In this edition of Ghost Bites:

- Coronation signs off on a disappointing period

- Datatec turned modest revenue growth into an excellent HEPS increase

- eMedia looks like they are being squeezed by an anaconda

- Frontier Transport must be thrilled with its electric busses

- HCI is now selling more coal than toys

- Pepkor is my pick in the clothing sector

- Santova’s results have been impacted by the Seabourne acquisition

- Stefanutti Stocks has moved past its most speculative era

- Tsogo Sun put in a commendable self-help effort

- Zeda is working out well for me

Coronation signs off on a disappointing period (JSE: CML)

Revenue growth was insufficient relative to operating expenses

Coronation’s numbers for the six months to March 2026 aren’t nearly as impressive as their billboards at the airport.

It’s been a rough time in the markets (outside of AI infrastructure and energy stocks) thanks to the Iran conflict that impacted asset values near the end of the period. Assets under management (AUM) dipped by 2% over the six months to R746 billion.

Thanks to an increase in the average AUM for the period, revenue was up by 3%. It’s not enough though, as total operating expenses increased by 4%. Thanks to other income and various funding line items on the income statement, we find an increase of 6% in profit from fund management.

Right at the bottom of the income statement, there’s a decrease in HEPS of 5%. It’s a “meh” set of numbers that are a reminder that Coronation is largely exposed to broader asset prices, as they don’t have a strong underlying distribution business (like PSG (JSE: KST) for example).

Ghost Bite: Coronation’s total return over the past year is 23%. These numbers don’t give much support to that move.

Datatec turned modest revenue growth into an excellent HEPS increase (JSE: DTC)

Can AI drive a juicy investment cycle for them?

Datatec has been a strong performer in recent years, but the share price dropped by almost 8% in response to the latest results. The market clearly saw something that it didn’t like.

One of the worries in the broader sector is that these IT distribution companies seem to be under eternal margin pressure. Sure enough, despite gross invoiced income growth of 9.3%, revenue was only up by 3.3%. Gross profit increased by 9.6%, so some of this is just the way in which the economics are recognised on the income statement. But still – there are concerns here.

Datatec has done an excellent job of turning that growth into profits for shareholders. Adjusted EBITDA was up by 17.8% and HEPS jumped by a delicious 56.5%.

The dividend was only up by 12.5% though, so cash quality of earnings is another question mark. Perhaps a prioritisation of debt reduction is the reason, as net debt reduced by 10.4%.

Management certainly sounds upbeat, with founder and CEO Jens Montanana describing this as “one of the strongest years in our history”. It also doesn’t take them long to talk about AI as a driver of demand.

A quick look at the segmental report shows that adjusted EBITDA margin increased across the three segments. Logicalis Latin America remains the relative headache, with margin of 5.4% vs. 8.9% in Westcon International and 9.2% in Logicalis International.

Ghost Bite: Datatec almost never gets mentioned in articles that talk about JSE-listed companies with great offshore businesses. That’s a pity, as they are actually one of the bext examples!

eMedia looks like they are being squeezed by an anaconda (JSE: EMH)

We are so far past the golden days of TV

You know things are tough in media when the opening line in the eMedia results is that they are “happy to once again present a set of profitable results” – talk about a low bar!

They are on a treadmill here, with the television advertising market going backwards by 8.7% in the latest year. YouTube is going to destroy the traditional TV model in the same way that the internet broke print media. The company famous for anaconda reruns (and spicier forms of entertainment back in the day on a Friday night…) looks like they are fighting for relevance in one of their action movies.

Revenue for the year ended March 2026 was down 5.2% and operating profit fell by 8.3%. HEPS came in 4.7% lower at 43.48 cents. Despite this, the dividend was maintained at 15 cents per share.

Ghost Bite: This is a slow puncture of note. There’s a distinct difference between a value stock and a value trap. In my opinion, this is firmly in the latter bucket.

Frontier Transport must be thrilled with its electric busses (JSE: FTH)

Diesel is not what you want to be buying right now

If there were any prizes for descriptive writing and flashy sentences in the results commentary, then Frontier Transport Holdings would trade at a higher valuation. Alas, investors tend to care more about the numbers than anything else, with little to get excited about in the year ended March 2026.

Revenue was down 6.5% and HEPS was up by just 0.3%. The dividend increased by 7%, but that’s clearly not a sustainable trend in the context of this HEPS move. The mitigating factor is that cash generated from operations jumped by 41%, so there’s plenty of cash running around.

This is an extremely tough business, with businesses like Golden Arrow Bus Services competing against players that aren’t renowned for ethics, like the taxi industry. Frontier also highlights how online gambling reduces people’s transport budgets. This is one example where I think that’s a fair point to make, as I can see the destructive online behaviour leading to people just sitting at home.

The company is investing heavily in electric buses, with debt levels up R340 million in the past year. Given the outrageous recent increase in diesel prices, that might turn out to be a great investment!

Ghost Bite: Frontier’s total return over three years looks excellent at 90%. But be careful: it’s been a sideways story for a long time now, with those gains mainly coming in late 2023. There is at least a very juicy dividend that pays you to wait!

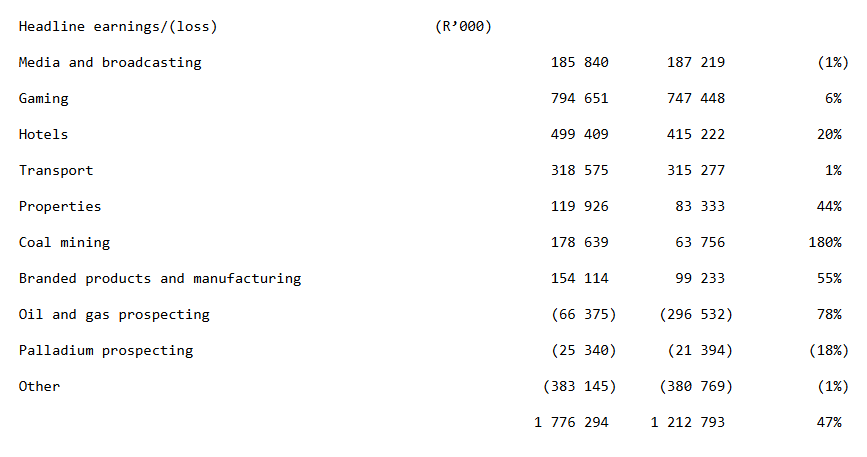

HCI is now selling more coal than toys (JSE: HCI)

This highly diversified portfolio always makes for interesting reading

The broader HCI stable is all over Ghost Bites today. eMedia, Frontier Transport and Tsogo Sun are all part of this family. And as you’ll see in those names, none of them are exactly thrilling growth stories right now. There are others that don’t feature today, like Deneb and Southern Sun.

Despite this, the HCI group story reflects a 50% increase in HEPS and 18% growth in the dividend per share. The thing you’ll notice from this breakdown is that most of the good news stories in HCI’s business won’t be found in the other listed companies at the moment (with the exception of branded products business Deneb):

HCI really is a fascinating group. Their revenue from the sale of toys, electronic games and sports goods is almost as high as their revenue from the sale of coal! Regardless of whether you’re naughty or nice, Santa can get what he needs for you from HCI.

Aside from the exceptional result at the Palesa Colliery (where EBITDA jumped by 128%) and the helpful jump in the property business from conferencing activities, the market will always spend time focusing on the oil and gas business at HCI.

They are still incurring heavy losses in that space, with a separate announcement noting a restructure to separate the Namibian exploration and development business from the South African portfolio. This will improve the chances of attracting other investors and achieving a decent value unlock in years to come.

Ghost Bite: The coal earnings are a welcome boost to the HCI story, particularly as many of the other key exposures are having a tougher time at the moment.

Pepkor is my pick in the clothing sector (JSE: PPH)

Mainly because it’s not just a clothing business

Pepkor is one of the better names in the local clothing sector. They largely stick to their knitting of focusing on value fashion, unlike some of their peers in the sector that love nothing more than to distract everyone with offshore deals.

A core feature of the Pepkor investment case is the fintech business and their banking ambitions in years to come. They layer this onto the value retail business like the icing on a delicious cake.

For the six months to March 2026, revenue growth was 13.2%. Group sales increased by 11.2%, or 5.8% if you exclude acquisitions. The strictest view on performance is like-for-like sales, which increased by 3.6%. The two-year compound annual growth rate (CAGR) in like-for-like sales is an impressive 5.7%.

The only banner in the group that suffered a decline in like-for-like sales was Ackermans, down 0.5% vs. a tough base that saw growth of 9.6%. I appreciate the fact that the management team attributes this to internal issues. It’s certainly refreshing vs. the commentary by Pick n Pay (JSE: PIK) where they blamed their much worse performance in Pick n Pay Clothing on the broader economy.

It’s also worth highlighting the 30.9% growth in online sales. If you think that value retail can’t find success online, you’re very mistaken.

Moving down the income statement, operating profit came in 10.0% higher on a normalised basis. Normalised HEPS grew by 12.1% despite a demanding base of 19.2% growth in the prior period. HEPS as reported is up by 10.3%. Either way, these are decent numbers.

Cash generated from operations increased by 15.1%. This is a very important metric for retailers.

If we dig into the segmentals, we will find significant deviation in the margin trends.

In clothing and general merchandise for example, revenue was up 11.6% and operating profit was up just 3.6%. In furniture, appliances and electronics, revenue was up 14.4% and operating profit increased just 1.0%. Operating profit margin is under pressure in both those areas.

Then we reach financial services, where revenue growth was 41.6%(!) and operating profit was even more impressive, with a jump of 63.4%. The informal market platform also has a great margin story to tell, with revenue growth of 10.4% and operating profit growth of 23.5%.

Is the shape of the group changing? The traditional retail segments contribute a combined 80% in operating profit, with financial services at 11% and the informal market platform at 9%. If the current trend in areas like FoneYam, Flash and Capfin continues, that shape is going to change a lot in years to come.

In the first eight weeks of the new period, like-for-like sales grew 3.7% despite a prior period base of 10.8%. They plan to open a whopping 200 stores over the full year, so Pepkor is expanding into a challenging market.

As a quick note on governance changes, Ian Kirk has been appointed as the lead independent non-executive director.

Ghost Bite: This stock remains my pick in the sector as a long-term play. I think it’s time to pull the trigger based on these results and the share price being down 17% year-to-date.

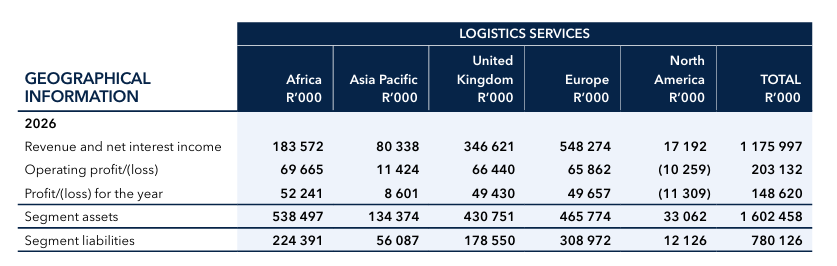

Santova’s results have been impacted by the Seabourne acquisition (JSE: SNV)

Get ready for some odd percentage movements

Santova’s results for the year ended February 2026 have some rather odd headline numbers. Revenue and net interest income jumped by 88.3%, yet HEPS was down 6.4%!

It doesn’t take long to see why: the acquisition of Seabourne has suddenly made the group a lot bigger at revenue level. If you exclude Seabourne, then comparable revenue was down 1.8%.

Due to acquisition costs and other expenses related to the Seabourne deal, the net profit contribution from this deal wasn’t nearly as significant as the increase in revenue. This period isn’t a reflection of the steady-state economics, but Santova has warned that group operating margin will be structurally different in the post-Seabourne era. This is because they’ve acquired a business with lower margin offerings (and the hope of strong revenue growth).

To give you an idea of just how globally diversified this business is, here’s the table with the geographical split:

Ghost Bite: Santova’s share price has been extremely volatile and the market tends to be nervous of smaller companies doing significant deals. Having dropped as low as R6.11, the share price has put in a decent run to R7.85. The 52-week high of R10.50 is still a long way away though.

Stefanutti Stocks has moved past its most speculative era (JSE: SSK)

They now need to focus on delivering their order book

Stefanutti Stocks has been on a charge. The share price is up by a ridiculous 63% year-to-date despite all the market upheaval. The return over 5 years? An hysterical 1,556%!

Welcome to the world of speculative stocks. Those who take a punt on the right ones can make a lot of money. It’s also possible to lose everything. Position sizing is absolutely critical in this space.

In the results for the year ended February 2026, Stefanutti Stocks has shown us how far they’ve come. Although contract revenue from continuing operations was up just 2%, profit from continuing operations tripled due to the recognition of the Kusile Power Plant settlement from Eskom.

The loss in discontinued operations was a lot smaller as well, so HEPS from total operations jumped from 109.36 cents to 359.26 cents. But I must stress that the Kusile amount contributed R492 million of the R620 million in profit from total operations for the period.

Perhaps the biggest achievement during the year was the restructuring of the loan that was due for repayment at the end of June 2026. The company now has a new five-year term facility at JIBAR plus 3.5%. To make shareholders feel even better, the proceeds from the Kusile settlement and recent business disposals were used to reduce the facility from R850 million to just R223 million.

With an order book of R17.2 billion, Stefanutti Stocks now needs to show sustainable growth and an ability to look after the balance sheet going forwards.

Ghost Bite: Stefanutti Stocks has a completely different risk/reward setup vs. what we saw in prior years. Don’t make the mistake of extrapolating the gains that got the share price to this point. Things should be more “normal” from here, at least by the standards of a local company trading at a modest valuation!

Tsogo Sun put in a commendable self-help effort (JSE: TSG)

But I still think it’s a value trap

Tsogo Sun’s results for the year ended March 2026 are about as flat as you’ll ever see in your life. Income, operating costs and adjusted EBITDA were all in line with the previous period. I don’t think I’ve ever seen that before!

Thanks to share buybacks (R438 million) and a reduction in debt (from R7.19 billion to R6.49 billion), this was good enough to drive HEPS growth of 8%.

These numbers were saved by Tsogo’s self-help initiatives across cost control and asset realisations (like the disposal of the City Lodge (JSE: CLH) stake for R215 million).

This isn’t a sustainable way to grow, with the company continuing to struggle with evolving consumer preferences away from in-person gambling towards online platforms instead. Adjusted EBITDA was down by 3% in the casino and hotel precincts.

One of the few growth opportunities in the casino business is to develop a casino in the Helderberg area. They are trying to get it done over the next two years, but a competitor instituting High Court proceedings could delay this.

The limited payout machines business managed growth in both revenue and adjusted EBITDA of 3%. This is impressive under the circumstances.

Tsogo Sun is trying to get a slice of the online action, but it isn’t easy. They’ve at least turned the corner in their online business, with adjusted EBITDA of R50 million vs. a loss of R15 million in the prior year. They are investing in executives who understand this space.

Ghost Bite: This remains in the “too hard” bucket for me. It may be trading on a P/E of roughly 5x, but I don’t see the trend around in-person gambling changing anytime soon.

Zeda is working out well for me (JSE: ZZD)

But they are exposed to the used car market residual values

My stake in Zeda was bought for one major reason: the share price was trading at a ridiculously cheap multiple. I waited for the balance sheet to start to improve and then I got involved. With a total return over three years of 77%, shareholders like me are pretty happy with how this went.

The funny thing is that the company is still at a very low multiple.

In the six months to March 2026, Zeda increased its HEPS by 6.1% to 201 cents. To work out the Price/Earnings (P/E) multiple correctly, we need to work with the last twelve months (or LTM) numbers, something you may have seen before in institutional presentations or on market systems like TIKR.

Zeda’s FY25 HEPS was 361 cents. Their interim 2025 HEPS was 189.7 cents. We can therefore isolate the second half of FY25 with HEPS of 171.3 cents.

Together with the latest interim result, that gives us HEPS on an LTM basis of 372.3 cents. The share price closed at R15.38 after the interim results came out, giving us a P/E of 4.1x.

I figured that this was as good an opportunity as any to just walk you through the way a trailing P/E multiple is calculated with interim numbers. If you simply double the interim number as a quick and dirty approach, then you’re (1) actually calculating a forward multiple instead of a trailing multiple, and (2) ignoring any seasonality in the business.

Digging into the interims now, we find revenue growth of only 3.2% and flat operating profit, with margin down from 15.8% to 15.2%. The earnings growth has therefore been helped by the financial leverage in the business rather than by an exciting underlying result. Finance costs were down 8.2% year-on-year.

The issue lies in the car rental business, where they talk about “challenging residual values” – in other words, the disruption to the automotive sector has also impacted the economics of this business. The pain felt by names like WeBuyCars (JSE: WBC) is being echoed in the car rental players.

Still, Zeda managed a return on equity of 21.2%. They’ve increased their dividend by a significant 45.5% to 80 cents per share, with plenty of dividend cover thanks to HEPS at 201.2 cents.

Ghost Bite: I can think of many reasons why this will be a tough year for Zeda, as confirmed by their outlook statement. I don’t mind riding out some volatility with a management team that is willing to show discipline in areas like dividends to shareholders. With a P/E of 4.1x, there’s a great margin of safety here – and I’ll happily buy more if the share price drops materially this year!

Results of previous poll:

Nibbles:

- Director dealings:

- Piet Mouton and various Mouton family trusts bought shares in PSG Financial Services (JSE: KST) worth a total of R9.6 million.

- iOCO (JSE: IOC) CEO Rhys Summerton bought shares in the company worth R408k.

- The CEO of British American Tobacco (JSE: BTI) reinvested dividend income in shares worth around R165k.

- Brimstone (JSE: BRT) has released a quarterly net asset value (NAV) update. Between December 2025 and March 2026, the intrinsic NAV per share has declined by 4.3%. On a fully diluted basis (which takes into account share options), it’s down by 4.7%. It’s an unfortunate reporting period that was impacted by the developments in Iran towards the end of the quarter. With Brimstone’s biggest exposures being to listed companies, the share price pressure in March has impacted the intrinsic NAV.

- It’s a pity that Africa Bitcoin Corporation (JSE: BAC) released results on such a busy day. I would’ve liked to have had more time to look at them. The Altvest Credit Opportunities Fund (ACOF) is the part that I care about. They are expanding that business into other African countries like Botswana and Namibia, with Uganda and Kenya on the horizon as well. I sincerely want that business to work, as I love the idea of SMEs having access to finance. My concern is that the loss after tax in the year ended February 2026 was R11.6 million, which isn’t much better than the prior year loss of R12.6 million. This is despite AUM jumping from R283 million to R502 million. I would feel much better about the African expansion if they were profitable in South Africa first. But if there’s one thing about this group that is consistent, it’s that they refuse to walk before they run!

- There’s an important update from ASP Isotopes (JSE: ISO) on their journey to commercialisation of enriched Silicon-28. The company is aiming to make initial commercial shipments in Q3 based on previously signed contracts. Importantly, the first 18 stages of the enrichment facility have now successfully operated for over three weeks at the target enrichment levels. The many challenges in getting to this point have included engineering issues with parts from external suppliers. Of course, if it was easy to get this far, the company wouldn’t have a moat! The executive quoted in the SENS is none other than Stefano Merani of Renergen fame. Even a cat would be impressed by how he managed to land on his feet after that colourful journey that eventually led to ASP Isotopes acquiring his company! Let’s hope that ASP Isotopes has considerably better success shipping the promised products than Renergen.

- It seems as though the fight between Novus (JSE: NVS) and the Takeover Regulation Panel is coming to an end. This goes all the way back to a firm intention announcement that was released in 2024! In a settlement agreement with the regulator, Novus has agreed to increase the price in the mandatory offer to Mustek (JSE: MST) shareholders. The new price is R15.41 per share, a long way up from the original R13.00 per share! Shareholder activist Albie Cilliers was one of the intervening parties here. I’ve had my fair share of disagreements with Albie on many things, but he certainly does play an important role in this market in trying to get better prices in deals for a wide range of investors. This is exactly why we have regulators and various legal channels available to market participants.

- Labat Africa (JSE: LAB) has announced another deal. They are acquiring a 20% stake in Mozfinders LDA, a Mozambique-based company that operates in areas as varied as supply chain management and industrial solutions. How on earth does this fit in with Labat’s IT strategy, you ask? It doesn’t. Simple as that. At this stage the Labat team is just throwing money at the wall to see where it sticks. The deal is worth R24 million and will be settled through a combination of R14 million in cash and shares issued at R0.05 per share. The current share price is R0.02. If they want to stop being a penny stock, Labat will need to start doing things that make sense to the market. A minority stake in a Mozambican company isn’t on that list.

- Spear REIT (JSE: SEA) has announced the pricing for the dividend reinvestment alternative. It works out to a 0.65% premium to the 30-day VWAP and a discount of roughly 4.5% to the current spot price.

- Hammerson (JSE: HMN) announced the results of the dividend reinvestment plan offered to shareholders. Holders of 0.8518% on the UK register and 0.09858% on the SA register elected to receive shares in lieu of cash. That’s not exactly an impressive uptake!