Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Kibo Energy’s subsidiary Mast is making progress – I think (JSE: KBO)

Further funding will be needed to support the projects

Kibo Energy continues to languish at R0.01 per share – the lowest possible share price. There are 73.6 million offers in the market at R0.02 and 17 million bids at R0.01, so more investors want out than in – even at this price.

Half the problem is that it’s quite difficult to figure out whether Kibo is delivering good news or not. The announcements are incredibly operational in nature and don’t give enough information in my opinion about the investment opportunities.

For example, the latest news at subsidiary Mast Energy Developments (MED) is that the Pyebridge flexible power generation asset was completed ahead of schedule and is back in operation. Also, the Hindlip Lane project has completed pre-construction work.

The announcement gives an indication of the gross profit margin income that Pyebridge could earn over the next couple of years, but gross profit doesn’t mean much. Net profit is what counts.

When you combine the limited financial information with the generic commentary about how MED is in discussions with various debt and equity providers, it’s really hard to understand how benefits will flow through to Kibo Energy. The only way this company is getting off the R0.01 mark is if they can drastically simplify the investment story and show more hard numbers, rather than endless paragraphs of operational information.

Some resilience at Nu-World, but when will it grow? (JSE: NWL)

Watch out for that working capital balance

Nu-World Holdings imports and distributes appliances, along with some other stuff like specialist liquor. That’s not an easy gig in South Africa, with consumers under pressure and infrastructure issues leading to the group needing to hold far too much inventory relative to sales. There’s nothing easy about a business model in South Africa that relies on consumer discretionary spending.

This is exactly why Nu-World has been putting a great deal of effort into offshore expansion, with those businesses now contributing more operating income than the South African businesses!

This hasn’t stopped Nu-World from being quite the value trap, with the share price not rewarding investors who are buying it at a price far below net asset value per share.

Still, there’s some resilience in this thing now thanks to the offshore exposure, with revenue for the six months to February down by 2.8% and HEPS down 5.0%.

Schroder’s real estate values are still under pressure (JSE: SCD)

Aside from the industrial portfolio, it’s still tough out there

Schroder European Real Estate announced property valuation movements for the quarter ended March 2024. Overall, the direct property portfolio fell by 1% for the quarter. This was driven by “continued outward yield movement” – a fancy way of saying that the capitalisation rate for the valuation was higher, which makes the present value of future cash flows lower. This leads to a negative move in valuations despite rental income being stable.

The highlight is the industrial portfolio, which saw valuations increase 0.4% for the quarter. The office portfolio wasn’t too bad actually, with valuations down 1.1%. The German retail portfolio brought up the rear for the traditional assets, with the valuation moving 2.3% lower. The alternative investments saw their valuations drop 3.2%.

The portfolio loan-to-value is 33% gross and 24% net of cash.

More retrenchments likely at Sibanye-Stillwater (JSE: SSW)

Another day, another s189 for the group

Although there are signs of life in PGMs and gold is at record highs, Sibanye-Stillwater still needs to carefully manage its operations to ensure that the business is run sustainably. The company isn’t shy to enter into retrenchment processes, with a few recent examples.

This time, the issues are losses at the Beatrix 1 shaft (which has not delivered planned production) and the problems at the Kloof 2 plant related to insufficient processing material available to cover overheads after closure of the Kloof 4 shaft during 2023. As a further problem, capital expenditure at Burnstone has been deferred, which means restructuring is needed to align with the reduced capital activities.

With less activity at the mines, the shared services functions for South Africa are surplus to requirements. The company also takes into account further planned investments when making this assessment.

These proposed restructuring activities could affect 3,107 employees and 915 contractors.

Little Bites:

- Delta Property Fund (JSE: DLT) announced that Brett Copans has been appointed as a non-executive director to the board. From what I can see, he’s also the Chief Restructuring Officer at Cell C. How many tough balance sheets can one person deal with at a time?

- Two non-executive directors at Renergen (JSE: REN) will be leaving. The chair of the audit and risk committee will be retiring as a director and another director is resigning with immediate effect for personal reasons.

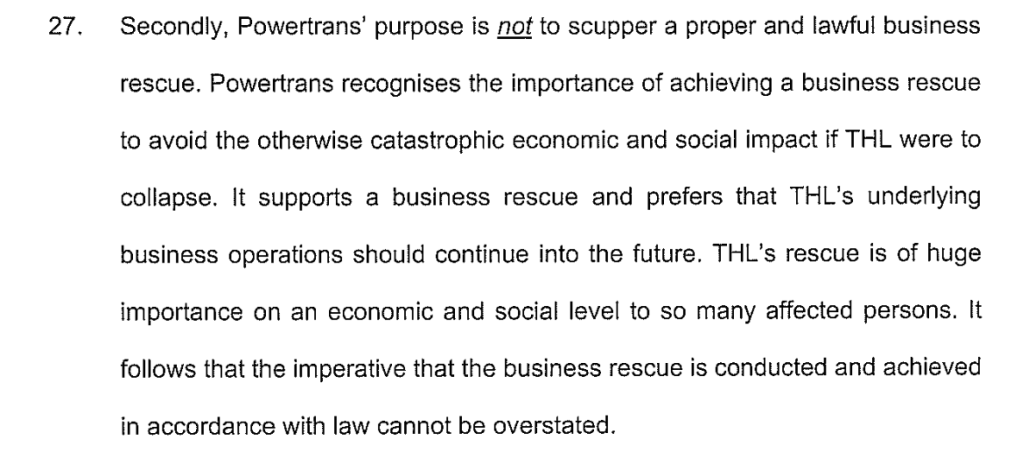

- Although it hardly matters to shareholders of Tongaat Hulett (JSE: TON) as there’s no equity value in the thing anyway, it’s worth mentioning that the drama still isn’t over. Powertrans Sales & Services has applied to court to have the business rescue plan set aside as unlawful. Having said that, a skim through the founding affidavit suggests that Powertrans isn’t blind to the bigger picture here. Check out the screenshot below and read through to the founding affidavit if you’re interested.