is almost completely gone. I think there’s been a lot of realisation that as an emerging market, yes, we have our challenges and sometimes we get dragged through the mud in the international media, but there are a lot of opportunities here for not just investors, but also entrepreneurs. I guess I’m a case in point in some respects, having started this business five years ago. I can’t imagine where else in the world I would want to live but South Africa, I love it here and this is where I want to build things.

You are here in South Africa, so clearly you feel the same. And of course, PSG’s business is in South Africa. That’s really its heart. But still, even with all of that said and the obvious business importance of South Africa, there aren’t a lot of corporates I think that look to play a genuinely active role, like you are doing in our society with your Think Big South Africa competition. And obviously that’s what we’re going to dive into in a lot of detail in this podcast.

But before we get into the real meat of it, could you just give us some background to the Think Big South Africa competition and why you believe so strongly that this thing is important?

Francois Gouws: Thank you. PSG is exclusively a South African company, so all our profits are generated domestically, and that means that you’re dependent on the South African economy. So if, if things go well here, then our business tends to do well and obviously the reverse. As commercial individuals, we always hope for the best, but we plan for the worst. And if there’s areas that we see require attention, we try and participate. And I think there’s been a couple of big topics that people have talked about in South Africa, but I think that last year we said that economic growth is a key driver for fixing inequality and dealing with poverty and dealing with unemployment. We had a lot of interest in that. And I think that debate on economic growth continued into the current year.

And I think this year, being a company that operates in capital markets and sees the need for finance, which is in short supply at the present moment, both locally and internationally, we thought it’d be a good idea to talk about it and specifically what the benefits of the capital markets, particularly as it helps economic performance and ultimately how it creates jobs. So, we’re eagerly awaiting what will come through in terms of the various essays and participants, but we think it’s a big topic, and I think you can’t really engineer economic growth if you can’t raise finance to support it. I think it’s going to be a critical debate, not just this year, but I think it’ll carry on into next year.

The Finance Ghost: Yeah, absolutely. I mean, as someone who’s obviously very passionate about capital markets myself, it is great to see this topic coming through. I’ve got to tell you, I’m pretty tempted to actually enter the competition, having looked at the topic and some of the requirements, it looks pretty interesting. So, we’ll have to see. We’ll have to see how that goes.

But you’re doing this in a partnership, right? This is with Economic Research SA. So how does that partnership actually work? Why did you partner with them? I’m interested in the backstory to this thing, actually.

Francois Gouws: Economic Research Southern Africa is a credible organisation that’s participating in all the key topics. Of course, they’ve got access to all the various universities, they’ve got a wide group of participants that attend their various conferences and so on. I think it adds credibility. It also brings impartiality; it brings objectivity to an important topic. And I think when you’re debating these issues, I think you’re always careful of bias and you want critical analysis. And I think that’s a key contribution which they make.

The Finance Ghost: Bias is a fascinating thing, right? Anyone who has spent any amount of time buying and selling shares will understand bias very well. Or at least should make an attempt to understand bias very well because it’s strongly gets in the way of critical analysis. And South Africa has got lots of different biases, like any country, I suppose, but ours is particularly unique and interesting. I think it’s really good to see just solid constructive debate around these points.

And it’s just so important, right? I mean, we’re in a country with such a high unemployment rate and yet so many great South Africans who are out there building things, and an informal economy that obviously is buzzing along – the unemployment rate really only tells you part of the story of what’s going on in South Africa. There’s so much else that bubbles underneath the surface all the time. And yet it’s not really a high-growth economy or it hasn’t historically been one. We don’t necessarily have as much access to finance as we would like, I think especially for smaller businesses. So, it is this very interesting, nuanced space.

I think resilience is the word that comes to mind for me when I think of South Africans, I just think of how strong they are. I think of how they always figure out a way to actually get through and win. I think we run our country a little bit like we play our rugby, where you really have to just keep grinding away until you get the victory, right? It feels a little bit like that. I mean, your experience running such a large company over the past decade has probably been something similar, I would think, including of course, a pandemic in the middle?

Francois Gouws: You know, what we try and do at PSG is think about things in international terms. I mean, there’s often a lot that you can learn from international markets, in this case international capital markets. So, when you have well developed capital markets, what you tend to see around the world, particularly in the US for example, you see high productivity, you see real wage growth, you see low unemployment, and that’s all because capital is being allocated in an optimal way, it goes to the causes and opportunity sets that justify those capital flows.

I think we in South Africa suffer from a constraint of financing. Given the wastage that’s occurred over the last 10 or so years and the degree to which it’s been funded by government debt, which is now at very, very high levels, approaching 80%, and where the IMF has indicated the numbers could be even higher, that means that finance is a constraint.

If you want to get things going from an economic growth point of view, you’re going to need funding. And that funding won’t just come from domestic institutions, it has to come from international institutions also. So, you need to make sure that you have the right policies, you need to have the right frameworks. But the good thing about South Africa is it’s one of the oldest capital markets in the world. If you go back in time, the Johannesburg Stock Exchange funded the start of the gold mining boom in South Africa. If you look at the state-owned enterprises, many of these enterprises were funded through capital market activities. Electricity, steel, you could just go on and on.

If we can develop the right policies, it’s actually – the benefit of South Africa is that we’ve got this very healthy ecosystem, we’ve got a great central bank with a lot of credibility. Notwithstanding the recent travails that we’ve had with the Treasury and the VAT question, highly credible Treasury. We’ve got a law system that works, we’ve got patent protection, you’ve got all the key ingredients to be able to raise the funds to secure investment. So there’s lots of reasons to be optimistic, but you nevertheless need to execute. And as you, the Ghost and I discussed at the start of the show, I think that’s harder than people think. And that’s why I think this is such an important debate – the practical elements to get things going and from our point of view, the capital markets being efficient and being able to raise the funds required to, to get growth going in South Africa.

The Finance Ghost: Yeah, we had a great little pre-show chat about just how it’s easy to have an idea and it’s much harder to build something…

Francois Gouws: …absolutely.

The Finance Ghost: Obviously with reference to what PSG has built, bluntly, it’s an incredible business with a wide moat. And I think what you referenced there about South Africa is just the guardrails in place that have managed to keep us going. Even though it feels like this bowling ball has been hitting them on both sides for the past decade or so, it somehow still made it, it’s still made it to the end and it’s hit some pins there, in South Africa’s ten pin bowling analogy. And you know, hopefully we can hit a lot more going forward.

A lot of it is going to come down to the policies that we set, which is I guess where this Think Big South Africa competition really plays a role. Because what you’re actually looking for is quite serious ideas from educated and experienced people. I’m going to reference the prize money here because I think it actually gives an idea of the quality of work that you’re expecting here. So in 2024, the first prize was R300,000, which is a pretty serious number. In 2025, it’s now R500,000, which is an even more serious number. And in fact, this year’s second prize is actually equal to last year’s first prize.

I guess not only are you clearly getting the outcomes that you want in terms of the competition, but you know, you’ve made the decision to increase the prize money. You’ve made the decision to say, hey, this is a lucrative use of your time, if you are an experienced and well-educated person who has a view here or just regardless, someone who actually can come in with some big ideas here to drive this conversation. I think it’s an amazing prize.

What was the thinking behind upping it in 2025? Is it just to kind of keep it going and keep attracting great ideas?

Francois Gouws: We’re capitalists, so we believe in efficient markets, sometimes we think our government underestimates confidence and aspirations and also incentives. So, in our own mind we wanted to create an incentive for serious people to tackle this particular problem. And in the context and the scope of the scale of trying to fix South Africa, I think the prize money is minuscule, but hopefully serves as an individual incentive for people to come with good ideas.

Some of these topics are difficult. There’s of course lots of international research about many of these topics – how capital markets help economic performance and deal with jobs and so on. But those aren’t really meaningful in a South African context always. So even if you invoke and use international research, you need to make sure that it applies to the uniquely South African circumstances – our very high employment rate, things like inequality, things like regional differences, a lack of skills and so on.

So there’s a variety of different things that you’re going to have to take into account when you deal with the South African circumstances. And then I think the other idea that we had is if you make these incentives significant, it also allows for groups of people to collaborate.

This doesn’t have to be a prize for an individual. It could be for a group of individuals who participate, let’s say at a university or a think tank or, or even business working with academic institutions or government institutions themselves. I mean, there’s no limitation in this competition on good ideas.

And then I think the last point perhaps as an incentive is our previous winners were masters students, we’ve had a university professor from Stellenbosch win second prize, so it’s not restricted only to academics, but it’s also open to anybody. And of course it’s prestigious, because the judges in the competition are all market professionals and recognised in their own right. I think beyond the financial incentives, I think just the incentive of recognition that you’re going to be competing in a tough competition with some very, very good participants and coming out on top or winning a prize is a tremendous incentive. So, yeah, we very eagerly await participation in this competition.

The Finance Ghost: I know that your background is also in investment banking and this reminds me of – there was just someone I worked for very early in my career and he always had this very tongue in cheek comment where he said: since money was invented, there’s really only one way to say thank you, which obviously is just quite funny in the context of this being a great prize, but as you say, there’s just the opportunity to actually engage with such experienced people. There’s the opportunity to meet other people who might put entries in. There’s the opportunity to take that research forward and actually discuss it in the right places.

It’s this really great combination I think, of there is a genuine financial incentive here and it is a serious one, but on top of that, there’s the ability to actually contribute. And sometimes we’re missing either one of those ingredients, right? It’s great that you recognise the need to say, hey, this is actually real incentivisation because people need to spend time on this to get high quality input into this competition.

I love the thinking behind it. And I also think it’s really interesting that there are a couple of special categories here. There’s one for people below the age of 25, so if you’re a youngster listening to this and you are feeling, you know, wow, this is very daunting, there’s these big shot professors and there’s all these people who’ve got lots of experience entering, get your entry in. Because the point is, there is a special category for people below the age of 25, and that’s obviously because Francois and the team are looking for youngsters to have a voice. This is the future of our country and there’s a good reason for that.

As well as those who are not in formal academic environments, there’s a category for that as well. And I guess, Francois, that’s just the desire of maybe the business voice coming through, the somewhat more “what’s happening in practice” kind of insights. I think that’s also an important one. I think you’ve done a very good job there of just making sure there’s space for everyone and actually allowing this stuff to come through.

Francois Gouws: You know, we. We believe in collaboration, we believe in participation. And I think that’s, as you say, that’s really what we’ve been trying to achieve. There’s lots of talk in South Africa about the “great debate” and sharing of ideas and so on, but often that’s restricted to politics or to macroeconomic issues.

And I think the financial community, the business community, the academic community has also got a large contribution to make in terms of finance. And ultimately, if you can’t fund the noble ideas which you have, then it won’t translate into tangible success.

In our minds, these debates are perhaps even more important than some of the political discussions that’s going on, because it makes those great ideas, it translates them into tangible things that you need to do to achieve success and certainly to fix some of the big problems that you have in South Africa.

The Finance Ghost: Yeah, I would agree with that. And I think that had we focused only on politics for the past 10 or 20 years and not actually had these guardrails in place from a policy perspective and the financial infrastructure that you mentioned, where would we be today?

So this stuff has got to carry on. It’s got to carry on in the background. It should be coming to the foreground. We should be talking less about politics and more about how this stuff is really filtering down. But we are somewhat in a clickbaity world and people do love reading about politics.

It’s great to see focus on this kind of stuff.

I also couldn’t help but notice that another change to last year is not just the higher prize money, but also that you will be a judge on the panel this year. You weren’t one last year. Was it just too much fun and you felt like you missed out last year and you wanted to get involved or what was the reason for coming onto the panel?

Francois Gouws: I think it’s pretty exciting. If you’re a market professional, as I’ve been for 40-odd years, you want to participate, you want to give some stuff back and you also want to learn. I mean, things are – you live in a dynamic world and finances are ever-developing concepts, so on a personal level, I’m delighted to be involved.

I also want to support the idea that you have fact based, impartial research. And sometimes I think when you read government legislation or policy, a lot of it is ideological. There isn’t enough by way of socioeconomic impact studies and asking some hard questions about why certain policies are followed and having the appropriate debates backed up by solid research. So this is an attempt to also not just have the debate, but also to encourage rigour in – and analytical – thinking to deal with real problems. And I think that’s important. It’s vital because otherwise how do you decide on one course of action as opposed to another?

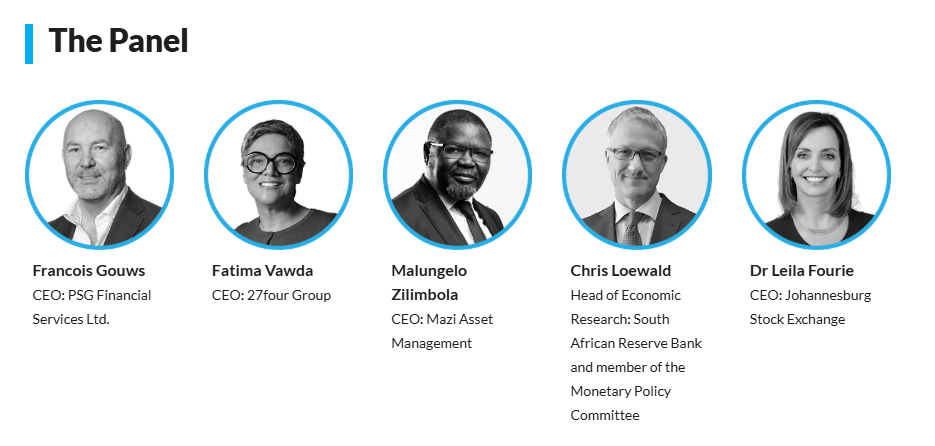

But I think the panel extends well beyond me. I mean, it also has Chris Loewald, who’s the chief economist at the central bank and MPC member. Fatima runs 27four as a chief executive, Malu, who runs Mazi, and then Leila, who’s the chief executive at the JSE. So there are highly experienced professionals, market practitioners from varied backgrounds that show an interest and a willingness to actually help.

It goes well beyond our own organisation. It shows that there’s interest in a variety of individuals with financial expertise to participate in the judging panel. And I think that elevates the importance of this work and it increases the prestige for all the various winners that eventually gets judged at the end of this competition in August.

The Finance Ghost: Yeah, totally agree. So, what have been some standouts for you from previous competitions in terms of stuff you’ve learned or papers that you thought were really just super interesting, ideas that came from, not necessarily from left field, but just what were some of your learnings from previous examples of this competition that has really made this so rewarding for you?

Francois Gouws: Well, if you go back two years, maybe two, three years, the narrative in South Africa hadn’t yet focused on economic growth and the fact that you need economic growth to deal with inequality, poverty and unemployment. It was only about two years ago that the president in his own speech acknowledged the importance of economic growth and as a driver to fix some of the most pressing issues that you have, so the fact that we ran the competition at the time, I mean it’s not just PSG, but I think there’s awareness amongst financial services and business executives that economic growth was vital. And I think that competition helped to elevate that debate.

And now, two years later, it’s pretty much conventional wisdom. Everybody now, if you talk to them, would say, yes, of course, economic growth is what you require to deal with these things. But that wasn’t the thinking at the time. You can perhaps ask why that wasn’t the thinking at the time, but it just wasn’t. So I think the mere fact that we, and many others by the way, helped to change the thinking and to start focusing on economic growth was a very important issue.

I think the other thing that came out of the research was you don’t just engineer economic growth through happenstance. It’s a highly technical area with lots of varied input. And you can’t just look at one variable, you need to look at multiple variables and you have to get them all in sync.

I think the research that came out of the last competition made that very, very clear. And I think where we are today is we perhaps realise that Operation Vulindlela, which had three elements of energy and logistics and crime, has to be extended beyond those three points if you really want to get economic growth going. Economic growth is a complicated subject. You have to deal with water, you have to deal with a variety of other topics and all of those things have to work in unison to actually engineer the economic growth.

And then some other highlights were it doesn’t all have to be at the macro level. It could also be at the micro level. It can be at the regional or sub-regional level in terms of microfinance, township economies, how they work, how they’re funded, why that helps the informal economy and perhaps creates employment which isn’t generally tracked. The fact that that’s an important area to look at I think came out of the research very, very clearly and perhaps was underestimated.

I think all these topics raise awareness that economics is a complicated and technical area and yet quite fact-based and informs, ultimately informs good decision making, which is really what we want to see is good decisions. And good decisions will kickstart economic growth and help South Africa to achieve its full potential.

The Finance Ghost: Yeah, the kasi economy as it’s called is a fascinating thing. I do have a great interest in that informal sector actually, and how much of it then comes into formal over time. It really is interesting. I think, some of those previous years’ topics, the concepts of, as you say, something like economic growth is actually very technical and it’s kind of that playground for economists and those who really understand those more macroeconomic and as you say, microeconomic points. I think what really piqued my interest this year is when I saw reference to capital markets, which of course is an area that I feel like I do understand as opposed to something like economic growth, where I have an appreciation for it, but I definitely don’t profess to be anything close to an expert in that space.

The capital markets are super interesting because that is basically connecting capital to opportunities. That’s what a capital market does at its core. And the South African capital market is world-class, literally. I wish it had more ability for people to raise money and more liquidity and we all wish those things. But the infrastructure is literally world-class. And so I think that is just a fascinating topic for it this year. It’s certainly, as I say, what grabbed my attention.

I think maybe we should talk a little bit about what the submission actually looks like because I’m sure by now those listening are, well, if they haven’t already googled while listening, they must be frothing to find out how it actually works. Let’s talk a bit about the submission itself.

It’s due by the 30th of August, so there’s still quite a bit of time. Document needs to be between 2,000 and 3,000 words in length. The topic is how capital markets enhance economic performance and facilitate job creation. So, super interesting. From what I’ve seen online, you’re looking for a narrative-driven analysis based on existing data, although original analysis is also welcome. And you’re looking for a paper that deals with things like the overall environment and what that needs to be for a capital market to thrive, but also just how capital markets can participate here.

It’s just a really interesting topic and what’s also very helpful I think is that on the website there is a good example of a submission. I’ll include a link to that in the show notes. And so I would encourage, obviously those listening to this podcast to give some proper thought to how you would want to actually make your voice heard because capital markets are fascinating. They are very interesting.

And Francois, as you said, these papers, yeah, prize money is great, but it’s actually way more interesting than that because these papers actually go somewhere. They drive thinking. And as you made the point, what is conventional wisdom today was not conventional wisdom a couple of years ago necessarily because policy changes over time and it changes in response to the feedback given by not just academics, but also business and on the ground and what’s really happening and the international investor community and what they’re looking for and how we participate in a global economy.

It is just a really great topic and I would certainly encourage people to give it a bash. Get your submissions in.

I think to bring this to a close – Francois, just any closing thoughts from your side in terms of this year’s topic? Maybe some of the stuff that you think is interesting or might be looking out for and just to encourage people to actually get that submission in?

Francois Gouws: There are so many different ways in which you can cover this topic. But in its simplest way, capital markets connect people who save and that could be directly or indirectly through you as an individual, as a pension fund participant, with the users of those funds. There’s a lot to talk about right there. And then of course, I think the key question in South Africa is because of the levels of debt, in order to fund growth, we can’t simply rely on domestic funding. We have to get international investors interested in South Africa. And sometimes I think the danger when people debate South Africa, they debate it in the context of a bubble, and yet we operate in a global marketplace where funds can go anywhere.

So I think – and we’ve had many questions on this – I think a key area will be particularly after our president when went to the US, a key question is really how do we get international funders interested in South Africa? What kind of conditions do we need to create and what will crowd them into South African investments, which is solely needed if we want to kick start economic growth and ultimately create employment?

I would just encourage people when they think about these topics, you can tackle it in so many different ways. I think some of the ideas I gave now will give you some direction, but honestly, we welcome any new ideas, any fresh ideas that haven’t been aired, so we’re very much looking forward to going through all the various submissions. But thank you very much for having me on your show.

The Finance Ghost: Yeah, it’s been a pleasure, Francois, thank you. And in my closing comments, I had a look at the weightings of how you will assess these papers. Originality and creativity gets a 30% weighting, so to those listening to this, you may not have written an academic paper in a while, you may be feeling like this sounds too much like a little masters – go and have a look at the example on the site. I really would encourage you to do that. Just Google PSG Think Big South Africa, you’ll find a landing page on the PSG website with lots of information. And then on Economic Research Southern Africa, that’s where you’ll actually find the submission form and just the final details you need on this. So just Google it. You will find it. That’s Think Big South Africa.

And get those ideas in, because I can see what’s being rewarded here is original, creative ideas with practical implementation. I think that the panel reflects the need for this to be practical. You do, at the end of the day, have the CEO of the JSE on this panel, among other leaders in this space.