Following a proposed refinancing of subsidiary Westcon International – by way of a partial refinancing of an existing US$450 million shareholder loan – and the sale of a 5% stake in the subsidiary for $25 million to General Atlantic’s equity funds, Datatec has announced its intention to pay shareholders a special dividend of c.$75 million (R7,1 billion).

Novus has acquired an additional 2,490 Mustek shares at R15.00 per share on the open market (outside of the Mandatory Offer) for R37,350. The company now holds 29,02 million Mustek shares constituting 50.44% of the issued shares in Mustek. Together with concert parties this shareholding increases to c.70.73%.

As of 26 June 2026, Africa Bitcoin’s secondary listing on the Developmental Capital Board of the Namibian Securities Exchange (NSX) has transferred to the Main Board of the NSX.

This week the following companies announced the repurchase of shares:

To reduce the share capital of the company and return capital to shareholders, Quilter commenced, in March 2026, a £100 million share buyback programme. Repurchases to date total £40 million of which £32 million were conducted on the LSE and £8 million were conducted on the JSE. The maximum aggregate purchase price payable by the Company under Tranche 2 is up to C.£30 million.

In 2026, Greencoat Renewables implemented a share buyback programme totalling €100 million over 12 months with a first tranche amounting to €25 million beginning on 5 March 2026 – representing 13% of the issued share capital. This week the company announced its intention to commence a second tranche which will return a further €25m of capital to shareholders, following the completion of the first tranche which is expected during July. The second tranche repurchase will be complete by end-December 2026. This week 1,113,295 shares were repurchased for and aggregate €837,197.

Bytes Technology announced in May 2026 its intention to implement a new share repurchase programme to purchase the company’s shares for an aggregate value of up to £25,0 million. This week the company repurchased 525,000 shares at an average price per share of £3.54 for an aggregate £1,86 million.

In December 2025, British American Tobacco extended its share buyback programme by a further £1.3 billion for 2026. The shares will be cancelled. Over the period 15 – 18 June 2026, the company repurchased a further 494,286 shares at an average price of £45.32 per share for an aggregate £22,4 million.

Ninety One plc announced an increase in the repurchase programme from £30 million to £55 million to be completed by 21 July 2026. The shares to be purchased on the open market will be cancelled to reduce the Company’s ordinary share capital. This week the company repurchased a further 827,059 ordinary shares at an average price 218 pence for an aggregate £2,02 million.

Anheuser-Busch InBev’s US$6 billion share buy-back programme continues. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 15 to 19 June 2026, the group repurchased 525,297 shares for €37,23 million.

During the period 15 – 19 June 2026, Prosus repurchased a further 2,291,242 Prosus shares for an aggregate €89,8 million and Naspers, a further 790,310 Naspers shares for a total consideration of R669,49 million.

Two companies issued a profit warning this week: Mantengu and Crookes Brothers.

One company issued or withdrew a cautionary notice: Sebata.

WeLight announced that the International Finance Corporation (IFC), has invested €27 million in the provider of rural electrification through mini-grids in sub-Saharan Africa. WeLight was founded in 2018 by AXIAN, Sagemcom and Norfund. The funding will enable the company to accelerate its geographic expansion with the launch of operations in Nigeria and the Democratic Republic of Congo (DRC), while strengthening its operations in Madagascar and Mali.

Spiro, the electric vehicle (EV) and clean energy infrastructure platform, announced the successful closing of its latest funding round at US$270 million. This comes from a newly finalised $55 million investment from NewTrails Capital. On the back of support from long-standing institutional partners such as FEDA, Spiro’s latest equity round also drew global capital from Europe and Africa, Impact Fund Denmark, Equitane and FEDA, on top of the recent backing from Nithio and the Africa Go Green Fund.

A Tunisian agritech firm, RoboCare, has secured a six-figure investment from venture capital firm 216 Capital to support its next growth phase and expand across Africa and the Middle East. RoboCare develops an agricultural management platform that helps farmers make better decisions through the intelligent use of multiple data sources: satellite imagery, drone data, IoT sensors, weather data, and field expertise. Through its AI models, the solution enables early detection of crop diseases and stress, optimises resource usage, and improves farm performance.

Agenz, a Moroccan proptech, has announced a US$5 million oversubscribed seed round led by BREEGA, Attijariwafa Ventures, and Saviu Ventures. The new funding will be used to accelerate its expansion beyond property data and transaction services and into the financial infrastructure layer of real estate.

The European Investment Bank’s international development arm, EIB Global, and Wema Bank, Nigeria’s oldest indigenous national bank, has announced a strategic partnership agreement with the signing of a €50 million SME-focused credit line for youth and women-focused businesses in Nigeria.

Section 75 of the Companies Act (the Act) provides that if a director has a personal financial interest (PFI), or knows that a related person has a PFI in a matter to be considered at a board meeting, that director must disclose that interest and must subsequently recuse themselves from consideration of the relevant matter. Failure to do so may render a decision, agreement or transaction invalid.

A PFI in respect of a person, as defined in s1 of the Act, means “a direct material interest of that person of a financial, monetary or economic nature, or to which a monetary value may be attributed”.

S75 of the Act extends the definition of “related person” in s1 of the Act to include “a second company of which the director or a related person is also a director”. Accordingly, a director does not need to control the relevant second company. It is sufficient that the director (or a related person) serves on that company’s board for it to be regarded as a related person for purposes of s75 of the Act. While the existence of a cross-directorship is generally straightforward to identify and disclose, the question arises whether this extends to foreign directorships. This question is of particular importance in the context of cross-border transactions, which dealmakers encounter regularly.

Foreign directorships

S1 of the Act limits the definition of “company” to juristic persons incorporated under the Act. On a strict interpretation, s75(1)(b) would therefore not apply to cross-directorships between a South African company and a foreign company. This gives rise to a potentially anomalous position, where disclosure of a PFI may be required where a cross-directorship relates to two South African companies, but not where the same decision, agreement or transaction involves a South African company and a foreign company.

Although there is no express statutory requirement to disclose a cross-directorship involving a foreign company, disclosure may nonetheless be required under common law, depending on the circumstances. These common law obligations should be carefully considered where directors sit on boards across multiple jurisdictions, and should also be kept in mind when multi-national companies consider the composition of their boards.

Relationship between the common law and the Act

Among other provisions, directors’ duties are partially codified in s75 of the Act. However, the common law continues to apply unless it is expressly excluded or in conflict with the Act.1

S75 deals with a director’s duty not to have a PFI in existing or proposed contracts with the company on whose board they serve, or in any matter in which the company has a material interest, and to disclose that interest and recuse themselves from voting on a matter where such PFI arises. Although not expressly codified as such, this captures (among other principles) the “secret profit rule” under the common law. This rule requires that directors must not make secret profits from their position, and must account to the company for any such profits. Specifically, a director should not obtain any financial benefit other than in terms of a contract with the company following full disclosure, or by virtue of their office (for example, remuneration). Such financial benefit will constitute a “secret profit” if the interests of the director and the company are in conflict.

Under common law, a director is required to disclose a financial benefit and recuse themselves from decision-making where a conflict exists. A failure to do so does not automatically invalidate an agreement. Instead, the agreement is voidable at the election of the company, and the director may be required to account for any profit made. While this differs from s75, where an agreement is automatically void but can be ratified, the practical consequences of the non-disclosure and failure to recuse are broadly similar.

In multi-jurisdictional groups, it is important not to overlook potential disclosure obligations arising under common law, notwithstanding the restricted definition of “company” in the Act. The mere existence of a cross-directorship with a foreign company does not, in and of itself, trigger a disclosure obligation. However, disclosure becomes necessary where a matter arises in which the foreign company has a financial interest, or where a director’s fiduciary duties place them in a position of conflict. Whether disclosure is required must therefore be assessed on a case-by-case basis, with reference to the specific transaction, contract or decision under consideration. The consequences of failing to do so are far-reaching – not only for directors themselves, who may face potential liability, but also for matters considered by the board of a company, where transactions or agreements may be voidable.

1 Dimension Data Facilities (Pty) Ltd and Others v Identity Property Co (Pty) Ltd and Others (2022/040174) [2024] ZAGPJHC 1209 (25 November 2024) 2 Ibid.

Andrew Westwood is a Partner and Saleem Firfirey a Senior Associate | Webber Wentzel

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Africa’s private capital market has reached a defining moment. 81 exits were recorded in 2025, representing a 27% year-on-year increase and the second highest annual total on record. Yet even as exit activity strengthens, exit conditions continue to top investor concerns, as cited by 73% of LPs and 62% of GPs polled by the African Private Capital Association (AVCA) for its 2026 Investor Sentiment & Outlook report. The gap between the appetite for liquidity and the availability of traditional exit routes has become a structural feature of the African private capital ecosystem.

Against this backdrop, secondary transactions have moved decisively from the periphery to the centre of liquidity strategies. Fund managers leaned more actively on sponsor-to-sponsor solutions to unlock liquidity, which represented 26% of all exits – another record milestone. In keeping with global trends, the African market is showing growing openness to mechanisms that can provide flexibility when traditional exit routes are constrained. For legal counsel advising on African private capital transactions, the deals are certainly there for the taking. The question is whether the legal architecture is ready to support them.

Valuation

Valuation can be the most contested element of any secondary transaction, and the challenge is particularly acute in Africa. Valuation misalignments were cited as a key market concern by 34% of LPs and 37% of GPs who responded to AVCA’s survey. The absence of deep, liquid comparable transaction data across most African markets means that net asset value is inherently more subjective than in markets where benchmark transactions are plentiful.

As much as standard international valuation frameworks provide a useful starting point, they have real limitations in illiquid frontier market conditions. Currency volatility compounds the difficulty for pan-African funds holding assets denominated across multiple local currencies. The legal consequences of these valuation challenges are significant and underexplored in African legal practice. If an exiting LP is cashed out at a net asset value that is subsequently shown to have been materially incorrect – whether through a GP-commissioned valuation that was overstated or an independent process that failed to account for local market realities – questions of liability, remedy and recourse arise that most existing African fund agreements do not answer.

Questions

Who appoints and instructs the independent valuer, on what terms, and subject to what conflict of interest restrictions? What dispute resolution mechanism applies where an LP challenges the valuation underpinning a secondary transaction? What information rights do LPs hold during the secondary process, given the inherent asymmetry between a GP who knows the portfolio intimately and an LP deciding whether to roll or exit? These are not theoretical questions; they will be live issues in every GP-led secondary that African fund managers pursue as the secondary market matures.

Secondary market

The secondary private equity market, previously limited, is evolving and growing rapidly to allow investors to trade existing fund interests and unlock liquidity. Among GPs who have either offered or considered these tools, GP-led secondaries accounted for 76% and LP-led secondaries accounted for 62%, dominating preferences. This trend tracks with the global statistics on this issue. According to Jeffries Private Capital Advisory, the global secondary market reached US$240 billion in transaction volume in 2025, representing a 48% year-on-year increase.

Themes

Several themes are poised to shape the next phase of market evolution in Africa, including the institutionalisation of secondary markets and the expanding use of structured liquidity solutions. What is less frequently discussed is the documentary foundation required to support this evolution responsibly.

Many existing African fund agreements were drafted at a time when secondary transactions were uncommon in the local market. They reflect the priorities of their era: capital commitment mechanics, investment restrictions and distribution waterfalls, rather than the governance infrastructure needed for a GP-led secondary or continuation vehicle transaction. This is not a criticism of how those documents were prepared; it is just a consequence of market timing. The secondary market has simply evolved faster than the fund agreements designed to govern it.

Guidance

In North America and Europe, this challenge was addressed through the development of industry-wide guidance. The Institutional Limited Partners Association has published principles and model provisions specifically addressing GP-led secondary transactions, continuation vehicle consent mechanics, LP information rights during secondary processes, and the governance standards expected of LPs’ advisory committees when approving conflicted transactions. These standards now form the baseline against which market participants and, increasingly, regulators evaluate whether a secondary process has been conducted fairly.

Evergreen vehicles – valued for their semi-liquid characteristics and long-term capital alignment – are used or planned by 61% of LPs, yet only a third of GPs report offering them a gap that itself reflects, in part, the absence of settled market practice and documentation templates to support these structures in the African context.

The development of Africa-specific secondary market guidelines could similarly be beneficial. Such guidelines would serve a dual purpose: providing GPs with a clear governance framework for conducting secondary transactions and giving LPs confidence that their interests will be protected when continuation vehicles or secondary transfers are proposed. Fund counsel, for their part, have both the opportunity and the obligation to advise GP clients on building secondary optionality into fund documentation at the outset, and not as a retrofit when the fund is already past its investment period.

Final note

The African secondary market is no longer nascent, and the transactional momentum is building. Trade sales and secondary exits are expected to remain the dominant exit routes, with a wider universe of buyers and, particularly, increased involvement from strategic acquirers and financial buyers across Africa. What is needed to meet this trend is a legal and governance framework equal to it, one that manages conflicts of interests with rigour, resolves valuation disputes with transparency, and equips African fund agreements to support the full lifecycle of a modern private capital fund. We can expect this to be an area of increased private capital activity in 2026 as the market matures.

Angela Simpson is a Partner and Lungelo Magubane a Senior Associate | Bowmans

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

Advances in AI and strong earnings from the tech firms have driven the Nasdaq to new highs recently. But with concerns about high valuations, investors are looking for ways to participate in the sector while protecting their downside.

The Nasdaq 100’s tech-led rally has gathered remarkable momentum, with the index rising from roughly 25,000 in early 2026 to multiple record highs, crossing the 29,000 mark for the first time in May. The longer-term picture is equally striking: the index is up 124% over the past five years.

The primary driver of this performance has been the artificial intelligence (AI) supercycle driven by the major hyperscalers, combined with robust earnings from megacap technology stocks, particularly the “Magnificent Seven” – Apple, Microsoft Corp., NVIDIA Corp., Google parent Alphabet Inc., Amazon.com Inc., Meta Platforms Inc. and Tesla Inc.

Strong fundamentals

The potential for continued growth remains strong, as prevailing tech sector fundamentals suggest that today’s market structure differs meaningfully from previous periods of excessive market optimism, with the sustained rally fundamentally supported by real and compounding profitability.

Furthermore, the major hyperscalers continue to generate massive free cash flow, which is the primary funding source for the massive capex budgets driving the AI and data infrastructure build out.

The financial resilience shown in the corporate revenue of the Nasdaq’s main constituent tech companies, despite macroeconomic headwinds, coupled with massive quarterly earnings beats, suggest the rally has more room to run.

Investing in the trend

Offering a viable solution to gain exposure to this investment theme, Investec has launched a structured term product that references the Nasdaq 100 and is linked to the index’s performance.

The Investec ZAR Nasdaq 100 Geared Growth Flexible Investment Note is a three-year and eight-month structured investment that provides investors with exposure to the tech sector, allowing them to participate in any continued AI-led growth while offering capital protection benefits.

“The product creates a structured payoff profile, providing exposure to the growth of the index, multiplied by a participation of 125%, up to a growth cap of 60% over the term,” explains Brian McMillan from the Investec Structured Products team.

This geared effect translates to a maximum return of 75% (125% x 60%) in South African rand (ZAR) over the term, equivalent to a maximum annualised return of 16.5% per annum.

Addressing investor concerns

However, should the outlook change, McMillan says the capital protection feature in the structured product addresses concerns investors may have about the length and durability of AI-driven growth in the tech sector.

“If the index does not perform over the period, investors get 100% capital protection if the investment is held for the full term, provided the index does not decrease by more than 40% on the final valuation date,” elaborates McMillan.

This downside protection on outright exposure offers a significant advantage over direct investments in the market through exchange-traded funds.

As such, with its focus on capital preservation and growth potential, the Investec ZAR Nasdaq 100 Geared Growth Flexible Investment Note may provide a suitable investment proposition for local investors looking to remain invested in tech sector growth stocks, while boosting offshore exposure without drawing on their annual single discretionary allowance (SDA).

Participating in the Investec ZAR Nasdaq 100 Geared Growth Flexible Investment Note requires a minimum investment of R100,000. Applications close on 10 July 2026, and the note will list on the JSE on 16 July 2026. The final valuation date is 7 March 2029.

For full regulatory disclosures, please click here

Anglo American unlocks a copper adjacency at Los Bronces

Growthpoint wants quality, not quantity

Nedbank’s performance looks decent

Optasia has resumed operations in Nigeria

Primary Health Properties is in negotiations around a private hospital joint venture

Schroder European Real Estate is throwing in the towel

Anglo American unlocks a copper adjacency at Los Bronces (JSE: AGL)

Copper is still the commodity that everyone is chasing

Anglo American has announced a joint mine plan with Codelco for the Los Bronces mine in Chile.

The adjacent Andina copper mine creates an opportunity for the two companies to work together, unlocking synergies and making more money for everyone along the way.

According to Anglo, this unlocks at least $5 billion in shared additional value, based on the uplift in production over the next 21 years.

Naturally, this number can technically be whatever anyone wants it to be – it all comes down to the underlying assumptions.

Ghost Bite: The actual value uplift is debatable, but the direction of travel is not – this seems like a sensible approach by the companies. It does remain subject to permits though, so something could still go wrong in the implementation process.

Growthpoint wants quality, not quantity (JSE: GRT)

But the numbers are still enormous at this R60bn market cap fund

Growthpoint has given investors an update on progress made over the nine months to 31 March 2026. It’s a very detailed look at the operations, so buckle up.

The iconic REIT is busy simplifying its portfolio and transitioning from quantity to quality, an important and necessary step in a difficult economy. South Africa has rewarded surgical strategies, not broad exposure. This is driving Growthpoint’s precinct-focused strategy, perhaps learning from the success of REITs who have been more focused.

We are talking serious numbers here, with previously targeted disposals of R3.5 billion for the year ending June 2026. B-grade and C-grade offices are on the chopping block, along with certain other assets. They’ve already sold and transferred R2 billion of assets at a modest profit to book value. Thanks to strong disposal activity, including the 55% interest in the Discovery building for R2.3 billion, they expect disposals of R5.1 billion for FY26 – way ahead of target.

Capital is being recycled into other, more desirable asset classes. This includes the Logistics & Industrial sector. Where it makes sense to do so, Growthpoint redevelops underperforming assets as well, with targeted investment of R1.3 billion in the year ending June 2026. Thus far, they’ve spent R793 million this year (including other capital expenditure).

It sounds like Growthpoint would be happy to pull the trigger on South African deals, as their balance sheet is almost too conservative now. It’s important for REITs to operate in an optimal window when it comes to leverage, especially when the weighted average cost of debt has come down (despite the recent SARB decision). Growthpoint has no problem tapping debt markets, evidenced by an oversubscribed R1.8 billion bond issuance in June 2026 at record-low margins.

One of the exciting projects in years to come is the Cape Winelands Airport, where Growthpoint will oversee Phase 1 of the development and will focus on the ancillary land opportunities thereafter.

The overall South African portfolio has seen vacancies improve from 8.2% to 7.3%. The lease renewal success rate is the highest in more than a decade, while negative reversions have improved from -4.0% to -2.8%. The office sector has been a notable source of improvement (from -9.6% to -7.1%), but I’m sure that is mostly thanks to the disposals of low-quality offices.

To give you an idea of the regional differences, Growthpoint’s office portfolio recorded vacancies of just 3.0% in the Western Cape vs. a massive 18.9% in Gauteng. KwaZulu-Natal sits at just 1.3%. Sure, the extent of the underlying portfolios will make a difference here, but Sandton is nowhere near the crown jewel that it once was.

Importantly, footfall in the retail portfolio increased by 1.2%. Malls are holding their own against eCommerce, at least for the time being. Trading density growth of 3.2% is decent, especially as it accelerated to 4.2% in the March 2026 quarter. Value-oriented formats continue to outperform, so take that into account as you consider your retail exposure.

The V&A Waterfront is the single most important asset in the portfolio, but EBIT was only up marginally year-on-year due to the redevelopment of the Table Bay Hotel. Footfall was up 1.2% and retail sales grew by 5.1%. There’s a significant development pipeline at the property, including more hotels and apartments. Residential sales will contribute to the expected double-digit growth in distributions for FY26.

On the international front, where Growthpoint has exposure to tricky markets like Australia, there’s a lot of talk around initiatives to unlock shareholder value. For now, Growthpoint Australia has reaffirmed guidance for funds from operations this year, despite the general challenges of that market.

I suspect that just about every option is on the table for the global assets. It will all come down to price and the opportunities that present themselves. One area where we know there will be action is Lango Real Estate, which is contractually required to list on a suitable exchange. The London Stock Exchange is the intended destination.

Overall, guidance for the year of distributable income per share growth of 3% – 5% is unchanged. The dividend per share growth expectation of 6.0% – 8.0% is also still in play. But Growthpoint has noted an overall shift towards a more conservative outlook beyond this period.

In leadership news, Norbert Sasse will step down as group CEO on 1 July 2026. Estienne de Klerk will step into the group role.

Ghost Bite: Growthpoint is up 31% in the past year, or 42% on a total return basis. This is one of the many reasons why I prefer putting my own money in REITs vs. a buy-to-let headache.

Nedbank’s performance looks decent (JSE: NED)

Especially in the context of the modest valuation multiple

Nedbank has added its name to the list of banks that have released pre-close updates. For the first five months of the year, headline earnings have been in line with management expectations. This has led to the group affirming its 2026 guidance.

Pre-provisioning operating profit has grown by high-single digits, which is encouraging. This was partially offset by higher impairments and the loss of associate income from Ecobank after they sold that investment. Thanks to share buybacks and other positive factors, it all filters down into growth in headline earnings of “upper single digits” – a reasonable outcome.

The core banking operation is making progress, with net interest income (NII) growth of low- to mid-single digits. Asset growth was in the mid- to upper-single digit range, but a decline in net interest margin took the shine off that number.

Where Nedbank seems to be deviating from peers is in the credit loss ratio, which is sitting in the upper half of the through-the-cycle range. This is worse than what we’ve seen in other recent sector updates. There was a major client default in Business and Commercial Banking that has affected the number, although it’s odd that there can be a client in the mid-market segment of sufficient size to have this effect.

Non-interest revenue managed upper-single digit growth, with insurance income as one of the major boosts.

Expense growth was below mid-single digits. They expect this level of control control to continue for the rest of FY26.

On the corporate front, the NCBA deal in Kenya has received a number a critical regulatory approvals. There are still some boxes to be ticked. Importantly, the offer to NCBA shareholders will close on 10 July, with the results expected to be announced by no later than 21 July.

Ghost Bite: On a P/E of just 7.6x, Nedbank achieving “upper-single digit” growth in headline earnings would put them on a PEG ratio of roughly 1x. Shareholders tend to make money when the valuation is that appealing.

Optasia has resumed operations in Nigeria (JSE: OPA)

But the damage to the investment case has been done

Having listed towards the end of 2025, Optasia promised the market a growth story built around distribution of financial and value-added services in Africa via smartphones.

It all sounded very impressive, with the share price doing well until the end of January. Then the story started to unravel, with considerable insider selling and of course the conflict in Iran as well.

But the real disaster was to come: a suspension of operations in Nigeria for regulatory reasons, along with damaging commentary from telcos about how little of an impact the loss of Optasia’s services was having on their business.

If your operations can shut down for a period of time without anyone really noticing, you have no moat. Without a moat, there’s no justification for a premium valuation.

The good news is that operations have resumed in Nigeria. The damage has been done though, with the share price having shed 31% of its value year-to-date.

Ghost Bite: IPOs are always very risky things to invest in. Even by those standards, this one fell apart incredibly quickly. They have much work to do to rebuild trust in the market.

Primary Health Properties is in negotiations around a private hospital joint venture (JSE: PHP)

There’s no certainty at this stage that anything will happen

Primary Health Properties previously told the market that they were looking at strategic options around the private hospital portfolio.

The company has now had its hand forced by press speculation, confirming that they are in negotiations around using the private hospital portfolio to seed a new joint venture.

Although they refer to “advanced discussions” with a potential partner, there’s no guarantee of anything going ahead. But this didn’t stop the share price from going bananas, up 26% on the day!

Ghost Bite: There’s nothing the market loves more than ignoring the risk of transaction failure. If you’ve ever been involved in dealmaking, you’ll know just how many transactions fall over during the negotiation stage.

Schroder European Real Estate is throwing in the towel (JSE: SCD)

They will execute an orderly wind-downover the next couple of years

Schroder European Real Estate released results for the six months to March 2026. But even more importantly, they are looking to achieve an orderly wind-down of the structure and a return of capital to shareholders.

This has been a terrible performer relative to sector peers, so I’m not surprised. It will take them two to three years to get it done, so this is a good example of the “marketability” discount in action – investors are smart enough to recognise the difficulties and delays in the sale of assets.

The group still hasn’t recognised a provision for the French Tax Authority dispute, despite it being an enormous €14.9 million vs. the current NAV of €151.3 million. Talk about an overhang!

I must note that the NAV fell by nearly 2% year-on-year purely due to valuation pressure in the underlying portfolio, so they have more problems than just the tax.

I had to chuckle at the Chairman’s comments that there’s a shift in investor sentient towards larger, more liquid equities. Sure, but there’s also a shift towards companies that aren’t at risk of losing 10% of their value to a tax dispute…

Ghost Bite: With a total return over 5 years of 7.4% (not per year – in total!), I don’t think anyone is going to miss this one.

Results of previous poll:

Nibbles:

Director dealings:

The CEO and founder of Datatec (JSE: DTC) repriced options over the stock worth almost R220 million. They expire at the end of August 2027. The collar has a put strike price of R91.57 and a call strike price of R121.78. The current spot price is R94.86, so this is giving strong downside protection from current levels.

A senior exec at Quilter (JSE: QLT) sold shares worth around R5.4 million.

The Chair of Gold Fields (JSE: GFI) bought shares worth R275k.

Salungano Group (JSE: SLG) released a trading statement for the year ended March 2026. They expect HEPS to jump to between 50.59 cents and 51.11 cents, vastly higher than 2.62 cents in the comparable period. Results will be released before 30 June 2026.

Crookes Brothers (JSE: CKS) released an updated trading statement. We already know from the initial trading statement that the year ended March 2026 was awful, with lower earnings across all group segments. Farming is incredibly tough, with their macadamia business described as being “commercially unsustainable” at current prices. The headline loss will be 167.2 cents, much worse than the guidance in the initial trading statement (of HEPS being between 2.35 cents and 27.85 cents). One of the reasons for this difference is deferred tax balances in Mozambique. Either way, it’s a disaster.

Greencoat Renewables (JSE: GCT) is moving ahead with the next tranche of share repurchases. They’ve completed €25 million of a €100 million share buyback programme. They are now commencing the next €25 million.

Wesizwe Platinum (JSE: WEZ) suffered a cyberattack in December 2024 that led to huge delays in financial reporting. As part of the recovery, they are busy with a major SAP ERP system implementation. They had planned a go-live in June 2026, but they are going to miss that deadline due to how long it took to catch up on their financial reporting. They’ve made a lot of progress on the implementation, but no new go-live date has been given.

Having moved its listing from the AltX to the Main Board of the JSE, Africa Bitcoin Corporation (JSE: BAC) has now executed a similar migration of its listing on the Namibian Stock Exchange. It wouldn’t make sense to be on the development board on one exchange and the primary board on the other.

PSG Financial Services (JSE: KST) has decided to withdraw their listing on the Stock Exchange of Mauritius (SEM). This will leave them with listings on the JSE and Namibian Stock Exchange only.

Omnia Holdings (JSE: OMN) received approval by the SARB for the special dividend of 280 cents per share. It will be paid on 8 June 2026.

Attacq’s precinct-focused approach is still paying off

FirstRand’s business is performing well – outside of the UK at least

Grindrod’s Port and Terminals business is the highlight of this period

Labat Africa declares a dividend and promises shareholder engagement

Sibanye-Stillwater gives investors plenty to chew on at the Capital Markets Day

Vunani has swung into profitability, with Fairheads as the anchor of the story

Attacq’s precinct-focused approach is still paying off (JSE: ATT)

The pre-close update looks encouraging

In Attacq’s pre-close update for the year ending June 2026, they gave performance highlights based on the 10 months to April 2026, as well as the most important news of all: they are on track to achieve the guided growth in distributable income per share of 11% to 14%.

This is being driven by factors like a 4.8% increase in the weighted average trading density in the portfolio, along with solid occupancy rates. They’ve even managed foot count growth of 1.5% on a rolling 12-month basis, despite all the risks of eCommerce adoption!

Attacq always has significant development projects on the boil. Waterfall City still offers plenty of opportunity across different asset classes. They believe in the precinct strategy and they aren’t afraid to take on development risk.

For example, the Gateway East office development has only signed leases for 37.6% of Gross Lettable Area thus far, with another 27.5% awaiting signature. It’s difficult to fully de-risk these types of developments, unlike in the logistics space where warehouses are often built to client spec based on long-term leases. But even among the warehouses, Attacq takes on some speculative developments for more generic buildings.

As a sign of the times, they are also busy with data centre developments in the precinct!

The balance sheet remains in good health, with a gearing ratio of 25.1% vs. 25.3% as at June 2025.

Ghost Bite: The collapse in Gauteng infrastructure creates opportunities for property funds to focus on making things as good as possible in a particular area. Attacq is one of the best examples of this strategy in action.

FirstRand’s business is performing well – outside of the UK at least (JSE: FSR)

The group is doing well in SA and Africa

FirstRand has given shareholders more information on the performance for the year ending 30 June 2026. As most companies have done, they kicked off the announcement by reminding investors of the macroeconomic disruption of the past few months.

But the biggest headache of the period by far had nothing to do with oil (or even Iran). The FCA UK motor redress scheme was the shock for FirstRand investors this year, with a further provision of £510 million raised during the year. This takes the total provision to £750 million.

This provision means that normalised earnings will drop by below 4% and 9%, with Return on Equity (ROE) below the bottom end of the targeted range.

Naturally, the next thing they want you to do is strip out this most unfortunate event. If you do that, they are in line with guidance for both growth in normalised earnings and ROE.

FirstRand is getting out of the entire UK business, so perhaps just ignoring it and moving on is the right approach for investors. Heavy-handed regulators in low-growth economies do no favours for their countries, with such authoritarian stupidity as common in Europe or the UK as it is in South Africa.

Focusing on the continuing operations, we reach the section of this announcement that is heavy on narrative and light on numbers, as is usually the case at the banks.

Thanks to strong growth in advances, net interest income (NII) is slightly higher than guidance, a pleasant surprise given the overall caution in the market among borrowers. Wesbank has been a major driver here, as has the rest of Africa. The credit loss ratio is expected to be at the lower end of the through-the-cycle range, so that’s a further boost to the lending business.

The non-interest revenue (NIR) side of the group is usually a strength at FirstRand, with this period once again delivering a positive performance in trading, investment and other sources of income. Interestingly, the private equity business had fewer realisations (crystallised sales of assets) in the second half vs. the first half.

Operating expenses are slightly higher than guided, with a few major projects taking them above where they wanted to be.

Results are due for release on 10 September 2026, at which time we will have all the details.

Ghost Bite: FirstRand can officially be added to the list of local companies that should’ve just focused on regions they fully understand.

Grindrod’s Port and Terminals business is the highlight of this period (JSE: GND)

This is the power of a focused strategy

After the simplification of Grindrod’s group, they are changing their approach to their financials. The segments going forwards will be Port and Terminals, Logistics and Group, so all the non-core stuff will be reported in Group.

In an update for the five months to May 2026, Grindrod highlighted a jump in earnings at the Port of Maputo of 23.3%. EBITDA margin in the Port and Terminals segment more than doubled (up from 15% to 38%).

It can’t all be good news, of course. The Logistics segment saw its EBITDA margin decline from 20% to 15%.

In the Group segment, they’ve benefitted from the Marine Fuels settlement with insurers, leading to a reversal of R90 million worth of credit losses.

From a balance sheet perspective, Grindrod’s net debt at the end of May was R38 million, a significant move vs. net cash of roughly R0.7 billion as at December 2025.

Looking at the underlying operations, the Port of Maputo’s dry-bulk terminal saw an increase in volumes from 5.2 million tonnes to 6.8 million tonnes. The Maputo Car Terminal enjoyed a 23% increase in volumes.

The Matola terminal wasn’t so lucky, with export volumes down 8% due to adverse weather (and overall volumes down 3%).

In South Africa, there were highlights at the Navitrade facility at Richards Bay and the Maydon Wharf multi-purpose terminal in Durban, up 46% and 42% respectively. But the other port facilities at Richards Bay were down year-on-year.

Ghost Bite: Simplification is a strategy that pays dividends – literally. Grindrod’s total return over 3 years is 225%!

Labat Africa declares a dividend and promises shareholder engagement (JSE: LAB)

This should be interesting!

Labat Africa has been a fascinating story. They’ve pivoted in the unlikeliest of ways, from cannabis to technology distribution. The group has changed completely, including the people involved, so a change of name is probably justified here as well.

The name stays the same for now, but at least there’s a dividend to show shareholders that there’s some value here. Incredibly, with shares changing hands at 3 cents each, there’s a dividend of 1 cent per share! You won’t see a yield like that every day.

This means that many of the investors who bought their shares in recent times at 1 cent each will be getting their entire investment back as a dividend. This is just one of the many crazy potential outcomes in penny stock land.

Labat has also promised a “comprehensive investor engagement and shareholder roadshow programme” – and I do hope that Unlock the Stock will be part of it. Let’s wait and see.

Ghost Bite: There are a number of “boring” companies on the JSE. Labat Africa certainly isn’t one of them!

Sibanye-Stillwater gives investors plenty to chew on at the Capital Markets Day (JSE: SSW)

Capital allocation is going to be key to the next phase of the journey

Sibanye-Stillwater hosted a capital markets day on Tuesday. This gives you a lovely opportunity to dig through the slides and learn more about the group.

The podcast I recorded with CEO Richard Stewart in May is just as relevant now as it was then. It gives you a highly efficient way route to understanding the strategy of the group. Listen to it below or check out the full transcript here.

Among many other things, it will help you understand what they mean at Sibanye when they talk about contiguous assets, a concept that comes through strongly in the presentation.

Perhaps the strongest concept of all is that Sibanye enjoys genuinely world-class PGM assets in South Africa, with the world taking a far more favourable view on the long-term relevance of these metals.

Along with the gold operations and the profits being generated by the broader group as well, this is driving an overall strategy at Sibanye-Stillwater that should see a reduction in debt and the payment of solid dividends to investors.

There’s far too much from the capital markets day to cover in detail here, particularly as Sibanye is such a large group. My strong recommendation is that you listen to the podcast and flick through the slides from the event here.

If you are a DRDGOLD shareholder, then take note that the company also presented at the Capital Markets Day. This is because Sibanye-Stillwater is the controlling shareholder. You’ll find that presentation here.

Ghost Bite: Capital Markets Days are beautiful things. I want to see more of them from more companies on the JSE!

Vunani has swung into profitability, with Fairheads as the anchor of the story (JSE: VUN)

They still have a number of marginal underlying businesses

Vunani committed one of the sins of financial reporting: an updated trading statement on the same day as the release of financials. I’ll never understand how this goes wrong in practice, as trading statements are meant to come out well ahead of earnings.

At least they had released an initial trading statement that wasn’t far off the final numbers, which is more than we can say for some companies on the JSE that go from initial trading statement to full results in the space of a few hours.

For the year ended February 2026, Vunani achieved a swing from losses to profits.

Revenue and insurance revenue climbed 17%, while results from operating activities increased 51%. HEPS was the real star of the show, moving from a headline loss per share of -2.8 cents to HEPS of 10.2 cents.

They are paying almost all of this out as a dividend, with 10 cents per share declared for the year. The dividend in the prior year of 35 cents per share is an anomaly.

The significant jump in the fund management segment’s revenue (from R136.1 million to R177.1 million) must be viewed in the context of the merger with Sentio Capital Management. They’ve highlighted underlying growth in funds under management as well, but you can’t extrapolate that growth rate as being a reflection of business as usual.

If you’re looking for a growth highlight, you’ll find it in the insurance segment as the largest contributor (R335.2 million in revenue, up 21%). But profitability remains marginal, with profit of only R5.5 million (vs. a loss of R3.6 million in the prior period).

The asset administration segment (Fairheads) is the anchor of the group, but showed very little growth with revenue of R215.5 million. Profit is a different story though, up from R34.6 million to R47.5 million.

Ghost Bite: Vunani is still a volatile group built around Fairheads as the most dependable operation. It will be interesting to see how the increased scale in the fund management business comes through in future periods.

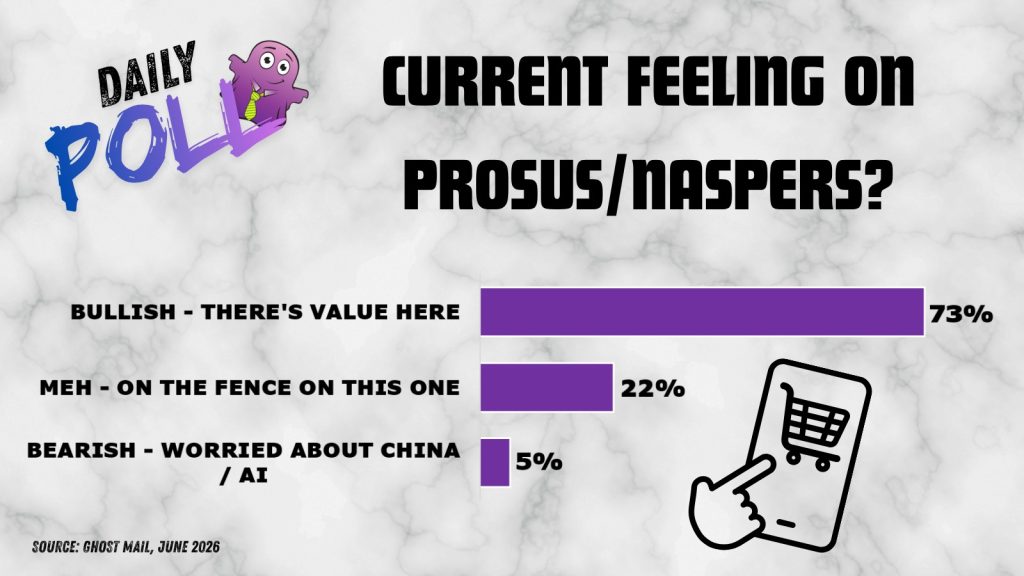

Results of previous poll:

Nibbles:

Director dealings:

An executive director of Trematon (JSE: TMT) sold shares worth R265k. Odd timing given the underlying value unlock strategy that is in progress.

The CEO of Choppies (JSE: CHP) bought shares worth R112k.

ASP Isotopes (JSE: ISO) announced that Renergen has entered into its first take-or-pay contract to supply contained helium to an Asian industrial gas company. They are targeting the commercialisation of Phase 1 of the Virginia Gas Project in the third quarter of 2026. This is a five year take-or-pay contract priced at $600/MCF of helium, covering roughly 15% of the expected production of Phase 1. Phase 2 is where the real money happens (we hope), with the project being 13 times larger than Phase 1! This is where the substantial funding from partners like the US DFC and Standard Bank will be utilised.

Equites Property Fund (JSE: EQU) noted that GCR Ratings has affirmed the credit rating of AA-(ZA) and A1+(ZA) for the long- and short-term ratings respectively. Among many other factors, this considers the impact of UK asset disposals and the logistics development pipeline in South Africa.

Santam (JSE: SNT) announced the appointment of Michael Fleming as an independent non-executive director. Fleming is the ex-CFO of Clicks and Tiger Brands, so there’s no shortage of experience here!

Grindrod (JSE: GND) announced that Raymond Ndlovu has been appointed as Chairperson, while Hubert Brody will be the Lead Independent Director.

There is growing talk in investment markets that the AI “bubble” may soon burst. However, evidence suggests those predictions are misplaced, although investors should remain cautious about risks.

In market terms, a bubble refers to irrational pricing. It happens when hype overshadows reason. Prices reflect investors’ urgency to buy because they fear missing out. This hype drives prices even higher, reinforcing positive sentiment in a self-perpetuating loop. Bubbles occur when asset prices far exceed sustainable value. Previous examples include tulip prices in the 1600s and tech stocks in the early 2000s.

Some analysts believe this is now happening with artificial intelligence (AI) shares. I am not convinced – as it is hard to foresee a world where AI becomes less relevant in our daily lives.

There have been many examples where analysts suggested stocks were irrationally overbought for years until they accepted higher prices as normal – think Naspers or Capitec a decade ago. Often in those periods analysts fail to appreciate that the market valued a stock or sector based on future potential earnings that had not yet materialised. Mr Market is, by and large, remarkably efficient at pricing assets and predicting trends.

The 2000 dot-com crash serves as a lesson from the past that informs the current market. In the early 2000s, there were naysayers who wrote the obituary for a tech industry that – at the time – looked like it had died before it had even matured. A few analysts were saying, “We told you so. This was all hype, all bubble, no substance.” But hindsight shows us that the market was not irrational in valuing highly the companies that would ultimately benefit from widespread Internet adoption.

Instead, the dot-com crash was simply a case of not all tech companies becoming winners. There’s a lesson there for today’s AI companies and today’s investors.

Markets tend to be remarkably resilient and efficient over time. The dot-com crash simply preceded an era of enormous stock market growth. Many of the companies that succeeded in the Internet age drove this. Were there failures? Of course. After the correction, many analysts pointed to the irrational behaviour of companies that were too eager to build the Internet’s infrastructure. This included laying the same fragile fibre-optic undersea cables that now enable our global connectivity. At the time, that infrastructure investment might have looked excessive. In hindsight, it proved essential. The rapid growth of AI may follow a similar path, but unlike the early internet, it will depend heavily on the infrastructure required to support it at scale.

The long-term market correction that followed the 2000s dot-com bubble highlighted the importance of staying calm and avoiding panic selling. It also showed why a diversified and disciplined risk management approach will always beat jumping onto investment bandwagons or trying to “time the market”.

Investors should be cautious yet open-minded about the current AI bull run. Will there be pain from AI? Yes. Some companies will disappoint. Are valuations stretched? I would agree, but traditional accounting isn’t great at measuring technology company value.

Like AI, other assets – such as cryptocurrencies and commodities – also face “bubble” warnings. But labelling everything a bubble is not helpful. It simply creates fear among investors. They then see those industries or stocks as irrationally priced. This affects their behaviour, and so they stay on the sidelines.

Unsurprisingly, bubbles and subsequent busts get a bad rap. But arguably the optimal amount of bubbles and busts over time is not zero. Society needs them to occur. If you consider truly societal game-changing technologies – railways, air travel, the Internet – it’s clear that we need periods where people lose their short-term sensibilities, so that the long-term infrastructure can be built that moves societies forward.

So instead of worrying about bubbles, investors should take a pragmatic, long-term view of the market. AI stocks may look expensive today based on fundamentals. But how relevant are those current fundamentals over the long term? Many of these companies are building infrastructure for tomorrow’s AI-powered world – not just digital platforms, but the underlying systems needed to make them work in the real world.

What is often overlooked in this discussion is that AI is not just a digital story, it is also a physical one. Like the Internet era before it, which required massive investment in fibre-optic networks and data infrastructure, AI’s expansion depends on reliable and scalable energy supply. Data centres, cloud computing and advanced chip manufacturing are all highly energy-intensive.

Recent disruptions in global energy markets have shown how quickly constraints in supply can ripple across industries and economies. While much of the current debate focuses on valuations, what happens next for AI will increasingly depend on whether energy is available, reliable and affordable.

The AI rollout assumes that data centres will have a stable, continuous supply of energy to keep these facilities cooled and running efficiently. Any serious energy disruption could prove disastrous for AI – and for markets in general. Market shocks, like the current oil price shock, can have far-reaching knock-on effects. For investors, this reinforces the importance of diversification – especially when outcomes are harder to predict.

We believe that investment in companies developing tomorrow’s AI infrastructure is still a sound move, but as with previous technological shifts, the winners will not only be defined by innovation but by their ability to operate in practice, including the infrastructure that powers it.

Keen for more? Listen to the recent podcast on this topic here:

Disclaimer

Satrix consists of the following authorised Financial Services Providers: Satrix Managers (RF) (Pty) Ltd and Satrix Investments (Pty) Ltd. The information does not constitute financial advice. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Gold Fields is trying to allay fears about the Tarkwa mine

A slower quarter at Standard Bank, but a positive outlook

Encouraging signs at Exxaro (JSE: GFI)

Detailed interim results will be interesting

Exxaro has released a pre-close message for the six months to June 2026. This is part of the broader capital markets day hosted by the company.

Exxaro has seen an increase in coal export, iron ore fines and manganese ore prices over the past year. Coal export prices spiked recently due to the Iran conflict and a switch from gas to thermal coal by many international users. Spot prices have since moderated, based on expectations of the conflict ending, but the spike obviously helped Exxaro on a short-term basis.

For this interim period, they expect coal production to be up by 10% and sales to increase by 6%. Export sales were up by 15%, so it was domestic sales that dragged that number down. Eskom demand is stable, while sales to the ferrochrome market and ArcelorMittal (JSE: ACL) were down.

The export business was assisted by an important 7% increase in performance at Transnet Freight Rail.

Capex in the coal business is expected to be 69% higher in this interim period, so they’ve had some significant capital replacement projects to execute. They expect capex for FY26 to be in line with previous guidance of between R4 billion and R4.5 billion.

Exxaro is also pushing hard in their renewables business, with construction of the Karreebosch wind farm in progress. They are also busy acquiring the operating assets of Acciona Energia, giving them more wind and solar power. Exxaro’s mix of legacy and renewable energy sources is particularly unusual.

The overall story is one of consistent full-year guidance in key areas, as well as some promising underlying metrics for the interim period. We will only know for sure when interim results are released in August.

Ghost Bite: Working through the detailed presentations from a capital markets day is always a good idea. You can find them here.

Gold Fields is trying to allay fears about the Tarkwa mine (JSE: GFI)

Media reports have suggested that there is a significant risk here

Various recent reports in the media have suggested that Ghana is considering a change of control of the Tarkwa mine, where the lease held by Gold Fields expires in 2027.

This is a critical asset for Gold Fields, accounting for roughly a fifth of the group’s total production!

Gold Fields responded to the media reports with a SENS announcement noting that negotiations with the Government of Ghana are in process, regarding the terms of the mining lease renewals. An early application for renewal of the leases had already been submitted in 2025, so this has been going on for a while.

Ghost Bite: Nothing is ever certain when you’re dealing with African governments. It wouldn’t surprise me at all if there’s at least some truth to the media speculation. Gold Fields will hopefully manage to get this one across the line.

A slower quarter at Standard Bank, but a positive outlook (JSE: SBK)

Periods of geopolitical upheaval are difficult for lending businesses

Standard Bank’s voluntary trading update for the five months to 31 May 2026 covers a volatile period in the market, where inflation expectations spiked thanks to the oil price.

We also saw a small rate hike by the SARB, as well as credit rating agencies recognising the progress made in South Africa.

In summary, it hasn’t been a boring time in the world!

If you’re hoping for precise numbers in this update, you’ll be disappointed. They are heavy on narrative and light on actual details, other than an overall message that earnings growth has “moderated” vs. the 12% earnings growth in the first quarter of the year. In other words, the second quarter was a slower growth rate, but we don’t know to what extent.

Africa is a critical part of the Standard Bank investment case. West and East Africa did well, more than offsetting a weaker performance in the South & Central Region.

It sounds like net interest income (NII) came under pressure due to lower average rates and particularly competitive environments in areas like home loans. Impairments were lower though, so that should drive a better result net of impairments.

Non-interest revenue (NIR) was boosted by trading revenue, which isn’t a surprise during a volatile period. They’ve also flagged strong momentum in the Insurance and Asset Management business.

Cost growth was in line with revenue growth, so there’s no sustainable margin uplift story to tell here. With impairments coming in lower though, we still might see a better percentage increase in earnings relative to revenue.

The balance sheet remains in excellent health, with a CET1 ratio of 13.2%. This measures the extent of equity on the balance sheet. A higher CET1 ratio is less risky for investors, but also makes it harder to generate a strong Return on Equity (ROE) as there is simply more equity running around.

For now, Standard Bank has left full-year guidance unchanged, while noting that this quarter put a dent in client confidence and related activity. The market is expecting these issues to dissipate, so Standard Bank remains positive on the full-year picture for now.

Ghost Bite: With Standard Bank’s share price up 46% in the past year and 13% year-to-date, the market hasn’t been concerned about the global geopolitical picture. Positive sentiment around Africa is carrying this share price.

Results of previous poll:

Nibbles:

Director dealings:

The crew at Vukile Property Fund (JSE: VKE) are cashing in on a fantastic run in the share price. Top execs, including the CEO and CFO, sold share awards (in excess of the taxable portion) worth a total of over R40 million. I must commend the company on the brilliant layout of their announcement, which makes it very easy to see the taxable vs. non-taxable portion. This should be the industry standard!

The CEO of SA Corporate Real Estate (JSE: SAC) sold only the taxable portion of a share award, but the same can’t be said for a few other execs who sold shares worth R4.7 million (including their taxable portions).

Good news for Pan African Resources (JSE: PAN) investors: the acquisition of Emmerson Resources has been approved by the shareholders of that company. Court approval in Australia has also been obtained, so Pan African has now been admitted to the official list of the Australian Stock Exchange (ASX) as well. Trading on a normal settlement basis on ASX will comment on 2 July 2026.

Eastern Platinum (JSE: EPS) is in the market for a new CFO, as Wylie Hui has resigned with effect from 10th July 2026. He will assist during a transition period for whoever the new CFO will be.

Quilter (JSE: QLT) is busy with a share buyback programme of up to £100 million. For context, the group market cap is R57 billion, so this is around 4% of the market cap. Thus far, they’ve repurchased £32 million in shares on the London Stock Exchange and £8 million on the JSE.

Mantengu (JSE: MTU) has released an updated trading statement that reflects a headline loss for the year ended February 2026 of 90 cents. To add further insult to the ridiculous situation that happened last year, the JSE has also censured Merchantec Capital for releasing Mantengu announcements that were found to be “speculative, unverified and lacking the required degree of specificity and precision”. As I was one of the people who Mantengu threw mud at in the hope that something would stick, I 100% support this decision. Lacking in precision is probably the nicest way to put it. Even Merchantec’s attempts to get the company to retract the announcements didn’t prevent this censure, giving the entire market a reminder of the responsibility carried by Sponsors and Designated Advisors who release SENS announcements on behalf of companies.

If you are a shareholder in Afine (JSE: ANI), the REIT that has a portfolio of fuel forecourts, then be aware that the company has announced the reinvestment price for the dividend reinvest alternative. Shareholders are able to reinvest up to 25% of their dividend in the company at 437.89 cents, calculated as the 30-day VWAP minus the gross dividend.

As a reminder of how dangerous the mining sector still is, Harmony (JSE: HAR) reported a tragic loss-of-life incident at Moab Khotsong mine. This was due to a fall-of-ground incident.

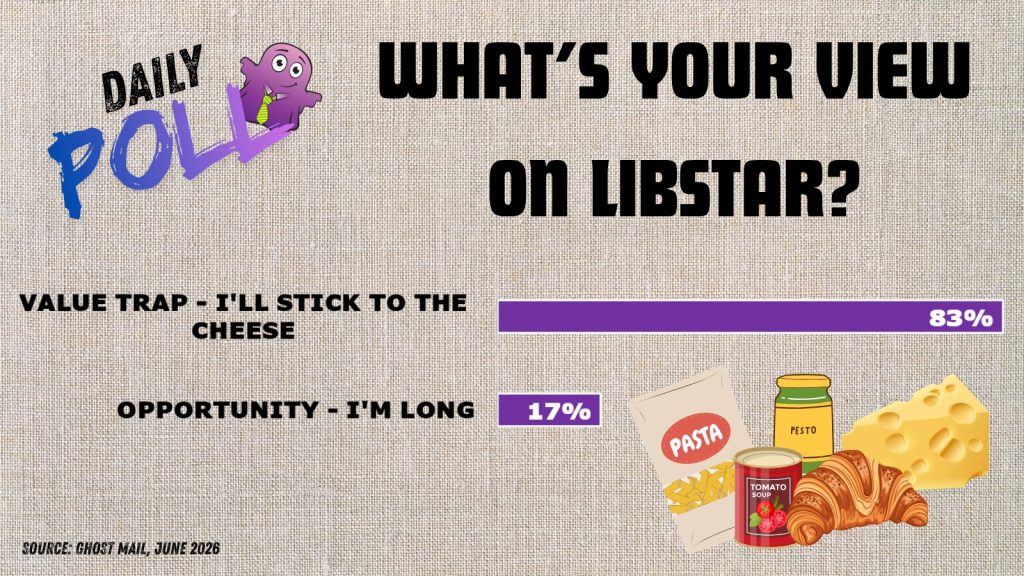

Datatec crystallises some of the value in Westcon International

The Heriot family is putting more assets into Heriot REIT

Prosus / Naspers gives us a peek behind the curtains at earnings

Datatec crystallises some of the value in Westcon International (JSE: DTC)

A special dividend of over R7 billion is on the horizon

Datatec shareholders have been thoroughly enjoying a value unlock strategy by the company over the past few years.

Through a combination of solid performance in the underlying businesses, as well as clever disposals of assets (leading to special dividends to shareholders), the total return to shareholders over 5 years is an insane 584%!

There’s another special dividend coming soon, as Datatec has attracted an investor in Westcon International.

Westcon is the part of the group that is primarily focused on technology distribution, which means they are constantly looking for products that offer decent margins alongside the ability to generate lucrative volumes.

If you’ve been following the mess at Bytes Technology Group (JSE: BYI), you’ll know that being too focused on distributing Microsoft products makes you a sitting duck for that giant to reduce distribution commissions. Diversification is very important in this space, with areas like AI and cybersecurity offering opportunities for distributors in search of better margins.

General Atlantic clearly likes the diversification story, as they are investing a total of $400 million in Westcon. $375 million is in the form of debt that will be used to refinance a shareholder loan from Datatec. $25 million is an equity investment, with General Atlantic acquiring 5% in Westcon from existing shareholders.

If you add in the effect of warrants, they will hold 8.7% immediately after the deal closes, with the ability to increase this over time depending how the warrants pan out.

Together with existing cash on the Westcon balance sheet, the net impact is that $434 million will flow up to Datatec shareholders in the form of a special dividend. This is roughly R7.1 billion, or approximately one-third of the Datatec market cap!

Something to keep in mind is that Datatec’s interest costs will go up after this, as they are replacing internal funding with external debt priced at 9% per annum (and maturing in six years).

This is a Category 2 transaction, so shareholders won’t be asked to vote. They certainly showed their support in the share price though, with Datatec closing 5.9% higher on the date of the announcement.

Ghost Bite: Management teams who complain about a persistent discount in the share price have two choices. They can either keep complaining without doing anything about it, or they can crystallise value further down in the structure and demonstrate the discount in action. Datatec follows the latter approach, to the benefit of all its shareholders.

The Heriot family is putting more assets into Heriot REIT (JSE: HET)

Interesting deal, but pity about the tightly held shareholder register

Heriot REIT announced the acquisition of 75% of Katleho Property Investments (KPI) from two entities that are part of the Heriot family structure. One of the entities already holds 89.07% in Heriot REIT, reminding us just how tightly held this share register is.

The portfolio consists of three office parks in Gauteng. We are at an interesting point in the cycle for both Gauteng and office properties in general. To sweeten the deal for minority shareholders in Heriot, the properties are being acquired at a 20% discount to net asset value (NAV).

When you hear something like that, the first thing you need to do is check how the assets are being paid for. If it’s a share-for-share deal, then a discount to NAV is all relative. In other words, if the shares in Heriot are being issued at a similar discount, then it all comes out in the wash.

The good news is that the NAV as at 31 December 2025 was approximately R22.90 per share. These shares are being issued at R23 per share. Although that NAV is out of date by six months, it seems as though the acquisition is at a significantly higher discount to NAV than the issuance.

The deal is worth R129 million, which is very small in the context of Heriot’s market cap of nearly R7.4 billion. Even though this is a related party transaction, it’s too small to even trigger the requirements for a “small related party transaction” under JSE rules.

But because itinvolves the issuance of shares to a related person, it falls under the ambit of the Companies Act and requires a special resolution by shareholders.

Ghost Bite: Heriot has extremely thin trade in its shares. If the company has any plans to do something about that and unlock liquidity, related party deals certainly won’t get them there.

Prosus / Naspers gives us a peek behind the curtains at earnings (JSE: PRX | JSE: NPN)

The numbers are up, but will it be enough to shift sentiment?

Within the Naspers / Prosus stable, it feels like they’ve been putting most of their effort into telling the Prosus investment story on the global stage. I’ll therefore start with Prosus when dealing with the results of this duo. As a reminder, Prosus is a subsidiary of Naspers.

In the year ended March 2026, Prosus delivered over $7.3 billion in revenue and $1.1 billion adjusted EBITDA in what they now call Ecosystem (formally called eCommerce). Most importantly, each of the underlying ecosystems is now profitable, which is key to the group’s overall “Tencent plus” strategy. In other words, they want the market to place meaningful value on the group excluding Tencent.

Thanks to this result, core HEPS from continuing operations for the N shares is expected to increase by between 19% and 28%. Taking out the “core” adjustments, HEPS from continuing operations for the N shares is up by between 6.7% and 15.7%.

A critical difference is that core HEPS excludes fair value investment movements within Tencent’s earnings. Tencent has acted as a source of venture capital in the Chinese tech market. Results have been mixed, especially as sentiment towards Chinese assets has been negative recently

Here’s a reminder of how closely correlated Tencent is to Prosus, with a view on the ADRs (American Depository Receipts – i.e. both measured in USD) of both companies over 5 years:

The businesses that are only in Naspers (and not Prosus) are too small to make a significant difference to the group, even though this includes the entire Takealot stable! At Naspers, the core HEPS move is between 20.8% and 27.8%, while non-core is between 8.3% and 15.3%.

Both companies are expected to release results on Monday, 29th June. The market will pay plenty of attention to them.

Ghost Bite: I remain long Prosus as an ex-US tech platforms play.

Results of previous poll:

Nibbles:

Director dealings:

To “rebalance their portfolios” (rather than because of a need to cover taxes), the CEO and CFO of Lewis (JSE: LEW) sold shares worth nearly R7.9 million in total.

An associate of a prescribed officer of Insimbi Industrial (JSE: ISB) bought shares worth R2.6 million. There’s been a lot of movement on that share register recently!

The company secretary of Mr Price (JSE: MRP) sold shares worth just over R1 million.

Castleview Property Fund (JSE: CVW) is an extremely tightly-held stock that rarely changes hands. Those who are on the register are smiling though, as the final dividend per share for the year ended March 2026 is 90.2% higher than the prior year! Full results are due on 26 June.

Sebata Holdings (JSE: SEB) has renewed the cautionary announcement regarding a potential disposal of assets. In any event, the shares are suspended from trading at the moment.

Stefanutti Stocks (JSE: SSK) announced that Zanele Matlala is retiring as chairman of the board, having served as a director since 2012. Howard Craig will replace her as chairman.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")