Bureaucratic delays and regulatory uncertainty are a few examples of the challenges that hamper the completion of transactions in Zimbabwe. These hurdles are made lighter by the Zimbabwe Investment and Development Agency Act (Chapter 14:37) (the Act) and, more importantly, the Agency established under it. Whilst the Act provides the general framework for investments in the country, the Agency is tasked, among other things, with streamlining investment approvals and promoting investment in general.

This instalment, the second in a three-part series, puts into focus the Act and the Agency and expands on how these two are critical components in Zimbabwe’s mergers and acquisitions (M&A) landscape. In addition, the article will reveal how both can be invoked to serve as crucial enablers of M&A transactions. By understanding the advantages proffered by the Act and the Agency, foreign investors and local dealmakers can rely on them to facilitate deal execution, investor protection, and ensure regulatory compliance.

ZIDA: THE ENGINE OF INVESTMENT FACILITATION IN ZIMBABWE

The starting point for assessing how one can benefit from the Act and the Agency is to understand the Act. The Act came into force in February 2020, and it is a piece of legislation meant to provide for the promotion, entry, protection and facilitation of investment; to provide for the establishment of the Zimbabwe Investment and Development Agency, and to provide for matters incidental to or connected to the aforementioned.

Therefore, ZIDA is reference not only to the Act itself, but to the Agency which is created under it.

Benefits under the legislative framework

(a) Streamlining processes:

Before the introduction of the Act, Zimbabwe’s investment framework was fragmented across multiple statutes, naturally creating delays, regulatory uncertainty, and inefficiencies in the M&A process. The Act thus consolidated the since-repealed Zimbabwe Investment Authority Act [Chapter 14:30], the Special Economic Zones Act [Chapter 14:34] and the Joint Ventures Act [Chapter 22:22] into a single, investor- friendly law.

The Act also provides a simplified understanding of the investment licensing procedure for Public Private Partnerships and Special Economic Zones, while the underlying and supporting regulations also allow for the issuance of tax and customs related benefits applicable.

For M&A professionals and foreign investors, this is key to providing transaction guidance, and it also constitutes a streamlined legal framework that improves transaction certainty.

(b)The priority list:

This is the equivalent of ‘jumping the bureaucratic queue’ – legally. It is a ‘super power’ for companies dealing with government departments. Sadly, this super power is either not entirely known or it is severely underutilised.

The ability to jump the bureaucratic queue is found under section 6 of the Act. The provision states that, “Every officer, organ or arm of the State, and every statutory body and local authority whose duty it is to consider any application for the grant of any permit, licence, permission, concession or other authorisation required in connection with any activity, or for the provision of a service, shall ensure that, as far as possible, priority is given to the consideration of any application therefor by an applicant whose activity is permitted or approved in terms of an investment licence issued under this Act.”

Therefore, once a company is granted this license, most (if not all) processes must, as a matter of law, be given priority. Sensitising the authorities on this aspect may provide efficiency for any transaction or related applications.

(c) Clarity and legal protection for investors:

The Act incorporates globally accepted investment protection principles that are critical for foreign investors, including: the National Treatment Principle (NT), whereby foreign investors must be treated no less favourably than domestic investors in similar circumstances; the Most-Favoured Nation (MFN) Treatment, whereby any benefits granted to one foreign investor must be equally available to others; the Fair and Equitable Treatment principle, whereby investors are protected from arbitrary regulatory changes and unfair treatment; and protection against expropriation, whereby guarantees are offered against forced takeovers and state interference without adequate, prompt and effective compensation.

Further to the above, the Act also provides for repatriation of funds, and accords investors the right to challenge decisions affecting their investment through dispute resolution mechanisms.

By embedding these principles, the Act seeks to reduce policy uncertainty – a key concern for investors considering Zimbabwe. However, although these principles are reflective of the intention to provide more investor clarity, it should be noted that there is still massive policy inconsistency currently prevailing in Zimbabwe, especially in respect of currency laws in the country. It would be interesting to see investors pivot on this Act to challenge certain policies that affect investment in Zimbabwe.

Benefits from The Agency

As alluded to in the initial article, the Agency is one of the key regulatory bodies that govern M&A transactions in Zimbabwe, and it is essential to drive M&A efficiency. While the Act sets the legal framework, the Agency is the operational body that executes the law, ensuring that M&A transactions proceed smoothly.

ZIDA serves as the primary investment promotion authority, facilitating dealmaking by reducing bureaucratic delays, offering post-investment support, and creating a more predictable regulatory environment. This is primarily done through its One-Stop Investment Services Centre (OSISC). A key obstacle to efficient deal execution in Zimbabwe has been the need to navigate multiple government departments for approvals. The OSISC integrates approvals from all the key regulatory bodies stated in the initial article.

In practice, the Agency also meets up with investors and key stakeholders, upon request, to cater to any investor issues, including any bottlenecks that may arise during subsequent transactions. By bringing these agencies under one coordinated platform, OSISC cuts approval timelines, eliminates redundant processes, and improves regulatory transparency, all essential for fast-tracking M&A transactions.

Unlike traditional regulators that focus solely on approvals, ZIDA provides ongoing support to investors and ensures that their business needs, from a regulatory perspective, are catered for. More recently, in 2024, ZIDA suspended its yearly licensing maintenance fee of approximately US$3,000, rightfully pointing out that the fee actually deterred investment and unnecessarily penalised investors. It also provides for regulatory updates, helping investors stay compliant with evolving policies, and even goes further by making available investment opportunities in different economic sectors in the country.

As Zimbabwe continues to refine its investment climate, the Agency and the Act are both critical components in the M&A landscape. Together, they create a structured, investor-friendly environment for M&A transactions. For investors and M&A professionals, understanding ‘the ZIDA advantage’ is not just advantageous – it is essential. By fully acquainting oneself with the elements provided by the Act and the Agency, one can ensure a more seamless transactional experience for investors in Zimbabwe.

Tapiwa John Chivanga is a Partner | Scanlen & Holderness

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

The Bisie tin mine in the DRC has resumed operations

Market sentiment is disastrous enough right now without taking into account additional risks like regional conflicts. This is why it was very important for Alphamin to get the Bisie tin mine operations in the DRC back up and running as soon as possible, although the conflict situation is obviously outside of their control.

The share price was in proper trouble before the news of the resumption of operations, having dropped around 40% year-to-date. Thanks to a sharp rally of 24% based on the latest news, that year-to-date picture has improved to a drop of 26%. It’s ugly, but less ugly at least.

Importantly, although the mine was evacuated in mid-March, tin concentrate export logistics continued without interruption. They have limited concentrate stock on hand, so they definitely can’t afford any more problems like this.

The insurgents are 130kms east of the mine. That’s not exactly the biggest margin of safety, so investors will still be wary here.

In a shock to no one, Assura has rejected the Primary Health Properties proposal (JSE: AHR | JSE: PHP)

I really didn’t understand the deal strategy here

UK-based healthcare property group Assura is the talk of the town. They’ve been looking at a potential offer from KKR and Stonepeak Partners that has now turned into a firm offer. It’s an all-cash deal, which is always appealing to shareholders who enjoy clean transactions with low implementation risk. The board has decided to recommend this offer to shareholders.

This means that the approach by Primary Health Properties has been rejected once and for all. I’m not surprised in the slightest. As I wrote at the time when the indicative terms first came to light, a part-share part-cash offer that is essentially a merger would need to be at a price that is a premium to the competing all-cash offer. You’re asking shareholders to walk a road of believing in synergies and taking on deal risk. How can you ask them to do that for less money than the alternative?

Weak corporate finance strategies aside, we can now just focus on the KKR / Stonepeak offer. It comes in at 49.4 pence per share, comprising 48.56 pence in cash to be paid by the offeror and the rest in the form of the quarterly dividend that existing shareholders will be permitted to receive. This works out to 33.9% premium to the 30-day VWAP up until 13 February, which is when the offer period commenced.

Alas, no sooner had Assura arrived on the JSE than it seems to be leaving. At least we will still have Primary Health Properties. I just hope they get better advisors, or more executives with corporate finance experience if they plan to be doing transactions like this. I’m all for throwing your hat into the ring, but at least give it a chance.

Jubilee has found an unnamed partner for its surplus PGM feed material in South Africa (JSE: JBL)

This is necessary because chrome production is much higher

Jubilee’s chrome concentrate production reached record numbers in the six months to December 2024. This has created a lot of PGM-bearing material on the surface as a by-product. Instead of investing in capacity to process this material themselves, Jubilee has opted to partner with a local company to do it – they just won’t tell us who it is.

Earnings from the project will be shared equally and there’s an initial term of 12 months. This sounds like a pretty smart plan that will do wonders for FY25 production levels and especially return on capital, as no additional capex is required.

The flywheel is spinning at Purple Group (JSE: PPE)

Assets are growing faster than clients – and that’s what you want to see

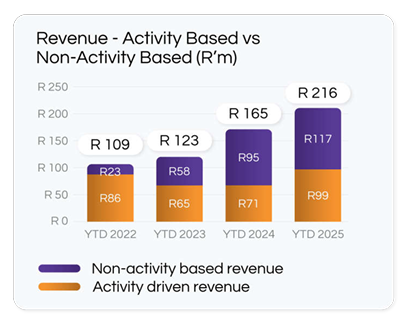

This is easily the best set of numbers that we’ve seen from Purple Group. That seems obvious when a metric like HEPS jumped by 204.1%, but that’s not even the best part. The key is to look at the sources of that growth, particularly in the core EasyEquities business.

The flywheel that needs to spin is client growth. Active clients grew by 8%, so that gets a tick in the box. The next all-important wheel is average inflow per retail client. Ideally, you want clients to put more and more money into the platform each year as their investment capability and level of financial acumen grows. Sure enough, the numbers per cohort are encouraging (longer standing clients are more valuable) and the average inflow per retail client is up 49% to R5,201. That’s still such a small number compared to how traditional brokers think about their clients, which shows you why this business is important.

Then, you want to see that costs aren’t growing as quickly as revenue. The HEPS growth kinda gives that away already, so you know there’s good news coming. There’s a comment in the CEO report that for every R100 increase in revenue, R70 is flowing through to the bottom line. That’s a strong incremental margin of 70%. For reference, the group profit before tax margin is currently 25%. This shows that top-line growth has every possibility of turbocharging the profit before tax growth.

For me, the best story in the group is the reduced reliance on activity-based revenue. Just take a look at this chart from the earnings report and consider how different this story would be if the purple bars weren’t there:

Aside from my worries about the valuation, my biggest gripe was that the immense multiple was being applied to revenue that isn’t recurring in nature. I wasn’t wrong, as you can see by the dips in the orange bars and the general lack of growth in that type of revenue, particularly when compared to the purple bars. These days, the multiple is far more reasonable and the underlying revenue is more recurring in nature.

With initiatives like EasyCredit, they certainly need to be careful about the risk that they introduce into the business model. The key is to go steadily rather than quickly. We’ve also seen very little progress thus far in the Philippines, with a current monthly cost of R1.5 million per month. Thankfully, the core business looks solid enough to support some initiatives that bring upside optionality to the story.

I’m finally ready to be long Purple Group, after a good few years of having to explain to people what the difference is between a great company and a great investment. If a share price is at reasonable levels, it’s possible for something to be both.

Nibbles:

Director dealings:

Des de Beer bought shares in Lighthouse Properties (JSE: LTE) worth R523k. This adds to his significant recent tally.

The COO of Spur (JSE: SUR) sold shares worth R421k.

The independent chair of KAP (JSE: KAP) bought shares worth R232k.

There are a couple of significant senior management changes at African Rainbow Minerals (JSE: ARI), with the current CEO of ARM Platinum moving across to run ARM Technical Services, a division that is being reintroduced at the group to focus on enhancing the efficiency and effectiveness of the group.

Anglo American is ready to demerge Anglo American Platinum (JSE: AGL | JSE: AMS)

And the name is going to change going forward

As part of Anglo American’s broader plan to simplify its group and focus on a smaller number of core assets (copper, premium iron ore and crop nutrients – note the lack of reference to diamonds), the controlling stake in Anglo American Platinum is being cut loose. As a sign of the severed ties between the groups, Anglo American Platinum is changing its name to Valterra Platinum as part of the process.

The renamed entity will be listed on the London Stock Exchange, thereby supporting a geographically diversified shareholder base.

Anglo American has already reduced its stake in Anglo American Platinum from 79% to around 67%. They plan to retain 19.9% after the demerger, which means that just over 47% of the total shares in Anglo American Platinum will be handed over (“demerged”) to Anglo American shareholders. Well, that’s what my maths says at least. The announcement says that 51% of the issued share capital will be demerged. Either I can’t do maths, or something isn’t adding up in the announcement.

The 19.9% will be retained for at least 90 days after the demerger, with Anglo eventually selling the entire stake down over time. They just need to do it slowly to avoid crashing the share price.

In more maths coming down the line, Anglo American is then planning a share consolidation that will provide consistency in the price before and after the demerger. Put simply, Anglo American is making its group smaller by handing a large asset to shareholders. A share consolidation would reduce the number of shares in issue on a proportionate basis, thereby increasing the price per share in order to achieve a comparable price to where it was trading before the demerger. They will work this out based on a three month VWAP for each company up until 20 May when the ratio is announced.

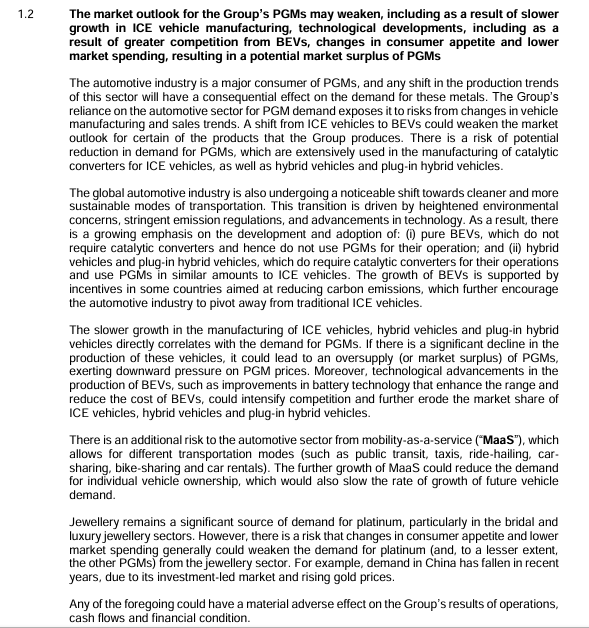

Due to the new listing on the London Stock Exchange for Anglo American Platinum (remember it will now be called Valterra), they’ve published a prospectus. I thought this this piece from the risk section is worth including here in full as it so succinctly describes the risk facing PGMs:

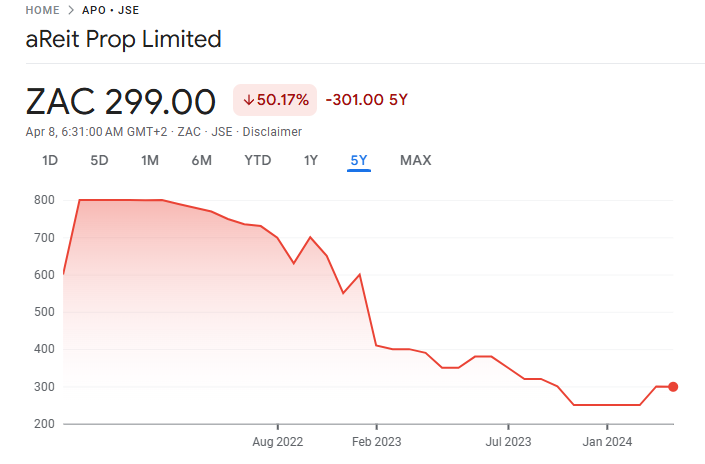

aReit’s impairments take it into a loss-making position (JSE: APO)

Surprise surprise: the NAV is coming down

When aReit listed, I made myself very popular with the company and its advisors by pointing out that the listing price was basically complete rubbish. Based on the yield being achieved by the assets, there was no way that the asking price was remotely fair.

Despite the protests at the time from those involved, it turns out that I wasn’t wrong:

Aside from the fact that they are currently suspended from trading because of how far behind they are on financial reporting, there’s now the additional pain of large impairments that need to be recognised to the assets. This is based on “a change to the discount rate and the variable income actually achieved” – in other words, both of the key ingredients in a property valuation.

The impairments are so large that the basic loss per share for the year ended December 2023 (yes, they are that far behind) was between 390 cents and 400 cents. The impairments don’t have an impact on HEPS, but they sure do bring the net asset value a lot closer to where the share price was trading.

Confusingly, the company has always announced a dividend for the 2024 financial year, which they reckon is 80% of distributable profit for that year – even though we are still waiting for 2023 financials. The dividend was 40 cents per share.

There are a zillion things you can invest your money in. Why this?

Cashbuild is clearly feeling more confident (JSE: CSB)

They are taking a controlling stake in a group of hardware stores

Cashbuild is subscribing for a 60% controlling interest in a company called Allbuildco Holdings. The gives them control of three hardware and building material stores in Pretoria and Limpopo. The total subscription price is R93 million, so this is a significant allocation of capital by a group that has been through some tough times.

Cashbuild describes this as an entry into a new customer base. Although they aren’t explicit on exactly how this is different, I Googled the stores and they seem to operate under the Mica brand. That seems very DIY-focused to me, so perhaps the idea is to go after more retail margins rather than selling to the trade?

Either way, they see this as a growth platform that they can grow alongside the existing shareholders, who will retain a 40% stake for now. Like all good listed company deals should include, there’s a pathway to control in the form of put and call options exercisable during the next five years. This will allow Cashbuild to pick up between 10% and 40% in the company i.e. it could lead to a 100% holding. The prices for the options have been capped.

Now, the post-money valuation of the business is R155 million (calculated as 93 divided by 0.6, as investing R93 million gets them a 60% stake). This means that the pre-money valuation was R62 million. This is because the R93 million is an injection of cash into the business, not a payment to the sellers.

Profit after tax for the year ended February 2024 was R12.8 million, so the Price/Earnings multiple here was 4.8x. This gives you an idea of the prices at which private companies change hands in South Africa. It’s actually much better once you work on adjusted net profit after tax, which comes in at R18.1 million and thus an implied multiple of just 3.4x!

That’s an appealing price in my books. Will it move the dial for the group? Probably not, since the market cap is R3.7 billion. If anything, it’s just good to see the management team feeling confident enough to pull the trigger on this.

Nibbles:

Director dealings:

Although the disclosure is a little odd vs. some of the other recent director dealings, it looks like Ivan Glasenberg bought shares in Glencore (JSE: GLN). At first I thought he crossed the 10% ownership threshold due to recent share buybacks, but other reports suggest he bought shares. Either way, directors at Glencore have been buying the dip like crazy. Do with that information what you will.

Des de Beer really got the hammer down with the latest purchase: a meaty R27.3 million worth of Lighthouse Properties (JSE: LTE) shares.

In a rather interesting transaction, the current CEO of Curro (JSE: COH) bought shares to the value of R5.85 million from the founder and ex-CEO. The deal was done at R9.40 per share, which is above the current price and way down from where it was trading at the end of 2024.

An associate of a director of Ethos Capital (JSE: EPE) bought shares worth R1.55 million.

There’s an unusual example of director dealings that has everything to do with a legal dispute and nothing to do with a view on the underlying share price, hence I’m including it here separately. An associated entity of Pieter Erasmus acquired shares worth R1.36 billion (not a typo) in Pepkor (JSE: PPH) through the exercise of rights under a pledge agreement related to how the Steinhoff mess was untangled. There is now a court battle between the legacy Steinhoff entity and the Erasmus entity related to the exercise of this pledge. I shudder to think of the sheer amount of money made by lawyers over the years in Steinhoff-related matters.

Standard Bank (JSE: SBK) has a management gap to fill, with Kenny Fihla on his way out to become the CEO of Absa (JSE: ABG). Sim Tshabalala, CEO of Standard Bank Group, will also take on the role as CEO of Standard Bank South Africa on a temporary basis. In a sign of where the group’s succession planning might be heading, but with no guarantees at all, Lungisa Fuzile (current Regional Chief Execution of the South & Central Region) has been made Interim Chief Executive of Africa Regions & Offshore. Where will this all end up? For now, we just don’t know.

MultiChoice (JSE: MGC) reminded the market that the long stop date for fulfilment of the please-save-us deal with Canal+ has been extended to 8 October 2025, hence all the dates in the previously issued circular will also be kicked out. At this stage, MultiChoice believes that the October deadline is still manageable.

Cilo Cybin (JSE: CCC) recently announced that it was seeking dispensation from the JSE to extend the date of distribution of the circular related to the acquisition of Cilo Cybin Pharmaceutical as a viable asset. This is due to the timing of publishing of financial information. The date of distribution of the circular has been extended out to 28 July 2025.

NEPI Rockcastle (JSE: NRP) announced that holders of 20.33% of shares chose the cash dividend election, while the other 79.67% went for the capital repayment (which was the default). There was no scrip distribution alternative on offer, as NEPI is trying to avoid having too many shares in issue.

Grand Parade Investments (JSE: GPL) has taken the same route as a number of small- and mid-cap players by moving its listing to the General Segment of the JSE. As I’ve mentioned each time we’ve seen news along these lines, the idea is to match the regulatory requirements to the size of the company i.e. to avoid placing a huge burden on smaller listed companies.

STADIO Holdings has a growth story to tell. That’s a rare thing on the South African market. The tertiary education space is booming and STADIO is addressing that demand through a combination of contact learning and distance learning offerings.

On this podcast, CEO Chris Vorster and CFO Ishak Kula joined me to talk through the strategy, the growth prospects, the capital allocation strategy and the risks that keep them up at night. If you want to really dig into the STADIO business model, you’re in the right place!

Please note: this podcast has been sponsored by STADIO. Where I work directly with companies, I always craft the questions myself without any influence from the company. My thanks to STADIO for valuing the broader Ghost Mail audience and for stepping into a new era of investor engagement. As always, you must do your own research and treat this podcast as only one part of your research process. You’ll find the most recent financial reports at this link.

Full transcript:

This episode of the Ghost Stories podcast is brought to you by STADIO Holdings. The goal is to give you further insights into the strategy and business model based on recent company announcements. I crafted the questions myself without any influence from the business. Please note that as always, nothing new here is financial advice. And you should not interpret this podcast as an endorsement of the company. Instead, use it as part of your broader research process in in your portfolio and be sure to refer to STADIO’s announcements and reports for more information.

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. It’s one that I’m particularly excited for because we’re doing something new here. We are taking a step into, I think, a new age of investor engagement. We are doing a podcast with STADIO around their recent annual financial results and the strategy at the company and what they’re busy with. And this is really a wonderful example of the management team at STADIO actually engaging with the market. There are obviously all the fancy conferences that happen and all the discussions with sell-side analysts, and this is a really great opportunity to bring some of those learnings to a broader audience.

So, my thanks to the management team at STADIO. And here today we have exactly who you want to hear from – that’s Chris Vorster and Ishak Kula, so that’s CEO and CFO of STADIO. Thank you so much for your time on this podcast. I’m really looking forward to it. And not only are we going to have some fun, but I think we’re going to learn a lot about STADIO, so thank you.

First question before I get you to say hello, must be of course: do you export anything to the United States? I think we have to start there. I’m just kidding, but welcome to the show – we don’t need to talk about that too much, at least you don’t export anything to the US and that’s happy news this week. You’re not competing with penguin colonies for trying to sell things into America and all the other chaos we’ve seen in the market this week. Luckily you’ve been somewhat immune from that and you can just get on with your core business, right?

Chris Vorster: Good morning. Let me start there and thank you for the opportunity. I actually last night checked in whether we have any students in the US currently studying with STADIO, and we did see that I think there are three students currently registered for distance learning programs, but they are all South Africans. I’m sure at some stage they will come back to the country. But yeah, we will have to look on how imports are going to be affected in that regard!

The Finance Ghost: No, it’s crazy. I mean, the markets are a volatile place and I think it’s always nice to see a company that just does the right stuff over time. I think that’s been a feature of the STADIO story: consistency. At the end of the day, you guys stick to your knitting. You know what it is that you do, you just move forward and make those incremental improvements in the business.

You’ve talked there about distance learning. So in that case, long distance learning, all the way in the US for a couple of students. I’m guessing most of the distance learning students are sitting in maybe smaller towns in South Africa or places not necessarily close to one of your campuses, right? What about students in Africa, for example? Do you have a lot of that?

Chris Vorster: So, yeah, it’s very interesting. If you look at the demographics of our distance learners, I would say 90% of distance learners are actually working adults, people taking up higher education to improve their employability in the workplace as well as positioning themselves for promotions or then also starting their own businesses. So it’s a whole combination.

And for that, you will see that the majority of distance learner students actually reside in city centres where big job opportunities are. Obviously, there are some students also in rural areas, but still the majority would be in our typical urban areas.

Africa, very small for us still. I think over time we will look at that market. For us, up to now, with such a young institution, it was always the strategy to make sure we build the right infrastructure, support structures and quality product to serve the South African market first. We believe that we are not 100% there yet, but we have laid very solid foundations to in future explore more markets outside the borders of the country.

The Finance Ghost: I think it also talks to the specialisation of some of the things you offer, right? There are some really specialist schools within the STADIO group. This would obviously encourage some of the distance learning, right? You can only get it in one place necessarily, or maybe a couple of places. What examples do you have off-hand of some of the really specialist stuff that you offer at STADO? Because I think it really talks to the strategic moat in the business.

Chris Vorster: Yeah, I think if you now just talk distance learning, one of the unique offerings that we have, but which is not really that big, would be our policing qualifications, which I think is quite unique to us and the relationship that we’ve built with the South African Police Services over the last few years. Ishak, you must help me here. I can’t think of something that’s really totally unique to STADIO that our big public universities won’t offer in this space?

Ishak Kula: Morning Finance Ghost. It’s Ishak here. Good to be here. I think latching on to that question around what makes STADIO unique – one of our businesses and one of our pillars in our business is AFDA, which is our film school, which operates predominantly in the creative economy space. I think what makes that offering unique is other than the institution being an award-winning institution on many fronts, it offers students quite a unique experience, a real-life unique experience in the creative economies to become actors or. film producers. To see these productions in real life is quite a proud moment for us as an institution. It’s amazing to see just the technology that’s embedded in those offerings and the actual true life experience that these students get, it’s really amazing. I think that’s one of the value propositions that makes that offering really world class.

The Finance Ghost: And AFDA is an in-person only option, right?

Ishak Kula: Yeah, Finance Ghost, that is purely contact learning. What we term as contact learning in our institution is typically a school leaver that then joins a physical campus. We’ve got a number of campuses across the country there, four predominantly to service those students in the creative economies.

The Finance Ghost: Fantastic. So that’s just a good example of how that police qualification you talked about is pretty much unique. That’s something you can do on a distance basis. And then on a contact basis, something like AFDA. There’s some interesting stuff in STADIO.

I think what always comes up and it’s always made quite clear in your reporting, is putting your contact learning student numbers versus your distance learning student numbers. You’ve made it clear throughout that this really is the overarching way to think about STADIO. And obviously the pandemic made everyone think about, well, just how much can you do online?

And it turns out that it’s a lot more than anyone thought, actually. There’s always going to be a piece of business that gets done in person, but there’s way more online than ever before. We are recording this online right now and it feels very normal because everyone is so used to having video calls. I remember, it was 10 years ago that I was in my corporate advisory career and you would go – sometimes the really big advisors would have a video room and it was a big deal. A whole fancy thing with a special shaped desk. That was where you did your really important, expensive calls.

So the world changes; it changes quickly. I think what’s interesting at STADIO is you are quite well-geared to this omnichannel model. If someone wants to do online, they can. If someone wants to do it in person, they can. What are your sort of broader targets here and how much flexibility does this give you in your business to have both?

Chris Vorster: Yeah, I think we made it very clear in our whole strategy from day one. We want to serve 80% of our student population in our distance learning mode and then put down infrastructure, campuses, bricks and mortar to accommodate 20% of our student population in the contact learning space, on-campus experience.

So just quickly to come back to what you said about COVID – due to all these distance learning capabilities that we have in the group and our experience in distance learning, Covid was a disruptor, but not as big as I think it was for many institutions. We actually adapted very quickly in moving students from the peer contact learning over to the distance learning mode and we could make sure that we support our students. And we lost very little teaching time, teaching and learning time during COVID.

However, that also came with a few challenges because it took time for our contact learning students actually to go back to the campus. If you look at our numbers from ‘20, let’s say ‘21, ‘22, up to where we are today, it was actually only – and Ishak will correct me, he’s the numbers guy – I think it was only in ‘24 where we saw this real big step back to the campus. I believe it had a lot to do with COVID and secondly also with our whole new thinking on what we’re going to offer at our different campuses.

If I might just use some time here, if you look at a pure or traditional private higher education institution, you will see the institution being in an office block where the focus is basically on teaching and learning and not so much creating or offering a full, holistic experience with extracurricular activities as well. So we took the decision in ’22: let’s sell off some of our smaller campuses and let’s really reposition ourselves when we talk contact learning that we put down a full holistic experience for a contact learner, giving the student that sense and feel of a full university experience.

And that led to our two big comprehensive campuses, the one there in Centurion and the other one that we are currently busy constructing here in the Western Cape in the Durbanville area.

The Finance Ghost: Speaking of university experience, I’ll never forget at Wits University – I’m a CA by profession, so you write those really tough exams in the later years. And a lot of the societies had these rooms underneath the one exam hall. It was like the mountaineering society – I’m pretty sure these people maybe went to a mountain once a year and the rest of the year it was basically just a room for them to drink on campus, bluntly. I distinctly recall listening to them having this wild Friday afternoon party downstairs. They were playing 99 Red Balloons, they were going absolutely ballistic. And I was writing like, I don’t know, FinAcc III or FinAcc IV. It’s just funny how you have those really precise memories in your life of that thing that hurt you.

But I guess the point is maybe not encouraging necessarily that kind of behaviuor, but student life is a big part of the tertiary experience and I think it is part of what attracts people to the traditional public institutions. But they come with some other challenges – we’ve had plenty of noise around stuff like “fees must fall” etc. It seems to have calmed down a bit recently, thankfully, there was a time when it was really bad. But there’s clearly space for this because there’s just a lot of people who want to study after school every single year. I see the stories of how there’s way more demand for tertiary education than supply and presumably that’s got to be one of the big drivers for you. Then other trends like semigration, for example, more people living in the Western Cape than at any time before. I imagine that’s also gone into your thinking around this Durbanville campus and just making it a place where students want to be, just giving another option in the Western Cape, essentially. Right?

Chris Vorster: Yes, definitely. We see a big demand currently, not just for STADIO, but I think for the whole private higher education industry with student numbers or matriculants qualifying for higher education increasing every year. And our public institutions just can’t keep up with this demand for higher education. So definitely a big market for us.

But we also want to emphasise: it’s so important that privates also meet the necessary quality offerings that we are going to offer, to make sure that the graduates that we’re going to deliver can actually meet the demands. It’s not just serving the demand, but that we actually produce graduates that will actually be employable and that can contribute to the economic development of the country. That should always be the focus and not just trying to get in more and more numbers, but to ensure that you’re actually contributing to what we actually stand for.

Ishak Kula: I think it’s such a good point, Chris, because I think generally there’s this perception out there with public institutions that somehow the hurdle rate or the barriers or the quality offering is potentially substandard. We always speak about in the eyes of the country or the population, there’s this notion that private schooling is superior to public schooling. But somehow when you get to public universities and let’s call them private higher education institution providers, that the public institutions are superior. So it seems to be the polar opposite. I think that’s one of our things in our institution is people need to realise that the barriers of entry and/or the levels of service and the quality of our offerings are on par with the public institutions. We need to go through the same accreditation processes, the same rigorous oversight mechanisms to make sure our service offering remains relevant and at the right levels. And that’s always this misnomer. It’s quite an interesting thing within the higher education industry.

The Finance Ghost: It’s fascinating actually. You know, you’re so right, you’re absolutely right and I’ve never really thought of it exactly that way around, but you’re right. So that’s obviously the disruption that you can now bring to the story. Tertiary education is particularly close to my heart. So one of the things I hope to do one day, once I’ve maybe built more of a track record, would be something like the opportunity to lecture at a business school, that would be amazing, on stuff like disruption because that’s obviously something I’m busy with as well. It’s a topic that’s very close to my heart, so it’s really great to see this kind of investment in South Africa.

There was something I wanted to ask you later, but I’m actually going to ask you now because I think it’s relevant, which is just to understand how you go about deciding what to offer. The typical kind of curriculum that comes in – this is a for-profit business, so it’s a bit different to a public institution that I think can sometimes offer courses that maybe aren’t as directly linked into employment opportunities. Or maybe I’m thinking about this the wrong way? Maybe you look at it and say: actually, we’re a university, and if someone wants to come and study a humanities degree where there’s no guarantee of a job afterwards, that’s okay.

So how do you actually go about thinking about this kind of stuff and the curriculum and how you offer things and where you offer them?

Chris Vorster: Yes, I think that is a very good question in the sense of, as a private obviously, we can’t offer all the programs that you would see at a big comprehensive public university because we also have to make sure that we look after our shareholders and that the institution remains profitable.

So, although we have a few programs that would typically not make the same profits as your more well-known programs, those programs actually contribute to our whole spread of qualifications, giving us comprehensiveness. So it’s a balance to get that right. But it’s also only fair for us to make that very clear that STADIO would never be in the position to offer all those smaller programs that you would see at a typical, public, well-known, matured university.

How do we do it? Obviously, we have our research that’s continuing in the background every year. But I think where STADIO gets the most traction on what we offer is our links with industry. We’ve made it very clear that part of our DNA is alignment with the world of work. We invite industry into our institution. From when we design a new program, we get them in to evaluate it for us to see whether everything is relevant, whether this is actually what is needed in the workplace. That being said, I must just also make it very clear that we have to meet certain academic standards for a program which is not negotiable, but we invite industry in, make sure that they are part and parcel of how the program looks. Then we invite industry into the classroom, come in and share your experience with our students.

And then thirdly, very important is then to evaluate and give feedback, evaluate the programs, tell us what happens with a STADIO graduate in your business and how are they actually performing? All of that information really gives us the blueprint on how we look at new programs, whether to phase out older programs that are no longer relevant in the workplace, and then to bring in new programs that are actually required by industry.

The Finance Ghost: Ishak, I guess this is where you have to keep everyone honest, right? Some course-level profitability and all that kind of stuff. So maybe I’ll throw this question at you because it’s also just related to the overarching product offering and the way that you guys think about the business.

Just around the growth runway, is it a case of saying, okay, our existing qualifications can just keep ticking over. We can add students every year. The beauty of distance learning is theoretically the number of students is infinite, right? So that’s quite nice. Or do you need to keep adding qualifications in order to achieve your growth targets?

And then anything you can give us around how you think about pricing versus volume, for example, I think it just helps investors understand the levers that you can pull to keep growing revenue at such a strong rate at STADIO. Because I think – well, I don’t think, I know STADIO is a growth stock. Everyone sees it as a growth stock, definitely. And so that’s what’s important, right, is to show ongoing growth?

Ishak Kula: That is exactly right. I think we have been blessed and fortunate with very strong growth. Remember, it’s a fairly young institution listed in 2017, really spun out of Curro at that point, and is now completely independent and separate and distinct. Of course there’s collaboration, but I think for the most part it’s two separate entities managed separately. I think it’s important.

We’ve been very blessed with our growth story, I think particularly in 2024. If you looked at our growth, 14% growth year-on-year. And to your point there, Finance Ghost, I think we’ve been very fortunate. That links directly to our strategies and institution is the bread and butter comes from distance learning, right? So strategically, we’ve positioned the business because that’s where we can pull a lot of leverage. Your incremental cost to serve a student in distance learning, I suppose, is insignificant as you add more students and therefore it allows you many opportunities when it comes to pricing strategies to keep those competitive. That’s how we really look at this business. We want to make sure we provide a high-quality offering at a good and competitive price. Therefore, pricing strategy is always one we want to track inflation or slightly above inflation, but it must remain competitively priced.

We certainly see ourselves from a pricing perspective on par with public universities in the contact learning space. In the distance learning space, no secret that our big competitor is UNISA. And there in the distance learning space in particular, we’re also very well priced against that competitor, certain qualifications probably slightly more expensive, whereas other qualifications slightly less expensive. It’s quite a dynamic thing. But I think it’s important that we stay true to our philosophy of widening access to quality higher education, which means it must also be affordable. That’s always the delicate balance, being a listed environment. I think to Chris’ earlier point, to make sure that we can run a profitable and a sustainable business, but yet serve our community and the dire need within our country.

The Finance Ghost: What’s really interesting and your old friends at Curro, I’m sure something that keeps them up at night is the birth rate. I read it in the hospital results, the maternity cases are dropping. They need children – that’s what they need at Curro. They need more of them! But we’re here to talk about STADIO, and I guess what’s interesting and the reason I raised that trend, is people having fewer kids and having them later – doesn’t that play directly into your business? People are studying for longer, they are putting more energy into their careers. Are there any trends that you’ve seen in terms of the age of students? Is it a little bit older? I’m very curious about what that driver might be because my gut feel is people are studying for longer, investing more in their careers. They understand that they’re on a pretty scary treadmill. There’s AI to worry about, which disrupts entire industries. The fundamentals of your business feel quite strong to me?

Chris Vorster: Yes, I think if we look at our business with the big adult learner component, we definitely see a lot of students coming back and reskilling or doing additional postgraduate qualifications. That’s something that is very noticeable over time, is the number of students taking up postgraduate studies. Now I’m talking about honours, postgraduate diplomas, which is very industry-linked, specific to a specific job. So yes, we do see that happening.

What is interesting though, is in our non-formal business where we look at short learning programs, since after Covid, that business is not really showing any growth. It’s stagnant. It looks like students rather now prefer to do a formal program, get a formal qualification, and even those who want to upskill also go for the formal route of a postgraduate honours, masters or then even a doctorate.

The Finance Ghost: Super interesting. So at the start of this podcast, I said to Chris and Ishak, they have to sit really still when they’re doing this podcast, otherwise the volume does crazy things. Ishak took it so seriously that the light in his office just went off and he had to wave his hands wildly to switch it back on again! You know, these are the joys of me having video on. You can unfortunately only hear this, but it was quite entertaining.

So Ishak, spotlight back on you, literally in this particular case. I want to ask you a financial question, that is around return on equity, which I think is a core metric that investors look at. Investors certainly should look at. If you’re listening to this and you don’t look at return on equity, you need to reevaluate some of your life choices.

This is a key metric when you’ve got stuff like fixed assets and capex. STADIO is interesting because the distance learning is obviously something you wouldn’t associate with capex, but the contact learning you would certainly, when you’re building things like a Durbanville campus, we’re definitely in capex land here now.

Return on equity, I had a look at your latest report, it’s gone up every single year since 2018. So that’s pretty impressive, up from 11.7% in 2023 to 13.6% in 2024, certainly a solid uptick. I think room for improvement there, I would imagine.

What are some of the drivers of that? How do you think about getting ROE up further?

Ishak Kula: Yeah, no, that’s spot on. I think, again, fortunate with the historic growth, but definitely room for improvement there. It speaks predominantly, I suppose, to the “youngness” so to speak. It’s still a young business, basically. I think we’ve been fortunate with really good growth.

When we look at the points you raised around capex, Finance Ghost, it obviously will have an impact going forward, but I think predominantly if we look at our growth trajectory and what we think is going to happen into the future, no one has a crystal ball, right? I think past performance and some good planning I think gives us some headway into what the future looks like. We certainly think that our strategy is, post the construction of Durbanville, which has commenced in October 2024, which is really phase one of our big capex project, we hope to conclude phase one at the end of December 2025 / early January 2026 so that we can open that campus, which will be a big chunk of our capex needs and requirements, that will obviously allow us to have hopefully a good student intake come January 2026 in our Durbanville campus.

I think it’s an important thing because strategically we set ourselves internally that although we want to return more value to our shareholders in the form of dividends, we want to continue to be prudent, we want to make sure that we have a good intake in Durbanville. And post that, certainly from the 1st of January 2026, we see the return on equity even going up more significantly on the back of that capex project being out the way and our capability to sustain a good level of earnings supported by very good dividend growth.

Our internal target is to, by 2030, we believe that we should get an ROE or return on equity of 20%+. I think that will keep us as a management team happy. But I think more so our shareholders.

The Finance Ghost: Yeah, at 20%+, this share is going to be trading at a very nice premium to book, I would imagine, because that’s typically the way it would work on the JSE. Speaking of the share price, I actually just went for fun now and I drew a five-year chart. Obviously that’s back to Covid lows, right, it’s April 2020 as an important reference point, but a casual 400% increase over five years. So well done. That’s pretty good.

I think the other thing that’s interesting to note is year-to-date, you’re actually pretty much flat. So that’s good in a market where there’s been a lot of pain this year, outside of very specific sectors on the JSE, I think that shows that there is support from investors for what you are doing. It’s fun to look at share prices when the market’s tight or difficult and you’re like, okay, what is this thing doing? It really tells you a lot about the resilience that’s baked in.

That brings me, I suppose, to probably my last question on the podcast actually, which would just be around things like a bit more around the dividend policy. You recently went and attended a conference where I think you had some questions around that, around share buybacks. What are investors saying to you? Are they saying, we love the story, take as much of our capital as you can and go bananas? Or are they saying, hey, we want dividends?

This could be a little case study in dividend policy. You can include this in your Durbanville campus commerce course or investment course when you have one. But yeah, it would be good to get some more insights. And maybe just some of the other top of mind stuff that’s coming through from investors and institutional investors? Part of this podcast is to help a broader audience understand what’s going on in the business and what people are thinking about. So that would be good to get a little temperature check on how those meetings went.

Ishak Kula: I think it’s a good opportunity to respond to that. Invariably, many shareholders ask us about our dividends and I think our dividend strategy has been clear and I think we’ve communicated it as such. We certainly want to target 85% of our free cash flow to be declared as a dividend – we want to work towards that post the construction of our Durbanville campus, which is our major capex project. I think that phase one, we estimate it to be around R220 million. We have strategic ideas potentially to accelerate the building, which might increase that phase one cost. But then there’s a future phase two, depending on how our intake looks like next year, phase two, we’ll really look at the timing of that.

But for all intents and purposes, our strategy is to get to 85% free cash flow over the next couple of years, which will increase the dividend substantially. It’s probably the first point I want to make.

The second is invariably our shareholders. I think there was, to be honest, a mixed bag. I think some shareholders liked the dividend on the back of what we declared, whilst others said to us and the feedback has been, we believe so much in the business, we think there’s so much growth opportunity, should you not look to reinvest it into the business? And our response to that is, I think although the dividend has been substantially increased from 10 cents last year to 15.1 cents in 2024, it’s still small relative to what the future state is.

I think the 51% increase, although it’s significant from a percentage perspective, we don’t think it dilutes our growth story at all. We think there’s still lots of runway and that’s how we’ve positioned the business intentionally. We’ve kept it lean, we don’t have any external debt at the end of December ’24. We’ll obviously incur a bit of debt now as we construct the Durbanville campus, but we really want to keep the business lean, which allows us a lot of leeway to move and pounce on opportunities. And that really has been our strategy and it allows us as really good opportunities come our way, we wouldn’t need to do unnecessary capital raises from our shareholders. We could fund it probably very comfortably off our existing balance sheet and/or debt, whatever business we acquire at scale.

To answer your last question, many shareholders ask us whether there isn’t an opportunity to acquire more shares. That’s something I think we as an institution need to look at. Our shares aren’t as liquid, we’re still a small cap. But many of our shareholders ask us, where can they, how can they get more shares? And that is one of our challenges I think that we need to overcome.

The Finance Ghost: It’s a nice question. It’s much better than being asked, please, we want to sell. How do we sell? Do you know anyone who wants to buy them? So you’d much rather be asked that question, that’s for sure.

I remember when you first announced dividends, speaking to institutional investors in the market, I think that South Africans really liked that because I think that South African investors are quite a browbeaten bunch. They’re inherently skeptical. They’ve been suffering for a decade, not a lot of growth stocks on the JSE, I think STADIO is a rare exception.

When they see something like a dividend, they go, oh, not only does it grow, but there’s some capital discipline, they’re not just going and buying whatever they can. Whereas I think American investors almost think the other way around. It’s like, oh, no, why are you paying a dividend? Have you run out of ideas? It’s just the American mindset versus the South African mindset. And I think what you’re doing is right for the South African mindset.

So, last question to bring this to a close. Chris, I’m going to aim it at you. If there was one thing that gets you the most excited about this business, what would that be? And what is the one thing that keeps you up at night?

Chris Vorster: That excites us, very much so, the growth opportunity still in this business. I think we’ve positioned the business extremely well for the future. That really excites us. The runway that’s still ahead – we haven’t even touched further education. There are a lot of opportunities still there.

What keeps us awake at night is, unfortunately, the South African economic situation, in the sense of there is this huge demand for higher education, but unfortunately, funding is lacking and affordability is still a big issue to widen access for more people to get into a higher education. So that’s something that we need to work on. A lot of work goes on behind the scenes to really crack that nut. But I think if we can do that, it would not just be fantastic for our business, but it would be fantastic for the country as a whole.

The Finance Ghost: Yeah, fantastic. I think we’ll leave it there. I just want to congratulate you again on a strong set of results and also just thank you for your support of the Ghost Mail platform and for valuing the Ghost Mail audience, for allowing me to do the work that I do.

Chris, Ishak, thank you so much. And to the listeners, go and dig into STADIO. Go and dig into as many stocks as you can, right? That’s why you read Ghost Mail. But I think STADIO is definitely one of the rare examples of a growth stock on the JSE and a lovely way to go and understand what that means is to go and read the annual report, go and check out the investor relations site, go and engage with the contents thereof and send through questions. It would be interesting – once you’ve listened to this podcast, what do you wish I’d asked? What do you still want to ask? You never know, we might be able to get some answers for you.

Chris, Ishak, thank you so much for your time and I hope we will do another one of these.

Chris Vorster: Thank you very much. We enjoyed it.

Ishak Kula: Thank you. Finance Ghost. Absolute privilege spending the morning with you.

The African Rainbow Capital offer is apparently fair to shareholders (JSE: AIL)

I’m just as surprised as you are

When the dust settles on this, many investors in African Rainbow Capital would’ve made money. Thanks to the performance of underlying businesses like Tyme and Rain, this ugly duckling ultimately turned into the least attractive swan in history:

The fact that things eventually ended in the green (albeit only just) doesn’t make it right. Over that period, management did far better than any of the investors did. The management fees were a source of constant criticism, with the company finally making changes along the way that made the fees slightly less ridiculous.

Now, the offer to shareholders is a price of R9.75 per share. Those who don’t want to accept the offer can continue to hold their shares in an unlisted environment. Given the way that minority shareholders were treated over the course of this journey while in the public eye, I would prefer to preserve the contents of my cat litter box – after my felines do their morning business – and display them on my coffee table rather than own unlisted shares in ARC.

The intrinsic net asset value (INAV) per share is R12.78, so the offer is at a 23.7% discount to that number. Due to the vast discount to INAV at which the shares trade, the offer price is actually a 21% premium to the 30-day volume-weighted average price (VWAP) before the deal was announced. You would therefore expect the independent expert to declare the deal to be unfair but reasonable, right?

Wrong.

Through some impressive mental gymnastics, BDO has in fact opined that the deal is fair to shareholders. How do they do this? Well, firstly, by only considering the detailed financial information of assets that represent 67.6% of the overall portfolio value. The materiality threshold they applied was that anything with a fair value of over R750 million would require detailed valuation work, whereas anything below that level would rely on an “Investment Report” – yes, a report prepared by the general partner in the fund, i.e. the management team.

So, to be very clear here, detailed work was done on just over two-thirds of the portfolio. As for the rest, it appears to have primarily been a case of “source: trust me bro” – and that’s not great in my books. I understand that it’s a large portfolio, but that’s a big chunk that didn’t get the benefit of a detailed review of the underlying financials. BDO is proud to include in the report that their work got very close to the management’s INAV anyway. Well, yes – across 67.6% of the portfolio, that is.

Even if we assume that this is a reasonable approach to valuing the full portfolio, we then arrive at the deferred tax liability for capital gains tax. Now, if I understand the circular correctly, this liability is a result of the plan to re-domicile the company to South Africa. In other words, they have valued the company based on a transaction that might be approved by shareholders, as opposed to the legal state of the company today. Again, I don’t like that. The deferred tax is responsible for taking the INAV down from R12.78 to R12.31 per share.

But how do we get from R12.31 per share to the BDO-suggested fair value range of R9.30 to R10.03 per share? Those management fees are back to haunt you, with BDO putting a negative value of R1.22 per share on the head office costs. In other words, the exorbitant cost structure impacts the valuation by roughly 10%!

It is correct to take into account costs? Absolutely, I would do the same thing. Should it have already been a feature of the INAV, thereby punishing management for loading up costs that negatively affect INAV over time? In my opinion, yes, although INAV rarely takes this into account at most investment holding companies. I think the issue just becomes more apparent when fees were already such a pressure point.

And finally, a holding company discount of 10% is applied, reflecting the underlying challenges that would be faced in disposing of all of the assets. Once this is done, the offer to shareholders falls neatly into the BDO fair value range, which means the expert has opined that the deal is fair to shareholders.

What this really does is send a message to the market that investment holding companies are where your capital goes to die. If you invested R100 at the INAV per share in a structure like this, you would immediately lose 10% to management costs and another 10% to a liquidity discount. Clearly, not all management companies are structured with such onerous fees, but the fact remains that these groups will always struggle to trade at anything close to INAV. This is why you’ll never see equity capital raises from these companies on the JSE anymore.

For the deal to go ahead, holders of more than 75% of shares eligible to vote will need to approve the delisting. Remember, each shareholder has the choice to accept the offer or not. If the delisting is approved, those who don’t accept the offer will move into unlisted territory. Perhaps this will make them fabulously rich, as assets like Tyme and Rain move closer to fruition. Personally, I suspect that any pot of gold at the end of this rainbow won’t be shared in a way that is any more equitable than what we’ve seen already.

Sirius Real Estate had a solid financial year (JSE: SRE)

The rent roll is up and so are the property values

Sirius Real Estate released a trading update for the year ended March 2025. Things went really well, as evidenced by a 6.3% increase in the like-for-like rent roll. Due to the effect of acquisitions, the total rent roll was much higher, up 12.8%. Like-for-like is the better way to judge performance though, with the group proud of the fact that this is the eleventh consecutive year of like-for-like performance above 5%.

To add to the strong rental growth, Sirius also expects property valuations to have increased during the year. As valuation yields have been pretty stable, an increase in the rent roll naturally drives an uptick in valuations.

Acquisitions will certainly be a feature of earnings in the year ahead as well, with Sirius having been very busy with deployment of the extensive amount of capital that was raised. After doing 11 deals worth over €250 million in the past financial year, they will be focused on actively managing the acquired assets to improve their values.

Investors will want to keep a close eye on financing costs. Although Sirius has a powerful balance sheet and enjoys strong support from its lenders, the reality is that recent debt raises have been at higher rates than the debt that was raised during the pandemic. This is simply a function of the interest rate cycle, leading to an increased overall cost of funding going forward. Provided that there is decent ongoing growth in the rent roll, that shouldn’t be too much of a problem.

Trematon’s INAV has dropped further (JSE: TMT)

This comes after decreases last year as well

On a day in which the troubles of investment holding companies were thrust into the spotlight, Trematon had the unfortunate timing of releasing its trading statement for the six months to February. Sadly, they weren’t positive.

The intrinsic net asset value (INAV) has decreased by between 15% and 18% year-on-year. This implies a range of 335 and 345 cents. The share price is sitting at R1.86, so that’s a fat discount of 45% to the midpoint of the INAV range.

In the comparable interim period, the INAV fell by 3%, so the decline has only gotten worse. Results are due for release on 10 April, at which time we will have full details.

Nibbles:

Director dealings:

Here’s an unusual update: a non-executive director of Italtile (JSE: ITE) has obtained approval under a pledge agreement with a creditor to sell shares worth R10 million by the end of April 2025. Average daily value traded in Italtile looks to be around R4.5 million, so that shouldn’t be too difficult to achieve.

A non-executive director of British American Tobacco (JSE: BTI) bought shares worth R2.6 million.

A director of Momentum (JSE: MTM) bought shares worth R413k.

A non-executive director of Glencore (JSE: GLN) bought shares worth over R290k.

A director of a major subsidiary of Shoprite (JSE: SHP) bought shares worth R198k.

I think it’s worth noting that all the directors and senior executives of Quilter (JSE: QLT) who received share awards only sold enough shares to cover the tax. Seeing a unanimous approach to this among the management team is unusual.

Regular readers will be aware that Assura (JSE: AHR) has a couple of potential suitors at the moment, one of which is Primary Health Properties (JSE: PHP). In order for the board of Assura to give reasonable consideration to the part-share, part-cash indicative offer on the table from Primary Health, they’ve asked the UK Takeover Panel for an extension to the Put Up or Shut Up (PUSU) deadline. Primary Health now has until 5 May to announce that they will or will not make a firm offer. And yes, it really is called Put Up or Shut Up.

Hyprop (JSE: HYP) has given itself some headroom by increasing the size of its domestic medium term programme from R5 billion to R7 billion. This doesn’t mean that they have already raised the additional debt in the market. It means that they are simply putting the steps in place to do so.

With the markets in disarray in the aftermath of tariffs, it looks like the theme this year is more around risk management in a bear market rather than which growth stocks to buy. Of course, this can change, as markets are volatile and are driven by a number of factors including geopolitics.

This volatility is exactly why diversification is so important. The risk of “diworsification” is ever-present in the strategic asset allocation decision, which is why it ends up being even more important than stock picking.

A quantitative approach to strategic asset allocation is baked into the Satrix Balanced Index Fund and related products. Kingsley Williams, Chief Investment Officer of Satrix, joined me to talk through the key concepts in diversification and the usefulness of a balanced fund.

This podcast was first published on the Satrix website here.

*Satrix is a division of Sanlam Investment Management

Satrix Investments Pty Limited and Satrix Managers RF Pty Limited are authorised financial services providers. Nothing you have heard in this podcast should be construed as advice. Please do your own research and visit the Satrix website for more information on all their ETF products.

Full transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. It’s going to be a really interesting one, as they always are. It’s another one with the team from Satrix, but this time we have a guest who you haven’t heard from in a little while, I think, and that is Kingsley Williams. Kingsey is the Chief Investment Officer at Satrix*, so he gets to have some really interesting conversations about broader investment strategies, what it all means for your portfolio and some of the products that they offer at Satrix.

It’s going to be a fun chat. It’s the end of quarter one of 2025 already, shockingly. If you feel like you haven’t made any progress on your New Year’s resolutions, I’m afraid you are a quarter of the way through the year, so better get cracking.

Kingsley, how’s your year going? How are your resolutions tracking? How’s your portfolio tracking?

Kingsley Williams: Yeah, it’s been a wild start to the year, both from a personal perspective – there’s lots going on at home, looking to do some enhancements there, so it’s been busy from that perspective, work is incredibly busy….

The Finance Ghost: …I’m trying to decide if enhancements at home means another room, or having a baby, or buying a better anniversary gift. You can’t leave it there, surely?

Kingsley Williams: Yeah, no, it’s – we’ve long thought about utilising this big space above our ceiling. We have quite a high roof, so we’ve been working on putting a loft in there. Adding an extra room, which has been quite a journey. But an exciting one. An exciting one.

The Finance Ghost: Building is not a joke. Building is not a joke at all. Building a portfolio is arguably easier than building onto your house, I think.

Kingsley Williams: Yeah, yeah.

The Finance Ghost: As you are perhaps experiencing right now?

Kingsley Williams: Firsthand, exactly. Markets have been pretty choppy as well, which I think we’re going to talk a bit about. Clients have been keeping us busy as well. We’ve been speaking at various investment conferences around the country, headed up to Sun City, which I’ll talk a little bit about as well. So, yeah, it’s been wild, but we’re still here. And, as you say, time flies when you’re having fun. We’re at the end of end of Q1 already, but it’s, it’s been really, really busy.

The Finance Ghost: Yeah, Q1 is fairly mental. My side as well, with all the earnings releases on the JSE, but also – well, everywhere actually, but the JSE because it runs on a six-month reporting calendar, you get these crazy busy seasons, whereas the US market is quarterly and does tend to be a bit more steady. It’s just always busy in the US as opposed to locally where there are clearly some very busy times.

And speaking of the US versus local, I had a look the other day. Satrix S&P 500ETF was down just over 5% year to date. The US market, as everyone knows, has had a bit of a wobbly this year. And the headlines are always full of tariffs this and geopolitics that – that’s obviously not helping. The Satrix 40, which tracks the JSE Top 40, up 8.5% year-to-date when I looked. Obviously those percentages will all be different by the time anyone listens to this. In fact, they’ll be different by the end of this podcast.

But it does show – I mean, that’s pretty meaningful outperformance locally, right? The international one down 5%, the local one up 8.5%. Diversification helping out here, right? Especially because I think the focus has been on offshore for the last couple of years. Most people, I would wager, have been shifting their money into offshore feeder ETFs, and it’s been the right choice for much of that period, let’s be honest. But in 2025, that seems to have shifted the other way. And that talks to diversification, right?

Kingsley Williams: It certainly does. And I think the old analogy of not having all your eggs in one basket is probably the simplest way to understand diversification. If you trip and fall carrying your eggs in one basket, you’re not going to have many eggs left. So I think that’s the simple analogy. And as I mentioned, we actually travelled up to Sun City recently for the recent Investment Forum conference up there. It was a stark reminder of the potholesand speed bumps that actually await investors when investing in risky markets. Those potholes and speed bumps which you encounter on the road from Lanseria up to Sun City sneak up on you when you least expect them. You’re comfortably cruising along at 120kms/hour, only to be greeted by a camouflaged speed bump with no warnings that it’s there. You really need to have your wits about you.

The Finance Ghost: I’ve lived in the Western Cape for too long now because when I hear someone talk about potholes, I’m like, yeah, that’s a cool analogy. But up there, it’s a lived experience. That’s the difference.

Kingsley Williams: It was very real. And Nico was actually driving, who you know well. Thankfully, he was super alert and was able to slow down in time. Otherwise we might have lost a wheel or our suspension.

The Finance Ghost: Yeah, please, we need Team Satrix out there. We don’t want to come and find you guys on the side of the road on your way to the bushveld.

Kingsley Williams: Exactly. So without taking the analogy too far, we know that section of the road is problematic because of the road signs, or some of the road signs. Word of mouth before we took the trip, and also the time that Google Maps indicates it’ll take us to get to our destination.

I guess in the same way, we also know that markets, by their very nature, are going to be bumpy. It’s a feature, especially of equity markets, it’s not a bug. We shouldn’t be worried when the occasional correction comes our way. That’s certainly what we’re seeing happen at the start of this year.

I’d also go further and actually caution investors to not be too concerned about this minor correction. Let’s just contextualise it. Three months is very short term in the context of what our investment horizon should be when investing, particularly in risky assets. We should have a minimum term of five years – five would be the absolute minimum – it should ideally be seven to ten years. That’s the term you want to be thinking about when investing in risky asset classes like equities.

The other thing that we should bear in mind when being exposed to markets is that past is not prologue. I was having a look at where that came from. It was actually past is prologue, which came from Shakespeare’s Tempest play, but when it comes to investing, past is not prologue. In other words, one interpretation of that is that past performance is no guarantee of future results.

Let’s just rewind a little bit. We’ve had phenomenal returns from the S&P500 over the past two years. 37.5% in rands in 2023, 26.2% in 2024. But interestingly, I was looking back, and it was down 13.5% in 2022.

Let’s contextualise that relative to the 5% down that we’re talking about now. I think that speaks a lot to human nature and our recency bias, where we forget more severe pain in the past because it’s a distant memory, and the more immediate pain which might not be as severe as what we experienced previously, occupies top of mind. It’s important to keep context in these things.

In the short-term, as I’ve mentioned, markets are inherently volatile, which is why time or the term you are invested for is such a critical consideration. You want to make sure that when you’re investing in risky asset classes like equities, when you’re taking additional risk by investing offshore, where the currency now plays a big role as well, that you give that sufficient time to play out. Three months is very much a blink of an eye and operating in the short-term space.

Prof Eugene Fama, who’s a Nobel Laureate in economics and finance, put it this way, and he said that if you’re worried about short-term corrections in risky assets, then you probably shouldn’t be invested in risky assets in the first place. Again, to what Nico said earlier, volatility and risk and corrections are a feature of investing in equity markets. They’re not a bug, so we should expect them.

And in fact, the bigger risk is not taking enough well-rewarded risk, which can significantly compromise your long-term wealth accumulation journey. So unfortunately we are bombarded with a lot of short-term news, daily market performance, that’s what you hear on the radio, that’s what people are talking about most of the time. It means it’s difficult to actually take a step back and see the bigger picture because all we hear about is the short-term.

But to get back to your original question, what does diversification actually mean? And it’s a bit of a technical answer, so I hope it makes sense. But essentially, when you’re diversifying, you want to achieve two things.