In this edition of Ghost Bites:

- Collins Property Group just banked 17% growth in the distribution per share

- The market paid Pick n Pay a premium to VWAP for Boxer, but a discount to spot

- Spear REIT is in talks to acquire a property – in the Western Cape, of course

- Here’s a first for South African property funds: Vukile Property Fund is going to invest in Italy

Collins Property Group just banked 17% growth in the distribution per share (JSE: CPP)

But they need to get that debt balance down

One thing I’m confident about is that the Collins Property Group earnings announcement hasn’t been written by AI. The introduction is so “human” in its approach, with management lamenting the significantly diminished likelihood of interest rate cuts this year.

I’m all for formal writing in company announcements, but there’s also something to be said for a fireside style – especially when thinking out loud about how the macroeconomic environment has turned against you!

The theme of inflation and interest rate risk is going to come through strongly in many company announcements over the next few months. Brace yourself for outlook statements that include cautious commentary.

Collins will need to be particularly careful, as they run a loan-to-value ratio of 49% (slightly down from 50% as at February 2025). This is well above the levels we see in most REITs.

Management believes that conservative property valuations are a factor here. I think the market would prefer to see valuations done in a way that reflects the actual value, not a conservative view. There’s no point in being conservative if you are spooking the market with a frightening ratio (especially one that kicks you out of most stock screeners that investors would use).

The good news is that distributable income per share was up by 12.8% in the year ended February 2026. They ramped up the payout ratio and delivered 17% growth in the distribution per share. It’s also worth highlighting the impressive 10% growth in net asset value (NAV) per share.

Unlike some of the other names in the sector that are focused on bringing capital home, Collins is busy shifting capital to Europe. I don’t mind a strategy of selling assets in Mozambique and buying in the Netherlands. Mozambique is for beaches and red drinks that give you earth-shattering headaches. It’s not a place I would want to take my money to.

Collins isn’t shying away from local opportunities, though. They are busy with developments in Paarl and Somerset West. They have also completed a development in Namibia, which is definitely a better choice than Mozambique.

The company has already reduced debt by R106 million in March and April. This isn’t much of a dent in the R6.2 billion debt balance as at February, but it’s a start. Given the outlook on interest rates, they need to do a lot more.

Ghost Bite: With pressure on consumers from the oil price and now the impact of inflation on interest rates, 2026 is deteriorating rapidly in terms of the outlook for the property sector. I expect to see more capital raises in the sector over the next few months. Funds will probably look to raise at what might be a near-term peak in the cycle.

The market paid Pick n Pay a premium to VWAP for Boxer, but a discount to spot (JSE: PIK | JSE: BOX)

It looks like Pick n Pay was expecting more

As I discussed with Stephen Grootes on CapeTalk / 702 last night (listen to it here), a good way to understand Pick n Pay is to imagine yourself in a situation where you can’t make ends meet and you’re forced to dig around in grandma’s jewellery to see what you can sell.

The risk is that you’ll run out of nice things to sell before fixing the core problem around your income vs. expenses!

Pick n Pay told us on Monday that they would be selling approximately an 11.5% stake in Boxer. In the end, they offloaded a 12.5% stake. This leaves them with a shareholding of 53.1% in Boxer.

They were targeting proceeds of R4.7 billion and they were successful in reaching this number. But they had to sell more shares than planned to do it, which tells us that they didn’t get the price they expected.

The market paid R82 per share, which is a 3.2% premium to the 30-day VWAP. But Boxer was trading above R88 per share before the accelerated bookbuild was announced, so the shares were placed at a discount of around 7.5% to the previous day’s closing price.

Although a premium to the 30-day VWAP is still a decent outcome, this shows us that institutional investors are wise to (1) the stretched valuation of Boxer, and (2) the likelihood of further sales of Boxer shares.

Pick n Pay’s share price closed 3% lower on the day. Boxer closed 7.5% lower at R82, a rare example of the share price settling at precisely the bookbuild price!

Ghost Bite: Pick n Pay is committed to two things: keeping a controlling stake in Boxer, and taking the core Pick n Pay Stores segment back to cashflow break-even. I remain unconvinced that either of those scenarios will be achieved in the medium-term. If this latest capital raise doesn’t achieve that outcome, then I think you’ll struggle to find many people who will be bullish on a Pick n Pay turnaround. But what do you think?

Spear REIT is in talks to acquire a property – in the Western Cape, of course (JSE: SEA)

They made it clear in the latest results that they are looking at deals

Spear REIT certainly isn’t wasting any time in growing its portfolio after the release of recent results.

Having indicated an expectation to do deals worth between R500 million and R1.5 billion in FY27, they’ve now released a cautionary announcement regarding negotiations for the potential acquisition of a Western Cape property.

The only other information we have right now is that this would be a Category 2 transaction. That’s not really a surprise in the context of a market cap of R6.6 billion. They would have to announce a monster of a transaction to fall into the Category 1 bucket!

Ghost Bite: To their absolute credit, Spear REIT remains one of the only geographically focused REITs on the JSE. Investors appreciate it when management teams stay in their lane and focus on what they are good it. In Spear’s case, they are very good at Western Cape property!

Here’s a first for South African property funds: Vukile is going to invest in Italy (JSE: VKE)

I suspect that fund managers are volunteering for site visits as we speak

Over the years, we’ve seen local property funds execute a number of offshore deals. Many went to Eastern Europe, particularly countries like Poland. Vukile Property Fund was an early adopter of the opportunities in Spain and Portugal, with other funds having followed suit. Now Vukile is once again leading the sector into a new market: Italy.

That may be amore, but it also requires more capital.

The company has announced an accelerated bookbuild of R2.8 billion. Part of the proceeds will fund the acquisition of three shopping centres in Italy (with a gross value of €115 million and an expected yield of 10%). The rest will fall into that bucket the REITs love so much: optionality and financial flexibility.

In other words: pay us now, and we will tell you later what we did with the money.

Given Vukile’s track record, I have no doubt whatsoever that institutions will throw money at this. As always, retail investors will be diluted here, and probably at a small discount. Such is life when we are in a capital raising cycle in REIT land.

To make sure that institutions are ready to dig into their pockets, Vukile also released an update confirming the guidance for FY26 of 9.3% growth in the dividend per share. Looking ahead to FY27, they expect to achieve growth in Funds From Operations (FFO) per share of between 8% and 10% for the year ending March 2027. That’s solid.

Just to further sweeten the deal, Vukile plans to increase the payout ratio from 83% to 85%. This is expected to take dividend per share growth to between 10% and 12% in FY27.

Notably, the guidance for FY27 has taken into account the planned transaction in Italy.

The announcement also confirms that the proceeds from the October 2025 capital raise of R2.65 billion, as well as the proceeds of Castellana’s retail park portfolio of €280 million, have been deployed. In South Africa, the acquisition of Botshabelo Mall for R432.5 million is expected to be approved by the Competition Commission in July.

It’s not all good news, though. Spanish subsidiary Castellana is fighting with the Spanish Tax Authority. Yes, the same tax authority who just got moered in the Spanish tax courts by none other than Shakira!

Her hips don’t lie and we can only hope that Castellana isn’t lying either, as management believes that the Spanish tax assessment (a cool €8 million) has a “remote” likelihood of being successful. More disclosure on this issue will be made when the financials are released in June.

Ghost Bite: I’m sure that many professionals in Claremont are busy justifying trips to Italy to go see this opportunity for themselves. Perhaps they can throw in a trip to Spain to speak to a tax lawyer.

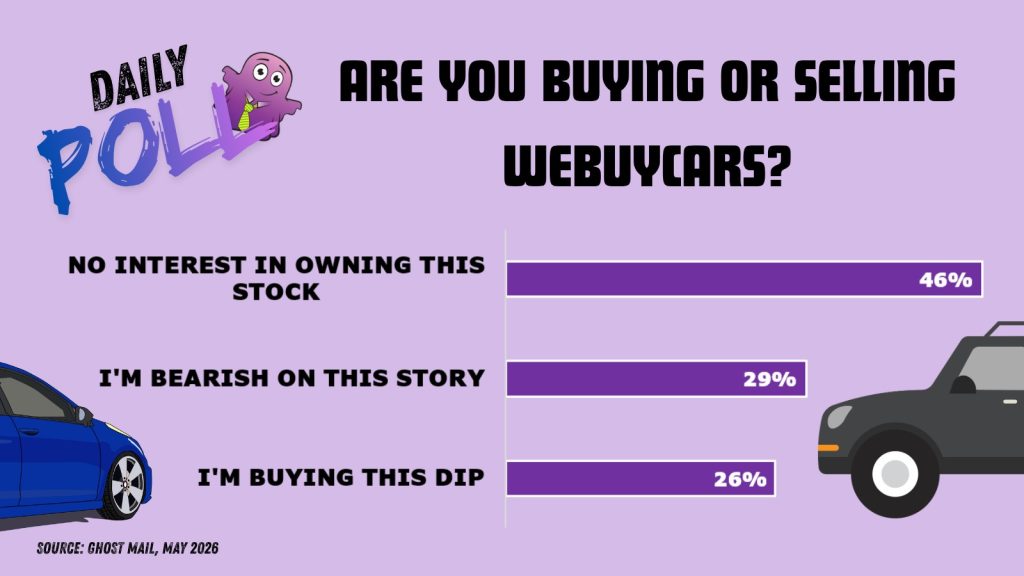

Results of previous poll:

Nibbles:

- Director dealings:

- For once, there’s nothing relevant to report here!

- Netcare (JSE: NTC) has announced that Melanie Da Costa, currently the group’s executive director in charge of strategy and health policy, will be taking over from Dr Richard Friedland as CEO. Friedland will formally retire on 31 December 2026 after co-founding Netcare and being there for around thirty years! Da Costa will get the top job from 1 January 2027. As is common in the market, the outgoing CEO will be available on a consultancy basis for a period of six months. I’m quite excited to see that Da Costa is a CFA, so we will see some proper capital allocation skills at the head of this company!

- Orion Minerals (JSE: ORN) is expecting to release a material announcement related to a planned capital raise. The mismatch between listing rules on the JSE and the ASX in Australia has been highlighted once more. Pending the announcement, there’s a trading halt on Orion shares on the ASX but not on the JSE. Orion’s share price fell 9.4% on this news.

- Novus (JSE: NVS) is in the process of disposing of the print letting enterprise. They previously agreed to extend the date for fulfilment of conditions precedent. They’ve now had to enter into revised agreements, with the good news being that the commercial terms are unchanged and the conditions are being treated as fulfilled.

- RMB Holdings (JSE: RMH) has received the compliance certificate from the TRP for the offer by AttBid. As approval was previously received from the Competition Commission as well, this now makes the offer unconditional. The offer remains open for acceptance until 29 May. Those who accepted by 15 May will already be paid on 22 May.

- Greencoat Renewables (JSE: GCT) is transferring its listing from the AltX to the Main Board of the JSE. This is a promising step. The challenge is that I keep hearing about investor frustrations related to the withholding tax process on dividends. They really need to find a solution there to address investor concerns.

- Zeder (JSE: ZED) announced a special dividend approximately a month ago. They still haven’t received approval from the SARB to pay the dividend, so the timeline is being revised. It’s truly beyond me how a regulator can make it this hard for a company to pay a special dividend.

- Lesaka Technologies (JSE: LSK) announced that Executive Chairman Ali Mazanderani’s contract has been extended. The expiration date has moved out from 31 January 2028 to 30 June 2029. Interestingly, he isn’t eligible for cash incentives beyond his salary and travel costs being covered. But he does have the option to buy 1,000,000 shares at $5 per share. That’s roughly in line with the current spot price, so the incentive is to grow the share price significantly over the next few years.