In this edition of Ghost Bites:

- Absa’s Africa Regions segment is struggling with interest margin

- Institutional investors were happy to throw money at Fortress Real Estate

- Gemfields is being severely hurt by its ruby business

- Harmony achieved production guidance in gold and copper

- Hudaco had a poor interim period

- PBT Holdings bucks the trend in consulting

- Sun International’s recent growth is in line with guidance

- Métier did the heavy lifting at Sephaku

- Resilient REIT lives up to its name

- Thungela was boosted by Transnet Freight Rail in this period

Absa’s Africa Regions segment is struggling with interest margin (JSE: ABG)

The credit loss ratio has helped, but watch that growth in expenses

Absa released a trading update for the six months to June 2026. We’ve now received updates from each of the four large legacy names in banking.

Absa managed low- to mid-single digit growth in revenue, with non-interest revenue (NIR) growing faster than net interest income (NII). That shape is what we are seeing across the sector, as NIR has been a focus area for banks due to its positive impact on Return on Equity (ROE).

The low-single digit growth in NII is a function of margin compression, with rates having come down in key African countries. Loans and deposits grew by mid-single digits.

On the NIR side, insurance and fee income in South Africa did well. Trading income had a strong first quarter and then slowed down, which is a bit of a surprise given the level of volatility we saw in the second quarter.

With operating expenses up by low- to mid-single digits, Absa’s cost-to-income ratio has moved the wrong way. This isn’t encouraging for margins, or for the value that investors are willing to put on Absa’s shares.

The credit loss ratio saved the day here, with flat impairments and thus an improved ratio. This transforms the weak performance in pre-provision operating profit into growth in headline earnings of mid- to high-single digits. It also means that ROE will be similar to the comparable period at 14.8%.

ROE for the full year is expected to be 15%, which is below the company’s expectations due to margin compression in Africa. The strong rand is also not helping their case when earnings are translated from African subsidiaries.

Ghost Bite: Absa is now underperforming Nedbank in 2026. The market wants to see expense growth below income growth, as the credit loss ratio isn’t a high quality way to achieve decent earnings growth. Nedbank has a tighter grip on expenses than Absa at the moment.

Institutional investors were happy to throw money at Fortress Real Estate (JSE: FFB)

And indeed, why not?

As expected, Fortress Real Estate had no trouble raising capital from the market. They initially planned to issue 52 million new shares. Thanks to the level of demand from institutional players, they upsized this to over 55.6 million shares.

Importantly, this was achieved at a discount of only 1% to the 30-day VWAP, so I can see why they happily increased the raise.

To give more context, this raise has increased the number of shares in issue by 4.5%. Fortress has raised R1.35 billion through this process, so that will give them more flexibility in the acquisition and development pipeline.

Ghost Bite: This is exactly why property funds enjoy being listed on the JSE. Being able to raise this kind of money overnight is genuinely incredible when you think about it.

Gemfields is being severely hurt by its ruby business (JSE: GML)

The CEO is out

Gemfields has been through an extremely tough period and things don’t seem to be getting any better.

The company is now parting ways with CEO Sean Gilbertson by mutual agreement. This is usually just a nice way of saying that they want to give someone else a try, with money changing hands to make that happen quickly. David Lovett is stepping up from CFO to interim CEO, having served as CFO for 8 years. Will that promotion stick? Time will tell.

This news accompanied ruby auction results that reflect total revenues of $23.1 million. This auction was in a new format that sits between mixed-quality auctions and the mini-auctions introduced in 2025. This is part of why auctions simply aren’t comparable, as the quality varies and so will the price per carat.

They sold 92.1% of lots offered for sale, which seems like a reasonable outcome.

The broader issues in the ruby business are a significant worry, with grades declining at MRM. The more favourable areas of the mine have been hard to access due to higher rainfall. There are also commissioning issues at the second processing plant.

Overall, these production issues are expected to have a “material adverse impact” on ruby auctions for the rest of the year. This was probably the final straw for the CEO, leading to his replacement.

To make things even worse for the ruby mine in Mozambique, there has been conflict at villages just 15 – 35km away from the mine. They also have a major problem with illegal mining. And as the icing on this terrible cake, they are owed $28.3 million in VAT refunds that aren’t coming through.

Ghost Bite: Mozambique is just a terrible place to do business. It’s as simple as that.

Harmony achieved production guidance in gold and copper (JSE: HAR)

Management is successfully controlling the controllables

Harmony Gold has met its gold production guidance for the 11th consecutive year. For a mining company, that kind of predictability is valuable in the market.

In a trading update for the year ended June 2026, the company also confirmed that they would meet guidance for their all-in sustaining cost in gold. Notably, capital expenditure has come in slightly below plan.

On the copper side, production is towards the upper end of guidance. This helped cash costs come in below guidance. This is the commodity that everybody is talking about of course, with Harmony investing heavily in copper.

The Eva Copper project in Australia is the asset of focus, with the project making considerable progress. There are some environmental hiccups though, with a protected species identified within the project area. They’ve been able to reprioritise workstreams for now, but this might end up causing delays.

Overall, it’s been a solid year of execution at Harmony. Management teams can’t control commodity prices, but they can control how successfully they mine those commodities.

Ghost Bite: Harmony’s share price is almost perfectly flat over 12 months. Commodity price volatility can make the mining sector a cruel place.

Hudaco had a poor interim period (JSE: HDC)

They are taking decisive action with two of their businesses

Hudaco released a trading statement dealing with the six months to May 2026. It’s not good news I’m afraid, with HEPS expected to fall by between 32% and 34%.

The company also reports comparable earnings per share, which strips out discontinued operations and fair value adjustments on vendor liabilities. In that case, earnings would be between 12% and 13% higher.

This tells you that the discontinued operations are a problem, with the announcement giving details on the two businesses that have now been classified as such.

The first is the alternative energy business, which has lost a tremendous amount of value since load shedding disappeared. That sector has become one big price war, leading to unattractive economics for Hudaco. They’ve recognised a R125 million impairment on their inventory. If you want energy backups, it sounds like Hudaco will sell you their products at clearance prices!

The second discontinued operation is the battery bay management and service business within Eternity Technologies. This is a low-margin business that provides products for forklifts, reminding us just how specialised things can get in the industrial sector. This is a particularly sad one, as 90% of the 245 staff members are being retrenched. Management blames the market entry of former staff members who had the support of a key supplier. Such is life in business.

Ghost Bite: This announcement came out after market close, so you can expect some fireworks in the Hudaco share price on Tuesday.

PBT Holdings bucks the trend in consulting (JSE: PBT)

These are good numbers

PBT Holdings released results for the year ended March 2026. The consultancy group put in a solid performance, with revenue up 6.0% and operating profit up 8.3%.

This looks like a solid top-line performance at a time in the world when tough questions are being asked about consulting business models. The group’s efficiency initiatives decreased operating expenses by 9.9%, driving strong improvements to margins alongside the revenue growth.

HEPS was especially impressive with 17.6% growth, but the group also reports normalised HEPS (a safer metric) with 10.8% growth.

The only blemish was cash generated from operations, which dipped by 6.6%. Operating cash can experience these swings based on the exact timing of working capital movements.

The total dividend for the year was up 8.1%.

Ghost Bite: This has been a solid stock over the past 12 months, with a total return of 22% thanks to the high dividend yield.

Sun International’s recent growth is in line with guidance (JSE: SUI)

That’s a good outcome, given the broader disruptions in the world

Sun International hosted a Capital Markets Day in March this year, so the company has nailed its colours to the mast in terms of growth targets and strategy. I always appreciate this, as it allows the market to accurately measure the performance of management.

With interim results due in September, Sun International has provided a brief update on trading performance for the six months to June 2026. Revenue is the only metric covered at this stage, with growth of 6% being in line with guidance.

They’ve also been repurchasing shares, having picked up 2% of issued share capital in the market at an average price of R50.08 per share. The current price is R54, up nearly 40% year-to-date!

Ghost Bite: The casino business has been having a tough time, but there’s more to Sun International than just the traditional casinos. The resorts etc. seem to have done well despite all the disruptions to travel costs from the Middle East conflict.

Métier did the heavy lifting at Sephaku (JSE: SEP)

It’s nice to see the South African operations on the up

Sephaku Holdings reported results for the year ended March 2026.

The financials can be complicated to interpret, as SepCem is accounted for as an associate. In simple terms, this means that Sepcem’s results are brought in as a single line on the income statement, with the detailed line-by-line numbers reflecting Métier as the 100%-owned subsidiary. In other words, if you look at group revenue for example, all you’re actually seeing is Métier.

Group HEPS increased by 20.3% to 37.91 cents. This was firmly thanks to Métier, where net profit after tax increased from R76 million to R107 million as EBITDA margin expanded. SepCem was a drag on performance, with profit down from R43 million to R25 million.

Ghost Bite: The share price has tracked earnings growth, with an increase of 23% over the past 12 months.

Resilient REIT lives up to its name (JSE: RES)

They still expect 9% growth in FY26

Resilient REIT has provided a pre-close update for the six months to June 2026.

In South Africa, retail sales were up by 3.3% for the five months ended May 2026. That’s lighter than we’ve seen at competing funds in South Africa, but Resilient has been busy with major development initiatives at six of its shopping centres. In that context, this is a decent performance.

Reversions were positive 3.2% in South Africa, with escalations agreed at 5.2%. This is the kind of inflation protection that investors are looking for.

In Europe, retail sales at the Spanish property increased by 5.1% for the five months to May. The French portfolio grew 5.0%, a solid performance that is well ahead of the macroeconomic story in the country.

Overall, guidance of at least 9% growth in the distribution for FY26 has been reaffirmed. Shareholders won’t complain about that.

Ghost Bite: The REIT sector is delivering solid growth at the moment, particularly where funds are invested in retail portfolios.

Thungela was boosted by Transnet Freight Rail in this period (JSE: TGA)

No, you didn’t just hallucinate that sentence

Thungela released a pre-close update dealing with the six months to June 2026. During the period, coal prices moved largely in line with the shape of oil and gas prices. In other words, prices rose in response to the Middle East conflict and then moderated.

The Richards Bay benchmark price has lagged the Newcastle benchmark price though, mainly due to weaker buying by Indian customers over the period. An interesting feature of the coal market is that the price will vary depending on where you are shipping from and who the end customers are.

With 6.3Mt of production in South Africa vs. only 2.0Mt at Ensham in Australia, the Richards Bay price is more important to Thungela. It’s a pity that it lagged, but realised prices were still 12% higher (in USD) than the comparable interim period. Alas, thanks to exchange rate movements, the rand price per tonne has actually been identical to the comparable interim period!

This leaves them reliant on export saleable production volumes in South Africa, expected to be slightly down at 6.3Mt vs. 6.4Mt in the comparable interim period. This puts the FOB cost per export tonne slightly above the guided range, as muted production volumes will always lead to higher costs per unit. They expect this to improve in the second half.

There’s one more very important factor: the performance of Transnet Freight Rail. Producing the stuff is one thing, but getting it to the ports is quite another. Thankfully, improvements in rail performance helped Thungela achieve an increase in export sales from 6.6Mt to 7.5Mt.

How lovely is it to read about Transnet actually helping the sector?

At Ensham, export saleable production jumped from 1.6Mt to 2.0Mt. Costs per tonne have come in lower than guidance. Although full-year guidance has been maintained on both production and costs, it’s clearly a strong start to the year in Australia.

On the capital expenditure side, South Africa is expected to be at R600 million for the interim period (R500 million sustaining and R100 million expansionary). Ensham needed R250 million in sustaining capital expenditure during this period. Full year guidance has been affirmed for capex for both countries.

Ghost Bite: The market didn’t love this update, with Thungela down 7.5% on the day. This takes the total return over 12 months to only 11%. Cyclical stocks are tough. I’m just happy to see that Transnet was a positive contributor in this period!

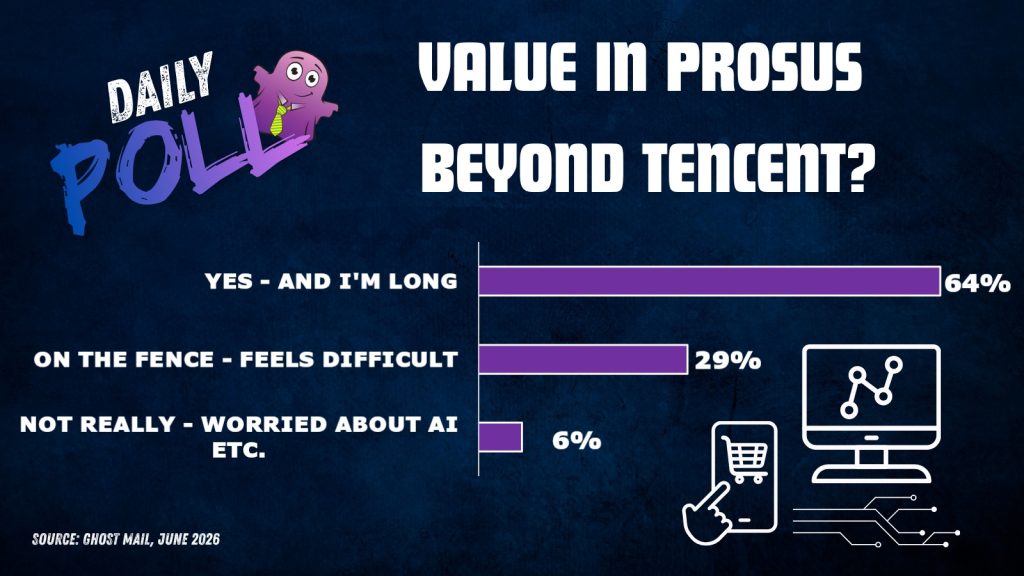

Results of previous poll:

Nibbles:

- Director dealings:

- One of the founding directors of Discovery (JSE: DSY), Barry Swartzberg, entered into a hedge over R92.5 million worth of shares. This takes the form of a put option with a strike price of R171.23. The current price is R264 per share. There’s no call option, so this is purely downside risk protection. Separately, Adrian Gore had to sell shares worth around R62 million as his hedge matured and call options were triggered. Like Swartzberg, Gore has now entered into a structure that only has downside protection (in his case, at R199.76 per share). Gore’s new hedge is over shares worth around R200 million.

- A director of Richemont (JSE: CFR) sold share awards worth R41 million. The announcements never even tell you the name of the director, let alone whether this is only the taxable portion or not.

- A director of Sibanye-Stillwater (JSE: SSW) bought shares worth R7.4 million.

- Here’s a nice bullish sign for a stock that has been under pressure: a director of Clicks (JSE: CLS) bought shares worth just under R3 million.

- A director of Trematon (JSE: TMT) bought shares worth R104k. A different director of the company sold shares worth R135k.

- With the Afrimat (JSE: AFT) share price in the toilet, it’s not helpful that a director has flushed some of his shares away. It might only be a sale worth R81k, but I would far prefer seeing insider buying rather than selling.

- Vodacom (JSE: VOD) has deepened its exposure to Africa. At the end of 2025, they announced that they wanted to acquire a further 20% in Safaricom in Kenya. It’s taken around six months to get the deal done, with all conditions having now been met. This has allowed Vodacom to acquire 15% in Safaricom from the Government of Kenya and 5% from Vodafone International. The company expects to update the market on medium-term targets before the end of July.

- Labat Africa (JSE: LAB) is moving ahead with the acquisition of a further 24.45% in Classic International. This will take them to a 100% stake in this technology distribution company. They are paying R27 million for this stake, a number that still makes absolutely no sense in the context of Classic’s profit after tax for the year ended February 2026 of R115.1 million. Labat is basically buying it on a P/E of 1x! They are paying for the acquisition with shares issued at R0.03 per share. Labat remains one of the true mysteries on the JSE. They desperately need to get on with explaining the strategy to the market if they want this share price to reflect the underlying value that appears to be there.

- Financial results at Nictus (JSE: NCS) only get a mention down in the Nibbles on an otherwise very busy day of news. That’s a pity, as this small cap achieved HEPS growth of 84% for the year ended March 2026! This was despite a decline in revenue of 17.7%. The dividend per share has jumped by 50%. Nictus isn’t as small as it used to be, with the market cap at R160 million after the share price climbed 45% in the past year.

- Acsion (JSE: ACS) is another name that only gets a passing mention down here today. For the year ended February 2026, revenue was up by 7% and HEPS increased by 23%. The discount to net asset value (NAV) in the share price remains enormous, with a NAV per share of R32.27 vs. the share price at R9.00!

- Salungano (JSE: SLG) ends up in the Nibbles as well due to low liquidity in the stock. For the year ended March 2026, they saw a substantial jump in EBITDA of over R300 million despite revenue increasing by only R100 million. The magic happened in gross profit, which was up by around R300 million – an increase that carried through into EBITDA. HEPS increased spectacularly from 2.62 cents to 50.85 cents.

- After selling its specialty chemicals company, Aimia (JSE: AIM) has used roughly half of the proceeds to repurchase Senior Notes worth $131.4 million. The remaining $137 million will be used for share repurchases, working capital and potential investments.

- Shuka Minerals (JSE: SKA) is still in the exploration phase, so their financial statements don’t reflect any revenue. It’s completely normal to see losses in this phase, with the operating loss having come in at £884k for the year ended December 2025.

- Kore Potash (JSE: KP2) is still flirting with potential buyers of the company. At one point there was only one party still interested, but a second party joined the fray in June. Competitive tension is critical in a process like this.

- Zeder’s (JSE: ZED) disposal of Zaad is taking longer than expected thanks to regulatory approvals. This is a common issue in large transactions. To allow for this, the long stop date has been extended to 30 November 2026.

- Sebata Holdings (JSE: SEB) has been catching up on its financial reporting. They’ve now released their interims for the six months to September 2025, reflecting a swing from a headline loss per share of 0.13 cents to positive HEPS of 3.26 cents. The company can now apply to the JSE for the lifting of its suspension, with the FY26 results needing to be released soon as well.

- In case you’re following Rex Trueform (JSE: RTO) or related company African and Overseas Enterprises (JSE: AOO), then be aware that the service level agreement with GMS (the CEO’s entity) is being renewed. This is obviously a related party deal that is accompanied by a fairness opinion by an independent expert.