Morocco’s ORA Technologies has closed a US$7,5 million Series A funding round led by Azur Innovation, who were joined by three local investors. The ORA app offers multiple features, including P2P transactions, an e-commerce platform, on-demand services, chat functionality, social networking, and a digital wallet to be launched soon.

Sahel Capital through its Social Enterprise Fund for Agriculture in Africa (SEFAA) has provided Kenyan fish processing and distribution company, Camino Ruiz, with a US$1 million loan facility comprising US$800,000 for capital expenditure and US$200,000 for working capital. Camino Ruiz has established itself as Kenya’s first consumer-focused fish brand through a strategic partnership with Global Tilapia Husbandry (GTH), securing a reliable supply of high-quality Tilapia. The company processes this into a range of value-added products under its flagship brand, Global Tilapia.

Vicenne, a medical equipment and healthcare services firm backed by private equity firm Amethis, listed on the Casablanca Stock Exchange on 15 July following an initial public offering which was 64 times oversubscribed. The company offered 2,1 million new shares at MAD236 each.

Egyptian fintech, Palm, has announced an undisclosed seven-figure pre-seed funding round led by 4DX Ventures and included Plus VC and a number of international angel investors. Palm enables users to save for life goals using smart nudges, embedded finance, and curated investments across fixed income, equities, and precious metals. It also offers exclusive merchant deals to boost savings value and reduce spending.

Verdant Capital Hybrid Fund has provided Bfree with a US$3 million loan for distressed loan portfolios from inclusive financial institutions in Africa. Established in 2020, Bfree is an ethical and digital credit collection company.

Corporate governance in South Africa has evolved significantly over the past three decades, with the King Code playing a central role in shaping responsible and sustainable business practices. In an era where environmental, social and governance (ESG) and business and human rights (BHR) considerations are no longer optional, but fundamental to corporate success, the release on 24 February 2025 of the draft King V Code on Corporate Governance by the Institute of Directors in South Africa (IoDSA) for public comment marks a pivotal moment.

This article briefly examines some of the key changes proposed in King V, particularly from an ESG and BHR perspective. It also acknowledges that the King Codes have, over the years, come under scrutiny, including the current draft, with concerns raised around their utility and effectiveness.

King V refines corporate governance by incorporating modern sustainability principles, streamlining its structure, and making governance guidance more accessible. Most notably, the inclusion of key terms such as “impact,” “impact materiality,” “Ubuntu,” and the updated definitions of “sustainability” and “value creation” signal a shift towards embedding ESG and BHR considerations into South Africa’s corporate governance framework.

The emphasis on impact and impact materiality reflects a move towards requiring businesses to assess not only how external factors affect their financial performance, but also how their operations affect society and the environment. The explicit recognition of Ubuntu — a philosophy centred on interconnectedness and human-centric values, including ethical responsibility — introduces a uniquely South African dimension to governance, reinforcing stakeholder accountability and social cohesion as core business principles.

Meanwhile, the refined definitions of sustainability and value creation underscore that corporate success is no longer measured solely in financial terms, but also in broader contributions to social, environmental and economic well-being.

These updates bring King V in closer alignment with global governance trends, while ensuring South African businesses prioritise human rights, ethical leadership and long-term sustainability as part of strategic decision-making. This evolution marks a departure from traditional compliance-based governance, placing ESG and BHR firmly at the heart of corporate responsibility and value creation.

King V’s evolution: A streamlined and impact-focused governance framework

Since its inception, the King Code has shaped South African corporate governance through progressive updates that reflect global trends, while remaining tailored to the country’s constitutional values and socio-economic context. A defining feature of King IV (2016) was its introduction of the “apply and explain” principle, requiring companies to demonstrate how they apply governance principles rather than merely confirming compliance. How this principle will be interpreted and whether substantive explanations will be required remains to be seen.

King V builds on this principle with several refinements: Simplified structure – the number of principles has been reduced from 17 to 12, enhancing clarity and ease of application.

Enhanced accessibility – the Code is now presented as a single, stand-alone document, reducing the need for extensive cross-referencing.

Greater emphasis on transparency – the Code encourages proportionality and adaptability to ensure governance practices align with an organisation’s size, structure and complexity.

The inclusion of a formal glossary in King V underscores its commitment to clarity, transparency and accountability, particularly regarding ESG and BHR considerations.

The executive summary of fundamental concepts published with the draft King V Code notes: “King V advocates integrated thinking which takes account of the combination, connectivity, and interdependencies between the range of factors that affect an organisation’s ability to create value over time. The necessity for integrated thinking is apparent when one acknowledges that all organisations function as integral and embedded components of the economy and society in which they exist. In turn, organisations and the economy, as well as other social systems, are integrated and embedded parts of the natural environment upon which these entirely depend. As a consequence of this integration or embeddedness, organisations affect and are affected by the health of society and the planet”.

It further states: “Integrated thinking operates as a thematic strand across the diverse domains or subject matter of governance that the Code encompasses: ethics and corporate citizenship, strategy and performance, reporting, governing body composition, governing body committees, delegation, risk and compliance, information and technology, remuneration, assurance, and stakeholder relationships. Where principles and practice recommendations in the Code refer to the economic, social, and environmental context within which the organisation operates or, from a more granular perspective, to the relationships and resources that organisations utilise and influence, these denote integration.”

What this means for businesses

King V aligns with the global shift towards recognising that companies can no longer focus solely on shareholder value. They must assess, disclose and manage their broader societal and environmental impacts. Sustainability is no longer a “nice-to-have” — it is a governance imperative.

Businesses must integrate sustainability into strategy, risk management and operations, rather than treating it as a separate compliance function. The inclusion of Ubuntu localises corporate governance within South Africa’s cultural and ethical framework. Companies are encouraged to adopt stakeholder-centred decision-making, reinforcing values such as community, respect and ethical leadership.

Value creation must now be holistic, considering financial, social and environmental returns. Organisations must define and measure success not only by profits, but by their positive contribution to society and the planet.

That said, the balancing act between profitability and operationalising ESG and BHR should not be underestimated. Business is a key driver of economic growth, and regulatory changes must not result in undue bureaucratic burdens. How these proposed changes will be implemented remains to be seen. It will also be important to monitor how the business sector responds and how ESG and BHR considerations are practically embedded in governance.

Why King V matters for South African business

The draft King V Code represents a potentially transformative step in South Africa’s corporate governance journey, though not without criticism, including claims that the Code serves as a political placeholder to signal compliance without necessarily driving change. By refining governance principles, emphasising impact-focused strategies, and embedding sustainability and ethical responsibility into its framework, King V aims to ensure that South African businesses remain globally competitive and accountable to their local communities and stakeholders – futureproofing their operations as a result. King V attempts to bridge the gap between traditional governance and modern ESG and BHR expectations, helping South African businesses become more resilient, responsible and relevant. As King V remains open for public comment, organisations should actively engage with the draft Code to ensure the final version reflects international best practice, the unique governance needs of South Africa, and importantly, is practical and implementable.

The King Code had long set the benchmark for corporate governance in South Africa. With King V, the country has an opportunity to lead globally by balancing financial success with ethical, social and environmental responsibility.

Businesses that embrace this evolution will not only future-proof their operations, but also build stronger stakeholder relationships and drive long-term, sustainable value.

Merlita Kennedy and Pooja Dela are Partners | Webber Wentzel

This article first appeared in DealMakers, SA’s quarterly M&A publication.

AngloGold pushes deeper into the US market with another acquisition (JSE: ANG)

They are acquiring Augusta Gold in a R2 billion deal

AngloGold recently moved its primary listing from the JSE to the New York Stock Exchange (NYSE). It remains listed on the JSE so that South African shareholders can continue to invest in the stock without any difficulties, but having a primary listing in the US is a clear sign of intent around global growth ambitions.

Speaking of growth, the company has announced another acquisition in the US market. They have agreed to acquire Augusta Gold in a deal worth nearly R2 billion. Augusta Gold is listed in Toronto, so the price is expressed in Canadian dollars. They are paying C$1.70 per share, a premium of 28% to the closing price on 15 July and 37% to the 20-day VWAP. The purchase price is being settled in cash.

The appeal here is that Augusta Gold’s assets are in the Beatty District in Nevada. They are also adjacent to AngloGold’s existing assets in the area, so they are consolidating their interests in that space and adding to their mineral resources.

Ultimately, by seeking gold assets in a region like the US, AngloGold is hoping to increase its valuation. Whether we like it or not, investors are more likely to pay up for gold assets in the US than in South Africa, as the regions have very different risk premiums.

Unless Trump starts trying to fire every Fed chair who doesn’t want to drop interest rates, that is.

A huge upswing in AUM at Coronation (JSE: CML)

Themarkets have thrown them a bone

The story at Coronation in recent times has been one of disappointing flows and management blaming things like South Africa’s poor savings culture, while competitors with advice-led businesses go out there and hunt for assets with success.

The good news for Coronation shareholders is that although I doubt the situation with flows has changed much, recent market performance has led to a substantial jump in assets under management (AUM), the basis upon which Coronation earns a living.

AUM was R737 billion as at June 2025. Coronation never ever gives comparable numbers in the same announcement (even when they’ve done well), so we have to go digging through SENS to find them. The June 2024 number was R632 billion, so they are 16.6% higher over 12 months. The March 2025 number was R676 billion, so they are 9% higher over three months.

Now, if only the trend around inflows would change! But I doubt that will happen without management investing in distribution, something they seem unwilling or unable to do.

Rough news for investors in Mpact: profits have moved sharply lower (JSE: MPT)

The plastics business dragged them down

Mpact has released a trading statement dealing with the six months to June 2025 and I’m afraid it’s not for good reasons. Brace yourself: HEPS from continuing operations is expected to be between 18.2% and 28.0% lower. And for total operations, the expected drop is between 30.8% and 39.1%. Ouch!

The paper business achieved revenue growth of 7% thanks to higher containerboard sales volumes in both the local and export markets, partially offset by lower cartonboard and corrugated sales volumes due to weak demand. But even this growth wasn’t good enough, as cost and margin pressures drove a decrease in operating profit.

The plastics business suffered a drop in revenue of 15%, with FMCG Wadeville struggling to replace volumes lost after expiry of two contracts with a major customer. There was also seasonal pressure in Bines & Crates, which should ease in the second half. Although Mpact doesn’t explicitly say it, profit is surely down significantly in this segment.

With group EBITDA down by 15% and underlying operating profit by 26%, HEPS never really stood a chance. The only highlight here is that net debt has reduced from R3.23 billion to R2.985 billion.

Detailed results are due for release on 4 August, at which point investors will know the full extent of the pain. The Mpact share price has lost 17% this year.

Sales are up at Richemont – but not by much (JSE: CFR)

They refer to 3% growth as a “solid start” to the year

The quarter ended June 2025 is the first quarter of Richemont’s financial year. They got off to a positive start at least, with group sales up 3% as reported and 6% in constant currency terms. Hardly a rocket to the moon, but in the green.

The trends in the underlying segments is fascinating. The Jewellery Maisons were up 11% in constant currency, while Specialist Watchmakers fell 7%. The “Other” bucket (which is nearly as big as Specialist Watchmakers these days) fell 1% in constant currency.

The regional story is also interesting. Asia Pacific finally bottomed out in terms of flat constant currency sales and a decrease of 4% as reported Although there was a 7% decline in China, Hong Kong and Macau, other Asia Pacific markets picked up that slack. The next largest segment is Americas, up 17% in constant currency and 10% as reported. Then we get Europe, up 11% (on both metrics as the reporting currency is the euro). Japan had a rough time vs. a very high base, with sales down 15% in constant currency and 13% as reported. Finally, Middle East & Africa was up 17% as reported and 11% in constant currency, with the United Arab Emirates as the unsurprising bright spot there.

As you can see, the currency is making quite a difference. A world of dollar weakness and euro strength isn’t ideal for Richemont.

On the balance sheet, net cash was €7.4 billion, only slightly up from €7.3 billion due to the YNAP transaction that was completed in April 2025. They’ve finally sold that messy thing to Mytheresa, although they had to put in more cash to make that happen and they now have a 33% stake in Mytheresa.

Richemont’s share price is up roughly 20% year-to-date.

Nibbles:

Director dealings:

The CEO of Vunani (JSE: VUN) bought shares worth R6k. This sounds like a silly number in isolation, but there has been a string of recent purchases.

And speaking of silly numbers, a prescribed officer of Acsion (JSE: ACS) sold shares worth R612.50. I’ll include the 50 cents for the fun of it.

In further egg on the faces of the Assura (JSE: AHR) board regarding the offer they chose to back, the letters from the employee representative show that employees are more concerned about the merger with Primary Health Properties (JSE: PHP) than KKR and Stonepeak. That’s not surprising, as a merger is far more likely to lead to job losses. Tell me again about how that merger is likely to be a net positive for investors vs. just taking a cash offer?

Visual International (JSE: VIS) released results for the year ended February 2025. This is a penny stock (it closed 50% higher at R0.03, mainly because that’s the only increment higher than the previous close of R0.02), so it only gets a mention down here. Beware: they are looking to raise capital through a bookbuild that they will propose at the AGM, so dilution is coming. The company is so small that revenue was just R1.8 million, while the loss before tax was R2.3 million. HEPS was 0.39 cents per share. There are also a whole bunch of related party balances going on here. It needs a lot of cleaning up.

Numeral (JSE: XII) released numbers for the quarter ended May 2025. This period includes the 51% interest in Cryo-Save South Africa, as well as the 51% in Longevity Lab and a short period of ownership of the 40% in Isopharm. In other words, the comparable numbers aren’t useful. Revenue was $543k and net profit after tax was $75.7k, so this obscure Mauritian structure is now generating positive earnings. There’s very little trade in this stock and it remains a penny stock of note (currently trading at R0.02), but maybe they will actually manage to turn it into something.

Supermarket Income REIT (JSE: SRI) has completed the transfer of its listing from the closed-end investment funds category to the equity shares category on the London market. This may sound like just a housekeeping thing, but it makes quite a difference in terms of index tracking funds and the mandates of institutional investors.

In the incredibly unlikely event that you’re a shareholder in Globe Trade Centre (JSE: GTC), you’ll be interested to know that the company has exercised a call option to acquire a residential portfolio. They are funding this with a combination of own cash resources and a loan to the company.

Assura releases the response document to explain why they turned away from KKR / Stonepeak (JSE: AHR)

Just finding the document on their website is half the battle won

Takeover processes are highly regulated things. Boards are required to issue various important documents. Under UK law, the Assura board was required to issue a response letter dealing with their views on the KKR / Stonepeak. And if you spend half your life scrolling down on this page, you’ll even find that document.

As a reminder, the KKR / Stonepeak offer came to an effective 52.1 pence per share, which is a 39.2% premium to the price on 13 February 2025 (the day prior to the commencement of the offer period). Based on the latest available prices, this bid is a discount of a laughably small 0.7% to the implied value of the Primary Health Properties (JSE: PHP) offer.

If you’ve been paying attention to Ghost Bites recently, you’ll know that the acceptance rate by Assura shareholders of the Primary Health Properties offer is very low.

In my view, this is for three reasons. Firstly, the KKR / Stonepeak offer is a cash offer at almost the same implied price, without the volatility of a share-based offer where the implied value changes every day. Secondly, the Primary Health Properties offer comes with plenty of merger risk, whereas the KKR / Stonepeak offer is a clean break. Thirdly, KKR / Stonepeak exercised their right to switch from a scheme to a takeover offer, which means that shareholders can choose to accept that offer instead.

Funnily enough, as there were directors of Assura who gave irrevocable undertakings to KKR / Stonepeak to accept their offer, they are still bound by those undertakings! This comes to only 0.1% of Assura’s shares in issue.

As I’ve said throughout this process, the Assura board’s decision to switch to a recommendation of the merger rather than the cash deal simply doesn’t make sense. The arguments are based on the benefits of a “larger and more efficient REIT” (words that don’t tend to go together) and enhanced visibility. But again, this is all fluff, whereas KKR and Stonepeak have put cold, hard cash on the table.

My guess is that the Primary Health Properties bid is going to fail and that shareholders will act against the recommendation of the board by accepting the KKR / Stonepeak bid. Let’s see what happens.

As an aside, the accelerated dividend that has been part of all the bid calculations has now been declared. It will only be paid if the Primary Health Properties offer becomes unconditional though, so don’t hold your breath.

Labat Africa might dispose of some businesses (JSE: LAB)

They are in discussions with a company called All Trading

Labat Africa is going through significant changes. They’ve now released a cautionary announcement regarding a potential disposal of “some” of their subsidiaries, with the counterparty being All Trading (Pty) Ltd.

There are no further details at the moment. One would have to assume that they are looking to get rid of legacy assets, leaving them to focus entirely on the new push into the technology sector.

MC Mining decided to use SENS as a PR tool (JSE: MCZ)

Points for creativity, I guess

If there’s one thing that small listed companies love doing, it’s using SENS as a public relations distribution tool. You don’t see it too often thankfully, as the JSE tends to clamp down on this behaviour when it gets out of line. Every now and then though, you’ll see some pomp and ceremony coming out on SENS.

MC Mining is a perfect example. They released an announced with this title: “MC Mining’s steel making coal strategy enters new growth phase through reimagined Uitkomst Colliery” – reimagined, nogal.

The TL;DR is that Uitkomst Colliery is now implementing a revised turnaround plan. Metalla Tutum Engineering has been appointed to assist with this, in case that means anything to you. Aside from reworking the mining layouts, they are reducing headcount from 430 to 366, with “minimal forced retrenchments” – so some of this reimagining will be people reimagining where they earn their wages.

Full marks to the PR company, with the share price closing 15% higher after basically telling the market that their asset is broken and they need to retrench people.

Ninety One’s AUM has moved higher (JSE: N91 | JSE: NY1)

And yes, this is the case even after adjusting for the Sanlam deal

Ninety One announced its assets under management (AUM) as at 30 June 2025. This is the first quarter of the 2026 financial year. AUM is the key metric for this group as it forms the basis upon which they earn management fees.

AUM was £139.7 billion, up from £128.6 billion as at June 2024 and £130.8 billion as at March 2025. This includes £1.9 billion from the transfer of Sanlam Investments UK’s active asset management business. The South African tranche of that transaction is still to follow.

If we split out that bump, then growth over 12 months in AUM is 7.2% and over 3 months is 6.8%. In other words, it was a strong quarter!

They don’t give any information on the extent to which this was driven by net flows vs. changes in overall asset pricing. That’s the real test of success in the asset management game.

Orion presses the green button on its share purchase plan (JSE: ORN)

We desperately need to see more of this on the JSE

Orion Minerals does things the right way when it comes to capital raising. They need to raise chunky amounts from strategic investors for their mining projects, but they also give the little guy a chance by allowing retail investors to get more shares at the same price as the strategic investors. In a world where companies do accelerated bookbuilds at a discount to institutional investors, while retail investors are left out in the cold, this is great to see.

The latest such plan allows shareholders to subscribe for shares in parcels from A$170 to A$30,000 (roughly R2,000 to R355,000). The issue price is 1.1 AUD cents per share or R0.13 per share, which is in line with the current share price of R0.14. The offer applies regardless of how many shares each eligible shareholder currently holds, so this is very different to a rights issue.

The raise from strategic investors will add equity of around R67 million to the balance sheet, some of which is from loan conversions. The share purchase plan could be as large as R46 million, although I’ll be surprised if they get to a number of that size. The funds raised will be used to develop the Prieska Copper Zinc Mine and the Okiep Copper Project.

Here’s the “catch” – the offer is only open to eligible shareholders, which means those who were already in the register on the record date of 7th July. In other words, you can’t buy shares now to take part in the offer.

The offer is now open and will close on 5 August 2025. I hope they raise a meaningful amount!

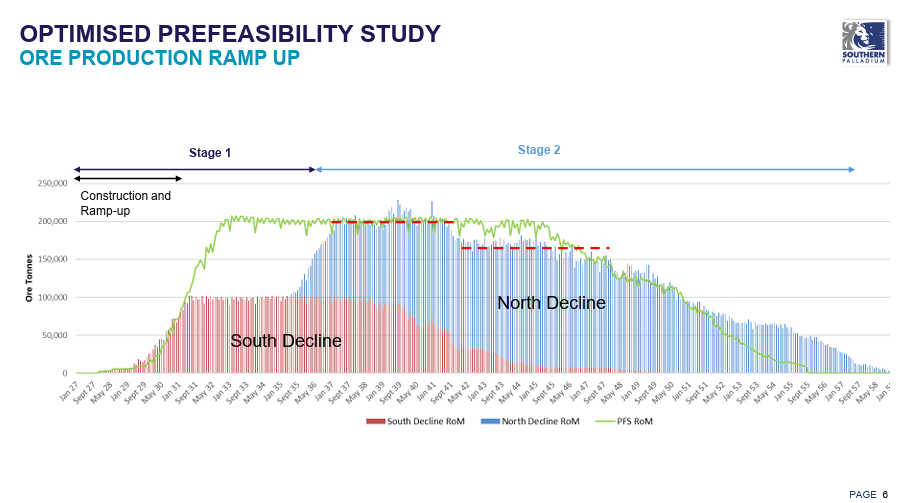

Southern Palladium has released a presentation with their optimised prefeasibility study (JSE: SDL)

It includes some pretty interesting charts

Southern Palladium recently announced the staged plan in its optimised prefeasibility study. As I wrote at the time, the goal is always to maximise the internal rate of return (IRR) and minimise the maximum capital requirement. Achieving this often requires a phased approach.

The company has made its roadshow presentation available, including some charts that show you what that phased approach looks like:

The expected post-tax IRR for stage 1 is 21.8% and for stage 2 is 26.4%. The peak funding requirement is $279 million, which is 38% less than they estimated in the prefeasibility study.

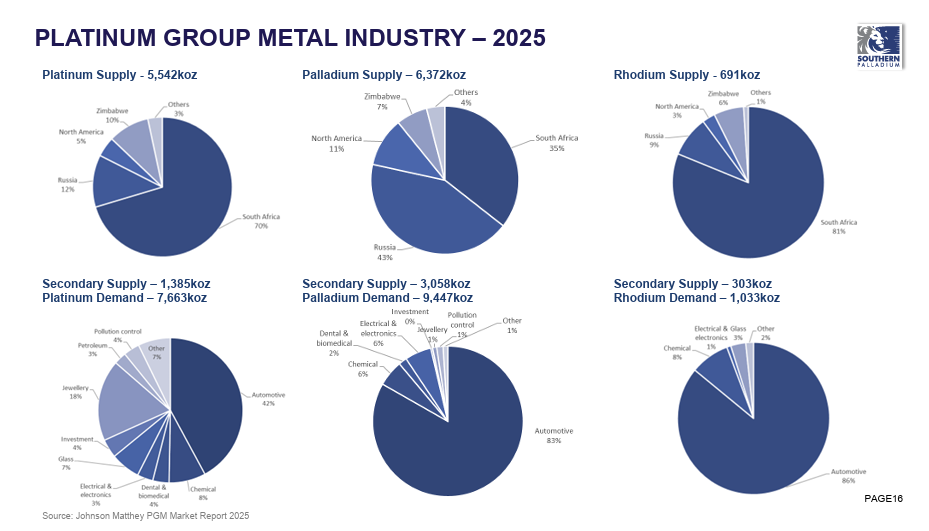

The deck also includes this slide showing the main suppliers of each of platinum, palladium and rhodium, along with the sources of demand:

An executive of Investec (JSE: INL | JSE: INP) sold shares worth R941k. The announcement doesn’t specify that this was the taxable portion of an award, so I assume that it wasn’t.

A director of a major subsidiary of PBT Group (JSE: PBG) bought shares in the company worth R74.5k.

Vukile Property Fund (JSE: VKE) has finished winding up the share purchase plan that was previously put in place for executives. This frees up R280 million in capital to deploy into other opportunities. Although this led to vast amounts in director dealings, these aren’t sales in the traditional sense i.e. they don’t tell you anything about the current level of the share price.

There’s a rather unusual announcement by enX (JSE: ENX) regarding three minority shareholders coming onto the register. Lockstock Investments now holds 7.07% of enX’s shares, Berkeley Capital has 5.22% and Skilgannon CC has 6.66%. I’m struggling to find any other information on these entities, including whether they are the counterparties for any of the recent corporate actions. I would keep an eye on this, as it’s not the norm to see a register churn like this as part of the ordinary course of trade in the shares.

Lewis Group (JSE: LEW) announced that Global Credit Ratings (GCR) affirmed its long- and short-term national scale issuer ratings at A+(ZA) and A1(ZA) respectively. Importantly, the outlook has been improved from Stable to Positive. This is informed by both the recent trading performance and the strength of the balance sheet. With Lewis having such a focus on credit sales, access to affordable debt (assisted by a strong credit rating) is key to the business model. So, this is good news!

HomeChoice’s (JSE: HIL) change of name has met all approval requirements and will become effective from 23 July. The new share code will be JSE: WVR.

It turns out that MTN Zakhele Futhi (JSE: MTNZF) didn’t need approval from the SARB for the special distribution that will pay R20 per share to investors. That’s a return of almost all of the current value of the company, with another R2 – R3 per share to go.

In case you were wondering what’s happening at Conduit Capital (JSE: CND) – and I know you you probably weren’t – the company has renewed its cautionary announcement. There’s no real update here, with the company still engaging with the liquidator of CICL and needing to publish financials for the year ended June 2023.

ArcelorMittal’s longs business is still likely to close (JSE: ACL)

Despite the social cost, there just doesn’t seem to be an economic solution

It’s an ugly thing unfortunately, but sometimes businesses fail. When small towns rely on them, those towns fall on very hard times. As much as everyone would like to avoid these realities, they are a part of life.

The frustration when it comes to ArcelorMittal is that it feels like the longs business is mainly a casualty of years of bad government policies and execution in South Africa, with only some of the blame lying with disruption in the market and other economic factors.

For example, poor rail service is 100% a failing of government, with ArcelorMittal noting that Transnet’s performance has deteriorated to its lowest levels ever (that’s a very different tune to what the coal companies have been singing lately). Weak domestic demand in construction is thanks to years of disappointing economic growth and deterioration in most regions in South Africa, leading to low confidence levels among property investors and businesses willing to take on projects.

There are other factors mentioned by the company, like the Preferential Pricing System and export tax on ferrous scrap that favours scrap-based steel makers rather than integrated steel makers. I don’t know anywhere near enough about the industry to have a view on that, so I’m just telling you what the company mentioned here.

The list goes on. There are insufficient import protections and it seems to be too easy for local companies to dodge the tariffs that are in place. And speaking of tariffs, our electricity tariffs are described by ArcelorMittal as being “globally uncompetitive” – again, I can’t comment on the validity of that claim in terms of industrial electricity costs.

If these problems sound hard to solve, that’s because they are. Back in March, ArcelorMittal announced that they would wind-down the longs business. The IDC then stepped in with a R1.7 billion facility to try keep things going while they figure out what to do. All this capital has been devoured and there’s still no solution for the business.

ArcelorMittal simply cannot keep this business going, or the entire group will collapse. For the six months to June, they expect a headline loss per share of R0.89 to R0.99, which is practically no improvement from the headline loss per share of R1.00 in the comparable period.

Sure, there are some external macroeconomic factors here, like a substantial increase in exports from China due to weak domestic demand in that region. When the global market is being flooded and South Africa has a combination of weak domestic demand and poor protections for the current industry (the estimate is that imports are more than 35% of local steel consumption), there’s really only one outcome. The IDC putting a R1.7 billion plaster on such a gaping wound is just throwing good money after bad.

It’s very hard to see how they will avoid closing this business this year.

Mantengu Mining wants you to know that it isn’t just a mining company (JSE: MTU)

A planned change of name will drop the word “mining”

Mantengu is certainly one of the more colourful companies on the JSE. After getting themselves into trouble with the exchange, they’ve stopped making wild accusations about share price manipulation. They also decided to change their Designated Advisor recently without really explaining to the market why they did it. There’s never a dull moment at Mantengu and the market tends to keep its distance.

The latest update is a step in the right direction in my opinion, as they are feeding a narrative to the market about the underlying assets instead of all the other weird stuff that has recently been the focus. By changing their listed name from Mantengu Mining Limited to just Mantengu Limited, they are sending a message that they are more than just a mining company.

In addition to the mining assets in the group (Langpan / Meerust / Blue Ridge), they recently acquired silicon carbide manufacturing plant Sublime Technologies in what looked like a bargain that is almost too good to be true. They’ve also acquired the assets of Masorini Iron Beneficiation.

The current strategy includes a willingness to acquire non-mining opportunities in verticals like base load power generation. So, you can expect to see activity from the company in mining, mining services and energy.

You can probably also expect to see further weirdness, unless the winds of change really are blowing.

There’s trouble at South32 (JSE: S32)

Electricity supply for the Mozal Aluminium smelter is uncertain

When you hear the word “smelter” you need to imagine the most power-hungry industrial installation imaginable. I’m certainly no engineer, but I know that aluminium smelters use a wild amount of power, as I remember seeing references during the worst of load shedding to just how severe the usage was.

Historically, most of the electricity needed for South32’s Mozal Aluminium smelter has been generated in Mozambique by the Cahora Bassa hydro-electric generator. Now, renewable energy is great and all, but it relies on mother nature doing her part. Recent drought conditions in Mozambique have led to the operator of the generator highlighting a risk to supply.

There’s a plan B: Eskom. These days, that’s even a decent plan B! The deal is that Eskom supplies power to Mozal Aluminium when the hydro-electric project can’t meet requirements. The problem is that the deal is up for renewal and South32 is unable to get an affordable price tariff from the parties on the other side (the Mozambique government, the hydro-electric company and Eskom).

This creates material uncertainty around the ability for the smelter to operate at all beyond March 2026. This would be a disastrous outcome for all involved, so hopefully a better solution is reached at the negotiating table. But in the meantime, South32 has flagged the risk and that there will be a large related impairment in the FY25 results.

At this stage, they haven’t given guidance on the size of the potential impairment.

Supermarket Income REIT picks up a new property on an attractive yield (JSE: SRI)

This pricing is food for thought

The UK is a developed market that has structurally lower yields than South Africa. UK 10-year Gilts (their bonds) are currently yielding 4.6%. South African 10-year bonds are yielding 9.9%. That’s a difference of more than 500 basis points!

So, you expect to see properties in the UK vs. South Africa following suit, with a large difference between the net initial yields they are acquired on. The latest deal by Supermarket Income REIT suggests that either UK supermarket assets are too cheap, or South African retail assets are too expensive – or perhaps both.

Supermarket Income REIT is acquiring a Tesco supermarket in Ashford for £54.1 million on a net initial yield of 7%. Remember, the higher the yield, the cheaper the property. The lease still has nine years to run and has annual inflation-linked rent reviews, with a cap of 5% and a floor of 0%. Now, this may be single tenant risk, but it’s apparently a great site that Tesco has been in for years. The risks seem more than manageable, with 7% as a hard currency yield being a great price for the REIT. South African retail properties change hands for only a few of hundred basis points more (i.e. on yields of around 9% to 11% for quality properties), a gap that feels too small based on relative bond yields.

This is a redeployment of capital that the REIT unlocked through forming a strategic joint venture with Blue Owl Capital. The net cash consideration on that deal was around £200 million, so they still have plenty of capital to deploy. Hopefully they can find more deals at this price!

Tharisa has corrected an error in its production report (JSE: THA)

The numbers are better than reported, but mistakes like these shouldn’t be happening

The good news from Tharisa is that they understated their net cash position as at 30 June 2025 when they released their second quarter production report. The bad news is that this is a material line item on the financials, so there’s a decent chance that the incorrect number was part of decisions made by market participants.

Somehow, Tharisa didn’t include a cash balance that they have on deposit with a financial institution. The correct cash number is $164.9 million, not $150.9 million. The debt number is correct at $121.5 million.

This means that net cash is actually $43.1 million, not $29.4 million as reported. That’s a 47% difference in net cash! $13.7 million in net assets (the difference) is roughly R245 million, or 3.8% of the current market cap. This unfortunately isn’t an immaterial error.

Nibbles:

Director dealings:

Fabricio Bloisi casually bought around R410 million in Prosus (JSE: PRX) shares in an on-market trade. R410 million!

An alternate non-executive director of WeBuyCars (JSE: WBC) sold shares worth a whopping R65 million to rebalance the portfolio. The stock has had a wild run, so this particular director sees this as a good opportunity to reduce exposure at a great price.

A director of a subsidiary of RFG Holdings (JSE: RFG) sold shares worth R826k.

The CEO of Vunani (JSE: VUN) bought shares worth R30k.

Assura (JSE: AHR) shareholders still aren’t falling over themselves to accept the Primary Health Properties (JSE: PHP) offer. The good news is that Primary Health Properties received regulatory approval in Ireland for the deal, which is the final approval they needed. The bad news is that holders of only 1.18% of Assura shares have accepted the offer. The offer closes on 12 August. A lot needs to happen in the next month for this deal to be a success.

Life Healthcare (JSE: LHC) confirmed that the proposed disposal of Life Molecular Imaging to Lantheus Holdings has now met all conditions precedent and will conclude on 21 July.

There’s generally been good news at Accelerate Property Fund (JSE: APF) recently, as the company looks to fix its balance sheet and move forward with Fourways Mall as a more successful asset than before. The latest news isn’t positive though, with lead independent director Derick van der Merwe resigning with effect from 11 July 2025 due to “strategic differences” – whatever those might be. It may be nothing, or it may be something. Only time will tell.

The meeting for the scheme of arrangement for the take-private of AH-Vest (JSE: AHL) has been convened for 11th August.

African Dawn Capital (JSE: ADW) has been suspended from trading due to failure to publish financial statements within the prescribed time.

With half of 2025 in the rearview mirror, it’s been a period in which investors have actively looked for opportunities beyond the United States. That’s good news not just for alternatives like Europe, but emerging markets like India and China as well.

Kingsley Williams (Chief Investment Officer of Satrix*) joined The Finance Ghost to talk about the key drivers and opportunities in each of China and India. The discussion also included insights from Ghost’s bottoms-up analysis of US-based companies and what those strategies teach us about what is happening elsewhere in the world.

There’s a lot more in the markets than just the S&P 500. This podcast will appeal to anyone looking to broaden their horizons and enhance their understanding of global investment opportunities.

*Satrix is a division of Sanlam Investment Management

Disclaimer:

Satrix Investments (Pty) Ltd & Satrix Managers (RF) (Pty) Ltd is an authorised financial services provider. The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information. For more information, visit https://satrix.co.za/products

Full Transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. It’s another one with the team from Satrix and this time we’ve got Kingsley Williams. He’s the Chief Investment Officer of Satrix*. I must say, he’s dressed like a Chief Investment Officer today in a very nice jacket. It’s a great shame that we aren’t using the video here, Kingsley, because you’re certainly dressed for it. But it is an audio-only podcast, so I just wanted to create that wonderful image in people’s minds. On this fresh, cold winter’s morning, you are certainly dressed well. So, thank you for being on this podcast and coming to share your insights with the audience as you so often do.

Kingsley Williams: Well, it’s always a privilege speaking to you, Ghost, and thank you for having me on the show again.

The Finance Ghost: No, it’s a great pleasure. And what an interesting time in the world, right? The markets are just never boring. I think it’s what I certainly really enjoy about them. I would imagine that a lot of the listeners have much the same view on the markets. There’s just always something to learn, always something to think about, and then always a decision to be made based on what you learned. That’s what keeps this so fresh and interesting. And of course, much of the narrative this year has been around trade wars. That really has been all over the headlines. It’s still all over the headlines!

It’s got political elements, it’s got macroeconomic elements, it’s got company strategy elements around supply chain and procurement and how consumers will respond. It really has been, if nothing else, a very useful learning experience for anyone who is following the markets.

And trade wars generally do send jitters through the market because tariffs are, at the end of the day, an interference in efficient markets, right? A purely efficient market would say: where can something be produced in the most efficient way possible? And if it is cheaper to make it somewhere else, bring it to our country and sell it here than it is to procure the thing locally, then that is what will happen.

So a tariff is, at its very core, an attempt to just interfere in the efficiency of markets. It also often just becomes a tax on consumers, right? It gets dressed up as a fancy political narrative, but at the end of the day it’s basically a tax because the tariffs are going to the government. So if there just isn’t an ability to tweak supply chains, then that’s where the money ends up going.

It is very, very interesting and a lot of these concepts are somewhat macroeconomic in nature. And we’re not going to have an economics podcast today, but I think it’s important for investors to understand how this stuff works. So, I’m going to open the floor to you for just some of your views around these attempts to close trade deficits and implement tariffs and what some of those impacts could actually be in time to come.

Kingsley Williams: Yeah, thanks, Ghost. It is a very, very interesting time. There’s never a dull moment in markets and this year certainly has been filled with the full ambit of roller coaster wild rides that we’ve come to be familiar with, I guess, particularly with the Trump administration and their very strong policy stance on what they’re trying to achieve.

But yeah, I think particularly with the US and with China and the trade war, for want of a better word, in that space. I did a bit of a recap, and I must give credit to BlackRock for some of their insights around this matter, which markets were grappling with a few months ago, particularly when tariffs started escalating and particularly so between the US and China. But some of the points that they raised is that at the end of the day, you can’t cheat economics, right? You can’t fool economics. The fundamental principles will come to bear.

And I think you did a great summary of distilling what the impact of tariffs are. At the end of the day, it does present an additional tax and inefficiency on the markets. And so there are going to be impacts and consequences to implementing those tariffs relative to living in a tariff-free regime.

So I think some of the things that we saw happen earlier, and some of the risks that you might face, is that by trying to close trade deficits that could ultimately lead to a shutting off of foreign funding. And where we particularly saw this come to bear was on US bonds. I think up to that point there was risk in the equity markets because no one was clear on where this was all going to land and what the impact was going to be on the companies affected. But where it really brought the chickens home to roost, so to speak, was on US bonds. And it’s important to remember that those – a quarter of US bonds are actually owned by international investors or investors outside of the US and so if there is too aggressive a stance taken on tariffs, that could ultimately lead to an increase in interest rates. I’m not going to explain all the logic around that, I’m not an economist, but that might ultimately lead to increased borrowing costs for the US government. And I think that is something that they’re very sensitive to.

And so that ultimately created a bit of a check on where tariffs are likely to land – what’s going to be a palatable level for the US administration to implement to achieve what they’re trying to get to without disrupting the whole apple cart and increasing their borrowing costs, which is at the end of the day, what they need to keep the economy going and to keep the administration going.

So the 90 -day suspension of tariffs was obviously partly in response to those – that step-up in yields that we saw in the bond market. So that’s the window we’re in at the moment. And we’re going to need to see where that all settles. I’ll come back to that in terms of where I think those tariffs may land.

The other thing that we saw was that if you’re going to implement tariffs to such a degree, particularly with China, where such a large source of your supply comes from, that effectively translates to a trade embargo with that economy. If you’re going to implement 100% or in excess of 100% tariffs on a particular country, it effectively says that we’re not going to trade with that economy anymore because it’s completely going to shut off supply because it’s not going to be cost effective to procure those goods.

A couple of practicalities with that. Firstly, China constitutes up to 100% of the trade in certain sectors and goods, particularly computers and electronics. Now, the US can’t function without having a supply of those goods, so you’re going to lose access to those critical goods which are required to keep the economy going. So that’s another key aspect needs to be considered in this whole trade war, is that you want to achieve an outcome, but you can’t do that at the expense of actually compromising the overall economy – there’s the markets and there’s the actual Main Street economy that are affected by this. And obviously there’s going to be an equilibrium that gets found in terms of trying to achieve the policy objectives, but also balancing that with what the markets demand and also what the Main Street economy demands.

So expectations are – and I mean, no one really knows, right? We’ll have to see. It’s always a little bit of an unknown quantity that you’re dealing with, an unestimatable situation that you’re dealing with when it comes to these policy interventions. But expectations are – and this is based on particularly where the UK has landed with its trade deal with the US and various other countries are following suit – post that deal, is that tariffs are likely to land somewhere between 10 to 15%.Now, just to contextualise that, that is about five times higher than where the average US tariffs were with the rest of the world at the beginning of this year at the end of 2024.

My information says that tariffs on average were at about 2.3% across the board on a trade-weighted basis with the US, so that’s across all countries if you average them all out. If we’re going to land at somewhere between 10% and 15%, that’s at least five times higher than where we were at the beginning of the year, which is significant. And that speaks to the tax you were mentioning earlier.

Now, against that backdrop, we’re also speaking a little bit about China. We are expecting their GDP to – it has been slowing, but we are expecting it to grow at 5% for this year. And let’s not forget that China have a deep interest in protecting their own industries. So to the extent that their tech industry is at risk of trade embargo and receiving key technology that they rely on from the US, they are going to try and develop their own hi-tech so that they are less dependent on the US. So that could be a growth area for the Chinese economy as they continue to invest and develop their own capabilities.

China is also fearful of the potential impact that this trade war may have on their markets. You know, who knows what might happen there? In terms of some of their larger names, larger companies which are listed in the US market as depository receipts, that’s a key source of funding that they’re able to access. But again, there are ways that they may be able to mitigate that by potentially dual-listing those businesses in Hong Kong, which is also very open to global capital markets. So, there are ways to mitigate against these risks.

But yeah, maybe just to wrap up some of my thoughts, we are seeing that with the suspension and the pause in tariffs, China is currently estimated to be at an effective average tariff rate of 32%, but that is down from the peak of where it was expected to be 103%, which was effectively a trade embargo.

But obviously that is still significantly higher – that’s specifically on China – but it’s still significantly higher than the 2.3% that we had at the end of 2024 and that’s the highest that it’s been since 1941. So, I think that just contextualises how much of an increase these tariffs are if you look at it in terms of multiples that it’s increasing by relative to what it’s been at the past.

So yeah, it’s a very dynamic space. No one can really predict what’s going to happen. But hold on to – fasten your seatbelts, put on your crash helmets, it’s going to probably be a wild ride.

The Finance Ghost: Yeah, there are some great charts that tell the story, right? So if you go and have a look at the US bond yield, there’s been lots of volatility, which as you mentioned was really just the market being able to express a view on what’s going on from a US fiscal perspective. The bond yield is about as close as you’re going to get to: what is the US’s share price per se. You have to be very careful with how you interpret it, but it is the purest play view on what does the market think of what the US fiscus is doing as opposed to the US economy, the companies in it, etc.

Speaking of companies, another wonderful chart is a year-to-date of Microsoft versus Apple. Now what’s really interesting here is obviously Microsoft is a services business. Apple, yes, there’s a big services component, but there’s a huge hardware component and they are in the crosshairs of this whole supply chain issue and the share price divergence.

They were both under quite a lot of pressure until sort of mid-April and then the divergence was extraordinary. So year-to-date, Microsoft is up almost 18% and Apple is down almost 20%. I mean that is a remarkable difference in performance from one just being more hardware focused than the other. In fact, Microsoft is bad at hardware in my experience, generally speaking, so this is actually helping them in this environment.

And part of why that Microsoft share price has done well and part of why some of these tech businesses have rallied is because of a weaker dollar, which is another chart that I would encourage people to go and draw. Don’t just draw the US dollar to the ZAR, which is the one that we’re all familiar with obviously. And it’s been very helpful to the rand, what’s been happening, but even against the euro, for example, I mean the truth of it is it’s not that South Africa’s done particularly well this year, it’s that the dollar has weakened against a global basket of currencies because of inflation expectations, because of what’s going on in the US and businesses like Microsoft, Netflix, all of them are, at the end of the day, exporters of services.

So, in South Africa, we’re so used to thinking, oh, we have a weak currency and so our exporters at least do well, but we get hurt as importers. US, you’re not used to thinking that way because the dollar’s always strong. But actually, these tech businesses, their international businesses become better effectively when they’re translating to a weaker dollar as opposed to a stronger dollar. So it’s just quite interesting to see how much has really changed this year in terms of how the market is framing what’s going on out there.

And you’ve raised China, you’ve raised their growth on that side. What’s interesting for me, and I think what people are not talking enough about, is that the Chinese market is pretty much shrugging off to some extent what’s really going on here from an equity perspective. And I’m just not sure that’s right, because if I look at some of the company results, and Nike is pretty hot off the press, and they were talking about how they would significantly reduce their procurement from China. There’s just a lot of manufacturing capacity in China, and I’m not sure that people are really thinking about what that capacity is going to be used for going forwards if a lot of these US companies can pivot their procurement away to other countries. And it’s all still very up in the air right now, but it is relevant for Chinese consumption – does that mean that Chinese consumers will start buying more local and you’re going to have this bigger divide between east and West? I mean, no one knows, that’s the truth, but I also just don’t think people are really talking about that angle to this story. I don’t know if you’ve seen much along those lines and what thoughts you might have on that Chinese market Kingsley?

Kingsley Williams: Yeah, thanks, Ghost. I love your anecdotes on those company specifics and how that provides a lens into what’s happening at a broader level. What we do know is that China has underperformed for the prior three years, except for the last year in 2024, when it staged quite a significant recovery. But prior to that, it deeply underperformed. And I’ll come to some of the reasons why that might be the case.

But what you find in markets is generally when things underperform, obviously the potential for them to add outperformance subsequently obviously increases because they’re priced at a discount. It doesn’t always work out that way, but always a healthy rule to remember that if something’s run hard, chances are it’s likely to run less hard going forward over a subsequent period. And obviously the converse is true. If something has corrected substantially, it’s got much more potential to outperform – the value investing 101, look for things that are undervalued, look for quality things that are undervalued. That’s where you’re going to find long term sustainable returns.

But you know, I think what we can’t discount or ignore is the impact of a centrally controlled government which operates within China and the impact that can have on markets with their coordinated central policy responses and interventions. And so that’s a factor that one always has to bear in mind, that the Chinese economy operates a little bit differently to more open and free market economies that are less centrally controlled, if I can put it that way.

So there are many positives for China equities, hence the bounce that we’ve seen. And I guess just a word of caution there is, just be careful excluding such a large market. It is a significant economy globally and to not have exposure to it or to be underweight to it is a risk that you may not want to have in your portfolio. But there are still numerous questions. The one that you’ve highlighted is a very important one, which I’ll touch on at the end.

But some of the others are the fact that growth for quite some time in the Chinese economy has been slowing down. And so that is a headwind. And if you think about valuing a market, you’re always going to have a growth assumption. The higher that growth is, the higher premium you can attach to that market in terms of the multiple that you’re willing to pay, because that’s going to pay itself back with the future growth. So, it might seem expensive today, but that growth into the future, it starts making the investment cheap.

But one of the other headwinds that China faces is an aging population. We know that they’ve rewound that policy in terms of the one-child policy, but we haven’t really seen a pickup in the Chinese birth rate and that population growth and the demographic bell shape now of their population really changing. And so that is a material headwind. That would be one source of obvious growth, if you’ve got a growing population and a growing workforce, but now you’ve got that one hand tied behind your back, and so all you’re left with to grow is productivity improvements.

One of the other risks that China faces is obviously deflationary pressure. I’m not going to elaborate too much on that. One of the other ones that is well publicised is the overextended real estate market, the property market and how overextended that is, and the cap that that puts on people borrowing more and using the equity in their homes and their real estate to fund growth. So that is a real, big source of risk. And potentially if investors have negative equity in their property exposure, that puts a cap on future growth.

And then obviously, what we’ve been speaking about today is tariffs and trade wars and geopolitics and the risk that you point out in terms of what that means for the Chinese economy to continue growing. If it faces all of these headwinds from a geopolitics and trade perspective, how are they going to stimulate or utilise the capacity that they’ve invested in? Obviously, the US is one market, but there are many other markets around the world that they could supply. But, yeah, it’s going to be very interesting space to watch.

I guess this comes back to a broader point, which is there will always be risks in investing in equity markets. It comes with the territory, that goes without saying. But what is very difficult to predict is policy responses and the need to respond in the face of competition and threats and risks. And those are very difficult to know – how an entity, a market, a company, and even a centrally coordinated government is going to respond in the face of those threats and risks.

This brings us back to why markets demand a premium, comes back to that fundamental law of economics. You can’t fool economics. So, there’ll be supply and demand laws, there’ll be funding requirements, but there are competitive actors in a market, and they are going to respond to the risks and the threats that they’re facing to deal with those and to mitigate those in order to remain viable and competitive.

The Finance Ghost: So, I know you enjoy the company anecdotes – I’ll hit you with two others. The first one is FedEx, who are busy putting in a lot of effort right now to trying to unlock additional trade lanes as opposed to just China – US. That’s clearly a response, looking ahead and saying, well, there’s going to be a lot of Chinese manufacturing capacity. There’s going to be products that need to go elsewhere – how does FedEx actually manage that? That’s a pretty interesting play.

Another one that’s quite fun to watch is a business called TJX. That’s an off-price retailer in the US. Basically, what they do is they buy up unsold bulk essentially, from all kinds of different FMCG businesses. And they have this treasure hunt model where you never quite know what you’re going to find in the store. It can be luxury stuff as well, so it can be basically anything. On their last earnings transcript, there were obviously some questions from analysts around: are you starting to see more opportunities in Europe where product is being diverted away from the US, or is there an expectation of lower demand in the US, stuff that might land in Europe? At the time they said no, but some of that will be a lack of demand factors as well, right? Because we know that the European economy has been pretty slow. So, it’s just this interconnectedness of the global economy really does come through when you’re looking at concepts like this, which I think does make it very interesting.

You’ve also touched there on the Chinese market valuation and of course it’s absolutely right in terms of where some of that rallies come from. And this is something that people don’t always pick up when they look at markets. You can’t just look at a chart in isolation and say, oh, chart’s up, therefore everything is better this year. It’s not necessarily exactly true. It can also be coming off a very depressed base. It can also be about what’s going to happen next year that might not be in the numbers yet, for example. So, I always look at historical P/E averages versus where something is currently trading. I find that’s a better tool in the market than just having an esoteric debate to say, well, one company trades at a 10 P/E, the other one is at a 20 P/E. That doesn’t really tell you anything. Actually, it tells you a lot more if you look at where each company is trading versus historical averages, when a whole lot of people in the market were battling it out, bulls and bears to say, hey, here’s what we’re willing to trade at – that’s your best data point. If a multiple is meaningfully higher or lower than its average, that tells you something, in my opinion, a lot more useful than just comparing it to another random data point. Each to their own, of course, but that has worked out well for me.

In terms of the Chinese market, I think you’ve got some stats for us on those P/Es and I’m going to then lead you into another market in the interest of time, which I think has been a lot more expensive and has done a lot better. And now of course the question is, is it too expensive, is it potentially overcooked? And that is India. So, first question is just where do those Chinese multiples stack up right now versus averages? And then just comments on India, I think are always interesting.

Kingsley Williams: So very quickly, the Chinese economy is currently valued somewhere between 10 and 13 P/E, depending which index and how you calculate that P/E ratio. Historically it’s traded between – in a range around 11 and its forward P/E ratio, which means what the P/E ratio is expected to be once future earnings or expected earnings come through, is going to roughly be at 11. So, it’s all very closely clustered around that 11 P/E mark currently and on a forward basis. I think you can say that the Chinese market, certainly not expensive, it’s probably fairly valued and it is at that level, taking into account all of the risks that I highlighted earlier regarding the Chinese economy.

But yeah, if we do move across to India and maybe just some quick anecdotal stats, we are one day away from the end of the first half of the year of 2025, so to Friday the 27th the S&P500 was flat year-to-date in Rand terms. Nasdaq marginally up 1.3%, developed markets up 3.5%, emerging markets more broadly up 9.3%. So outpacing developed markets by 6%, outpacing the US by 9%. China up 13% year to date, and then India up 13.5% year to date. So been another strong showing for India this year.

And that’s really off the back of interest rate cuts. In June they cut – the Indian economy cut by another 50 basis points to 5.5%. It’s now at its lowest level since August 2022. Economic growth has also surpassed expectations to the end of March at 7.4%, outpacing expectations of 6.5% for 2025. And that’s largely driven by domestic demand, government spending on infrastructure as well as a surge in digital payments. So I think that’s a nice segue into some of the reasons why the Indian economy is growing so strongly.

The one is a big digitisation drive, increasing digitally connected customers, drawing first time investors into capital markets. There’s this unified payments interface which does over 10 billion – 10 billion! – transactions per month. I mean that’s just enormous. And they’ve also implemented biometric IDs and proof of address technology which has had a knock-on impact of making it easier for first time investors to access the markets in terms of their know-your-client onboarding process. So, they can very quickly and seamlessly get involved in the financial system with this new technology. So really, we’re seeing a big drive of investing being democratised in the Indian market.

The other force that’s at play within India is demographics. And almost contrary and opposite to China, we’ve got a growing workforce that’s expected to continue for the next two decades with an economy that is able to absorb that workforce because it’s growing so strongly. And this contrasts with many other markets around the world that are experiencing aging populations and declining workforces.

So, a growing middle class that’s digitally connected, it compounds those productivity gains. You don’t have that one hand tied behind your back. You’ve got the productivity gains as well as a growing population which is supported by those digital platforms, artificial intelligence and obviously with an underpin of growing population scale.

The Finance Ghost: Yeah, again you’ve touched on so many great points there. It has been a wonderful time for emerging markets. And a lot of that is just the shine being taken off this US Exceptionalism, the US dollar. And a very, very strong dollar ends up being quite oppressive for currencies, especially in frontier markets. I’ll give you another company anecdote which I know you like, Kingsley, which is the MTN share price up 53% year-to-date. It’s been absolutely incredible. This is not in any way, shape or form because everyone is suddenly using their cell phones more. This is because, based on what I’ve read as well in a lot of the recent banking updates, and specifically ABSA and Standard bank, is that the African currencies have had a much better time this year than they really expected.

Now, obviously for MTN, with lots of exposure into these frontier markets where the currency has been a huge issue for them in recent years, it’s this lack of strength in the dollar, right? We just have finally stemmed the bleeding in these African currencies. And that’s very, very good news for the companies that are operating in that space because they can finally get a breather. They can actually generate some capital, they can generate some profits, they can pay down some US dollar-denominated debt, get a little bit off that treadmill. It’s like if you go to the gym and you put the treadmill on maximum gradient and 10kms/h, you’re not going to last too long unless you are very, very fit. And that’s what it’s like to be operating in Africa, dealing with a currency that’s going backwards all the time, the dollar just gets a bit weaker. That gradient just goes down. You can just run either faster or for a bit longer. And that works really well for these companies. That works really well for some of the investors in these stocks.

So, I think let’s just get back to India then as a great example of an emerging market. It really has been the emerging market superstar. You often find though with countries that the stock market doesn’t always reflect what’s actually on the ground. I mean, South Africa is a perfect example. Right? One of the biggest companies that you can invest in here is the Prosus / Naspers group. And there is very little exposure to South Africa on the ground in that group. It’s a tiny, tiny blip. It’s mainly Chinese exposure and then big tech platforms in Europe, in Latam.

So, what is the situation for India? If you go and buy the Indian stock index, are you actually getting the Indian economy or what are you buying?

Kingsley Williams: Yeah, good question. You know, I ran through some of the larger names and I think I’ll skip the financial companies because those probably are more directly linked to the Indian economy but not necessarily as interesting, apart from obviously the digital payments boom that they would be enabling, which I spoke to earlier.

But yeah, I mean, I think some of the big companies that you find in India is Infosys, big technology, services and consulting company. In many ways – I was running through these list of companies that you see operating in India and in many ways, they mirror what you see in the US where the company’s domiciled in the US or it’s domiciled in India, but it’s actually a global business. And it’s no different, Infosys operates in 56 countries. It is actually also listed on the Nasdaq exchange in the US.

Another one is Mahindra. We would know it, Mahindra Limited, we would know that company with the vehicles that they sell in South Africa, but they also sell farm equipment, tractors, they’ve got services in tech, financial, logistics, etc. Operate in 126 countries, so truly a global business. And 26 of those countries, they have a presence in those countries beyond just sales. So, there is real presence and capability distributed around the world.

Company I’d never heard of before, Larsen and Toubro, if that’s the correct pronunciation. It’s an industrial business, operates in 50 countries and they operate in the engineering, procurement and construction space.

But yeah, India is renowned for its business process outsourcing. So, it’s very much a service-based business as per what you were speaking about earlier in terms of Microsoft. So, they service their global businesses and their customer base. You can think of these as being more high quality, more stable businesses. It’s difficult to stop outsourcing processes that you’ve outsourced to Indian businesses that run various critical processes on your business. It’s not discretionary spending – that’s part of how you run your business. So has a much higher moat. It’s less discretionary spending.

One final point on equity markets, particularly with India, is that it actually represents a tiny portion of the Indian economy relative to the size of the Indian economy, which is now, I think the fourth largest economy in the world behind the US, China and Germany. It’s just surpassed Japan. It’s really an enormous economy, but its equity market is still relatively small. But we are actually seeing against that backdrop the Indian market growing and more and more companies being available within the Indian equity market. And that’s against the backdrop of companies actually delisting globally. You’re seeing equity markets shrink in many, many countries around the world. Fewer and fewer companies being crowded out by the larger businesses. But in India you see more and more companies actually coming into the index. We’ve seen that happen here in South Africa with delistings, I’ve noticed it in other indices around the world. But India is an exception, its equity market is actually growing. So I think that’s an interesting dynamic.

And maybe if I can just wrap up on valuations to close the point, we are seeing the Indian market trade at much higher multiples, but like I said, I think that’s an underpinning with its technology, service and business process outsourced services that it offers and services many developed economies around the world. So very akin to what US businesses actually offer. It does trade at a P/E between 24 to 26 times, quite a lot higher than China. The average is 20 to 22 times. So, it is at a premium to what it has been historically. Forward P/E at 22 times. So that’s very much in line with where its 10-year and 5- year average has been. So, I think we can safely say it probably is trading more expensive. But then one always needs to remember that growth always appears expensive because investors are paying for those future earnings that they’re going to receive. And obviously the Indian economy is certainly delivering on that front.

The Finance Ghost: Yeah. I’ll tell you where I’d like to finish this discussion off is another point that makes India quite different to a lot of the other emerging markets, certainly to China. And that is that India is the world’s most populous democracy.

And there are two very important points there. The one is the sheer number of human beings. So, you referenced there how India has overtaken the Japanese economy. The demographic issue in Japan around birth rate is huge. And there are a lot of other countries that are going to get themselves into the same problem in our lifetime. It’s happening in front of us, it literally is.

And then the points around democracy and that just really means a government where investors feel like there are basic rights upheld; they don’t do crazy authoritarian things. There’s a fair amount of stability. And unfortunately this is where China has really hurt its valuation multiples in recent years, is we have seen some moves by Chinese Communist Party where they’ve clamped down from time to time on sectors like tech for example. And then it makes people nervous. It means that people are not going to pay the same multiple for Alibaba that they might pay for a US-based tech firm or a high-growth Indian business. It’s just the reality.

And there’s a lesson in there for South Africa as well, there’s a lesson in there for all emerging markets and frontier markets is that if you want to create wealth in the hands of your citizens, you need to create a business friendly environment and you need to allow for capital to flow and then enable people to actually participate in that, which of course is why I’m always so happy to do this stuff with Satrix. Because if there’s one business in this world that is very good at helping South Africans invest in the market and participate in this stuff, it’s you guys.

I think this has been another just really good chat on some of the trends out there at the moment. To the listeners, I would encourage you to go and actually familiarise yourself with the breadth of ETF offerings that are available at Satrix, because it certainly is so much more than just an S&P 500 or Nasdaq-100. And as you do your research, you’ll be able to then see, oh, is there a product where I can actually go and invest in the specific theme? I like India or I like China or I like Europe or I like emerging markets or I don’t like emerging markets or whatever view you arrive at – the point is that there’s a product for you.

So, Kingsley, I just wanted to thank you for coming in and sharing these insights. Lots of great points raised. To the listeners, I hope you’ve enjoyed this. If you’ve got specific stuff that you’d like us to cover in future, of course you’re always very welcome to submit those ideas. Let us know what you thought of the show. And Kingsley, I look forward to getting you back, probably in a few months’ time if our usual cadence is anything to go by. Hopefully in some warmer weather and maybe another nice jacket, but just minus the jersey!

Kingsley Williams: Yeah, no, really appreciate the time Ghost and really couldn’t have summarised your views on what provides investor confidence and an underpinned to achieving growth – I really couldn’t have said that any better. I completely echo your sentiments there. And yeah, thank you for the time.

Browse the full range of ETFs available from Satrix here.

What did George Foreman, the man who once flattened Joe Frazier in two rounds, know about small kitchen appliances? Apparently, quite a lot – at least when it came to selling them.

We live in the age of influence. According to recent estimates, the global influencer marketing industry is now worth over $21 billion, with brands pouring money into partnerships with TikTok stars, YouTubers, and Instagram personalities in the hopes that a single “Get ready with me” video or haul can drive a fortune in sales. These influencers have perfected the art of making a product feel personal, like they’re letting you in on a secret rather than selling you something.

But before the rise of #sponcon and algorithm-curated feeds, brands turned to a different kind of familiar face: the celebrity. Long before MrBeast moved merch or Hailey Bieber sold out lip gloss, it was athletes, actors, and musicians who helped bring products into living rooms. Michael Jordan had his Air Jordans. Cindy Crawford had Pepsi. And in one of the more unexpected twists of marketing history, George Foreman – former heavyweight boxing champion – became the face and name of a countertop grill.

The birth of the Fajita Express

The earliest version of the grill came from the mind of Michael Boehm, an inventor based in Batavia, Illinois. Boehm wanted to create a compact indoor grill that could cook food evenly on both sides, while draining excess fat away. Together with engineer Bob Johnson, Boehm built a prototype: a bright yellow grill with a floating hinge and a sloped cooking surface that let grease slide off into a separate tray.

It was called the Fajita Express, and it was as quirky as it sounds. The original design included risers to hold taco shells and catch fat from sizzling fajita meat. There were even dual trays – one for grease, and one to keep your tacos upright.