Listen to this podcast to get insights into the retail sector from the first few weeks of trading in 2025.

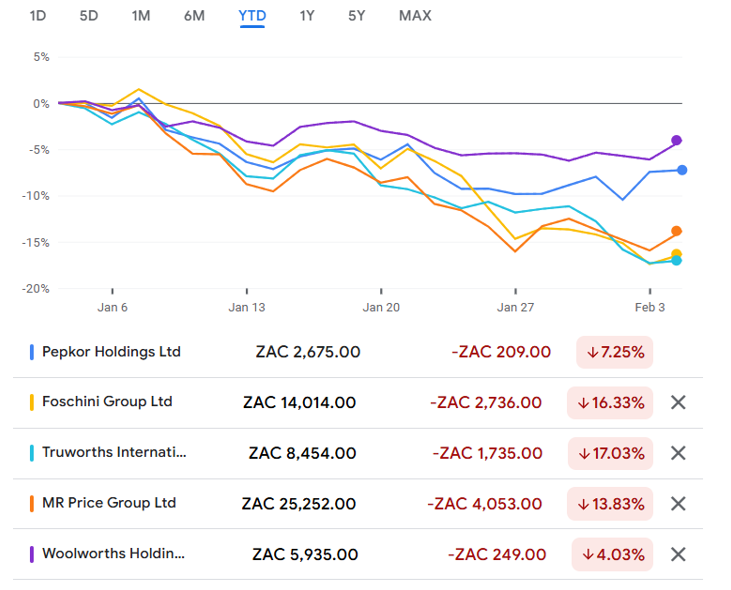

In clothing, it’s quite clear that Pepkor and Mr Price had stronger numbers than The Foschini Group and certainly Truworths, yet the baby has been thrown out with the bathwater in that sector.

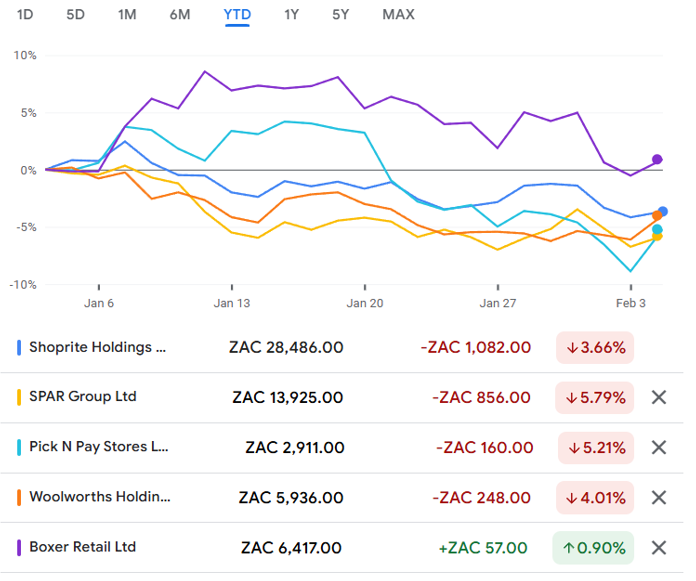

Woolworths is a hybrid model and this is reflected in the performance, with the food business looking far stronger than the rest of the group.

In grocery, Boxer has been the most defensive stock thus far in 2025 and had a solid festive season. Shoprite put in a predictably strong performance as well vs. peers. There are signs of life at Pick n Pay, but it remains well below Shoprite. Spar hasn’t delivered a trading update yet, so the focus there is on cleaning house and getting out of broken investments (like Poland).

We save the best for last: Lewis. The latest numbers are highly impressive and when you consider the discretionary nature of the business, the share price resilience in 2025 has been especially promising.

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

Listen to the podcast here:

Transcript:

Some months are trickier than others when it comes to picking the key themes to cover in this podcast. Luckily, January 2025 was rather obvious though: the retail sector.

If my Little Ghosts had come into this year holding a basket of local retail stocks, they would definitely be telling me about their “owie” – and I’m afraid that neither a kiss nor a plaster would fix it. The clothing retailers really bore the brunt of the sell-off, with Woolworths as the best of a bad bunch, down 4%. Let’s face it, that’s only because of the Food side of the business, which makes Woolworths quite hard to classify in terms of its true peer group.

Truworths is down 17% thus far this year, deservedly holding the wooden spoon in the sector. The Foschini Group isn’t far behind with a 16% drop. Mr Price has been dealt a rather harsh hand I think, down nearly 14% despite releasing strong sales numbers. Pepkor is down 7% and that’s also despite releasing really strong numbers.

It’s a bloodbath.

On the food side, with Woolworths shown once more for completeness, we see the defensive nature of these stocks shining through. The market is still strongly in support of the Boxer story, with a flat performance there despite some pressure in late January. Predictably, Shoprite has suffered less than its peers (other than Boxer), but is still in the red. SPAR has had a tough start to the year and Pick n Pay has been similar.

Not shown on either of these charts is Lewis, with a decline of just 0.9%. Yes, when it comes to the retailers, only Boxer has beaten Lewis thus far in 2025. How many people would’ve guessed that, coming into this year?

Clothing: the tide is out

We can well and truly see who has been swimming naked. Truworths is the worst of the lot, with Truworths Africa down 1.1% for the 26 weeks to 31 December. Sure, they may have achieved 9.9% growth in Office UK (measured in ZAR), but Truworths Africa is still two-thirds of group revenue and we know how fickle the UK retail market can be. Banking on sustainable growth into the UK is a risky game and the market clearly shares that view, as the share price has been punished for the tepid growth in Truworths Africa. For the 26 weeks to 29 December 2024, Truworths expects HEPS to be between 4% and 8% lower. That’s poor.

The Foschini Group is better than Truworths but is in no position to be looking smug here either. Although we have to be careful here as we aren’t looking at exactly the same reporting period, TFG Africa grew 5.3% for the quarter and just 2.2% for the financial year-to-date – so that’s better than Truworths at least. TFG London was up 45.5% for the quarter and 7.2% for the financial year-to-date, both percentages in ZAR, so they are also seeing some joy in that market at least. As for TFG Australia though, the quarter saw a decrease of 3.0% and the year-to-date performance is a drop of 5.2%. TFG Australia is slightly bigger than TFG London, for now at least, so that offset much of the happiness in the UK and the group sales result was just 1.6% year-to-date. At least the third quarter saw growth of 8.4%, so there’s some positive momentum there, but it is still nothing amazing.

We now move on to Mr Price, where there’s a strong story to tell for the 13 weeks to 28 December 2024. Credit sales were up 5.7% but that’s not even the highlight. No, that honour goes to cash sales, up 11.1%. The group has won market share for six consecutive quarters and they even achieved the recent growth at a higher gross margin than in the comparable period. They came into the year priced for perfection in the market after a huge rally in 2024 that caught me by surprise. The recent sell-off is more a function of that valuation I think, than the recent results which were strong.

Finally, Pepkor. In my opinion, this is the best story of the lot. The two major segments put in solid high single digit growth and fintech was up a delightful 35% for the three months to December 2024. PEP and Ackermans (the key banners in the group) both put in strong performances and this is exactly why the fintech business also did well, as they work so closely together. In fact, Pepkor refers to it as a credit interoperability strategy. Tongue-twisters aside, it works and it works well. The disappointment in Pepkor was Avenida, the Brazilian business that I’m enjoying keeping an eye on. Like-for-like sales fell by 2.7% and they need to get that back on track. Still, that’s a small negative in an otherwise powerful result and the good news at Avenida is that sales have improved in 2025.

Woolworths: the hybrid option

Sometimes I wonder whether Woolworths will ever spin the food business off and list it separately. I don’t think it will happen as the operations are intertwined with the clothing side of the business, but it’s a nice dream. It’s certainly a far superior business to the Fashion, Beauty and Home (FBH) offering.

For the 26 weeks to 29 December, Woolworths Food grew 9.0% excluding the acquisition of Absolute Pets. FBH could manage just 2.5%, which puts them ahead of Truworths admittedly (not much of a benchmark) and pretty much nobody else. In fact, it may even be worse than that, as FBH growth was a paltry 0.9% in the last eight weeks of 2024, so it just got worse and worse. For two years in a row, they’ve been blaming supply chain issues. Look, if festive supply chains keep catching you by surprise, then I’m really not sure that retail is the right sector for you bluntly. It becomes almost a little embarrassing now to keep blaming external factors while underperforming competitors. It also keeps getting worse in Australia as well for them, with Country Road Group sales down 6.2% for the period. The same pressures that are seeing at TFG Australia are playing out at Woolworths.

If Food and FBH were listed separately, the share price chart would look like the two lines had a terrible fight and never wanted to speak to each other again, such would be the speed at which they headed in opposite directions.

Shoprite still leads

The giant of local supermarket retail continues to remind us why they are so respected. For the six months to 29 December 2024, sales from continuing operations increased 9.6%. Supermarkets RSA was good for 10.4%. Digging even deeper, Checkers and Checkers Hyper were up 13.5%, so that’s strong outperformance even vs. Woolworths Food as their arch-rival, never mind the rest of the sector. Shoprite and Usave were up 6.7%, which is still impressive, albeit much slower than Checkers and Checkers Hyper.

With the growth in the right place from a margin perspective, I expect to see a juicy jump in HEPS when results come out on 4th March.

Hot off the press, there’s an update from Pick n Pay. Although it’s strictly part of February, it would be really silly not to include it here. Pick n Pay managed like-for-like sales growth in the 19 weeks to 5 January of 3.0%. That’s an improvement on where they were of course, but it’s still way below Shoprite and you have to remember that Pick n Pay is closing supermarkets, so like-for-like growth is probably the most flattering view of the business. It’s also the most important view, but without new stores, there’s no other growth to add on top of that. Within that segment, we find Pick n Pay Clothing with like-for-like growth of 3.6%, so even that’s not much of a growth engine anymore it seems.

Over at Boxer, which of course is now separately listed, we see like-for-like growth of 5.5% over the 19 weeks to 5 January and total growth of 10.8% as the store footprint is still expanding. Boxer is the food retailer that is capable of keeping Shoprite on its toes, albeit in only one customer vertical.

In case you’re wondering, there’s no sales update from Spar. All we know is that the nightmare in Poland has come to an end and they’ve effectively paid the buyer R2.67 billion to drag the carcass away. Good riddance to it.

Ending on a positive note with Lewis

I can’t bucket them in with the clothing retailers or the supermarket retailers, even though there’s some overlap at category level or with specific divisions, like the furniture piece of Shoprite that is currently being sold to Pepkor. No, Lewis deserves to stand on its own here, particularly after the recent update.

Merchandise sales have been heading higher. For the third quarter, they came in at 9.9% – a lovely acceleration from 7.7% in Q1 and 9.3% in Q2. As this drives income and ancillary services revenue, the overall group result was revenue growth of 13.6% for the nine months to December. Suddenly, Lewis is putting its hand up as a growth stock rather than a value stock.

Much like at Mr Price, the big jump at the end of the year was cash sales. I think that tells us a fair bit about where the two-pot withdrawals went. After all, this is furniture we are talking about, suddenly paid for with cash.

This is the one obvious caution that I’ll leave you with: double-digit cash sales at Lewis almost certainly aren’t sustainable. But still, they deserve to do well after years of solid execution and great capital allocation decisions. Bravo!