Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.

In the 50th edition of Unlock the Stock, Fortress Real Estate Investments joined the platform for the first time to talk about the recent performance and strategic focus areas for the group. The Finance Ghost co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

Jubilee Metals needs to make a decision soon on the Large Waste Project (JSE: JBL)

They are trying hard to de-risk the potential acquisition

Jubilee Metals had a pretty rough time recently, with production challenges due to electricity issues at the Roan project. These problems are largely behind the group now, which frees them up to work towards making a decision by mid-May on the acquisition of the Large Waste Project in Zambia. This is part of the company’s copper strategy in the country.

The incentive to do the deal is certainly there, as the price has dropped from $30 million to $18 million. If they go ahead, the $11.5 million in remaining consideration for the full deal would need to be settled over 12 months. In deciding whether to exercise the option to acquire the assets, they’ve been busy with extensive due diligence and pilot scale trials. They’ve also locked in an off-take agreement for 10 million tonnes of the estimated 260 million tonnes, valued at $6.75 million. This will give them insight into how the material performs.

You certainly can’t fault their efforts to try and reduce risk on the potential deal, with lots of clever corporate finance strategies at play here.

The Murray & Roberts business rescue plan is out in the wild (JSE: MUR)

This is a very good reminder of the difference between secured and unsecured creditors

When the wheels come off in a business, value moves very quickly from equity holders to debt holders. Equity holders get to enjoy upside potential. In return, they give away downside protection.

Murray & Roberts Limited is in business rescue and is giving us a great practical example of this situation. The straw that broke the camel’s back was De Beers pulling back on its mining capex, which essentially means that Murray & Roberts was a downstream victim of lab-grown diamond disruption! Never, ever underestimate the power of disruption. Of course, this wasn’t the only reason why the group fell over, but it was certainly the finishing touch.

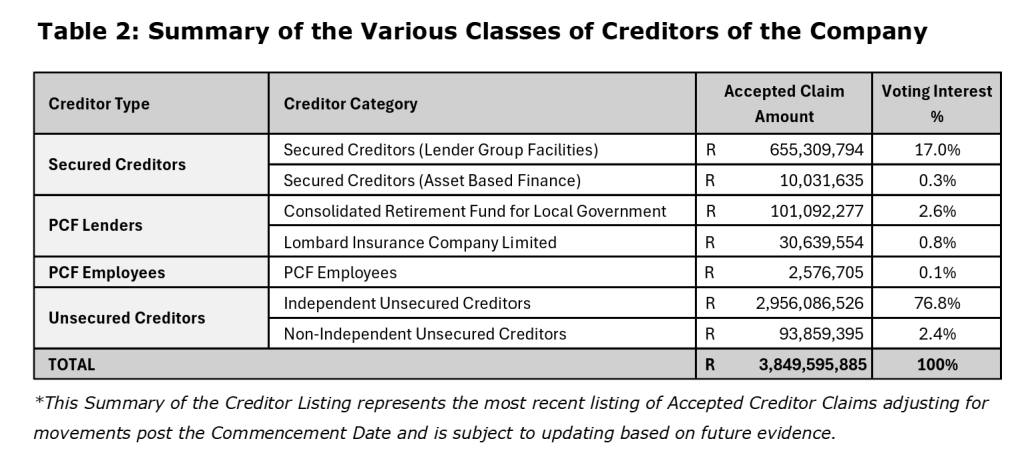

I’ll include a couple of snippets from the full business rescue plan. For example, this table shows you how the various claims against the company are tallied and categorised:

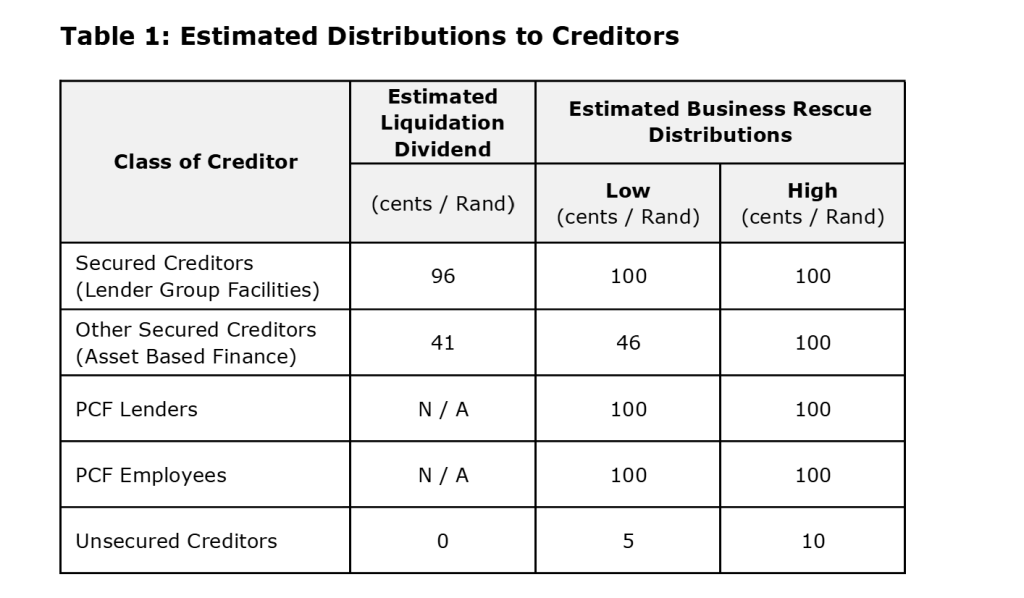

And then this table, which technically appears before the other one, shows you what each type of creditor can expect to receive under the plan:

As you can see, unsecured creditors will lose between 90% and 95% of their money. This means that there won’t be anything left for shareholders, who sit even further down the pecking order than unsecured creditors.

It’s called “business rescue” rather than “shareholder rescue” and now you can see why. So, how will the business be rescued? How will this plan be implemented? An investor named Differential Capital is swooping in on the mining assets. This transaction would facilitate the payment of the creditors as per the table above, while saving the majority of the 2,800 jobs at risk.

As this thing heads to zero, it’s hard not to think back to the ATON offer in 2018 that the board refused to back. Hindsight is perfect of course, but what a terrible journey it has been.

A change in leadership at Orion Minerals (JSE: ORN)

With the DFS reports out in the wild, Errol Smart is passing the baton

Errol Smart has been running Orion Minerals for 12 years. This journey culminated in the recent release of the Definitive Feasibility Studies (DFS) for both the Prieska Copper Zinc Project and the Okiep Copper Project. You might recall that they were released on the same day.

The focus now will be on getting these projects built, which of course means arranging all sorts of things including funding. Smart has decided that this is the moment to hand over the reins, with Tony Lennox (currently a non-executive director) stepping into the role as CEO. He has over 40 years of experience in mining, particularly in project development and operations.

This sounds like a solid succession plan.

Primary Health Properties is trying to seduce Assura shareholders (JSE: PHP | JSE: AHR)

This announcement is designed to give Assura shareholders something to chew on

As things stand, Assura is being pursued by two parties. KKR and Stonepeak are cash buyers, with the Put Up or Shut Up (PUSU – a real thing) deadline having been extended to 11 April. By that date, as the rather blunt name suggests, the parties need to either confirm that they are making an offer, or confirm that they are not making an offer.

I’ve seen the PUSU deadlines get pushed out many times in UK deals, although there aren’t usually two parties involved. I presume that the deadline has more teeth in a potentially competitive process, otherwise what would the point of it be?

The competitive tension in the deal is coming from Primary Health Properties. Hilariously, both Assura and Primary Health Properties are recent additions to the JSE. It seems like the curse of JSE delistings just won’t go away!

Primary Health’s indicative offer is a mix of cash and shares. Including the dividend that Assura shareholders would be allowed to receive, the price implies 46.2 pence per Assura share. Interestingly, if the combination of the groups went ahead, existing Assura shareholders would hold 48% of the enlarged group. Such a deal would create the eighth largest UK listed REIT.

The deal would push the combined group’s loan-to-value ratio above the targeted range of 40% to 50%. The expectation would be to return to targeted levels within 12 to 18 months of the deal being completed.

By now you must be wondering what the competing potential cash offer from KKR and Stonepeak looks like. As a reminder, the last announcement was for an offer to the value of of 49.4 pence per share (including the dividend that Assura shareholders would retain). Primary Health is therefore 6.5% below the competing cash proposal. To further complicate things, the part-share part-cash nature of the Primary Health proposal means that the value fluctuates constantly based on the Primary Health share price.

Normally, you would expect to see the part-share proposal at a premium to a clean cash proposal. I’m not sure that the promises of synergies in a combined group will be enough to get shareholders to put pressure on the Assura board to take this deal seriously.

Nibbles:

Director dealings:

Gold Fields (JSE: GFI) directors have made an absolute fortune thanks to the rally in the gold sector. A bunch of directors sold shares worth a total of R38 million. The announcement doesn’t indicate whether this was only the taxable portion of the gains.

MTN (JSE: MTN) announced various sales by directors, with a mix of taxable and non-taxable portions. In my view, the important thing to highlight is that the CEO retained a portion of the share award and so did a couple of other execs, but most of the participants appear to have sold the full awards.

The COO of DRDGOLD (JSE: DRD) sold shares worth R2.2 million.

An associate of a director of Ethos Capital (JSE: EPE) bought shares worth R560k.

The CFO of York Timber (JSE: YRK) sold shares worth R51k.

In a rare show of capital allocation maturity among listed property funds, Supermarket Income REIT (JSE: SRI) has elected to suspend its scrip dividend alternative for the latest quarterly dividend. This is due to the shares trading at a discount to the net asset value per share.

Iqbal Khan, the COO of Brimstone (JSE: BRT | JSE: BRN), has retired from the group due to health reasons. A replacement hasn’t been named as of yet.

Rebosis (JSE: REA | JSE: REB) is suspended from trading and thus needs to release a quarterly progress report. You may recall the public sale process that the company went through as part of the business rescue initiatives. The update is that all but one of the properties sold through that process have been transferred to the purchasers. The exception is Bloed Street Mall (how’s that for an ironic name?), where the delay is around a dispute on the remaining period of the land lease agreement. The City of Tshwane council is involved here as well.

Sail Mining Group (JSE: SGP) is another example of a suspended company that has released a quarterly update. After many delays, the audit is underway for the 2022 – 2024 financials. Also, the business rescue plan for subsidiary Black Chrome Mine (Pty) Ltd has been approved. They are moving ahead with a Mine Restart and Trade Out Plan, which is believed to achieve the best outcome for the stakeholders involved.

Yet another company in the naughty corner is aReit Prop (JSE: APO), a listing that I warned about at the time that it came to market. The price looked like complete nonsense to me and sadly I was proven correct. They’ve also been dealing with some technical accounting issues that led to major delays to the 2023 financials. They now expect to publish them by the end of April. They expect a large impairment to the leasehold properties to be raised. It won’t impact headline earnings or distributable income.

Nigerian energy company Oando (JSE: OAO) is also on the wrong side of financial reporting deadlines, albeit only slightly. They were meant to publish the 2024 financials by the end of March. An acquisition has delayed this process, as has the introduction of more onerous audit requirements due to a change in legislation. They expect to only get everything done by the end of May 2025.

Assura plc, the UK healthcare REIT with an inward listing on the JSE, has received an improved offer from Primary Health Properties (PHP) for an all-share combination implying an initial value of 46.2 pence for each Assura share, inclusive of the Assura dividend of 0.84 pence per share due to be paid on 9 April 2025. Under the terms of the combination, shareholders would receive for each Assura share held, 0.3838 new PHP share and 9.08 pence in cash. Based on the PHP closing share price of 94.35 pence on April 2, 2025, the 9.08 pence cash consideration would represent 20% of the total consideration. The offer values Assura at c.£1,5 billion – a 22.2% premium to the 3-month volume weighted average of the Assura share as of 13 February 2025, the day prior to the commencement of Assura’s offer period. Should the offer be accepted, Assura shareholders will hold c.48% of the combined group’s issued share capital. The cash consideration by PHP will be fully financed through new third-party debt. The Assura Board is reviewing the PHP proposal and will make an announcement as appropriate.

Liberty Kenya, in which Liberty holds c.58%, has exited its 60% stake in Heritage Insurance Tanzania, representing a strategic shift by the Kenyan company to strengthen its focus on the Kenyan market.

Accelerate Property Fund is to dispose of its proportionate ownership in the Portside Office Tower in Cape Town. Penalten Investments will acquire the ground floor retail, office floors 9-18, 623 parking spaces and related common areas for an aggregate R580 million payable in cash. The deal is a category 1 transaction and therefore requires shareholder approval. A circular will be distributed in due course.

Jubilee Metals has announced it has secured exclusive rights to the Large Waste Project in Zambia. The deal first announced in Q4 2023 was in the form of a joint venture with International Resource Holding for a purchased consideration of $30 million. Jubilee will now pay a reduced $18 million and has until mid-May 2025 to elect to acquire the assets and settle the c.$11,5 million remaining consideration over a period of 12 months.

enX has divested of its interest in West African International (WAI), a business involved in importing, warehousing and selling and distributing polyolefins, styrenics, rubber and specialised chemicals into the Southern African market. Trichem SA which is ultimately owned by the Houston based-Tricon Group, will acquire a 25% stake with the option to acquire the remaining 75% for a maximum ownership capped at R450 million. The transaction represents an attractive opportunity for enX to divest while operational synergies for WAI with a global player will unlock further value for the company.

AECI through its wholly-owned subsidiary Improchem, is to dispose of its Public Water business to a local majority black-owned special purpose vehicle, with Nsukutech as the controlling shareholder and Junaco (T), a Tanzanian company as the minority shareholder. The disposal, the value of which was not disclosed, is in line with its strategy to divest of non-core assets and to streamline operations.

In line with its strategy to exit the Namibian market, Safari Investments RSA has disposed of Safari Investments Namibia which owns and manages the Platz am Meer Shopping Centre in Swakopmund, Namibia. The disposal is to NSE-listed Oryx Properties for a cash consideration of N$290 million. Safari will re-invest the proceeds in new development opportunities in retail shopping centres in the rural and township areas in SA.

EPE Capital has disposed of 0.81% of the Optasia equity, representing an 11.1% share of its 7.3% economic interest in Optasia. EPE Capital will receive US$7,3 million for the sale of the stake to an existing shareholder.

Cilo Cybin is to approach the JSE for a further extension of the circular distribution date. The proposed acquisition of Cilo Cybin Pharmaceutical awas announced in December 2024. The company wishes to have the audit of its annual financial statements for the year ending March 2025 finalised prior to the distribution of the circular. Give this, the parties have extended the date by which the conditions precedent to the acquisition are required to be fulfilled or waived from 31 March to 20 August 2025.

In November 2024 Novus breached (together with related parties) the 35% shareholding level requiring it to make a mandatory offer to Mustek shareholders in terms of the local takeover rules. Not wanting to delist the company, Novus offered shareholders three options – cash of R13 per Mustek share, a combination of R7 cash plus one Novus share, or no cash and two Novus shares for those shareholders wanting to swap into Novus. The company received irrevocable undertakings from shareholders holding 20.29% of Mustek’s shares that they would reject the mandatory offer. Novus offered a maximum of R335 million in relation to the mandatory offer. The TRP which unconditionally approved the offer in November has now withdrawn its approval, requiring Novus to publish a revised firm intention announcement withing 20 business days – an action Novus intends to appeal against.

In November 2024 London Finance & Investment Group plc announced the sale of its liquid investments and a return to shareholders of an estimated 71 pence in cash for each ordinary share held in early 2025. The company’s listings on the LSE and JSE will cease on 2 May and on 9 May 2025 respectively.

Unlisted Companies

Smollan, a South African retail solutions company with operations across 61 markets, is the latest strategic investor in local delivery management platform Loop. The new investment together with support from long-standing investor Lightstone, will scale Loop’s next phase of growth.

Medu Capital Fund III has completed its exit from Jacana Capital, a holding company of businesses providing insurance broking, employee benefits and risk consulting to commercial and personal clients. Jacana Capital owns 70% of Bay Union Financial Services, 33% of MRA Group, 39% of STP Holdings and 25% of Kapara Insurance Brokers. During Medu Capital investment period, it contributed significantly to the development of a robust platform for insurance brokerages, enhancing governance structures and bolstering the group’s leadership.

The Public Investment Corporation (PIC) representing the Government Employees Pension Fund (GEPF) South Africa, has made an investment of US$40 million into pan-African infrastructure investor and asset manager Africa50. The PIC is the 36th shareholder in Africa50, expanding the investor’s footprint and shareholder base in Southern Africa.

SiyaQhubeka Forests, in partnership with Mondi and SAFCOL, has transferred an increased equity stake to its community empowerment partners SiyaQhubeka Community Trust. The increased stake, from 5.4% to 15.4%, marks a significant milestone in the transformation and inclusive growth of the forestry sector in South Africa.

Kore Potash has raised a further £385,000 by way of a placing of new ordinary shares at a price of 1,7 pence per share with two separate trusts related to company Chairman David Hawthorn. The funds, along with the £7,7 million raised in March, will be used to pay PowerChina International Group for optimisation work, impact assessment update, fees and working capital.

Fortress Real Estate Investments will transfer 7,534,415 NEPI Rockcastle (NRP) shares to Fortress shareholders who opted to receive a dividend in specie of NRP shares in lieu of the cash dividend. As a result, Fortress retained R831,52 million cash not utilised to pay the cash dividend.

Finbond will issue 23,392,070 shares to shareholders receiving the scrip dividend option in lieu of a final cash dividend, resulting in a capitalisation of the distributable retained profits in the company of R12,4 million.

The Board of Supermarket Income REIT plc has decided that it is not in the best interests of shareholders to offer the scrip dividend alternative in respect of the third quarterly dividend, as the company shares currently trade at a discount to the published EPRA Net Tangible Assets per share. Shareholder will receive 1.53 pence per ordinary in respect of the period from 1 January 2025 to 31 March 2025.

In an operational update, Accelerate Property Fund this week reported its immediate focus area in terms of the Group’s restructuring is the conclusion of a further fully underwritten Rights Offer of R100 million by end-June 2025. This time last year Accelerate raised R200 million in a rights offer. Funds will be used for additional capital expenditure on Fourways Mall and for working capital requirements. Shareholders will be updated in due course.

Oando has informed shareholders that it was unable to publish its 2024 Audited Financial Statements by the regulatory deadline of 31 March 2025. Reasons given included the accounting for the Nigeria Agip Oil Company acquisition and expanded Internal Controls Over Financial Reporting (ICFR) requirements. The company now anticipates completing and filing the 2024 AFS on or before May 30, 2025.

aReit Prop expects its annual financial statements for the year ended 31 December 2023 be published before the end of April 2025. The main reason given for the delay was the company’s valuation of its leasehold properties. The valuation approach has now been resolved, and a trading statement will be issued shortly. The company’s listing on the JSE remains suspended.

This week the following companies repurchased shares:

Netcare concluded a further intra-group repurchase with subsidiary Netcare Hospital Group in terms of which Netcare acquired 24,642,572 ordinary shares at a price of R12.96 per share.

Schroder European Real Estate Trust plc acquired a further 127,100 shares this week at a price of 66 pence per share for an aggregate £83,886. The shares will be held in Treasury.

On March 6, 2025, Ninety One plc announced that it would undertake a repurchase programme of up to £30 million. The shares will be purchased in the open market and cancelled to reduce the Company’s ordinary share capital. This week the company repurchased a further 481,237 ordinary shares at an average price of 147 pence for an aggregate £704,652.

In its annual financial statements released in August 2024, South32 announced that it would increase its capital management programme by US$200 million, to be returned via an on-market share buy-back. This week 1,170,548 shares were repurchased at an aggregate cost of A$3,87 million.

On 19 February 2025, Glencore plc announced the commencement of a new US$1 billion share buyback programme, with the intended completion by the time of the Group’s interim results announcement in August 2025. This week the company repurchased 12,750,000 shares at an average price per share of £2.87 for an aggregate £36,53 million.

In October 2024, Anheuser-Busch InBev announced a US$2 billion share buy-back programme to be executed within the next 12 months which will result in the repurchase of c.31,7 million shares. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 24 to 28 March 2025, the group repurchased 824,801 shares for €47,27 million.

Hammerson plc continued with its programme to purchase its ordinary shares up to a maximum consideration of £140 million. The sole purpose of the buyback programme is to reduce the company’s share capital. This week the company repurchased 321,235 shares at an average price per share of 248 pence for an aggregate £798,030.

In line with its share buyback programme announced in March 2024, British American Tobacco plc this week repurchased a further 389,348 shares at an average price of £31.36 per share for an aggregate £12,2 million.

During the period 24 to 28 March 2025, Prosus repurchased a further 4,700,875 Prosus shares for an aggregate €204,19 million and Naspers, a further 333,748 Naspers shares for a total consideration of R1,56 billion.

During the week one company issued a cautionary: ArcelorMittal South Africa.

Diageo plc has announced the sale of its 54.4% stake in Seychelles Breweries to Mauritius’ Phoenix Beverages for approximately US$80 million. Diageo and Phoenix have an existing partnership in the Indian Ocean region. Under the terms of the agreement, Diageo will retain ownership of the Diageo brands currently produced by Seychelles Breweries (Guinness and Smirnoff RTDs) as well as distribute IPS in-market, which will be licensed to Seychelles Breweries under a new long-term license and royalty agreement.

Dutch family-backed impact investor, DOB Equity has invested in Kenya’s FarmWorks, an agribusiness focused on providing smallholder farmers with consistent, off-take channels for their produce. The investment will assist FarmWorks to expand its sourcing network, boost its technology platform and broaden its product offerings.

Golden Deeps and Coniston have entered into a sale agreement for the acquisition by Golden Deep on an 80% stake in Namex, which owns 100% of Nambian company Metalex Mining and Exploration, the owner of four Exclusive Prospecting Licences in the Otavi Mountain Land in Namibia. As consideration, Golden Deeps will issue Coniston 23,103,352 new shares and make a cash payment of A$250,000. The agreement also allows for a second tranche of shares to be issued based on specific milestones.

Dislog Group will acquire a 70% stake in Morocco’s Afrobiomedic for an undisclosed sum. Afrobiomedic specialises in the import and distribution of medical devices for interventional cardiology, structural cardiology, and rhythm therapy. The company is also active in vascular interventional neuroradiology.

Egypt’s InfiniLink, a semiconductor startup founded in 2022, has closed a US$10 million seed funding round led by MediaTek and Sukna Ventures. Other investors in this round included Egypt Ventures and m Empire Angels.

Tanzanian FMCG distribution company, Sumet Technologies, has raised US$1,5 million in a debt and equity pre-seed funding round. Investors included ABAN, Catalytic Africa and an angel syndicate from Egypt.

Access Bank has provided Lagos-based value airline, Green Africa with a naira debt facility to part fund the acquisition of its first aircraft, an ATR 72-500.

ASX-listed MetalsGrove has entered into a binding term sheet with Desert Metals to acquire three gold joint venture permits in Côte d’Ivoire. The three permits (Vavoua, Vavoua West and Kounahiri West) cover a total area of approximately 950 km2.

As institutional investors have, for many years, dominated the share registers of JSE-listed companies (ListCos), it is unsurprising that shareholder activism in South Africa (SA) has, in the past, occurred mostly through private engagement, often referred to as “soft” or “behind-the-scenes” activism. However, over recent years, commentators, smaller retail investors and other shareholder activists have also become increasingly vocal and influential in pushing for greater corporate accountability amongst ListCos, including on matters such as executive remuneration, board composition, and ESG reporting and disclosure. Other shareholder activists may have purely financial goals in mind, such as pressuring companies to distribute perceived excess cash reserves, dispose of certain assets, or facilitate (or frustrate) a takeover or other M&A transaction.

In some cases, shareholder activism may benefit companies by leading to necessary operational, governance or other changes, while other campaigns could have negative impacts, such as forcing a company to prioritise immediate shareholder demands over long-term growth or to prematurely disclose its acquisition strategy or targets, which can detrimentally affect the ListCo’s share price.

There has, against this background, been a growing trend towards public activist campaigns, often conducted through social media platforms to mobilise public support and intensify pressure on ListCos.

It would, therefore, be prudent for a ListCo to pro-actively identify and address potential concerns (and update investors on progress to address previously raised concerns) before they become ammunition for a full-blown shareholder activist campaign, and to consider the steps that it should take if targeted by such a campaign.

BEFORE A PUBLIC ACTIVIST CAMPAIGN IS LAUNCHED

Maintain open lines of communication ListCos should communicate transparently and regularly with shareholders and be receptive to shareholder feedback, where reasonable. Such communication will occur primarily via the JSE’s Stock Exchange News Service (SENS) and formal events, such as annual general meetings (AGMs), but should preferably also include wide audience investor presentations, as well as one-on-one engagement with key investors (always bearing in mind that price sensitive information should only be disclosed via SENS). By fostering an “open door” culture and building a relationship with key long-term shareholders, a ListCo is able to receive valuable feedback and build trust with its stakeholders. Such engagements allow ListCos to articulate their current and long-term value proposition to shareholders, while countering any short-term issues.

Know your shareholders and understand their priorities By regularly engaging with key shareholders, analysing AGM voting trends and shareholder “track records”, ListCos can better understand the priorities of their shareholders, thereby gaining valuable insight into how they may vote if approached for support by either an activist or ListCo.

ListCos should closely monitor trading activity in their stock, considering both the company’s share price and its shareholder make-up, thereby gaining advance notice of key shareholding blocks being acquired and positions being built (e.g., in anticipation of a potential takeover), as well as known activist shareholders joining the register.

Activism trends and “pain point” check-ins ListCos should regularly consider factors that are likely to draw activist scrutiny and keep abreast of current activist campaigns in the SA market (especially involving companies in the same sector). Where a ListCo performs well and delivers strong returns, this should negate most shareholder concerns – therefore, a focus on performance remains key. The rolling list of potential “pain points” include – • Declining financial metrics • Poor share price performance (especially where it underperforms ListCo peers or the applicable index) • Low or no dividend payout • Conservative or an over-geared balance sheet • Unjustifiable executive remuneration practices • Board composition deficiencies, independence concerns and lack of diversity • ESG shortcomings, including insufficient reporting • Operational challenges relative to peers • Poor strategic decision-making • Unsuccessful mergers and/or acquisitions

Where such an issue applies to a ListCo and the company is able to resolve it, this reduces the risk of activist attacks. In other instances, the risk of such attacks (or their impact) may be minimised by explaining the approach being followed to address the concern (e.g., improving operational performance) or by setting out the company’s view on the matter (e.g., instead of distributing it now, the company is retaining cash to position itself for future accretive acquisition opportunities).

Assign a team (and be perpetually prepared) Activist campaigns are often launched swiftly and unexpectedly, creating disruption and uncertainty for a ListCo. It is, therefore, critical that a ListCo has a designated response team on standby with a strategy in place for how it will respond when facing an activist attack (including clear communication lines with the media). Without preparation (which could include mock activist campaigns to stress test the ListCo’s response framework), ListCos risk disorganised responses, potential missteps (such as premature responses on social media without having all the facts available), and reputational harm. Such designated teams usually comprise executive directors and members of the ListCo’s investor relations, legal and financial teams, as well as outside advisors (when required).

Keep pace with emerging trends Shareholder activists have become adept at using a range of tools, including social media, to maximise their impact on target companies. With the rapid advancement of artificial intelligence (AI), it is only a matter of time before activists widely leverage AI to analyse publicly available company data in order to identify vulnerabilities sooner. However, AI need not remain solely a tool for activists. It would be prudent for ListCos to explore how AI can be strategically utilised to their advantage.

AFTER A PUBLIC ACTIVIST CAMPAIGN IS LAUNCHED

Play the ball, not the man Activist campaigns often involve personal attacks on management or board members, but it is crucial to resist retaliation. Instead, ListCos should address the principal concerns raised, substantiated by facts and data. In doing so, directors and management will continue to safeguard their credibility while maintaining shareholder trust and public confidence in the ListCo’s governance practices.

Communication is the name of the game When responding to a public activist campaign, a ListCo must act swiftly to establish and control the narrative. Delays can allow others to shape public perception, potentially undermining the ListCo’s reputation and management’s credibility. The response should be tailored to the actual issue raised, the activist who launched the campaign, and the audience (including key shareholders and stakeholders). If the ListCo does not believe that the activists’ proposed changes are in its best long-term interests, it needs to explain to investors why this is the case, and how the company reached this conclusion. On the other hand, if the company has decided to make some changes, it should be open about what those are, as this will show that it is receptive to shareholder suggestions and takes them seriously.

When activists are considering “Vote ‘No’” campaigns or proxy fights (for example, on director remuneration resolutions or board elections), they will need the support of other shareholders to be effective. While they will try to influence other shareholders via public platforms, they will, in many instances, already have approached large shareholders before the campaign. It is, therefore, essential for a ListCo to engage with key shareholders early, to explain its position and to secure their support.

Proactive and transparent engagement might not necessarily end each and every activist campaign, but it will serve the ListCo in building trust amongst stakeholders and counteracting misinformation. Such engagement will be easier and more effective where the company already has a good relationship with its major shareholders, pointing again to the importance of ongoing regular interaction with shareholders.

CONCLUSION

In future, public shareholder activism in SA will likely continue to increase. One immediate cause may be the incoming remuneration-related amendments to the Companies Act, together with the increased focus on reporting and disclosures by JSE-listed companies.

It is important that ListCos position themselves proactively to respond to public campaigns. In this case, as with many things in life, failing to prepare is preparing to fail.

Henning de Kock is CEO and Johann Piek a Director | PSG Capital.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Mergers and acquisitions (M&A) in Africa have traditionally presented complex challenges, including intricate regulatory landscapes, extensive due diligence requirements, and the need to navigate diverse legal systems. For foreign investors seeking opportunities within Africa’s expanding markets, these complexities have often resulted in increased costs, prolonged timelines, and heightened risks. However, the advent of legal technology is transforming M&A transactions across the continent, introducing efficiencies that mitigate these challenges and foster a more streamlined deal-making process.

From due diligence to post-transaction integration, legal technology is revolutionising core stages of M&A transactions, offering tools that enhance accuracy, reduce human error, and improve decision-making for stakeholders.

REVOLUTIONISING DUE DILIGENCE

Due diligence is one of the most critical phases of any M&A transaction, providing the foundation for informed decision-making. Historically, legal teams would manually review extensive documentation over several weeks or months, a time-consuming process susceptible to human error. Today, artificial intelligence (AI)-powered tools, employed by leading law firms such as DLA Piper, are automating this process with remarkable efficiency.

These tools leverage machine learning algorithms to review voluminous datasets, identify risks, and highlight key information in a fraction of the time required for manual analysis. By automating repetitive tasks, these technologies ensure comprehensive and accurate due diligence, enabling foreign investors to better assess potential risks and opportunities. This is particularly advantageous in Africa, where access to reliable data can be inconsistent.

STREAMLINING CONTRACT NEGOTIATION AND REVIEW

Contract negotiation and review are central to M&A transactions, which require meticulous scrutiny to ensure alignment with legal requirements and the interests of all parties. Legal technology now plays a pivotal role in this area, utilising AI-driven tools to analyse contracts, identify critical clauses, and detect discrepancies or risks.

These platforms not only expedite the contract review process but also assist legal professionals by suggesting edits and ensuring compliance with local laws and regulations. In Africa’s diverse legal environment, such tools are invaluable for tailoring contracts to address jurisdiction-specific challenges. Consequently, investors can approach transactions with greater confidence, knowing that agreements are both legally sound and strategically advantageous.

OPTIMISING DEAL STRUCTURING AND INTEGRATION

The structuring of M&A transactions often involves balancing complex considerations, including regulatory compliance, financial implications, and strategic goals.

Legal technology facilitates this process through predictive analytics and data-driven insights, allowing negotiators to evaluate various deal structures and simulate potential outcomes.

For transactions within Africa, where regulatory requirements can vary significantly between jurisdictions, these tools are instrumental in ensuring compliance and reducing the risk of post-transaction complications. Furthermore, legal technology supports post-deal integration by managing data, streamlining communication, and providing project tracking capabilities, thereby enhancing operational efficiency and long-term success.

ETHICAL CONSIDERATIONS AND EMERGING RISKS

While legal technology offers significant benefits, it raises ethical concerns, particularly around data privacy and AI reliability. AI tools rely on vast datasets, often containing sensitive financial and personal information, increasing the risk of data breaches. In Africa, where data protection laws are still evolving, companies must ensure compliance with local and international standards.

The reliability of AI-generated outputs depends on the quality of training data. Biases or inaccuracies can lead to misleading results, as seen in Mavundla v MEC: Department of Co-Operative Government and Traditional Affairs KwaZulu-Natal and Others (2025). In this case, a law firm faced scrutiny for citing fictitious case law, potentially AI-generated. The court dismissed the appeal after finding most references were non-existent, highlighting the need for rigorous oversight.

AI also has financial and environmental costs. Training large models requires vast computational resources, contributing to carbon emissions. The recent release of DeepSeek by China has intensified market competition, raising concerns about AI’s sustainability. Legal professionals must balance AI’s efficiencies with its ethical and environmental risks, ensuring it enhances rather than undermines legal integrity.

THE REGULATORY LANDSCAPE FOR AI IN AFRICA

As the adoption of AI accelerates, several African countries are developing frameworks to regulate its use. While no jurisdiction has enacted AI-specific legislation as of January 2025, notable advancements have been made:

Egypt: Released the Second Edition of its National Artificial Intelligence Strategy 2025–2030 in January 2025.

Ghana: Published the National Artificial Intelligence Strategy 2023–2033 in October 2022.

Kenya: Unveiled the Kenya National Artificial Intelligence Strategy 2025–2030 in January 2025.

Nigeria: Introduced a draft National Artificial Intelligence Strategy in August 2024.

South Africa: Released the National Artificial Intelligence Policy Framework in August 2024, emphasising ethical AI use, personal information protection, and enhanced government efficiency.

These initiatives reflect a growing recognition of AI’s transformative potential, coupled with the necessity of safeguarding ethical standards and data privacy.

The integration of legal technology into M&A transactions is reshaping the African deal-making landscape, offering tools that enhance efficiency, reduce risks, and ensure more successful outcomes. By automating labour-intensive processes such as due diligence, matter management, and contract review, and by providing actionable insights for deal structuring and post-transaction integration, legal technology is enabling investors and legal professionals to navigate the complexities of African markets with greater confidence.

Nevertheless, the adoption of these technologies must be approached with caution. The Mavundla case serves as a stark reminder of the potential pitfalls of uncritical reliance on AI, underscoring the need for human oversight and ethical diligence. As Africa continues to refine its regulatory frameworks for AI, legal practitioners must strike a balance between embracing innovation and safeguarding the principles of accountability and professionalism that underpin the legal profession.

Tevin Ramalu is an Associate Designate and Lemont Shondlani a Candidate Legal Practitioner in the Corporate Department. Supervised by Amy Eliason, a Director | DLA Piper Advisory Services

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

I’ve had the immense joy (quite recently, actually) of seeing the view from the top of the Portside building. It’s every bit as spectacular as you imagine it would be. In case you aren’t familiar with the Cape Town CBD (the only functional CBD in the country), Portside is the very tall glass building.

It’s been a painful trophy for Accelerate Property Fund, adding to the overall illusions of grandeur that got the fund into huge trouble in the first place. COVID was of course a disaster for office property, so owning the most impressive building of the lot just meant having bigger headaches. Accelerate is focused on turning the Fourways Mall around, so they can’t afford to have any other risks right now.

After making it pretty clear recently that the “For Sale” sign was outside the door of Portside, the Accelerate has now agreed a deal with Cavaleros Group Holdings for Accelerate’s proportionate ownership in the office tower. This means floors 9 – 18, along with 623 parking bays and the common areas. I checked the last annual report and based on the GLA that I found, this means a complete exit for Accelerate from the building.

The price? R580 million. The last valuation? R609 million. That’s a discount to net asset value (NAV) of just 4.7%. Meanwhile, Accelerate is trading at R0.50 per share and the NAV per share as at September 2024 was R2.60. Clearly, the discount achieved on the Portside sale is actually a massive premium to what the share price is implying.

This stock is looking more interesting by the day. They just need to keep the bankers at bay while continuing to deliver improvements at Fourways Mall.

Life Healthcare shareholders love the LMI deal (JSE: LHC)

You won’t often seen an approval rate this high

Life Healthcare recently announced a deal to sell Life Molecular Imaging (LMI) to Lantheus Holdings. The back story is that Lantheus is the counterparty to the sub-licensing agreement linked to LMI that was announced in mid-2024. During the due diligence process, Lantheus liked the asset so much that they wanted to buy the whole thing!

It’s an elegant deal for Life Healthcare. They expect to receive net proceeds of around R3.7 billion, most of which will hopefully be paid to shareholders as a special distribution within the next year. Importantly, they retain upside exposure to the LMI products, based on an earnout linked to US and global sales. The global rollout is therefore a pressure point for the Lantheus balance sheet rather than the Life Healthcare balance sheet, with Life still able to take a clip of the future economics.

I’m therefore not surprised to see that the deal got nearly unanimous approval at the Life Healthcare shareholders meeting. It’s a clever deal that has supported a 29% increase in the share price over the past 12 months.

Nibbles:

Director dealings:

A director of a major subsidiary of AVI (JSE: AVI) received share awards and sold the whole lot to the value of R874k.

The company secretary of Bidvest (JSE: BVT) sold shares worth R807k that were related to a share award. The announcement isn’t explicit on whether this is only the taxable portion.

A podcast that I recorded with Kingsley Williams will be released in the next few days. We covered a variety of concepts linked to diversification. In the meantime, you can enjoy this article by Kingsley to whet your appetite.It was first published here.

Over the last few weeks, I’ve been approached by various people seeking my perspective on the recent market turmoil, particularly in the US, where that market was down almost 6% since the end of 2024[1], and down 10% since its peak almost a month ago[2]. Investors seeing their portfolios decline in value may be questioning whether their current strategy is still right, or if a change is needed.

I always begin by asking what the investor is aiming for and how long they have to reach that goal. While other factors matter, this is the key determinant of whether their strategy is still appropriate.

At Satrix, we don’t predict short-term market movements. Markets can be highly unpredictable in the short term, and equities tend to have more volatility.

What we do know is that, over longer periods, markets behave more predictably. However, any prediction still carries a high degree of uncertainty due to unpredictable shifts in the investment, regulatory, inflation, and geopolitical landscapes. So, what can investors do to better reach their goals?

Match your investment term with the right mix of asset classes

Diversify your strategy – it’s one of the only free lunches in investing

Manage your costs

The principle is simple: riskier asset classes should be held for longer periods to pay off. In the short term, they are more volatile, but over time, their value should align more with fundamentals. Higher returns for taking on more risk make sense in the long run.

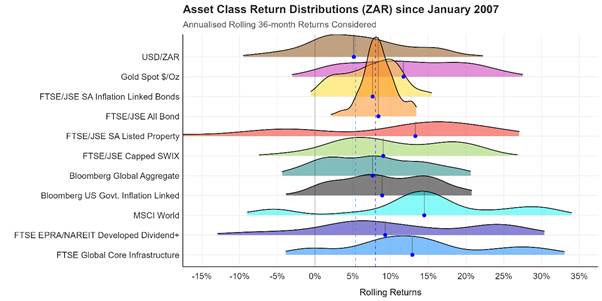

Charts comparing asset classes since January 2007 show that some, like local inflation-linked bonds (yellow) or nominal bonds (orange), have a narrower range of returns over all three-year periods, offering more certainty. In contrast, other asset classes show a much wider range of outcomes, providing less certainty over the same period.

Figure 1: Asset Class Return Distributions (ZAR), annualised rolling three-year periods. Source: Satrix, as at 28 February 2025.

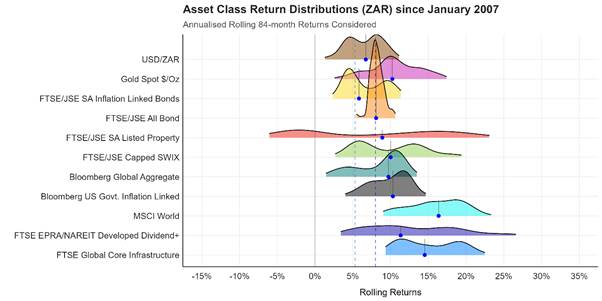

As the holding period is expanded to seven years, the return distributions of all asset classes narrow, although some narrow a lot more than others. All asset classes, except for local listed property (red), have delivered a positive return over all seven-year periods. Nominal bonds (orange) have never delivered a return below inflation. Local equities (FTSE/JSE Capped SWIX), in light green, have delivered a median CPI+5% outcome, albeit with a high degree of variability around this. What is also noticeable is how much higher the median return for developed market equities (MSCI World) has been as it has benefitted from a weakening rand and the strength of the US equity market after the global financial crisis.

Figure 2: Asset Class Return Distributions (ZAR), annualised rolling seven-year periods. Source: Satrix, as at 28 February 2025.

The purpose of showing these charts is not to provide an expectation of the return for each asset class – past performance is no guarantee of future results – but to show why more time is necessary when investing in riskier asset classes. It also shows that in most cases, but not always, more risk is generally compensated with higher returns.

Diversify Your Investment Strategy

Both within each asset class, and across asset classes, diversification allows you to reduce idiosyncratic risk to a minimum, so you’re only left with systemic risk. As one of my colleagues likes to say, “Volatility (or systemic risk), is a feature of investing, not a bug!” The only way to really manage this risk is to ensure you invest for a suitably sufficient time frame, which gives your investment time to reward you for your patience and for taking the risk.

An example of diversifying your risk would be not to hold only US equity exposure, but include broader developed market exposure in your portfolio, such as tracking the MSCI World Index. While this index is still heavily dominated by the US, it also includes exposure to Europe, Asia and Australasia. You could also consider investing beyond developed equity markets, by, for example tracking emerging market equities, which, over the same year-to-date period, are up over 3%[3]. Some of the performance delivered by indices outside of the US equity market year-to-date, over the relatively short period, show how differently markets can behave, and why you don’t want all your eggs in one basket[4]:

MSCI China: 16.7%

MSCI Europe: 12.2%

FTSE Global Core Infrastructure: 2.4%

Bloomberg Global Aggregate: 2.4%

Bloomberg US Government Inflation-Linked Bond: 2.9%

Another factor to carefully consider is currency exposure. The above global indices are all denominated in US dollars. When converted to rand, which has strengthened relative to the US dollar, these US dollar-denominated returns have faced headwinds, while our local equity market is up 3.6% in rands[5], or 5.3% in US dollars.

It is tempting to believe that what has worked for the last 10 years will continue to work for the next ten. However, markets do eventually respond to longer-term fundamentals, meaning expensive markets and asset classes are more likely to underperform their undervalued counterparts. We accounted for this when reviewing the Strategic Asset Allocation for our range of multi-asset funds. Our analysis indicated US equity markets were expensive, so instead of allocating more capital to the expensive US equity market, we increased our allocation to emerging markets during our September 2024 rebalance.

So far, this overweight tilt in favour of emerging markets relative to the MSCI All Country World Index (ACWI) – which includes exposure to both developed and emerging markets – has paid off well. As has our exposure to global listed infrastructure, which acts as a more defensive equity play. The global listed infrastructure index that we track selects companies that operate infrastructure assets, whose revenue is often directly linked to inflation, providing a highly predictable long-term revenue stream, regardless of market or economic conditions.

Similarly, our recently launched Satrix Global Balanced FoF ETF (ticker: STXGLB) – the first of its kind on the Johannesburg Stock Exchange – has overweight exposure to emerging markets and a material allocation (10%) to global listed infrastructure, which has helped soften the impact to the US sell-off.

Manage Your Costs

I think about investment costs in relation to the expected real return. A low-risk investment, like a money market fund, may outperform inflation slightly over one-three years. However, when investing for growth above inflation, costs should be considered relative to that goal. For instance, a high-equity balanced fund might be expected to deliver a 5% real return above inflation (before costs), but if it costs 1.5%, plus 0.5% for platform access, the total cost is 2%. This means the cost is 40% of the expected return. It’s no wonder investors are left disappointed when they achieve only 3% real growth, having expected 5%. The impact of compounding, especially the negative effect of fees, is significant over the long term, so managing costs is crucial.

A similar balanced fund with a cost structure of 0.50% and accessed through the same platform, would now only cost 1% or 20% of your expected return, leaving you with 4% real growth.

When investing for the long term, market corrections and drawdowns are inevitable. Staying the course and resisting the urge to make drastic changes to a well-thought-out strategy is more likely to help you reach your investment goals on time, rather than constantly realigning your entire portfolio. Eventually, the market smooths out, allowing you to reach your destination as planned. As it turns out, the S&P 500 has recovered somewhat since 13 March 2025, and is now only down 1.7% as at 24 March 2025. Avoiding the urge to act, often at the most inopportune time, is a discipline that has shown to serve investors well.

Disclaimer

*Satrix is a division of Sanlam Investment Management

Satrix Managers (RF) (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). The information above does not constitute financial advice in terms of FAIS. Consult your financial adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs, the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document. A fund of funds portfolio is a portfolio that invests in portfolios of collective investment schemes that levy their own charges, which could result in a higher fee structure for the fund of funds. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information.

iOCO has been focusing on margins – and with great success (JSE: IOC)

Life-after-EOH is showing positive momentum

In case you’ve forgotten or haven’t really kept up with this story, iOCO is the renamed EOH. What is in a name, you ask? Well, in this case, quite a bit. Instead of focusing on legacy issues and getting tons of bad press, the company is working on getting its profits to head in the right direction.

This is working, despite a drop in revenue of 6.4% for the six months to January 2025. With gross margin up 300 basis points to 30%, gross profit increased by 2.8%. The real highlight is on the EBITDA level, which improved by a massive 159%. EBITDA margin increased from just 3.1% to 9.2%!

This is the joy of coming off a really low base for margins. Below the EBITDA line, there’s further room for improvement thanks to a reduction in net finance costs. These factors are why HEPS swung wildly from a loss of 11 cents to profit of 19 cents per share.

The share price is up 176% over 12 months, which is obviously immense. At the current share price of R3.16, simply annualising the interim result to get to earnings of 38 cents per share would imply a P/E of 8.3x. This isn’t exactly a demanding valuation, but isn’t a bargain either. To really push the share price beyond this level, they would ideally need to show the market that iOCO can become a revenue growth story, not just a margin story.

With plenty of narrative in the results around plans for revenue growth, they just might get it right!

A wobbly at Kore Potash (JSE: KP2)

There’s a delay to the Summit Consortium term sheet

Oh boy. So it begins. Despite the Summit Consortium having an incredibly long lead time to think about how to finance the Kola project that Kore Potash is putting together, the consortium has missed the communicated deadline to submit a non-binding financing term sheet.

Kore Potash expected to receive it by the end of March. With various excuses linked to religious holidays, the consortium has now asked for more time. They expected to deliver it before the end of April and “hopefully” by the middle of the month.

Hope isn’t what investors want to see here. They want to see a funding deal for the project. Although it’s entirely possible that everything is still on track, this is the kind of wobbly that gets people concerned.

Renergen’s quarterly update comes after a period of extreme price volatility (JSE: REN)

The share price is up 96% over one month and just 2% year-to-date

The latest Renergen quarterly update is certainly one of the more interesting ones. As usual, there’s good news and bad news.

An example of bad news is that Renergen still doesn’t know how to fill large iso-containers at the extremely cool temperatures needed. The good news is that they’ve figured out a plan B with smaller containers. They did at least fill a smaller container during this quarter, which is why the share price went nuts.

Quietly in the background, LNG production increased 22% quarter-on-quarter. That’s clearly good news. It just has little bearing on the long-term investment case.

Speaking of the investment case, we now get to the scary stuff. The dispute between Tetra4 (Renergen’s South African subsidiary) and Springbok Solar was heard in the High Court on 20 February. Judgment has been reserved, which means that the court is taking its time to deliver a ruling. In the meantime, Tetra4 has filed an appeal with the Department of Mineral Resources regarding the approval that the solar developer obtained. The fight continues, with potentially severe consequences if the court rules against Renergen.

Despite the uncertainty, the show must go on in terms of finding funding for the development of the helium asset. Renergen included some commentary in the announcement about working on a liquidity solution to enable the completion of Phase 1, with negotiations expected to be concluded in the coming weeks. That could mean anything, to be honest.

On the exploration side, there was no drilling during this period. Instead, the focus was on analysing previously obtained data.

Never a dull moment then, with all eyes on the court case.

Nibbles:

Director dealings:

The founders of Discovery (JSE: DSY) are fans of putting hedges in place over their shareholdings. This strategy seems to have rubbed off on the CEO of Discovery Bank, who has put a collar in place over R20 million worth of shares. The call strike price is R248.86 and the put strike price is R200.63. For reference, the current price is R205, so this collar is strongly focused on protecting against downside risk from this level. The expiration date is March 2027.

A non-executive director of Shaftesbury Capital (JSE: SHC) bought shares worth R450k.

An entity related to the chairman of Stor-Age (JSE: SSS) bought shares worth R434k.

In the recent Fortress Real Estate (JSE: FFB) dividend election, a number of directors of Fortress and/or NEPI Rockcastle (JSE: NRP) elected to receive shares in NEPI instead of a cash dividend. Remember, Fortress holds a substantial investment in NEPI and has been using that stake strategically for capital structure purposes. Receiving the NEPI shares was the popular choice, with holders of 90.57% of Fortress B shares making that election.

In one of the smallest director dealings I’m sure you’ll see for a while, a director of Cilo Cybin (JSE: CCC) bought shares worth just R2k.

Sibanye-Stillwater (JSE: SSW) hasn’t had much in the way of good news lately, although the share price is up a meaty 40% year-to-date based on a run in platinum prices. Although I don’t think the latest announcement is the kind of news that can move the share price, it’s still good news for renewable energy enthusiasts that the Castle wind farm has achieved commercial operation. This is the largest private offtake wind farm in the country, located near De Aar in the Northern Cape and providing power to Sibanye’s operations via a wheeling agreement with Eskom. This is a prime example of Eskom’s infrastructure being used for transmission rather than power generation. This project is expected to supply 5.5% of Sibanye’s energy needs in South Africa at a significant discount to what Eskom power would cost.

Shaftesbury Capital (JSE: SHC) didn’t waste any time in getting the deal to sell a 25% stake in Covent Garden across the line. It’s all done and dusted, which means that Norges Bank Investment Management is now the proud owner of a minority stake in this excellent London property.

In similar deal news, Mondi (JSE: MNP) has completed the acquisition of the Western Europe packaging assets of Schumacher Packaging. This adds to Mondi’s existing European network of corrugated solutions plants. Despite the name of the asset being acquired, this deal wasn’t that quick to get across the line, with the initial announcement having been made in October 2024.

Lighthouse Properties (JSE: LTE) has finalised the price for the scrip dividend. Those who elect to receive a scrip dividend (i.e. more shares in Lighthouse) in lieu of a cash dividend will receive shares based on a calculation that is takes into account a 2% discount to the Lighthouse price on the JSE on 31 March (adjusted for the amount of the cash dividend). In other words, there’s a minor discount.

The CFO of MAS (JSE: MSP), Nadine Bird, has resigned with effect from 30 June 2025, having been in the role since February 2023. After much was achieved around the debt management strategy, this was a successful, albeit short stint. A replacement has not been named as of yet.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")