Wine in Focus is an Investec Focus Radio five-part vodcast series hosted by Lerato Motshologane, a dealmaker at Investec for Business and founder of Discover Wines.

To coincide with Investec’s sponsorship of the Trophy Wine Show, we recorded this from Grande Roche, in the stunning Paarl winelands.

Lerato chats to wine makers, investors, farmers and judges on everything from how to invest in wine, to innovations changing the way we farm, and South Africa’s growing prominence on the international fine wine market.

In Episode 1 of this series, you can listen to Johan Malan from Wine Cellar, Mike Ratcliffe (co-founder of Vilafonté) and Investec’s Roy van Eck as they discuss how to invest in fine wine. They cover how you tell the difference between a premium vintage and plonk, how to age wine, a wine bond, and their hopes for SA’s wine industry.

If you enjoy this, be sure to visit this page for more information and for upcoming episodes.

Lerato Motshologane works at the intersection of finance and fine wine. As a dealmaker at Investec for Business, when she isn’t shaping funding solutions for her commercial clients, she’s promoting and trading in South Africa’s finest wines. As founder of Discover Wine, she’s passionate about educating the local consumer about the value and quality of our wines and enjoys hosting international wine lovers in our beautiful winelands.

The African Rainbow Capital Investments offer found very few takers (JSE: AIL)

Many shareholders will move into unlisted territory

You may recall that when the offer to shareholders of ARC Investments was announced, I noted that it felt like a cheeky price. The mental gymnastics that were used to determine the offer price as being fair were even more impressive.

The rather pitiful take-up of the offer tells you that the price was low. The offer was accepted by holders of just 18.64% of shares eligible to accept the offer, or fewer than 1 in 5 shares. This works out to 6.31% of total shares, giving the offerors a stake of 55.13% as they move into the unlisted environment.

This means that a large number of shareholders will hold unlisted shares, presumably holding on for a big payout down the line from assets like Tyme. If liquidity discounts were a problem while the company was listed, then you can imagine what it will be like when unlisted.

Altron is focusing firmly on profits (JSE: AEL)

There might not be much revenue growth, but just look at HEPS

Altron has released results for the year ended February. If you exclude the sale of the ATM business, revenue was up just 3%. That doesn’t sound exciting at all, yet HEPS from continuing operations was up by a whopping 73%. This was driven by an increase in gross margin of 200 basis points and a 50% increase in operating profit thanks to solid cost control.

The percentages just get silly if you look at the group including discontinued operations, with HEPS swinging from a loss of 25 cents to positive 134 cents. Interestingly, the dividend is up by 52% though, so perhaps that’s the right measure to look at.

Within the group, Netstar grew EBITDA by 17% thanks to subscriber growth of 16%. With 91% of its revenue being of an annuitised nature, Netstar is a strong business. At Altron FinTech, they enjoyed EBITDA growth of 38% thanks to the SME customer base and the associated growth in transactions. Altron Document Solutions has now been reclassified as a continuing operation and that’s not the worst thing, with EBITDA swinging from a loss of R74 million to positive R84 million.

If you start digging deeper into individual businesses within these segments, then you get the typical mix of good news and bad news. This isn’t unusual for large companies. The important thing is that group profitability has improved and so has the balance sheet, with a notable 58% increase in net cash and cash equivalents.

The outlook statement does include a word of caution about growth in FY26 given the broader operating environment. They don’t give specifics on what the impact might be. Medium-term margin targets are still in play, as is the dividend policy of paying out at least 50% of HEPS.

Barloworld’s HEPS decline: from Russia, with no love (JSE: BAW)

At least EBITDA margin moved higher excluding VT in Russia

Barloworld has released results for the six months to March. Given the underlying offer to shareholders that still hasn’t reached enough acceptances for it to go ahead, these numbers are particularly important. Shareholders that haven’t accepted the offer need to decide whether there’s enough in here to justify hanging onto the shares in the hope of a better return down the line.

Including the Russian business tells a sorry tale. Group revenue is down 5.8%, EBITDA fell by 9.1% and HEPS took a nasty 20.5% drop. The ordinary dividend is down dramatically from 210 to 120 cents per share, a drop of 43%. It’s important to look through the noise though to assess how the group is doing excluding Russia, as that’s the best indication of whether the offer price is appealing.

Revenue excluding Russia fell by 2.2% and EBITDA was up 3.0%. This means that EBITDA margin expanded from 11.9% to 12.5%. Normalised HEPS excluding Russia was flat at 356 cents per share.

The Equipment Southern African business warrants its own discussion, as EBITDA fell by 6.9% to R1.3 billion. The EBITDA profit margin was down by 10 basis points to 11.5%. They attribute this to a change in sales mix.

The most important growth asset in the group is Equipment Mongolia, which saw EBITDA improve by 14.5% to R549 million. Still, EBITDA margin of 23.0% was below the prior period margin of 24.7%.

Ingrain also deserves a mention, with EBITDA up 10.1% to R411 million and margin expanding from 11.7% to 12.9% due to cost reduction measures.

This means that although group margin improved excluding Russia, this was due mainly to mix effects rather than stronger margins in the underlying businesses. Sure, Ingrain went in the right direction, but it’s also the smallest segment. Equipment Mongolia grew strongly and runs at a much higher margin than the other segments, hence it now contributes a higher percentage of group EBITDA and the change in mix drives a higher EBITDA margin.

There are of course some other businesses in the group, but they are too small to really feature in any decisions for shareholders here.

Annualising HEPS in such a cyclical business is dangerous at best, but the FY24 numbers were a surprisingly evenly split between H1 and H2. So, if we simply double this interim HEPS of 423.2 cents, it gives us indicative forward earnings for FY25 of 846.4 cents. The offer price is R120 per share, a forward earnings multiple of 14.2x. As I’ve written a few times now, if I was a Barloworld shareholder, I would take the offer and run. Each to their own.

As a further overhang from Russia, the deadline for the voluntary self-disclosure to the US Department of Commerce’s Bureau of Industry and Security (BIS) has been extended from 2 June to 2 September. I am no expert in this space, but I suspect that the word “voluntary” is working hard here.

Blue Label Telecoms highlights the Cell C business model (JSE: BLU)

The journey to a separate listing has begun

Blue Label Telecoms has started the process of getting the market used to Cell C as a standalone entity. They are looking to restructure and separately list the company, which means they need to drum up investor support for it.

Cell C has completely repositioned itself to be a capex-light buyer of network capacity. This feels at first blush like a market position that is ripe for disintermediation, but in practice I can imagine why it wouldn’t make sense for each partner (e.g. retailers selling cellphone products) to engage with each network. Cell C does all the hard work in the middle, creating an easy solution for companies with strong distribution channels who want to get a piece of the action here.

I will note that the “smarter” and more capex-light the business model, the greater the chance of attracting competitors. Cell C has over 90% MVNO network share, which is an extraordinary market share that will be hard to defend over time from disruptors.

Still, it’s great to see Cell C doing so well and it’s especially good to see the slick branding and the overall smell of success that the business gives off, a most welcome change from the stench of failure that followed it around for so many years.

I recommend that you at least flick through the presentation here.

A juicy jump in HEPS at Dis-Chem (JSE: DCP)

Full details will be availablelater this week

It looks as though Dis-Chem had a grand old time in the year ended February 2025. HEPS is expected to be between 19% and 21% higher, which means an expected range of 136.4 cents to 138.7 cents. The trigger for a trading statement is 20%, so they are right on the cusp here and hence they needed to release this update.

The reason for the tight range is that results are due for release on 30th May (later this week), so there must be very few moving parts left. At the midpoint of that range, Dis-Chem is on a Price/Earnings multiple of just under 25x after closing 6.4% higher in response to results.

Double-digit dividend growth at Exemplar (JSE: EXP)

A focus on retail space in low-income areas is working

The name Exemplar REITail may be somewhat contrived, but shareholders couldn’t care less when they are enjoying growth like this. In the year ended February 2025, net property income was up 10.2% and the total distribution per share grew by 10.4%. To add to the party, the net asset value per share increased by 13.2%. To my mind, this makes Exemplar the pick of the recent results in the sector.

It’s just an absolute shame that there is close to zero liquidity in this stock. It almost never trades, so the most you can really do is treat it as evidence of how strong the low-income retail model is. This plays firmly into the trend of formalisation of consumer spending, with township consumers choosing to spend more on their routes home or at malls near where they live. This addresses a very real consumer need, as transport is such an onerous cost for these South Africans that it often shuts them out from being able to reach other malls.

At R4.4 billion market cap, it’s a significant fund. The lack of liquidity is a result of a tightly held share register rather than anything else. Will someone ever swoop in to pry it from the fingers of the McCormick family and their business associates? The offer price would probably need to be so high to convince them to sell that any such deal is unlikely.

Hyprop may make a play for MAS (JSE: HYP | JSE: MSP)

This comes after the particularly weak bid by MAS’ joint venture partner

Regular readers would’ve seen a rather odd offer that came through to MAS shareholders from an entity that is a joint venture between MAS and Prime Kapital Developments. When I wrote about it in Ghost Bites earlier this month, my overall view was that it’s a “why bother?” offer at a discount to the current traded price, which makes it a rather nonsensical attempt. To make that offer worse, it then includes the proposed inward listing of an instrument that will almost certainly have even lower liquidity than existing MAS shares.

Hyprop clearly felt the same way when they saw it, with the company considering an opportunistic share-for-share offer that would allow MAS shareholders to swap their exposure for more liquid Hyprop shares. The pricing would be with reference to the closing price of MAS shares before this announcement came out, rather than the cheeky bid put on the table by the Prime Kapital joint venture.

The Hyprop bid isn’t a firm offer at this stage. It also comes with a strange precursor where Hyprop will issue shares for cash as part of its general authority to do so, noting that this is in preparation for the voluntary bid. Java Capital is running the book on an invitation-only basis, so this isn’t an offer to the public to subscribe for shares.

But what happens if the bid doesn’t go ahead, or if acceptances exceed the cash alternative that Hyprop is willing to put on the table? In such a case, it seems as though investors would’ve put cash into Hyprop for a deal that may not even happen.

There’s nothing boring about the deal activity around MAS, that’s for sure.

Can Pick n Pay carry some momentum into the new financial year? (JSE: PIK)

Goodness knows they need it

Pick n Pay raised billions for its recovery efforts through a combination of a R4 billion rights offer and the listing of Boxer on the JSE. They are sitting on net cash of R4.2 billion. In the 53 weeks to 2 March 2025, they suffered an attributable loss after tax of R736 million, so they need that cash balance if they are to have any hope of achieving a turnaround.

The good news is that like-for-like sales were up 3.3% on a 52-week basis for Pick n Pay company-owned supermarkets. That’s a very specific data point, but it’s an important one. That’s a lot better than a decline of 1.2% in the comparable period. But for Pick n Pay as a whole (i.e. including franchise and the impact of store closures), sales were down 0.3%. That’s still way off the 10.4% growth at Boxer.

Speaking of a long way off, Pick n Pay believes that its core business will only break even in FY28, having previously guided for FY27. This is after the deduction of interest expenses for leases, a result of how silly the accounting standards are that put lease expenses down as a financing cost. Just imagine owning this business yourself – would you ever tell someone about your profitability excluding the cost of leases? Of course not, as they are integral to any retailer’s business.

This is the difference between trading profit (which turned positive in H2 of the year) and profit that shareholders actually care about. Trading profit excludes lease costs and is therefore a useless metric. This isn’t Pick n Pay’s fault – it’s the fault of those who set the new leases standard under IFRS.

Sticking with the theme of a long way off, Sean Summers has agreed to extend his term to FY28, in line with the path to break-even. It’s not every day that a CEO can take longer to execute a turnaround and then earn a salary for a longer period as well, but such is life.

At least the first 8 weeks of the new financial year are showing some signs of life, with like-for-like sales growth at Pick n Pay of 3.8%. Company-owned supermarkets are up 4% and franchises are up 2.1%.

Special mention must go to Pick n Pay Clothing, which put in a strong recovery in H2 (like-for-like sales growth of 10.7%) after a poor start to the year due to port delays. This remains a bright spot in the business and it shows that Pick n Pay is capable of some innovation at least. They would do well to take the DNA of that business and inject it across more of the group.

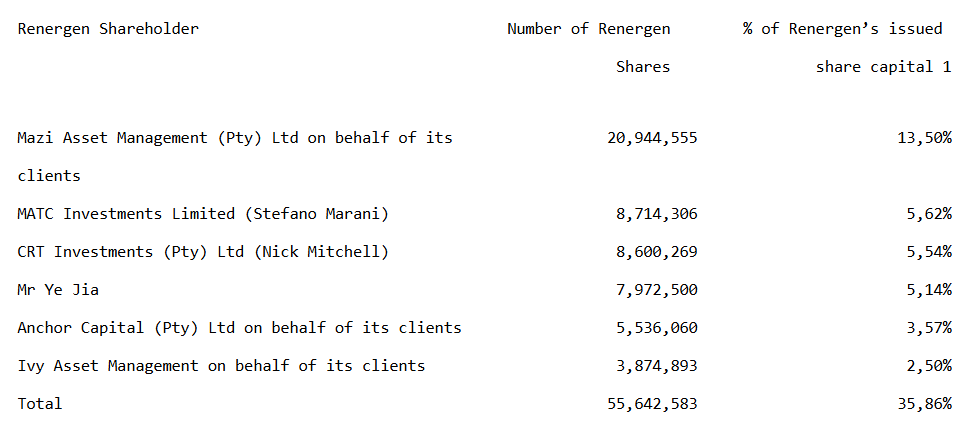

A regulatory win for Renergen (JSE: REN)

Uncertainty around the helium rights has been removed

Here’s some good news for Renergen shareholders – and those who plan to invest in ASP Isotopes when it comes to the JSE, based on the current likelihood of a deal happening there.

The Minister of Mineral and Petroleum Resources has dismissed the appeal launched by Springbok Solar, which means the debate around Renergen’s right to extract and commercialise helium has come to an end. This takes away a material uncertainty around the company. It also feels like it is firmly in the best interests of the country and the sector in general, as investors would be properly spooked if mining rights could evaporate based on technicalities.

Renergen is now seeking relief against further construction related activities by Springbok Solar, with the court expected to hear this in the early part of June 2025. The parties will at some point get around a table and find a position that works for all involved.

Nibbles:

Director dealings:

As part of broader hedging transactions over Discovery (JSE: DSY) shares, Adrian Gore sold R29 million worth of shares. This is because the share price at the maturity of this particular collar was higher than the strike price on the call options, so the call options were exercised and Gore was forced to sell. In a new transaction, he’s bought 525,000 put options at a strike of R209.21 and sold the same number of call options at a strike of R445.61 per share. The options are exercisable in May 2031. The current price is R213, so you can see how this protects against downside while giving away upside above a certain level.

The CFO of Impala Platinum (JSE: IMP) sold shares worth R8.2 million and a prescribed officer sold shares worth R2.84 million.

An independent non-executive director of South32 (JSE: S32) bought shares worth $121k (roughly R2.15 million).

Family members of the CEO of Spear REIT (JSE: SEA) bought shares worth around R65k.

Thungela (JSE: TGA) announced that Benjamin Kodisang, currently an independent non-executive director, will be appointed as lead independent director. That’s an important role on the board.

Caxton and CTP Publishers and Printers (JSE: CAT) shareholders almost unanimously approved the resolutions for the odd lot offer. It will therefore proceed at R14.20 per share and will be structured as a dividend. The current share price is R12.00 per share. Before you wonder about that gap, the odd lot offer net of tax is R11.36 per share.

African Bank’s ordinary shares aren’t listed at the moment, but they have other instruments that are. Given the overall relevance of the bank to the economy, I’ll give it a mention down here that the six months to March saw growth in net profit after tax of 15%. There was particularly strong growth in non-interest income. The traditional lending activities were given a boost by an improvement in the credit loss ratio.

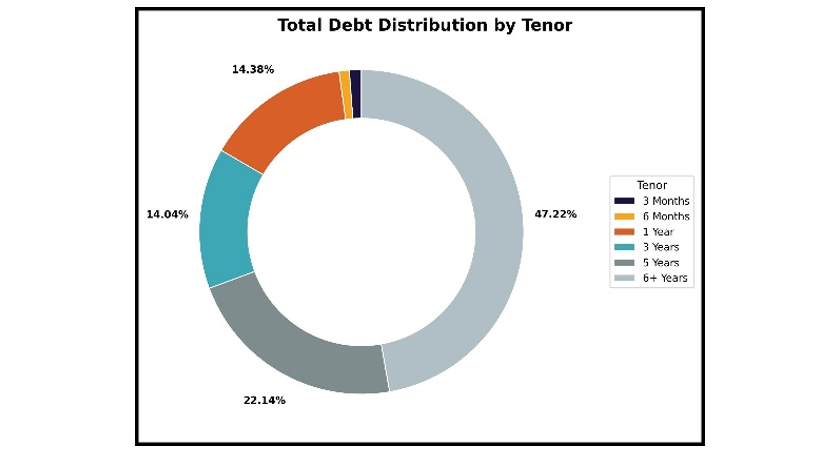

South Africa’s listed debt market presents an intriguing blend of opportunities and challenges. Characterised by its unique structure, participant dynamics, and liquidity constraints, this is a space worth examining for institutional and retail investors alike. Understanding the nuances of this market provides insight into how investment strategies are shaped and how market participants operate within the boundaries of the South African economy. This overview is brought to you by Intengo Market.

South African Debt Market Structure and Dynamics

Our local debt market is considered a “buy-to-hold” market, with minimal trading activity in the secondary market. Institutional investors, such as life insurers and asset managers, dominate the primary market, accounting for a significant portion of activity within this space, and these institutions generally prefer to hold assets to their maturity.

Participants are drawn to the listed (or public) debt market because of its potential for steady yields and minimal volatility, aligning well with the conservative fixed income investment mandates of insurers and large asset managers.

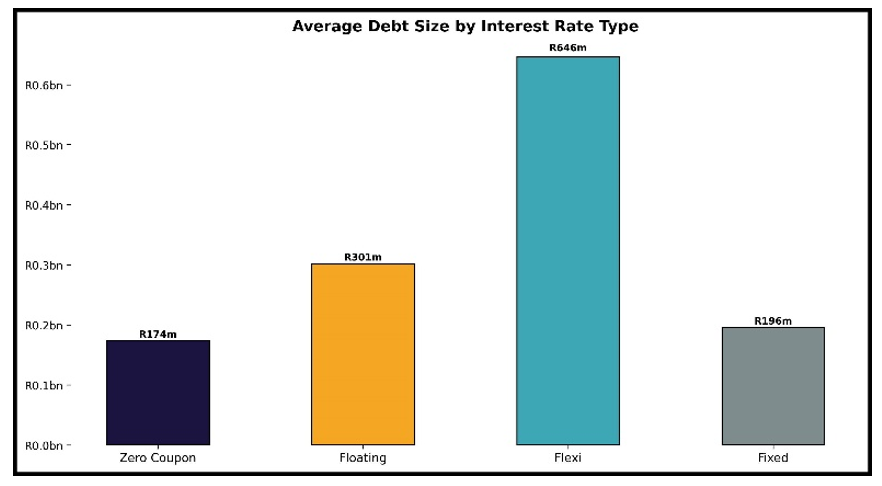

A large majority of the non-government issued fixed income instruments in our local market are also issued as floating rate notes. These generally reset their reference interest rate every 90 days and this mitigates a significant amount of interest rate risk for the issuer and investor.

Key Market Participants

The primary issuers in local listed debt market include the government, state-owned enterprises (SOEs), financial institutions and large corporates. Each year, only around 25 entities (excluding the Government) come to market to issue debt instruments, providing significant opportunities for investors. Of these, 19 issuers have been relatively consistent participants, issuing debt annually, while the remainder alternate every other year or two. This rotation provides a measure of diversity in the market, although the dominant presence of consistent issuers underscores the predictability of the debt issuance landscape.

The opportunity for private credit is, however, is much broader than that in the listed space in terms of number of issuers, as there are almost 300 listed companies in South Africa and most of them require debt funding in some shape or form (we will dive deeper into the private credit market in a future article, as it deserves much more focused attention).

Around 100 institutional investors are regularly active in this market. In addition to institutional investors, it includes five major local banks and several smaller banks. Among the five, three are relatively active in the secondary credit market, offering pricing to the market for most of the high-quality corporate credit issuances. These participants are often referred to as the “sell-side” as they are generally distributing (i.e. selling) products or instruments to the broader market. Their role in providing pricing mechanisms contributes to some level of market efficiency; however, even this active pricing is insufficient to foster a liquid secondary market in bank and corporate credit. Then there are also debt brokers, who act much like real estate agents in the property market – using their networks and skills to bring buyers and sellers together at a price that leads to a deal.

The ”buy-side” would traditionally encompass the institutional asset managers and life insurers. They are generally buying debt directly from the issuers (in the primary market) or from the sell-side (in the secondary market) into their portfolios.

Recent developments (supported by regulatory changes) have seen hedge funds entering the local fixed-income space. These funds are beginning to carve out niches through innovative strategies and risk management approaches. This emerging presence hints at potential shifts in market dynamics, although the impact of hedge funds remains relatively nascent and limited in scope at this early stage.

Illiquidity as a Defining Feature

One of the most notable characteristics of South Africa’s listed debt market is its illiquidity. The lack of a robust secondary market means that once debt instruments are issued and purchased, they rarely trade hands. This illiquidity is rooted in several structural factors, including the dominance of buy-to-hold strategies among institutional investors and the limited number of banks prepared to take on the other side of any potential trade.

For example, if the entire buy-side was looking to sell the same instrument, you could theoretically have 100 sellers. The sell-side, on the other hand, is at most five large banks and a few debt brokers. As a result, while the local banks play an essential role in pricing corporate debt, their efforts do not translate into active trading volumes.

The scarcity of buyers and sellers of the same instrument at the same time in the secondary market perpetuates the cycle of illiquidity, limiting the market’s attractiveness for those investors seeking flexibility and exit opportunities.

Opportunities and Constraints

For investors who align with the buy-to-hold approach, the South African listed debt market offers distinct advantages. These include relatively predictable income streams and relatively stable portfolio performance. However, the constraints posed by illiquidity cannot be overlooked, as they restrict the ability to rapidly reallocate assets or respond to evolving market conditions. Ignoring market crises, like the sell-off during COVID, this can be most observed during times of negative issuer news when asset pricing can fall substantially in very short spaces of time – far beyond what might be expected in a more liquid market.

Institutional investors often navigate these constraints by adopting rigorous due diligence frameworks and focusing on diversified credit portfolios. The emphasis is placed on selecting high-quality corporate credit names that deliver consistent returns while mitigating credit risk.

Another important factor in investor behaviour is that the yield on longer term South African government bonds (“SAGBs”), more often than not, makes it relatively unattractive for any conservative asset manager to purchase anything else. Some investors might take the view that a 10-year SAGB offers significantly better liquidity than even a 1-year high quality corporate bond. The return on the SAGB thus becomes far more attractive and many institutions find themselves reluctant to diversify away from this risk-return-liquidity combination.

Market Statistics

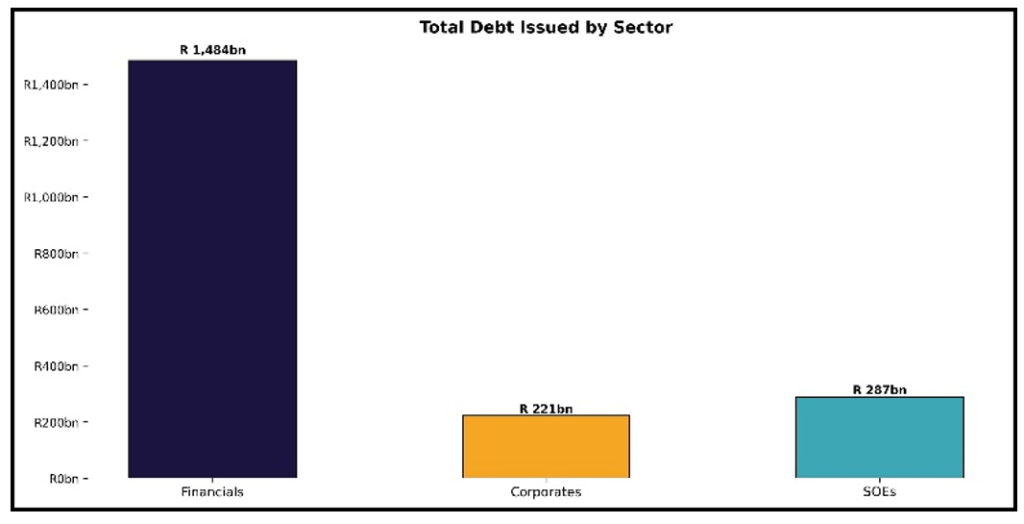

The South African listed debt market is a significant component of the country’s financial ecosystem, supported by a diverse range of participants and instrument types. The market, as at time of writing, has around 7,000 instruments totaling R6.7 trillion which settle through public market infrastructure. Not all of these are listed instruments, but these still constitute the public domain (in contrast to private credit instruments like loans). Around R1.2 trillion of this is bank and financial institution debt and only around R220bn is corporate debt. As a result of the large proportion being SA government debt, we exclude them from the below graphics as they tend to distort the scale of the graphs:

Note: all charts are based on data from Intengo Market’s platform

Emerging Trends and Future Outlook

Despite the prevailing illiquidity, the South African debt market shows signs of gradual evolution. The entry of hedge funds into fixed-income strategies introduces a layer of innovation and potential liquidity enhancement. While hedge funds are currently a minor presence, their growth could pave the way for more active trading and secondary market participation.

Further progress may depend on structural reforms, such as efforts to digitise interactions and find ways to incentivise secondary market activity. Initiatives to enhance transparency, streamline pricing mechanisms, and facilitate the introduction of new participants (foreign investors, retailers, or the newer banks, for example) could play a pivotal role in addressing liquidity and other systemic market challenges.

Understanding the intricacies of this market remains essential for informed investment decision-making and strategic portfolio management. Intengo Intuition offers its institutional users powerful analytical tools to better understand the market and the relative value of available instruments. In addition, the Intengo Platform is looking to address some of the structural reforms required to remove friction costs and democratise the playing field.

To find out more about how Intengo is addressing these issues, please visit www.intengomarket.com or connect with Ian Norden on LinkedIn. You can also contact Intengo Market here.

Get more insights by listening to Episode 60 of Ghost Stories, in which Ian Norden went into more details on the structure of the debt market and the role played by Intengo:

Accelerate Property Fund is still fighting the good fight with its balance sheet (JSE: APF)

Turnarounds don’t happen in a straight line

If you’ve been following the Accelerate Property Fund story, you’ll know that they have all to play for when it comes to the turnaround of Fourways Mall. They are making progress in that regard, having brought in external experts to breathe some life into the mall.

The group’s fortunes were also boosted by the recent agreement to sell the Portside asset in Cape Town at only a modest discount to its valuation.

Unfortunately, the recovery journey is neither smooth nor linear. The group’s balance sheet is still a significant risk. Although GCR Ratings improved the outlook on the Secured Notes from Negative to Evolving, the overall issuer ratings have been downgraded to SD due to historic non-payment of interest under SPV facilities. Accelerate had notified the funder in this regard and is working with its bankers to emerge with a sustainable balance sheet.

In the meantime of course, the ratings agencies must do their jobs and make notes of these things. Speaking of doing their jobs, Accelerate’s management managed to get the funding partners to extend the term loan facilities out to March 2027, so they’ve bought themselves time to get this sorted.

Accelerate remains a speculative play, which means that chunky risk/reward numbers are a feature of this story.

Primary Health Properties has done enough to get Assura’s attention (JSE: AHR | JSE: PHP)

The board has decided to give the revised proposal a chance

The independent board at Assura is being kept nice and busy, as is the case when a bidding war kicks off. There’s always the chance of a competing bid coming through for a listed company, as each step of the way is publicly announced and thus anyone can decide to swoop in with a more compelling offer.

Just when it looked as though the private equity consortium of KKR and Stonepeak had it in the bag, Primary Health Properties came in with an improved proposal. Their initial proposal was oddly weak and had been thrown back at them by the Assura board. Version 2.0 is a lot better. Although I’m not convinced that it’s high enough, as it offers only a modest premium to the private equity deal and required shareholders in Assura to be willing to accept part of the price in shares, it’s at least high enough to have gotten the Assura board to take it seriously.

Assura has commenced a due diligence process with Primary Health Properties to figure out whether to recommend this offer to shareholders. In order to give this a fair chance, they have adjourned the upcoming meetings that were scheduled to deal with the cash offer from KKR and Stonepeak.

Sekunjalo plans to take AYO Technology private (JSE: AYO)

I somehow doubt that many tears will be shed when this one goes

AYO Technology reckons that the decline in its share price over the past few years (and the mounting losses) are due to negative media coverage. The company is dealing with tons of litigation, including against the media as well as South African banks. It’s just a messy thing that is very difficult for anyone to build a credible bull case around, which is why is makes zero sense for them to be listed.

Sekunjalo Investment Holdings (which already holds 45.92% in the company before you even consider concert parties) will therefore look to take AYO Technology private at 52 cents per share.

The deal structure is an all-cash deal that also gives shareholders the opportunity to remain invested if they so desire, provided that they are comfortable being in an unlisted environment as AYO will delist as part of the deal. The price is a 30% premium to where the share price was trading before this announcement, so that’s a pretty reasonable offer price under the current circumstances.

It will be interesting to see what the fair and reasonable opinion says when the circular is released.

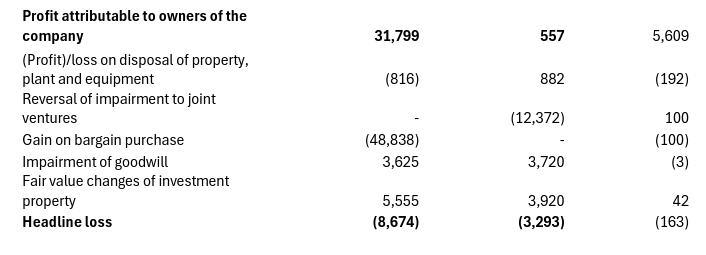

There’s progress at Finbond, but HEPS is what matters (JSE: FGL)

In fact, this is a perfect example of the value of HEPS

I write about HEPS all the time in Ghost Mail. It stands for Headline Earnings Per Share, which is the South African industry standard in assessing the profits attributable to shareholders. There are specific rules that govern what gets adjusted to get from earnings to headline earnings, with the idea being to catch as many once-offs and non-recurring items as possible.

Finbond has released results for the year ended February 2025 and on paper they look great, with turnover up 7.9% and profit attributable to shareholders jumping from R0.6 million to R31.8 million. The fact that the highlights section in the SENS announcement is devoid of any mention of HEPS is the first clue that you need to go digging.

Sure enough, there’s a headline loss of R8.7 million for the period vs. a headline loss of R3.3 million in the comparable period. In other words, things actually got worse despite the results telling a very different story.

The big jump in profits is because of a gain on bargain purchase, which means they bought assets for a price below their identifiable fair value. Once you strip out that gain (R48.8 million) and the other fair value moves, you get to the negative view of headline earnings:

Once you dig deeper, you find that net interest income (the key metric for profitability as Finbond is a lending institution) fell by 5%. Some of this is because of deliberate action taken in the North American business to be stricter on new loans and to close underperforming branches. The book churns very quickly, with an average loan term of 3.5 months in South Africa and 1.95 months in North America.

A lot happens below the net interest income line, like a 6% increase in fee income and a 9% increase in other operating income. Operating expenses were contained at just a 5% increase.

Finbond isn’t a straightforward business to understand. They have certainly made a ton of progress since the worst of COVID, evidenced by an 83% increase in the share price over 12 months. Liquidity remains thin though and the market cap is only R387 million, so this is a speculative play. It would certainly help if they were reporting positive headline earnings instead!

ISA Holdings impacted by DataProof (JSE: ISA)

The frustration comes through in the SENS announcement

ISA Holdings is a technology company with a market cap of just R315 million. They have the liquidity in their stock to match unfortunately, with thin trade on an average day.

The year ended February 2025 is an unfortunate story, as the core business did well and an investment in an associate did not. Revenue was up 17% and gross margins were only slightly down. Combined with operating expenses growth of 10% (which is well below revenue growth), you would think that the net profit story is great.

Alas, equity-accounted investment Dataproof saw the share of profits drop by 51% to R6.1 million. These aren’t exactly huge numbers, but they matter for a small cap. The drop at Dataproof was due to a large cybersecurity deal in the base period, as well as poor performance in the record management division at the company.

With all said and done, HEPS fell by 12%. If you exclude Dataproof, earnings would’ve been up 17%. Sadly, you can’t just ignore one part of the business, no matter how well the other part is doing.

The turnaround continues at Nampak (JSE: NPK)

Double-digit revenue growth from continuing operations is impressive

Nampak has released results for the six months to March 2025. The top of the income statement boasts an 11% increase in revenue from continuing operations, so that sets the scene for a strong set of numbers.

The highlights were Diversified South Africa and Beverage Angola, with Beverage South Africa performing reasonably but not as well as the others. Beverage South Africa is unfortunately the largest contributor, with EBITDA of R512 million and an increase of 6%. Next up is Diversified South Africa, with EBITDA of R233 million and an increase of 53%. Beverage Anglo contributed EBITDA of R146 million, up 36%.

The operating cash flow situation is interesting. Before taking into account working capital changes, it increased by 38%. After taking those changes into account, it fell by 42%. Although some of this is due to the timing of a COVID insurance claim, most of it relates to disposal activities and how working capital is impacted when a business is about to be sold. There’s also an element of growth capital, as you can’t grow revenue at a high rate without putting working capital into a business. Still, this is a key focus area for them.

The good news on the balance sheet can be found in the net debt disclosure, where net debt is down 33% (excluding lease liabilities). Net finance costs thus fell 38%, giving a strong boost to profitability.

There’s been a big swing on the tax line though, as Nampak has moved from a tax credit to paying taxes at the normal effective tax rate. This is one of the reasons why HEPS from continuing operations only increased by 5% in this period. Notably, HEPS from total operations (i.e. including discontinued operations) more than doubled!

Although there’s some messiness in these numbers thanks to elements like discontinued operations and certain adjustments in both the prior and current periods that impacted HEPS, the direction of travel for Nampak does appear to be up. There’s still no dividend though, indicating that there’s a long way to go.

Powerfleet is performing in line with guidance (JSE: PWR)

They’ve also given guidance for FY26

Powerfleet is participating in an investor conference in the coming week, so they’ve updated the market on FY25 performance vs. guidance and what their expectations are for FY26. This is obviously so that they can give more details than would otherwise be possible at the conference.

For FY25, revenue was up 25% and adjusted EBITDA increased by 65%. Net adjusted debt is expected to be $230 million. This performance was in line with previous guidance for revenue and slightly better than guidance for adjusted EBITDA and net adjusted debt.

The FY26 guidance is for revenue growth of 20% to 25%, along with adjusted EBITDA growth of 45% to 55%. This is firmly a growth company. The share price certainly hasn’t been enjoying the same growth, down 7% over 12 months.

Quantum Foods: a huge jump in the right direction (JSE: QFH)

Welcome to the best example of operating leverage

Quantum Foods released results for the six months to March and they paint a picture that is typical in the poultry game: when revenue goes the right way, growth in profits can be immense. In this case, a 20% increase in revenue was good for a 244% jump in HEPS!

The year-on-year story was one of no load shedding (vs. plenty in the base period) and also no avian flu outbreaks (once again vs. a rough base). It also helped that soya meal prices came down enough to largely offset the impact of higher yellow maize prices. Poultry groups can be quite flexible in how they structure their feed costs.

Quantum Foods has a strong eggs business and although egg prices fell by 14.1%, there was a 78% increase in supply that strongly offset this impact. They even resumed operations at the Pinetown egg packing station thanks to higher availability of eggs. On the farming side, the layer flock was rebuilt in this period, leading to better margins. The broiler farming business also saw an increase in production. And finally, the animal feeds business saw a 15.1% increase in volumes that managed to offset the impact of higher raw materials costs.

In the rest of Africa, Zambia had a difficult period due to drought conditions. Uganda was strong though, with that economy punching above its weight as usual. As for Mozambique, looting in December 2024 significantly impacted the business.

With the first six months of the year behind them, a strong second half will depend on whether avian flu stays away. There are obviously many other factors, like feed costs, but nothing comes close to the risk of avian flu. And in good news for Eggs Benedict enthusiasts like me, egg prices are expected to keep dropping!

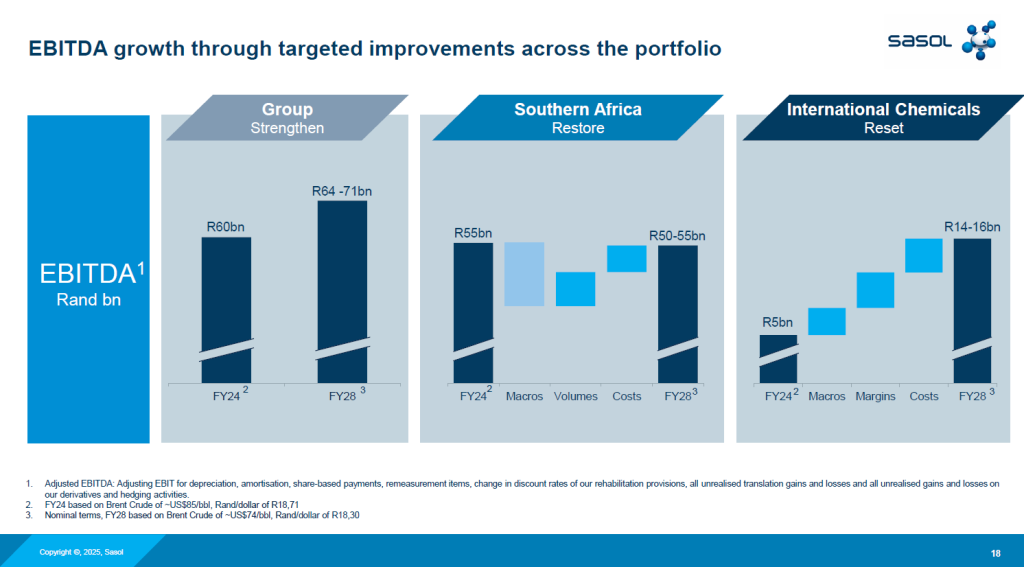

A boost for Sasol (JSE: SOL)

And they need all the help that they can get

Sasol’s capital markets day made it pretty clear that there’s going to be nothing easy about the next few years at the company. Although the market seemed to appreciate what it saw from the management team, what I see is a story that is strongly dependent on the chemicals business tripling its EBITDA and the oil price not falling over.

Any bit of extra help they can get will be most welcome by shareholders. In June 2024, the High Court ruled that Transnet owes Sasol Oil R3.9 billion plus interest. Transnet sought leave to appeal and put in a claim of R855 million against Sasol Oil for a different matter. The parties have agreed to settle, with Transnet paying Sasol R4.3 billion in full and final settlement (this shows how significant the interest burden may have become).

That’s good news for Sasol. As for Transnet, this is hopefully a reminder of how critical it is that they sort the place out.

Nibbles:

Director dealings:

The company secretary of a major subsidiary of MTN (JSE: MTN) sold shares worth R1.6 million.

Super Group (JSE: SPG) has declared a special dividend to shareholders of R16.30 per share, which is more than half of the current share price of R30.00 per share. This is from the proceeds of the disposal of SG Fleet in Australia. Super Group has hard work to do in its remaining businesses, as they are dealing with the disruption to the auto industry from the Chinese manufacturers.

Vodacom (JSE: VOD) and Remgro (JSE: REM) have extended the long stop date for the Maziv fibre deal to 13 June 2025. They keep doing these small extensions to give both parties flexibility in case something else comes along. In the background, the hearing dates at the Competition Appeal Court have been set for 22 to 24 July 2025.

If you are a shareholder in MTN Zakhele Futhi (JSE: MTNZF), then you’ll be interested in the update that indicates the latest debt levels in the structure. This comes after the extension of the structure to November 2027, as well as the recent payment of a dividend by MTN. I remain surprised by the relative lack of action in this share price relative to the recent rally in MTN’s shares.

Public backlash may be loud, but it appears as though capitalism has noise-cancelling headphones.

A few years ago, I watched a documentary film that left an indelible impression on me. Titled Blackfish, the film focuses on the story of Tillikum, the captive orca whale responsible for the deaths of three people (two of which were trainers) at SeaWorld Orlando. At the time (somewhere in 2013), it felt like a cultural reckoning. Public backlash was swift: celebrities tweeted, public opinion nosedived, and SeaWorld’s stock price did a painful bellyflop. Surely, I thought, this would mean that the days of synchronised hoop jumps were numbered. SeaWorld would have to cut their losses on the whales and pivot into a less risky mode of entertainment if they wanted to stay in business, right?

Imagine my surprise when I saw a headline last week: SeaWorld Orlando has been ordered to pay a fine of $16,550 by OSHA (Occupational Safety and Health Administration) after a trainer was injured by an orca in September 2024. That’s 11 years after the release of Blackfish. Tilikum himself may have died in 2016, but the show is apparently still going on.

To me, this begs a difficult question: what exactly is the half-life of public outrage these days? Is the “court of public opinion” just a sternly-worded press release with no follow-through? If a company can take the reputational hit, pay a fine and get right back to business as usual, did it ever really matter that people got upset?

A word from the bird

If you want a more recent example of public outrage directed at a business, you don’t have to look much further than the debacle that Duolingo is creating.

The language-learning app with the cheeky green owl mascot has gotten itself on the wrong side of the public after sharing that it was going to replace contractors with AI and become an “AI-first” company. It’s not hard to see why users don’t love this idea. For years, Duolingo’s lessons were crafted by real people: linguists, translators, and educators, all of whom helped to bring cultural nuance and personality to the content. In arecent press release, the company’s co-founder and CEO Luis von Ahn wrote: “Developing our first 100 courses took about 12 years, and now, in about a year, we’re able to create and launch nearly 150 new courses. This is a great example of how generative AI can directly benefit our learners. This launch reflects the incredible impact of our AI and automation investments, which have allowed us to scale at unprecedented speed and quality.”

Scale may be accelerating, but goodwill is definitely lagging behind. Users have taken to social media to voice their frustration, with many claiming to have deleted the app and urging others to do the same. The backlash reached such a pitch that Duolingo quietly wiped its TikTok and Instagram accounts, despite their combined 10 million+ followers. Both platforms had become less about language memes and more about AI-driven outrage.

Scroll through the comment sections of any recent Duolingo post, and you’ll find that the conversation has veered sharply off-script. A light-hearted video hopping on the “Mama, may I have a cookie” trend was quickly derailed by replies like: “Mama, may I have real people running the company” and “How about NO AI, keep your employees”. Another video, featuring How to Train Your Dragon’s Hiccup, got the brutal comeback: “Was firing all your employees and replacing them with AI also a hiccup?”.

But not all the comments were tongue-in-cheek. Some were pointedly serious. “Using AI is disgusting,” wrote one user. “Language learning should be pioneered by PEOPLE. By making this decision, Duolingo is actively harming the environment, their customers, and employees when it hurts the most”. Another chimed in with: “What kind of audience do you think you’ve built that it’s okay to go ‘AI first’? We don’t want AI, we want real people doing good work. Goodbye, Duo. If this is the way you’re going, you won’t be missed”.

Then there were the heartbreakers: “Deleted Duolingo last week. A 650+ day streak never felt so meaningless once I saw the news”. It’s one thing to lose a customer. It’s another to make them feel like their dedication was pointless.

None of this backlash seems to be hurting where it counts though. Duolingo’s latest earnings report shows 130 million monthly active users, up 33% from last year. Paid subscribers jumped 40%. Revenue is up. Profit is up. Recent conference presentations make no mention of waves of cancellations. And the stock nearly tripled in the past year. The owl may have been roasted in the comments, but on Wall Street, it’s soaring.

Apparently, you can fire your staff, upset your users, mute your social channels and still make a decent profit.

SeaWorld: still fishy

It’s no surprise that SeaWorld has plenty of feelings about Blackfish, and none of them are positive. In the wake of the film’s release, SeaWorld Entertainment’s second-quarter net income plummeted 84%, from $37.4 million in 2014 to just $5.8 million in 2015. Revenue slid by 3%, and attendance dropped by 100,000 visitors, a 2% decline compared to the previous year.

SeaWorld initially tried to brush off the hit, blaming the dip on an uncooperative Easter calendar, bad weather in Texas, and a vague category it called “brand challenges” in California. Notably absent in its reporting was any mention of Tilikum (who seemed quite determined to live up to the “killer whale” moniker) or the film that had by then become a cultural flashpoint.

Still, the company spent $15 million on an ad campaign to do some narrative damage control, spotlighting their marine research and conservation efforts while quietly sidestepping the more uncomfortable parts of the story. None of this fooled stockholders though, and by 2020, SeaWorld settleda $65 million lawsuit brought by investors who alleged they’d been misled about the documentary’s real impact on attendance. That legal chapter closed, but the public scrutiny didn’t.

Under pressure, SeaWorld announced it would end its orca breeding program in 2016, declaring that the current generation of whales would be the last under its care. A symbolic shift, though not an immediate one, since Takara, one of the orcas, was pregnant when the announcement was made.

SeaWorld’s theatrical orca shows officially ended in San Diego in 2017, and in Orlando and San Antonio by 2019. If you’re confused by those dates, you’re not alone – I was also wondering how a trainer could have been injured by an orca at a show in 2024 if the shows supposedly ended five years prior. Turns out it’s a matter of semantics: the “theatrics” may be gone, but the orcas are still performing in what SeaWorld now calls “educational presentations”. Fewer flips, perhaps. Same tanks, and same paying audience though.

As for the whales themselves, SeaWorld says they can’t be released, and that’s likely true. Many were born in captivity, and the ones that weren’t have long since lost any realistic chance at survival in the wild. Still, with lifespans reaching up to 30 years, we’re likely to see these so-called educational encounters continue for quite some time.

Outrage is noble, but tiring

In the end, Blackfish didn’t sink SeaWorld, in the same way that Duolingo’s AI-pivot (probably) won’t kill the owl. Both were just forced to rebrand. In the case of SeaWorld, the company adapted, the outrage faded, and the system absorbed the shock. That’s the rhythm of modern scandal: loud outcry, a dip in profits, a flurry of statements and settlements, and then… business as usual. It’s not that people stopped caring – it’s that caring competes with everything else demanding our attention.

As for markets, they care even less. They don’t hold grudges. They reward resilience, reinvention, and just enough change to keep the wheels turning. If there’s a lesson here, it’s that public accountability has a short shelf life, but corporate survival tactics are built to last.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

And no, this has nothing to do with sharks in a good mood

The banking industry uses the term “jaws” quite frequently. It’s a measure of the difference between growth in income and the increase in expenses. If income is growing ahead of expenses, you have positive jaws and margins are increasing. If expenses are growing faster than income, you have negative jaws and margins are shrinking. The ominous nature of the term becomes very real in a negative jaws scenario.

Thankfully, there is no such issue at Investec. In the year ended March 2025, they grew revenue by 5% vs. an increase in operating costs of 2.8%. This drove growth of 7.8% in pre-provision adjusted operating profit, taking it above the £1 billion milestone for the first time in the group’s history. The contribution to income growth was from a broad range of sources in the group, which is encouraging.

The credit loss ratio increased from 28 basis points to 38 basis points. Although that’s well within the through-the-cycle range of 25 to 45 basis points, it did take the shine off the growth in pre-provision profit. Translating the numbers into rand also impacts growth, which isn’t something that South Africans are able to say very often!

Adjusted operating profit was up just 2.8% in ZAR. HEPS was down 1.6% in ZAR. The dividend per share tells a more pleasant story, up 5.8% (that’s in GBP as they declare it in pence) vs. a HEPS decline of 0.4% (also in GBP), so the payout ratio has moved higher.

Return on equity dipped by 70 basis points to 13.9%, with a gain recognised on the combination of Investec’s UK wealth business with Rathbones contributing to a higher equity base (the denominator).

Another metric worth noting is tangible net asset value per share, which grew by 6% in GBP or 5.1% in ZAR. Over time, this is a key driver of the share price.

Here’s a fun fact to finish off: Investec is targeting mid-sized corporates, with the goal being to take the Investec private client experience (which is objectively excellent) to these companies. They plan to triple the current client base and achieve market share of 8% by 2030. Companies like Investec grow by finding specific verticals where they can win share.

Amazingly, despite plenty of volatility over the past year, the share price is now perfectly flat over 12 months! And I mean perfectly, to the cent.

Double-digit growth in Life Healthcare’s dividend (JSE: LHC)

Operating leverageis in their favour at the moment

Hospital groups are well known for earning returns that are below their cost of capital. It’s very much a game of inches, as a modest improvement in the revenue growth rate can tip the scales in the direction of positive operating leverage, which means that margins improve and investors are healed along with the patients. And vice versa, of course.

For the six months to March 2025, Life Healthcare grew revenue from continuing operations by 8.1%. This was achieved through a combination of pricing increases and a 2.0% increase in paid patient days. The interim cash dividend increased by 10.5%, so we have a rare example of double-digit growth. Having said that, normalised earnings per share was up by 9.1%, so a more aggressive payout ratio helped dividend growth sneak into the teens.

If you look at HEPS though, you’re in for a big surprise. It came in wildly negative for the period. This is because although HEPS is designed to capture as many non-recurring items as possible, there will always be stuff that falls outside of its defined exclusions. In this case, HEPS was impacted by a large negative fair value adjustment on contingent consideration liabilities.

What on earth does that mean? Well, because of the price achieved on the sale of Life Molecular Imaging (LMI) on its disposal, Life needed to pay an “agterskot” of sorts to the previous owners of the business. This is a payment that happens down the line on an old deal, depending on how the asset performed and exactly what the terms of the original deal were.

This has led to a situation where current liabilities exceed current assets at Life, which makes it look as though the company is at risk of not funding its operations. The good news is that the payment on the contingent consideration is going to be paid from the proceeds related to the disposal. Accounting rules are forcing Life to account for the provision now and the proceeds on disposal only when the LMI deal closes. The balance sheet is actually in decent shape, with net debt to normalised EBITDA of 0.65x.

The LMI transaction is expected to close in the second half of the financial year, which will then lead to a much simpler balance sheet in the full-year numbers. From an operational perspective, Life expects paid patient days to grow by 1.5%, which does imply a slight slowdown in the second half vs. the first half.

Pick n Pay is still making losses (JSE: PIK)

Retail turnarounds are no joke

I’ve been pretty bearish on the overall turnaround at Pick n Pay, as regular readers will know. It’s an extremely difficult thing to get right, particularly when up against a competitive juggernaut like Shoprite (and others in the sector).

Although there have been some helpful changes to local operating conditions, like the near-disappearance of load shedding, Pick n Pay’s business still has major structural challenges. I don’t know about you, but I still see far more turquoise motorbikes on the road than anything else.

In a trading statement for the 53 weeks to 2 March, they’ve confirmed that the core Pick n Pay segment is still making losses after deducting lease costs. Thanks to how utterly daft the modern accounting standard for leases is, you actually have to specify whether lease costs are in or out of operating profit, as those costs are recognised as part of net finance costs. Sigh.

At group level, they’ve certainly made progress in reducing the losses. The headline loss per share has reduced by 55% to 75%, which means an expected range for the 53-week period of -77.49 to -43.05 cents.

Funnily enough, having the extra trading week in a 53-week period is a drag on earnings when you’re a loss-making business. There’s an extra week of losses, rather than an extra week of profits. The 52-week vs. 52-week disclosure in the detailed results will be interesting, as it will allow the market to isolate the final week and see exactly how loss-making the group still is based on the latest numbers.

I must point out that a major driver of the reduction in losses is that Pick n Pay tapped shareholders for equity capital so that they could reduce debt, thereby reducing finance costs as well. The real question here is around return on capital, which at the moment is still negative.

Despite the obvious risks, the share price is up 44% in the past 12 months and even closed 3.5% higher on the day of this trading statement.

Shaftesbury: London’s West End keep working (JSE: SHC)

Focused property funds can do very well, provided they focus in the right place

If you’ve ever had the joy of walking around London on a bright summer’s day (that part is very important), then you’ll know just how impressive areas like the West End are. Wealthy people from all over the world want to live and shop there, which is great news for property funds like Shaftesbury who specialise in the area.

They are having no problem with demand, with an update at their AGM noting that recent leasing transactions have been 8% ahead of their December 2024 Estimated Rental Value (ERV) and 9% ahead of previous passing rents. There’s 3% growth in the like-for-like annualised rent roll. Vacancies are down from 2.6% to just 1.7%.

At the beginning of April, Shaftesbury announced a long-term partnership with NBIM, the Norwegian sovereign wealth fund. This sees NBIM acquire a 25% stake in the Covent Garden estate, unlocking £570 million in capital for Shaftesbury.

This gives them plenty of money to deploy into new opportunities. Heck, they can even afford to shop at Harrods with that kind of money!

With a loan-to-value ratio of 17% after taking into account all the recent activity (way down from 27% at the end of 2024), I expect to see deal announcements from them in the coming months. I just hope they don’t lose their strategic focus.

Ever heard of Shuka Minerals? (JSE: SKA)

The company quietly listed a couple of days ago

Some companies list with a bang. Others sneak in, like a ghost in the night (of the non-finance variety). Shuka Minerals was certainly the latter. I thought I was hallucinating when I saw this new name come up on SENS!

Shuka is a junior African mining group that is listed on the AIM in London and now on the JSE as well. Their first update to the local market is about the restart of the Rukwa Coal mine in Western Tanzania. This will be needed to bring operational cashflow to Shuka, so that already gives you a flavour of where they are in their journey.

They anticipate a rather astonishing internal rate of return (IRR) of 80% on the staged ramp-up of the mine. All I can really say is that if every junior mining house always hit its targeted IRR, investors in the sector would have had a very different experience in years gone by.

Good luck to them – I look forward to following this story.

Modest growth at Spear REIT, but the direction of travel is still up (JSE: SEA)

The sector is taking a breather this year

Spear has announced results for the year ended February 2025. With the share price up more than 22% over 12 months despite growth of just over 3% in the distribution per share, we don’t need to look much further for evidence of how market sentiment towards South Africa has improved. With a portfolio focused on the Western Cape, Spear is seen in a particularly positive light.

Trading on a dividend yield of 8.3%, Spear’s yield is currently over 200bps lower than the SA 10-year bond yield. This implies that (1) the market is willing to pay up for focused Western Cape exposure and (2) Spear still needs to achieve strong growth over time to make up the differential to the “risk-free” return on offer with bonds.

Where does this growth come from? One source is positive reversions i.e. new leases being at better rates than the expired lease. Spear achieved positive reversions of 4.18% in FY25, so that’s decent. They’ve also been busy with major transactions, something that they should keep doing if the market is willing to pay up for their equity. You want to raise equity when your shares are expensive, not when they are cheap. Recycling capital (selling existing properties at great prices to then reinvest in properties at cheaper prices) is first prize of course, but if you run out of assets that you want to sell, then raising equity is the next port of call.

There are a few other metrics that are worth touching on. The industrial portfolio has an occupancy rate of 98.85% and in-force escalations of 7.3% – in short, the Western Cape is firmly open for business. The retail portfolio managed positive reversions of 8.53% and in-force escalations of 7.25% – the Western Cape is also open for shopping. And finally, the office portfolio had negative reversions of just -3.17% and occupancy of 92.99% – the Western Cape is increasingly open for people to do meetings in person rather than over Zoom while persuading their cat to stop meowing*.

The group expects distributable income per share to grow by between 4% and 6% for the year ending February 2026. The payout ratio is expected to remain at 95%.

When I read results like this, I remember why I semigrated 10 years ago.

*references to cats are based on my lived experience

A period to forget for Tharisa (JSE: THA)

In mining more than any other sector, there are good times and bad times

And this, dear reader, was a bad time. For the six months to March 2025, Tharisa suffered a drop of 23.9% in revenue and 45% in EBITDA. Net profit after tax tanked by 78.9%. Yikes.

Cash from operating activities fell by 58.2%. It’s just as well that capital expenditure was 46% lower, as this helped protect the overall strength of the balance sheet in a difficult period.

And despite all this, the interim dividend was identical to the comparable period at US 1.5 cents per share. Companies would sooner sell off their first-born child than cut their dividends.

So, what went wrong in this period? One of the issues was that PGM production fell at exactly the wrong time, as this was a rare example of a period in which average PGM basket prices actually moved higher. Chrome output was also negatively impacted, in both cases due to an inconsistent ore mix. This is why PGM gross profit margin more than halved from 15.2% to 6.2%, while chrome gross margin also took a serious knock from 26.5% to 17.4%.

They seem confident that they can make up for it, as they are maintaining their guidance for FY25.

Nibbles:

Anglo American (JSE: AGL) announced the results of their dividend reinvestment plan. Shareholders didn’t exactly surge to the front when it came to this opportunity, with holders of just 1.77% of shares on the UK register and 0.89% of shares on the SA register electing to receive shares instead of cash.

I generally don’t comment on non-executive director appointments unless I see something that really catches my eye. Santam (JSE: SNT) announced that Richard Wainwright will be appointed as an independent non-executive director. The reason that this is interesting is that Wainwright was the CEO of Investec’s banking business until as recently as 2024.

Schroder European Real Estate (JSE: SCD) certainly can’t be accused of not keeping the market updated on operational news. They’ve renewed a lease with DIY group Hornbach, which contributes 11% of income in the Schroder portfolio as the second largest tenant. The new lease is for 12 years and is a triple net lease that is subject to indexation, which is a fancy way of saying that Schroder has great certainty over the amount they will earn and it will increase by an inflation-linked amount each year. They note that the new lease is ahead of the Estimated Rental Value (ERV), but they don’t indicate by how much.

Greencoat Renewables is coming to the JSE (JSE: GCT)

We are getting another new listing on the local market!

Here’s some exciting news: the JSE has granted approval for a fast-track secondary listing of Greencoat Renewables on our local market. This is an Irish renewable energy infrastructure company that invests in European renewable electricity generation and storage assets.

With a market cap of roughly €844 million, this is a substantial business. There are plenty of renewable energy enthusiasts in South Africa and this will give them something new to sink their teeth into.

To get to grips with the portfolio and its mix of wind, solar and battery storage assets, along with its focus on delivering dividends to investors, you can register for an upcoming Unlock the Stock session with the management team on 29th May at 12pm.

Hammerson boosts FY25 guidance based on recent activity (JSE: HMN)

They are singing a positive tune over there

With a share price that has delivered a 4% drop in GBP in the past year and a 1.7% drop in ZAR, Hammerson hasn’t exactly been a market darling. The property fund is trying to change that, with recent deal activity and a positive tone to the latest update.

They expect a gross revenue increase of 10% for 2025, which is way ahead of the 4% – 6% medium-term CAGR that they aim for. They have reaffirmed adjusted earnings guidance though, so the uptick in revenue doesn’t seem to be flowing through to shareholders yet.

One of the reasons for the increase is the acquisition of almost all the remaining ownership units related to Brent Cross, with the price representing a 16% discount to book value and a net initial yield of 8.6%. Combined with another recent deal, this means that they recycled the capital from the disposal of Value Retail (at an exit yield of 3.4%) into gaining control of assets at an average yield of 8.5%. That sounds solid.

Like-for-like sales growth isn’t quite as exciting, up just 1% for the first quarter. Remember that the UK is a structurally lower growth market than South Africa (and certainly the European regions that our local funds love), so you would expect to see modest growth.

The company has noted that there’s a real estate conference this week and that they will publish updated investor information.

Mahube Infrastructure’s earnings have taken a big knock (JSE: MHB)

This is due to the change in dividends from portfolio companies

Mahube Infrastructure released a trading statement for the year ended February 2024. HEPS is expected to decrease by between 32.87% and 39.26%, so that’s a significant drop.

They attribute this to lower dividends from the investee companies, at least to some extent because of special dividends in the prior period from refinancing of solar projects. Detailed results are due for release on 30 May.

MultiChoice is getting the right advice on dealing with the Competition Commission (JSE: MCG)

The Commission is recommending that the Canal+ deal be approved

The South African Competition Commission is a tough beast to deal with. They are pretty famous at this point for regulatory overreach, with the term “public interest” being used and sometimes abused to force greater levels of e.g. B-BBEE than would otherwise be the case.

Advisors are clearly learning from this and are trying to go on the front foot, advising clients to rather go in with a proposed package of public interest considerations vs. sitting back and waiting for the regulator to get creative. Believe me, nobody needs or wants creative regulators.

MultiChoice has shown the way here, having proposed various public interest commitments related to B-BBEE and SME participation in the audio-visual industry in South Africa, while supporting local content. This is another reminder of how broad the thinking is at competition regulators and how much of their work goes way beyond what anyone would traditionally think of as competitive factors i.e. whether consumers have sufficient choice.

The Competition Commission has accepted the proposed commitments and will recommend to the Competition Tribunal that the deal should be approved. Given all the financial difficulties being faced by MultiChoice right now, I think it’s pretty clear that a successful deal here is firmly in the public interest.

Tough numbers at Reunert (JSE: RLO)

Earnings are down even if you exclude the battery storage business

Reunert released a trading statement for the six months to March 2025. It’s not pretty, with an expectation for total HEPS to drop by between 19% and 24%.

Now, you may be hoping that things get better if you look at continuing operations, but that isn’t really the case. Even if you exclude the Blue Nova Energy battery storage business that they have decided to cut their losses on and sell, the drop in HEPS would be between 17% and 22%.

This tells you that there are troubles elsewhere in the business. Some of this is a timing issue, like a delayed contract in the Defense Cluster and lower cable sales based on a delayed energy infrastructure investment programme. Perhaps the most comforting news for investors is that a COVID business interruption claim in the base period was good for 32 cents worth of HEPS. That’s obviously a non-recurring source of income, so more than half of the drop in continuing HEPS of between 50 and 66 cents is attributable to the insurance claim.

Still, the share price closed 3.9% lower off the back of this news. Detailed interim results are due to be released on 28 May.

RFG dragged down by the international segment (JSE: RFG)

Margins are under pressure

RFG Holdings released results for the six months to March 2025. They struggled, as group revenue growth of 3.5% didn’t convert into profit growth. In fact, due to pressure on margins, HEPS came in 11.9% lower.

The trouble was in the international segment. While the regional segment grew revenue by 7.6% and only saw its operating margin dip by 90 basis points, the international segment suffered a 17.2% drop in revenue and a collapse in operating profit margin from 11.5% to just 0.1%! Ouch. This is what happens when there is severe selling price deflation coupled with a decline in volumes.

This means that literally all the operating profit in this period was from the regional business. Luckily, it’s by far the largest part of the business (even before international profits collapsed), so the impact on group earnings was painful but manageable. It also helped that average debt and interest rate levels were lower, leading to a significant decrease in net interest costs.

Looking to the second half of the year, they expect the regional segment to continue its momentum. The international segment is showing signs of improvement. This should support a better final dividend, with the interim dividend only representing a payout ratio of 33% (the group target is 50% – so this implies a catch-up later this year).

Despite this, the share price is up around 38% over 12 months and closed 3% higher after this earnings update. The market must be strongly believing in what the second half might bring.

Sanlam teams up with Tyme Bank (JSE: SLM)

The focus is on personal loans with an embedded credit life product

Sanlam just never sits still. It’s incredible how regularly they announce deals and major partnerships. This one is admittedly very close to home of course, as Tyme is part of the African Rainbow Capital stable, which in turn is run by ex-Sanlam execs.

One of Sanlam’s many businesses is called Sanlam Personal Loans. They give loans of between R5k and R300k for between 12 months and 6 years – a typical model in this space. It’s a big book, coming in at R5 billion as at December 2024.

As for Tyme Bank, they have 11 million retail and business customers, so that’s a substantial distribution channel.

The parties have decided to start a new joint venture. Sanlam will sell its loan generation business into the joint venture at an effective valuation of R63 million, as Tyme will buy a 50% stake in the joint venture for R31.5 million. Then, Sanlam will sell 50% of its retail credit loan book for R400 million plus the capital value. Finally, Tyme will pay R320 million for shares that give it 50% of the credit life results related to the loans in the joint venture.

Essentially, what they are doing here is building a lending business on Tyme Bank’s infrastructure, targeting the client base of both entities. They will of course take advantage of Sanlam’s experience in credit life insurance.

As this is a small related party transaction, it can only go ahead if there’s a fairness opinion backing it up. Deloitte have opined that the terms of the deal are fair.

There are a few regulatory hurdles to be overcome, including approval from the Prudential Authority and the Competition Commission. They hope to be done with the deal by the end of March 2026.

Spear REIT picks up a business park in Paarl (JSE: SEA)

There’s plenty of growth around Paarl, so this seems sensible

Although everyone talks about the semigration from Joburg to Cape Town, I don’t often see people refer to the rotation of capital from Cape Town into the winelands. The growth in Val de Vie and neighbouring estates is quite something to behold. Paarl is part of that broader growth story, attracting many families who either work remotely or have jobs in the winelands.

As more people move to these areas, it stands to reason that demand for commercial property will increase. It therefore makes sense to see Spear REIT announcing the acquisition of the Berg River Business Park in Paarl for just over R182 million. If you include transaction costs and immediately required capital expenditure, this increases to R187.5 million.

This is an industrial asset that they are acquiring on a purchase yield of 9.35%. The seller has guaranteed the rental for certain occupied units for 18 months and has also committed to guarantee electricity savings from a recent solar energy installation.

The weighted average lease duration is 5.27% and the weighted average escalation is 7.12%, which is solid. Spear’s investment thesis is built around focused exposure in the Western Cape and they are doing a good job of sticking to their knitting.

Southern Sun has much to be proud of (JSE: SSU)

This remains the best option in the sector

Southern Sun is doing really well. They play exactly where you want to be in the hospitality space: hotels in business centres that play to higher income tourists, business travellers and from time to time, locals. What you don’t want to own right now is old-school casinos. I also remain bearish on cheaper accommodation aimed at local business travellers.

For the year ended March 2025, occupancy grew by 220 basis points to 60.8%. This drove income growth of 9% and EBITDAR (not a typo) growth of 14%. Thanks to a reduction in debt and thus net finance costs, adjusted headline earnings per share climbed 34%. But the best growth rate was saved for the dividend, which casually doubled (that’s a 100% growth rate) to 25 cents per share. Mooi.

Speaking of mooi, the beautiful Western Cape continues to be extremely lucrative for hotel groups, with revenue up by 17% and EBITDAR up 26%. But here’s the real surprise: Gauteng grew even faster (revenue up 19% and EBITDAR 35%) albeit off a more depressed base, helped along by conferencing demand. Alas, KZN and Mozambique can’t say the same, with a lack of conferencing in Durban hurting the story. In Mozambique, political unrest has an incredible way of making people choose other destinations for a holiday. Strange, that.

Although the business is doing really well, it’s still not a simple thing to run. For example, they’ve closed Paradise Sun in the Seychelles for a full refurbishment to help reposition the hotel as a premium leisure resort for European travellers.

The group’s balance sheet is incredibly strong. Provided that South Africa can maintain a decent reputation on the global stage despite the best efforts of certain countries, they should keep doing well.

Nibbles:

Director dealings:

Des de Beer is back on the bid for Lighthouse Properties (JSE: LTE), buying R1.4 million in shares.

Although this sale of shares is entirely to cover the tax on share-based payments, I’m still going to mention the extent of sales by directors of Northam Platinum (JSE: NPH) after the vesting of shares under an old plan. The sale comes to a total of R105 million – and remember, that’s just the taxable portion! Best of all, it’s just three directors. It’s a good life.

Interestingly, with James Formby (ex-CEO of RMB) expected to replace Gareth Ackerman as chairman of Pick n Pay (JSE: PIK) from August, Formby is going to step down as chair of Boxer (JSE: BOX). Sean Summers is going to replace Formby as the chair of Boxer from February 2026. So, a few familiar names here playing musical chairs. An additional change worth noting is that Pooven Viranna will be the new independent non-executive director of Pick n Pay, replacing the role that Formby leaves vacant as he moves to chair the board there.

Curro (JSE: COH) has had its credit rating affirmed with a positive outlook by GCR Ratings. They note that the maturity of the school portfolio and the associated cash flows were positive factors here. As I always remind you, the lens for debt is very different to that of equity investing. Debt investing is about managing downside risk, while equity investing is about chasing risk-adjusted upside.

Capital Appreciation Limited (JSE: CTA) has been busy with share buybacks, having repurchased 3.26% of shares in issue based on the general authority given by shareholders for buybacks at the September 2024 meeting.

Deutsche Konsum (JSE: DKR) probably isn’t in your portfolio. Just in case it is, I’ll mention that the company has appointed GPEP GmbH to take over the asset and property management for its portfolio. It’s not unusual for the day-to-day management of properties to be outsourced by funds. It all depends on their operating model.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.