In this edition of Ghost Bites:

- 4Sight is getting more and more attention

- Slow and steady at Emira Property Fund

- A surprising margin increase at ISA Holdings

- Reinet is the definition of a fortress balance sheet

- Sygnia had an excellent interim period

- Telkom shareholders are celebrating

4Sight is getting more and more attention (JSE: 4SI)

And for all the right reasons

4Sight Holdings is putting together quite the growth story. For the year ended February 2026, revenue was up by 16.3% and HEPS jumped by 46.1%. That’s good even by global tech company standards!

The bulk of the business lies in Software-as-a-Service (SaaS) offerings, where revenue increased by almost 20% to R645 million. When the management team presents on Unlock the Stock later today, I’ll be asking them about how they are navigating the threat from AI that is hurting the global SaaS sector.

There’s also a healthy consulting business at 4Sight that grew by 12% to R345 million. The rest of the money is made across services like software licences and infrastructure data automation.

Geographically, they make roughly 62% of their revenue in South Africa. 32% is generated in the rest of Africa, with the remaining sliver coming from developed markets.

With HEPS of 10.732 cents for the year, the current share price is a Price/Earnings multiple of 7x. In the context of this exceptional growth rate, that makes 4Sight a very interesting company indeed.

Ghost Bite: It’s always a good sign when a company is willing to invest in an Unlock the Stock session. It means that they want to tell their story to investors. I look forward to learning more about 4Sight!

Slow and steady at Emira Property Fund (JSE: EMI)

Perhaps too slow?

Emira Property Fund’s results for the year ended March 2025 show only modest growth in distributable income per share of 3.7%. The dividend per share increased by 4.1% and the net asset value (NAV) per share was up 1.3%. This means that the company has protected its investors against inflation, but hasn’t done much else.

Emira feels like more of a defensive play, as the company has taken the approach of spreading its risk and looking for through-the-cycle returns vs. trying to extract growth from one particular strategy.

This includes stakes in other listed REITs, like the 6.9% interest in SA Corporate Real Estate (JSE: SAC). When I see stakes like this, I immediately get family office vibes from Emira.

The directly held South African portfolio is where you’ll find the bulk of the local exposure. Emira has 48 properties, although 13 of those properties are large residential plays that have a total of 1,970 underlying units! And you thought your buy-to-let investment was a headache to manage…

The offshore exposure includes six grocery-anchored retail malls in the US, as well as a 45% stake in Poland’s DL Invest Group. These investments represent 24% and 9% of the total portfolio respectively.

The loan-to-value ratio of 30.2% is a significant improvement from the 36.2% we saw in the prior period. This has been assisted by asset disposals across the commercial and residential portfolios.

The targeted distributable income per share for the 2027 financial year is 133.53 cents. That would represent growth of just 3%. If you’re looking for excitement, this is the wrong place to find it.

Ghost Bites: In my next life, I’m coming back as a corporate CEO. The former CEO of Emira was paid a R33.6 million employment termination settlement after resigning in April 2025. The rest of us can only dream.

A surprising margin increase at ISA Holdings (JSE: ISA)

The technology group has highlighted the broader sector challenges

ISA Holdings has released results for the year ended February 2026. With revenue growth of 9% and HEPS up by 10%, this is a solid performance by the company at a difficult time in the sector.

82% of this technology company’s revenue is derived from subscriptions, with particular strength in information security and infrastructure management platforms. As we know, the subscription model is under a lot of pressure right now. The margin on the sale of third-party products is also an issue.

Despite this, ISA has increased gross margin from 48% to 50% thanks to a push into higher margin service offerings.

After a concerning recent trend in DataProof, ISA Holdings sold that business subsequent to the current reporting period. It’s always good to see that kind of discipline.

Investors will want to see a significant improvement in the cash situation in the next period. With debtors up by 39% and cash down by 63%, investors will need to believe management’s assertion that this is merely a timing issue.

Ghost Bite: Nobody really knows what the likes of Claude will mean for a business like this. On a Price/Earnings multiple of 11.5x though, it doesn’t feel like there’s much of a margin of safety in ISA’s valuation.

Reinet is the definition of a fortress balance sheet (JSE: RNI)

A cash pile of over R100 billion is no joke

Reinet is Johann Rupert’s “stay rich” company. This just means that you’ll see a spread of diversified investments with an offshore focus, designed to balance some of the risk you’ll find elsewhere in his portfolio. For those looking to invest alongside Rupert, this offers a very different experience to his other plays like Remgro (JSE: REM) and Richemont (JSE: CFR).

The big question is, what is Reinet planning to do with its mountain of cash? Having previously sold the stake in British American Tobacco (JSE: BTI) and now Pension Insurance Corporation, the company has €5.5 billion on its balance sheet.

Yes, you read that correctly.

Translated to rand, that is a cash balance of over R100 billion!

For context, this means that they could buy a company like Bidvest (JSE: BVT) or Pepkor (JSE: PPH) and still be left with R20 billion to mop up smaller companies on the JSE. Put differently, they could buy both Pepkor and The Foschini Group (JSE: TFG). Rupert and his crew are rich in ways that few people can actually grasp.

For now, they continue to drip capital into various offshore private equity funds. If markets suffer a substantial correction, they are clearly ready to pounce.

Ghost Bite: I doubt that Rupert is going to pay much attention to investors who put pressure on Reinet to go faster and find deals.

Sygnia had an excellent interim period (JSE: SYG)

The products are clearly resonating with investors

Sygnia seems to be having a good time at the moment. The share price is up 25% in the past 12 months and the latest trading statement lends strong support to that move.

For the six months to March 2026, HEPS has increased by between 20% and 25%. We don’t have any other details at this stage, with full results due for release on 8th June.

Ghost Bite: The founder may not be everyone’s cup of tea, but there’s little doubt that Sygnia is a solid business that is successfully riding the wave of passive investing.

Telkom shareholders are celebrating

This is a great trading statement

Telkom closed 12% higher as the market celebrated the trading statement for the year ended March. With HEPS from continuing operations up by between 45% and 55%, what’s not to love?

Well, the trading statement does also remind the market that HEPS in the prior year was impacted by once-off events to the tune of 115.7 cents per share. If we make that adjustment to the base, then the growth this year was between 16% and 24%.

That certainly feels a lot more reasonable. It’s also still very good.

Telkom’s turnaround has been an impressive story. Unlike the other local telcos, they are achieving this growth without chasing it in risky African markets. This is the power of recovering from a low base, with a total return over three years of more than 170%!

Results will be released on 2 June.

Ghost Bite: It’s been a while since I saw any jokes online about how impossible it is to cancel a Telkom contract. That’s probably another bullish sign.

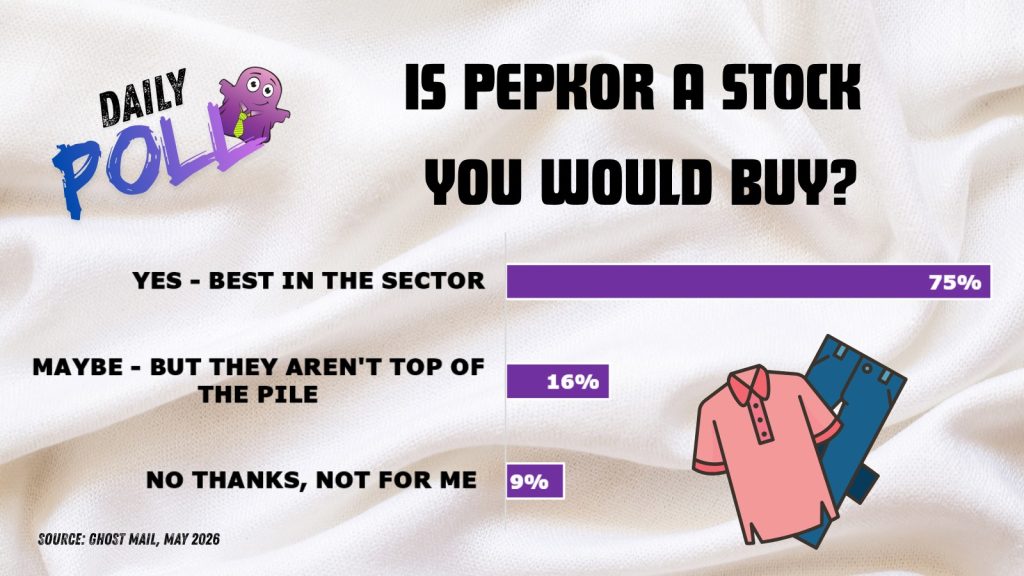

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Africa Bitcoin Corporation (JSE: BAC) and his associates bought ordinary shares in the company worth R96k. He also bought preferred A shares worth R2.6k.

- Brikor (JSE: BIK) is one of the smallest names on the JSE, with a market cap of around R120 million. They may not be on the market for much longer, with the company releasing a cautionary announcement related to a potential scheme of arrangement and delisting of the company. It really doesn’t make sense for companies like this to be listed.

- Zeder (JSE: ZED) is busy with the disposal of Zaad. They’ve met a number of conditions precedent already, but they still need competition authority approval from a few African regulators. The timing of these things is always a lottery.

- Afine Investments (JSE: ANI) has very little liquidity in its stock. This company has a portfolio of petrol stations with an asset value of R449.8 million. It’s a pity that the shares are almost impossible to buy in the market, as the results for the year ended February 2026 reflect a 39.9% increase in distributable earnings! A 34.5% increase in the final dividend means that the total dividend for the year increased by 22.7%.

- Like the JSE, I was also on the receiving end of Mantengu’s (JSE: MTU) accusations and incredibly flimsy “evidence”. I can therefore understand why the JSE has taken action to censure the company based on the announcements it made to the market in 2025. The entire market was thrown into disrepute, with Mantengu accusing many people of share price manipulation. None of these allegations have been proven. According to the JSE, even the company’s designated advisor wanted to retract the announcements, yet the company insisted that they stay out. Given the lack of underlying evidence and what that means for the integrity of SENS, the JSE has publicly censured Mantengu and fined the company R100k. The fine is suspended for three years provided that the company doesn’t breach the Listings Requirements again.

Lewis – what a company. 5 PE , 10% dividend yield. Never lets you down.

Sick!!