Dividend darling Clientèle wants to delist (JSE: CLI)

When shares trade at a discount for long enough, this is what happens

Clientèle is one of the companies on the JSE that has historically offered a fat dividend yield. This is because the market isn’t willing to pay up for the shares, despite the company generating decent growth at times.

Lack of liquidity in the shares creates a structural impediment for the valuation, as it means that institutional investors struggle to get involved here.

This creates the perfect conditions for a buyout offer.

In this case, Clientèle is giving investors a chance to remain invested in the delisted company. It’s always worth remembering that liquidity in unlisted companies is close to zero, so investors must think carefully here.

The offer price is 85% of the embedded value per share as at December 2025, which implies a base price of around R19.25. Before the news of the offer, the shares were trading at only R16.

The offer price escalates over time, with the company assuming an offer price of R19.90 with a payment date of 29 June 2026. An independent expert opinion on this price will be included in the circular that will be distributed to shareholders in due course.

It’s worth noting that there is also a process that will allow executive directors and members of management to subscribe for up to 4.8 million shares at the same price as the offer price. This will be funded by Clientèle Life on favourable terms, so you can essentially think of this as a management incentivisation programme.

There’s a maximum acceptance condition in this deal. If more than 8% of the offer shares are tendered in the offer, then the entire deal falls over. This should be fine, as irrevocable undertakings not to accept the offer are in place from holders of 93.08% of shares.

Holders of 30.74% of shares eligible to vote have already provided irrevocable undertakings to vote in favour of the delisting. There’s still a long way to go here, as they need 75% approval for the delisting.

The announcement also notes that Acacia Empowerment Investors (a subsidiary of the Hollard Foundation Trust) will invest over R270 million in new shares in Clientèle. This will help address the challenge of Black Ownership, which has dipped below 10%. It will also do wonders for Clientèle’s post-offer balance sheet. Technically, this subscription for shares isn’t inter-conditional with the delisting.

Glencore is telling a bullish story after Q1 (JSE: GLN)

With the share price up 40% year-to-date, the market was expecting nothing less

Glencore has released its production report for the first quarter of 2026. They’ve reiterated guidance for full year 2026, so things have gone to plan thus far in terms of production.

This doesn’t mean that there aren’t huge percentage movements on a year-on-year basis (like cobalt production down 39% and copper up 19%). It just means that they are running more or less in line with internal expectations and forecasts.

In the mining operations, the energy price spike is putting pressure on input costs. For now at least, price increases in commodities like copper, zinc and energy coal are more than offsetting the cost impacts, so Glencore has flagged margin expansion as a likely outcome this year.

But the real treat lies in the Marketing business, essentially Glencore’s energy trading activities. Glencore’s team has a reputation for being the Wall Street bankers of the mining sector. As the market expected, their brains trust made a killing this quarter. If they keep up the performance seen in Q1, they will “comfortably exceed” the top end of the long-term adjusted EBIT guidance range of $2.5 billion to $3.5 billion.

Remember: volatility is how trading houses make their money. This is exactly why I have long-term investments in US banks like JPMorgan and Goldman Sachs – global equity markets are highly interconnected places that regularly dish up dislocations that can be taken advantage of. Glencore does much the same thing in energy markets, so those who hit the BUY button on this stock in response to the war in Iran are certainly smiling.

Merafe should have an answer on electricity tariffs by June (JSE: MRF)

A public participation process will take place in May

Merafe shareholders are anxiously awaiting a solution to the crisis facing the company’s ferrochrome smelters. This is also relevant to shareholders in other companies like Afrimat (JSE: AFT), where the pain in the industry is being felt further up the value chain.

Engagements with Eskom and NERSA have been encouraging, with Eskom and Merafe agreeing on a proposed tariff that has been submitted to NERSA for consideration and approval.

A public participation process for the tariff will be held on 25 May. NERSA expects to publish a final decision by 15 June. Merafe is pushing the regulator as hard as possible, as a section 189 retrenchment process at Merafe hinges on the outcome.

MTN continues to print money in Nigeria (JSE: MTN)

The relative strength of the naira is supporting earnings

With Nigeria as a major oil producer, the recent spike in the oil price is supporting the economic story in that country. The naira actually strengthened against the US dollar during the first quarter of the year, giving MTN Nigeria a buffer against capex and other inflationary pressures.

This is really important, as currency movements have historically been a huge headache for MTN’s ambitions in the country. With all outstanding foreign currency loans repaid, they’ve derisked the business significantly.

The latest results are great, with service revenue up by a meaty 41.9%. You would expect data revenue to be doing well (up 56.2%), but a significant increase in voice revenue of 22.5% is a reminder that Nigeria is a frontier market with immense upside.

EBITDA jumped by 68.1%, with EBITDA margin expanding by 8.7 percentage points to 55.3%.

Capex increased by 92.8%, serving as the perfect reminder of how currency weakness can take capex to really difficult levels. Even with the strength of the naira, capex increased at a much faster rate than EBITDA. This is why free cash flow was up by “only” 55.6%.

MTN Nigeria is investing in network capacity and quality while the going is good. This is a sensible strategy, as they are playing the long game in the country. With smartphone penetration up by 5.5 percentage points to 66.2%, the growth opportunity in areas like data is clear.

Notably, with diesel costs locked in for Q1 and Q2, they have indicated a potential negative impact of 180 – 200 basis points on full year EBITDA margin if costs remain elevated. This is due to the energy component of tower lease costs.

At corporate level, they are looking at separating the fintech businesses from the rest of MTN Nigeria. This will allow MTN Group Fintech to take a 60% stake, with MTN Nigeria holding 40%. Activity like this is aimed at creating different entry points in the group for investors with specific mandates e.g. those who are only interested in the fintech business.

You might be wondering about the suspension of airtime credit services and the impact this had on the Optasia (JSE: OPA) share price. Optasia is down 11.5% year-to-date, with one of the factors being that MTN Nigeria has simply switched off the airtime and data credit offering due to the implementation of new regulatory processes.

Here’s the real concern though:

“Following the initial impact of the suspension, recharge patterns have continued to normalise as affected customers settle outstanding balances and maintain service usage. This has supported a progressive recovery in revenue driven by higher self-funded recharges.”

Correct me if I’m wrong here, but if MTN Nigeria can just switch off Optasia and then see a normalisation in demand, what exactly is Optasia’s moat?

Now that we’ve covered both Glencore and MTN today, give me your views on investing in the oil theme:

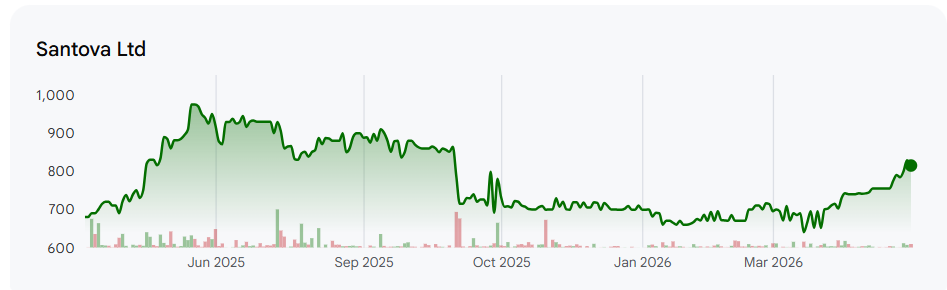

Santova clawed back some lost ground in the second half (JSE: SNV)

The full-year HEPS decline is far better than the interim numbers were

Santova has released a trading statement for the year ended February 2026. They have flagged a decline in HEPS of between 4.9% and 9.9%.

That’s not great of course, but it’s a whole lot better than the nasty decline in HEPS of 23.1% that shareholders were asked to stomach for the six months to August 2025.

Santova’s share price has bounced back strongly since the immense pressure it came under in the aftermath of those interim numbers:

With a 52-week low of R6.11 and a spot price of R8.15, those who bought the dip are solidly in the green. Investors will have to wait for 26th May to get the details on the improved financial performance in the second half of the financial year.

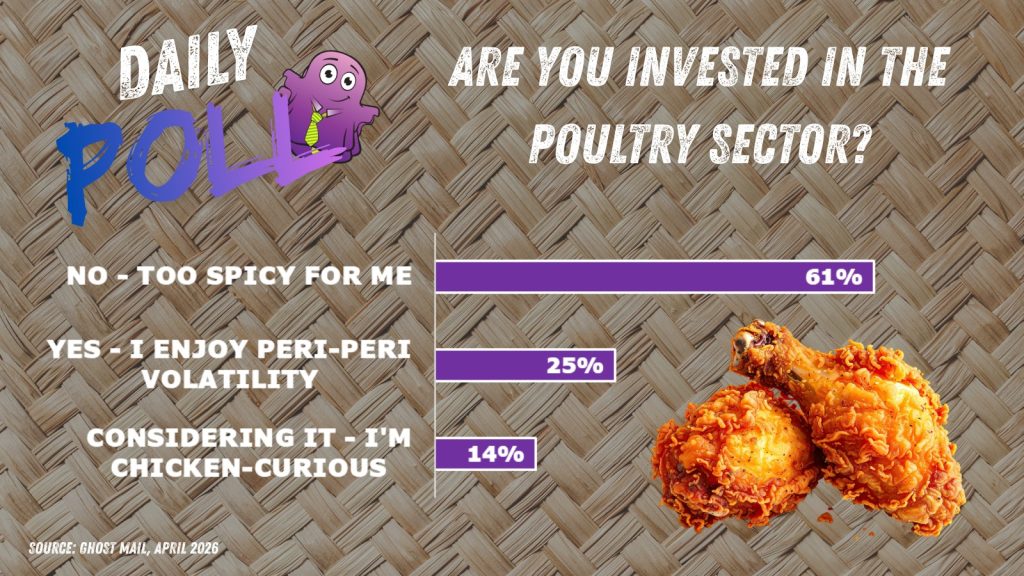

Results of the previous poll:

Nibbles:

- Director dealings:

- A director of Sasol (JSE: SOL) sold shares worth R2.25 million. The share price has more than doubled year-to-date thanks to the oil price spike.

- An associate of a director of South Ocean Holdings (JSE: SOH) bought shares worth R193k.

- In case you wanted more details on the excellent recent performance at CMH (JSE: CMH), the company has made the analyst presentation available on its website here.

- MC Mining (JSE: MCZ) released an activities report for the three months to March 2026. They suspended operations at Uitkomst Colliery with effect from 1 March, so they are looking to minimise the pain there while they deliver the far more exciting Makhado Project. Kinetic Development Group has a 51% stake in MC Mining after investing a further $6 million during April 2026. This capital, along with the previous investments by Kinetic, is being used to develop Makhado into South Africa’s largest hard coking coal producer. Development work was slow at the beginning of the quarter due to flooding, but picked up towards the end. Hot commissioning activities and the start-up of the coal plant are scheduled for May 2026.

- South32 (JSE: S32) released an update on the Taylor zinc-lead-silver project at Hermosa in the United States. Infill drilling programs have taken the life-of-mine to 33 years, an increase of 5 years since the final investment approval. At the adjacent Peake deposit, exploration activities have increased the Mineral Resource estimate by 32%. Unfortunately, there seem to be performance issues with the development contractor, with first production now expected in H2 FY28 and nameplate capacity by FY31. They are putting $3.3 billion into this project, with expected steady-state EBITDA of $650 million and a net present value of $3.1 billion. If spot prices hold, which is a very big “if”, then EBITDA would be $800 million and the net present value would be $4.5 billion. Mining development is a game of educated guesses.

- Orion Minerals (JSE: ORN) released a quarterly update that reflects the company’s transition from an explorer to a base metals producer. The main achievement during the quarter was the finalisation of the agreements for the prepayment facility and concentrate offtake with Glencore (JSE: GLN). They are aiming to complete the remaining conditions precedent in the second quarter. The broader plan for the year is to commence the construction of the Uppers at Prieska Copper Zinc Mine and to finalise the optimisation studies at the Okiep Copper Project. Another useful milestone was the selection of Orion’s Northern Cape exploration portfolio for the 2026 BHP Xplor accelerator programme.

- Kore Potash (JSE: KP2) added its name to the list of quarterly operating updates. There are various workstreams underway at the Kola Project. There’s also a party busy with a due diligence process on potentially acquiring the entire company, so current shareholders might be out of this thing before it even reaches production. But for now, absolutely nothing is guaranteed. The company had $8.3 million in cash as at 31 March 2026 to fund ongoing activities. They continue to engage with OWI-RAMS regarding financial packages for the full project, with development finance institutions having indicated the importance of Kola appointing a suitable contract operator. It seems like there are a bunch of moving parts and interdependencies at the moment.

- Just to add insult to considerable injury, ArcelorMittal (JSE: ACL) released its audited financials for the year ended December 2025 along with a “change statement” – a rare thing on the JSE. It means that something changed between the initial financial release and the final audited accounts. There are a few changes, with one example being the impairment of a gas treatment plant by R112 million. This is a non-cash charge, but it’s still a perfect summary of the troubles that the group is currently dealing with.

- Salungano (JSE: SLG) has released interim results for the six months to September 2025. As you can see, they are still catching up on their financial reporting. In this now very outdated period, normalised EBITDA jumped from R272 million to R511 million. HEPS was 38.48 cents vs. 21.56 cents in the comparable period. This was thanks to a sharp increase in the Moabsvelden mine’s production, as well as the restart of Vanggatfontein. Given the underlying momentum here, I’m sure the company is looking forward to being in a position to lift the trading suspension on its shares.

- Zeder (JSE: ZED) shareholders have given near-unanimous approval to the transaction to dispose of Zaad. Only 0.01% of votes at the meeting were cast against the transaction.

- enX (JSE: ENX) has now completed the disposal of the remaining 75% stake in West African International to Trichem SA. Just under R295 million has flowed, although there are still post-closing adjustments to work through. Once that has all happened, the board will consider a return of net surplus cash to shareholders.

- Hammerson (JSE: HMN) announced that CFO Himanshu Raja will be retiring as a director on 12 August 2026 after the publication of results for the year ending June 2026. He’s served as CFO for five months and will stick around for a 12-month transition period. Richard Shaw, Deputy CFO, will become Interim CFO when Raja steps down.

- In case you wondered whether we were firmly in a return-to-office environment in large corporates, Aspen (JSE: APN) announced the resignation of Group Chief Corporate Officer Reginald Haman due to his desire to relocate to the Western Cape. At that level, you would think that a relocation is something that could be managed without losing such a senior resource.

- Heaven knows what the backstory is here, but Labat Africa (JSE: LAB) announced the removal of Farook Paruk as a director of the company based on “certain governance matters” and Paruk being the “subject of an external investigation” (with no conclusions reached at this stage). I can’t find any other information online on this matter.

- Cilo Cybin Holdings (JSE: CCC) announced that Jessica Moodley-Theron has been appointed as acting CFO. She was already on the board as a non-executive director, with the switch in role necessitated by the resignation of the group CFO.

- African Dawn Capital (JSE: ADW) is suspended from trading. They are way behind with financials, having been suspended since July 2025 for failure to release February 2025 accounts. They aim to catch up on the outstanding annual and interim financials by June 2026 – just in time to be behind on February 2026 numbers!

- Trustco (JSE: TTO) is suspended from trading due to the time it has taken to finalise the appointment of auditors that meet the requirements for the dual-listed structure in Namibia and on the JSE. They are in the process of appointing suitable auditors from a JSE perspective, with the Namibian process ongoing at subsidiary and investee levels.

- Globe Trade Centre (JSE: GTC) has almost no liquidity at all in its stock on the JSE. In case you are somehow sitting with shares here, you’ll want to know that the results for the year ended 31 December 2025 have been published. FFO (funds from operations) halved and the net LTV (loan-to-value) jumped from 52.7% to 57.0%. Ouch.

Please do unlock the stock with LABAT

Thanks