In this edition of Ghost Bites:

- Hammerson recycles capital at a premium to book

- As expected, Hyprop ended up raising more than R500 million

- Trustco’s investment in Meya Mining is in serious trouble

- Nibbles: MAS, Prosus and more

Hammerson recycles capital at a premium to book (JSE: HMN)

Investors place a lot of importance on these transactions

Property funds are generally valued with reference to their book value, or net asset value (NAV) per share. These funds “recycle capital” by selling existing properties and putting that capital into new properties. But what is the link to NAV?

Well, each of the underlying properties in the fund contributes to the NAV by having its own book value. If the fund is recycling capital (i.e. selling properties) at a premium to NAV, or in line with NAV, then it gives the market evidence that the overall fund NAV is credible. If you want to prove the value of something, the best way is to turn it into cash!

Hammerson has announced the sale of £69 million of non-core assets, including a number of properties in Dublin that were sold to Transport Infrastructure Ireland to unlock the city’s planned Metrolink train system. Together with smaller disposals earlier in the year, Hammerson has sold £75 million in non-core assets at a “substantial premium to book value”.

It would be nice if the announcement indicated the exact premium, rather than being coy about the numbers.

Hammerson’s recent capital allocation strategy has focused on taking control of joint ventures, so it will be interesting to see how they allocate the latest capital inflow.

Ghost Bite: Hammerson has been through some rough times, but the recent share price trajectory has been solid. The total return over 12 months is almost 20%!

As expected, Hyprop ended up raising more than R500 million (JSE: HYP)

The market remains highly supportive of REITs

On Tuesday, when Hyprop told the market that they were looking to raise R500 million in fresh equity, I wrote in Ghost Bites that there was a good chance of them upsizing the raise based on market demand. Recent capital raising activity in the REIT sector has been strong, with investors throwing money at the best of the local REITs.

Sure enough, Hyprop has increased the raise to R739 million, the absolute maximum that the company could issue based on current authorities in place from shareholders. The price of R58.50 is actually a 1.4% premium to the 30-day volume-weighted average price (VWAP). The spot price is R59.32, so at least we aren’t in a crazy scenario where investors are paying a premium to spot.

The book was oversubscribed. Although the announcement isn’t 100% clear, I think this means that there was even more demand than the R739 million that was eventually raised. It’s pretty obvious that it was oversubscribed with reference to the initial R500 million raise, otherwise they wouldn’t have upsized it!

Ghost Bite: This is another excellent example of the depth of the capital pools on the JSE, particularly for property stocks.

Trustco’s investment in Meya Mining is in serious trouble (JSE: TTO)

Unsurprisingly, Meya Mining hasn’t escaped the destruction of the mined diamond industry

A few years ago, I was one of the only analysts in South Africa who was pounding the table (as they say) about the end of the mined diamond industry. My conviction stemmed directly from my then-girlfriend (and now-wife) specifically requesting a lab-grown diamond. Suddenly, I was paying attention to this sector. The more I researched it, the more I realised that mined diamonds were in huge trouble.

This disruption has been even more extreme than Chinese cars disrupting European and Japanese brands. Where the Chinese are offering an acceptable substitute at a much lower price, lab-grown diamonds are a perfect substitute at a vastly lower price. That’s a recipe for serious change in an industry.

With names like De Beers struggling to carve out a sustainable future, Meya Mining in Sierra Leone (part of the Trustco portfolio) doesn’t stand much of a chance.

Although Meya Mining raised a $25 million facility earlier this year, things have gotten even worse since then. The asset is in care and maintenance based on conditions in the diamond market, with this status set to continue until at least the fourth quarter of the 2026 financial year.

The risk to Meya is significant, with the auditors flagging a going concern risk in the 2025 financial statements. Although Trustco hasn’t provided any guarantees, Trustco does have a loan receivable of $46 million from Meya. The recoverability of this loan is clearly in doubt, with Trustco considering the carrying value of that loan as part of its current audit procedures.

Ghost Bite: Essentially, Trustco is flagging a substantial potential impairment here. There’s already a huge amount of noise around the company, so this won’t do them any favours.

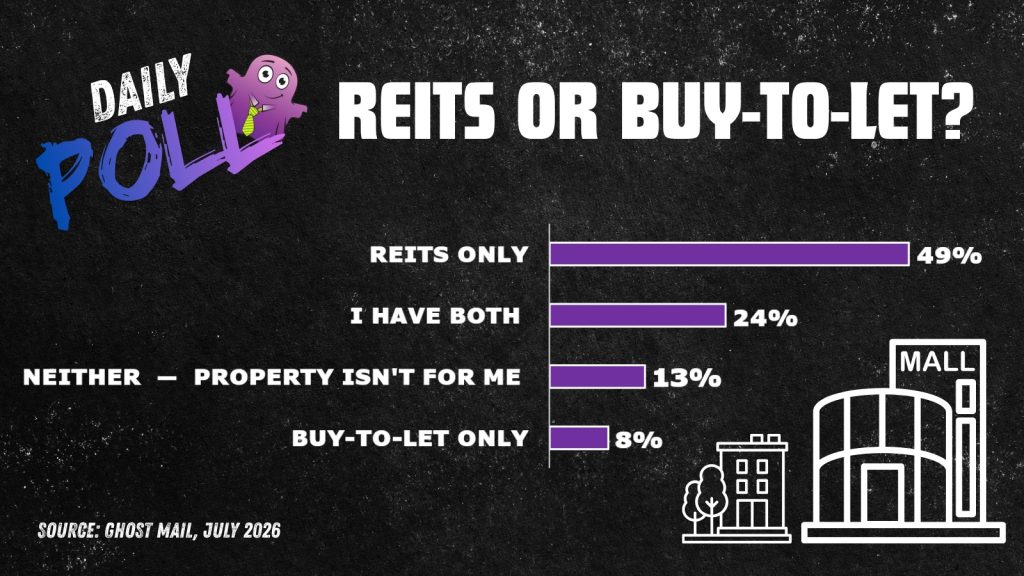

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Marshall Monteagle (JSE: MMP) converted warrants into ordinary shares worth a juicy R16.4 million.

- A founding director of Famous Brands (JSE: FBR) sold shares worth over R2 million.

- An independent non-executive director of CA Sales Holdings (JSE: CAA) bought shares in the company on the Botswana Stock Exchange to the value of around R170k. The awkward part is that the first trade was on 29 April 2026, so this isn’t exactly a timeous notification by that director.

- A director of Santova (JSE: SNT) sold shares worth R119k.

- A director of Trematon (JSE: TMT) bought shares worth R4.1k.

- In late May this year, MAS (JSE: MSP) announced the disposal of various assets, including six open-air malls in Romania. That specific disposal has now been completed. When the deal was first announced, MAS expected the net selling price to be €197.7 million (based on the property values, less the bank loans specific to the entities holding the properties). The latest announcement doesn’t give an updated number, so we have to assume that this is how things ended up.

- Prosus (JSE: PRX) has been having a tough time on the market this year thanks to the selling pressure on Tencent. But if you look beyond this issue, you’ll find that the ecosystems business has become cash flow positive. This helps the Prosus balance sheet tremendously, with numerous knock-on benefits including access to debt. The company is now refinancing $1 billion in notes due in January 2027 and $614 million due in July 2027. These will be replaced by notes due in 2036 and 2033, priced at between 5.528% and 5.873%. This gives you a good idea of the cost of the group’s debt funding.

- If you’re paying very close attention to Burstone (JSE: BTN), then be aware that the company picked up some errors in the reviewed financial statements for the year ended March 2026. Seeing a “change statement” is a rarity on the JSE, but it does happen from time to time, as reviewed financials are released before the final audit is completed. The change is a minor deterioration in the diluted loss per share, along with a few other changes to how certain numbers are classified. It doesn’t look material overall.

- Labat Africa (JSE: LAB) has received approval to transfer its listing to the General Segment of the Main Board of the JSE. This is certainly a step in the right direction. The effective date of the transfer is 13 July 2026.