Coronation’s AUM has dipped in the past three months (JSE: CML)

The general risk-off vibes in the market wouldn’t have helped here

Coronation announced its assets under management (AUM) as at March 2026. As always, they don’t include any comparatives whatsoever, so readers are forced to go digging. I’ll truly never understand this approach, especially from an asset management firm that should know better than to irritate investors.

AUM was R746 billion at the end of March, down 5.1% from R786 billion at the end of December 2025. But if we compare to the R676 billion as at March 2025, AUM is up more than 10% in the past 12 months.

AUM will ebb and flow with the general markets. The more interesting trend will be client flows, something we will only know more about when the company releases detailed financials.

Labat Africa has flagged big moves in its key numbers (JSE: LAB)

So much has changed at the group

If you’ve been following the Labat Africa story, you’ll know that the group has transformed from a cannabis company to an IT company. Management has changed, assets have been bought and sold and they should probably have changed the group name by now as well.

Labat’s financial year-end is in May, while a couple of major subsidiaries are in February. They will consider aligning the reporting periods over time. I suggest they do, as the market doesn’t enjoy any complications like these.

The percentage moves aren’t that important when there have been major acquisitions, as the group has changed so much in a short space of time. Still, revenue is up by between 146.78% and 166.78%, while HEPS is expected to jump by between 96.48% and 116.48%.

More importantly, HEPS is expected to be around 11.15 cents per share, while the net asset value (NAV) per share is expected to be 34.36 cents. Why does this matter? Because the share price is just 5 cents per share.

Yes, that’s a P/E of below 0.5x. The market really has no idea what to do with this thing at the moment.

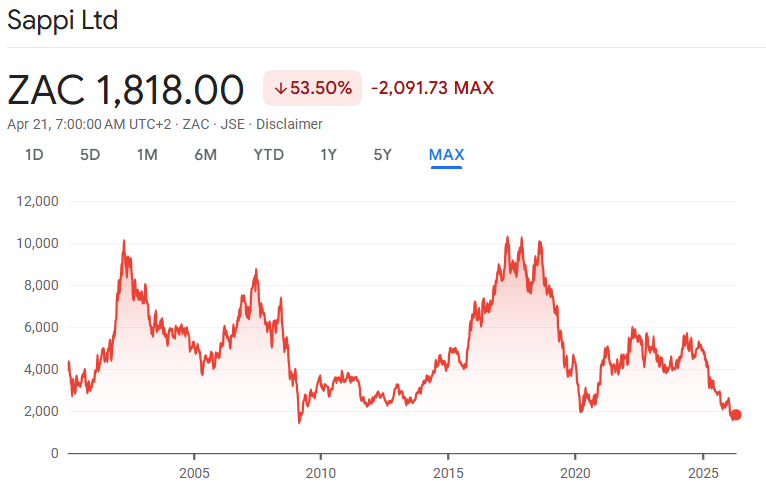

Sappi is still working on the graphic paper JV agreements (JSE: SAP)

These corporate transactions can take a long time to close

In large and complex deals, the negotiation process can take many months. The first step in the dance is a term sheet, which typically triggers a detailed announcement to the market with the high-level transaction terms. But once that’s out of the way, there is still much to be done before definitive agreements are ready to be signed.

This is the part of the process that Sappi is currently working through, in the proposed formation of a joint venture with UPM and Sappi’s graphic paper business in Europe.

It’s a Category 1 transaction, so nothing can be implemented before a circular goes to shareholders and a vote is held. To get to that point, they need to finalise the agreements. As you can see, this deal still has some way to go.

They are aiming to have definitive agreements signed before the middle of this year.

In the meantime, the share price remains in the doldrums. This is a nasty part of the cycle for Sappi. Those with (very) patient capital and a strong stomach may find this chart interesting:

Sibanye-Stillwater puts the spotlight on its international and recycling operations (JSE: SSW)

In other words: not the SA PGM and SA gold businesses

Sibanye-Stillwater is a massive group with interests in various underlying commodities and business models. This can make it tricky for investors to fully understand what’s going on, especially when recent share price movements (up 138% in the past year!) have been driven primarily by the PGM and gold businesses.

The company hosted a focused capital markets day that looked only at the international and recycling operations. This includes the US PGM business. I’ll just touch on a few things here. Those who want to check it out in detail will find the full pack here.

As you might expect, there are a few slides dealing with the expectations for favourable supply and demand dynamics in PGMs over the next decade. The slower adoption of electric vehicles has been bullish for the PGM players, particularly when combined with limited investment in new supply of platinum and related metals.

Sibanye has some exposure to the EV trend through its lithium investments. One of the points made in the deck is that in a “de-globalising world” – in other words a world in which East and West are becoming more isolated from each other – Europe is short on regional lithium projects. This is where the Keliber project in Finland is useful.

There are tons of slides dealing with the Keliber project and the US PGM operations in the deck. There’s also a section dealing with the smaller recycling operations, which have gold, PGMs, silver and copper as their outputs. The recycling business contributed 16% of group revenue in 2025 and 6% of group EBITDA.

If you want to get a much deeper understanding of the group, I recommend working through the slides. There are 94 of them!

What are your thoughts on this part of Sibanye’s group?

Nibbles:

- Director dealings:

- The chairman of Pan African Resources (JSE: PAN) sold shares worth nearly R35 million. This represents a third of his holdings. That’s a very large disposal indeed.

- ArcelorMittal (JSE: ACL) has renewed the cautionary announcement related to the negotiations with the IDC. They are still trying to find a sustainable solution for the future of the business. Unfortunately, this is another example of the “greater good” argument, where South African taxpayers will almost certainly end up subsidising this industry in one form or another so that we can protect jobs.

- RMB Holdings (JSE: RMH) announced that AttBid has picked up some more shares in the company. This takes AttBid to 10.65%. Combined with Atterbury Property Fund’s stake of 32.77%, the parties have 43.42% in total.

- For those keeping score, Premier Group (JSE: PMR) confirmed the position of a couple of major shareholders after the scheme of arrangement that merged the company with RFG Holdings. Titan Premier Investments, Dr. Christo Wiese’s investment entity, holds a voting interest of 36.01% and an economic interest of 22.83% in the merged entity. Brait (JSE: BAT) has voting rights of 7.21% and an economic interest of 18.81%.