The world’s largest mining house? (JSE: GLN)

And if Glencore and Rio Tinto do tie the knot, what will be excluded?

We are firmly in an environment of mining mega-mergers. We’ve seen it with Anglo American (JSE: AGL) and Teck Resources – you know, the “merger of equals” that we keep hearing about. We are potentially going to see it in Glencore (JSE: GLN) and global giant Rio Tinto as well.

And based on their market caps, if a deal does go ahead between Glencore and Rio Tinto (and assuming that not too much is carved out of the merged group and spun off), it would create the world’s most valuable mining group. That probably stings for BHP (JSE: BHG) who tried to cement their position at the top of the pile by making an unsuccessful play for Anglo.

There’s a lot going on in the sector, with the big guns all making moves to distinguish the transition metals from the “dirty” fossil fuels like coal.

Nothing is guaranteed at this stage, but Glencore’s share price is roughly 10% higher than it was before the announcement. This story will be in the headlines for a long time to come, regardless of whether it goes ahead or not. The intent for more huge mergers is clearly there.

Grindrod’s Port of Maputo investment is looking good (JSE: GND)

They handled record volumes in 2025

Grindrod highlighted a press release by the Maputo Port Development Company that paints a rosy picture. Grindrod holds a 24.7% stake in this company as part of its core logistics business.

The Port of Maputo enjoyed an all-time high in volumes in 2025, with a 3.4% increase in total tons processed. The growth rate is actually more important than whether it’s a record, but it still makes for a nice story.

Some other highlights include 6.4% growth in direct operations, as well as a 17% increase in rail volumes.

There have been important infrastructure products at the facility, including expansion to both the bulk terminal and the container terminal. Along with improvements to the logistics corridor, momentum is positive for the business.

Keeping the government happy is always an important consideration in frontier markets like Mozambique. With concession fees up by 4.5% to $48.9 million (excluding any taxes and dividends), all the port’s stakeholders are winning.

Northam Platinum produced more PGMs when it counted (JSE: NPH)

This is what you want to see when prices are moving higher

Northam Platinum released a production update for the six months to December 2025. They achieved a 3.7% uplift in total equivalent refined PGMs, as well as an increase of 14.8% in chrome concentrate production.

Eland was the star of the show, with a 19.6% increase in PGM concentrate production and a 44.7% jump in chrome production. The only negative move across the board was a 0.4% decline in chrome production at Zondereinde.

Equivalent refined PGMs from third parties increased by 39.7%.

There are a number of projects in progress at the various mines. With prices looking more favourable, it’s a lot easier to justify capex. In fact, the market will demand that capex takes place to support production!

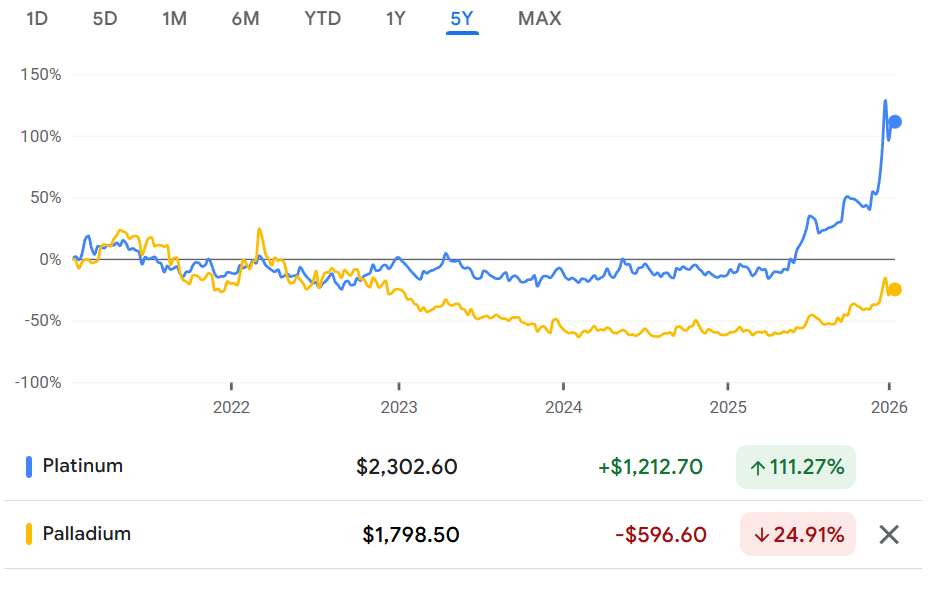

If you’ve ever wondered how important the PGM basket impact is (i.e. the performance over the underlying metals), check out this five-year chart of platinum vs. palladium:

You can also clearly see why the PGM names spiked so strongly towards the end of 2025!

Primary Health Properties celebrates 30 years of dividend growth (JSE: PHP)

It’s a clickbaity milestone, but an impressive one nonetheless

Primary Health Properties kept the headlines busy in 2025 with the Assura deal. The transaction created a much larger healthcare REIT that is still focused on the UK and Ireland. For South African investors looking to diversify their exposure, it’s good to have stuff like this locally available on the JSE.

The focus of a company like this will always be on paying a dependable, growing dividend. This is why it’s a big deal that they’ve just achieved their 30th year of consecutive dividend growth. Naturally, the growth rate is what really counts, as a tiny increase each year just for the sake of that milestone wouldn’t be helpful.

Thankfully, the dividend is up 2.8% on a per-share basis despite such a large acquisition having taken place. This was supported by rent reviews up 3.2% on an annualised basis, so the group is doing a good job of managing inflation. Remember that this is a hard currency play that needs to be seen in the context of developed market inflation and the trajectory of the GBP/ZAR. The cost of debt is also much lower in that market, with a weighted average cost of debt of 3.7% for the company. You therefore can’t compare these percentages to South African property funds without making allowance for the structurally different regions.

The aftermath of the combination with Assura seems to be going well. They’ve already delivered 60% of the total annualised synergies of £9 million, mainly through reducing duplicate roles and professional fees. I’m sure that the remaining 40% won’t be quite as easy.

The other challenge is to get the balance sheet back to the stage where they are within the targeted leverage range of 40% to 50%. A temporary increase in debt ratios is normal in the wake of an acquisition, with strategic asset disposals as a likely strategy in bringing debt levels back to where they want them. They’ve also already refinanced £225 million of the £1.225 billion acquisition facility, so they don’t waste any time at this place in getting things done.

Fitch currently has the company on BBB- with a negative outlook. This is based on execution risk around asset disposals, so any progress made in addressing that risk will do wonders for the credit rating and cost of debt.

Looking deeper at the performance for the year ended December 2025, rental growth on a like-for-like basis was up by 2.7%. The contributions were similar: PHP at 2.6% and Assura at 2.8%.

There is a significant development pipeline across the enlarged group. With completion dates in 2026 and 2027, the pipeline has a remaining cost to complete of £39.5 million and a yield on cost of 5.4%.

Other than a strange spike in early September 2025, the share price has been range bound for the past six months. There is some positive recent momentum though. The market tends to be cautious in the period immediately after an acquisition, although I think that this announcement will do wonders to calm those nerves.

Shuka Minerals is finally ready to move forward with its acquisition (JSE: SKA)

It’s certainly taken long enough to raise the money

You have to feel for Shuka Minerals. They’ve been put through a horrible experience by their funder, Gathoni Muchai Investments. I’ve lost count of how many announcements I’ve seen about delayed funding, despite numerous promises that it would come. The fact that the acquisition of Leopard Exploration and Mining didn’t fall through is nothing short of a miracle.

There were four announcements over the just the past few days, which tells you how closely the situation was being monitored by Shuka’s management team and the company’s stakeholders.

Thankfully, a further payment of £815k was received by the company from its funder, with teeth having been pulled to reach a paltry balance of just £1.115 million (this really is a tiny number in a corporate funding context). A further £385k is undrawn under the facility.

The other big news from a capital raising perspective is that £1 million has been raised through a share placement at 4 pence per share. That’s well below the current (illiquid) share price of R1.07, although it traded as high as R1.50 just yesterday. The bid-offer spread is wide enough that you could park all the recent SENS announcements in that gap and still have space.

There’s also an issuance of share warrants to the equity investors that could raise an additional £2 million at 8 pence per share (valid for 3 years).

What is the prize at the end of all this? Well, acquisition target Leopard Exploration and Mining brings them Kabwe, which they describe as “one of the world’s richest and most notable zinc mines” – and with a production track record going back to 1904! The mine was closed in 1994 as it had become uneconomical to run based on commodity prices at the time.

The zinc and lead resources at Kabwe are estimated to have value of over $2 billion. Naturally, you still have to get the stuff out the ground, with work having been done to establish positive expected returns.

With the funding for the acquisition in place and now additional funding raised, the company will look to undertake drilling work and associated studies (including technology that wasn’t used before at Kabwe, like gravity and magnetic studies). They also need to upgrade infrastructure. The goal is to update the resource estimate later in 2026. This will be key to securing further funding.

Shuka also owns the far less exciting Rukwa coal project in Tanzania. They reckon they can invest just $150k to achieve a staged ramp up to 5,000 tonnes per month in washed coal. This implies an IRR of 80%. $150k is literally pocket change in any corporate context and that IRR is huge. If those numbers are true, they should have no problem raising the money.

Speaking of money being raised, remember that capital raises are going to happen frequently for a company like this. Junior mining is all about reaching milestones and raising capital accordingly. Volatility is really the only guarantee.

Better production yields gave Tharisa a year-on-year boost (JSE: THA)

But the quarter-on-quarter comparison is less favourable

Mining is a difficult game. Not only do you have to navigate commodity prices that can be highly volatile, but you also have to actually produce the commodities in question! Only the latter is within the control of management, so mining houses tend to be judged on their production numbers.

Tharisa has released their production report for the quarter ended December 2025. This marks the first quarter of the 2026 financial year.

The main highlight is a substantial improvement in recovery rates (i.e. the production of PGMs and chrome relative to the reef they processed). This is important, as it can make up for a period in which total material processed was lower.

On a year-on-year basis, PGM production was up nearly 30% and chrome was down 6.7%. It would obviously be nice if both were positive, but PGMs are what counted in that quarter based on a delicious spike in the commodity price.

If you compare the December quarter results to the September quarter results (i.e. a sequential quarter-on-quarter view), you’ll find that PGM production fell 6.1% and chrome was down 14.2%. That’s obviously far from ideal, with weather and other impacts this quarter. It’s also worth noting that the net cash position fell from $68.6 million as at September 2025 to $47 million as at December 2025.

Full year guidance is for PGM production of between 145 koz and 165 koz. Although production is rarely a straight-line thing, guidance can be assessed in the context of Q1 delivering 38.8 koz. On the chrome side, guidance is for 1.50 to 1.65 Mt, with Q1 having delivered 0.35 Mt.

Nibbles:

- Director dealings:

- An entity associated with Johnny Copelyn, CEO of Hosken Consolidated Investments (JSE: HCI) bought shares worth R31.6 million. That’s a substantial purchase!

- Prosus CEO Fabricio Bloisi’s wife bought shares in the company (JSE: PRX) worth a cool R19 million. That’s a solid show of faith in her partner!

- A non-executive director of MTN (JSE: MTN) bought shares and sold them within roughly a month for a profit. The total value of the sale was roughly R1.75 million. Concerningly, clearance to deal does not appear to have been obtained.

- An associate of a non-executive director of Afrimat (JSE: AFT) sold shares worth R440k.

- Acting through Titan Premier Investments, Christo Wiese is back on the bid for Brait (JSE: BAT). He bought shares worth over R260k across various trades.

- The CEO of Spear REIT (JSE: SEA) bought shares in his family investment vehicles worth over R121k.

- Jan van Niekerk and Piet Viljoen are using Maximus Corporation as their primary investment vehicle to hold their stake in Goldrush (JSE: GRSP). A number of CFD transactions were entered into to effect this restructure. Maximus has direct and indirect exposure to 18.61% in Goldrush.

- Trustco (JSE: TTO) has been trading under cautionary for ages now in relation to the company potentially going private. They’ve noted that based on the simplified listing requirements that have been released, they might rethink this decision. As always, there’s never a dull moment with them.

- Labat Africa (JSE: LAB) has renewed the cautionary announcement regarding a potential AI and technology company with operations and a significant footprint within the SADC region. As for who it is, we have no idea at this stage. Remember, there’s no guarantee of a deal going ahead here, hence the need to exercise caution.

Thanks for all your great work.

Can you do a Supernatural podcast dealing with investing in a company based on good, dynamic and ambitious management? [With examples from JSE companies]

Thanks

Thanks! Yup nice topic. Any management teams that specifically come to mind for you?

Super Group – Peter Mountford fixed the business, sold possibly at perfect time, trusted pair of hands

Hudaco – Can’t get more solid mang. team

OMU – out with the old and in with the new – do you back Jurie

Prosus – I know you like Balasio

MRP, WHL, TFG – Should be fired, stupid deals

Afrimat – Was great until 2025 wobble

Harmony – Fixed gold prod. and entered copper at nick of time

Labat – would’t touch it with van Rooyen, but now its a different game

But the point is to look at a solid management team and buy based on that.

I’ll leave it to you!