ADvTECH pushes deeper into Africa as a growth area (JSE: ADH)

And their track record certainly supports this decision

ADvTECH’s schools business does well because it has a differentiated offering of private schools that appeal to high income parents. This has proven to be the right approach, with Curro (JSE: COH) struggling to fill its school footprint that is essentially a broader offering to middle-to-higher income parents. Let’s also not pretend that the birth rate isn’t a serious issue here, with a more focused offering of fancier schools looking less vulnerable than a wide footprint of underutilised schools.

Part of ADvTECH’s strategy also includes high quality schools in Africa, appealing to expats and wealthier locals. Again, it’s a good model. They are expanding this offering in Kenya through the acquisition of Regis Runda Academy for around R172 million. This will be rebranded as Makini Schools Runda, which means it will operate within ADvTECH’s existing brand in Kenya.

Given the track record of success with schools like these, this seems like a sensible acquisition to me.

Blue Label Telecoms plays its cards close to its chest (JSE: BLU)

A trading statement for the year ended May 2025 has the bare minimum disclosure

There’s a particular feature of trading statements that is very important for investors to understand: they are triggered by earnings moving by a minimum of 20% vs. the prior period. This means that when a trading statement notes that earnings moved by “at least 20%” then the company is essentially giving the bare minimum required disclosure. You can contrast this to MTN below for example, where the trading statement gives an earnings range.

Over at Blue Label Telecoms, despite this trading statement dealing with the year ended May 2025 (which is now behind us by a couple of months), they’ve only taken the route of indicating moves of at least 20%. This is across HEPS, core HEPS and earnings per share (EPS) as well. In reality, the likely move is significantly higher than that, evidenced by a share price that is up by a colossal 280% in the past 12 months!

Blue Label will release earnings on 27 August. They have indicated that a further trading statement will be released before then, dealing with a specific earnings range for these core metrics.

A bit of love from the market for Metair’s turnaround (JSE: MTA)

The share price closed 6% higher on the day of a trading update

Metair is busy with a tough turnaround. The company has far too much exposure to new car production in South Africa, a long-term risk that they are trying to mitigate by moving into the aftermarket parts business. Even if we stopped manufacturing cars tomorrow, there are still millions of cars on the road in South Africa. I therefore see it as a sensible strategy to tap into this market, executed through the acquisition of AutoZone that adds to existing businesses in this vertical that offer products like batteries.

Of course, it doesn’t hurt in the meantime if volumes at the South African manufacturers move higher, with the added benefit of Metair making progress with its strategy to improve businesses like Hesto Harnesses. Production volumes in the South African market increased by 4% this period. Thankfully, Metair’s customers don’t supply directly into the US market, so there’s no direct impact from tariffs. It’s about time that Metair had some good luck. They’ve had more than anyone’s fair share of bad luck!

For the six months to June 2025, revenue from continuing operations increased by between 52% and 54%. This immediately needs to be followed up by two important nuances. The first is that Hesto is now accounted for as a subsidiary, so its revenue wasn’t in the base period (it was accounted for differently before). The second is that AutoZone is now in these numbers and wasn’t in the base.

The percentage move is therefore unhelpful. It’s much more useful to just note that revenue will be close to R8.7 billion, with expected EBIT of R440 million to R460 million. As you can see, margins are still far too low in this business, coming in at just over 5%. AutoZone is a drag on margins at the moment with negative EBIT, as they acquired it out of business rescue and will need to improve its performance as quickly as possible to get the most out of that opportunity.

From continuing operations, HEPS is expected to be between 69 cents and 72 cents, down between 6% and 10%. This is a sign of stabilisation in the core business, as the driver of that decrease is the punt on AutoZone.

Importantly, Metair has met all covenants of its restructured debt package. They aren’t completely out of the woods yet (and there’s still the overhang of the European Commission’s investigation into battery manufacturers in Europe that impacts one of Metair’s businesses), but they are clearly on the right track.

MTN’s African subsidiaries have driven a wild positive swing in earnings (JSE: MTN)

Despite Nigeria and Ghana having already reported, MTN still rallied on this news as though it was a surprise

MTN’s share price is up 123% in the past year. That’s a pretty spectacular situation for investors, helped along by the share price closing 5% higher on Thursday in response to MTN releasing a trading statement for the six months to June 2025.

With MTN Nigeria and MTN Ghana having already released strong numbers for the second quarter, it was clear that the MTN group numbers would be solid as well. But the market seems to have gotten a positive surprise from just how good they were, otherwise we wouldn’t have seen another 5% rally on the day of results.

The percentage move is slightly insane, with HEPS improving by more than 300%. What this really means is a substantial swing from a headline loss per share of -256 cents into expected positive HEPS of 614 cents to 666 cents.

Detailed results are due on 18th August.

RCL Foods had a solid year – but the second half was much slower than the first half (JSE: RCL)

The sugar business had a tough end to the year

RCL Foods released a voluntary trading statement for the year ended June 2025. After an interim period in which underlying HEPS jumped by 28.9% and HEPS as reported was up 38.8%, shareholders will probably be disappointed to see that this is only a voluntary trading statement, as it means that the full-year move isn’t more than 20%.

Sure enough, HEPS from total operations will be between 5.6% and 12.6% higher, while underlying HEPS from continuing operations will be between 9.6% and 17.5% higher. Viewed in isolation, that would be decent. But after what happened in the interim period, it’s almost a tough pill to swallow.

The challenge in the second half was in the sugar business, with RCL Foods attributing the issues to the presence of imports that took market share from local volumes at a time when global sugar prices moved lower.

For all the significant movements in earnings, the share price has managed to come out flat over 12 months.

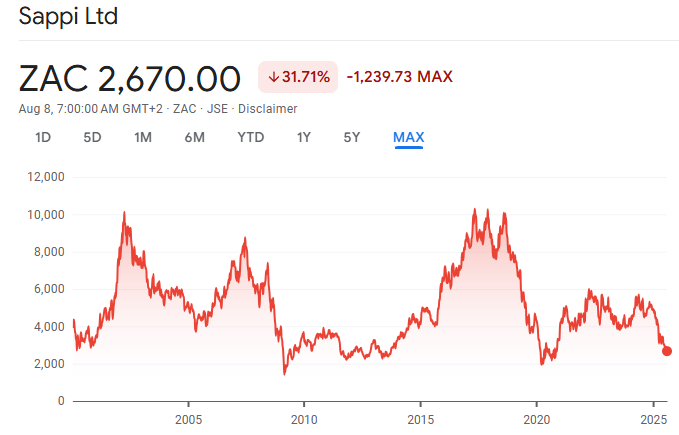

The Sappi rollercoaster ride continues (JSE: SAP)

I don’t think there’s a more volatile sector out there than paper

Do you miss Ratanga Junction in Cape Town? Wish you could get to Gold Reef City more often? Well… do I have a stock for you!

If that’s what the volatility looks like over such a long period, you can imagine what it looks like from one quarter to the next. For example, in the quarter ended June 2025, revenue fell 4% year-on-year and adjusted EBITDA tanked by 46%. With net debt up 45%, this combination was enough to push them into a net loss of $33 million vs. profit of $51 million in the comparable quarter.

But if we look over the nine months to June vs. the comparable nine months, the situation is reversed in terms of net profitability. Despite revenue being up just 1% and adjusted EBITDA falling by 15%, the bottom of the income statement shows a swing from a loss of $46 million to profit of $17 million.

The reason for profits that bounce around like a Jack Russell on heat is that the global paper sector is cyclical. Sappi is a price taker, not a price maker – just like a mining company. Then you can layer on forex movements, potential manufacturing issues across a number of underlying facilities and of course the fair value adjustments to the forestry assets as well.

And even when Sappi manages to navigate the cyclical difficulties, they sometimes have to deal with a structural decline like we’ve seen in graphic papers.

Above all, it looks like the biggest current stress is the leverage ratio increasing to 3.2x, with a perfect storm of weaker performance and a heavy capex programme at Somerset Mill. Although the worst of the capex is behind them, they now have to claw their way out of the debt. Much as one may hope that the expansion at Somerset Mill will have an immediate positive impact on profitability, the reverse is unfortunately true – there will be a period of optimising and ramping up that project.

They do at least hope that adjusted EBITDA for the upcoming fourth quarter will be above that of the third quarter that they just reported on. Let’s see if they are right.

The Foschini Group’s share price is sliding again (JSE: TFG)

The market is unhappy about something here

The retail apparel sector has had a tough time this year. I recently switched out of my Sibanye-Stillwater position (leaving a small amount behind) and bought Mr Price (JSE: MRP), hoping for a recovery there as it strikes me as the baby thrown out with the bathwater this year. With a much more difficult portfolio that includes international exposure (and no plans to pull back from that), The Foschini Group strikes me as the bathwater itself.

The share prices are highly correlated, but I’m not convinced it will play out that way for the remainder of the year:

My thesis is strengthened by the market’s sharp negative reaction to the quarterly trading update from The Foschini Group, with the share price down 5.7%. On the same day, Mr Price was flat.

The first important point when looking at the trading update is that you need to exclude the acquisition of White Stuff in the UK. Like all acquisitions, the timing impacts comparability, as you have a business included in one period and not the other. On that basis, group comparable sales for the first quarter were up just 2.5% (in ZAR), while TFG London was down 2.6% in local currency. As for TFG Australia, sales were down 2.8% in local currency. Ouch.

As we’ve seen at rival Woolworths (JSE: WHL), the Beauty category is doing the heavy lifting at the moment. The Foschini Group’s sales in this category in TFG Africa grew by 24.5%, which is way higher than Clothing (4.2%) and Homeware (8.5%). Sadly, Beauty is just 3.2% of TFG Africa’s sales, so it’s much too small to offset slower growth elsewhere.

Store sales in TFG Africa increased by just 3.2%, while online sales were up 40.2% thanks to Bash. Online is now 7% of total TFG Africa sales, up from 5.2%. The omnichannel model is certainly working well.

Credit sales in TFG Africa increased by 9.3% to now contribute 28.2% of total TFG Africa sales. They aren’t explicit in the announcement, but some quick maths shows that cash sales must therefore have grown 3.7%.

The announcement is very light on details on TFG London, which doesn’t help when sales excluding White Stuff are down. They unfortunately don’t give online sales growth with an adjustment for White Stuff either, but we do know that online is 43.1% of TFG London sales. Sales growth excluding White Stuff was 6.3% for the three weeks to 19 July 2025, but I would be very nervous putting much faith on such a short period.

And in TFG Australia, there’s also little to hang your hat on – they blame the macro environment and its impact on consumers, along with the overall extent of promotional activity in the market that is hitting margins.

In addition to this update, the market has the Capital Markets Day presentations to chew on. It includes some great stats, like in the omnichannel deck where there’s a note that omnichannel customers spend up to 9x more without cannibalisation (i.e. of in-store sales), which improves share of wallet and customer retention.

I think this is the most worrying slide for me, showing White Stuff as being right in the middle of this quadrant that describes the competitive environment:

If you try and appeal to everyone, you appeal to no one. I’m certainly no retail exec, but “bridge market” just sounds like to me like a strategy that doesn’t know what it actually is. Zara is the most valuable name on that chart and they aren’t anywhere near the centre.

As for TFG Africa, apart from the deck including an incredibly odd map that talks about the “national footprint across South Africa” and then has pins only on the Western Cape, they’ve also put out an astonishingly ambitious 3-year CAGR for turnover of 12.9%. This would drive a 3-year CAGR for EBIT of 15.9%. I think the market would be pretty happy with even half of that, so that’s a huge target to make a public commitment to.

Time will tell!

Nibbles:

Director dealings:

An associate of a non-executive director of Glencore (JSE: GLN) bought shares worth around R330k.

Montauk Renewables (JSE: MKR) is an obscure name in the market, as the company is engaged in renewable energy projects in the US. There’s not much familiarity with the business among local investors and the company doesn’t really put in any effort to change that. So, I’ll just give the quarterly results a brief mention down here on an otherwise busy day of news from companies that you’ll recognise. For the quarter ended June 2025, Montauk increased revenue by 4.1%, but suffered a 27.7% drop in adjusted EBITDA. This was driven by a 22.4% decrease in pricing for the renewable fuel that they produce. The net loss for the quarter was $5.5 million, worse than $4.8 million in the comparable quarter in 2024.

An important milestone has been achieved in the Prime Kapital offer to shareholders of MAS (JSE: MSP). The SARB has approved the inward listing of the preference shares on the Cape Town Stock Exchange. This is a biggie, as it removes a concern around South African shareholders who might otherwise have needed to accept share-based settlement without a guarantee of the listing being approved. That uncertainty is now gone and investors can consider the preferences shares based on their merits rather than their potential existence.

Life Healthcare (JSE: LHC) has announced a special dividend of 235 cents per share from the proceeds of the disposal of Life Molecular Imaging. For context, the share price is around R13.60, so this is roughly 17% of the market cap.

Here’s your daily update on acceptances in the Primary Health Properties (JSE: PHP) offer to Assura (JSE: AHR) shareholders: with less than a week to go in the offer period, acceptances have been received by holders of 3.38% of shares.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.

In the 59th edition of Unlock the Stock, Capital Appreciation returned to the platform to walk us through their recent performance and their growth areas going forwards. I co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

What do the colours of a popular toothpaste tell us about how we think about wealth?

In the latest episode of the No Ordinary Wednesday podcast, Alexandra Nortier and Marc Romberg, joint heads of Wealth Management at Investec Wealth & Investment International, join Jeremy Maggs to explore how the nature of wealth is changing.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Collins Property Group’s Netherlands subsidiary has concluded a series of inter-conditional agreements with Budé Beheer B.V. to acquire the property letting enterprises in respect of the associated properties of eight Do It Yourself stores (Gamma and Karwei franchise stores). The properties will continue to be tenanted by these franchise stores. The cash purchase consideration of €31,5 million may be adjusted upwards but is capped at €32,79 million.

In a deal which further expands its footprint in East Africa, ADvTECH has acquired Regis Runda Academy located northeast of Nairobi in Kenya. The academy, acquired for KSh1,23 billion (R172 million) will be rebranded as Makini Schools Runda.

Sirius Real Estate has acquired a further two business parks. The first, acquired for €23,4 million is in Dresden, Germany. Sirius plans to convert this into a multi-let industrial park. The second acquired for £16,13 million is a UK multi-let business park in Bedford, comprising warehouse, leisure, studio and office space.

Prime Kapital Investments (PKI) has launched its conditional voluntary bid to acquire those MAS plc shares not already held. The condition refers not to the acquisition of all outstanding MAS shares but rather to at least 10% of minorities accepting the offer of €1.40 per share. PKI has received SARB approval to list the consideration instruments on the CTSE. The offer period closes on 14 August 2025.

Prosus has led a US$4,17 million (R75 million) pre-Series A funding round in Arivihan, India’s first fully AI-based learning platform. The funds will be used to scale Arivihan’s go-to-market strategy and to building localised distribution networks in new geographies.

Deneb Investments has disposed of a property, considered non-core to its strategy, to Earth Instyle for a consideration of R48,5 million. The property situated at 195 Leicester Road, Mobeni in Durban was valued in the last company audited results for 31 March 2025 at R50,2 million. Proceeds will be applied to reducing debt.

To ensure compliance with the foreign control restrictions relating to the mandatory offer by Canal+, MultiChoice South Africa will be reorganised – details of this have now been announced. For an excellent explanation and analysis of a complex set of sequential inter-conditional transactions read Ghost’s summary here.

In its latest update, Primary Health Properties plc (PHP) says it has received valid acceptances for c.3.38% of Assura plc shares (110,278,589 shares) under the revised offer. Assura shareholders have until 12 August 2025 to accept the offer.

Unlisted Companies

Local travel fintech startup TurnStay has secured US$2 million in seed funding in a round led by First Circle Capital with participation from TLCom Capital, Enza Capital, Incisive Ventures, CVVC and Equitable Ventures. The funds will be used to expand its innovated stablecoin-based payment solution for Africa’s tourism sector. Tourism operators can accept card payments for international travellers in their local currencies while settling locally in stablecoins. This slashes transaction costs by as much as 70% and significantly accelerates the payout cycle, helping improve cash flow and reduce dependency on global travel platforms. TurnStay raised $300,000 pre-seed funding in July 2024.

Super app-as-a-service platform Flood has raised US$3,5 million in seed funding from venture capital firm CRE.vc and backed by angel investors. This follows a $1 million round in July last year. The platform which operates in SA, India and the Maldives will use the funds to expand into new emerging markets over the next few years. Flood’s value proposition for the digital commerce ecosystem in emerging markets is to onboard offline merchants to streamline financial inclusivity by partnering with telecos and banks to support this process.

Altera Biosciences, Africa’s dedicated cell and gene therapy biotech company, has successfully closed a R29 million pre-seed funding round. The investment, secured from venture capital firms including OneBio Venture Studio and E Squared Investments, will be used to further develop a universal donor cell platform.

Afriwise, a legal and regulatory intelligence platform for Africa, has acquired LawExplorer, a South African provider of regulatory monitoring and legislative tracking solutions. Financial details of the transaction were not disclosed.

IZI Group has completed its acquisition of G4S Cash Solutions (SA), following the receipt of all regulatory approvals. The deal was structured to ensure continuity for staff and suppliers and customers.

Life Healthcare (LHC) has declared a special cash dividend of 235 cents per ordinary share, payable from income reserves derived from the net proceeds received following the disposal of its interest in in Life Molecular Imaging. In January 2025, LHC announced the disposal to Lantheus Holdings in a deal valued at $750 million (R13,8 billion).

In terms of Sirius Real Estate’s dividend reinvestment plan (DRIP), shareholders on the UK share register holding 1,38% of the company’s issued share capital opted to receive shares in terms of the DRIP, resulting in the purchase of 540,336 shares in the market at an average price of £0.99 per share. Shareholders on the South African register holding 7.81% of the company’s issued share capital took up the DRIP option resulting in the purchase of 2,944,999 shares in the market at an average price of R24.85. The purchased shares represent a cash equivalent of €4,3 million.

Novus has acquired on the open market 22,355 Mustek shares at a price per share of R13.00. The shares were acquired outside of the Mandatory Offer for an aggregate value of R290,6 million.

In line with Glencore’s policy to maintain the number of treasury shares below 10% of the total issued share capital of the company, 50 million treasury shares have been cancelled. Following this, the total number of treasury shares held represents 9.57% of the company’s total issued share capital.

PK Investments has received SARB approval for consideration instruments to be listed on the CTSE. Following this approval, the listed consideration instruments will be issued to MAS plc shareholders electing to receive these instruments in respect of all or some (cash alternative) of their MAS shares.

This week the following companies announced the repurchase of shares:

Over the period 5 August 2024 to 5 August 2025, PBT Group repurchased 4,120,447 ordinary shares for an aggregate R23,37 million. The shares were acquired at an average price of R5.67 per share and will be cancelled and delisted. The company may repurchase a further 6,26 million shares representing 6.03% of the ordinary shares in issue.

iOCO will embark on a share repurchase programme to repurchase up to a maximum of 1,8 million of its ordinary shares. The programme commenced on 1 August and will be for a maximum of six months.

During the period 28 November 2024 to 31 July 2025, Datatec repurchased 4,147,205 shares on the open market for an aggregate R227,6 million. The shares were delisted on 6 August 2025.

Glencore plc’s current share buy-back programme plans to acquire shares of an aggregate value of up to US$1 billion. The shares will be repurchased on the LSE, BATS, Chi-X and Aquis exchanges and is expected to be completed in February 2026. This week 6,6 million shares were repurchased at an average price of £2.98 per share for an aggregate £19,47 million.

In May 2025 Tharisa plc announced it would undertake a repurchase programme of up to US$5 million. Shares have been trading at a significant discount, having been negatively impacted by the global commodity pricing environment, geo-political events and market volatility. Over the period 28 July to 1 August 2025, the company repurchased 17,743 shares at an average price of R21.44 on the JSE and 253,538 shares at 91.29 pence per share on the LSE.

In May 2025, British American Tobacco plc extended its share buyback programme by a further £200 million, taking the total amount to be repurchased by 31 December 2025 to £1,1 billion. The extended programme is being funded using the net proceeds of the block trade of shares in ITC to institutional investors. This week the company repurchased a further 578,159 shares at an average price of £41.41 per share for an aggregate £23,93 million.

During the period 28 July to 1 August 2025, Prosus repurchased a further 2,189,791 Prosus shares for an aggregate €110,08 million and Naspers, a further 139,626 Naspers shares for a total consideration of R792,8 million.

One company issued a profit warning this week: Metair Investments.

Rasaad Nigeria, a family-led agribusiness that aggregates high-quality cocoa and cashew nuts from over 1,000 smallholder farmers, has raised a US$590,000 loan facility from Sahel Capital’s Social Enterprise Fund for Agriculture in Africa fund.

Egyptian digital procurement platform Suplyd has raised US$2 million in a pre-Series A round led by 4DX Ventures, Camel Ventures, and Plus VC, with participation from Seedstars and existing investors. This funding will support the company’s mission to build a comprehensive infrastructure for restaurant operations and expand into untapped areas across Egypt.

Kasada, a leading pan-African hospitality investment platform, recently closed a €15 million debt facility provided by the Africa Go Green Fund, managed by Cygnum Capital. The facility will provide finance for a greenfield hospitality development in Abidjan, Côte d’Ivoire. The project, which will be in the Angré district, will feature a hotel with a total of 170 keys, co-working facilities under the Wojo brand, and a dedicated MICE (Meetings, Incentives, Conferences, and Exhibitions) venue. The hotel is expected to attract regional business traffic, including from Small and Medium Enterprises located in the area, while introducing Angré’s first EDGE-certified hotel.

The International Finance Corporation and Sony Innovation Fund have announced an investment into Nigeria-based Filmmakers Mart (FMM), Africa’s first integrated digital production platform, to enhance access to production services in Africa’s film and entertainment industry. The investment will support FMM expansion from its current markets in Nigeria, Kenya, Ghana, Morocco and South Africa into new markets. It will also fund the development of new platform features, including subscription models, post-production tools, and training programs designed to serve a growing community of creators.

Egypt-based Saas provider Wuilt has raised US$2 million in a funding round led by follow-on investment from Flat6Labs and MTF VC, with participation from Hub71, JIMCO, Purity Tech, and a group of other angel investors. With the new capital, Wuilt plans to launch its free platform in the UAE in Q4 2025, followed by GCC countries and Turkey in Q1 2026. This comes after Wuilt’s April 2025 announcement it would offer its core platform completely free in Egypt, eliminating all subscription fees and forgoing hundreds of thousands of dollars in annual recurring revenue in a move to accelerate merchant adoption. Since then, over 20,000 merchants have joined the platform.

Mediterrania Capital Partners has announced an investment in Dislog Dispositifs Médicaux (DDM) through a DM 540 million capital increase together with CDG Invest Growth. This fund-raising – the largest in Dislog’s history –marks a decisive turning point in the development of its healthcare division. Morocco’s healthcare sector is set to accelerate its growth, driven by increasing investments and untapped potential in healthcare spending and infrastructure. The sector thrives on population growth, rising GDP, and expanding medical coverage, setting the stage to realise its full potential.

The Trans Hex write-down has hurt Astoria (JSE: ARA)

The rest is a mixed bag at the moment

Investment holding company Astoria is one of the victims of lab-grown diamond disruption. The group has fully written down the value of the investment in Trans Hex and Marine Diamond Operations, which were collectively valued at R72 million as at the end of December 2024. That’s around 10% of the NAV at that date, so it hurts. The silver lining is that the management team has chosen to rather walk away from giving further support to this asset vs. the alternative of throwing good money after bad.

With the NAV down 9.1% from December 2024 to June 2025, the diamond write-down explains the negative move. The rest of the portfolio has some ups (like Leatt and Goldrush) and downs (Outdoor Investment Holdings).

The largest asset by far is Outdoor Investment Holdings, in which Astoria has a 40.2% stake. It now represents over 60% of the NAV thanks to the disappearance of the diamond values. Recent turnover growth has been modest and margins have taken a knock, leading to a 4% decline in the value of that stake.

After the investment in Leatt (R84.7 million), the third largest asset is now cash and receivables (R63.1 million) thanks to the disposal of the stake in ISA Carstens. This means that nearly 10% of the NAV is in cash.

Speaking of the NAV, Astoria’s NAV per share is R10.65 and the share price is R7.90.

Collins Property does it themselves in the Netherlands (JSE: CPP)

They’ve bought a substantial portfolio of properties with DIY tenants

Collins Property Group has taken the route that a number of other South Africans have taken in the past few years: looking for opportunities in the Netherlands. Perhaps they really like the colour orange, or Max Verstappen. I suspect that above all else, they like earning euros.

Collins (part of the broader Christo Wiese stable, as you may recall) is acquiring a portfolio of 8 properties for €31.5 million. Adjustments might take the price as high as €32.8 million. The tenants are DIY stores that are being sold to a new owner, so Collins is swooping in and doing the property leg of the deal.

Although this does introduce the risk of the tenants being under new ownership, Collins would’ve done their homework here. They’ve already got exposure in the country, which would’ve assisted with the due diligence. The leases are also structured as triple net leases, which means there is low variability of expected income – provided that the tenants pay, of course.

But now for the most important part: the acquisition yield. Based on the forecast net profit attributable to the properties, the yield after tax is expected to be 3.3%. You can’t compare this directly to net initial yields on most property acquisitions, which are before tax. I’m not sure why Collins doesn’t disclose net initial yield in line with market practice. I’m also not sure why they don’t indicate the level of debt associated with the deal and whether that is impacting the expected profit after tax.

Collins currently trades on a dividend yield of 8.7%, so this transaction will be dilutive to that yield. Will South African investors give enough credit to offshore exposure? Or does Collins even care? There’s an argument that because the shares are tightly held, the underlying exposure is managed in such a way that mainly suits the anchor shareholders.

Glencore hopes for a better second half in copper (JSE: GLN)

And either way, there’s a self-help strategy around costs

Glencore has released its financials for the six months to June. They had a rough time, with flat revenue and a 14% drop in adjusted EBITDA. There’s once again a net loss that shareholders need to stomach, except this time its gone up from $233 million to $655 million.

Before you panic, the loss isn’t an indication of cash flows. They generated $3.15 billion in funds from operations. Still, that’s 22% lower than the prior year. There are a bunch of other moving parts on the balance sheet, including the receipt of proceeds from the sale of Viterra. If you include those proceeds (received just after period-end on 2 July), then net debt to adjusted EBITDA is at 1x. So, the balance sheet is healthy, hence why Glencore is able to press on with share buybacks while the share price is at depressed levels.

The problems in the first half of the year were mainly thanks to lower coal prices and a drop in copper production. There’s nothing that they can do about the former. In terms of the latter, Glencore is looking ahead to a much better expected copper output in the second half of the year. They are also looking at $1 billion in recurring cost savings (measuring vs. 2024 as a baseline), which they expect to fully deliver by 2026. They plan to be 50% through the savings by the end of 2025.

There’s a lot riding on the second half of the year, with Glencore’s share price down 19% year-to-date.

Jubilee Metals updated the market on its copper business (JSE: JBL)

And with plans to sell everything else, this is the important bit

Jubilee Metals has a few irons in the fire when it comes to copper in Zambia. They have their mine-to-metals business, which is the Sable refinery combined with nearby copper mines. They also have the Roan concentrator, which processes third-party copper feedstock. Finally, they can process surface stockpiles and tailings that they’ve been acquiring.

The Roan concentrator has had a lot of focus recently, with an upgrade that is now fully operational and exceeding targeted monthly production. That’s just as well, as production in the first half of the year was severely impacted by power and infrastructure issues. It was so bad that Roan was placed under care and maintenance!

The open-pit mining is much earlier in the process, with Jubilee undertaking drilling work. As for the tailings, Jubilee is trying to prioritise its capital spending by selling the tailings that it considers non-core. They are also looking to dispose of their chrome and PGM operations in South Africa, with a circular expected to be distributed this week for that deal.

Jubilee only managed to produce 2,211 tonnes of copper units in FY25. Their guidance for FY26 is 5,100 tonnes, so that will be a massive recovery if they can get it right. They have little choice, as they’ve thrown everything behind the Zambian copper strategy. The share price is down 18.6% year-to-date.

A juicy jump in the dividend at Quilter (JSE: QLT)

The increase in earnings is more modest

Quilter has released results for the six months to June 2025. This has been a strong performer on the JSE, with a wealth and asset management business model that enjoys powerful distribution in the UK. The share price is up 23% over 12 months and 10% on a year-to-date basis.

The key metric is net inflows, with the distribution part of the business doing its job. Assets under management and administration (AuMA) enjoyed core net inflows equal to an annualised 8% of the opening value. That’s a very strong driver of earnings that makes the company less reliant on overall market values in the portfolios. AuMA increased by 6% from December 2024 to June 2025.

Profit growth was modest, with adjusted profit before tax up 3% and operating margin increasing by just 100 basis points to 30%. This is because revenue was only up 2%, so they found it harder to drive revenue despite the uptick in assets. A dip in interest revenue was also a contributor here.

This didn’t stop Quilter from pushing the dividend a lot higher, with an increase of 18% to 2.0 pence per share (it’s a UK company).

Sirius Real Estate announces more acquisitions in Germany and the UK (JSE: SRE)

They don’t waste time when it comes to deploying capital

When listed property funds raise capital from the market for general acquisition purposes, the risk to shareholders is that the fund sits on the capital rather than deploying it. This leads to a cash drag effect that hurts returns. With the inclusion of these latest acquisitions, Sirius Real Estate has managed to do €165 million worth of acquisitions in 2025. They are certainly doing their best to avoid the cash drag trap!

The latest deals include a business park in Germany for €23.4 million and one in the UK for £16 million. Both are off-market deals, which means Sirius avoided being part of a bidding war. When you’re a regular acquirer of assets, you get access to the best deals before the general market does. In the area in Germany where the latest property is located, Sirius already has three other properties. This is the value of building relationships through focusing on specific regions. Interestingly, this region in Germany (called Dresden) is attracting investment from semiconductor companies like TSMC, so that has incredible knock-on benefits for the broader area.

As usual with Sirius, there are plans afoot to improve the yield on the properties. The site in Germany currently has one tenant (being the seller of the property) who will vacate after a year. At that stage, Sirius will convert the property to a multi-let business park. The site currently generates a net initial yield of 9.13%.

The property in the UK is already a multi-let park and offers a net initial yield of 9.52%. 36% of tenants are in the defence sector, so that seems like a clever play in Europe at the moment. 67% of tenants have “lease events” within the next two years, which is an opportunity for an uptick in rates on the leases. Although Sirius notes that Bedford is the site for a proposed Universal theme park that would bring benefits to the area, I’m not sure the defence tenants care too much!

Separately, Sirius sold off a small property in the UK for £1.55 million, which is a 7% premium to the most recent book value. Even on small sales, achieving a premium to book is what helps give support to the Sirius valuation.

Nibbles:

Director dealings:

A director of Richemont (JSE: CFR) sold shares worth around R73 million. In a separate announcement, a director sold shares worth nearly R30 million. As the primary listing is in Switzerland, famous for helping rich people keep things a secret, we don’t know which directors sold shares.

Absolutely zero marks to Raubex (JSE: RBX) for the disclosure around directors and execs selling shares from the long-term incentive scheme. No effort is made to indicate the taxable vs. non-taxable portions. On sales of over R17 million, that’s a frustrating lack of useful information for shareholders.

The director of Santova (JSE: SNV) who has recently been selling shares is at it again, offloading shares worth R4.1 million.

The CEO of Vunani (JSE: VUN) is picking up whatever shares he can get his hands on in the market, with the latest purchase being for R2.7k.

Spear REIT (JSE: SEA) announced the acquisition of Berg Business Park in Paarl back in May. The company has confirmed that the deal has now met all conditions and that transfer is expected to take place in October.

The latest acceptance level for the Primary Health Properties (JSE: PHP) offer to Assura (JSE: AHR) shareholders shows that holders of 3.13% of shares have accepted the offer. The closing date is 12 August.

The mess that is aReit (JSE: APO) continues. The latest issue is that the auditors have resigned because they don’t have access to the resources required for timeous release of financials. Specifically, aReit is stuck because they can’t get outstanding financial information from third parties associated with their tenants. The company is suspended from trading. It turns out that I wasn’t wrong about the bright red flag of the company releasing its initial listing docs without even having a finalised website.

Nedbank Group is one of South Africa’s four largest banks, with Nedbank Limited as their principal banking subsidiary.

They offer a wide range of wholesale and retail banking services, as well as other financial products, through their frontline clusters: Nedbank Corporate and Investment Banking, Nedbank Retail and Business Banking, Nedbank Wealth and Nedbank Africa Regions.

Despite delistings, the JSE itself is growing earnings (JSE: JSE)

The loss of small caps with low liquidity isn’t making much of a dent

It’s always fun for market newbies to learn that the JSE itself is a listed company. In fact, it’s listed on its own product! Hence, JSE: JSE is a share code.

One might logically assume that with more delistings than IPOs, the numbers are under pressure. This would be an incorrect assumption. For the six months to June, revenue was up 11.8% and earnings before interest and tax (EBIT) jumped by 15.4%. This is despite personnel expenses climbing by 13.2%, which is a higher growth rate than revenue. Luckily, there are a lot of other overheads in the company and they grew at a far more palatable rate, hence the margin expansion.

Net finance income is very important at the JSE, as they sit on a huge amount of capital for regulatory purposes (ring-fenced and non-distributable cash and bonds of R1.31 billion). Although there was a 4.3% dip in that net finance income, net profit after tax came in 13.2% higher and HEPS was up 13.4%.

I think this table is pretty interesting, as it shows that the market is in a healthy space thanks to e.g. a 28% increase in the JSE’s cut on equity trading activity:

The share price is up 11.6% year-to-date and 27% over the past 12 months.

Not much growth at Nedbank to get excited about, with stubbornly low economic activity (JSE: NED)

But at least the direction of travel is up

Nedbank is a very handy way to take a view on the SA economy as a whole. They are playing a defensive game vs. the likes of Capitec, so their fortunes are tied mainly to the macro factors rather than any specific business decisions. And with less exposure to non-SA markets than other large peers, the macro influences on Nedbank are primarily South African. With plans at Nedbank to sell the stake in Ecobank, the relative exposure to South Africa will increase even more.

Thus, when South Africa has been devoid of much in the way of growth, it negatively affects Nedbank. For the six months to June, revenue was up just 4%. The 6% jump in HEPS (and the interim dividend) was mainly driven by a substantial improvement in the credit loss ratio from 104 basis points to 81 basis points. That’s unfortunately not a sustainable source of margin improvement, as the ratio is unlikely to improve further from the current level.

The thing to be most worried about, in my view, is the 9% increase in operating expenses. That’s way ahead of revenue growth and it shows the extent of the role played by the credit loss ratio in saving these numbers.

Of course, the group numbers are a roll-up of many underlying strategic decisions around where to focus. Banks actively manage their balance sheet exposures, with Nedbank having tilted towards home loans, vehicle finance and deposits. That may all sound obvious to you, but note the lack of e.g. commercial property in that list. Banks have a long list of products that they offer, so focusing on just a few makes a difference.

The thing that would help them most is growth in net interest income. With interest rates slowly coming down and putting pressure on net interest margin, this is only going to happen if demand for credit picks up. This is the SA macro story that I spoke about. Non-interest revenue growth did help in this period, contributing to a modest improvement in return on equity from 15.0% to 15.2%.

Overall, it’s an unexciting story that is at least positive overall. The market didn’t like it, with the share price closing 5.5% lower. This takes the year-to-date move to a rather ugly -16.6%. It’s hard not to compare this to Capitec, up 11% over the same period.

Positive momentum at Pick n Pay (JSE: PIK)

Franchise stores are still lagging corporate-owned stores

Pick n Pay has released a trading update for the 17 weeks to 29 June 2025. There are a number of encouraging signs in it.

I’ll start with the absolute highlight: the Clothing business. In standalone stores, they grew sales by an outrageous 12.5% on a like-for-like basis and 17.3% overall. There’s a soft base effect here and the timing of the onset of winter does make a significant difference in the clothing sector, but that’s still a great number. You can expect more modest growth as it normalises over the rest of the year.

I’ll just give a passing mention to Boxer, which is separately listed (JSE: BOX). Pick n Pay obviously benefits from Boxer’s performance, as they still have a controlling stake in that group. As we already know from the recent Boxer update, turnover was up 12.1% and like-for-like sales increased 3.9%.

From a Pick n Pay perspective though, the major focus in the market is on Pick n Pay Supermarkets themselves. Company-owned supermarkets have been outperforming franchise supermarkets recently and that trend has continued. It really is peculiar, as franchise stores usually do better due to being owner-managed. But at Pick n Pay, company-owned supermarkets grew 3.1% in H1’25, 3.6% in H2;25 and now 4.0% in the latest 17-week update, with clear positive momentum. Franchise-owned supermarkets are much scrappier, with moves of -1.4%, 1.1% and 0.2% for those three periods respectively.

Here’s another interesting point: Pick n Pay’s like-for-like sales growth came in at 3.6%, but turnover growth as reported was up just 0.1% if you include Rest of Africa, or flat at 0.0% if you exclude it. In other words, store closures are perfectly offsetting like-for-like sales, leading to flat total sales for the group. This is why retailers are usually hesitant to close stores, as it leads to a loss of market share. But sometimes, it’s the right choice for the group in terms of building a stronger and more profitable business.

Another point worth noting is that Grant Pattison (ex-Massmart and Edcon) will be joining the board. He certainly knows his way around a retail turnaround story, so that’s a useful addition I think.

The Pick n Pay share price was down roughly 10% year-to-date coming into this update. The market liked it though, so perhaps it will stage a recovery. A 2.2% positive move by close of play is a good start to clawing its way back.

Shoprite is achieving growth that feels almost impossible (JSE: SHP)

South Africa’s best retail story is still cooking – but watch that momentum

Shoprite has released a trading statement for the 52 weeks to 29 June 2025 and the numbers are astonishing. HEPS from total operations is expected to be between 15.2% to 25.2% higher. From continuing operations, they expect HEPS growth of 9.4% to 19.4%. To be pulling off those growth rates in this economy for a business the size of Shoprite is truly excellent.

Sale of merchandise in continuing operations was up 8.9%. Supermarkets RSA leads the way with 9.5% growth, while Supermarkets non-RSA was up 6.4% and other operating segments only grew 5.2%.

I must point out a concern around momentum here. Although overall sales are strong, they grew 8.1% in the second half of the year vs. 9.7% in the first half. In Supermarkets RSA, by far the most important segment, growth slowed from 10.4% in the first half to 8.5% in the second half. This is despite selling price inflation increasing from 1.9% to 2.7% in the second half, suggesting a significant slowdown in volumes growth. This is worth keeping an eye on.

Some of the selling price inflation is probably just the mix effect across the different stores, as Checkers and Checkers Hyper grew by 13.8% for the full period, while Shoprite and Usave were up 5.9%. One would realistically expect to see higher price inflation at Checkers and Checkers Hyper where there’s a wider assortment and customers are less sensitive to price than at Shoprite and especially Usave, so this could be impacting the inflation number.

The group continues to expand its footprint, opening 194 “main banner” supermarkets and 79 stores across their other formats, with Petshop Science as the fastest growing with 60 new stores. Little Me opened just 1 more store to get to 11 stores vs. Petshop Science at 144 stores. If ever you needed proof of the birth rate vs. pet ownership trends at the moment, there’s your answer. For most people, their “little me” these days is fluffy.

In case you’re wondering about the discontinued operations, these mainly relate to the furniture business that is being sold to Pepkor. Despite the Competition Commission initially being fine with the deal, the Competition Tribunal allowed Lewis to intervene in the process. This has now delayed the process while the Tribunal considers the applications. Shoprite believes that the deal is highly likely to close, but the timing is uncertain. Other discontinued operations include the businesses in Malawi and Ghana, as well as furniture in Mozambique and Angola.

If ever there was a chart that demonstrates that investment returns are a function of what you pay for the stock and how the company is performing, it’s this one of Shoprite vs. Pick n Pay over the past 12 months:

Before you question your sanity, here’s the five-year view:

And yes, eagled-eyed readers who noticed that the share prices are slightly different in the two charts, the price moved as the market was live while I was flicking between 5 years and 1 year! The joy of liquid stocks – the price never sits still.

Shoprite closed 0.5% lower on the day of results, showing just how much good news is already baked into the price.

The market expected more from Telkom (JSE: TKG)

Despite growing earnings, the share price fell more than 9%

It’s quite incredible that we’ve reached a point in Telkom’s journey where the market has high expectations of them. Imagine telling someone this just a few years ago, when Telkom was desperately trying to offset its dying legacy business?

Even after a 9% drop on Tuesday, the share price is up 129% in the past 12 months. It makes for quite a chart:

Now, the drop could be due to profit taking by a couple of major players, which isn’t uncommon after such a large run in the price. But it could also be because revenue for the first quarter ended June 2025 was up 1.1% and EBITDA grew by 6.5%, which is helpful as protection against inflation, but certainly not exciting. It’s a lot less thrilling than what we’ve seen from MTN’s African subsidiaries in the past week or so, with the market expecting a strong announcement from MTN regarding group results.

In fact, adding in MTN and Vodacom on the above chart shows that Telkom has now dipped below MTN on a year-to-date basis, although all three have been lucrative:

The negative story in the Telkom numbers is clearly BCX, with a revenue decline of 8.3%. They are working on a “faster” turnaround in this business, so the market will watch that closely.

Elsewhere, key revenue drivers were up, like mobile data revenue up 9.6% and Openserve fibre data revenue up 11.3%. Another useful statistic is that homes passed by Openserve increased by 12.6% and homes connected were up 17.5%, so that speaks to successful conversion of potential customers. Data revenue is now almost 60% of group revenue!

Group EBITDA margin improved by 140 basis points to 25.9%. On such modest overall revenue growth, that’s encouraging. BCX is the bright red pimple here, with EBITDA margin down 150 basis points to just 6.5%.

In terms of the balance sheet, the Swiftnet disposal proceeds allowed them to settle R4.75 billion in debt. They paid a R500 million special dividend in July and retained the rest of the R6.6 billion proceeds for general corporate purposes. They also received R158 million from property sales, with a further R121 million from property sales expected to be received over the course of the year.

Overall, it’s a decent set of numbers for Telkom. It’s just less than the market was expecting, as there’s now too much exuberance in the telcos sector. I never thought the day would come where I could write that!

Nibbles:

Director dealings:

Adding to the extensive recent purchases by directors and senior execs of Primary Health Properties (JSE: PHP), the CEO bought shares worth R1.8 million.

The buying of Vunani (JSE: VUN) shares by directors continues, but low liquidity in the market remains a struggle. The CEO bought shares worth R3k in an on-market trade. Another director bought shares worth R4.6k in an off-market trade.

The board of MAS Real Estate (JSE: MSP) has noted the bid by Prime Kapital. The independent board will comment on the terms and risks “as soon as it is practicable” – while highlighting that the Prime Kapital offer also has an unusual offer timeline. They aren’t wrong about that, as the offer closes before the extraordinary general meeting that is scheduled for later this month.

Although the market’s focus has been on the impact on FirstRand (JSE: FSR) of the ruling in the UK regarding the vehicle finance sector, there’s also relevance to shareholders in Investec (JSE: INP | JSE: INL). Investec has noted that whilst the judgement is a welcome step towards clarity, there is still uncertainty around their provision. Investec is carrying a provision of £30 million, with the UK Financial Conduct Authority expected to publish a consultation on an industry-wide redress scheme by October 2025.

Novus (JSE: NVS) is buying up shares in Mustek (JSE: MST) while the process around the mandatory offer continues. The latest example is an on-market purchase for R290k, taking the Novus stake up from 39.92% to 39.95%. Together with concert parties, the move is from 60.20% to 60.24%.

If you’re interested in Orion Minerals (JSE: ORN), you could check out the presentation that they just released to the market that gives a helpful overview of their story. You’ll find it here. I would also highly recommend watching the recording of their recent Unlock the Stock appearance, which you’ll find here.

Glencore (JSE: GLN) shareholders gave strong approval to the plan for off-market share buybacks. Glencore’s share price has been under pressure and the company wants to use this point in the cycle to achieve meaningful buybacks. The theory is that this benefits the shareholders who decide to stick around.

Regular readers may have seen the recent note in Nibbles (and certainly across local media) regarding the censure imposed by the Johannesburg Stock Exchange (JSE) on Anushka Bogdanov concerning academic qualifications she allegedly claimed while serving on the board of EOH (now iOCO). In response, her office issued the following statement: “I am aware of the SENS announcement published by the Johannesburg Stock Exchange (JSE) on 25 July 2025 referencing my academic qualifications. The announcement contains several factual inaccuracies and misrepresentations. I have submitted all relevant documentation from accredited institutions, including doctoral research, to the JSE in good faith and in full transparency, and I remain committed to engaging constructively to clarify and resolve the matter.” In my view, there are only three possible interpretations of “inaccuracies” in this context. Either Bogdanov did not claim the qualification in the manner described by the JSE, or she did claim it and does have it, or there is some other technical issue with the JSE process and announcement. I’ve posed these points to her office and am awaiting clarification. I guess time will tell.

China offers an exciting emerging markets opportunity, driven by the country’s vast manufacturing base and the progress made in areas like artificial technology. But geopolitical risks and the volatility that plagues emerging markets is also present, making it more difficult for investors to add exposure to this market.

With the launch of two new structured products that reference the Shanghai Shenzhen CSI 300 index, Investec has sculpted two payoff profiles that could appeal to investors of varying risk tolerances. With a combination of mechanisms that create capital protection and enhanced upside under certain outcomes, these products aim to take advantage of the opportunity in China, while reducing the overall risks.

Brian McMillan and James Cook of Investec joined me to talk through not just the appeal of China, but also the way in which the two products work. There’s a wealth of information in this discussion on the Investec ZAR CSI 300 Digital Plus and the Investec USD CSI 300 Geared Growth products.

Applications close on 13 August, so you must move quickly if you are interested in investing. As always, it is recommended that you discuss any such investment with your financial advisor.

You can find all the information you need on the Investec website at this link.

The Finance Ghost: Welcome to the Ghost Stories podcast. I’m really looking forward to digging into the latest structured product offerings from the team at Investec. We have Brian McMillan joining us today – the voice that you will certainly recognise if you’ve been listening to a lot of these podcasts from the team at Investec. And we have a new face and a new name and therefore a new voice on the show as well, and that is James Cook. James, Brian, thank you for joining me on the show. I’m really looking forward to talking about, actually, two different product launches and unusually with two different payoff profiles. So looking forward to getting into the details of that – but both of which at the end of the day point to China, so I’m excited to also understand more about the Chinese investment thesis.

Let me say hello to the two of you first, Brian, James, welcome to the show.

Brian McMillan: Thanks very much. Ghost.

James Cook: Thank you.

The Finance Ghost: So let’s start with just understanding the relevance of China, I think, to any kind of global markets discussion. And this has been a particularly interesting year, right? A lot of people are looking for opportunities beyond the US and that’s a bigger debate around whether or not you can find good stuff in Europe, etc. But certainly people are looking at emerging markets. They’re asking all kinds of questions. And what’s happening out there is this rift. It’s just getting wider and wider between East and West. At least that seems to be what’s going on out there. And there’s certainly a school of thought that perhaps this will force China to actually focus more on domestic consumption, growth in technology, developing their own AI, for example, their own supply chains, the whole story.

Is that one of the reasons why maybe investors should be paying attention to what’s going on in China. And then what are some of the other factors that you think make China interesting at the moment? Because I think the important context here for listeners is that Investec chooses where to do these new structured products based on markets that you think are interesting at a point in time. So, the fact that the new products are referencing China, is actually interesting in and of itself.

Brian McMillan: Yeah. Ghost, that’s something that we do take into account. We go out into the market, we speak to our clients when we’re putting a new product out, but we’re also receiving information back from them, from our clients and where their interest is.

And I think over the last few years, one of the interesting things about structured products is that it really allows you to enter into these new types of markets with a bit of confidence because you’ve got that capital protection. You can take on a new theme. As you mentioned, we’ve got two – one is in rand and one’s in dollars. We give you multiple ways to get access to this market. But it’s also nice to try new and different indices when you’ve got that capital protection.

Not a lot of people have direct access to China in their portfolios. Obviously there’s some through the JSE, through Naspers and Prosus, but for the Greater China Index, which we’re doing, it makes sense to try and capture some exposure to what is essentially the second largest economy in the world. And this allows us to do that. I’ll let James explain some of the reasoning, why specifically at this time we went for China.

James Cook: Yeah, sure. China’s been in the news a lot recently, specifically around tariffs and trade negotiations. And I think if we go back to when Trump first came into term, it really highlighted the importance for China to start diversifying their trade relationships, to start really focusing on internal consumption, as you mentioned, and highlighting the importance of becoming independent from a technology point of view.

We’ve seen from a trade relationships point of view, decreasing exposure to exports to the US, increasing it to other countries. There’s been quite a lot of change from that point of view. In terms of the internal consumers, you have a very large economy, you’ve got 1.4 billion people. And unfortunately, there’s just a consumer sentiment issue at the moment where there’s just this depression that’s happening.

I think that the government is very aware of this and focusing quite heavily on creating policies and government stimulus to try and rectify that situation to get people to start spending again. And we are starting to see that coming through. As an example, if you go back to September 2024, there was a stimulus package that was released. The results of that was met quite favourably by the market. We saw a 32% increase in the CSI 300 Index over a two-week period. I guess at the moment things are just very in the air, we don’t really know what’s going to happen in terms of negotiations with the US. The sentiment seems to be that they’re kind of holding back, seeing how things evolve and they will then decide how much more to go in on that front.

Then lastly, just on the technology front, I think the fact that there are these restrictions around technology exports is forcing China to innovate and invest heavily into these – AI, renewable energy, the energy to promote or to allow for AI to develop. And I think that drives innovation and hopefully we’ll see that coming through.

Brian McMillan: It’s interesting that there are two centres of AI knowledge building up in the world. The US obviously leads the way, but China has obviously taken the view that they need to go it alone. The launch of Deep Seek on Trump’s inauguration date, I think that was timed. And they’re obviously drawing in a lot of knowledge workers into China, like America is. And I think there’s going to be two clear winners in terms of AI throughout the world and that’s going to be the US and China. So to get exposure to that market through a structured product is a good way to do so.

The Finance Ghost: Yeah. And it’s not actually easy to do through buying Western companies. So you referenced Naspers / Prosus there and then obviously the look-through is Tencent. But another great example we saw with Nvidia this year, they had a bit of a wobbly in their earnings because they were actually blocked from selling a specific product into China. And people almost forget that Nvidia is actually an American company. It’s easy to just get confused and bundle the stuff together as being “somewhat Taiwan related” – but Nvidia is as American as anything and that means you’re not necessarily getting that uptick of what’s happening in China if you own a company like Nvidia. It is quite interesting, it’s quite difficult to be able to get some of this direct exposure.

You’ve referenced the index there already, but it’s the Shanghai Shenzhen CSI300 index, not necessarily one that will roll off the tongue for most people or that they might have heard of before. I think before we maybe talk about relative valuation, let’s just quickly touch on: this index seems to track a basket of companies across two different exchanges. Is that correct?

James Cook: Yes, that’s correct. It’s the Shanghai Stock Exchange and the Shenzhen Stock Exchange and It’s the top 300 companies based on market cap and liquidity from those two exchanges.

The Finance Ghost: Yeah, so this is not some look through…

Brian McMillan: No, yeah, yeah, it’s very much China focused. So obviously a lot of the internet and tech stocks are listed on the Hong Kong exchange. This particular index is really looking at China as – manufacturing base, finance base, banking, consumer discretionary – and really focusing on the economy of China rather than the internet stocks of China.

The Finance Ghost: That’s a really important nuance. Thank you for confirming that. And I guess that explains as well why from a valuation perspective it looks quite appealing at the moment, because that would include a lot of sectors that have somewhat been left behind by the big boom in technology and where market sentiment has been. Of course, any investment return is a function of not just what you buy, but also how much you paid for it.

We look at a market like India, which of course is the other gigantic emerging market that everyone talks about. That market has been red hot, basically. Investors have been loving the combination of the more services driven economy rather than manufacturing, the world’s biggest democracy, essentially. People love that as well. So, from a China perspective, and particularly this index, which then references life on the ground in China, essentially, what are the catalysts for a potential valuation uplift there? Or do you think it’s a case that there’s enough growth in the underlying companies to drive the returns here, even if you don’t see much of a structural improvement in valuations?

James Cook: Sure. Well, maybe just to touch on what that valuation looks like, you have the CSI 300, which is the index that we are referencing. Since its high in February 2021, it’s now down 31% from that point. Whereas if you compare that to other major indices around the world, they’ve gone up quite significantly over that same period. That’s been driven by factors like quite hectic lockdowns around Covid, supply chain disruptions, initial trade disruptions in terms of the negotiations with Trump in his first term, there were factors like that property market was quite a big catalyst for that downturn as well. That’s resulted in a lot of negative sentiment that has been priced into the market. And you see this through the price/earnings ratio being 13.8x compared to America, or the S&P 500, at 23.5x. So it’s significantly – not undervalued, but looks like a relatively attractive valuation from that point of view. On that basis it seems to be a fairly decent point to get into the market.

If we see things as we discussed earlier, like a boost in internal consumption and the results of the innovation investment and technology coming through, which would boost earnings and result in an increase in the index, those kind of things could start seeing the index rise.

The Finance Ghost: Yes, there are a few levers to pull here. And the nice thing, it’s almost the “every dog has its day” trade. But of course, when you’re doing it as a structured product and you’ve got some capital downside protection, those trades become a lot more interesting, particularly when you’re going into indices that have maybe had a bit of a tough time. It’s not clear that they’re ready to actually start firing and it’s nice to have some protection in case they don’t. But obviously we’ll get into some of those specifics when we talk to the payoff profile.

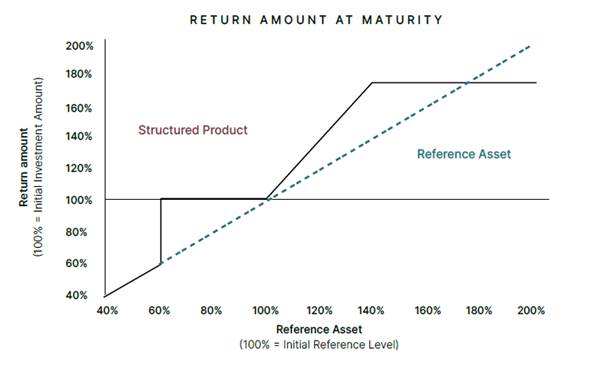

Before we get there, I said at the beginning of the podcast that you’ve got two different structured products on offer. This time around, both of them are tracking that index, the Shanghai Shenzhen CSI300. One is in ZAR, one is in US dollars. Now I was kind of expecting that that’s where the differences would end, but definitely not this time around. The payoff profiles are actually very different and we’ll get into those payoff profiles shortly. But I guess just to set the scene, why two such different payoff profiles this time around? It’s not just a currency difference.

Brian McMillan: Yeah, so as you say, it’s not just the currency difference. We often offer a rand listed one which goes on the JSE and then our offshore ones which we have Dublin listings for. As I mentioned earlier, we speak to a lot of clients, we get a lot of feedback and there is a base of client out there that is very conservative. They want exposure to certain markets but they want the full hundred capital protection. They don’t want to risk downside. In this particular case, when we priced it up in rands, we could get a decent return on a rand basis with capital protection. When we went offshore into the US, the pricing is not as attractive and so that’s why we have a downside barrier. So it’s not 100% capital protected in all cases. It does mean that if the index is down more than 40% in three and a half years that you do have capital at risk, but at the same time, we’re offering more upside.

There are two views in the market. One wants to be very conservative and then other people want the exposure to China and are willing to take gearing on it. So that’s why we have two different kinds of products in two different kinds of currencies.

The Finance Ghost: Yeah, it’s interesting. This is the magic of being able to do some financial structuring, right? As you can basically carve out these payoff profiles to match what clients are asking for.

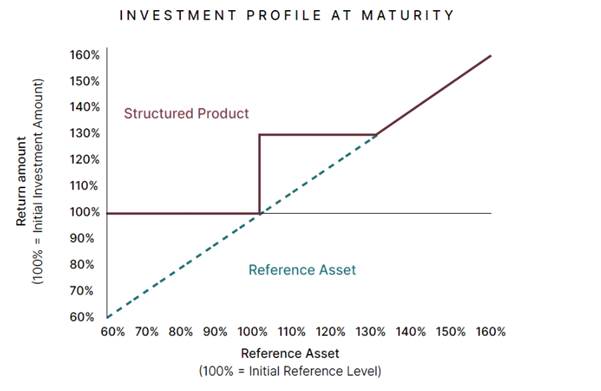

I think let’s dig into that because that’s where it gets very interesting. And to anyone listening to this who maybe doesn’t have the transcript in front of them, if you’d like to see a chart of what these payoff profiles look like, I’ll include that in the show notes. And obviously you can find that on the Investec website as well, just in case the payoff profile is not the easiest thing to follow as you’re listening to it, because it is a little bit complicated. But let’s start with the rand note, which is the Investec ZAR CSI 300 Digital Plus. And those who have gained some familiarity here with Investec’s structured products will probably be happy to see that this is where the capital protection is when the asset closes below 100% of its starting value at maturity, which is three and a half years later. I was mildly horrified when I read the brochure to see that three and a half years is in 2029. That was a slight shock. I saw 2029 and thought, wow, that’s far away, and then realized it is in fact three and a half years away! But that’s where we are.

And so this is the one that’s got all of the downside protection. This is the one that therefore probably has less upside. I’ll let you speak to that now. I’m also curious to exactly what a digital return is – does that just mean that you’re not delivering the money yourself, Brian, James, to someone at the end of the three and a half years? They’re getting it in a bank account.

James Cook: The term “digital” comes from coding, where it’s either a yes or no, it’s a 0 or 1. So in this case, what it means is that how the payoff profile works is that at maturity, if the index level is either the same or higher than it was when we started, then the condition is met and you’re going to jump straight up to a digital return. In this case it’s 30%, but if it ends below where it was, then you don’t get your 30%.

The payoff profile for this one says if markets drop, you get your money back because it has 100% capital protection. If it’s flat or positive, you’ll get 30% and that 30% is equivalent to 7.8% in rand compounded each year. If the market does more than 30%, then you also get the upside. So it’s almost like you’re keeping your options open. If the market really does recover, then you have unlimited upside potential, if it does more than 30.

Source: Investec brochure

The Finance Ghost: Okay, fantastic. So that is something that I’ve learned today, is the concept of a digital return. I didn’t think it was a toggle between the carrier pigeons and an EFT, but it’s good to understand that it’s basically binary, it’s 1 or 0. That’s essentially what it is. In this case it’s just 30% or nil for any close between 100 and 130, right? And then above that you’ve got your upside. So actually, you’re not giving away much upside at all for this downside protection, are you?

James Cook: The product is designed more on the conservative side because you have 100% capital protection. And it also does fairly well if markets just move sideways. But what’s really nice is that, that you’re not introducing a cap, so you’re keeping your options open. And given the fact that the market seems to present a fairly decent entry point, if any of the things that we discussed earlier play out, it could be quite a nice upside potential.

The Finance Ghost: Yeah. The big difference here is that what you’re not getting is a geared return, right? As you say, if the markets kind of go sideways, you do quite well. If they go above 30%, you probably get what you essentially would have gotten otherwise. But you’re not getting a geared, accelerated, supercharged upside that you’re getting in some of the products, one of which will be that USD product which we’ll get to soon.

I think let’s just finish off on the ZAR product while we can. This is a flexible investment note that is listed on the JSE as I understand it. I think let’s just touch on the advantages of that and the liquidity. And then also does that mean that this note, because it’s ZAR-denominated, it’s listed here, does this not count then towards the offshore investment allowance that everyone gets annually?

Brian McMillan: As you mentioned, the rand note will be listed on the JSE. The advantage of us listing it on the JSE is it will be inward listed, so investors can invest in it without using any of their offshore allowance because essentially it’s inward listed. So they have full access to it, investors don’t have to use their allowance.

And it’s a little bit different from what we were doing two years ago in that we call this a flexible investment note. Now what we’ve done is that we’ve listed a note for 20 years. We list this note for the next 20 years and what we then do is we place this particular structured product in it. So this is called investment profile number one of this 20-year note. It will last three and a half years. Hopefully the index is up, you get a 30% return, let’s say you get the digital return and at that point you will be able to as an investor roll this forward without getting paid out.

So what used to happen is would pay everybody out their 30% return plus their capital and then we would say we have a new product, would you like to invest in that? Everyone would give us back their R130 and they would start a new one. With this one, it allows us to roll it forward, which has some benefits because obviously it’s a bit quicker as well. So we’re not paying everybody out then a week later asking them for the money back, we’re just going to roll it forward. And then of course their capital protection – and let’s say we did a product over the EURO STOXX that had a digital of 40%, it can change index, it can change currency, it can change a whole lot of different features, but your capital protection is now on 130. You’re able to roll up that capital protection as you go along over time, which has some benefits down the line because you’re constantly stepping up and locking in as your investment goes along. And we’ve seen that in a number of – one of the disadvantages of things like an ETF is client will invest in it, they’ve been in it for five, 10 years, they’ve had good returns, they don’t want to divest from it because you have a tax event at that point. But of course you have the full downside. Whereas every time you lock into one of these on our products, within the flexible investment note, you’re locking in all the gains that you’ve made and that should have some benefits over the 20-year period.

The Finance Ghost: Yeah, that sounds very clever. It’s basically for those looking and saying, well, we want this interesting offshore exposure, we’re quite happy to lock up a sum of money for a period of time and then let it roll, let it compound, see what Investec brings to the table each time.

And I guess if they want to, at the point of rolling, they can cash out, right? From a liquidity perspective, I know liquidity along the way maybe comes with some limitations and I think let’s just deal with that quickly. But there is a liquidity event if they want at the end of the three and a half years, right?

Brian McMillan: Yes, absolutely. They can exit at that point and that’s frictionless. There’s no fees or anything at that point, no brokerage. But they can also at any time – because we list this on the exchange, we actually provide a market on a daily basis.

So let’s say the index does go up and let’s say it goes up on day one by 10% and stays 10% up over the next three and a half years. Our product will actually grow over those three and a half years up to that 30% digital return. But if you were two years into the product and you wanted to exit, you needed the money, you can at any time by just selling that note on the exchange. We will make a daily market in that and it’ll reflect the price of that structured product at that point in time.

The Finance Ghost: Yup, so there’d be a spread on that obviously which people should take into account. But at least there is some liquidity along the way, just in case. But I think what’s always come through in everything you’ve ever put out to the market really is for people to understand – treat this as a three-and-a-half year thing at least. Don’t even think about putting money in there that you’re going to need in less time than that. Then you are not understanding the product. And again this is where working through an advisor is very important. But for advisors listening to this, also make sure that you realise that this is at least a three-and-a-half-year commitment.

I think let’s move on then, with the liquidity out the way. We’ve done the ZAR note, let’s talk about the USD one. And again, it’s not just the currency that’s different here, it’s a lot of things that are different. The payoff profile is particularly interesting. James, I’m excited to hear how you plan to describe this particular shape. It looks like a nice art project and I’ll make sure that it’s in the show notes.