In this edition of Ghost Bites:

- ASP Isotopes wants to list the helium assets separately on the Nasdaq

- CA Sales executes another bolt-on acquisition

- Hyprop proves that destination shopping can take the fight to eCommerce

- Mantengu is very unhappy with its auditors

- Sappi releases the circular for the European joint venture

- Sirius Real Estate recycles capital in the UK

ASP Isotopes wants to list the helium assets separately on the Nasdaq (JSE: ISO)

The Virginia helium assets seem to have a bright future

ASP Isotopes recently gave the market some good news about the commercialisation of Renergen’s helium assets. There’s a much bigger update now, with the group looking to combine Renergen with ENDRA Life Sciences and then list the newly merged entity on the Nasdaq.

The name will be Noble Africa, which is the name of the subsidiary through which ASP Isotopes holds the Renergen investment. I suspect that the Renergen name will stop being used entirely once this deal is done.

ENDRA is already listed on the Nasdaq. They operate in cutting-edge imaging for early detection and monitoring of steatotic liver disease.

What does this have to do with helium, you ask?

I think they are bringing the route-to-market skills in the medical sector closer to the helium business, as they are reaching the point where the South African helium assets need to find global customers. There’s no shortage of smart people at ASP Isotopes, that much I can tell you.

Noble Africa will receive roughly $50 million in capital to make this happen, including $20 million from ASP Isotopes and a further $750k from directors of ASP Isotopes.

ASP Isotopes is expected to own 89% of the combined company. Current ENDRA shareholders would have just 3%, while the rest will go to the providers of fresh capital.

Ghost Bite: This is another great example of how important it is to hitch your trailer to the right horse. I cannot imagine how Renergen would’ve gotten this far without the ASP Isotopes deal. If anything, that structure was headed for financial failure instead!

CA Sales executes another bolt-on acquisition (JSE: CAA)

They aren’t wasting any time in their new digital strategy

They’ve been busy at CA Sales Holdings (or CA&S) recently!

After announcing a deal for 30% in The Digital Media Consultancy (TDMC), CA&S sent a message to the market that they will be stepping into the eCommerce arena. This is an important move for the business, as omnichannel retail is all the rage.

They’ve now announced a second transaction that adds to this platform strategy.

They are acquiring a 51% stake in Pantry Club, an FMCG platform business that manages bespoke online purchasing platforms and marketplaces. They have the ability to increase this stake by a further 9% in future.

Ghost Bite: The deal is too small for any financial details to be announced, but I think investors will appreciate the underlying strategic move.

Hyprop proves that destination shopping can take the fight to eCommerce (JSE: HYP)

This is a strong performance

In a pre-close update dealing with the five months to May 2026, Hyprop delivered good news to investors. They are on track to deliver growth in distributable income per share for the year ending June 2026 of between 10% and 12%. This is in line with the guidance provided in September 2025.

In the South African portfolio, the retail centres saw a 5.5% increase in tenant turnover, with trading density up by 4.4%. Footcount was up 2.1%, so they are holding their own against eCommerce adoption.

A particularly exciting metric is positive reversions of 9.8%, with vacancies at low levels and tenant demand clearly coming through.

My gut feel is that malls either need to offer genuine destination shopping experiences (like Canal Walk with its lifestyle and entertainment offerings), or they need to be on busy commuter routes. There’s a half-pregnant strategy in the middle that I don’t believe will do well in years to come. Hyprop sits on the destination shopping end of that spectrum, and they are executing well on that strategy.

In Eastern Europe, tenant turnover was up 4.4% and trading density increased 4.2%. Footcount was up 5.0%. Here’s the real winner though: the vacancy rate is 0%! Talk about demand for space.

Naturally, with demand like that, reversions were in the green (positive 3.4%).

To add to the strong underlying performance, the cost of borrowing has come down in South Africa (from 8.6% to 8.5%) and Europe (from 4.0% to 3.9%). It may not sound like much, but every bit helps.

Ghost Bite: My Hyprop position is now up 78% since I bought it a couple of years ago. I’ll take that with a smile.

Mantengu is very unhappy with its auditors (JSE: MTU)

Read the full announcement and decide for yourself

Mantengu has released results for the year ended February 2026. As you’ll soon see, the audited numbers look different to how management would tell the financial story.

I can’t recall having ever seen an announcement in which management so openly disagrees with the approach of the auditors. I’m not sure how they think this builds trust with investors, particularly after all the recent bad press around being censured by the JSE. But more on that later.

First, we deal with the audited numbers and a headline loss per share of 90 cents, which is much worse than the headline loss per share of 23 cents in FY25. The net asset value has plummeted from 178 cents to 71 cents.

The Sublime Technologies business, which was the source of their bargain purchase gain in a previous financial year, contributed R168 million of the R315 million loss. This is because the business cannot operate without a special tariff deal from Eskom, an issue that has been plaguing operators of furnaces across the country (including in the ferrochrome space where there is now some relief for that industry).

Perhaps the sellers of the business knew this when they walked away for a “bargain” price? It’s not certain how things will turn out with Eskom, but the risk was surely always there.

We then arrive at the chrome business, which contributed R115 million of the loss. According to management, the Langpan business has been the victim of sabotage. The group cannot give more details on this due to legal process. They’ve also had to put in place new offtake agreements on better commercial terms. Things will hopefully improve significantly now.

Blue Ridge lost R26 million due to ongoing monthly expenses before the asset could produce any income. They are now in negotiations to sell the asset for R50 million.

Those are the numbers according to the auditors, at least. We now reach the number of ways in which management disagrees with them, ranging from the treatment of a liability in Blue Ridge Platinum through to the audit approach to inventory balances.

I can only suggest that you read the full announcement and then arrive at your own conclusion. It’s so detailed and complicated that I’m not even going to attempt to summarise it here.

As for my opinion on this, Mantengu is either the unluckiest company in history, or there are issues there. It’s incredible that so many things can happen to just one company.

It takes a lot of consistent work to create trust in the market. Sadly, having had a front-row seat to the “evidence” they used to try and implicate me in their broader fight with the JSE, I now find it harder to put much faith in their claims.

It’s possible for auditors to get things wrong of course. It’s also common for IFRS-compliant accounting to spit out results that are far removed from commercial reality. But it’s also reasonable to think that a management team having a public disagreement with the auditors (including calling their work “derelict”) is something that probably only ends well if the management team has a sparkling reputation.

I strongly suggest that you read the announcement and form your own view.

Ghost Bite: Nothing would send a positive message to the market quite like director purchases of shares, especially with the share price down 41% year-to-date. Money talks the loudest.

Sappi releases the circular for the European joint venture (JSE: SAP)

Can scale solve the problems in this business?

Sappi has released the circular for the 50/50 joint venture for graphic paper in Europe with UPM. The deal carries total advisory fees of $32 million, so it’s a monster of a thing.

Advisors are the only people who have done well out of Sappi recently. The share price is down 60% year-to-date, a spectacular drop driven by the combination of a weak balance sheet and a horrible point in the cycle.

This graphic paper joint venture certainly won’t solve all of Sappi’s problems, but at least it creates more scale in Europe and gives that business a better chance.

The joint venture helps with capacity utilisation, as the core graphic paper industry is in structural decline thanks to global digitalisation. Put simply: printing magazines isn’t a good business to be in.

They anticipate at least €100 million in synergies per annum, a suspiciously round number if ever I’ve seen one. It will be interesting to see how close they actually get.

From UPM’s side, they are contributing the communication papers business. Essentially, this joint venture is the combination of two businesses that are facing considerable headwinds.

Will scale save the day? Only time will tell.

And of course, it just wouldn’t be a deal in Europe if one of the four key benefits provided in the circular wasn’t related to climate impact!

Ghost Bite: If you want to see what a proper M&A circular looks like, then check it out here.

Sirius Real Estate recycles capital in the UK (JSE: SRE)

This is exactly how their business model works

Sirius Real Estate has a strong reputation for active management of its portfolio. The latest activity in the UK is a perfect example, with the fund selling two non-core UK assets and acquiring three UK-based self-storage opportunities.

The sales are for a total of £5.3 million, which is a 3% premium to book value. They are stable properties that have limited upside opportunity from here, making them less suitable for Sirius’ strategy.

On the acquisition side, they are looking to develop three self-storage opportunities with total site acquisition costs of £12.6 million. The gap between the current disposals and this acquisition cost will be covered by other planned disposals of non-core assets later this year.

Two of the development assets are expected to open in 2027, with the third expected in 2028.

The expected internal rate of return (IRR) is in the double digits, well in excess of Sirius’ cost of capital (especially in hard currency).

Ghost Bite: Selling mature assets and taking on development / redevelopment / active opportunities is exactly what Sirius does. Much of their recent activity has been in defence-focused assets in Germany, but that’s certainly not all that they do.

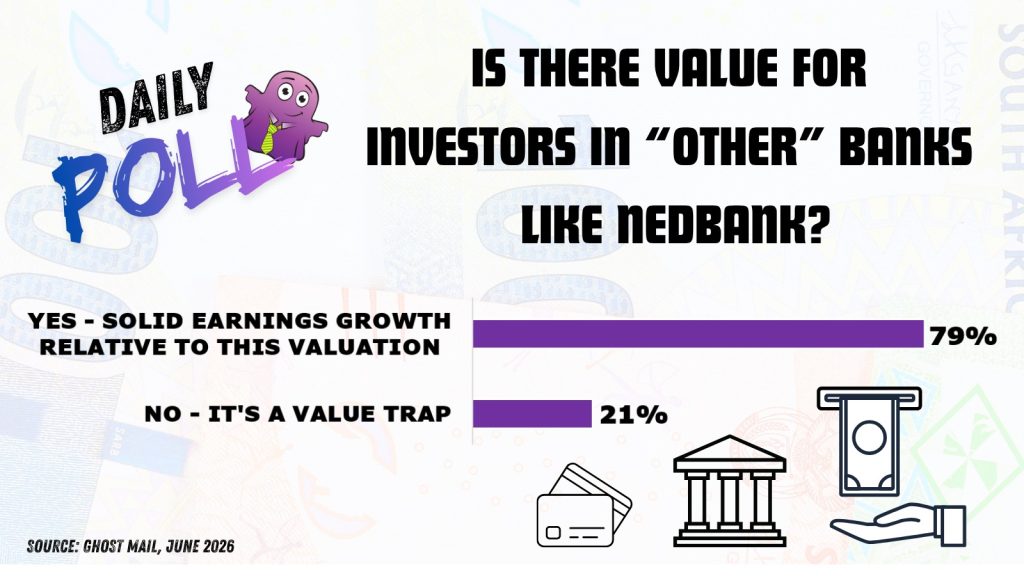

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Pan African Resources (JSE: PAN) refinanced a collar structure over 500,000 shares (R11 million at spot price). These shares are pledged as security for a loan of R11.86 million. The put option strike price is R23.72 and the call option is priced at R33.61 per share. The spot price is R21.91. The loan redemption date is 30 November 2027.

- Two founding directors of Brimstone (JSE: BRT | JSE: BRN) bought shares worth a total of R9.3 million.

- The CEO of Lewis (JSE: LEW) sold shares worth R4.7 million. They describe this as part of rebalancing his portfolio, but a sale is a sale regardless of the reason.

- A prescribed officer has bought shares in Exxaro (JSE: EXX) worth R992k.

- A director of Mr Price (JSE: MRP) bought shares worth around R700k.

- Tharisa (JSE: THA) announced that Nedbank has provided a revolving facility of R750 million to support the company’s transition to underground mining. There’s an accordion that allows Tharisa to take it up to R1.25 billion on the same Ts & Cs as the initial R750 million. This specific facility is for the underground fleet, so this is actually an asset finance deal – just a much bigger one than you might have for your car! Tharisa has also raised significant debt raised from other banks and funding providers for the broader underground strategy. They are using this favourable point in the PGM cycle to invest for its future.

- Sebata Holdings (JSE: SEB) released a trading statement for the six months to September 2025. Yes, they are still behind on their financial reporting! HEPS is expected to be between 3.24 cents and 3.27 cents, a significant swing from the loss of 0.13 cents in the prior period.

- In case you’re following WBHO (JSE: WBO) closely, shareholders have approved the resolutions for the B-BBEE transaction with Akani.