In this edition of Ghost Bites:

- The Foschini Group hasn’t stabilised yet

- Mr Price enjoyed a partial share price recovery

PS: I’ve launched my YouTube channel! Check it out here and please consider subscribing.

The Foschini Group hasn’t stabilised yet (JSE: TFG)

Negative operating leverage continues to plague shareholders

The Foschini Group is in a tough spot. Shareholders don’t get the warm and fuzzies when they read things like “trading conditions deteriorated across all operating regions” and see references to negative operating leverage.

Group sales may have been up by 7.1% for the year ended March 2026, but the acquisition of White Stuff is heavily skewing this metric. The underlying reality is that group sales were up just 2.8% excluding that acquisition. Combined with a substantial gross margin contraction of 120 basis points, profitability never stood a chance.

HEPS is down 33.5% and the final dividend is down 39.1%. It’s not difficult to see why the share price is down 56% in the past 12 months.

The business in South Africa isn’t the worst of the issues, as TFG managed to increase market share in key areas like womenswear (up 50 basis points).

But even in the home market, there’s a worrying trend underneath the sales growth for the year of 5.0% (like-for-like up 3.5%). H1 growth was 5.3%, while H2 was only 4.7%. The only category that accelerated in H2 vs. H1 was jewellery, which contributes just 3.7% of TFG Africa’s sales. Weak momentum into the end of a period always spooks the market.

The Bash platform remains the bright spot, with online sales up 49.2%. Most importantly, they are achieving a structurally equivalent gross margin to the bricks-and-mortar business. Such is the growth differential that online sales reached 10% of group sales in the fourth quarter of the year.

Given the current state of play in the broader TFG financials, the capex-light nature of Bash makes it a highly attractive growth engine.

It’s also worth noting that credit sales growth of 4.6% was conservative vs. total growth. Credit sales contributed 25.8% to TFG Africa sales.

The much bigger issue in TFG Africa lies one level down in the gross margin. A contraction of 100 basis points to 41.6% isn’t what investors want to see in TFG’s core market.

The pain in gross margin means that TFG Africa didn’t get anywhere near covering the percentage increase in operating expenses. The resultant negative operating leverage took segmental EBIT down by 14.7%!

This all looks like a picnic in the sunshine compared to TFG London. Sales excluding White Stuff were flat for the year in local currency. White Stuff itself achieved growth of 4.3%, so the recent acquisition is doing better than the rest of the business. But that clearly isn’t saying much.

In an inflationary environment, flat sales can only end in tears. Sure enough, TFG London’s segmental EBIT fell by a nasty 65.4% (excluding the impact of White Stuff). That’s a proper mess.

TFG Australia is also quite the horror show. Sales were down 1.5% for the year and 3.4% on a like-for-like basis (both in local currency). The momentum tells an even uglier story, as the H1 sales decline of 0.5% worsened to an H2 decline of 2.4%. As you’ve probably guessed by now, segmental EBIT at TFG Australia also headed firmly in the wrong direction, down by 27.2%.

Early trading activity for the new financial year doesn’t look much better. Sales in TFG Africa were up by just 2.2% for the 9 weeks to 30 May 2026. TFG London was up 1.7% and TFG Australia fell by 2.3%, both in local currency.

Gross margin is up by 80 basis points in TFG Africa, 130 basis points in TFG London and 100 basis points in TFG Australia. Talk about small mercies.

Net debt to EBITDA has increased from 0.99x to 1.44x, driven by a small increase in net debt and a sharp drop in EBITDA. Return on capital employed has dropped from 14.8% to 10.9%. Things need to turn the corner – and quickly.

Ghost Bite: The Foschini Group is facing a crisis, evidenced by the interventions ranging from headcount reductions through to capex decreases and tighter lending books. They are talking about optimising the store footprint and reviewing marginal brands. In summary, they need to stabilise before they can possibly hope to grow again.

Mr Price enjoyed a partial share price recovery (JSE: MRP)

There’s still a long way to go to the pre-NKD share price

Mr Price closed 15% higher on Friday after releasing results for the 52 weeks to 28 March 2026. This doesn’t repair the damage of the NKD transaction, but it does take them to a flat year-to-date performance:

The costs related to the NKD transaction (R217 million) significantly impacted the period. HEPS as reported was up by just 2.1% for the year. Mr Price’s normalised view of HEPS (which strips out the once-off costs) reflects HEPS growth of 7.7%.

Retail sales growth of 4.3% was slightly ahead of the broader sector. But with weighted average space growth of 3.6%, there’s very little underlying organic growth to feel good about. Comparable store sales growth was just 1.1%, with group volumes up 0.5%.

To be fair, the second half of the year was up against a very tough base period with high growth. Despite this, they managed 3.3% revenue growth in H2. I believe that this would’ve been one of the catalysts for the positive share price move.

The other major highlight was in gross margin, which expanded by 70 basis points to 41.2%. That’s an impressive outcome in a difficult market, with a highlight being Mr Price Sport’s margin expansion of 110 basis points.

The group generated a 42.0% margin on merchandise and only 20.7% on telecoms, so keep an eye on the mix effect on gross margin. There’s a structural gap in the economics of these different categories.

Although there was pressure on operating costs (particularly occupancy costs and utilities), Mr Price still managed to increase normalised margin by 50 basis points to 14.7%. Normalised operating profit growth was 8%.

The group story is thus one of surprising H2 sales growth, accompanied by margin expansion in the numbers that suggests a strong foundation in the local business. This is, after all, why I bought shares in Mr Price in the first place (before the NKD madness).

Mr Price remains well off the pace from an online perspective, with online sales growth of just 4.9% (only slightly ahead of in-store growth of 4.4%). They seem unbothered by the omnichannel opportunity, despite 55% of online orders being collected in store.

An exception to this approach is Yuppiechef, which started life an an online store and then went the omnichannel route. This has been a helpful growth engine for Mr Price, with double-digit sales growth and an expanded footprint of 25 stores.

Another useful growth engine is telecoms, now up to 86 standalone stores alongside the 482 store-in-store concepts. Gross margin in this segment may be dilutive vs. the rest of the group, but it’s a great underpin that builds some resilience into the model.

The focus on cash sales remains, up 4.4% and contributing 89.4% of group sales. Credit sales increased by just 3.5%.

In terms of outlook, the group acknowledges that the introduction of debt for the NKD deal has taken them to a place where they need to focus on the balance sheet. The FY27 capex expectation is R1.1 billion in South Africa, which would be roughly in line with FY26. This will be accompanied by €24 million in Europe as NKD expands.

NKD was included in the group from 31 March 2026, so the next set of numbers will include the European acquisition that broke the trust between management and the market.

Ghost Bite: Given the market response to these numbers, a small amount of that trust might be coming back. The real test is whether some positive momentum will stick.

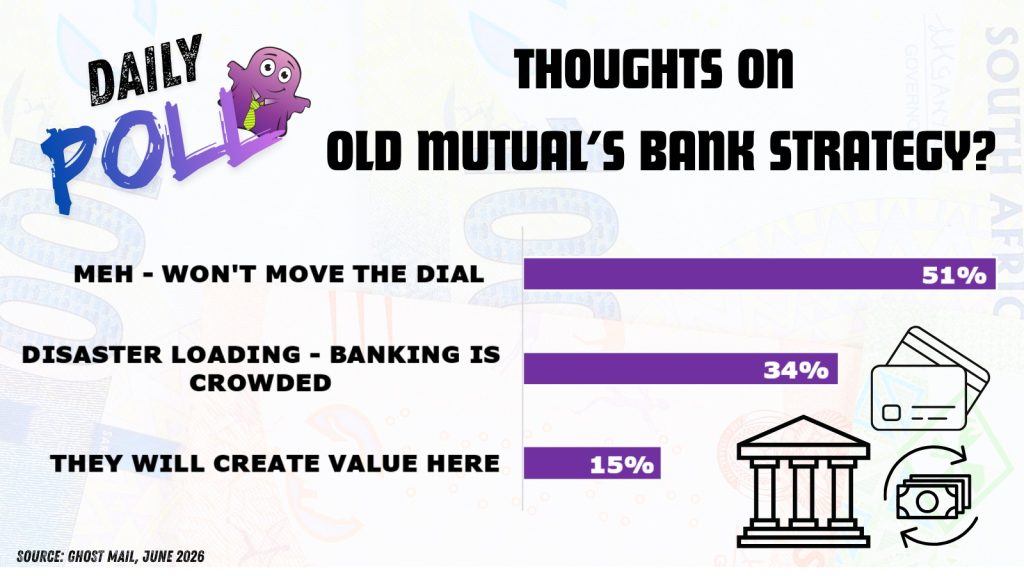

Results of previous poll:

Nibbles:

- Director dealings:

- A director of MTN (JSE: MTN) sold shares worth over R19 million. That’s a substantial disposal.

- The CEO of British American Tobacco (JSE: BTI) bought shares worth around R4.7 million.

- A director of AVI (JSE: AVI) received shares awards, and sold the whole lot worth R4.7 million.

- Aside from a restructure of shares from his personal name into that of an associated entity, the CEO of Pan African Resources (JSE: PAN) also entered into a long CFD contract over shares worth nearly R2.5 million.

- Des de Beer has bought another R1.4 million worth of shares in Lighthouse Properties (JSE: LTE). If history repeats itself, you’ll soon see why I mention de Beer by name here. Chances are, he’ll be buying a lot of shares…

- A director of PSG Financial Services (JSE: KST) bought shares worth R439k. For whatever reason, there were identically-sized purchases of shares by three other directors of major subsidiaries, all at an identical price. Odd.

- The family trust of a director of CMH (JSE: CMH) bought shares worth R95.4k,

- Novus (JSE: NVS) has acquired a further R16.3 million worth of shares in Mustek (JSE: MST). This takes them from a direct stake of 39.96% to 41.85%. Together with concert parties, they now hold 62.14% in Mustek.

- Hudaco (JSE: HDC) announced a small related party deal in which an operating subsidiary (Ambro Steel) has renewed its lease of a building that is 82% owned by the CEO of Hudaco. Ambro Steel has been in these premises since before Hudaco acquired the company in 2008. To protect shareholders from the obvious conflict of interest, the independent directors considered the terms of the lease renewal without the influence of the CEO in the process.