This results summary is brought to you by Sasol and does not include any opinions or editorial by The Finance Ghost.

Sasol’s financial performance for the six months ended 31 December 2024 was impacted by a challenging macroeconomic and operating environment. However, stringent cost and efficient capital management helped to offset the impact and improve free cash flow generation compared to the previous corresponding period.

Revenue of R122,1 billion is 10% lower than the prior period, mainly due to a 13% decline in the average Rand per barrel Brent crude oil price and a significant decline in refining margins and fuel price differentials, as well as a 5% decrease in sales volumes as a result of lower production and lower market demand. This was detailed in the Production and Sales Metrics published on 23 January 2025.

Adjusted earnings before interest, tax, depreciation and amortisation (adjusted EBITDA) of R23,9 billion is 15% lower mainly as a result of the aforementioned lower revenue with stringent cost management implemented in response helping to mitigate the impact. The relative contribution from International Chemicals increased from 6% to 13%.

Earnings before interest and tax (EBIT) is 40% lower to R9,5 billion. This was impacted by non-cash adjustments including:

A net loss of R6,2 billion from remeasurement items compared to a net loss of R5,8 billion in the prior period, mainly due to further impairments of the Secunda liquid fuels refinery cash generating unit (CGU) of R5,0 billion and the Sasolburg liquid fuels refinery CGU of R0,6 billion. Both CGUs remain fully impaired, resulting in amounts capitalised during the current period being impaired.

Unrealised losses of R0,1 billion on the translation of monetary assets and liabilities, and valuation of financial instruments and derivative contracts compared to unrealised gains of R2,7 billion in the prior period.

As a result of the above, basic earnings per share (EPS) decreased by 52% to R7,22 per share and Headline earnings per share (HEPS) decreased by 31% to R14,13 per share compared to the prior period.

Cash generated by operating activities increased by 20% to R17,6 billion compared to the prior period mainly due to changes in working capital. Capital expenditure, excluding movement in capital project related payables, amounted to R15,0 billion, 6% lower than the prior period.

At 31 December 2024, our total debt was R116,9 billion (US$6,2 billion) compared to R117,7 billion (US$6,5 billion) at 30 June 2024. Sasol deposited R5,4 billion (US$0,3 billion) on the Revolving credit facility during the current period. Our net debt (excluding leases) was R81,8 billion (US$4,3 billion) compared to R73,7 billion (US$4,1 billion) at 30 June 2024 with the increase due to the aforementioned negative free cash flow.

Dividend

The Company’s dividend policy is based on 30% of free cash flow generated provided that net debt (excluding leases) is sustainably below US$4 billion on a sustained basis. Free cash flow is a deficit of R1,1 billion and the net debt at 31 December 2024 of US$4,3 billion exceeds the net debt trigger, therefore no interim dividend was declared by the Sasol Limited board of directors (the Board).

Tax-free savings accounts (TFSA) are one of the most building blocks in any equity portfolio. The advantage of compounding tax-free returns over a long period is incredibly powerful and can really turbocharge a long-term wealth creation journey.

To discuss the importance of TFSA investments and the opportunities available to investors in the ETF universe, familiar voice Siyabulela Nomoyi of Satrix* returned to the Ghost Stories podcast.

*Satrix is a division of Sanlam Investment Management

Satrix Investments Pty Limited and Satrix Managers RF Pty Limited are authorised financial services providers. Nothing you have heard in this podcast should be construed as advice. Please do your own research and visit the Satrix website for more information on all their ETF products. This podcast was published on the Satrix website here.

Full transcript:

Introduction: This episode of Ghost Stories is brought to you by Satrix, the leading provider of index tracking solutions in South Africa and a proud partner of Ghost Mail. With no minimums and easy, low-cost access to local and global products via the SatrixNow online investment platform, everyone can own the market. Visit satrix.co.za for more information.

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. It comes hot on the heels of a pretty crazy time in South Africa where our budget speech casually did not happen! When I was prepping for this podcast with my guest today, we talked about: wow, you know, I wonder if the tax-free savings limits will be increased and if there’ll be something to encourage people to save? Then meanwhile, there’s a budget that basically wants to fleece us of more money through VAT and it got thrown out. So, not exactly what anyone was hoping for, I don’t think. But anyway, it is what it is. We’ll wait and see what the next version of the budget speech looks like in this ongoing little disaster.

And in the meantime, all of us as South Africans will just keep doing what we do, which is doing our best to move forward in life. To help with an understanding of how tax-free savings can help you with that, we have Siyabulela Nomoyi from Satrix* on the show.

Siya, you’ve been on many, many times. You’re certainly no stranger to the listeners of the Ghost Stories podcast. Having said that, we had some big tech issues with your laptop now, so even though your laptop has also been on many, many times, it decided that today was not its day. This podcast was almost like the budget speech in that it last minute almost didn’t happen. But luckily here we are, you came up clever plan and we can do the show. So welcome.

Siyabulela Nomoyi: Yeah, thanks Ghost. Thanks for having me. Bit of drama to start off, but let’s do it.

The Finance Ghost: No, absolutely. We made a plan.

Tax-free savings accounts, that’s a favorite topic of mine. I think it’s a favorite topic of yours. And yet I think there are still a ton of people out there who firstly just don’t really understand them or why they are valuable. Then for those who do understand that this stuff exists, there are a lot of mistakes that get made out there, some of which is just driven by, in my opinion, quite bad advertising, etc. We can get into that later.

For me, it’s a mistake not to have a tax-free savings account. It’s rare to make a blanket statement like that, but I feel confident in saying that if you don’t have a tax-free savings account, as a South African, you are severely missing out, right? It’s a liquid way to save with a government incentive. That’s a wonderful thing, right? Would you agree with that?

Siyabulela Nomoyi: Yeah. I think it’s quite important that anyone listening to this recording goes and actually educates themselves more on their tax experiences which they are exposed to when they are investing in their direct accounts or using platforms, brokers, LISPs through a bank and so on. For anyone to actually appreciate the importance of a tax-free savings account, they need to first understand that part, otherwise this topic won’t make any sense to them.

Very quickly, when you are investing in capital markets, holding shares, commodities, bonds and so on, the aim there is to have your capital grow, right? Otherwise you would not be investing. Also, I know South Africans love dividends, they love dividend income. Others actually invest just to get income as well.

The taxman also takes a cut from your gains, unfortunately. And this comes in the form of being liable to pay capital gains tax. And when you receive dividends, you are taxed on your income and interest as well.

So, this applies to every legal investment you do. You will be taxed. This is where the tax-free savings account actually comes in. And it’s in the name: tax free.

This means that you can open account in your name, in your kid’s name, in your spouse’s name or your grandma or whatever, and that is actually tax free.

You can look at it like this: when you look at all the pockets on your pants, that one small pocket which you can only stick one finger in, that’s your tax-free savings account. This means whenever you invest, you can put money in all your pockets, front, back pocket, you can go to the pocket that’s down by your knees, but the taxman is always going to come and tax your gains in those pockets. This is where the small tax-free savings pocket comes in. All the money you put in it, if you have gains or you receive income like dividends or coupons in there, the taxman does not touch it, it’s all yours.

But remember, it’s quite a small pocket. It’s got its limits, value wise. At the moment clients are only able to save up to R36,000 per year and can’t go over that. Otherwise, they will be taxed on the difference.

It’s quite a tax efficient way of investing and it’s a way to encourage individuals to actually save or should I say to invest more while not actually being worried about things like tax.

The Finance Ghost: So Siya, I never thought I’d say this out loud ever in my life, but now I’m imagining what your pants look like – awkward, I know – with that pocket down the front by your knees. I feel like I don’t have a pocket down by my knees. I need to see what kind of pants you’re wearing because you clearly have more pockets than me. Maybe there’s some other ways of saving that you know about that I haven’t figured out yet.

Siyabulela Nomoyi: You need to keep up with the fashion, eh?

The Finance Ghost: Apparently! I just don’t have enough pockets. This is clearly an issue in my life, but I think the point is that you’ve got to take advantage of the pockets that you do have. And this is why I say a tax-free savings account is just always a good idea. Even if you’re not able to max it out every year, at least do what you can.

I think the name tax-free savings is just so misleading in my opinion. I wish this thing was called a tax-free investment account because that’s the way to treat it. That’s what you should be doing with this thing. You should be putting money in and letting it grow over the long term so that you are compounding your returns pre-tax effectively. It really makes a gigantic difference. Those who understand the power of compound interest will know that if you’re compounding pre-tax gains, that looks very different to compounding post-tax gains. It really does. I’ve seen ads out there, I won’t mention specific names but I’ve seen ads of stuff like oh, save towards your wedding using a tax-free savings account. Now the issue with that is yes, it might give you a short-term boost to your savings because you’re not going to pay tax. But if you’re saving towards an event, you have to withdraw for that event, right? You’re specifically saving towards a date and when you withdraw from your tax-free savings account, that’s it, your contribution limit is a lifetime limit. There’s no allowance to say, okay, well sorry that you had to take some out, don’t worry about it, you can put that back in later. Once you’ve hit your lifetime limit, you’ve hit your lifetime limit.

What are your views on this? Do you also wish it was called a tax-free investment account like I do?

Siyabulela Nomoyi: Yeah, so funny part about this Ghost is that if you go on the SARS website, it’s actually called the tax-free investment. It’s actually TFI there. They are literally talking about investing and not savings. There you go. It’s actually tax-free investments. But look, there’s a long list of providers who offer this type of account either through a licensed bank or an FSP, insurers and the government and so on. Some of them actually have savings products and I guess Ghost, marketing is not my strongest skill, but I’m guessing TFSA is much more sexier than TFIA, right?

So, back to your point, I would encourage anyone to make use of tax-free savings accounts for long-term investing rather than short-term savings. I mean you’re quite right when you’re saying that it’s going to give you a short-term boost, but you really want to realize that over the long term. And for the positions that you buy inside your – I’m going to call it a TFSA to shorten it – all the income and realized gains are all yours. You can rotate between positions, buy and sell positions in there like ETFs or unit trust without worrying about hitting tax deductions.

A tax-free savings account should be untouched money. It should not be your emergency fund or your wedding savings. It should be there for the long-term. If you started investing to the annual limits from the start when they introduced this thing back in 2015, by 2030 you should be hitting the R500,000 lifetime limit. If you have this invested in capital markets, it’s a huge advantage on how much you would be avoiding to pay on tax. The opportunities there are actually endless.

The Finance Ghost: Yeah, absolutely. It’s also why I say even if you can’t do the full amount in a year, do what you can because if you have a windfall next year, you can still only do R36,000 in a tax year. Even if you have the year of your life, you’re going to have to then wait and max it and then the following year max it again. So don’t let a year go by in which you put nothing in. If you can’t do R36,000 then you can’t do R36,000. But even if you can just do R10,000 or R12,000, it’s R1,000 a month, it makes a significant difference.

To your point, there’s a lot you can do around rotating exposure, etc. That’s some of the more advanced concepts and maybe we can chat about a few of those later. That’s certainly something that I very much enjoy doing in my tax-free savings account. It’s something we’ve talked about before and I’ve written about before on various platforms.

I think before we get to that, people need to understand what they can actually buy inside a tax-free account. You’ll sometimes hear people talk about how it’s quite limiting and you can’t go and punt on single stocks. And yes, that’s true. If you want to do some trading, the government is not going to give you a tax-free outcome there. That kind of behaviour is not what they are encouraging here. They are trying to encourage saving and investing, hence the instruments that you can buy are limited, but it also isn’t really limited because you can pretty much buy the entire suite of ETFs or exchange traded funds of which Satrix has a huge range.

I think this is a good opportunity to maybe just open the floor to you to just on a high-level explain what that ETF universe looks like. Because it is so much more than just oh, I’m going to invest in the JSE Top 40.

Siyabulela Nomoyi: Firstly, yeah, I think it’s important to know that an individual can actually open as many tax-free savings account as they want. The only thing you need to keep track of is the annual R36,000 limit. Well, that’s the limit at the moment. If you’ve got those different pockets and different providers, you can actually split that R36,000 and as you mentioned you can actually split that over the year. People do debit orders over the year for this to actually have it add up through the year. You can split that amount amongst your tax-free savings accounts but just be careful on not going over that limit.

Now, the underlying investments here, you could have this in a fixed deposit, you can buy unit trusts under it. Also what you have mentioned, you can buy ETFs and have exposure to them in your tax-free savings account. The longer your investment horizon, or should I say your term of investing, the more you would actually probably want to be bit aggressive in terms of what you want under your tax-free savings account. Also, if you have an investment that you know generates a lot of income, maximizing exposure to them using the tax-free savings accounts is also actually a good idea.

Investors have access to a wide choice of local and international funds covering all risk profiles. Our ETF landscape in South Africa allows investors to choose from quite a lot of options. Just talking about ETFs in general in South Africa, 117 ETFs listed on the JSE, that’s actually more than the tradable universe of stocks on the JSE! That includes the 26 active ETFs recently listed on the stock exchange.

From that, investors have a choice of investing in foreign equity ETFs which have 50% of the entire ETF landscape, while they can also invest in local equities and bonds and whatnot. If you go into the Satrix universe, there’s plenty of choice there. We have about 38 ETFs listed on the JSE out of that 117, so you can have exposure to tracking indices like the MSCI World, the S&P 500, the Nasdaq. Internationally there’s quite a lot of opportunity there in terms of diversification.

Also, you have the choice of investing in our property ETFs if you are looking for yield and generating income, or a divi kind of strategy. The Top 40 that you mentioned, if what you want is beta exposure to the market at a very low cost, then that’s where you’d want to actually be in. Unfortunately, you can’t buy individual stocks. I think you mentioned that. You can’t buy commodity ETFs, the government doesn’t want you to be taking too much risk. As you said, the aim there is to actually encourage people to save and invest.

Those will be your limits in terms of what type of products you can go for. But in terms of investing in ETFs and also unit trusts, there’s quite a lot of variety there. Whether you are just going the Satrix route through our Satrix platform or you go another route from a broker.

The Finance Ghost: I think an important point to raise here is when you’re looking at all these options, just take into account where you’re going to get the best tax benefit. The point of a tax-free savings account – everything you can buy in your tax-free account, you can also buy in a normal account. Because you are limited in your tax-free savings account, let’s assume you have the financial means to invest more than R36,000 rand a year and you’re maximising your tax-free account and you’re doing more than that on top. Great! Now you’ve got to think to yourself, okay, what do I put in my tax-free account versus the rest? And here you need to look at: where am I paying the most tax?

For example, property funds, specifically REITs, they are taxed as income. It’s as though you owned the property and you rented it out to someone yourself, right? You are taxed at your income tax rate. You are not taxed at a capital gains tax rate, you are not taxed at a dividend withholding tax rate, both of which are much lower than an income tax rate. On a property fund you’re going to pay a lot more tax. In fact, you’re going to pay – I think it’s probably the highest. Even if you go and buy government bonds and you earn interest, everyone still gets a certain amount of interest free every year. But you don’t get any allowance for, hey, I got some REIT dividends, so I think that’s effectively your biggest tax burden. If you like property funds and property funds are something you want to own long-term, then that’s a really smart inclusion in a tax-free savings account because there are some very good property ETFs available.

As I say, those property distributions then are tax free. Remember, REITs themselves basically don’t really pay tax. What’s happening is you are then turning yourself into a little pension fund, right? You’re saying, I’m going to go and invest in these REITs, they don’t really pay tax, I’m not paying tax in my tax-free savings account. There’s zero leakage. It’s the same life that pension funds enjoy when they don’t pay tax. That’s why pension funds love investing in property funds so much.

So, that’s quite a favourite of mine. It just shows the value of the tax-free savings account. It’s in the name, it’s the “tax-free” piece. So, make sure you understand that stuff and think about where you’re going to put your money accordingly, right?

Siyabulela Nomoyi: 100% Ghost. I think the other part that I would mention is that when it comes to long-term investing, when you think about your kids, you think about the investment horizon or the time that you would want them to have an investment account. If you are saving or investing for your child to be at university and they’re still quite small, that’s quite a lot of years to actually be invested. You want to be investing in a product where the capital gains that you’ll be realizing in 15 years’ time, they’re all coming to you. You don’t want to be having this investment that has grown quite a lot over the years and then suddenly when you want to actually disinvest, you have all these tax payouts that you actually need to take care of.

I think the other part of that, outside the income part, is also just the underlying products that you consider and would like to actually hold for the long term where you don’t want to be taxed on your realized gains. I think that’s also very important for investors as well.

But definitely the part which I also consider as well is the REITs, the property funds, where there’s yield, that part where you get taxed more. You need to consider that.

The Finance Ghost: Yeah. I want to touch on this concept of how a tax-free account kind of becomes this beautiful little walled garden of money. You build it up every year, you put your R36,000 in or whatever it is that you can do, or if they ever actually increase that limit, we can only hope, then you’re building up over time.

This actually becomes quite a meaningful amount of money a few years down the line because remember, it’s growing as well. That R36,000 a year is your contribution limit. Obviously the great hope is that it’s growing in the background, it’s compounding all the time, so it can actually become quite a chunk of money over time.

That goes back to that point about how you can then rotate exposures. If you have made a lot of money, say on the US market through the S&P 500 or the Nasdaq-100, and let’s say valuations have gotten to a point where you’re now feeling quite uncomfortable, but you really like what’s going on in South African property, you like where we are in the cycle, you can now rotate exposure. This is a very real-world example because it’s exactly what I did. You can now rotate exposure, reduce some of your US exposure, jump into SA property, all doing this via ETFs and there’s zero tax leakage along the way.

Now I know that this can be done through a brokerage account, but the question I wanted to ask you is: on the SatrixNOW platform, which is another way to invest in ETFs, does it also allow for the buying and selling of ETFs within a tax-free savings account? What sort of functionality does the platform have in that regard?

Siyabulela Nomoyi: Sure. Thanks, Ghost. The SatrixNOW platform certainly allows for that. The platform allows investors to open under their name a standard direct investment account. They can open a retirement annuity and a tax-free savings account. You have that under your profile and have these different tabs that you can actually go and switch between. Once you’re in, you can choose from what I call the Satrix universe of products. You switch between ETFs in the platform, as you mentioned, so you can gain exposure to for instance, your Satrix Top 40 ETF.

Then if there is a point where you want to rebalance against your portfolio and want to buy property, the Satrix property ETF or the unit trust, or you want the international route where you want exposure into the Nasdaq or our infrastructure ETFs, you can actually do that inside the platform. I don’t like talking about withdrawals, but that’s also there as well as part of the platform. If you have been investing with us for quite a number of years, you want to withdraw money from your investments, you can certainly do that. You can also deposit, you can arrange for debit orders on the platform where you can actually split your debit order, whether you want to buy into one individual ETF or you want to split your debit order between different products, you can do that. So if you want, with your debit order, you can have that directly investing in one product as your product of choice or you can split it, have 50% in setting a certain ETF or unit trust. You can set that up in the platform.

As I mentioned, you can switch between ETFs on the platform. You can deposit, you can withdraw money from the SatrixNOW platform. The reason why I’m saying I don’t encourage withdrawals or I don’t like talking about that – I mean, there’s something about opening the platform and watching your money grow. It doesn’t have to be on a daily basis. That’s where a lot of investors actually start panicking. When you refresh your platform every day, you’re looking at your returns on a daily basis. If you’re investing for the long term, you don’t want to be doing that. You can check and see if your views, I guess, on what you invested still match with what you have as an exposure on your portfolios, but it’s always good to actually just go and check what your returns are in the platform.

You can download statements. But of course, the other advantage if you are in the SatrixNOW platform is that there are no minimums to investing. You can literally buy an ETF with your last R10. You can deposit the money to the platform and you can just buy a fractional share of the ETFs.

You can also get access to it through the SatrixNOW app. You can download that from your app store and you get exactly the same stuff that you see on the website on the platform. You log in there, you just check on your investments, you can switch between the products or on the app as well and also you can switch between the products inside. Let’s say if you want to disinvest money from your direct investing product and you want that money to go into your tax-free savings account, you can do that in the platform. I’ve seen people who actually get dividends from direct investments and then they want to take those dividends and invest them into topping up their tax-free savings account. You can actually switch between those platforms. You get everything there. The only thing that you can actually trade in the platform is the Satrix universe. All the unit trusts, all the ETFs that you can invest in Satrix, they are all in there.

The last part I wanted to mention is that you can also buy vouchers to gift people, which is I think the quite cool and unique way of gifting. You can buy a voucher, let’s say for R2,000, you can allocate to someone and then they can actually start the investment journey, which is, I think it’s a great way of starting or a great way to actually gift someone.

The Finance Ghost: Yeah, absolutely. All of these are really important points and I think the debit order can be really powerful. South Africa doesn’t have a budget right now, but you certainly should as a listener to this podcast! That means that if you understand how much you can save every month, if you set it up as a debit order, you can actually get to your limit every year just with a monthly debit order. It’s happening consistently in the background and you’re just managing your month-to-month expenses and in the background you’re busy saving.

That works really, really well for someone who’s maybe not watching the market all the time and trying to pick exactly what they’re doing. To your point here, sometimes that behaviour is really not a good way to create wealth over the long term. People look at this the wrong way.

I think speaking of the ways to do it, maybe as we bring this podcast to a close, I think it might be quite fun to talk about how we each use our tax-free savings account. To the extent you are willing to share, what are some of the ETFs that you have in yours? Is it a bit of a mix between local and offshore? What do you look at?

Siyabulela Nomoyi: Yeah, so currently it’s actually quite concentrated on what we spoke about and that’s going to be the Satrix Property ETF. I feel like the SA equity valuations are cheaper when you compare them to offshore, so I also have a big exposure into our Satrix Capped All-Share ETF in the tax-free savings account. This is for the long term because this is definitely money that I don’t actually touch. But also as I mentioned when we were starting the podcast, sometimes you want to be more aggressive, especially if you’re looking over the long term. Certainly the Satrix Resi ETF is one of the ETFs that I hold and quite a big chunk of it because some of these miners are also still paying dividends. They made up quite a lot of the divi strategy, which means they do actually pay quite a lot of dividends, but they’ve been battling quite a lot. I’ve been buying up some Resi exposure in the last period to actually have that turnaround in that ETF. It’s one of my favourites anyway, if you look at it over the long term as well.

Then just exposure to the US market, I mean the valuations are quite high. I’ve reduced my exposure there and I think I’ve taken my gains there. As you mentioned with the rotation part, I think I’ve done my part there, but I still do have a bit of exposure just to follow what the sentiment is in the US markets.

The Finance Ghost: So yeah, in terms of what’s in my portfolio, I’ve got the Satrix S&P 500 ETF. That’s quite a big exposure for me. So obviously that’s giving me the offshore exposure. Then there’s a Satrix Property ETF as well, and as mentioned earlier, I really like the fact that I get the REIT distributions tax free. That’s been nice for me. There, when you’re looking at the performance in your portfolio, you have to be careful because it’s going to show you, I guess depending which platform you use, it’s going to show you the capital growth. But a big part of why you would invest in property is because you’re earning dividends and those would then land in the cash portion of your account. They won’t necessarily show as a gain on that position, but in reality your total return on that position should include the dividend. So that’s just an important nuance.

Similarly, I think you’ll be proud of me here – a bond ETF! We’ve done some fixed income ETFs before, Siya, I see you nodding there happily. Kind of a similar vibe, I guess, in terms of earning interest, so there’s a tax benefit there. Yes, I made the point earlier around getting an annual amount of interest tax free, but once you go above that then you’re no worse off whether you’re earning interest in your tax-free savings account or a REIT distribution. So that’s just quite interesting diversification.

I’ve got some other stuff in there as well. Obviously, there’s a wide world of ETFs out there, but I think what’s great about Satrix is you have a really good mix of products. You have the ability for people to pretty much express a view on almost anything.

Here we are at the end of February. We’re going to get this podcast out before the end of the month. And if you haven’t maximised your tax-free savings, then just try your best to get it in there. If you can’t do anything about it still this tax year, then at least plan for the coming year to try and do as best as you can with your tax-free savings account. It really is the starting point, in my opinion, for anyone. If you’re interested in shares or whatever, that’s where you start. Until you’ve maxxed out your tax-free savings account, I genuinely don’t think that anyone should be dabbling in single stocks. Go and get the market exposure, go and start buying those ETFs and learn about how the markets work. That’s very much my view. It’s the approach that I’ve taken with my money. It’s the approach that when friends and family ask me for an opinion, it’s the same opinion that I give them. That’s just my approach, Siya. I’m really grateful that you could join me on this show to unpack why these tax-free investments are so valuable.

Siyabulela Nomoyi: Awesome, Ghost. Thanks so much for inviting me. It’s been a great topic to go through.

The Finance Ghost: I think just to finish off for those who are interested in SatrixNOW and want to go and find out more and invest that way, what is the website that they can go and visit?

Siyabulela Nomoyi: Yeah, so they can go to satrix.co.za. Obviously that website will show them the info about what Satrix is about, but there’s also a tab where they can actually register or log in to our SatrixNOW platform. They can go directly to the SatrixNOW platform if they search for it or they can go to the website, they can register. It’s quite quick these days.

Back in the day when you register on these platforms you have to wait for FICA documents to actually run. So now it’s all running in the background. You can register now and within a day or so you’re ready to actually invest and deposit your money.

They can go on that website. As I mentioned, the other alternative is download the SatrixNOW app on their app stores and also just log in there.

The Finance Ghost: Absolutely. Nice and easy and well worth it. So to the listeners, if you’re not already busy with a tax-free savings account, go and check it out, do the research. And Siya, maybe one of the next shows we should do is about how to read the fact sheets of these exchange traded funds, these ETFs so people can understand what the options are to look at.

But I think that’s a great topic for another show and we’ll do one of those soon. This one was very much about these tax-free investment accounts. So thank you for joining me for that. And to the listeners, as I keep saying, go and check this out. You really are leaving money on the table if you’re not taking advantage of this.

Siya, thanks. I look forward to having you back.

Siyabulela Nomoyi: Awesome man. Thanks. Cheers.

*Satrix is a division of Sanlam Investment Management.

Disclaimer:

Satrix Investments (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities. The information above does not constitute financial advice in term of FAIS. Consult your financial advisor before making an investment decision. Collective investment schemes are generally medium to long-term investments. In Unit Trusts and ETFs the investor essentially owns a ‘proportionate share’ (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With unit trusts, the investor holds participatory units issued by the fund, while in the case of an ETF, the participatory interest, while issued by the fund, is made up of a listed security traded on the stock exchange. ETFs are index-tracking funds, registered as a Collective Investment, and can be traded by any stockbroker on the stock exchange or via investment plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments/units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document (fund fact sheet) or upon request from the manager. Collective Investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document. The manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The index, the applicable tracking error, and the portfolio performance relative to the index can be viewed on the ETF Minimum Disclosure Document and/or on the Satrix website. A feeder fund is a portfolio that invests in a single portfolio of a collective investment scheme, which levies its own charges and which could result in a higher fee structure for the feeder fund. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information. A money market portfolio is not a bank deposit account. The price is targeted at a constant value. The total return to the investor is made up of interest received and any gain or loss made on any particular instrument and in most cases the return will merely have the effect of increasing or decreasing the daily yield, but that in the case of abnormal losses it can have the effect of reducing the capital value of the portfolio. Excessive withdrawals from the portfolio may place the portfolio under liquidity pressures and in such circumstances a process of ring-fencing of withdrawal instructions and managed pay-outs over time may be followed. Seven day rolling yield is calculated by taking into account the interest earned by the fund during a 7 day period minus any management fees incurred during those seven days. Income funds derive their income primarily from interest-bearing instruments. The yield is a current and is calculated on a daily basis. Tax Free Savings Accounts: Annual limit of R36000, lifetime limit of R500 000, 40% tax penalty applicable for contributions above the limit, per individual. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down.

Big tech stocks have stabilised after the DeepSeek shock in January, but will they continue to dominate the market this year, or is the next disruption around the corner? Tinus Rautenbach, head of Investec’s new trading and investing platform, Clarity, shares his views on the latest episode of the No Ordinary Wednesday podcast.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Dis-Chem’s wholesale strategy is really working (JSE: DCP)

Retail sales aren’t shabby, either

Dis-Chem has released a trading update for the five months to January 2025. Group revenue growth came in at 7.2%, which is a highly respectable performance.

Digging deeper reveals that retail revenue managed growth of 5.6%. Like-for-like sales were up 2.9%. Now, that’s not bad, but it’s clearly not the main driver behind the group number. That honour goes to wholesale revenue, which jumped 11.1%. That’s properly impressive growth!

Sales to Dis-Chem’s own stores increased 9.6%. When viewing this against the retail sales growth of 5.6%, this means their wholesale penetration rate (the proportion of products in a Dis-Chem store that came through their own wholesaler) must’ve gone up.

The real highlight was growth in revenue from external customers, up a delightful 18.8%. Independent pharmacies increased 18.2% and The Local Choice franchises were up 19.5%.

On a Price/Earnings multiple of 27x before this release, Dis-Chem needed to post solid numbers to justify the share price. The group hasn’t escaped the pressure on the retail sector this year, with the share price down 6.4% year-to-date coming into this release. It dropped another 4.4%, so its now down over 10% in 2025. Sentiment in the sector has really depreciated recently and load shedding certainly won’t help.

Gold is the highlight at Sibanye-Stillwater (JSE: SSW)

They would also really like you to focus on adjusted EBITDA

Adjusted EBITDA is the favourite metric of tech companies, particularly in the US. It lets them reverse out all kinds of inconvenient truths, like stock-based compensation (shares issued to staff in lieu of cash). Although a scan of the reconciliation suggests that Sibanye-Stillwater doesn’t attempt nearly that level of nonsense, it’s still worth making sure that you know which metric you’re looking at when reading financials.

Sibanye has released earnings for the six months to December. One of the key selling points is that adjusted EBITDA is stable for the third sequential six-month period. The same certainly can’t be said for headline earnings. Although annual headline earnings came in slightly higher, the last three six-month periods were -R4.1bn, R0.3bn and R1.5bn respectively!

Consistent? Not quite, despite adjusted EBITDA being between R6.4bn and R6.65bn over those three interim periods.

If you dig into the segments, you’ll see even greater divergence. Sibanye-Stillwater is a diversified group, but the key exposure in recent years was PGMs. This has now changed. In this analysis, we can use adjusted EBITDA when looking at the segments, focusing on the direction of travel and relative size rather than the quantum.

If we look at full year 2023, the South African PGM operations made R17.6 billion in adjusted EBITDA and gold managed just R3.5 billion. In 2024, local PGMs suffered a collapse to just R7.4 billion, while gold grew strongly to R5.8 billion. The shape of the group has certainly changed, with other pieces like US PGMs and nickel neither here nor there. For context, group adjusted EBITDA was R13.1 billion, so everything else in the group other than SA PGMs and gold actually contributed negative adjusted EBITDA of R0.1 billion!

It’s therefore pretty clear that gold saved the day at Sibanye. This is the first time since 2017 that adjusted EBITDA from SA gold exceeded SA PGMs. Unless something drastic changes for either commodity, I don’t expect that situation to reverse anytime soon.

Notably, if you use profit before royalties, carbon tax and tax rather than adjusted EBITDA, local PGMs made more than SA gold. This was mainly due to large movements on financial instruments. The use of adjusted EBITDA does complicate things, but I think the key points stand: (1) gold has become the strongest part of the business and (2) much of the diversification at Sibanye is actually just noise.

Aside from cost cutting initiatives in the US PGM business to try and improve performance, there’s also some hope that there will be a change to US regulations regarding the Inflation Reduction Act. Alas, with the new sheriff in town in the US, counting on any previous regulatory direction to be continued isn’t wise. Sibanye has acknowledged this, hence they are pushing on with cost reductions.

The other focus area is of course the balance sheet, with net debt to EBITDA of 1.79x at the end of December 2024. After adjusting for a stream financing deal that is expected to close soon, it should drop to around 1.08x.

The share price is down 20% over 12 months. It’s down a pretty spectacular 77% over 3 years.

Nibbles:

Reunert (JSE: RLO) announced that Mark Kathan has been appointed as the successor to outgoing CFO Nick Thomson. Kathan previously served as CFO of AECI from 2008 to 2022, so he has plenty of experience in these types of roles.

I know that Altvest (JSE: ALV) is trying to consistently portray an image of being at the cutting edge of the ways in which financial markets could evolve, but I think they’ve misread the room here. The company announced that they’ve acquired a bitcoin (for around R1.8 million) as part of its treasury strategy. Altvest’s profitability is still far from proven, so should they really be adding a risk like this to the balance sheet? My view is that they need to keep things as simple as possible, particularly as there are so many other things about the group that are unusual.

In sad news from the mining industry, Harmony Gold (JSE: HAR) reported a loss-of-life incident at Mponeng Mine near Carletonville. This was the result of a fall of ground following a seismic event. It’s a reminder that mining remains a dangerous industry for those who work hard to get the stuff out of the ground.

African Dawn Capital (JSE: ADW) announced that after a “thorough risk assessment” by PKF Octagon Incorporated (or PKF as everyone just calls them), PFK has resigned as the auditor of the company. They will need to appoint new auditors.

Europa Metals (JSE: EUZ) released an odd announcement in which directors tried to reassure the market that there’s no need for the share price on AIM (the London market) to be declining. This is due to the implied net asset value (NAV) of between 2.5p and 3p per share based on the Denarius Metals Corp exposure. Europa fell to 1.2p per share and then partially recovered to 1.55p after the announcement. The directors have perhaps not heard of companies trading at a discount to NAV when the market has lost interest.

Some people will do absolutely anything to win. In some instances, we call that determination. In others, we call it greed. Just how blurry is the line between those two things? Take a lesson from the most tested athlete in the world.

In the most spectacular case of nominative determinism that I’ve seen in ages, current men’s tennis world number one Jannik Sinner received an immediate three-month suspension from WADA (World Anti-Doping Agency) earlier this month. His crime? Two positive drug tests he had last year.

Tennis stars and fans alike are up in arms over this outcome, mostly due to the perceived leniency of the punishment and the convenient timing of the ban (the three months fall precisely between the Australian and French Opens, meaning Sinner will still be able to participate in both). Sinner’s ban also didn’t result from a hearing before an anti-doping tribunal or the Court of Arbitration for Sport, as has been the case with other tennis players who have received bans in the past. Instead, his suspension was the product of a “case resolution agreement”, also known as a negotiated settlement between WADA and Sinner.

While many are accusing WADA of favouritism, there are logical reasons why Sinner has come off comparatively lightly in this case. The tennis star tested positive for clostebol, a steroid banned by the World-Anti Doping Code, in March 2024. Sinner argued the banned substance entered his system after he received a massage from a physiotherapist in his entourage who had used a cream with clostebol to treat a cut on his own finger.

Both WADA and the International Tennis Integrity Agency accepted Sinner’s version of events and have labeled his transgression as an “unintentional doping offence”. Since athletes are held responsible for the negligence of their entourage, Sinner bears the punishment despite not being directly responsible for the mistake.

Drown out the noisy debate about convenient timing and back-door negotiations, and Sinner’s case is a story of negligence – an athlete paying the price for a careless mistake. Lance Armstrong’s story, on the other hand, was pure greed. His downfall wasn’t the result of a minor slip-up but a calculated, years-long doping scheme designed to dominate cycling at any cost. If Sinner’s suspension has sparked debate over fairness, Armstrong’s scandal exposed the ruthless pursuit of victory that can corrupt an entire sport.

Hope on a bicycle

In 1996, up-and-coming cyclist Lance Armstrong was fighting for his life. Diagnosed with metastatic testicular cancer that had already spread to his lungs and brain, his odds of survival were incredibly slim. But against all odds he beat it, and when he returned to cycling the following year, the world watched.

Armstrong dominated on his return, winning his first Tour de France and launching one of the most extraordinary comebacks in sports history. He started the Lance Armstrong Foundation, later renamed to the Livestrong Foundation, which has raised over $500 million in aid of cancer research. Over the next seven years, he made winning the Tour de France look routine, claiming seven consecutive titles and transforming himself into a symbol of resilience, a global inspiration, and the face of cycling itself.

His success helped propel cycling into mainstream popularity, drawing new fans to a sport that had long struggled for global recognition. Even after retiring on a career high at 33, Armstrong couldn’t stay away. He returned in 2008, still brushing off doping allegations and insisting he was ready to put in the extra work to compete at an elite level, even at 37.

ESPN followed his return closely, profiling him ahead of his first race back, the Tour Down Under, in January 2009. But if fans were expecting a triumphant comeback, they were in for a reality check. Armstrong finished a forgettable 27th out of 127 riders.

Questions kept swirling about whether he had ever raced a clean Tour de France, but Armstrong pressed on, lining up for the 2009 edition of the race. He finished third that July, which was not the fairytale return he might have hoped for, but still remarkable given that he was 38 and had spent three years away from the sport.

The fall of the idol

Before the 2010 Tour de France, Armstrong announced it would be his final race. But as he prepared for his last ride, a storm was brewing. His former US teammate Floyd Landis (himself stripped of a Tour de France title for doping) sent emails to cycling officials, admitting his own drug use and accusing Armstrong and other teammates of doing the same.

“I want to clear my conscience,” Landis told ESPN at the time. “I don’t want to be part of the problem anymore.”

Armstrong, as always, denied everything. He dismissed the accusations as baseless and insisted there was no proof. Seemingly unshaken, he raced in the 2010 Tour de France just months after the Landis revelations, finishing a lackluster 23rd. In press conferences around that time, he continuously referred to himself as “the most frequently tested athlete in the world”, and claimed to have been tested more than 500 times over the course of his career without a single positive result.

His second attempt at retirement didn’t shield him from the growing scandal. By 2011, more of his former teammates started speaking out, previewing the damning evidence they would ultimately provide in the US Anti-Doping Agency’s (USADA) case against him.

In October 2012, USADA released a scathing report that left no room for doubt: it proved that Armstrong had doped for most of his career. He chose not to fight the charges, and the consequences were swift and brutal. Every achievement from August 1998 onward was stripped from him, and he was banned from cycling for life.

Three months later, in a much-hyped sit-down with Oprah Winfrey, Armstrong finally confessed. The interview can only be described as flat and emotionless. Armstrong admitted to doping in every Tour de France he had competed in and won, and while he admitted that he knew that this was wrong, whether he truly regretted it remained unclear.

After his admission of guilt, Armstrong’s empire crumbled overnight. Every major sponsor cut ties with him, and he reportedly lost $75 million of sponsorship income in a single day.

In February 2017, a federal court ruled that a $100 million civil lawsuit against Armstrong (initiated by Floyd Landis on behalf of the US government) would go to trial. The case revolved around the US Postal Service, which had paid Armstrong and his team $31 million in sponsorship money between 2001 and 2004. The Department of Justice accused him of breaching his contract and committing fraud by repeatedly denying his doping.

Armstrong settled the lawsuit in April 2018, agreeing to pay the US government $5 million. It was far less than what was originally sought but still a costly reminder of his downfall.

Choose how you want to win

Armstrong’s story offers us more than a juicy sports scandal. It’s also a masterclass in what not to do in business. His calculated deception may have brought him years of dominance, but the price of cutting ethical corners was total ruin. The same applies to businesses and brands that prioritise short-term wins over long-term integrity. Fraud, false promises, and unethical practices may offer a temporary edge, but eventually, the truth surfaces. And when it does, the fallout can be swift and unforgiving.

Reputation is a company’s most valuable asset. It takes years to build and seconds to destroy. Armstrong spent over a decade crafting the image of a champion, a survivor, and an inspiration, only to see it unravel in a matter of months. Perhaps the best symbol of Armstrong’s tattered legacy is the rebranding of his foundation from the Lance Armstrong foundation to the Livestrong Foundation – a directional change that was made in 2012, when the USADA report was released. A CNN article from that year reported that many former supporters of the Livestrong Foundation were defacing their iconic yellow wristbands in protest. Some crossed out the “V” in “LIVESTRONG” to spell “LIE STRONG,” while others altered the lettering to read “LIVEWRONG”.

Sustainable success isn’t about how quickly you can get ahead, it’s about whether you can withstand scrutiny when it comes. And take it from Lance Armstrong – it always comes. The businesses that endure aren’t the ones that take shortcuts. They are the ones that build something rooted in integrity.

In the end, the greatest victory isn’t in fooling the world. It’s in never having to.

And as for Jannik Sinner – let’s just hope that the only dirty thing going on really was the cut on the physio’s finger. Armstrong’s story tainted the world of cycling and the same would happen in tennis.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Adcock Ingram has released results for the six months to December 2024 and they were below expectations. Demand was an issue, particularly as pharmaceutical wholesalers went through a period of destocking. For a production-focused business like Adcock Ingram, a drop in volumes is bad news for margins.

Sure enough, a 1% decrease in revenue was made worse by a 5% decline in gross profit and a 9% drop in HEPS. This is a classic case of operating leverage working against a company, as fixed manufacturing costs are only your friend when volumes are going up. The worst of the pressure was felt in the prescription business, where revenue fell just 5% and yet profit was down 52%!

Sadly, they do not expect to see an increase in output at the Wadeville facility in the next six months. The single exit price adjustment of 5.25% should relieve some of the margin pressure. In the meantime, Adcock Ingram plans to find more brands and partnerships to boost sales.

The interim dividend fell by 8% to 115 cents per share.

AECI expects a huge drop in HEPS (JSE: AFE)

The market didn’t seem to mind

AECI’s share price came into this update down 12.7% in the past year. It had tanked 22% over 6 months. The market knew that there were troubles at the firm, with a trading statement confirming that earnings are deeply in the red.

How red, you ask? Well, HEPS is expected to be between 32% and 42% lower. The expected range is 662 cents to 770 cents for the year ended December 2024. Although the direction of travel is clearly negative, the market responded positively with the share price up 5.4% by lunchtime trade.

The release is strongly based on a narrative of this being a transition year full of difficult decisions that were required to position AECI for better growth going forwards. For an example of a silver lining in the group, AECI Chemicals actually grew EBITDA by 25%. AECI Mining’s EBITDA was down 13%, but there were large once-off costs related to plant shutdowns and the momentum into the end of the year was positive.

If we read deeper, we find that there were R860 million worth of non-recurring costs in the group. This included R467 million went to transformation project costs and R186 million linked to business sales. They’ve also noted R204 million in investment spend on statutory shutdowns, although we are now really stretching things to suggest that a statutory requirement is non-recurring. Is it a once in a lifetime requirement? Happy to be corrected if that’s the case, but I somehow doubt it.

AECI Schirm Germany also remains a headache, with R56 million in turnaround costs. This excludes substantial non-cash impairments that impacted earnings per share (EPS) but not HEPS.

AECI Much Asphalt is recognised as a discontinued operation as it is being sold to Old Mutual Private Equity for R1.1 billion. That deal is expected to close in the first half of 2015. They recognised R732 million in impairment costs on this asset, net of tax.

After a year of focus on the turnaround, investors will expect to see results in 2025.

An ugly set of numbers at Anglo American and things are getting even worse at De Beers (JSE: AGL)

Do you believe me yet about lab grown diamonds?

I first started writing about lab grown diamonds in August 2023. To my knowledge, my column in the Financial Mail (alongside my writing in Ghost Bites of course) was one of the first arguments put forward in South African financial media about the threat to mined diamonds. A lot of people disagreed with me at the time.

Billions of dollars in impairments later at De Beers and those dissenting voices have all but disappeared. The debate now isn’t whether lab grown diamonds are a fad. It’s whether mined diamonds have any staying power at all.

My view hasn’t changed in the past 18 months. Mined diamonds should be luxury products (they should always have been luxury products instead of affluent products) and this means higher prices and lower volumes. Unfortunately, this doesn’t work for the way De Beers and the broader diamond industry has been set up in terms of the cost base, so there is much pain and disruption in this space.

If you search the words “lab grown” in the latest Anglo American report, you’ll find the reference in the impairments section. There’s something rather poetic about that, as disruptive forces have precisely that effect on dominant players in the market: a reduction of value. At Anglo, you’re just witnessing an extreme version of it.

The net impairments of $3.8 billion at Anglo took the loss attributable to shareholders to $3.1 billion. To ignore impairments and get a sense of maintainable earnings, we can look at headline earnings of $875 million for the year. Sadly, that’s way off $2.5 billion in the prior year. HEPS is the metric that the market will use and it fell by a spectacular 65%.

If you wondered why Anglo needed to strip a huge dividend out of Anglo Platinum before that demerger, wonder no longer. Between that dividend and the sale of the steelmaking coal and nickel businesses, they will generate cash of roughly $6 billion. Of course, this in no way solves the huge headache of what to do with De Beers. They are planning to “separate” it, but who will buy it? Are they hoping to just unbundle it to shareholders and make it their problem?

Even copper production fell by 6% year-on-year, so there really isn’t much to hang your hat on here. They at least generated much stronger profits in copper, up from EBITDA of $3.2 billion to $3.8 billion. Sadly this was nowhere near enough to make up for the drop in iron ore from $4 billion to $2.7 billion.

De Beers is a small part of Anglo, with a loss of $25 million in this period vs. profit of $72 million in the last period. The lab grown issue therefore isn’t the biggest challenge at Anglo American. It’s just a juicy story that shows how no company or sector is immune from disruption.

They have copper on the brain at Anglo and it is now the largest individual contributor to EBITDA. To add to that momentum, they separately announced that a memorandum of understanding has been entered into by Anglo’s 50.1% owned subsidiary and the Chilean state-owned mining company Codelco for a framework to implement a joint mine plan for the adjacent copper mines owned by the two companies in Chile. Anglo reckons that the net present value (NPV) uplift is $5 billion and half of that will be attributed to the subsidiary. It therefore seems as though $2.5 billion in value has been created here for Anglo shareholders, according to my interpretation at least. It’s all paper money anyway, for now.

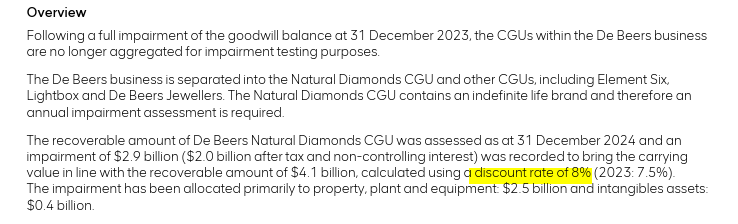

That almost makes up for the $2.9 billion impairment that was recognised at De Beers in this period. Diamonds may be a small contributor to profits at Anglo, but there’s still a carrying value of $4.1 billion here. Also, they calculate the carrying value using a discount rate of 8%, which in my view is impossibly low. It should be a lot higher to reflect the risk, in which case the impairment would’ve also been higher. Here’s the relevant section:

As a fun final comment, one of the strategies is as follows (lifted straight from the report): “De Beers also announced the launch of DiamondProof™, a new device to be used on the jewellery retail counter for rapidly distinguishing between natural diamonds and lab-grown diamonds.”

I just love the name DiamondProof. They are still trying to desperately convince the world that natural diamonds are chemically superior to lab-grown diamonds. Both are diamonds – one is just a much cheaper way of getting them. Consumers have voted with their feet (or ring fingers).

Flat revenue at Barloworld (JSE: BAW)

Will this inspire more shareholdersto take the money and run?

With Barloworld under offer from the consortium that includes its CEO, the release of a trading update for the four months to January 2025 is a helpful way to assess recent performance. With revenue growth of just 1%, there hasn’t been much performance to talk about!

Of course, as you dig deeper, you find divergence in growth. The southern African mining sector has been struggling with lower commodity prices (with the exception of gold and copper), which means less capital investment in the assets that Barloworld supplies. Thankfully, the environment in Mongolia is one of growth and this helped to offset the pressure.

Despite a 4.7% drop in revenue in Equipment southern Africa, they managed to generate higher operating margins and offset some of the impact in that business. As for Mongolia, revenue growth of 80% is pretty wild. Before you get too excited, the Russian business saw revenue drop by 23.3% and is only slightly above breakeven levels. Over at Ingrain, revenue grew 1.6% and both gross and operating margins moved higher.

If you read between the lines here, I think there’s a decent chance that the profit performance was better than revenue growth. Still, it’s not a strong period at group level. A pre-close update closer to the end of March will hopefully give more details on profitability.

And in case you’re wondering, the independent investigation into potential export control violations is ongoing.

Flat earnings at Blue Label Telecoms (JSE: BLU)

It remains by far the best performing telecoms share price over 12 months

Those who were willing (and able) to pick through the Blue Label Telecoms web of financial reporting were richly rewarded in the past 12 months. So were those who opted to depend entirely on the analysis of others. And of course, momentum traders got on this train for the ride as well.

This is the beauty of the markets: there’s something for everyone. Personally, companies with such complex structures aren’t for me, hence I’ve avoided Blue Label (to my own detriment).

The numbers for the six months to November 2024 reflect flat core HEPS of 47.20 cents. Finance income helped get them to a flat result, as they were down 6% at EBITDA level.

There’s a long back-story to the deal, but essentially Blue Label has increased its economic interest in Cell C by 10%. Those who are punting Blue Label are particularly bullish on the prospects of Cell C, which does seem to have gotten into its stride in terms of its latest strategic positioning.

Distribution per share guidance is unchanged at Equites (JSE: EQU)

Property disposals have helped to reduce the loan-to-value ratio

Equites Property Fund released a pre-close update dealing with the year ending February 2025. They had a busy period of selling properties in their UK portfolio, with the first slide in the deck reminding the market that they intend to remain invested in the UK. Still, the focus remains on deploying capital into the South African market, where demand for prime logistics assets is apparently outpacing supply.

This doesn’t mean that there were no disposals in South Africa as well. Property funds are constantly looking for ways to recycle capital and improve returns. Equites is no exception, although they do note that they are close to the end of their South African disposal programme.

The impact of all these disposals is that the loan-to-value ratio is expected to improve by 400 basis points. It was 41% at August 2024 and is expected to be 37% by the end of February. The timing of property disposals might still impact this.

Naturally, they are also enjoying the decreasing interest rate environment, with new debt being priced lower than the debt being replaced.

Distribution per share guidance of 130 to 135 cents per share is unchanged.

Gold Fields enjoyed a jump in earnings despite production and cost challenges (JSE: GFI)

Thank goodness for such a strong year in the gold price

Over 12 months, Gold Fields is up 42%. AngloGold, which released absolutely incredible results earlier in the week, is up 80%. This is because AngloGold did everything right at a time when the gold price was favourable, whereas Gold Fields has some iffy underlying metrics around production and costs.

For example, gold produced by Gold Fields fell by just over 10% and all-in sustaining cost per ounce jumped by 25.8%. Although there was strong momentum in the second half of the year vs. the first half, it’s still a pity that they missed out on making even better profits. Perhaps the gold price will continue to increase and give them a chance to make up for it.

Shareholders might be wishing that they held more AngloGold instead, but there’s still nothing to feel sad about with an increase in the total dividend for the year of 34.2%.

Hulamin isn’t concerned about the latest US tariffs (JSE: HLM)

This shows you how inflationary a tariff system actually is

Hulamin has noted that around 11% of its rolled products volumes are achieved through exports to the US. This obviously makes the group sensitive to changes in the tariff structure, especially if South Africa gets hit with additional tariffs.

For now at least, we aren’t being penalised with specific tariffs. Instead, Hulamin has been paying a 10% flat rate duty that applies to most (but not all) countries. The US has now ramped that up to 25% and has made it applicable to all countries, including those that were previously exempt from the 10% duty.

Hulamin reckons that they are probably in the same net position here, as all competitors will now be subject to the 25% tariff. They hope that their relative increase in volumes might offset any overall volumes pressure.

It’s obviously difficult (if not impossible) to guess how markets will respond to tariffs. Perhaps the bigger lesson here is that tariffs are inflationary in nature, as all these aluminium products will become more expensive in the US.

A tough set of numbers at Mondi (JSE: MNP)

Margins and cash flow went the wrong way

Mondi didn’t have a particularly great time in the year ended December 2024. Revenue increased by just 1% from continuing operations. If we exclude forestry fair value gains from EBITDA, we find that EBITDA fell by 3%. This means that EBITDA margin contracted, which isn’t a surprise in the context of such tepid revenue growth.

Sadly, those forestry fair value gains are part of headline earnings and they were far lower this year than in the prior year. Combined with the dip in operating earnings, this drove a decrease in HEPS of 58%.

Cash generated from operations was also in the red, down by 26% due to working capital outflows. Despite this, Mondi kept its ordinary dividend at 70 euro cents per share. Companies would rather donate their most loved family members to science than cut their dividends.

Tiger Brands expects to meet earnings guidance (JSE: TBS)

Margins have been the recent highlight here

Tiger Brands has released an operating update for the four months to January 2025. With inflation down at roughly 2.5% for food and non-alcoholic beverages, one would hope to see a meaningful uptick in volumes. Growth in group revenue of 3% for the period means that there was a modest improvement in volumes, so perhaps South Africans are so used to tightening their belts that they keep them tight even when they don’t have to?

At least margins have a better story to tell, with product mix and efficiencies both relevant here. Although Tiger doesn’t give specifics, they make it fairly clear that operating profit has grown by a higher percentage than revenue. They expect to see earnings growth in line with the previously provided guidance to the market for the six months to March 2025. I’ve gotta tell you that I spent some time digging around for that guidance and all I could really find was an expectation of “high single digits” operating margin. The comparable interim period saw operating margin of 6.9%, so we can therefore deduce that margins will indeed be higher year-on-year.

On the corporate front, the sale of the Baby Wellbeing division is pending competition commission approval. They are also busy with the disposal of Empresas Carozzi in Chile, with most of those conditions expected to be fulfilled in March 2025.

Focus areas within the continuing business include work on distribution channels for Albany, a deliberate focus on the “Power Brands” (where Tiger gets the best return on marketing spend) and general efficiencies in the group. So, all good stuff.

Tiger is up 28% over 12 months and is trading on a P/E of 15.7x. That feels rather high to me.

Nibbles:

Director dealings:

A non-executive director of BHP Group (JSE: BHG) bought shares in the company worth around R1.2 million.

Super Group’s (JSE: SPG) disposal of its stake in SG Fleet has achieved another milestone. Australian courts have approved the dispatch of the scheme documents to SG Fleet shareholders for the general meeting of SG Fleet shareholders to approve the scheme. The SG Fleet independent expert has opined that the scheme is fair and reasonable. SG Fleet shareholders (including Super Group) must now attend the meeting and vote.

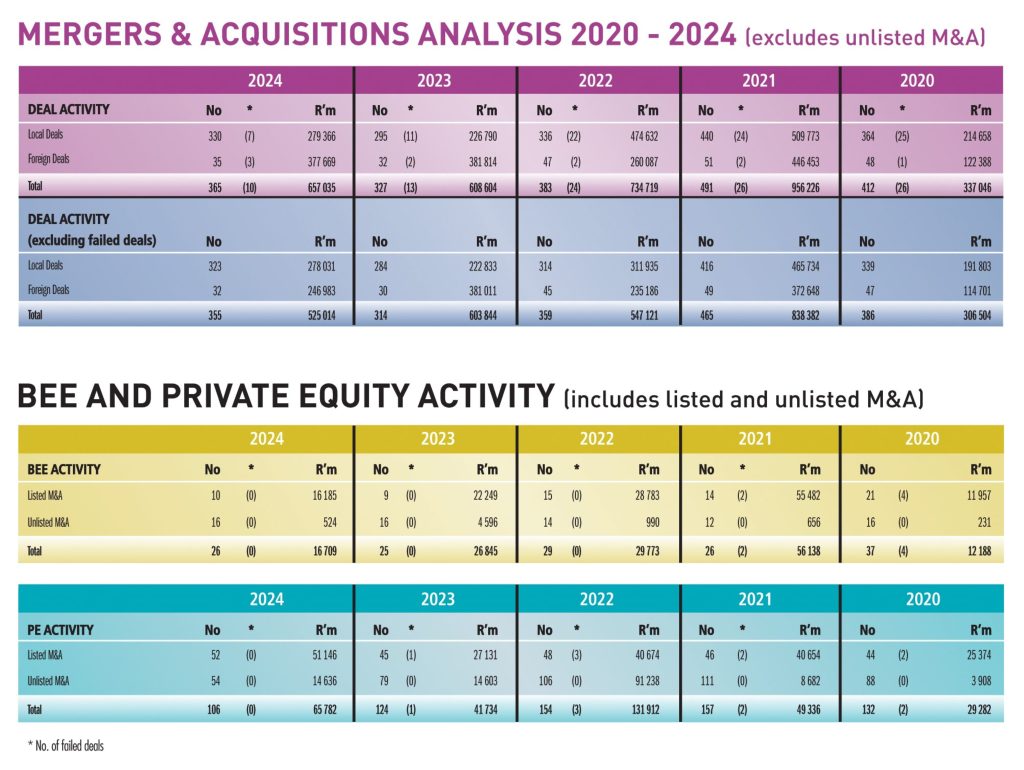

South African M&A activity in 2024 showed an improvement when compared with the previous year, with a favourable re-rating of equity prices due to a combination of economic and political stabilisation and sectoral growth, which in turn increased investor confidence.

Deals announced during the year increased 12% to 365 deals valued at R657 billion (2023: 327 deals valued at R608,6 billion). R377,7 billion of this total value represented deals by foreign companies with secondary listings on the JSE. 10 deals failed – the largest by value being Mondi’s proposed acquisition of DS Smith valued at c. R123 billion. The real estate sector remained buoyant, accounting for 34% of M&A activity in South Africa during 2024. This trend underscores ongoing investor confidence in the country’s property market, with significant transactions contributing to the sector’s dynamism.

High profile deals during the year included Groupe Canal+’s acquisition of MultiChoice – which won the award for Deal of the Year – Barloworld’s take private, and the sale by Telkom of Swiftnet, its telecom tower portfolio. The JSE welcomed WeBuyCars and Boxer Retail to the bourse, in addition to three inward secondary listings by Powerfleet Inc, Assura plc and Supermarket Income REIT plc, with a combined market capitalisation of c. R100 billion.

Behind the scenes, in what DealMakers categorises as general corporate finance activity, 275 transactions were recorded, amounting to R532 billion. Share repurchases of R217 billion accounted for the lion’s share of the total value, with the repurchase programmes of Prosus and Naspers dominating. The local listing of Boxer Retail in November was a significant event in the capital markets, with a market capitalisation at the time of listing of R29,05 billion. There were 15 listings on South Africa’s exchanges during 2024 – eight on the JSE (including three inward listings), six on A2x (with two inward listings), and one on the Cape Town Stock Exchange.

M&A activity in 2025 presents potential challenges, including global economic uncertainties and possible shifts in U.S. trade and investment policies under a new Trump administration. However, if South Africa continues to implement pro-investment reforms and stabilise key industries, the pipeline of deals could become a reality, and M&A momentum sustained.

The winners of the gold medal subjective awards are as follows:

Ince Individual DealMaker of the Year – Sally Hutton

(L-R) Andile Khumalo (Ince), Sally Hutton (Webber Wentzel), Zoe Smith (Ansarada), Laban Nyachikanda (Ince), Justin Smith (Ansarada) and Marylou Greig (DealMakers)

Brunswick Deal of the Year – Groupe Canal+ acquisition of MultiChoice

(L_R) Steven Budlender (MultiChoice), Diana Munro (Brunswick Group), Zoe Smith (Ansarada), Justin Smith (Ansarada), Marylou Greig (DealMakers)

Exxaro BEE Deal of the Year – Coronation Fund Managers

(L-R) Richard Lilleike (Exxaro Resources), Mary-Anne Musekiwa (Coronation), Anton Pillay (Coronation), Sonwabise Mzinyathi (Exxaro Resources), Zoe Smith (Ansarada), Justin Smith (Ansarada)

Catalyst Private Equity Deal of the Year – Harith InfraCo’s acquisition of assets from the Pan African Infrastructure Devlopment Fund

(L-R) Emile du Toit (Harith General Partners), Zoe Smith (Ansarada), Sandile Zungu (Zungu), Justin Smith (Ansarada) Marylou Greig (DealMakers)

Business Rescue Transaction of the Year – West Pack Lifestyle

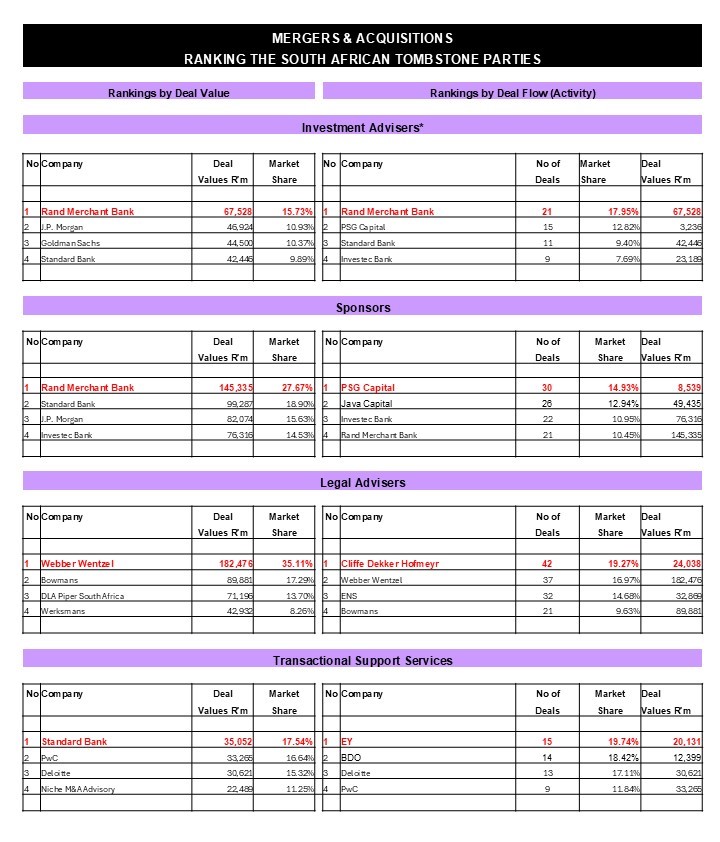

The category of Investment Adviser (by deal value) was won by Rand Merchant Bank. (L-R) Krishna Nagar (RMB), Zoe Smith (Ansarada), Justin Smith (Ansarada) and Marylou Greig (DealMakers)The category of Investment Adviser (by deal flow) was won by Rand Merchant Bank. (L-R) Krishna Nagar (RMB), Zoe Smith (Ansarada), Justin Smith (Ansarada) and Marylou Greig (DealMakers)

SPONSORS

The category of Sponsors (by deal value) was won by Rand Merchant Bank. (L-R) Valdene Reddy (JSE) and Masechaba Makhura.The category of Sponsor (by deal flow) was won by PSG Capital. (L-R) Valdene Reddy (JSE) and Mmakobela Mathabe (PSG Capital).

LEGAL ADVISERS

The category of Legal Adviser (by deal value) was won by Webber Wentzel. (L-R) Simla Ramdayal (WTW) and Christo Els (Webber Wentzel).The category of Legal Adviser (by deal flow) was won by Cliffe Dekker Hofmeyr. (L-R) Simla Ramdayal (WTW) and Roxanna Valayathum.

TRANSACTIONAL SUPPORT SERVICES

The award for Transactional Support Services Adviser (by deal value) was presented to Standard Bank. Khutso Manthata received the award from Marylou Greig (DealMakers).Femcke du Plessis received, on behalf of EY, the award for the Top Transactional Support Services Adviser (by deal flow) from Marylou Greig (DealMakers).

Winners of other awards presented on the night were:

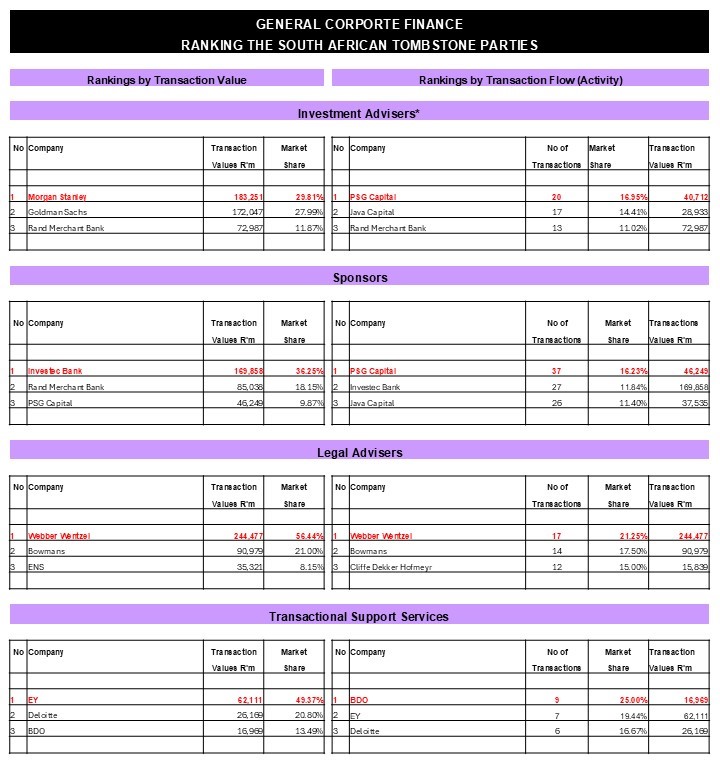

In the category of General Corporate Finance:

Investment Adviser (by transaction value): Morgan Stanley Investment Adviser (by transaction flow): PSG Capital Sponsor (by transaction value): Investec Bank Sponsor (by transaction flow): PSG Capital Legal Adviser (by transaction value): Webber Wentzel Legal Adviser (by transaction flow): Webber Wentzel Transactional Support Services (by transaction value): EY Transactional Support Services (by transaction flow): BDO

Anglo American plc has announced the signing of a memorandum of understanding between its 50.1% owned subsidiary Anglo American Sur SA and the Chilean state-owned mining company Codelco for a framework to implement a joint mine plan for the two companies’ respective, adjacent copper mines of Los Bronces and Andina in Chile. A new operating company will be jointly owned and controlled with the resulting copper production and value generated, as well as any costs and liabilities from the joint mine plan, shared equally. They will retain full ownership rights of their respective assets and will continue to exploit their respective concessions separately.

In addition, Anglo American plc has entered into an agreement to sell its nickel business in Brazil to MMG Singapore Resources Pte for a cash consideration of up to US$500 million. The nickel business comprises two ferronickel operations and two high quality greenfield growth projects. The agreed cash consideration comprises an upfront cash consideration of $350 million at completion, the potential for up to $100 million in a price-linked earnout and contingent cash consideration of $50 million linked to the Final Investment Decision for the development projects.

Vunani’s subsidiary Vunani Capital has concluded and agreement with Old Mutual Corporate Ventures (Old Mutual) to dispose of a 30% stake in each of Fairheads Benefit Services and Fairheads Financial Services businesses for R70 million. The deal will give FBS and FFS to grow activities within their core focus areas and to expand into new areas, leveraging off the skill available that comes with the strategic partnership with Old Mutual. The deal is a category 2 transaction.

CA Sales has entered into an agreement to acquire a 35% stake in Tradco Group, a market solutions business based in Kenya. Tradco offers logistics, warehousing and distribution solutions across the continent. The company has the option to increase its shareholding in Tradco by a further 20% which it is entitled to exercise at its sole discretion in the future. Financial details were undisclosed.