Sea Harvest financials for the year ended December 2025

“Sea Harvest Group’s latest annual results reflect a strong operating performance, supported by robust demand for wild-caught seafood and favourable hake fishing conditions. Improved volume efficiencies, lower fuel costs, and continued discipline in cost management further contributed to the Group’s solid financial outcome.”

Felix Ratheb – CEO

Sea Harvest Group has delivered the strongest performance in its history for the year ended 31 December 2025, driven by improved hake fishing conditions and firm global and domestic demand for sustainable wild-caught seafood, disciplined execution of its strategy, and improved operational efficiencies across the Group.

Felix Ratheb, CEO of Sea Harvest, says the Group’s strong performance reflects the deliberate steps it has taken over time to position the business for sustainable growth. The Group invested in organic expansion and acquired best-in-class fishing businesses in South Africa, ensuring that it was built on a solid operational foundation. “Once these strategic initiatives were fully embedded and operating conditions turned in our favour, we were well positioned to capitalise on the opportunity.”

Delivering as the tide turned

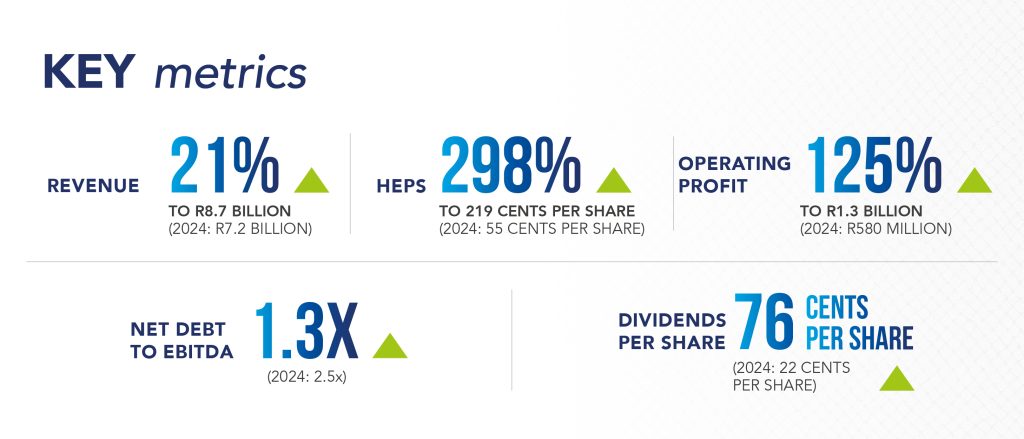

Revenue for the Group surged by 21% to R8.7 billion (USD548 million), while operating profit jumped 125% to R1.3 billion (USD82 million), improving the operating margin from 8% to 15%. Headline earnings per share (HEPS) from total operations climbed to 219 cents, a four-fold increase from 2024’s 55 cents. The Group declared a dividend of 76 cents (2024: 22 cents per share). “Demand for Cape Hake remained very firm, particularly in Europe, supported by reduced supply from competing species such as cod, where volumes declined significantly,” says Ratheb.

A favourable exchange rate, lower fuel prices, and a disciplined focus on cost management – developed over the past three challenging years – contributed to margin expansion, with the gross profit margin increasing to 36% and the earnings before interest, tax, depreciation and amortisation (EBITDA) margin to 28%. “Debt reduction improved, supported by our robust performance,” says Muhammad Brey, CFO of Sea Harvest, adding that net debt improved by R417 million to R2.24 billion, further strengthening the balance sheet and lowering the net debt to EBITDA ratio to 1.3x (from 2.5x in 2024). Importantly, the Group recorded a solid improvement in return on invested capital (ROIC) relative to weighted average cost of capital (WACC), a key strategic focus area and important metric for the business, reflecting improved capital efficiency.

Harnessing strong demand to deliver performance

“The results reflect operational tailwinds and hard-won operational gains,” says Ratheb, adding that the star of the show was firm global and local demand for wild-caught, sustainable seafood, which lifted pricing across markets and channels. “Hake, our anchor species, benefited significantly from improved biomass and catch rates, with volumes increasing by 17% driven by a higher total allowable catch (TAC) and a 42% improvement in catch rates reflecting favourable fishing conditions. This performance was made possible through the additional fishing capacity we acquired, improved utilisation of our world-class assets, and strong planning and execution.”

He adds that this was complemented by an exceptional performance in the pelagic business where strong volumes and improved fish oil yields contributed positively. “Although wild-capture businesses in South Africa continued to anchor our earnings as expected, a recovery in Australia supported our global portfolio. Sea Harvest Australia posted revenue growth of 13% to R1.13 billion, aided by better prawn pricing and engineering-business performance.” He notes that volume efficiencies and good cost control were experienced across the Group.

Back home, Ladismith Cheese delivered improved efficiencies on the back of increased milk flow of 8% and muted inflation.

“Our abalone business, the smallest component of the Group, underwent structural challenges related to revenue pressure from slow demand in China. We are consistently right-sizing the business to ensure it is fit for purpose and ready when the Chinese market rebounds,” says Ratheb.

The investment case: A laser-focus on core operations

A headline strategic development in November 2025 was the proposed disposal of Ladismith Cheese for R840 million in 2026. Even though Ladismith Cheese has been a sound investment over the past six years, in a growing sector, the proposed disposal forms an integral part of Sea Harvest Group’s sharpened focus on building a streamlined, diversified seafood portfolio.

Ratheb explains that the disposal is intended to redirect capital towards higher-return areas, enhance margin quality, and accelerate debt reduction. “Part of our strategic investment case is that we are a diversified seafood business with exposure to all material wild-caught fisheries in South Africa and Australia. The disposal not only strengthens our investment proposition but also ensures we remain focused on delivering what is on the box, fully aligned with our strategy,” he says.

In addition, the Group’s hake and pelagic offerings are secure: It holds long-term security of tenure through 15-year rights in hake and pelagics in South Africa, complemented by perpetual rights in Australia. Its South African hake and Australian prawn fisheries are Marine Stewardship Council (MSC)-certified, and Sea Harvest Pelagic is Marin Trust-certified, underscoring the Group’s sustainability credentials.

“We have a geographically diverse customer base that provides a strong rand hedge, with approximately 54% of sales from export markets, which will expand to 64% following the Ladismith Cheese disposal, making Sea Harvest and an excellent portfolio diversifier,” says Ratheb. For investors who may be cautious about supply-demand dynamics in the fishing industry, Ratheb notes that sector fundamentals remain attractive. “Global demand for premium, wild-caught, sustainable seafood continues to exceed supply, while aquaculture is one of the fastest-growing global food sectors. Notably, aquaculture output now exceeds wild-caught fisheries, and fishmeal and fish oil – core products in our pelagic operations – are essential components of aquaculture feed.”

Aquaculture operations globally depend on high-quality feed, with the Group’s fishmeal and fish oil primarily supplied to salmon farms. As the premium species within global aquaculture, salmon represents approximately 2% of total aquaculture production yet contributes close to 20% of the industry’s value. This allows the Group to participate in an attractive and high-value segment of the aquaculture ecosystem.

Outlook

Sea Harvest expects 2026 to present both opportunities and choppy waters. “The hake TAC was reduced by 5% at the start of 2026, and the pelagics TACs remain under pressure. A strengthening rand may also temper pricing tailwinds. We are responding with continued focus on efficiencies, cost discipline, and creating value from local and international markets,” says Ratheb.

The pelagic division enters the year with stronger fishmeal and fish oil pricing, although currency movements may offset some of these benefits. Investment in two new pelagic vessels and the upgrade of the fishmeal plant remain on track, supporting the Group’s medium- to long-term growth capacity. In Aquaculture, the near-term outlook remains muted until Chinese consumers increase their discretionary spend. With the Ladismith Cheese disposal anticipated to conclude in the first half of 2026, the Group’s diversified seafood-focused strategy will become even more pronounced and aid in strengthening its balance sheet.

Ratheb says that a sharper, more focused seafood business is better positioned to deliver higher margins and improved free cash flow conversion, which are expected to support improved dividend capacity and enhanced long-term shareholder returns. “Tightening the net over the next three-year period reflects a mature organisation, one that is leaner; more disciplined; and focused on long-term, sustainable value creation for all stakeholders.” For investors, the latest results should demonstrate that Sea Harvest is not simply casting nets but is instead providing a compelling catch built to outlast any season.

VIEW THE FULL RESULTS HERE >>>

Note: Sea Harvest values the Ghost Mail audience and the company has placed its earnings here accordingly. This article reflects the views of the company. For the views of The Finance Ghost, refer to the section in Ghost Bites dealing with these results.