When lunch needs a payment plan, something’s gone sideways. Klarna’s rollercoaster ride through the American dream is a cautionary tale with extra guac.

Never heard of Klarna? That’s only because they haven’t quite made it to the southernmost tip of Africa yet. I only really know about them because my social media feeds have recently been flooded with memes of Jenga towers built out of burritos. Obviously, I needed to know what that was about. When I dug a little deeper into this tempting rabbithole, I discovered that a company I had never heard of before was suffering massive losses because they were making it easier for consumers to finance their takeaway orders. Colour me intrigued.

Klarna is the Swedish fintech that turned checkout into a check-you-later. At the core of their model is something called “buy now, pay later” (BNPL). If you’ve ever used PayJustNow in South Africa, then you’ve had a taste of what this is. It’s essentially a payment option that lets shoppers walk away with the goods today and settle the bill in bite-sized, interest-free instalments, spaced a few weeks apart. Or, if they prefer, they can pay the full amount within 30 days. For bigger purchases, Klarna offers longer-term financing through its banking partner, WebBank.

It sounds like a credit card, but it isn’t. In fact, Klarna proudly positions itself as the antidote to them, calling itself “the global leader in the generational shift away from credit cards.” This is another way of saying: debt, but with better UX.

Founded in Stockholm in 2005, Klarna quickly became a national fixture in its local market. In 2024, 7 out of 10 Swedish consumers claimed to have used Klara to fund an online purchase in the last year. Buoyed by hometown success, Klarna set its sights on conquering a new market – one where consumers were under pressure, debts were stacking up, inflation was running rampant and paychecks weren’t stretching quite as far as they needed to. The perfect environment for a business that makes money out of people going into debt.

South Africa? No, actually. The United States of America.

The difference between biting off and chewing

Klarna touched down in the United States in 2015, setting its sights on a market ten times the size of Sweden’s and infinitely more addicted to shopping. It got off to a flying start by landing a coveted partnership with Macy’s and promptly made the US its top priority for growth. Back home, Swedish officials beamed with pride and exchanged congratulatory handshakes. That same year, the country’s Minister of Enterprise dubbed Klarna one of the nation’s “five unicorns” – shorthand for startups that had made it big on the global stage.

But the fairytale couldn’t last. In 2021, Klarna’s valuation hit a sky-high $45.6 billion based on a funding round in the frothiest of markets. By July 2022, it had plunged 85% to $6.7 billion after raising $800 million in a subsequent (and far more brutal) funding round that mirrored the tech sector’s broader reckoning. Klarna posted a$580 million loss in the first half of that year and later laid off about 100 staff members to stem the bleeding.

Still, the company kept one eye on Wall Street. Klarna had been preparing to go public in the US, eyeing a $15 billion IPOin April 2025; about one-third of its pandemic-era peak. But that debut was put on ice amid fresh uncertainty: a trade war between the US, Canada, and Mexico, not to mention some uncomfortable math around rising defaults.

By the first quarter of 2025, Klarna’s user base and revenues were still climbing, but so were its losses. Net losses doubled year-over-year, and consumer credit lossessurged 17% to $136 million. More people were signing up (and racking up debt), but fewer people were making their repayments. The American dream wasn’t quite panning out as expected.

Not for Klarna, anyway.

Debt-to-your-door

Across the board, BNPL borrowers are slipping behind on their obligations in the United States. According to a recent LendingTree survey, 41% of BNPL users admitted to making late payments in the past year. That number is up from 34% the year before. The more worrying statistic – and the one that really gives you an insight into what’s happening to the average American consumer – is that over 25% said they’d used BNPL to buy groceries. That’s not a typo. People are financing apples and cereal. Two years ago, the percentage of people doing that was just 14%.

So it’s not just a Klarna problem, it’s a symptom of a stretched consumer. In this proverbial coal mine, Klarna is the woozy-looking canary. US household debt climbed by $167 billion in Q1 to an all-time high of $18.2 trillion, according to the New York Fed. Credit card balances and auto loan debt dipped slightly (post-holiday normalcy) but student loan delinquencies exploded from under 1% to nearly 8%, as the Trump administration ramped up enforcement on federal borrowers.

Klarna may not have foreseen this challenging environment, but their strategy didn’t really help them much either. First, they booted Affirm from Walmart to become the retail giant’s BNPL provider of choice, and then they teamed up with DoorDash. If I were to draw a South African parallel, you would have to imagine Checkers and Mr Delivery allowing people to finance their groceries and takeaways through PayJustNow. The problem becomes obvious when the repayment isn’t made. How does a company plan to repossess a $15 pizza that was financed last month?

What also doesn’t help is the fact that Klarna doesn’t set a minimum credit score to qualify for its finance products. There also isn’t a predetermined credit limit per customer. According to the FAQs on their website, they may look at a new customer’s credit report as a whole before making a decision, but since there is no minimum qualifying score to get in, there’s a chance that more than a few uncreditworthy spenders are getting access to financing.

The idea that fast food now comes with a repayment plan might sound like a punchline, but it’s actually a major red flag. When short-term credit becomes essential for life’s smallest purchases, you’re not looking at innovation – you’re looking at distress.

Not just an American issue

Klarna’s troubles are a reflection of a much larger, more systemic issue: the softening, stretching, and slow unraveling of the American middle class. On paper, the US economy looks relatively solid. Unemployment is low. The stock market is hitting new highs. Tech companies are racing to build the AI future. But look closer and the cracks are everywhere. Household finances are buckling under the triple punch of inflation, rising interest rates, and the long-dreaded return of student loan payments. Meanwhile, wages have stagnated in real terms, while the cost of simply staying afloat – rent, healthcare, education, childcare – has soared.

In the middle of this squeeze, Klarna steps in with what sounds like a lifeline: “Buy now, pay later.” No interest. No stress. Just four easy instalments. But what feels like flexibility in the short term is often fragility in disguise. BNPL has become a fallback for people who can’t afford the basics in the moment.

How does all this affect us down here in sunny South Africa?

Not directly, thankfully. Klarna doesn’t have a footprint here (yet), and our BNPL market is still nascent. But the story matters – not because we’ll share the fallout, but because we can learn from it. Klarna’s trajectory is a reminder that consumer debt, when unchecked and increasingly desperate, is one of the clearest indicators of a country’s financial pulse.

If you want to measure the economic health of a nation, don’t just look at GDP or tech IPOs. Ask a simpler question: how many people need to borrow money to buy their lunch today?

And if you think the South African Budget Speech was a circus, then I hope you’ve been paying attention to DOGE and the One Big Beautiful Bill in the United States – and of course the subsequent fallout between Trump and Musk. All is not well there.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Fairvest’s B shares are doing very nicely (JSE: FTA | JSE: FTB)

The B shares are the “risk” shares that do well in the good times

Fairvest offers a dual-share class structure. Their A shares are designed for more income-focused, risk-averse investors. The dividend on the A shares increases each year by the lower of 5% or the most recent CPI number. The B shares then get the residual, which means great growth in the good years and possibly even no growth (or worse) in rough years.

Thankfully, things are good at the moment. The distribution per B share is up 8.8% for the six months to March 2025, driven by strong underlying metrics like 5.1% growth in like-for-like net property income. Another useful factor has been the lower finance charges, with the loan-to-value ratio dropping from 32.6% to 31.8%.

One of the significant changes in recent months was an increase in the stake in Dipula Properties from 5% as at September 2024 to 26.3% as at March 2025.

Fairvest’s portfolio includes 127 properties across retail, office and industrial. By revenue, the split is 69.8% retail, 18.4% office and 11.8% industrial. Within this, they need to try and find the best growth drivers, as evidenced by the deal announced this week that will see Fairvest acquire a portfolio of township-adjacent / busy commuter route retail properties from Collins Property Group.

The Collins acquisition isn’t in these interim numbers. Neither is the recent capital raise by Fairvest that saw the issue of new Fairvest B shares to raise R400 million, with those funds being put towards various opportunities, including of course the Collins deal.

Fairvest has guided growth of between 8% and 10% for the 2025 financial year. This implies strong momentum into the second half of the year.

Fortress is running in line with guidance (JSE: FFB)

Earnings are growing by mid-single digits

Fortress Real Estate has delivered a pre-close update for the year ending June 2025. With a combination of a strong logistics and retail portfolio, along with a sizable stake in NEPI Rockcastle, the fund has done a great job of navigating life-after-REIT, despite all the worries that they had about what the reaction to the loss of REIT status would be.

As is so important for property funds, they are “recycling capital” i.e. selling properties at appealing prices, having achieved sales of R1.44 billion at a premium to book value of 3.0%. The market treats this as an indication that the book value is grounded in reality.

The retail portfolio has achieved like-for-like tenant turnover growth of 4%. Retail vacancies are just 0.9%, which is the same as the vacancy rate in the SA logistics portfolio. The same can’t be said for the Central and Eastern European logistics portfolio, which saw vacancies increase from 1.4% to 2.5%. The local industrial and Inofort portfolio saw vacancies increase from 9.8% to 10.0%. As for the office portfolio, which is non-core and less than 1.5% of total assets, vacancies are still very high at 24.7% (but better than they were at 25.5%).

The company is enjoying strong support from the debt market, with R820 million raised under the DMTN programme in May 2025. The cost of funding reduced by 21 basis points on the three-year and 24 basis points on the five-year note, with the tighter funding margins reflecting improved sentiment in the market. The group also took advantage of early refinancing with Nedbank at a favourable rate.

Total distributable earnings guidance for FY25 has been maintained. On a per-share basis, this means an expected 160.26 cents per share for FY25 (up 5.7%), with guidance given for FY26 of between 169.88 and 172.27 cents per share (up 6.0% – 7.5%).

Solid numbers at Mr Price (JSE: MRP)

Their caps may be red, but their numbers are very green

Mr Price has released results for the 52 weeks to 29 March. It’s a story of revenue growth (7.9% at group level) and higher margins, with gross margin up 80 basis points to 40.5% and operating margin up 20 basis points to 14.2%. Diluted HEPS therefore achieved double-digit growth of 10.1%.

The second half was stronger than the first, with HEPS growth of 12.1%. This sets them up well for the new financial year, with the market no doubt appreciating the underlying momentum.

It’s pretty interesting that group in-store sales were up 7.8% and online sales were up 7.9%, reflecting no obvious consumer preference between the two. Although Mr Price puts this forward as an indication of a successful omni-channel strategy, I’m not sure I agree with that take. Most retail businesses are seeing online growth that is well ahead of in-store growth, as it is coming off a much lower base, so is Mr Price really competing effectively here? The group is delivering strong numbers overall, but I would keep an eye on this.

They certainly aren’t shy to open new stores, so the online strategy is perhaps less important right now anyway. Weighted average trading space increased by 4.3% and they indicate that new stores are achieving returns “well in excess” of the group’s weighted average cost of capital (WACC).

Another interesting insight is that Mr Price’s credit approval rate has increased based on a better credit environment. If we consider this statement in the context of what we’ve seen at the likes of Lewis, it does make sense. This helped drive revenue growth in the financial services segment of 5.7%.

In terms of margins, the uptick in gross profit margin was thanks to lower markdowns and a better inventory strategy overall, with margins on the up in both merchandise and telecoms. This increase was very important in the end, as total expenses increased by 10% and operating margins would’ve been under pressure if not for the higher gross margin. Much of the expense growth was related to the enlarged store footprint.

Another note on margins is that the telecoms segment is at a much lower gross margin than merchandise, coming in at 20% vs. 41.3%. This is relevant because this segment also had the highest sales growth (13.2% vs. 7.9% in Apparel and 6.4% in Home), creating a potential drag on margins over time due to the changing mix.

I must also point out that gross inventory was up 10.6%, which is ahead of sales growth. This isn’t uncommon when there’s a store expansion strategy in process, but it’s worth watching to make sure they don’t end up overstocked.

Within Apparel, Power Fashion is the fastest growing division. In Home, it’s no surprise at all that Yuppiechef managed another double-digit growth period with gains in gross margin as well. Sheet Street was the surprising highlight though, with the highest sales growth recovery in the second half vs. the first half.

Mr Price is clearly on the hunt for more acquisitions, with a statement in the outlook section that their “focused research is going to identify the next growth vehicle that will support the achievement of the long-term vision” – a strong statement to advisors to bring them suitable assets. And with strong cash generation in this period and evidence that previous acquisitions have worked, I suspect that shareholders will be happy to see further deals.

PK Investments makes a better attempt to woo MAS shareholders (JSE: MSP)

At this point, there’s still nothing binding on the table

I must say, it’s not super clear to me why PK Investments didn’t wait for Hyprop to go first here. Hyprop has now raised R808 million and is sitting with that cash drag on its balance sheet, which means that they need to get on with it and make some kind of cash-and-shares offer for MAS. Instead of waiting to see what that offer looks like, PK Investments has gone ahead and given Hyprop more information to work with.

Anyway, having initially put in a non-indicative bid that was somewhere between laughable and just plain sad, PK Investments has gone off and sharpened the ol’ pencil. The revised indicative bid no longer envisages a delisting of MAS. They have also increased the cash consideration from EUR1.10 per share to EUR1.40 per share, with the maximum cash amount up from EUR80 million to EUR110 million.

But alas, the structure still includes the strange redeemable preference shares. So now, assuming I’m understanding this correctly, shareholders who accept this deal from PK Investments would still be swapping MAS listed exposure for what will almost certainly be a less liquid instrument, without MAS even enjoying the benefits of being delisted.

On the plus side, the EUR1.40 value per share works out to around R28.40 per share, which is well above where MAS is currently trading. Even though it’s still such an unappealing structure, it now makes any potential takeout offer by Hyprop even more expensive to implement.

There are a lot of pieces on this chessboard at the moment.

Spear REIT raised R749 million in fresh equity (JSE: SEA)

They’ve now used up their authority from shareholders to issue shares

It’s pretty common for companies to get a resolution in place each year that gives them authority from shareholders to issue up to 5% of shares for cash. This allows the company to raise money during the year without running to shareholders each time. Shareholders aren’t quick to grant this power, so it’s a sign of success when a company gets this authority in place.

Spear REIT has been doing a fabulous job of growing its portfolio and allocating capital, so investors are happy to grant that authority. The company has made full use of it, raising fresh equity at a premium of 1.06% to the 30-day VWAP. Pricing like this is why shareholders really don’t mind.

The raise itself is a combination of shares issued for cash under the general authority, as well as a vendor consideration placement. They will use the proceeds to settle debt and fund further solar and other growth opportunities. With a loan-to-value ratio of 18% to 20% after this raise, there’s plenty of headroom here for deals.

A better second half at The Foschini Group, but growth excl. White Stuff is weak (JSE: TFG)

Online is the bright spot: Bash is profitable two years ahead of expectations

The Foschini Group has released results for the year ended March. With operations across three major regions, the performance does tend to vary significantly by geography. This year was no different.

Performance can also sometimes vary from the first half to the second half, with the 2025 financial year as a perfect example of this.

And as a further nuance, there was a major acquisition during the period that really boosted sales. Group sales growth was 3.6% for the full-year, but it would’ve been just 0.3% without the acquisition.

Before we dig into the regions, it’s important to note that HEPS was up just 4.6%, yet the final dividend per share came in 15% higher.

We begin with TFG Africa, where full-year growth was just 3.7% (or less than half the Mr Price growth rate). They had a very poor first half of the year, with sales down 0.1%. The growth in the second half of 7.0% helped them get into the green. Notably, online platform Bash reached profitability two years ahead of expectations, which is excellent. Online sales growth was 43.5% and now contributes 5.8% to total TFG Africa sales.

With a 69.7% contribution to group sales, it’s so important that TFG Africa does well. Sales only tell part of the story, with gross margin being key to profitability. After plenty of clearance activity in the prior year, gross margin achieved a 150 basis points uptick to 42.6%. This drove gross profit growth of 7.6% vs. the prior year.

Another trend worth noting is the increase in acceptance rates for new accounts. As at Mr Price, we’ve seen South African retailers opening the taps on credit sales.

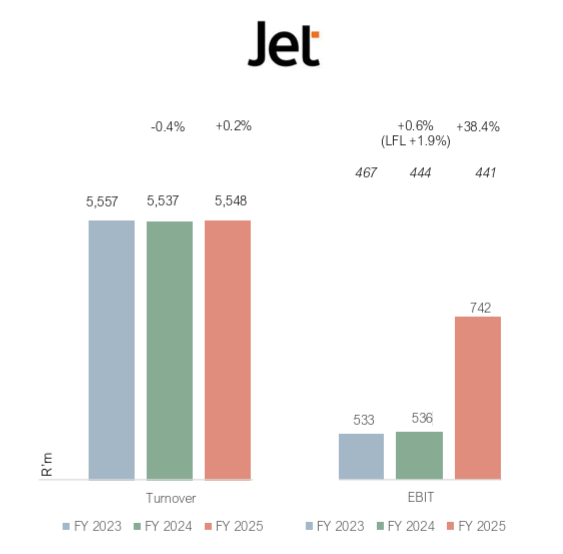

As a final comment on TFG Africa, the value offerings (like Jet) saw a jump in profit of 38% despite turnover growth of just 1%. It’s great to see that they are getting that acquisition to work for them. Check out this chart of turnover and EBIT (a measure of profitability) as a great example of turning water into wine:

Moving on to TFG London, I’m afraid that I don’t have good news. The acquisition of White Stuff in October 2024 massively flattered the numbers, with comparable sales being down 9.5% in TFG London (in ZAR) or 8.6% in local currency. You can’t fix a business by buying more revenue, so investors will definitely want to see an improvement in the group excluding White Stuff. If you include White Stuff, then sales were up 15.3% for TFG London.

In TFG Australia, sales for the year fell by 6%. After the investment in White Stuff in TFG London and now the dip in TFG Australia, the two offshore operations have nearly identical contributions to group sales at around 15.2% each. Sales in Australia were down 2.6% in local currency, with gross margin falling by 80 basis points. They managed to mitigate some of that impact through operating cost control.

The first eight weeks of the new financial year reflect growth in TFG Africa’s sales of 9.9%. The UK business is still in trouble, down 1.7% excluding White Stuff. Australia is even worse, down 3.4% in local currency.

As a general comment, I worry about the lack of commentary around balance sheet metrics in the results. You have to dig into the analyst presentation rather than the SENS announcement to find anything useful. With return on capital employed of 14.5%, down from 14.6% in the prior year, that might be why. That isn’t a strong enough return in my books, with a further challenge being that stock turn dipped from 2.4x to 2.3x as inventory moved 17.5% higher excluding White Stuff.

And yet, despite what certainly seems to be healthier momentum at Mr Price at the moment, The Foschini Group has been the better performer over five years:

And even more surprisingly, over 12 months as well:

Nibbles:

Director dealings:

A senior executive of Sirius Real Estate (JSE: SRE) sold shares worth nearly R7 million.

There’s yet more buying at Santova (JSE: SNV), with a director of a subsidiary buying shares worth R229k.

A director of NEPI Rockcastle (JSE: NRP) bought shares worth R138k.

Assura (JSE: AHR) has confirmed that it is still busy with the due diligence on Primary Health Properties (JSE: PHP). This comes after Primary Health Properties improved its bid to the point where Assura had to take it seriously, resulting in the meeting to vote on the cash bid from KKR and Stonepeak being adjourned. In the meantime, the KKR and Stonepeak bidco (the entity making the offer) has gotten a few regulatory clearances out of the way.

Delta Property Fund (JSE: DLT) is in the process of disposing of the property known as 88 Field Street in Durban. This is a category 1 deal, so they need to get a circular out. The JSE has granted an extension for the circular to be issued by no later than 31 July 2025.

At least one layer of uncertainty around Telemasters Holdings (JSE: TLM) has been removed, with the company no longer considering an acquisition. The cautionary related to a potential acquisition of shares by a B-BBEE investor is alive and well, with the recent update being that the party has secured funding and that documents are being negotiated.

The CFO of Coronation (JSE: CML), Mary-Anne Musekiwa, has tendered her resignation in order to pursue an international opportunity. The resignation is effective 30 November 2025. The process to appoint a new CFO will begin soon.

If you are a Powerfleet (JSE: PWR) shareholder, then you may want to check out the amendment to the severance agreement with the CEO. It relates to the bonus that would be payable to the CEO in the event that employment is terminated.

Alphamin will have a new controlling shareholder (JSE: APH)

Is this the first step in a broader takeover plan?

Alphamin has alerted the market to an agreement entered into by its 57% majority shareholder, Tremont Master Holdings, to sell almost all those shares to International Resource Holding (IRH). IRH is based in Abu Dhabi, so this is an interesting further investment from the Middle East in African mining. IRH already holds upstream and midstream assets in the global raw materials market.

This would mean a change of control, so the regulatory pieces could get quite interesting. Alphamin is a Mauritian company that is listed in Canada and on the JSE. The press release by Tremont and IRH indicates that this was a block trade at a price not exceeding 115% of the market price of the shares, hence it qualifies for a private agreement exemption under Canadian takeover law.

Mauritian law does make provision for mandatory offers though, so Alphamin will need to waste no time in clearing up what the legal position is here. I have no idea exactly what the end result will be, so please don’t assume that any mandatory offer might become applicable.

Interestingly, the IRH press release does note that they “may in the future consider the appropriateness of exploring one or more transactions to acquire the balance of the outstanding Common Shares after discussion with Alphamin’s shareholders, board of directors and/or other stakeholders” – in other words, this may well be the first step in the dance.

As always in corporate transactions, nothing is guaranteed and its best to wait for the company to clarify things.

The JSE gives AYO Technology a going away present in the form of a censure (JSE: AYO)

The fine probably won’t be payable though

AYO Technology shouldn’t be listed. It’s time for the company to just be taken into the private space, something that Sekunjalo is now trying to do. A timely reminder of this is a censure by the JSE that has been imposed on AYO for not meeting disclosure requirements back in 2023.

It feels like two years is a long time to finish a disclosure investigation, but it is what it is. The transgression related to the lack of a SENS announcement in March 2023 dealing with the specific repurchase of shares that was necessary for AYO’s settlement with the PIC and GEPF. Primarily, the issue was AYO’s lack of compliance even after the JSE pointed out the need for the announcement. It took AYO roughly two months to actually comply, which the JSE finds unacceptable.

The JSE has imposed a fine of R500,000 on AYO. The fine is wholly suspended for five years, provided there are no further breaches of “similar provisions” of the Listings Requirements. Given the efforts to take the company private, it seems unlikely that they will be listed for long enough to be in breach once more.

Anything is possible though.

Brimstone’s NAV has been hammered by its listed stakes (JSE: BRT | JSE: BRN)

Oceana and Sea Harvest in particular are well down this quarter

As an investment holding company, Brimstone focuses on intrinsic net asset value per share. This is the correct approach. They also give a voluntary quarterly disclosure, which is pretty good going when most JSE companies only report every six months.

Sadly, the latest quarter was very unkind to Brimstone. From December 2024 to March 2025, the INAV per share plummeted by 24.1% to 842.1 cents. The main culprits here are Oceana and Sea Harvest, collectively contributing 77% of Brimstone’s gross asset value. Both companies are listed and suffered nasty drops this quarter of 13.7% and 18.5% respectively.

To add to the pain, the value of Phuthuma Nathi literally halved in this period. It may only be a small stake (and is now even smaller), but it still stings.

Once you factor in a 3.9% increase in net debt at corporate level, you unfortunately reach the position where NAV per share has lost nearly a quarter of its value. Not fun.

Fairvest is buying some retail properties from Collins (JSE: FTA / JSE: FTB | JSE: CPP)

In both cases, these funds are demonstrating strategic focus

Here’s a solid example of two listed funds each applying their minds (and capital) in the right places. I’m a big fan of focused strategies, especially in the property market.

Fairvest wants more retail properties that are servicing township areas and busy commuter routes. This is a huge growth area in South Africa, capturing the shift from informal into formal trading. They aren’t straightforward to run though, with Collins Property Group deciding that they would rather be sending their capital offshore. It therefore makes plenty of sense that Fairvest is buying five such retail properties from Collins for a meaty R477.7 million.

The properties are located in KZN and the Western Cape. The blended yield for the acquisition is 9.81%. The anchor tenants are all grocery retailers as one would expect, including Shoprite, Boxer and even a SuperSpar.

As for Collins, they plan to invest the net proceeds (after costs and minority interests) in the Netherlands. They’ve also indicated that the selling price is in line with the fair value of each property as determined by the directors of Collins.

Jubilee Metals is selling the South African chrome and PGM operations (JSE: JBL)

This is a major strategic decision for the company

Jubilee Metals operates in South Africa and Zambia. Much of the focus and excitement has been around the copper assets in Zambia. Going forwards, that will be (almost) the entire focus, as Jubilee has received a conditional binding offer for the chrome and PGM operations in South Africa.

The price on the table is up to $90 million, with the usual conditions and adjustments being part of the deal. The reason why I included the “(almost)” above is that Jubilee will retail all rights to the Tjate Platinum mining project, so there’s some ongoing exposure here in case PGMs do well.

The main reason why Jubilee is serious about this offer is that the chrome and PGM operations are mature. To achieve further strong growth, they would need to invest capital in them. With so many copper opportunities in Zambia, this is simply too much for the Jubilee balance sheet. It therefore makes sense to offload the assets to someone else, thereby injecting plenty of capital into the group for the Zambian opportunity.

Importantly, this is a more appealing funding prospect than the Abu Dhabi investment firm that was sniffing around the copper assets. Selling off the chrome and PGM assets allows Jubilee to fund the copper assets without diluting its stake in them.

Notably, the cash would be received over three years, so the $90 million doesn’t arrive up-front. There are also a number of conditions, including a shareholder approval.

Separately, Jubilee noted that they’ve secured a further run-of-mine stockpile in Zambia, which they’ve paid for by issuing new Jubilee shares at a 14% premium to the closing price on 3 June. Nice!

MultiChoice is still making fat losses (JSE: MCG)

The vast investment in Showmax continues

As I’ve said many times, the Canal+ deal isn’t just important for MultiChoice, it’s a matter of life or death. A trading statement for the year ended March 2025 gives further evidence for this view, as they are still making a headline loss per share. Sure, it might have narrowed by between 62% and 66%, but it remains a loss.

They try and use non-IFRS measures to improve the story, like “organic trading profit” which excludes the impact of forex. When you’re building a business across Africa, excluding forex from the numbers is like asking people to focus only on your star players in your team. Sadly, life isn’t that simple.

The profit on sale of a 60% shareholding in NMS Insurance Services to Sanlam certainly helps the overall numbers (and is excluded from HEPS), but that’s obviously not an indication of maintainable earnings. The fact remains that MultiChoice is throwing everything at Showmax, while blaming everything from macroeconomic factors through to the rise of piracy(!).

Top tip for MultiChoice: if your technology was better and your pricing wasn’t designed to actively rip off anyone looking for a decent sports bouquet, you would do a great job of getting rid of privacy. I pay for the full bouquet because it’s the only way to get all the sport I want, but there are many who don’t or can’t. It’s incredible to me that there still isn’t a SuperSport-only bouquet for a reasonable amount every month.

Anyway, it will hopefully be Canal+’s problem soon. I hope they have a plan to fix the South African business.

NEPI Rockcastle is looking for a new CEO (JSE: NRP)

Time to dust off that CV?

NEPI Rockcastle has had an exceptional few years. The market loves the story, with the company enjoying exposure to exciting markets in Europe that offer a mix of growth and currency stability.

Rudiger Dany has been leading the company as CEO during the COVID period and has decided to conclude his tenure in March 2026. The group is therefore looking for a replacement, with the search opened up to both internal and external candidates.

The market will hope for certainty on this as soon as possible.

Nibbles:

Directors:

Here’s one to take note of: the CEO of Bidvest (JSE: BVT) bought shares worth R10 million in the company.

Another one that I think is worth paying attention to is the trend in director dealings at Santova (JSE: SNV). After some initial on-market buying by directors after the announcement of the recent acquisition, a few directors have now exercised share options. But here’s the interesting thing: only one of the directors chose to sell a portion. Although I’m usually nervous of reading much into share-based awards, this is effectively a “buy” for me under the circumstances, as it implies that the directors are funding the tax with other cash resources.

An associate of a prescribed officer of Thungela Resources (JSE: TGA) sold shares worth R91.4k.

There’s nothing you can read from this into the share price as its a forced sale, but I always like highlighting how these hedge transactions play out. Adrian Gore of Discovery (JSE: DSY) had to sell around R38 million in shares as the share price at the collar’s maturity was higher than the strike price on the call options. Similarly, Barry Swartzberg sold R75 million in shares.

As unusual and illiquid stocks on the JSE go, Nictus (JSE: NCS) is right up there. The tiny company just saw a major jump in earnings though, with HEPS up by between 74.07% and 94.07%, which means a range of between 35.61 cents and 39.71 cents for the year ended March 2024. The current share price is R1.45.

Telemasters Holdings (JSE: TLM) renewed the cautionary announcement. This relates to the two largest shareholders of the group having been approached by a B-BBEE investor. The investor has now secured funding, so the parties are in the process of negotiating agreements.

Twenty years on, the managers of the Investec UCITS World Axis Core Fund reflect on what two decades of global investing have taught them and what investors should expect next.

From shifting geopolitics to enduring investment truths, this episode of No Ordinary Wednesday, with Investec Investment Management’s Head of Multi-Manager Investments Ryan Friedman and Fund Manager Bronwen Trower, explores the art of staying the course in a world that rarely does.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

There’s finally a succession plan at CMH (JSE: CMH)

The gives the market some certainty

To say that the CMH directors have been around for a while would be an understatement. CEO Jebb McIntosh has been on the board since 1976 (12 years longer than I’ve been alive) and financial director Stuart Jackson has been on the board since 1986 (when my parents were no doubt starting to have conversations about bringing a little ghost into this world).

We can therefore agree that it’s time for a succession plan. Charles Webber, the CEO of the group’s motor retail and distribution division, will be appointed to the board and is clearly being prepared to take over as CEO. For now, McIntosh remains CEO.

Priya Govind has been nominated to take over as financial director from Stuart Jackson, having been with the group since 2023. The announcement doesn’t give a specific date for the handover, but rather talks about an “orderly transition” in the role.

It’s hard to let go after that many years. At least the process is finally happening.

Double-digit earnings growth at Invicta (JSE: IVT)

As always, HEPS is the metric to look at

Invicta has released a trading statement dealing with the year ended March. They seem to have done well, with expected HEPS growth of between 11% and 17%. This takes them to a HEPS range of 520 cents to 548 cents. The mid-point of that range is a Price/Earnings multiple of 6.3x.

There’s a big difference between Headline Earnings Per Share (HEPS) and Earnings Per Share (EPS) in this update due to a profit on disposal of the main warehouse in Singapore by Kian Ann Engineering. EPS growth of between 54% and 60% therefore isn’t reflective of the maintainable underlying growth in the group.

The market enjoyed what it saw, with Invicta trading over 5% higher by afternoon trade.

Ninety One had a much better second half to the year (JSE: N91 | JSE: NY1)

But not enough to fully offset the first half

Ninety One has reported results for the year ended March 2025. It was very much a tale of two halves, as the financial cliché goes.

In the first half of the year, they suffered net outflows of £5.3 billion. In the second half, they managed net inflows of £0.4 billion. That’s quite a swing! Thanks to overall market returns, assets under management (AUM) increased by 4% for the year to £130.8 billion.

It’s interesting to see where the growth was. The alternatives asset class was a star performer, with AUM up 21% to £5.2 billion. They note the alternative credit strategies as a particular highlight here. The South African fund platform was even better, up 19% off a larger base to finish at £13.2 billion. A modest 3% increase in equities to £60.1 billion also contributed. Fixed income was a drag on growth, ending slightly down at £31.8 billion. The final category is multi-asset, up 1% to £20.5 billion.

It’s interesting to note that AUM from UK clients fell by a pretty nasty 13% to £21.1 billion, due to large clients “rebalancing their portfolios” with reduced allocations to certain strategies. Meanwhile, clients in Africa (including SA) contributed 9% growth in AUM to £55.6 billion. Asia Pacific was a bright spot, up 14% to £23.6 billion.

Another way to slice and dice the business is institutional vs. advisor AUM, with the former up 6% to £85.5 billion and the latter down 1% to £45.2 billion. Having a primarily institutional business does open the group up to significant flow decisions by large clients, as evidenced by the UK business in this period.

Despite the 4% increase in AUM, adjusted operating revenue grew by just 1.1%. Adjusted operating expenses increased by 2.3%, hence adjusted operating profit fell by 1.4%. Adjusted operating margin dipped by 80 basis points to 31.2%. Finally, HEPS was down by 7%.

So, on the whole, a poor start to the year made it difficult for them to try and save the year. The market certainly appreciated the second half momentum though, as well as the total dividend per share for the year being down just 1%. Ninety One was trading over 6% higher in afternoon trade.

SPAR has tons of work to do (JSE: SPP)

Even continuing operations are under plenty of pressure

SPAR has released results for the 26 weeks to 28 March 2025. They are pretty rough I’m afraid, so buckle up.

After learning very hard lessons in Poland, they are being more decisive with getting out of difficult offshore businesses. It’s certainly better to sell something while it still has some value, rather than waiting to pay someone to drag the carcass away. SPAR Switzerland and AWG in England have been recognised as discontinued operations, which means they were impaired by R4.2 billion in the process. Ouch! The post-tax losses in those operations (including the impairment) come to R4.4 billion. Of course, merely determining that something is held for sale and actually selling it are two different things.

If we then focus on continuing operations, we see that turnover dipped by 0.2%. Under the circumstances, it’s not a bad outcome that operating profit was up 1.6%. HEPS fell by 0.4% to 450.1 cents.

The Southern Africa business is dealing with low food inflation, just like everyone else in the sector. This makes them reliant on growth in volumes, which is tough when the rise of on-demand shopping has cast serious doubt on the competitive advantage of SPAR’s convenience locations in strip malls, where you can park and run in quickly to get something. The parking and running is being done by a scooter driver these days, often to the soundtrack during delivery of an over-excited toddler who thinks that every Sixty60 driver is a superhero.

So, competition has come to SPAR and in a big way. They managed like-for-like retail revenue growth of just 1.6%. Remember, the owners of your local SPAR aren’t obligated to buy from the holding company listed on the JSE, so there’s a difference between retail revenue growth and wholesale revenue growth. Grocery and liquor wholesale revenue was up just 1.1%. Interestingly, they believe that growth was better among lower-income segments vs. middle- and upper-income segments. I have to believe that this is the Sixty60 / Dash effect, with Pick n Pay’s ASAP offering gaining traction as well. SPAR2U might be up 174% in delivery volumes, but I can still count on my fingers the number of times I’ve seen one of those vehicles on the road.

Build it was actually a highlight in this period, which isn’t something that we’ve seen for a while. Like-for-like sales were up 5.4% and gross margins went higher. The DIY sector is finally seeing some love!

SPAR Health is also doing well, with revenue up 13.7%. Loyalty (the way they measure the extent to which franchisees procure from the holding company) increased significantly from 53.2% to 58.0%. SPAR is up against other major wholesalers in the market, including those operated by Clicks and Dis-Chem.

The business in Ireland is significantly smaller than in Southern Africa, contributing around a third of operating profit. Local currency revenue fell by 0.6%, with the opposite issue on that side of the bond in terms of higher inflation putting pressure on volumes.

With net borrowings at R6.6 billion and net debt / EBITDA in continuing operations sitting at roughly 2x, the balance sheet is in decent shape overall. It’s going to come down to how efficiently they can sell the businesses in Switzerland and England. Negotiations are already in progress with interested groups.

There are a number of management initiatives in both Southern Africa and Ireland. I expect that focusing on just two regions will improve the situation in both of them, with the group expecting to see margin improvement in the second half of the year. The market seemed to like this, with SPAR closing 3.3% higher on the day.

Nibbles:

Director dealings:

An executive at Richemont (JSE: CFR) sold shares in the company worth R69 million. This individual can certainly afford to buy the company’s watches!

Oando (JSE: OAO) finally released results for the year ended December 2024. They include roughly four months’ worth of numbers from Nigerian Agip Oil Company, which was acquired in August 2024. This contributed to a 44% increase in revenue. Profit after tax was up 267% off a small base. And in good news for the balance sheet, they are enjoying the support of lenders, as evidenced by an upsizing of the reserve-based lending facility to $375 million. There’s very little liquidity in this stock, so you would have to be very excited at the thought of the Nigerian oil sector to spend much time on this.

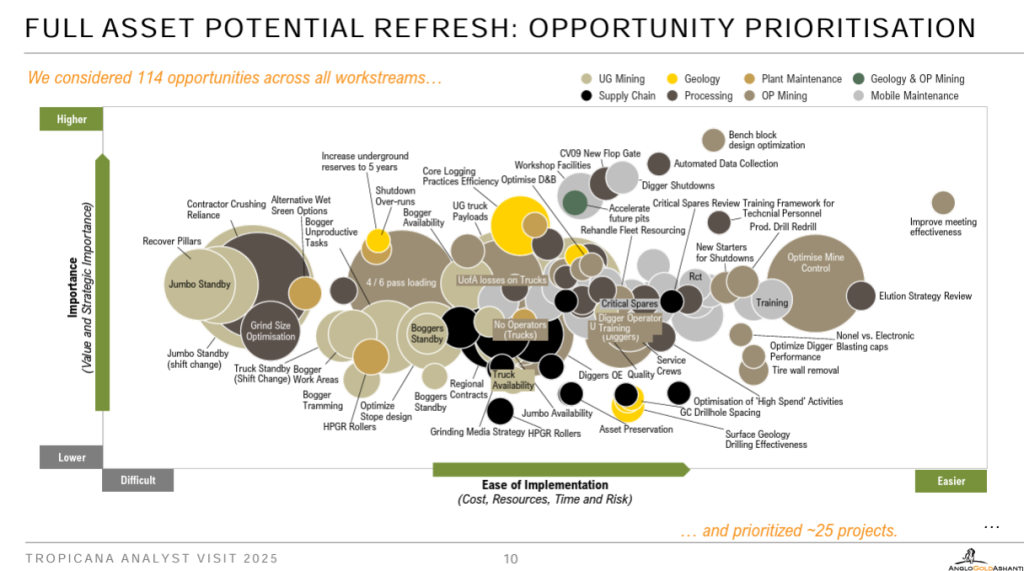

If for some reason you would like to learn more about AngloGold Ashanti’s (JSE: ANG) exotically named Tropicana mine in Australia, then the company has made a presentation available. I’ve seen some wild slides in my life, but this surely takes the cake:

Datatec (JSE: DTC) has released the circular for the scrip distribution alternative. This gives shareholders the ability to receive more shares in lieu of a cash dividend. If you’re a shareholder, I suggest that you check it out.

Gemfields (JSE: GML) likes to report something called the G-Factor, which it came up with in 2021. Essentially, it measures the percentage of natural resource revenue paid to governments of countries from which the resource is derived. When you’re doing business in frontier markets, you need to extra steps to make sure that government is happy – and even then, they had issues like the Zambian government slapping an export tax on them out of nowhere (and subsequently removing it). For the 10 years from 2015 to 2024, the G-Factor is 20% for the Kagem emerald mine in Zambia and 25% for the Montepuez ruby mine in Mozambique. Perhaps the Zambian government is just jealous.

Shuka Minerals (JSE: SKA) has received interim approval from the Competition and Consumer Protection Commission (CCPC) for the acquisition of a 100% interest in Leopard Exploration and Mining in Zambia. They still need to get a final approval, but they can now continue as though that approval will come.

UK-based property fund Hammerson (JSE: HMN) announced that CEO Rita-Rose Gagné intends to retire as CEO in 2026. This gives them time to find a suitable successor. This hasn’t been the longest stint around, as she only took the top job in 2020.

Acsion (JSE: ACS) has renewed the cautionary announcement related to a potential acquisition. There’s no further insight at this stage into exactly what they are up to.

Harmony Gold (JSE: HAR) announced a loss-of-life incident at the Joel mine in the Free State. It’s another tragic reminder that mining in a dangerous industry, even though so much effort is put into safety.

Bell Equipment gives more details on the state of the market (JSE: BEL)

The CEO gave a business update at the AGM

The timing of Bell Equipment’s reporting calendar is such that the company released a trading statement earlier this week that flagged an expected 50% drop in HEPS for the six months ending June 2025. The AGM for the year ended December 2024 was held a day later, so that was an opportune moment for the CEO to give the market an update on what’s really going on out there.

The AGM business update is very narrative-focused rather than full of specific numbers, as you would expect when the interim period hasn’t even concluded yet. The overall message is one of soft demand, leading to worldwide industry inventory levels peaking at levels last seen in the Global Financial Crisis. That’s no good for margins, inventory obsolescence risks or cash flow. In the context of that broader trend, it sounds like Bell is in a reasonable inventory position overall. We will see when the numbers are available.

One of the negative surprises has been the cooling off of the mining sector in the Southern Hemisphere. Bell has a large business in the Northern Hemisphere, including a manufacturing base in Europe for the ADT vehicles that made Bell famous. The frustration is that the European manufacturing base (in Germany, to be precise) supplies the United States, so the tariff uncertainty is an issue at the moment.

A group like this will always have focus areas (like the aftermarket business and non-Bell OEM contract manufacturing in Richards Bay) and areas where they are pulling back (underground mining machines).

The market will now wait for the release of more detailed financial numbers for the interim period. I imagine that a further trading statement would be the logical next step, probably somewhere in July.

British American Tobacco is running ahead of their expectations this year (JSE: BTI)

The second half of the year will be even more important

As we head towards the end of British American Tobacco’s interim period in June, the group has given the market an update on how 2025 is going thus far. The good news (for the company at least, if not for society) is that revenue growth for the full year is expected to be 1% to 2%, which would then support adjusted profit from operations growth of 1.5% to 2.5%. The focus at British American Tobacco is firmly on grinding out higher operating margins and then converting that operating profit to cash.

The first half of the year is going to reflect lower numbers than that, as they expect performance to be weighted towards the second half of the year. The US market remains difficult for various reasons, although they have managed both revenue and profit growth there for the first half of the year.

Importantly, they expect to achieve operating cash flow conversion of at least 90% for the full year. Through a combination of operating cash flows and the decision to sell down part of the stake in Indian business ITC, they expect to be back within the adjusted net debt : adjusted EBITDA range of 2.0x – 2.5x by the end of 2026. Getting into that target range would support higher dividends and share buybacks in future.

The share price is up 40% in the past 12 months, so the market is enjoying the story in this environment.

Hudaco makes a small acquisition (JSE: HDC)

This is a typical example of a bolt-on acquisition

I like bolt-on acquisitions. In a world of swashbuckling M&A deals, bolt-ons are the everyday heroes that help businesses add a few percentage points to their growth rate over time.

Simply, a bolt-on acquisition is like adding another Lego block to the house that you’ve already built. This is the process of looking out for ways to plug gaps in the service offering, or just add complementary businesses that might be able to achieve synergies over time in areas like route-to-market strategies.

Industrial groups are big fans of these types of deals, as there are loads of small industrial companies that can be mopped up by larger groups over time. Hudaco’s acquisition of Flosolve is a perfect example of this.

Flosolve is an importer of specialised equipment for the servicing and refuelling of plant and machinery in the mining industry in particular. It therefore makes sense that the business is based in Gauteng and Middelburg. Hudaco sees this as a great fit in its engineering consumables segment, where they have a lot of overlap in terms of customers.

Although Hudaco hasn’t disclosed any details around the profits of Flosolve, we know that the initial payment for the business is R45 million and the maximum consideration payable over three years will be R125 million. This is structured as the acquisition of the business as a going concern, rather than the legal entity in which they are currently housed. It’s also very normal to see an earn-out structure like this.

As this is such a small transaction that doesn’t even meet the Category 2 reporting threshold, we won’t see any further details on the deal. Hudaco made this announcement on a voluntary basis.

In a completely separate announcement, Hudaco noted that a subsidiary of the company has entered into related party leases with an entity that is 82% held by the CEO of Hudaco. The business has been in the premises for over 21 years. An independent expert must sign off on small related party transactions like these. Merchantec Capital has opined that the terms are fair, so there’s no further discussion on these leases.

Momentum’s capital markets day gives tons of details on the business (JSE: MTM)

I’ll just touch on a few details here

Capital markets days are wonderful things. Essentially, they are an effort by listed companies to engage with analysts and institutional fund managers who really move the dial for the share price when they make decisions about the company. Momentum delivered a highly detailed set of presentations that explain the group-level focus, along with what they are doing in each underlying business.

Something that is made very clear in the pack is that they are following an advice-driven strategy. They describe it as “putting advisers at the heart of the brand story” and they firmly believe that face-to-face advice is here to stay. I couldn’t agree more.

They are also building out a number of interesting businesses, not all of which have Momentum branding. For example, Curate was launched with a best-of-breed model for selecting local and global fund managers, growing assets by R2.7 billion in the process.

Along with extensive projects aimed at achieving cost savings, the various initiatives all roll up into a 2027 ambition of 20% return on equity, 2% new business margin and R7 billion in earnings (you can see what they did there). Right now, they are tracking against their targets for earnings and return on equity, but they seem to be behind on margins. Overall, they see the goals as still being achievable.

If you would like to dig into the strategy and any of the underlying business units, you’ll find all the presentations here.

Nibbles:

Director dealings:

Various Santova (JSE: SNV) directors have put their money behind the growth story, especially now that the acquisition of Seabourne Group has been announced. Four directors / directors of subsidiaries bought a total of R1.2 million.

Italtile (JSE: ITE) gave an update on shares held by an entity associated with a non-executive director that had been pledged as part of a finance deal. As part of that deal, shares worth R33 million have been released for sale before the end of June. Liquidity in Italtile stock isn’t bad but also isn’t amazing (average daily value traded is around R4.1 million), so those who are involved in the stock may want to keep an eye on the price this month.

The executive chairman of Southern Palladium (JSE: SDL) bought shares in the company worth just over R200k.

The expected announcement from SA Corporate Real Estate (JSE: SAC) has come: Cervantes Investments (which we now know for sure is linked to Castleview Property Fund – JSE: CVW) now holds a 15.01% stake in the company.

The dust has settled on the Anglo American (JSE: AGL) demerger of Valterra Platinum (JSE: VAL). Anglo American now holds 19.9% in Valterra through various entities. Anglo American shareholders get 110 Valterra shares for every 1,075 shares held in Anglo. Furthermore, every 109 existing Anglo shares will be consolidated into 96 new shares, a process that Anglo is following in order to try and avoid the share price chart breaking from a comparability perspective. The consolidation is designed to offset the effect of the Valterra exposure moving outside of the group.

Absa (JSE: ABG) announced that the resolution for the repurchase of its preference shares (JSE: ABSP) via a scheme of arrangement was approved of by shareholders of those preference shares.

Wesizwe Platinum (JSE: WEZ) has had its listing suspended by the JSE as the company has not published its financials for the year ended December 2024.

Walking before they run definitely isn’t the approach here

Altvest certainly can’t be accused of being light on ambition. As their latest annual results show, they are planning to launch a further 6 funds over the next 12 months or so. This adds to the Altvest Opportunities Fund, Altvest Growth Fund and Altvest Credit Opportunities Fund.

To add to the complexity, they also give small businesses the opportunity to access the market through distinct listed preference shares, as they did with Umganu Lodge and Bambanani restaurants. Heck, they are even involved in bitcoin!

They are also trying to get a slice of the Springbok action, with the group trying to put a deal together to allow South Africans to invest in their most widely-loved sports team. Again, no shortage of ambition.

The challenge is that they are trying to do a lot. I’m all for the ambition here and they certainly need to scale quickly to get past the overheads of being listed, but this really is like building a gigantic house that currently has very little furniture in it.

For context, the most exciting business they have at this stage is the Altvest Credit Opportunities Fund, which has R365 million in committed assets under management. That’s a great start, but it’s far too small to be profitable on even a standalone basis, let alone large enough to carry the group’s ambitions.

I’ll give Altvest a lot of credit for the extent of disclosure here. Check out this chart on disbursements by that fund, with a weird drop to zero in Januworry:

As for the other businesses, Umganu Lodge recognised a small operating loss in the year ended February 2025. Poor Bambanani lost R4.8 million this year vs. a loss of R4.2 million in the prior year. A new restaurant in Bedfordview was part of the expenses, but the fact of the matter is that the business is now in a turnaround situation despite being around for 15 years. As a dad, Bambanani looks like a delightful place to take the kids – but that doesn’t mean I want to own shares in it.

Altvest’s reporting is objectively beautiful and they care deeply about the brand and what they are building. I just hope that they will find sufficient support along the way, as they really are trying to fly an executive-level jet while building it, never mind a plane.

AngloGold Ashanti to sell a Brazilian mine (JSE: ANG)

This is part of a more focused strategy at AngloGold

AngloGold Ashanti has agreed to sell its interest in Mineração Serra Grande mine in Brazil. The buyer is Aura Minerals.

The up-front amount is $76 million, subject to working capital adjustments at closing. Deferred consideration payments will be paid quarterly, equal to 3% net smelter returns participation.

The mine has an uncomfortable place in the AngloGold portfolio, with a high cost of production and a small contribution to the overall story. It therefore makes sense to send it on its way to a new owner, unlocking a cash payment in the process along with future potential payments.

That Bell Equipment take-private offer is a distant memory (JSE: BEL)

And the earnings trajectory is a major worry

I’ve written a few times now that the minority shareholders who blocked the Bell Equipment take-private were being greedy at the time. I fear that the same thing is happening at Barloworld at the moment, but time will tell.

When there was a deal on the table for Bell Equipment, it was at R53 per share. Today, the company is trading at R41.50. That’s already a painful example of what might have been. But if the current earnings trajectory continues, it’s going to get a lot worse.

For the six months ending June 2025, Bell expects HEPS to be at least 50% lower than the comparable period. This implies that interim HEPS will be no more than 160.5 cents for the period. Worst of all, with a month to still go in this period, it’s very possible that the drop is actually a lot worse than 50%, as they are still just guessing at this stage. The words “at least” are very dangerous.

The US tariff uncertainty has added to a situation where there’s a global slowdown in demand in key markets. I’ll say it again – those who are being greedy at the moment in the Barloworld deal are taking fat chances in my opinion. Current global conditions aren’t great for cyclicals.

Hyprop had no problem raising over R800 million (JSE: HYP)

The question is now whether they will make a serious bid for MAS

In response to a very cheeky bid put on the table by the joint venture partner (PK Investments) of MAS, Hyprop came out recently with a plan to raise equity as a pre-cursor to a potential offer for MAS that would be more appealing than the offer by PK Investments. Look, putting a better offer on the table than the PK Investments offer isn’t much of a challenge, as it really was the strangest thing I’ve seen in ages.

The market seems to be happy with Hyprop even contemplating such a move, as an accelerated bookbuild saw the company raise R808 million at a really great price. They issued the shares at R42.50 per share, which is a premium of 0.3% to the 30-day VWAP. Despite this strong pricing, the book was oversubscribed!

The funds will be used to reduce debt and for a variety of growth initiatives, with the possibility being that the MAS deal is one of them. The MAS market cap is over R14 billion, so it wouldn’t be a full cash deal anyway – it would be a share-for-share deal with a cash alternative.

We now wait and see what Hyprop will do.

Momentum is pushing hard on margins (JSE: MTM)

A business of this size needs to keep grinding away

When you get to the size of a business like Momentum, there are few quick wins. Instead, you have to work diligently over time to do the right stuff and find growth along the way, while making sure that margins are protected – and even enhanced! A lot of it comes down to margin mix and how the underlying business shifts over time.

For the nine months to March 2025, headline earnings was pretty consistent across the three quarters. This is despite the first two quarters enjoying substantial positive market-related variances.

Top-line sales aren’t where the good news is to be found, with present value of new business premiums (PVNBP) down 4% year-on-year for the nine months. Momentum Corporate took the biggest knock here, down 29%. The largest area is Momentum Investments and this unit grew PVNBP by 1%.

Value of new business (VNB) was up though, albeit to a lesser extent than in the first two quarters. This is due to a favourable shift in margin mix in the group.

Expenses grew slightly above inflation, with IT investment as one of the usual suspects for that pressure. They expect to unlock the benefits from their optimisation efforts in FY26.

The balance sheet is healthy and the Prudential Authority gave Momentum approval for a R1 billion share buyback programme that commenced in May.

Momentum’s share price has had an incredible run, up nearly 60% over 12 months.

Raubex: results are out and the whistleblower investigation is behind them (JSE: RBX)

There was no evidence of unlawful or unethical conduct

On the 9th of May, Raubex announced that the board had received an anonymous whistleblower report that warranted an investigation. The share price was at R45.70 before the announcement and got as low as R40.90 before the latest updates. That’s a pretty nasty 10.5% drawdown.

With the news that the whistleblower allegations didn’t lead to anything being found, along with the financials having now been released, the share price is back up to R45.20 – almost where it started. I’m sure some punters made money in this process!

The results for the year ended February 2025 saw a meaty revenue increase of 21.0%. Despite operating profit being up just 1.3%, HEPS increased by 25.9%. That’s an oddly-shaped income statement. Helpfully, cash generated from operations was up 31.8% and the final dividend was 13% higher. I would keep an eye on the debt-to-equity ratio, which increased from 26.0% to 31.7% thanks to a 32.2% increase in borrowings.

The pressure on operating margin (which at group level deteriorated from 8.8% to 7.4%) was mainly suffered in Bauba Resources. This is found in the Material Handling and Mining division, which saw operating profit margin plummet from 14.6% to 1.7%. They attribute this to the unfortunate deterioration in the chrome price at the same time that designed feed capacity at the chrome ore wash plant and crushing circuit was achieved.

Thankfully, there were offsetting impacts elsewhere. Construction Materials saw operating margin jump from 4.8% to 10.6%, driven by strong contract demand for bitumen and asphalt volumes. It’s a coincidence that revenue growth in that segment was also 10.6%.

In Roads and Earthworks, operating profit margin increased from 5.8% to 8.6%, driven by significant revenue growth of 19.9% and a well-executed strategy during the year.

The Infrastructure division saw operating margin decreased from 9.5% to 8.9%, but they did manage impressive revenue growth of 27.4%. They attribute this to new contracts in South Africa and solid results in Western Australia.

So, the chrome exposure is proving to be problematic at the moment, with the rest of the group enjoying a positive overall outlook. Raubex remains exposed to the whims of government spending though, so that’s a risk that shouldn’t be ignored.

Sabvest is investing in the pet sector (JSE: SBP)

Let’s face it – it feels like there are more pets than kids these days

With the birth rate going through the floor, fur babies just might be a better investment than human babies. Sabvest is clearly seeing opportunity in this space, as their 39.31%-held portfolio company Valemount Trading is making serious strides in this space and Sabvest has committed a funding line of up to R200 million to make it possible.

Historically, Valemount has supplied retailers, pet stores and co-ops with primarily birdseed and feeder products. They do have other products in the range and they provide logistical services to independent pet product suppliers through nationwide distribution centres.

In the current period, they’ve relocated to a new R160 million production facility in Modderfontein. They’ve made some interesting acquisitions, including dog and cat biscuit manufacturer Ourebi Trading, premium dog food business Complete Pet Foods and regional birdseed supplier Commix. They’ve also entered into discussions to potentially acquire a UK-based cat food business.

Sabvest sees this as a major growth investment and they are looking to increase their exposure over time. Interesting!

Per-share numbers at Sirius suffered from recent capital raises, but the fund marches on (JSE: SRE)

This isn’t an uncommon situation in the property sector

Property funds that are on a growth trajectory tend to raise capital quite often. Sirius Real Estate is one of the best examples of this, with the market only too happy to keep giving this management team equity capital. And why not? Sirius has been doing a great job of actively managing its property portfolio.

But all these extra shares running around do create a problem: growth on a per-share basis suffers because of the lag in deploying the new capital. This comes through strongly in the results for the year ended March 2025, where great numbers like a 6.3% like-for-like increase in the rent roll and an 11.8% increase in funds from operations (FFO) were diluted by all the extra shares.

FFO per share actually fell by 5.7% and the total dividend per share for the year was just 1.7% higher.

As busy as they’ve been with acquisitions (six in each of Germany and the UK), they are sitting with a whopping €571 million in cash and a loan-to-value ratio of 31.4%.

Sirius is poised to do deals. They just have to find them!

Solid earnings growth at Sygnia, but a modest payout ratio (JSE: SYG)

These businesses are usually seen as cash cows

For the six months to March 2025, Sygnia achieved growth in assets under management and administration of 18.8%. That’s an impressive result!

As we dig deeper, we find strong net inflows of R43.1 billion, while a further R12.4 billion increase came from positive market moves. Another point to note is that the institutional assets under management delivered the biggest growth. For context, institutional assets under management come to R326.7 billion vs. R78.7 billion in retail assets under management.

Now, the challenge is that the institutional business is at much lower margins than retail, hence why revenue was only up by 11.6%. That’s still solid of course, driving growth in diluted HEPS of 13.0%.

Oddly, the interim dividend per share is only 8.9% higher. The payout ratio has dropped from 89% to 87.6% – a minor decrease, but still noticeable. There’s no obvious indication why they’ve taken this route.

Telkom dials up the earnings (JSE: TKG)

It’s been a much better time for the telecoms sector

You aren’t imagining it – the telecoms sector has been a far happier place recently. Telkom is just further proof, although much of this improvement is thanks to the restructuring efforts they’ve been through.

In an updated trading statement for the year ended March 2024, Telkom has indicated growth in HEPS from continuing operations of between 55% and 65%. This is a better metric than looking at total operations, which include Swiftnet, in which case HEPS is up by between 40% and 50%.

But perhaps the best metric of the lot is adjusted HEPS from continuing operations, which splits out vast restructuring costs and the impact of converting the Telkom retirement fund to a defined contribution fund. In other words, this metric gets closer to how the actual operations are performing. Growth on this basis is 95% to 105%, which means that HEPS essentially doubled!

Detailed results are due for release on 10 June.

Nibbles:

Director dealings:

The CEO of Investec (JSE: INP | JSE: INL) sold shares worth just over R20 million.

An associate of the CFO of Standard Bank (JSE: SBK) sold shares worth R10.6 million, adding to the extensive selling of shares in the bank that we’ve seen in recent months.

A non-executive director of KAP (JSE: KAP) bought shares worth R99k.

A director of Spear REIT (JSE: SEA) bought shares worth R52k.

Emira Property Fund (JSE: EMI) has bought even more shares in SA Corporate Real Estate (JSE: SAC). In April, they had a stake of around 12.8% based on my maths and a cryptic announcement about “Cervantes Investments” acquiring a stake of that size. Emira has acquired a further 99.4 million shares for R284 million, which looks like a further 3.8% in the company. If that’s true, I expect to see an announcement about them going through the 15% level. Stay tuned!

The demerger by Anglo American (JSE: AGL) of Valterra Platinum (JSE: VAL) – previously Anglo American Platinum – is now effective. Anglo American holds 19.9% in the company and will hold this for at least 90 days, as they need to achieve a responsible separation without flooding the market with shares for sale.

Tsogo Sun (JSE: TSG) announced that CFO Gregory Lunga has resigned as executive director. Chris du Toit, an existing director of the company, will serve in that role on an interim basis.

The nerves continue for investors in Kore Potash (JSE: KP2), with the company continuing to draft non-binding term sheets with the Summit Consortium. They plan to make an announcement as soon as negotiations are complete. Importantly, Kore Potash is keeping its options open in terms of potential funding partners.

Clientèle (JSE: CLI) announced that the acquisition of Emerald Life has become unconditional.

AECI (JSE: AFE) has confirmed that Ian Kramer has been appointed as the permanent CFO of the group. He’s been in an acting role since December 2024.

Afrimat (JSE: AFT) announced a couple of heavy-hitting non-executive director appointments. Jacques Breytenbach was the CFO of London-listed Petra Diamonds until 2024. Pierre Joubert was an Executive Vice President of Ivanhoe Mines, with extensive experience in Africa. There are a couple of retirements of non-execs as well, so the company is having no difficulties in attracting talented directors.

Numeral (JSE: XII) has received approval from the Stock Exchange of Mauritius (its primary regulator) for the financials for the year ended February 2025 to only be released by the end of June.

African Dawn Capital (JSE: ADW) has been delayed in getting financials out for the year ended February 2025. They expect to release them by the end of June, along with the annual report by the end of July.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.

In the 54th edition of Unlock the Stock, Calgro M3 returned to the platform. With a new CEO in place, they discussed the recent numbers and the growth strategy. I co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

Five years ago, the world was a wild place. We were “staying home and staying safe” – and global central banks were cutting rates dramatically in an effort to stimulate economies under impossible circumstances. This created an unprecedented situation for equities in particular.

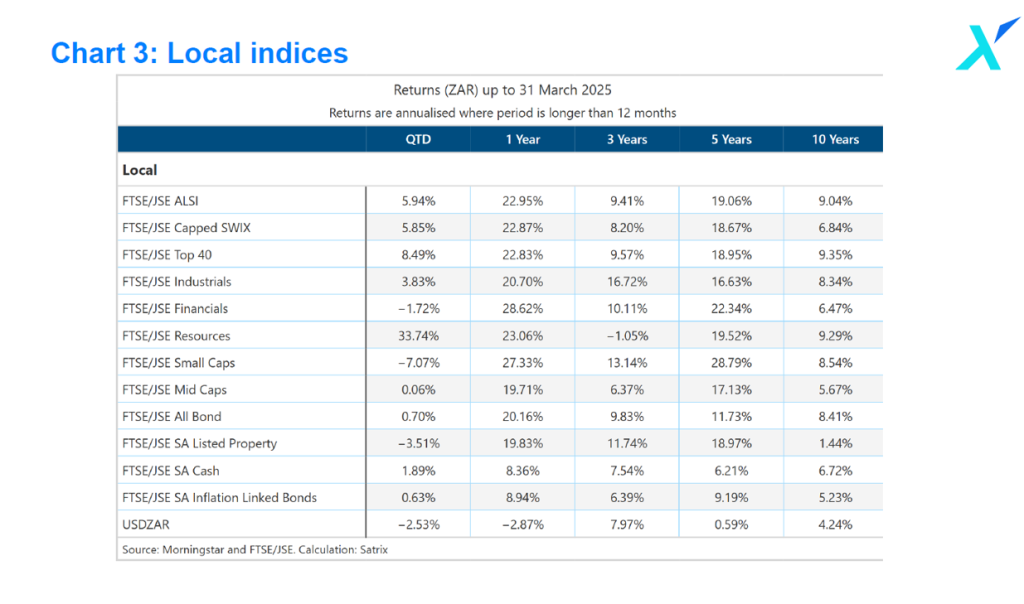

It’s certainly been a great time to be invested in the markets, but which indices have done well and which ones have been disappointing in relative terms? How does the local vs. offshore story stack up? What about developed vs. emerging markets? And what of government bonds?

With a great selection of statistics to share with the listeners, Siyabulela Nomoyi of Satrix was a wealth of knowledge in this podcast.

*Satrix is a division of Sanlam Investment Management

Satrix Investments Pty Limited and Satrix Managers RF Pty Limited are authorised financial services providers. Nothing you have heard in this podcast should be construed as advice. Please do your own research and visit the Satrix website for more information on all their ETF products.

Full transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. It’s another one with the team from Satrix. There have been so many of these and they’ve all been really, really good. I’ve enjoyed all of them.

Today we’re going to do something a little bit different. We do try and think of original stuff for these podcasts. Obviously, as our listeners, if you have any ideas of what you’d like to hear from the team at Satrix, you’re always most welcome to share them. But what we will be doing with Siyabulela Nomoyi this month round from Satrix is we will be looking at a five-year view on the markets. And of course what makes that really interesting is five years is a pretty common view to look at. If you go onto Google Finance, for example, you can typically draw a five-year chart. It’s quite common as sort of a longer-term view. But what makes five years really interesting right now is that five years ago the world went mad. So here we will be looking back on five years of life since COVID – it’s not exactly five years obviously, it was March 2020 where everything went crazy. But I mean we’re now in May, so that’s pretty close for a five-years-since-the-bottom kind of view. Let me welcome you to the show first and then we can dig in and see what interesting stats you’ve got for us here.

Siyabulela Nomoyi: Yeah, hi Ghost, and hi to the listeners. Always great to be on your podcast. Second one between us this year and the last one I believe did exactly what it intended to do: educate more people out there. So, thanks for inviting me again. Quite excited about this one as well.

The Finance Ghost: Yeah, absolutely. Look, the insights are always great, and I think today will be no different. So, let’s jump straight into it, which is a look at how we would measure, I guess, just how mad the world can get. Five years ago, things got a little crazy and I know you’ve done some work looking at major drawdowns not just in that year, but versus years before that as well as the years since then, because market volatility is a feature, not a bug, and these drawdowns are going to happen. Covid was just one such catalyst for a drawdown. So, I’m quite curious to understand firstly, how do you actually measure a drawdown? Is it a peak-to-trough thing? Over what period? How exactly do you actually measure these things?

And then what are some of the data points that you’ve found particularly interesting, not just in terms of what happened during COVID but also before and after?

Siyabulela Nomoyi: Yeah, look, five years ago, Ghost, we watched as the President sent us to lockdown. And I remember waking up the next morning looking out the window and felt like we were in a sci-fi movie.

But look, the finance world did not hit a pause button, with so many things digital these days. But you’re absolutely right – there was some form of madness, if I may call it that, that resulted in how things were at that point.

So just to explain the drawdowns quickly as you’ve asked, anyone who’s invested in any asset class or any asset expects it to actually appreciate in value. It should grow to a level higher than what they’ve purchased it. But with asset pricing you seldom see anything that grows in a straight line up.

There’s always price movement along the way, which we call volatility, as you’ve mentioned at the beginning of the show, in financial markets. When you speak about drawdowns, this is where you measure how much the asset has lost since it hit a certain peak level to where it hits its lowest level.

So, silly example – it’s almost like bungee jumping off a bridge. The peak is where you jump off, but the drawdown is an equivalent to the lowest point of how far you fall. And it’s very, very important to actually understand that.

The Finance Ghost: That’s – sorry, that’s a great analogy by the way. That’s a very good analogy, Siya. I like that. Bungee jumping is exactly it.

Siyabulela Nomoyi: Yes. And it’s very important to actually understand firstly how far you’re going to fall because now you understand which ones you can actually take in terms of the risk that you want to take. So that part is quite important.