This week, Sanlam disclosed in its annual financial statements that the group had agreed to subscribe for additional shares in Indian conglomerate Shriram’s wealth and stockbroking businesses increasing its effective economic shareholding from 26% to 50%. The group also subscribed for additional shares in Shriram’s listed asset management operations to increase its effective economic shareholding from 16.3% to 34.8%. The combined aggregate purchase price of R946 million is to be funded from discretionary capital.

Lighthouse Properties is to acquire the Alcalá Magna mall in the greater Madrid metropolitan area. The mall which serves as the commercial centre of Alcalá de Henares will be acquired for a total gross purchase consideration of €96,3 million from Trajano Iberia, a listed company of BME Growth, representing a gross asset yield of 7.6% (before transaction costs).

Healthcare REIT Assura plc has disposed of seven assets into its £250 million joint venture for a gross consideration of £64 million. Assura retains a 20% equity interest in the joint venture resulting in net proceeds of £51 million. The proceeds will be used to reduce acquisition debt used to finance the £500 million private hospital portfolio acquired in August 2024 at a 5.9% yield on cost.

AECI plans to implement a new broad-based ownership scheme which will see the AECI Foundation subscribe for a new class of ordinary shares in AECI Mining. The Foundation will hold an effective interest of 15.5% in AECI Mining which comprises the AECI Mining Explosives and AECI Mining Chemicals divisions. 73,59 million AECI Mining B shares will be issued, equivalent to a total transaction value of R522 million, equating to an issue price of R7.10 per B share. The Foundation will fund the consideration through a cash contribution from AECI Mining for 35% and notional vendor financing for the remaining 65%. The Foundation will receive trickle dividends equating to 20% of the distributions made related to its shareholding in the local operations of AECI Mining in the first 10 years, and 25% of the relevant cash distributions thereafter for the balance of the notional vendor financing period. The balance of the dividends attributable to the B shares will be applied towards servicing the notional vendor financing. The transaction is a category 2 deal with no shareholder approval required.

In a move to diversity and strengthen its portfolio, Labat Africa is to acquire a 51% stake in Ahnamu, an ICT importer and distributor of computer hardware solutions across the SADC region. The acquisition will complement recently acquired Classic International. Labat will pay R25 million for the stake to be settle by way of the issue of 200 million share at an issue price of R0.10 per share (a premium of 25%) and R5 million in cash.

The recently JSE-listed UK real estate investment trust Supermarket Income REIT plc has reached an agreement with Atrato Group to internalise its management function – subject to shareholder approval. The £19,7 million which it will pay Atrato, will be funded from the proceeds recently received from the sale of its large format omnichannel Tesco store in Newmarket.

Transcend Property Fund, a subsidiary of Emira Property Fund, has disposed of its interests in several residential properties to The Urban Impact Rental Trust for an aggregate consideration of R530 milllion. The target properties which are located in Pretoria and Johannesburg include Molware, Urban Ridge East, Urban Ridge West and Urban Ridge South.

MultiChoice and Groupe Canal+ have extended the Long Stop Date for the fulfilment of conditions for the implementation of the offer to MultiChoice minorities. The extended date is 8 October 2025.

UK investor in modern primary healthcare properties, Primary Health Properties plc has acquired state-of-the-art Health & Wellbeing Clinic which offers urgent care and diagnostic facilities in Cork, Ireland. The property, acquired for €22 million, at an accretive earnings yield of 7.1% is fully occupied and leased to Laya Healthcare, part of AXA.

Sable Exploration and Mining (SEAM) has entered into a Memorandum of Understanding with Boo Wa Ndo, for the acquisition of a 55% interest in the prospecting rights and mining permits over the properties Moskow and Zoetvelden farms in the Limpopo province. These properties contain Vanadium, Titanium and Magnetite resources. SEAM will issue 6 million shares at R1 per share for the stake. The transaction is a category 2 transaction and as such does not require shareholder approval.

MAS plc has entered into an agreement with Prime Kapital for PKM Development (the joint venture) to repurchase the 60% equity held by Prime Kapital which will give MAS control, terminating the joint venture 10 years earlier than the minimum contractual term. Because this is a related party transaction in terms of the JSE Listing Requirements, a circular will be sent to shareholders in due course. In addition, MAS has completed the disposal of its Strip Malls in Romania for a cash consideration €43,6 million.

Rex Trueform has acquired a further 5.72% stake in unlisted property fund Belper Investments for a cash consideration of R3,86 million, payable in monthly tranches from 3 March 2025 to 1 August 2025. The deal increases the company’s stake in Belper Investments to 84.74%.

Following the rezoning of vacant land known as Stellendale Gardens in Cape Town, Visual International has acquired the property for R28 million from related party RAL Trust. The development of Stellendale Gardens envisages a mixed-use development including retail, commercial, offices and residential accommodation. Visual is currently developing NSFAS approved Stellendale Junction apartments for students.

Unlisted Companies

UK-based RSK Group has acquired Pegasys, a strategy and management consulting group. Headquartered in Cape Town, Pegasys specialises in developmental impact in emerging economies with expertise in the development and management of climate change, cities, energy, resilience, transport, waste, and water sectors. The deal will accelerate Pegasys’ growth and broaden its global impact.

In August 2024 MC Mining secured potential investment of US$90 million to fund its Makado, Vele and the Greater Soutpansberg Projects. The investor, HKSE-listed Kinetic Development Group (KDG) agreed to invest via two tranches for a controlling 51% in the exploration, development and mining company. The initial tranche was for 13.04% (62,1 million shares) for an aggregate consideration of US$12,97 million. The second tranche which was conditional on the fulfilment of conditions precedent will now go ahead for an aggregate $77 million taking KDG’s interest in MC Mining up to 51%.

Lesaka Technologies has issued the first of two tranches of shares in the part settlement of its acquisition of Recharger announced in November 2024. 1,092,361 shares with a value of R98 million have been issued for the South African prepaid electricity submetering payment business with the second tranche (R75 million) due on 3 March 2026.

The change in names of Dipula Income Fund to Dipula Properties and of Transaction Capital to Nutun will become effective from 12 March and 18 March 2025 respectively.

Salungano whose listing is currently suspended on the JSE has advised that it intends to release the FY2024 financial results around 31 March 2025 and the FY2025 interim financial results shortly thereafter. Given this timeline, the company estimates that the suspension of its listing will be lifted around mid-April.

This week the following companies repurchased shares:

Over the period 28 January 2025 to 4 March 2025, Invicta repurchased 4,921,642 shares for an aggregate R156,48 million. The shares were repurchased in accordance with the general authority granted at the annual general meeting in September 2024, representing 5.08% of Invicta’s issued share capital. The buyback was funded from cash generated from operations.

Brikor has entered into an agreement with the Brikor Share Incentive Scheme to repurchased 15,900,000 shares at a purchase price of 14 cents per share for an aggregate R2,385,000. The repurchase is still to be approved by shareholders.

In its annual financial statements released in August 2024, South32 announced that it would increase its capital management programme by US$200 million, to be returned via an on-market share buy-back. This week 47,089 shares were repurchased at an aggregate cost of A$1,7 million.

On 19 February 2025, the Glencore plc announced the commencement of a new US$1 billion share buyback programme, with the intended completion by the time of the Group’s interim results announcement in August 2025. This week the company repurchased 15,000,000 shares at an average price per share of £3.19.

Schroder European Real Estate Trust plc acquired a further 113,100 shares this week at a price of 66 pence per share for an aggregate £74,533. The shares will be held in Treasury.

In October 2024, Anheuser-Busch InBev announced a US$2 billion share buy-back programme to be executed within the next 12 months which will result in the repurchase of c.31,7 million shares. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 24 – 28 February 2025, the group repurchased 540,000 shares for €29,78 million.

Hammerson plc continued with its programme to purchase its ordinary shares up to a maximum consideration of £140 million. The sole purpose of the buyback programme is to reduce the company’s share capital. This week the company repurchased 370,874 shares at an average price per share of 269 pence.

In line with its share buyback programme announced in March 2024, British American Tobacco plc this week repurchased a further 445,306 shares at an average price of £30.95 per share for an aggregate £13,78 million.

During the period February 24 – 28 2025, Prosus repurchased a further 6,538,359 Prosus shares for an aggregate €278,04 million and Naspers, a further 473,814 Naspers shares for a total consideration of R2,18 billion.

Four companies issued profit warnings this week: Merafe Resources, Thungela Resources, Mustek and SAB Zenzele Kabili.

During the week, five companies issued cautionary notices: MAS plc, TeleMasters, Labat Africa, Vukile Property Fund and Mustek.

Sahel Capital has announced a US$400,000 working capital loan to MM LEKKER through its Social Enterprise Fund for Agriculture in Africa. MM LEKKER, based in Benin, specialises in selling soybean, shea nuts and cashew nuts, catering to both local and international markets.

A Ventures has increased its investment in Egyptian waste management platform, Mrkoon. The bridge funding round will increase A Ventures’ equity interest to 28%. Mrkoon allows enterprises, especially in industry and manufacturing, to offload surpluses and scraps through a B2B platform. The company is preparing for regional expansion, with plans to enter the GCC, where the scrap and surplus materials market exceeds US$150 billion.

Houston-based Vaalco Energy has farmed into the CI-705 block in the Tano basin offshore Côte d’Ivoire. Vaalco will become the operator of the block with a 70% working interest and a 100% paying interest though a commercial carry arrangement and is partnering with Ivory Coast Exploration Oil & Gas SAS and PETROCI.

Nigeria’s Tantalizers Plc, which operates in the quick-service restaurant sector, has announced its expansion into Nigeria’s blue economy sector with the acquisition of 10 fully equipped modern trawlers and the signing of a landmark partnership agreement with a US-based marine Group and Consortium led by Mr. Charles Quinn, the Consortium Chairman. The MOU establishes a framework for technical collaboration, operational capacity building, and export market access, all of which will strengthen Tantalizers’ position in the evolving Nigerian Blue Economy space. The partnership will also involve technology transfer, compliance with global best practices in sustainable fishing, and adherence to international seafood processing standards, ensuring Nigerian seafood products meet global export requirements.

Having faced numerous challenges, including muted economic growth, geopolitical upheaval, high food prices, spiking interest rates and power supply interruptions, South Africa (SA) is fast improving its prospects for growth and becoming an attractive proposition for companies looking to raise equity capital. The formation of the Government of National Unity (GNU) has been positively received by the market and has lifted both international and domestic investor confidence.

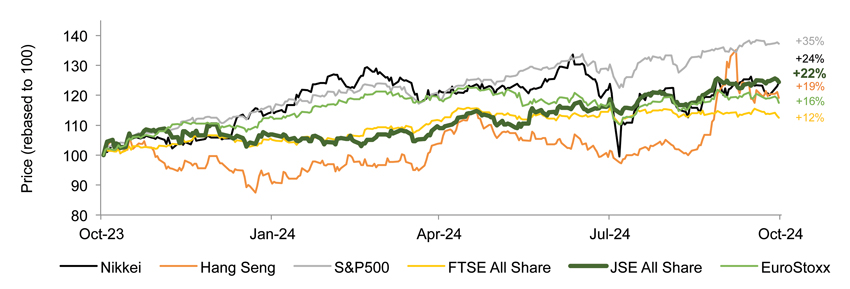

On the valuation front, SA trades at a price-to-earnings (PE) discount relative to both developed and emerging markets, presenting an opportunity for global investors to deploy capital into the South African listed environment. Currently, the JSE All Share trades at a forward PE multiple of 12.6x, which represents a 21.3% discount to the average forward PE multiple of 16.0x reported in developed markets. Relative to emerging markets with an average forward PE multiple of 14.5x, the JSE trades at a 13.5% discount. Over the past 12 months, the local bourse has outperformed its global counterparts, such as the FTSE All Share, EuroStoxx and Hang Seng, underperforming only the Nikkei and S&P 500, demonstrating higher market confidence in the South African equity environment, and an improved investor outlook.

Global equities performance (LTM) – Source: Bloomberg

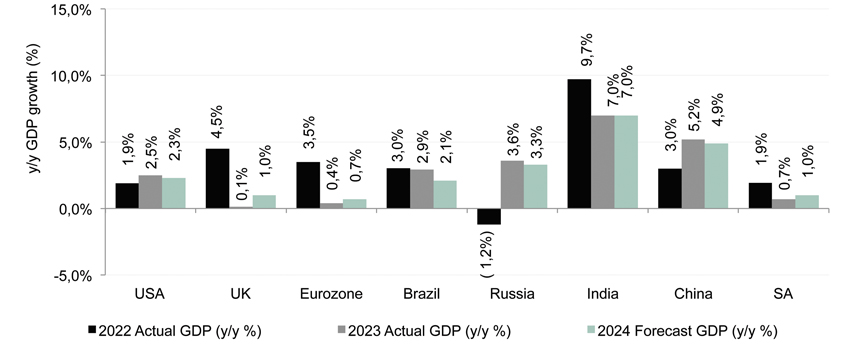

On the macroeconomic front, SA’s gross domestic product (GDP) is expected to climb moderately from the subdued 0.7% year-on-year growth in 2023 to 1% in 2024 and 1.7% in 2025. Relative to the United States and BRICS nations, forecasted SA output will remain subdued, albeit in line with the lacklustre GDP growth seen in the United Kingdom and eurozone. Rand strength, lower inflation and interest rate cuts will be key factors to propel equity capital market deal flow.

GDP performance (2022 – 2024) – Source: Bloomberg

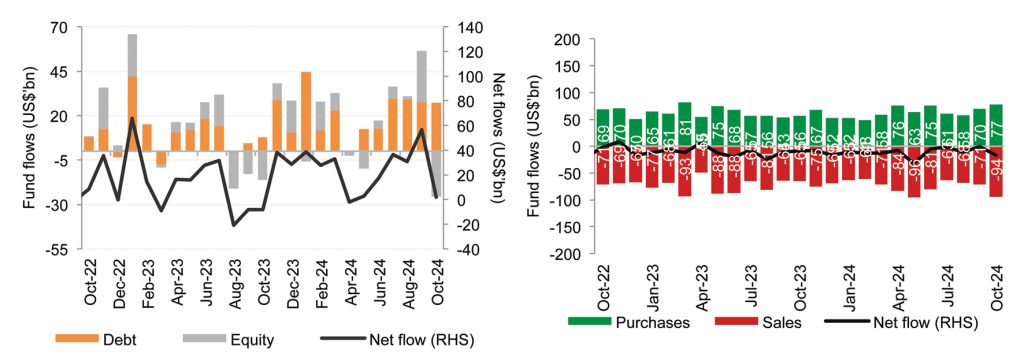

The recent amendment to Reg 28, increasing the institutional fund offshore investment weighting from 35% to 45% of portfolio allocations, has negatively impacted the South African equity market over the past two years, resulting in the net selling of South African counters as investors looked for investment in global equities instead of local stocks. However, with the JSE currently outperforming emerging markets, the capital outflow trend may be only short-term as local and global investors regain confidence in the local bourse. As institutions seek to meticulously allocate their capital to markets that will deliver higher equity returns, competitive dividend yields and attractive valuation metrics, emerging markets are expected to see an increased inflow of capital from local and foreign investors, with the JSE expected to benefit from this trend as investor sentiment and market conditions continue to improve.

Emerging markets and JSE capital flows – Source: Institute of International Finance (IIF), JSE

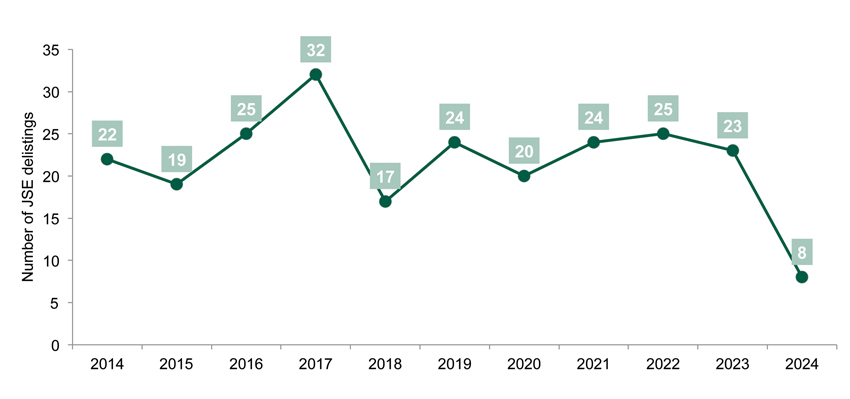

New primary markets issuance on the JSE is also showing signs of improvement. In the past 10 years, we have seen over 230 companies delist from the JSE due to various reasons, such as excessive listing costs, stringent regulatory requirements, lack of trading activity, management buyouts, and merger and acquisition opportunities that have enabled businesses to grow further after being acquired and taken private. Some notable delistings from the JSE over the past five years include Royal Bafokeng Platinum, Distell Group, Mediclinic International, and PSG Group. Notwithstanding this grim historical picture, the local bourse is now turning the tide from a wave of delistings as capital market activity increases and a significant pipeline of new initial public offerings (IPOs) has built. Recently, every company that has listed on the exchange did so due to unbundlings driven by debt-related pressures experienced by the holding company. Examples are Premier, WeBuyCars, Zeda and Boxer Superstores, which were unbundled from Brait, Transaction Capital, Barloworld and Pick n Pay respectively.

Delistings on the JSE (past 10 years) – Source: JSE

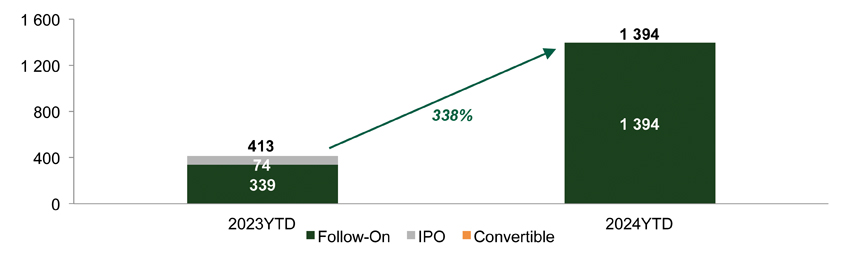

With a stabilising rate environment, easing inflation and higher growth outlook, South Africa is set for increased equity capital markets (ECM) deal flow across various equity offerings, including through IPOs, secondary inward listings, rights issues, accelerated bookbuilds and share buybacks. Notable ECM transactions concluded on the JSE in 2024 include the R8,5bn Boxer listing, R9,6bn Anglo American accelerated bookbuild, R4,0bn Pick n Pay rights offer and Pepkor R9,0bn accelerated bookbuild. The investment community is optimistic and anticipates more activity in the ECM environment, with over 10 deals already concluded in 2024 YTD. The pipeline of IPOs in SA includes African Bank, Fidelity, Coca-Cola, and other companies that envisioned coming to market in the pre-COVID-19 era.

SA ECM volumes (US$m) – Source: Dealogic

We have witnessed the JSE make efforts to simplify regulatory requirements to encourage more listings and equity issuances. Recently, we have seen secondary listings on the JSE become thematic. UK-listed companies such as Assura plc and Supermarket Income REIT have identified the opportunity to broaden their access to capital and diversify their shareholder base by pursuing listings on the JSE. As the global macro environment improves – inflation remains controlled, interest rates are cut further and the rand holds its ground – SA will see a significant increase in equity capital markets deal flow, which will further bolster local growth and attract investment.

Leago Papo is an Investment Banking Associate: Equity Capital Markets | Nedbank Corporate and Investment Banking.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Private equity (PE) investments are known for their significant potential for returns, but navigating the path to a successful exit can sometimes be challenging.

Historically, typical South African PE funds are structured as en commandite (limited liability) partnerships with a predetermined term, often 10 years (plus two one-year extensions). At the end of the term, the investments are usually realised, and the investors share the returns. Common ways of exiting private equity funds are either via sales to other companies or secondary buyouts to other PE firms.

However, fund managers may face the challenge of trying to exit at the end of the pre-agreed life of the fund when investments are performing well and an exit would diminish value, or when market conditions are not conducive to an immediate exit. A practical solution may be to set up a continuation fund.

Continuation funds A continuation fund is a vehicle used to extend the life of a PE fund beyond its original term. Existing investors have the option to roll over their interests into a new fund structure, allowing the fund manager to continue managing the portfolio beyond the initial investment.

However, navigating a continuation fund as a way to exit a PE fund requires careful consideration due to the tax implications.

Tax implications The en commandite partnership of a typical PE fund does not enjoy a separate legal or tax persona. In terms of common law, the property of a partnership is co-owned, in an abstract sense, by the partners themselves in undivided (but not necessarily equal) shares, proportionate to their interest in the partnership and on the terms and conditions laid out in the partnership agreement.

The dissolution of a partnership will attract capital gains tax (CGT) for the partners if the division of the assets constitutes a ‘disposal’ or is deemed a disposal for tax purposes.

Disposals A ‘disposal’ is defined in South Africa’s Income Tax Act, 1962 as including ‘any event, act, forbearance or operation of law which results in the creation, variation, transfer or extinction of an asset’. The definition provides particular inclusions with terms such as ‘conversion’, ‘sale’ and ‘exchange’.

When partners initially make their capital contributions to the private equity fund, each acquires an undivided share in the assets. In Chipkin (Natal) (Pty) Ltd v Commissioner for the South African Revenue Service (SARS) (the Chipkin Case), it was confirmed that the undivided share in the asset and its ‘partnership interest’ are mutually exclusive.

Following the Chipkin Case, the disposal of a partnership interest where ownership is transferred to a third party or an existing partner will result in the disposal of an ‘asset’ for CGT purposes.

The proceeds less the base cost of the asset will result in either a capital gain or a capital loss in the hands of the partner. If the partner is a South African company and there is a gain, it will be subject to CGT at an effective rate of 21.6%, while a capital loss may be capable of being off set against capital gains realised by the partner, provided none of the loss limitation rules apply.

Partners ‘re-investing’ in the continuation fund While the dissolution of a partnership would, at face value, constitute a ‘disposal’ for tax purposes, the principle underpinning a disposal is that a person must have disposed of an asset in the sense of having parted with the whole or a portion of it.

In terms of a typical private equity fund, partners’ rights and interests are established upfront by having regard to, inter alia, the profit-sharing waterfall that would be set out in the partnership agreement. Until the disposal of a partner’s interest in the underlying partnership asset, the value of each partner’s interest typically fluctuates. Particular to a general partner of a fund, the value fluctuates disproportionately to the general partner’s initial capital contribution. These changes arise as a result of the partnership interests established upfront.

Mechanically, the termination of a partnership will trigger a replacement of the abstract proportionate co-ownership of the underlying assets with actual ownership of the underlying assets. In this regard, the investor has not parted with anything, nor gained anything. The subsequent contribution of the assets to the continuation fund is then represented by a partnership interest in the new fund.

In the continuation fund, a partner’s interest may differ from that of the old fund, although we assume, for the purposes of this article, that the partner’s interest does not differ in value. For example, an exiting partner may have been a general partner in the old fund but a limited partner in the continuation fund. In respect of the asset itself and the partner’s co-ownership rights in the asset, provided the partner does not monetise the value, the partner will have parted with nothing.

A limited partner in the old fund that contributes its shares to the continuation fund as a general partner will not give up value on the date of admission to the new partnership because the value of the contribution equals the value of the shares distributed from the old fund. The profit-sharing waterfall in the continuation fund needs value accretion or depreciation from that point. Accordingly, a disposal for CGT purposes should not arise upon admission into the continuation fund. The application of this view is supported in SARS Binding Private Ruling 391 (2023 (BPR 391)).

Included within the ‘disposal’ rules is a deemed disposal referred to as a ‘value shifting arrangement’. The value-shifting provisions apply primarily to a movement in a partnership interest in respect of an existing partnership. Accordingly, these shifting provisions should not apply on the dissolution of a partnership as the said partnership is no longer in existence.

This view was also confirmed in BPR 391, where SARS held that the dissolution of a partnership did not result in any change in the rights held by the partner and, therefore, would not constitute a ‘value-shifting arrangement’.

Once the benefits of utilising a continuation fund to cater for specific commercial needs at the end of the term of a fund have been taken into account, one would also need to consider the rights/ entitlements of each specific partner in such fund to determine whether a tax disposal event arises. Unless a particular partner monetises its interest in the dissolved partnership, the contribution of the co-owned interest in the underlying assets to the continuation fund should ordinarily not result in a disposal for CGT purposes.

Jutami Augustyn is a Partner, Michael Rudnicki an Executive in Tax, Diwan Kamoetie an Associate, and Eamonn Naidoo a Candidate Legal Practitioner | Bowmans South Africa.

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

We are grateful to the South African team from Lumi Global, who look after the webinar technology for us, as well as EasyEquities who have partnered with us to take these insights to a wider base of shareholders.

In the 48th edition of Unlock the Stock, Afrimat returned to the platform to talk about the recent performance and strategic focus areas for the group. The Finance Ghost co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

The market response on Thursday morning should be interesting

Attacq released a trading statement and updated its market guidance on Wednesday. If you’re wondering why the share price barely moved, that’s because the announcement only came out after the close of trade. Look out for the market reaction on Thursday morning, which I’m quite sure will be strongly positive.

For the six months to December 2024, Attacq expects to see its distribution per share jump by 46.7% to 44 cents. This is thanks to a lovely jump in distributable income per share.

After such a great start to the year, they also have better expectations than before for full-year earnings. The updated guidance shows growth in full year distributable income per share of 24% to 27%.

Cashbuild’s gross margin is a disappointment (JSE: CSB)

This isn’t what I was hoping to see

Regular readers will know that I took advantage of a tactical entry point in Cashbuild late last year. Although it worked beautifully, I’m starting to wonder about my plans to keep it. The share price has been one-way traffic this year and not towards the top right of the page.

Some momentum in revenue has been the good news up until now. Alas, we’ve now seen the margins for the interim period and they aren’t strong. With gross profit margin down 40 basis points on revenue growth of just 5%, HEPS could only manage 1% growth thanks to inflationary pressure on costs. That’s better than it being down, but not by much.

At least working capital has become more efficient, with 88 days of stock instead of 90 days. This boosted cash and cash equivalents by 20%, showing you once again how small changes in retail can have a large impact.

Although revenue in the first 7 weeks of the year increased by 6%, I now have to wonder about the underlying margins being achieved in 2025. Revenue growth doesn’t mean much for investors if the dividend is flat.

The share price closed 3% lower on the news, taking the drop this year to 19.4%. The fact that I’m still way up in this position tells you how daft the market was last year when it created that surprising entry point in August.

Curro needs more kids, but earnings are up at least (JSE: COH)

How much more can be squeezed out of parents?

Curro has a pricing vs. volumes problem. It’s clear as can be. Weighted average learner numbers were up just 1% for 2024, yet tuition fee revenue was 7%. I don’t need to sit in one of the maths classes to know that the difference has to be fee increases.

Now, if the schools are sitting with extra capacity (and they certainly are), then why such high fee increases? Surely it’s better to have a few years of below-inflation increases to try and improve capacity utilisation?

In the absence of that strategy, I can only assume that many of the schools are in areas where there simply aren’t enough kids anyway. The birth rate is a known issue and so is emigration. If that’s the situation, then fee increases are unfortunately the only option available to Curro.

We will have to see how this plays out in years to come. For now, the group managed recurring HEPS growth of 13% for the year ended December 2024. They are still investing in new campuses, despite the difficulties in filling the ones they already have.

Schools built before 2009 are only running at 74.7% capacity. Acquired schools are running at an average of 72.7%. Although there are clearly regional nuances, is the reality that South Africa simply has too many private schools?

Emira’s subsidiary is selling a large residential portfolio (JSE: EMI)

The announcement is frustratingly missing one key metric

Right at the beginning of 2024, Emira Property Fund concluded the acquisition of Transcend Property Fund. The idea of buying the entire fund was to get the portfolio at a discount, with the ability to dispose of assets piecemeal to unlock value.

So, for Emira shareholders, it’s encouraging to see news of a substantial disposal by Transcend, which is a wholly-owned subsidiary of Emira after that deal. The total price is R530 million, so this is a substantial deal covering literally hundreds of sectional title residential units.

At this point, you must be itching to know how the price compares to the value on the Emira balance sheet. That makes two of us. Alas, Emira decided that this wasn’t worth including in the announcement. The only thing we know is that the price was “fair market value” – according to the directors of Emira, that is. Very helpful.

The net operating income for the six months to September 2024 was R25.3 million. If we annualise this, the yield is 9.6%. That does sound like a reasonable yield, so in reality they properly did get this disposal done at a premium to what they originally paid for the portfolio.

But why not explicitly say that?

Growthpoint’s earnings are inching higher (JSE: GRT)

At least the direction of travel is up, if not by much

Growthpoint released a trading update for the six months to December 2024. It’s a voluntary update, mainly because Growthpoint’s growth rate is in a different postal code to the level that would trigger a trading statement.

For the interim period, distributable income per share is expected to grow by between 3% and 4%. Talk about a game of inches! This is actually better than they expected, so full-year guidance has been increased to growth of between 1% and 3%. The market appreciated this news, sending the share price 3.5% higher.

Old Mutual’s operating profit seemed to disappoint the market (JSE: OMU)

At least returns on shareholder funds gave HEPS a boost

We’ve been seeing some pretty impressive numbers coming out of the insurance industry lately. The market didn’t appreciate what it saw at Old Mutual though, sending it more than 5% lower based on the release of a trading statement.

“Results from operations” is the primary measure of operating performance and unfortunately it wasn’t great, with a range of -6% to 14%. The mid-point of that range is in the low-to-mid-single digits. That’s not exciting.

The per share numbers are better thanks to share repurchases. Combined with the benefit of investment returns on shareholder funds, HEPS is up by between 13% and 33%. They also give a range of adjusted HEPS of 7% to 27%.

Returns on shareholder funds aren’t strong every year as they depend on the whims of the market. This is why investors tend to put more weight on the operating earnings.

The share price is now slightly down over 12 months, which is quite extraordinary when viewed in the context of Sanlam up 14%.

Double-digit growth in the Quilter dividend (JSE: QLT)

And the market celebrated

Quilter is a great example of the power of building distribution in financial services. Their efforts in the UK market have been excellent, with total assets under management and administration up 12% and boosted by core net inflows of 5% of the opening value. They also had great momentum in net inflows during the year, with the fourth quarter being the strongest.

So, for the year ended December 2024, they managed to grow revenue by 7% and keep operating expenses under control, with an increase of just 3%. This is why adjusted diluted earnings per share rose by 13%. On an unadjusted basis, HEPS actually swung sharply negative. Given the underlying growth here and the 13% increase in the dividend as well, I’m inclined to go with their adjusted view here.

Across both the Quilter and IFA channels, gross flows were strongly up on the prior year. Although there are obviously many nuances within the business, the direction of travel is clearly up.

Spur still gives you wings (JSE: SUR)

But be careful of the impact of Doppio Zero

If you have small children, you fully understand the importance of the Spur business model. For many parents, it’s a place of safety and sanctity while their offspring go and rip up the play area instead of the house. I’m convinced that the best restaurant model of all is the one that includes a play area. Customers are infinitely more forgiving of the food if there’s a safe place for the kids.

This is certainly reflected in Spur’s numbers for the six months to December, where franchised restaurant turnovers are up 10% and revenue increased 13.8%. Group HEPS increased by 11.8% and the interim dividend per share followed a similar path, up 11.6%.

It’s important to note that roughly 6% of restaurant sales came from Doppio Zero, which was acquired with an effective date of 1 December 2023. This means that it was hardly in the comparable period, so the double-digit group sales growth is largely thanks to acquired revenue. If you look at group revenue instead of restaurant turnovers, you’ll find growth of 7.6% excluding Doppio. Decent for sure, but not as exciting as the numbers would initially suggest.

The cash story is great, with cash generated from operations up by 79%. This gives the group plenty of firepower and of course it makes capital allocation discipline very important.

STADIO’s growth story continues (JSE: SDO)

Tertiary education is an exciting industry in South Africa

STADIO has a reputation for being one of the better growth companies on the JSE. The share price has been doing plenty of growing lately, up 47% over 12 months!

There’s a good reason for this, with HEPS up by between 23.3% and 33.1% for the year ended December 2024. If you prefer to use core HEPS, you’ll find an almost identical growth percentage.

When local investors love a company, it can easily trade at a P/E in the 20s. STADIO is in that club, with the midpoint of the latest earnings guidance suggesting a P/E of 22.6x. If growth remains strong, then local market trends suggest that the P/E can stay there. In a consistent multiple situation, shareholder returns will then be similar to underlying earnings growth. Of course, if the multiple unwinds in a case where growth is disappointing, those returns can wash away very quickly.

For now at least, STADIO is getting full marks from the market.

Trellidor’s earnings are so much better (JSE: TRL)

But there’s still no dividend

Trellidor’s recovery story is proving to be as challenging as trying to break through one of their famous products! If you backed them 12 months ago, you would certainly be smiling now with a 77% increase in the value of your investment. If you’ve been there for three years, you would still be down a third. This company has had quite an adventure.

Revenue for the six months to December 2024 was up just 4.1%, so the recovery isn’t being driven by top-line fireworks. HEPS was much stronger, up 38.3% to 26.6 cents. An improvement in operating profit margin from 12.3% to 14.7% did wonders here.

The group remains in a situation where its core Trellidor business is underperforming in South Africa and doing well in the UK. I think market saturation is the real issue here, along with the ongoing shift towards living in complexes. People are trading security bars and gates for guards in a complex. This is forcing Trellidor to become more efficient in the business, which perhaps isn’t the worst thing.

Cash generated from operations is important to keep an eye on. It was actually slightly down for the year, despite the improvement in profits and a useful decrease in finance costs as well. A quick look at the balance sheet reveals the culprit: a substantial jump in trade and other receivables.

Although they don’t say it, I suspect that working capital pressures were one of the reasons why there’s no interim dividend.

Woolworths continues to slide (JSE: WHL)

The fashion businesses really are a drag

Woolworths closed 6.3% lower after releasing interim results. This takes the year-to-date drop to nearly 14%. Ouch.

Let’s start with the highlight: Woolworths Food. Turnover was up 11.4% overall and 7.3% on a comparable store basis. The Absolute Pets acquisition is skewing this performance, with sales up 9% excluding that deal. Still, with that kind of revenue growth and an increase in gross margin of 30 basis points, South African shoppers still love getting their Woolies Food fix. Expenses jumped by 15.2% though, so Woolworths shareholders have only seen an increase of 7.8% in adjusted operating profit. One thing that they can’t afford right now is pressure on margins in the only part of the business that is really working.

This brings us to Fashion, Beauty and Home. It just wouldn’t be a Woolworths result without some kind of excuse about inventory availability, with new processes and systems at the distribution centre to blame this time. They also put the blame on late supplier deliveries. Considering the number of people I’ve seen online complaining about Woolworths clothing quality (along with my own experience of it), I suggest they use one of the many mirrors in the store and look at themselves for this performance instead of hunting around for others to blame. Turnover was up just 2.5%, gross profit fell by 170 basis points and adjusted operating profit declined 17.7%. Frankly, it’s time for proper accountability here.

Over at Country Road Group, the challenges of retail in Australia (and New Zealand) continue. Sales fell 6.2%, gross margins took a 320 basis points knock and adjusted operating profit tanked by 71.7%.

Clearly, everything other than Food (and pockets of good stuff elsewhere, like Beauty) sucks right now. The group result therefore makes for painful reading, with the interim dividend down 27.7%. I genuinely don’t understand how the narrative in the apparel business can still be so focused on blaming external factors, or why large shareholders are letting the group get away with that.

Director dealings:

Director dealings:

A director of NEPI Rockcastle (JSE: NRP) bought shares worth around R300k. In a completely unrelated situation, the company also realised that an associate of a different director opted to receive a scrip dividend instead of a cash dividend. This wasn’t known at the time.

Vukile (JSE: VKE) is still serious about the acquisition of Bonaire Shopping Centre in Spain. This is the property that was damaged by flooding in October 2024. The property has been repaired and has reopened, with trading having commenced in mid-February. Vukile’s subsidiary Castellana still has exclusivity over the property and the parties are busy negotiating. Hence, Vukile has renewed the cautionary announcement.

Invicta (JSE: IVT) has been busy with quite the repurchase programme in the past few months, buying 5.08% of its shares in issue in on-market trades. They still have a general authority in place for another 14.92%, although they don’t indicate in the announcement whether they will get there.

For those following Metrofile (JSE: MFL) in detail, or Sabvest (JSE: SBP) for that matter, you’ll be interested to know that Afropulse Group and Sabvest Investments extended the put-call period over the 21 million Metrofile shares by 12 months to November 2026. Afropulse holds the call option and Sabvest holds the put.

Those who were too stubborn to listen to actual experts when SAB Zenzele Kabili (JSE: SZK) listed are still licking their wounds. The share price is down at R36, at one point trading as high as R180 when it somehow became a local example of a meme stock. The AB InBev (JSE: ANH) share price hasn’t done well, hence the B-BBEE structure has reported a terrible drop in net asset value per share of between 55% and 59% for 2024. The expected FY24 range is R26.91 to R29.67, so it’s still trading at a premium!

Tariffs may have a diminished impact on China, as the country has strategically restructured its supply chains to lessen its reliance on the US, says Campbell Parry, global resources analyst at Investec Wealth and Investment International. Speaking on the latest episode of No Ordinary Wednesday, Parry discusses prospects for the Chinese economy and the country’s investment case.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

At Brimstone, intrinsic NAV is what counts (JSE: BRT)

And it hasn’t gone in the right direction

Brimstone Investment Corporation released results for the year ended December 2024. They start with a note that HEPS was up 51%. To be very clear, HEPS is the single most useless metric you can look at in an investment holding company. Ignore it.

If HEPS mattered here, then why is the dividend flat when HEPS is up 51%? Also, why has the intrinsic net asset value (INAV) per share – the metric that the market uses to assess the share price – decreased by 8.5%?

The problem is that HEPS is highly affected by the accounting policies applied to the underlying stakes. When the percentage held in investee companies ranges from portfolio investments (not even a significant minority stake) through to consolidated investments in which Brimstone has control, HEPS can bounce all over the place as the accounting treatments are so different.

In case you need final proof, the share price is flat over 1 year. That wouldn’t be the case if HEPS mattered.

It’s high time that Brimstone stopped focusing on HEPS and started putting INAV at the centre of its reporting.

Packaging remains the growth area at Caxton & CTP (JSE: CAT)

But not enough to offset the decline in publishing and printing revenue

Caxton & CTP released numbers for the six months to December 2024. Revenue fell by 1.6%, as the company faces the problem of having a legacy side of the business (publishing and printing) and a growth area (packaging). The latter isn’t growing quickly enough (+3.0%) to offset the pressure in the former (-8.1%).

Thankfully, profit is what really counts. With operating profit moving 14.7% higher and HEPS up by 12.3%, the pursuit of efficiencies paid off for them. It sounds like this has included a particular focus on staffing costs and restructures, with staff costs up just 1.4%.

Community newspapers are under the most pressure it seems, with local advertising revenues down 4%. I think that people are now getting their community news through WhatsApp groups and direct comms from local schools etc. I distinctly recall the weekly paper arriving at my house as a kid, which I then read through with my mom in the afternoon. I’m not sure that this happens in households anymore with either parent!

Even at The Citizen newspaper, growth in the legal advertisements was the major source of improvement. It’s extremely tough to convince advertisers that they can get decent return on investment in the newspaper space. It’s sad in some ways, but that’s how disruption works.

CA Sales Holdings flags strong growth in HEPS (JSE: CAA)

The strategy continues to deliver

CA Sales Holdings just seems to get it right time after time. For the year ended December 2024, they expect HEPS to jump by between 23% and 28%. That’s a very juicy increase, achieved through the combination of organic growth and bolt-on acquisitions that the company is so well known for.

The danger of using Earnings Per Share (EPS) instead of HEPS comes through clearly here, as the comparable period included a R123.6 million bargain purchase gain on the T&C Group acquisition in Namibia. EPS is therefore pretty flat for the year because of the large number in the base.

HEPS is the right number to use when assessing true financial performance. On that metric, the company is doing very well.

Exceptional results at Discovery (JSE: DSY)

They’ve earned those smoothies

Discovery had a really great time of things in the six months to December. No matter where you look, the metrics are great.

Normalised headline earnings increased 34% and the same is true for the dividend, so we can tick the box for the cash quality of earnings. Normalised return on equity increased from 12.6% to 15.0%, so that’s a win for capital allocation. The life insurance sector metric looks even better, with annualised return on embedded value up from 12.1% to 19.0%!

Basic embedded value per share is one of the methods used by the market in valuing the company. It increased by 16% to R179.47. With return on embedded value well above the cost of equity, it means that the market is happy to pay a juicy premium to embedded value per share. Discovery’s share price is at roughly R209 per share. The market is therefore pricing Discovery at an effective return on embedded value of 16.3% (19.0% * R179.47 = R34.0993 and then take this and divide it by the share price of R209).

Although things are obviously a lot more volatile when you dig into business unit performance, it’s worth noting that both the Discovery SA Composite and Vitality Composite grew normalised profit by operations by 27%. They are seeing good things happen across the group.

Another notable performance is Discovery Bank, where revenue increased 42% and they are now at monthly operational breakeven.

The share price is up 56% in the past year. The group has had a few exciting times that turned out to be disappointments in the past decade. Is it finally different this time?

A record interim dividend at Harmony (JSE: HAR)

And they still have their eyes on copper

Life is good in the gold industry. In fact, it’s fantastic. Harmony grew revenue in the six months to December by 19% and saw net profit jump by 33%. That also happens to be the growth in earnings, with HEPS up 33%. The dividend story is even better, up 54.4% to a record of 227 cents per share!

This all happened despite a 4% decrease in gold production, which the company says was planned. They certainly didn’t plan for the gold price to do quite as well as it did, so that part was pure luck.

Earnings were boosted by all-in sustaining cost (AISC) coming in below guidance, although it was 15% higher as the group faced cost pressures. Combined with the lower production, this shows how different things might have been if not for the average gold price received being 23% higher.

If you CTRL-F in their detailed earnings, you’ll find three references to the word “copper” – and I suspect that might be higher by the time we get to full-year numbers. They describe themselves as being “on the cusp of introducing near-term copper” – watch this space!

Solid growth at HomeChoice (JSE: HIL)

You can engage with management directly next week on Unlock the Stock

HomeChoice International has released a trading statement for the year ended December 2024. It looks very strong, with HEPS up by between 20% and 30%.

This puts the range of expected earnings at 371.2 cents to 402.1 cents. With the share price at R28, the mid-point of that range is a P/E of around 7.2x.

There aren’t many companies on the local market at single digit P/E multiples with that kind of growth rate. You have the perfect opportunity to learn more about the company on Unlock the Stock next week. Attendance is free for the management presentation and facilitated Q&A at 12pm on 13th March. You just need to

The long-stop date for the MultiChoice – Canal+ deal has been extended (JSE: MCG)

With MultiChoice under so much pressure, that’s not good news

Right now, there is one thing and one thing only that is propping up the MultiChoice share price: the offer by Canal+. Based on the underlying earnings at MultiChoice, I genuinely don’t know where the bottom would be for the share price in the absence of that offer.

Sadly, due to ongoing regulatory processes, the long stop date of 8 April 2025 for the deal isn’t going to work. Even worse, they aren’t expecting to miss this date by a small margin. With the extension of the long stop date all the way out to 8 October, they are sending a message to the market that things are going to take a long time at the regulators.

They describe this as “ample time” for the fulfilment of conditions. I should certainly hope so!

MultiChoice’s share price fell 4.5% in response to the news, as the market applied the time value of money to the expected proceeds.

Double-digit growth in HEPS is good going at Nedbank (JSE: NED)

A bank this size is beholden to the broader country’s trajectory

Nedbank has released results for the year ended December 2024. It was of course a very strange year, with the first half filled with load shedding and election jitters, while the second half was filled with promises. I’m not sure that South Africa saw much execution of the GNU hopes, especially if you read results from sectors like construction.

It wasn’t an easy year in which to run a bank, so I think that Nedbank’s growth in headline earnings of 8% was presentable. Due to share buybacks, HEPS was up 11% and the full-year dividend per share grew 10%. The other key metric for investors is return on equity, up from 15.1% to 15.8%.

In a country with low growth, the important thing for banks is to keep their costs under control. Nedbank has various initiatives underway to try and achieve this. Despite this, the cost-to-income ratio has crept higher from 53.9% to 55.9%. This is due to revenue increasing by just 4% vs. 8% growth in expenses.

So then how did earnings end up higher? The answer lies in the credit loss ratio, which improved significantly vs. the prior year. Naturally, investors would prefer to see strong growth in revenue, as a solid improvement in the credit loss ratio isn’t something that will be experienced every year.

The net asset value increased 4% to R240.39. The share price closed 2% higher at R291.

Nedbank values the Ghost Mail audience and has given more details on their financial performance in your favourite publication at this link.

Higher debt and far more shares in issue ate up Sea Harvest’s profits (JSE: SHG)

They are calling this their most challenging year since listing in 2017

Sea Harvest Group released results for the year ended December 2024. Although revenue increased by 16% and gross margin improved by around 200 basis points to 26%, that’s the beginning and end of the highlights reel.

Firstly, that revenue number isn’t nearly as exciting as it looks. The increase is thanks to the acquisition of Sea Harvest Pelagic and Aqunion. Adjusting for acquisitions, group revenue was flat. Volumes fell and price increases were enough to offset the impact.

Group operating expenses jumped 20%, with the acquisition and general inflation having an impact here. The improvement in gross profit margin means that gross profit was up 25%, so thankfully they still managed some operating margin expansion here. By the time you go through some fair value and other adjustments to reach EBIT, growth on that line is just 8% and margins went backwards.

Now we get to the bad news. Net finance costs increased by 24% thanks to higher levels of debt after the acquisition. This is obviously a much higher jump than the growth in EBIT, so headline earnings fell by 37%.

It gets worse I’m afraid. Due to the large number of additional shares in issue, HEPS tanked by 45%. If you adjust for a once-off gain on purchased loans is the prior year, the drop was 17%. The dividend has tracked HEPS lower, down 45%.

Here’s another metric that is well worth noting: South African catch rates are at historical lows and down a whopping 30% vs. 2020 levels in the second half of the year. Pricing increases helped, but couldn’t protect margins in that part of the business.

Is there a silver lining here? Cash from operations probably fits the bill, with a positive swing of note in working capital. Despite higher interest charges, cash from operating activities was much higher at R774 million vs. R450 million in the comparable period. With net debt up by R334 million, they could do with another period of strong cash generation.

The oceans are unpredictable things. This makes it difficult to provide an accurate outlook on the business. One thing is for sure: catch rates desperately need to move higher.

Shoprite keeps eating everyone’s lunch (JSE: SHP)

And don’t make the mistake of ignoring their up-and-coming banners

At this stage, it doesn’t surprise the market when Shoprite releases incredible figures. It’s practically the expectation, which is a dangerous recipe for a share price. After all, investors make the most money from a positive surprise in the market. When something is priced for perfection, the risk is that there’s a disappointment.

Much like the broader retail sector on the JSE, the Shoprite share price is taking a breather right now. Down 9.3% year-to-date, the return over 12 months is just 3%. This is despite a set of numbers that just saw group revenue up 9.4% for the 26 weeks to 29 December 2024 and diluted HEPS up 9.9%. The interim dividend increased 6.7%.

For Shoprite to keep growing off this base is not straightforward, which is why investors are now experiencing single-digit returns. Although the grocery business at Shoprite clearly has room to keep winning market share from its competitors, Shoprite isn’t sitting back and hoping that this will be enough to keep driving growth. They have worked hard on introducing new store formats, like Petshop Science which has grown from nothing to 129 stores. Sales for the interim period were up 56.9% in that business. This strategy is in contrast to the approach taken by the likes of Woolworths, where they went the route of acquiring Absolute Pets instead.

If we dig a bit deeper, we find Supermarkets RSA with growth of 10.4%. Like-for-like sales increased 6.1% and customer visits increased by 4.1%. Some of Shoprite’s competitors can only dream of growth in volumes like this.

In the higher margin side of the business, Checkers and Checkers Hyper grew sales 13.6% and those famous Sixty60 scooters saw sales growth of 47.1%. Petshop Science, Uniq and obviously Checkers Outdoor are reported as part of these numbers. The group is building an incredible dataset of its customers thanks to the Xtra Savings card. As they add more specialist stores, the data will keep getting better.

Shoprite and Usave increased sales by 7.1%, so there’s a considerable gap between this business and the premium offering. The positioning of Checkers has proven to be a masterstroke.

Supermarkets non-RSA was a drag on growth, up 4.1% in rand terms and contributing 8.6% to group sales. Other operating segments also didn’t grow as quickly as the supermarkets business, up 6.2% and featuring a notable performance by OK Franchise of 8.8%.

In terms of trading margin, a 20 basis points increase in Supermarkets RSA was enough to offset the pressure in Supermarkets non-RSA, so group trading margin increased by 20 basis points to 5.7%. The daft approach in modern accounting rules is for lease costs to be excluded from trading profit, as the charges on leases are instead found in finance charges. This is why finance costs were up 28.3%, with the cost of the group’s expansion coming through on that line.

I have yet to meet a single person who likes the way leases are now treated for accounting purposes. Not one.

The second half has a tough base to grow against. The comparable period saw 10.1% growth in H2 and although sales in the first few weeks are ahead of last year, I doubt they will manage much more than mid-single digit growth vs. that base. Then again, Shoprite certainly keeps delivering!

WBHO shows that construction can make money (JSE: WBO)

How does a 30% increase in the interim dividend sound?

The construction industry has claimed many investor scalps. It’s not uncommon to see a complete collapse, often due to one or two really bad contracts. Thankfully, WBHO looks like the class captain in the sector, with all the important metrics heading in the right direction.

Revenue for the six months to December 2024 was up 10% and operating profit from continuing operations was good for 15%. HEPS from total operations jumped by 19.5% and the dividend was the best news of all, up 30% to 300 cents per share!

Future earnings are of course driven by the order book. This increased 7% in the period, which does look a bit light relative to earnings growth.

Here’s a fun fact for you: in Gauteng, data centre projects contributed 21% of revenue, commercial offices were 52% and residential work was 16%. Sadly, Gauteng as a whole suffered a contraction of 11% in building revenue, while coastal regions were up 19%. It says something about the trend of where people are living and working that office and mixed-use developments contributed 42% of revenue derived from the Western Cape. In the Eastern Cape, the only activity seen by WBHO has been industrial and warehouse developments.

On the roads and earthworks side, revenue in South Africa was up by 25%. Mining and energy sector projects contributed 43% of local revenue, while road projects were 41%. Water infrastructure was just 6%, which is a larger worry in our country!

In case you’re wondering whether public sector problems are unique to South Africa, hopes of an upswing in public spending by the new Labour Government in the UK have not materialised and WBHO’s UK business has been negatively affected. In practically every country, politicians are heavy on promises and light on delivery.

Overall, a solid set of numbers that support the 42% increase in the share price over the past 12 months.

Nibbles:

Director dealings:

The executive of the main subsidiary at Lewis (JSE: LEW) who has been selling shares recently is at it again. The latest disposal is of shares to the value of R2.45 million.

Mustaq Brey, non-executive director of Oceana Group (JSE: OCE) and of course the driving force behind Brimstone (JSE: BRT), bought shares in Oceana worth R1.2 million.

A couple of Kumba Iron Ore (JSE: KIO) directors and the company secretary sold shares worth around R16 million. Although they relate to old share awards, the announcement isn’t explicit on whether this is only the taxable portion.

One of the executives of Vodacom’s (JSE: VOD) South African subsidiary sold shares worth R1.3k.

Acting through Titan Fincap Solutions, Christo Wiese bought R12.2k worth of Brait Exchangeable Bonds (JSE: BIHLEB). This is pocket change on that side of the fence – literally. To give you an idea of how much ammo is flying around in the Titan stable, Wiese also restructured his stake in Collins Property Group (JSE: CPP). The ultimate beneficial ownership hasn’t changed, but we are talking about a shuffling of chairs to the tune of R864 million!

Labat Africa’s (JSE: LAB) new IT-focused strategy has been given a boost by the acquisition of a 51% stake in Ahnamu for R25 million, payable mostly (R20 million) through the issue of Labat shares at 10 cents a share. That’s a premium to the current prevailing share price. R5 million is payable in cash. This is a hardware distribution group, so that’s a pretty tough way to make money with paper thin margins. I have to believe that there’s a typo in the announcement, with profit after tax for the acquired business meant to be R7.8 million rather than R78.8 million. The net asset value is R64 million. If it is indeed R78.8 million, then Labat did the deal of a lifetime.

Supermarket Income REIT (JSE: SRI) has achieved very little liquidity on the local market. They also have an old-school management structure in the form of an external management company that is now being “internalised” at great quote. This used to be an issue on the JSE, with property executives enriching themselves in the process. At this UK-based REIT, the management company will be paid out £19.7 million, funded by proceeds from the recent sale of a Tesco store. With cost savings of £4 million, they are effectively achieving a yield of 19%, which is better than any of the other capital allocation opportunities they have available. Still, such structures should never have been allowed to exist.

Telemasters (JSE: TLM) is back under cautionary, with the two largest shareholders having received an expression of interest from a B-BBEE company to acquire their shares. There are a bunch of conditions attached, including the raising of funding it seems, so this is by no means a done deal. The proposal is for due diligence and negotiation of documents to be concluded by the end of March. That sounds extremely ambitious. The relevance to other shareholders is that if a deal does get done here, it would trigger a mandatory offer to all shareholders at the same price.

It’s the end of an era (or is that an error?) at Transaction Capital (JSE: TCP), with the name set to change to Nutun Limited (JSE: NTU) from 26 March.

There’s another name change on the local market – a subtle one, but perhaps therein lies a clue. Dipula Income Fund (JSE: DIB) is changing its name to Dipula Properties Limited with effect from 17 March.

The operating environment in 2024 remained challenging, with economic activity relatively weak as evident in SA GDP growth expectations of only 0,5% for the year when compared with 0,7% in 2023. The first 6 months were particularly difficult given geopolitical uncertainty, high interest rates and general uncertainty ahead of SA’s national election. A peaceful and fair election outcome and the swift formation of a government of national unity brought cautious optimism in financial markets resulting in lower bond yields, stronger equity markets and a stronger rand, while credit default swap spreads also improved. As the environment improved gradually into the fourth quarter of the year, inflation declined further towards the low end of the SARB target range (its lowest level since the Covid-19 pandemic), the MPC cut interest rates by a cumulative 50 bps and business confidence improved. Household credit growth, however, continued to slow to 3,0% by the end of the year, and corporate credit growth increased by 5,4%, remaining relatively volatile and not yet reflective of a material improvement in fixed-investment activity.

Performance:

In this context, Nedbank Group delivered an improved financial performance as headline earnings increased by 8% to R16,9bn and the group’s ROE strengthened to 15,8%, from 15,1% in the prior period, reflecting steady progress towards our ROE targets. HE growth was underpinned by good NIR growth, a lower impairment charge and targeted expense management, offsetting muted NII growth given slower loan growth and margin pressure. DHEPS increased by 11%, benefiting from the share buy-back we executed in 2023. Balance sheet metrics all remained very strong, enabling the declaration of a final dividend of 1 104 cents per share, up by 8% at a payout ratio of 57%.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")