Corporate actions may be quiet, but JSE Limited is doing just fine

There’s much to learn from Nedbank’s interim numbers and their focus areas

Corporate actions may be quiet, but JSE Limited is doing just fine (JSE: JSE)

There’s much more to the owner of the JSE than people think

JSE Limited is a listed company. This always surprises market newbies.

People refer to “the JSE” as the exchange, but it’s also a listed company with a market cap of R13 billion and a 12-month share price increase of 12%. Add in the dividend and you get to a total return of over 19.5%. Clearly, they are doing well.

But how can that be? All we hear about is companies delisting from the market. Surely the JSE is going bankrupt at the speed of light?

Although losing listed companies isn’t helpful, the truth of it is that companies with very little liquidity aren’t of much value to the exchange. If they just sit there, often late on financial reporting and dealing with other issues, they just cause far more headaches than they are worth.

Another important point is that the equity market is just one part of the business model at JSE Limited. There’s a vibrant debt market for example, along with other areas like derivatives. The JSE is also required to have an enormous regulatory capital balance (currently R835 million), so the results are impacted by investment returns on that capital. It’s not just about the number of listed companies.

Here’s the proof: we certainly haven’t seen a 14.1% increase in the number of listings on the market, yet that’s the revenue growth that the company achieved for the six months to June 2026. Interesting, right?

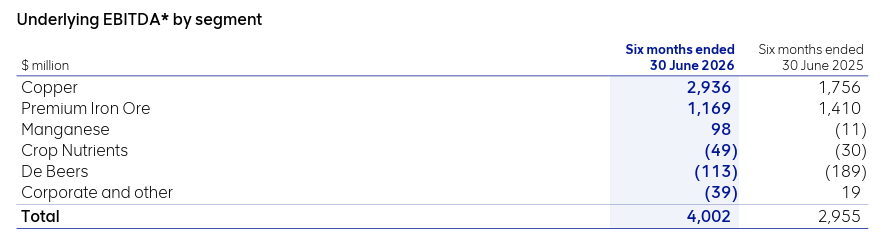

This table shows you how diversified the business actually is:

One area where the lack of activity is being felt is in JIS, which earns revenue based on corporate actions (among other things). JIS was down 5.6%, although I suspect that the underlying corporate action revenue was down by a lot more. The corporate finance industry (where I spent several years after articles) has been forced to focus on private company transactions in recent years, as there just isn’t enough going on in the listed space.

Total expenditure grew by 11.5%, so they have achieved margin uplift (revenue growth was ahead of expenses). I must point out the 22.8% increase in personnel expenses within that number. This is something to keep an eye on, although a fair chunk of it seems to relate to “organisational redesign”. If you accept the company’s adjustment for once-off costs, then personnel expenses were up by 7.8% – a far more reasonable number.

Earnings before interest and tax (EBIT) increased by a juicy 21.4%. Below that line, net finance income actually declined by 9.8%, so that took some of the shine off.

Net profit after tax increased by 16.9% and HEPS was up by 18.8%.

Net cash from operations was up by 20.6% to R625 million, so there’s solid conversion of EBIT (R774 million) into cash. But the capex number really stands out, having ballooned from R27 million to R110 million. They don’t really give further details, noting only that they are focused on “protecting and growing the core business” – in other words, it’s a mix of sustaining and expansionary capex.

This is a strong set of interim numbers. Revenue will hopefully continue its positive trajectory in the second half of the year, as expense pressures are coming through the system. The company has revised its full year 2026 operating expenses growth to 6% – 8% (up 100 basis points vs. previous guidance). Full year capex is expected to be between R190 million and R230 million, in line with previous guidance.

Ghost Bite: JSE Limited is certainly investing heavily for growth. I’ll always want to see this translate into more listings, but the business is much broader than that.

There’s much to learn from Nedbank’s interim numbers and their focus areas (JSE: NED)

The strategy in Africa is one thing, but the South African numbers are filled with interesting nuggets

Nedbank has released results for the six months to June 2026. Before I give you my views on them, I want to thank the group for valuing the Ghost Mail audience. Nedbank has placed their results on the Ghost Mail website for your convenience. Please do check them out!

As always, what you’ll read below is my independent take on the numbers.

The green bank came into 2026 expecting a year that would be anything but green. Headline earnings were flat for the six months, with the group noting that this outperformed their expectations. I must immediately highlight that if you exclude the base effect of Ecobank, you’ll find headline earnings growth of 12%. Diluted HEPS on that basis was up 15%. That’s more like it!

Another stat I’ll quickly deal with is the credit-loss ratio, which has moved up from 81 basis points in H1 2025 to 95 basis points in H1 2026. The retail book is currently running above the through-the-cycle target range, so that’s a concerning data point for South African consumers. There’s been a particularly nasty spike in home loans and credit cards.

Just when investors in South African consumer stocks thought it couldn’t get any worse, we get a data point like this. Sigh.

Nedbank’s interim dividend per share is up by 2%, so that’s probably the fairest reflection of the underlying growth in the group at the moment. The numbers only inched upwards as Nedbank moves through a critical transition phase.

But the future is what really counts. Nedbank is making significant strategic changes to their group that will hopefully pay off in years to come. With the shares trading on a P/E multiple of roughly 7.5x, the market isn’t exactly putting a premium on the growth prospects right now. Nedbank bulls will argue that this is where the opportunity lies.

The obvious strategic change for me to mention is in Africa. Having gotten out of Ecobank, Nedbank decided to go after a controlling stake in NCBA Group. This is an East African financial services group that would give Nedbank a far more compelling presence in Africa than they’ve had before.

An argument could certainly be made that the 21% stake in Ecobank was a half-pregnant strategy, which simply doesn’t cut it vs. what competitors like Absa (JSE: ABG) and Standard Bank (JSE: SBK) have been doing on the continent. But with NCBA, the size of the prize after this deal is a controlling stake in a tier 1 bank in Kenya. That’s a whole lot more interesting.

In terms of the deal process, the NCBA offer closed on 10 July and was accepted by enough holders for Nedbank to achieve the desired 66% stake. They now need to achieve the various regulatory approvals to get the deal across the line.

But here’s the thing: even with this transaction, the pro-forma split of headline earnings would be roughly 86% from South Africa. The Africa story is becoming more interesting, but remains small overall.

In Nedbank’s home market, the recent acquisition of iKhokha is an important step into the SME market. The integration of Eqstra has given them a stronger business in fleet management. We have a very competitive market, with Nedbank trying to focus on specific growth engines.

This means we need to take a closer look at the segments.

The Corporate and Investment Banking (CIB) business, which focuses on the biggest corporates, achieved growth in advances of 8%. This part of the business tends to be driven by sector specialisation and deep relationships. For example, trade finance revenue was up by 18% thanks to flows in commodity trading and agriculture.

Deposits went up 14%, so these companies are sitting on significant cash at the moment. Non-interest revenue increased by 16%, driven by strong deal flow.

In Business and Commercial Banking (BCB), which focuses on the mid-market and SME space, advances were up 6% and deposits grew by 7%. This segment doesn’t appear to be as cash flush as the biggest corporates. Non-interest revenue increased by 14%.

In Personal and Private Banking (PPB), which is the retail banking segment, main banked clients actually increased by 2%. I think that’s pretty good when you consider the competitive bloodbath out there. On the higher income side, they grew clients in Private, Wealth and Stockbroking by 8%. Another juicy growth engine to note is insurance income, up by 21%.

With deposits up by 4%, retail deposit market share increased from 16.8% (December 2025) to 17.0% in May 2026. Their target is to be above 17%, so that’s encouraging.

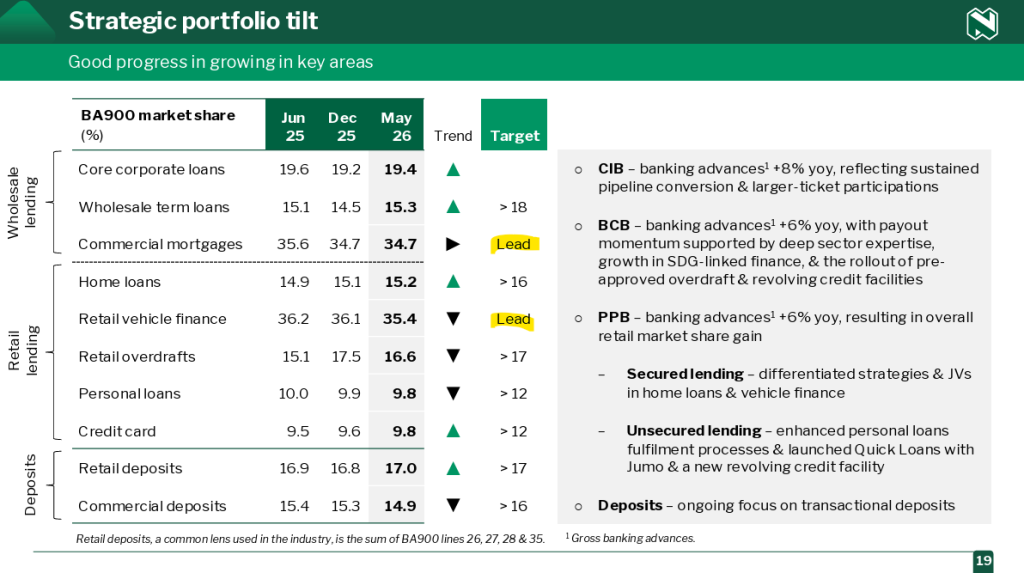

This is a good opportunity to bring you a particularly interesting slide from the analyst presentation. Regulatory filings (the “BA900” reference) allow Nedbank and its competitors to accurately work out their market share across different categories. As you’ll see below, Nedbank is actually the market leader in commercial mortgages and retail vehicle finance. I must, however, note the decline in retail vehicle finance market share, something to keep an eye on given how lucrative this space is in South Africa:

Another area that I want to focus on is renewable energy financing. They have exposure of R56 billion to this asset class, with a further pipeline of R26 billion for the second half of 2026. To understand more about this space, I recently recorded a podcast with Tokollo Tau of Nedbank. Listen to it below or get the transcript here.

Overall, Nedbank expects Return on Equity (ROE) – currently at 15% – to move above 15% in 2026. Shareholders will be happy to see that direction of travel.

Ghost Bite: The medium-term goal is for ROE to reach 17%. I can tell you for sure that the additional 2 percentage points will be very hard to unlock. If Jason Quinn gets that right during his tenure as CEO, it will go down as a highly impressive stint in local banking.

Nedbank financials for the six months ended March 2026

“Following the bold strategic decisions we made in 2025 to become more client-centred, unlock growth and cross-sell opportunities, diversify earnings, and enhance productivity, benefits have become more evident across our business clusters in the first half of 2026.”

Jason Quinn – Chief Executive

FINANCIAL HIGHLIGHTS

Headline earnings of R8 405m, up by 0.1% (June 2025: R8 399m)

Revenue of R38 235m, up by 6% (June 2025: R35 981m).

Credit loss ratio of 95 bps (June 2025: 81 bps).

Total operating expenses of R21 696m, up by 3% (June 2025: R21 067m).

Cost-to-income ratio of 56.2% (June 2025: 56.9%).

Diluted headline earnings per share of 1 803 cents, up by 2% (June 2025: 1 762 cents).

Headline earnings per share of 1 841 cents, up by 2% (June 2025: 1 800 cents).

Basic earnings per share of 1 830 cents, up by 16% (June 2025: 1 571 cents).

Interim dividend of 1 052 cents per share (June 2025: 1 028 cents).

Net asset value per share of 25 486 cents, up by 4% (June 2025: 24 522 cents).

Common equity tier 1 ratio of 12.6% (June 2025: 13.1%).

FOCUSED EXECUTION AND GROWTH

The US–Iran war and the closure of the Strait of Hormuz weighed on the global economy in the second quarter of 2026. Higher energy prices pushed global inflation higher, prompting a more hawkish monetary policy stance in some markets.

The operating environment in SA during the first half of 2026 was mixed. Real GDP growth in the first quarter surprised on the upside, while higher fuel prices drove local consumer inflation up from a low of 3% in February and, in response, SARB’s Monetary Policy Committee increased interest rates by 25 bps in May, taking the prime lending rate up to 10.5%. Industry credit growth strengthened modestly, with corporate credit growth accelerating off a low base, while household credit growth improved gradually but remained constrained by affordability pressures.

SA’s economic outlook continues to show encouraging signs of improvement, underpinned by a more credible fiscal trajectory, progress on structural reforms, and recent credit rating upgrades. Many of the country’s positive prospects as an attractive investment destination remain intact despite global uncertainties and the conflict in the Middle East.

Headline earnings (HE) for the 6 months to 30 June 2026 were flat yoy at R8.4bn, outperforming our expectations at the start of the year. HE benefited from improving net interest income growth, strong non-interest revenue growth and very disciplined expense management, offset by a higher impairment charge and no further recognition of associate income from Ecobank Transnational Incorporated (ETI) following the disposal of our investment in 2025. When excluding the ETI base effect, HE growth was strong at 12%, reflecting a strong underlying operational performance. Diluted HEPS increased by 2% to 1 803 cents and growth was ahead of HE growth due to the run rate impact of the well-timed share buybacks executed in 2025. Return on equity (ROE) of 15.0% (H1 2025: 15.2%) remained above the group’s cost of equity of 14.0%. Balance sheet metrics remained strong, supporting the declaration of an interim dividend of 1 052 cents per share.

Following the bold strategic decisions we made in 2025 to become more client-centred, unlock growth and cross-sell opportunities, diversify earnings, and enhance productivity, benefits have become more evident across our business clusters in the first half of 2026. In CIB, growth momentum improved as stronger, more diversified, pipeline conversion and participation in larger transactions supported advances growth, while trade finance and commission and fee income benefited from strong deal flow. In BCB, investments in the new cluster and recent acquisitions have started to deliver revenue benefits, with advances growth accelerating, commission and fees increasing strongly, and early synergies emerging from the iKhokha and Eqstra acquisitions. In PPB, growth and efficiency initiatives supported continued advances momentum, market share gains in advances and deposits, very strong growth in insurance and payments, and further productivity improvements. In NAR: SADC, strategic execution supported strong advances and NIR growth, improved operational efficiency, and an increase in ROE.

In Q1 2026 we announced our intention to acquire a controlling interest in NCBA Group plc, a leading East African financial services group, supporting our ambition to grow and diversify earnings in attractive markets. The offer closed on 10 July 2026 and was accepted by shareholders representing 79.9% of NCBA shares in issue, enabling us to achieve our targeted 66% shareholding. Key regulatory approvals have been obtained, with the remaining approvals expected towards the end of Q3 or early in Q4 of 2026.

We continued to make good progress on our strategic value unlocks. Digital volumes and values increased strongly as more clients across all our businesses embraced the benefits and convenience of digital channels. Our AI and data capabilities are delivering tangible benefits across revenue generation, credit effectiveness, client experiences, productivity, cost optimisation, and fraud processes. Client satisfaction metrics remained at the top end of the peer group, while the value of the Nedbank brand increased by 16% to R24bn. Total clients increased by 4% to 8 million, supported by growth across individuals and SMEs. Under strategic portfolio tilt, we recorded market share gains in home loans, credit cards, wholesale term loans, and retail deposits. Our increased focus on insurance and payments saw strong growth, with MyCover insurance gross earned premiums increasing by 23% and digital payments NIR in PPB increasing by 15%. Lastly, lending to clients that creates lasting positive impacts, sustainable development finance, increased to R213bn, representing 21% of total gross loans.

Looking forward, SA GDP growth is expected to improve modestly to around 1.3% in 2026 and 1.4% in 2027, supported by resilient consumer spending but constrained by weak business confidence, subdued fixed investment and global energy price risks. Inflation is expected to average around 4.0% in 2026, remaining above SARB’s 3% target but within its tolerance band, and the prime lending rate is expected to increase by a further 25 bps in September 2026 before declining in 2027. Banking conditions should improve gradually, with credit growth projected to remain positive and end the year at around 7%, although risks remain tilted to the downside. We expect the underlying growth momentum across all our businesses to continue in H2 2026, supporting an improvement in HE growth from the flat outcome reported in the first half. ROE is expected to remain above 15% in 2026, heading towards 2025 levels. In the medium term, we remain focused on delivering an ROE of around 17% in 2028, underpinned by stronger revenue growth and continued operational efficiency gains.

I thank all our Nedbank colleagues for their contribution to the strong underlying momentum evident in the first half of the year. We deeply value the continued trust of our clients and the constructive engagements with investors, regulators and other stakeholders. As Nedbank, we remain committed to using our financial expertise to do good.

Jason Quinn

Chief Executive

* Our guidance and targets are not profit forecasts and the group’s joint auditors have not reviewed or reported on them.

This short-form announcement is the responsibility of the directors.

Investment decisions should be based on consideration of the full unaudited condensed consolidated interim financial results for the 6 months ended 30 June 2026, as this announcement does not contain full or complete details.

MTN’s share price has been slashed in response to recent numbers (JSE: MTN)

The Q2 slowdown in MTN Nigeria is the likeliest cause of this pain

Before I dig into the recent financials from MTN Nigeria and MTN Ghana, I want to highlight the progress made on the IHS transaction. MTN is in the process of acquiring the remaining shares in IHS, giving them more control over the infrastructure that they rely on across Africa. Importantly, shareholders of IHS have approved the transaction. This leaves them with only the regulatory approvals to get in place.

Now, let’s get to the really juicy stuff.

MTN’s African subsidiaries always release their results before the mothership brings us numbers. In practice, it’s the African numbers that tend to drive the MTN share price, as the South African business is a relatively steady (and slightly boring) story.

The recent updates from MTN Nigeria and MTN Ghana drove a nasty correction in the MTN share price:

If you look at the numbers through a six-month lens, then both of the subsidiaries look great. But if you take a quarter-on-quarter view to assess momentum through the period, you’ll find a problem in MTN Nigeria that has spooked the market.

Buckle up!

MTN Nigeria: a wobbly, or a bigger problem?

We begin with MTN Nigeria, easily the most important of the African subsidiaries. This means it has caused the strongest headaches and driven the most exciting upside for MTN investors. After all, Africa is always a game of risk and reward.

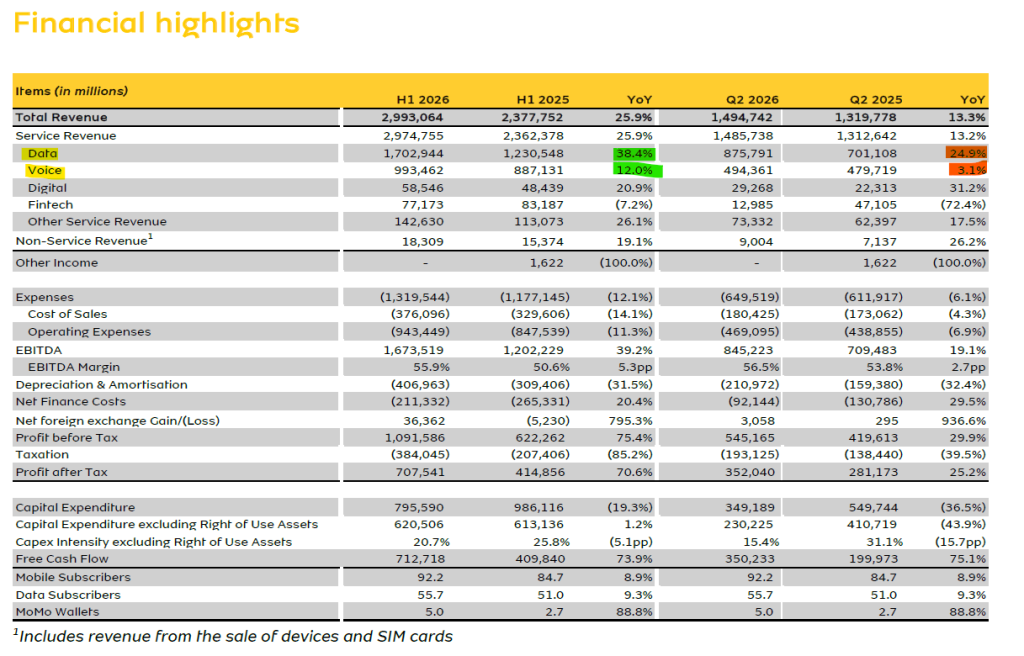

For the six months to June, MTN Nigeria grew subscribers by 8.9% to 92.2 million. They have 55.7 million active data users. This immediately gives you an idea of the growth runway for data relative to other services.

Thanks to an increase in activity per user, service revenue for the six months was up by a juicy 25.9%. That’s ahead of the medium-term guidance of “at least low 20% growth”. It’s also 10.4 percentage points above the inflation rate for the period, so they are delivering real growth here.

If you exclude the airtime and data credit service (which is where Optasia (JSE: OPA) plays), then growth for the six months was 27.3%. You can see why the market has become worried about whether Optasia has any moat at all. The second quarter tells a very different story though, perhaps giving some reassurance to Optasia investors who have seen their share price fall by 31% year-to-date.

To finish off on the numbers for the first half, operating expenses grew by 11.3%, or less than half the growth rate in revenue. This led to EBITDA jumping by 39.2%, with EBITDA margin expanding by 5.3 percentage points to 55.9%. By the time we reach the bottom of the income statement, we find profit after tax up by a delicious 70.6%. Earnings per share followed suit.

The big question is always around free cash flow, as the telcos can be capex-hungry beasts at times. This period was an exception, not least of all because the naira strengthened against the US dollar (much of the capex is driven by US dollar costs). This is why capex (excluding leases) was up by only 1.2%. Free cash flow jumped by a spectacular 73.9%.

All of this is good news alongside the strong balance sheet. There’s a net cash position of ₦116.3 billion, up 11% from December 2025. This is giving them the confidence to pay dividends.

So, what’s the problem here?

The slowdown in growth in Q2 vs. Q1 is the likeliest cause for the concern in the market. The second quarter only achieved year-on-year growth of 13.2% in service revenue, way below the 25.9% achieved for the six months. Profit after tax for Q2 increased by “only” 25.2%.

The impact of the airtime credit suspension is clearer here, as fintech revenue fell by a nasty 72.4% in Q2. Fintech only contributed 3.6% of service revenue in the comparable period, but that’s still enough to have knocked growth by a couple of percentage points.

The bigger stress points are data and voice revenue, where growth in the second quarter was way down on the first quarter. I’ve indicated in the screenshot below where you would see those percentage movements:

Perhaps the lack of airtime credit services in the second quarter had a much bigger impact than MTN was letting on? If so, then MTN has severely downplayed their importance to the market, much to the detriment of the Optasia investment case.

All eyes are on the second half of the year. The airtime credit issues are behind them, so the market will hope to see a return to growth across the board. It helps that capex intensity (currently 20.7%) is expected to moderate – i.e. it should come down, which implies that capex will grow at a slower rate than revenue in the second half of the year.

The medium-term guidance is unchanged. They are aiming for revenue growth in the low-20% region. EBITDA margin is expected to be in the mid-to-high-50% range.

Another point to note is that MTN Nigeria is still keen to carve out the fintech business and turn it into a distinct business.

MTN Ghana: less to worry about (well, mostly)

At MTN Ghana, let’s just get the new risk out of the way first. The company announced that Clydestone has sued the company based on claims that MTN used Clydestone IP for the launch of mobile money in Ghana. MTN Ghana has come out strongly in response to this case, noting that they are not recognising any related liability.

This is a classic example of a “legal overhang” in the market. Nobody actually knows how it will turn out, but investors need to think about it anyway.

Onwards to the numbers. Mobile subscribers increased by 8.5% to 32.8 million. Active data subscribers jumped by 17% to 21.3 million. It’s a much smaller business than MTN Nigeria, but still a very important one.

Service revenue increased by an impressive 32.3%, a country mile ahead of the average inflation rate of 3.8%. This is significantly higher than the real growth rate we saw in MTN Nigeria. One of the factors was that the fintech business didn’t have any regulatory issues to deal with, so MTN Ghana could just get on with growing their business.

Operating expenses grew by 24.2%, so there’s clearly investment required to achieve these levels of growth. Still, that’s well below revenue growth, so EBITDA was up by 39.8%. This drove EBITDA margin expansion of 3.4 percentage points to 61.8%.

Other notable line items include a 26% increase in depreciation and amortisation, as well as a 12.6% increase in net finance costs. The EBITDA growth was more than enough to cover this, so profit after tax increased by 43.3%.

Capex (ex-leases) for the period was down by 13.3%. This took capex intensity down from 20.4% to 13.0%.

The frustrating thing is that they don’t specifically disclose free cash flow. I can eyeball the numbers and see that it’s gone the right way, but it takes time to calculate properly. MTN Ghana should be providing this number to its investors in the highlights section.

In terms of momentum during the period, the second-half growth in service revenue (29.2%) is only slightly down on the 32.3% for the six months. This shape is repeated in EBITDA and profit after tax. But where you’ll find a big difference is in capex ex-leases, up 12.6% for Q2 vs. a decrease of 13.3% for the six months.

MTN Ghana is ahead of MTN Nigeria in the fintech separation process, having successfully completed the structural separation of the Mobile Money business. It’s just awkward that they now have a legal irritation to deal with.

Ghost Bite: Volatility at MTN is a feature of the story. Now on a P/E of 16x and with group numbers coming soon, they are still trading at a premium valuation that requires significant growth to be justified. The debate is raging around MTN Nigeria’s growth and whether this slowdown will stick. Here’s a five-year chart to give this move more context:

Nibbles:

Director dealings:

A senior exec at Hammerson (JSE: HMN) sold shares in the company worth £204k. This comes just after the company raised capital from outside investors, so that’s not a particularly great look.

A director of a major subsidiary of Vodacom (JSE: VOD) sold shares in the company worth R1.7 million.

A director of Canal+ (JSE: CNP) bought shares worth €75k (around R1.4 million).

The CEO of Sirius Real Estate (JSE: SRE) and a close associate bought shares in the company in their self-invested pensions worth around R775k.

The CEO of Salungano (JSE: SLG) bought shares worth R461k.

An entity linked to a few directors bought shares in Sebata Holdings (JSE: SEB) worth R9k.

As a reminder of how big some of the corporate balance sheets out there actually are, British American Tobacco (JSE: BTI) casually priced $1.5 billion worth of notes as part of a general refinancing of the balance sheet. This is typical of a treasury strategy at a company of this size, with the proceeds likely to be used primarily for repayment of other notes or debts.

In case you’re an IFRS nerd and you want to dig into Sanlam’s (JSE: SLM) new reporting framework, the company has announced the release of 2025 comparative information under that new approach. This is in preparation for the release of interim financial results on 10 September.

Here’s an interesting one: Grindrod (JSE: GND) announced that Value Capital Partners (VCP) now has a stake in the company of 5.239%. This announcement is triggered by VCP moving through the 5% milestone. These sorts of things happen often on the JSE. The difference is that VCP is rarely a completely passive shareholder like most institutional asset managers. Will VCP stop there, or is there a broader plan here?

Zeda (JSE: ZZD) announced that a company named Mandisa Holdings now has 5.19% in the company. This is worth keeping an eye on.

Aimia (JSE: AII) has been busy with its share repurchase programme. The company repurchased 0.2% of its shares during July at a weighted average price of $2.67 per share. There’s literally no liquidity in this stock on the JSE. The local market is waiting to see what this company’s bigger plan is.

Numeral (JSE: XII) released results for the three months to May 2026. There’s almost no liquidity in this tiny (R35 million market cap) company. Revenue for the three months was down 1% at $467k. The group reported a very small headline loss per share.

Here’s a fun one: Old Mutual (JSE: OMU) announced that Old Mutual Zimbabwe’s listing will migrate from the Zimbabwe Stock Exchange to the Victoria Falls Stock Exchange. It certainly has a more exciting name! In case you’re wondering, this has no impact on South African investors.

How do you know whether your investment performance is actually good?

In this episode of Ghost Stories, The Finance Ghost is joined by Siyabulela Nomoyi from Satrix to unpack one of the most important, yet often misunderstood, concepts in investing: benchmarks. From retail portfolios to institutional mandates, we explore why returns only tell half the story and why every investment outcome needs a meaningful point of comparison.

The discussion goes well beyond the basics, covering how benchmarks are selected, the role they play in risk management, the differences between indices and other benchmark types, and why ETFs offer investors an accessible way to measure performance against the market. Siya also shares practical insights into index construction, concentration risk, tracking error and the common mistakes investors make when choosing benchmarks, reminding us that outperforming a benchmark isn’t always as impressive as it sounds.

In this episode:

Why benchmarks are essential for evaluating investment performance

How investment mandates, time horizons and risk tolerance influence benchmark selection

The difference between indices, benchmarks and hedge fund hurdle rates

Why ETFs are a practical way to access investable benchmarks

How index construction and weighting methodologies affect risk and returns

The importance of tracking error, fees and liquidity when assessing ETFs

Why beating a benchmark can sometimes be misleading

Common mistakes investors make when choosing and using benchmarks

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. I’m your host, The Finance Ghost. My guest today is Siyabulela Nomoyi from Satrix. And let me tell you, we have both been having the Monday of all Mondays. We’ve had to move this a couple of times while we deal with some respective tough stuff.

But thank you for nonetheless making time for this, and I’m really glad that we actually got a chance to sit down and do this in the end.

Siyabulela Nomoyi: Yeah, Ghost, thanks for having me. Mondays are like that; it is what it is. That’s the life. Hi to the listeners as well and thank you for inviting me again.

The Finance Ghost: So, Siya, let’s make the most then of the time that we do have, which I am really looking forward to. And we’re going to be talking about benchmarks today. And that’s because you wrote quite a cool piece recently on this entire topic.

I think that people, when they talk about returns on their stocks or their investments, they’re really only giving half the picture, right? They’re basically telling you how they did, but it doesn’t give you the context of how everything else did and things with maybe similar risk profiles and that kind of stuff. And we’ll talk about that on the show.

But I think let’s maybe just cover why it’s important to have a benchmark in the first place. And obviously this is something that as an ETF specialist, you live and breathe, which we’ll also cover in this discussion. But initially, just to kick us off, take us through why it’s important to actually have a benchmark.

Siyabulela Nomoyi: Sure, Ghost, thank you. So, as you mentioned, the other day I wrote an article on this and believe me, my marketing team actually trimmed it to fit media house limits. I had about five pages of writing on it. In other words, I think it’s very, very important and I hope our discussion can actually shed light on the why of that.

I’m hoping both retail and institutional investors can appreciate this. But choosing the right benchmark is one of the most significant decisions in investment management and one of the most underappreciated as well.

So, firstly, let’s just step back a bit, and ask what a benchmark is before we continue. Just in case there’s someone curious about that part (and has not really or exactly appreciated why we would be talking about today).

So very, very loosely, think of a benchmark as a standard way to test or use to measure and compare how well something performs, right? So, in investments you can use it as a baseline to measure how yourself and how your portfolio is doing; or the market, or any other player that’s out there.

Or if you want to look at peers or anything like that, you can actually look at how well you’re doing in relative terms compared to those.

So, there are investors out there who spend their days trying to beat a certain benchmark (the market in this instance), and so they compare themselves to an index that would be the benchmark. Others actually just prefer to be in line with the market, just want the market exposure and don’t bother with outperforming it.

To quote what I had mentioned in the article, is that for a fund manager, a benchmark is often a constraint, the reference point against which performance will be measured and against which any deviation must be actually justified. So, in investment terms, we would talk about tracking error here or an active return.

But now, if you are sitting in an investment committee, it might function more as a goal, where it acts as a proxy for the return of the portfolio that you expect to deliver.

But also, for risk management as well, it does act as a blueprint; a description of what the market exposure of the portfolio is designed to actually replicate or actually approximate.

But look, a well-chosen benchmark serves all those three purposes simultaneously. It sets a realistic performance expectation, defines the risk profile of the investor, whatever that investor has agreed to actually accept in terms of risk. It also creates accountability as well, which is very important, especially in my field. So, giving both the investor and the manager a shared language for evaluating outcomes.

So, you want to sit there and evaluate whether this manager is doing well, you should ask: doing well compared to what or relative to what? I should just mention that choosing a benchmark should never be a tick-of-a-box exercise. A well-chosen benchmark serves all the purposes that I’ve just mentioned.

It sets a realistic performance expectation. It also defines the risk profile of the investor. As I mentioned, the accountability part. If you are telling me, Ghost, that your portfolio is doing well, I need to just ask you: performing well relative to what? Especially in a space where I need to actually evaluate your answer within some investment risk spectrum.

The Finance Ghost: Siya, thank you so much for setting the scene for us there. And in the world of professional money management (and I think most people listening to this will be retail investors, but if we just borrow from the professionals for a moment) then the benchmark essentially is related to their investment mandate, right?

But for retail investors, it’s not necessarily that formal. You can technically pick whatever benchmark you like. You should just pick something that makes sense. You know, if you’re investing in South Africa, then something like the JSE Index would make a lot of sense. You wouldn’t go and choose something random like another emerging markets index. That wouldn’t really make any sense in the context of that portfolio.

So perhaps just dealing with the professional side of things for a moment, how does the investment mandate of a professional asset manager actually inform their choice of benchmark?

Siyabulela Nomoyi: It’s an important question and I think it covers the entire investment world, whether retail or professional management.

And I’m saying that because I think as a retail investor I might sit at home, look at my returns and I think I’m doing very well for what I’m investing for. But there is nothing that I’m actually benchmarking myself to, to actually see that relative return.

And this is where the word mandate comes in. Just moving into the professional management part, but it applies to retail as well. What is the aim here in terms of the money invested? What is it supposed to do and when? And that translates to how someone actually views the risks that their mandate can actually partake in.

Before this recording, Ghost, we were talking about marriage; weddings. And if my mandate is to actually save and invest for a wedding in six months’ time, my mandate is totally different from if I’m investing for my two-year-old’s varsity fees, for instance.

It’s the same in the professional world, where people are investing in these different unit trusts. Whether you’re talking to a pension fund trustee or a fund selector, what they want in the time horizon is very important, which is influenced by the fact that they would have a mandate for the money that they want to invest.

The mandate actually answers three basic questions which then help with how to actually choose the benchmark. Firstly, what is this money for? Secondly, when does it actually need to be available? And what are the risks that are acceptable in the pursuit of these returns, right?

The wedding in six months versus varsity fees in 16 years example comes in here. Although I think if you have a wedding in six months and you start now, you might be late to the party.

Let’s just look at a pension fund, for instance. They would have long-dated liabilities, right? So future benefit payments. Its benchmark must reflect the duration and also the asset class exposure required to actually match those liabilities over time, right?

If they choose a super conservative benchmark, for instance, they would definitely not be able to actually match those payouts in the future, because there’s inflation and it would have eaten into the real returns of that portfolio.

While if there’s too much risk taken while there’s quite a huge beneficial payout coming very soon, and then the market tanks or something happens in the market, they would fall into the same trap in terms of the payouts.

So, retail clients also face the same challenge on a smaller scale. Someone saving for retirement in 30 years has very different needs from someone who’s preserving capital for property purchase or the wedding example that I made.

So, the benchmark should just reflect the time horizon, the liquidity requirement that talks to when the money is needed, and then the tolerance for drawdowns in terms of what you can take, given that you want to chase the returns that you want.

In other words, the dream must always match the returns and risks profile. So, the risk part is very important to understand. It can be expressed in terms of volatility, tracking error, relative the benchmark, and all those things, as it often does.

But I think it’s very, very important that as a client talking to your fund manager, or as a retail client sitting at home trying to manage your own portfolio, it’s very, very important to just understand firstly what the mandate is, and how that translates to, “Okay, this is what I want to measure myself against” and whether that benchmark actually makes sense.

The Finance Ghost: Lots to think about there. And that’s because benchmarks are confusing things for people who haven’t really dealt with them before, and complex things even for people who have.

And it also gets quite complex when you get into areas like hedge funds, right? Because here they have things like hurdle rates and performance hurdles and that kind of thing, which is not quite the same as a benchmark, because that’s typically how a hedge fund would earn its fees.

Whereas in other types of funds, the benchmark will be just how you measure performance, but not necessarily how they earn a fee. And of course, that is a nuance that people need to understand when they’re looking at fact sheets.

Maybe the other thing to just touch on, Sia, for us is whether or not a benchmark is always an index or can it be something else? Just take us through the differences there between hedge funds and long-only funds and how they think about this stuff.

Siyabulela Nomoyi: The short answer to your question is definitely a no. The benchmark is not always an index. In an index you think about as, “Okay, there’s constituents, create weights for those constituents. And this is the index that I want to follow”.

Yes, a lot of people, including myself, always think of a benchmark as an index that’s made up of constituents. For instance, S&P 500 or the ALBI or just the FTSE/JSE Top 40, for instance, as that index. So institutional investors like pension funds do use non-index benchmarks.

So again here, going back to my liability matching example or what I mentioned previously, is that institutional investors who actually use benchmarks like liability matching, which uses future cash flow projections. So in order to actually manage that part and see if you are successful there, the fund needs to actually always be maintained to track those obligations. It’s very important to just keep track of that.

And of course, the other one would be inflation-linked benchmarks, where maybe there’s like a fixed number or a moving target relative to inflation. So, I’m pretty sure anyone who’s actually listening to this, would have seen funds that target inflation, 3% inflation plus 5 and so on.

So those move with inflation and they change. And then that also influences how an investment manager actually changes their asset allocation to their fund to match how they can actually beat that benchmark.

And the other part is probably some sort of industry or peer group average, for instance. So, an investment manager, for example, let’s say they manage a fund on local equity and then they have an average or the median of the ASISA general equity category as the benchmark. So, they measure themselves versus the peers.

That’s where your question about hedge fund or the hurdle rates that comes in, where in order for them to actually get any performance fees, there should be an amount that actually can go over in terms of their performance, which can allow them to charge the investment fee and then on top of that actually charge the performance fee.

There’s quite a lot of other ways of actually having a benchmark, but it just again fits back to I guess the mandate part that I spoke of previously. And that fits in terms of how you understand or which benchmarks you want to choose for your portfolio.

And also very, very important, especially if you’re someone who… again going back to this performance fee part… if you are someone who’s selecting funds or buying into funds which have that, it’s very important for you as the investor to look at the portfolio and then look at the benchmark and be able to actually evaluate whether that benchmark makes sense.

What’s going to happen there sometimes is that what if that fund manager is always beating the benchmark, then there’s always going to be the performance fee, for instance, and why it actually makes sense, that’s the case.

So, you need to just make sure you understand if that benchmark makes sense. That is a measure for that fund. There’s over 1,600 unit trusts out there to choose from, so you don’t have to stick to one player.

So, if there’s information that you’re not understanding in terms of the benchmark, then you need to evaluate the next one, up until you’re actually comfortable enough to say, this is the fund manager that I want to go with. If you are interested, active management or buying into portfolios that outperform the benchmark.

At the same time, when it comes to the benchmarks that I’ve just mentioned, in terms of fluctuations, they’re linked to a target that’s moving. You should ask: does that make sense in terms of your time horizon and the mandate that you have as well?

The Finance Ghost: Siya, I think the big thing we’re learning today is that the benchmark just needs to make sense in the context of your entire investment strategy and everything you’re actually doing. Because if you don’t understand the risk of what you’re doing, then you’re going to do a really bad job (in all likelihood) of picking a suitable benchmark.

And I will say that ETFs are actually a really good way for people to not just bring market returns into their portfolios, but also just to see how something is performing. Investors can explore the Satrix ETF range to see how different ETFs track various benchmarks and indices. So, I actually do that all the time when I look at a particular stock and I think to myself, “Okay, what would make sense? How would I compare this to, for example, the JSE?”

It’s actually quite easy to go and get a traded price for a Satrix ETF, because the point is, that’s an investable benchmark. As opposed to an index which you can’t actually buy. You need to go and buy an ETF that tracks the index. And then there’s a very small layer of fees, which of course is the Satrix brand promise, to do this as cost-effectively as possible.

And once you subtract that, then you actually get an idea of the investable index, and you can then use that as a benchmark.

Now, you are certainly an expert on indices, you live and breathe this stuff, so perhaps you can just walk us through any other characteristics you want to raise of an index that you would look out for when you’re actually choosing a benchmark.

You’ve already mentioned so many. Is there anything else that you think is worth highlighting for the listeners?

Siyabulela Nomoyi: Sure, sure. Now we’re talking Ghost. That liability matching stuff. Definitely not my area, but ETFs and indices, we can sit and talk about those the whole day. It’s very, very important for clients or investors or anyone who’s listening to actually just understand what that entails.

Because ETFs, they generally just track an index or a benchmark. So as an individual, you can attempt to just track how the certain market performs and not worry about performance. You could just go for an ETF that tracks the JSE capped all share, for instance, for the SA local markets, S&P 500 for the US or the MSCI World. If you’re looking to developed capital markets and so on.

You can’t just wake up and select an ETF blindly, right, for your investments. I would hope not. The ETF you buy into will match back to what your mandate is. Investors looking to access ETFs directly can invest through SatrixNOW as part of their broader investment process. And that mandate helps you to just filter through 140-odd ETFs listed on the JSE, which includes actively managed ETFs.

You need to look at that list and just filter through in terms of what you want. So as an investor, you need to actually be able to read through the index that the ETF tracks, and be able to see if it will give you the exposure that you actually want for your overall portfolio’s needs or the mandate that you have.

But there’s a couple of things that you actually need to look out for. The index should represent the market or the segment or the sector; the country, whatever, that it actually claims to cover. That’s very, very important. So, if the index says China, it needs to give you China. If it’s saying Japan, it needs to give you Japan. Property, it needs to give you property.

A quick example would be FTSE/JSE capped all share index again. So, does that index really give you SA local equity exposure? The answer is yes, because if you’re looking at the fact sheet, for instance, the Satrix capped all share ETF, you’ll see that that index has about 119 stocks in it, right?

But it still gives you a broad exposure to companies that are representing 99% of the total market cap of the JSE-listed companies. So that definitely gives you SA local equity.

So, anyone who’s listening, I think you need to be careful at looking at concentration, especially if you look at broad world indices, which tend to actually have a big skew towards one country like the US. The definition is to also speak to what the exposure gives you.

The other part is actually how the weights (which I guess talks to the concentration part) of the constituents are making up that index that’s being tracked. That part is very, very important.

The most common one will be market cap weighting. So, the biggest companies will be at the top and the smallest will be at the bottom. This has got the practical advantage of reflecting the actual investable universe and keeping turnover low as well.

But it also means that an index can become increasingly concentrated in companies that have already risen sharply in prices, which introduce momentum risk and potential overvaluation bias as well. An index can be influenced by one or two names. Think of the Korean index as well, Kospi, where one or two stocks are actually influencing the volatility of that market.

Something to consider here is that, especially if there’s quite a lot of concentration towards single names, is things like equal weighting schemes or fundamental weighting; think value investing. But my point is that as an investor, you need to actually make sure that you understand the weighting methodology of the index that the ETF that you want to buy into actually tracks.

Ghost. I think very important more for fund managers here as well. The benchmark also is useful if a fund can actually track it or replicate it at a reasonable cost. I was speaking to another interviewer the other day and I mentioned that the JSE has this Africa 30 index, excluding South Africa index, right?

It’s a great index but wait until you actually try and track this by buying the actual companies that are in those different countries. Let’s just say as an investment manager myself, I never want to actually see myself in such a situation ever again. So, it’s very important that you see the definition, you see the benchmark, but it’s also able to actually replicate that.

So, liquidity is very important as well. Otherwise just a terrible way to actually just track the funds.

And I did say I might be all day on this point, Ghost, so maybe let me just close my answer by mentioning that the indices that ETFs track are not static. They rebalance frequently to adjust weights. Some constituents can be added, or they can be dropped from that index, so the ETF actually does the same.

So, the methodology is important to understand as the cost of that fund comes from that methodology. So, if an index is rebalancing way too often and has large turnovers, that’s also going to mean that the running costs are also high.

So, investors, please look at the total expense ratio and transaction costs of the fund that you are looking at; and historically, tracking error of any fund against its stated benchmark. Don’t just look at the headline fees. This is extremely important.

The Finance Ghost: Yeah, I know this is a passion point for you, Siya. And I know full well that you can probably take us through a five-hour podcast series by the end of which everyone will understand everything there is to know about ETFs and benchmarks.

It is something I do really enjoy about you. I love the mention of Korea there. That’s actually an index that has suddenly become really important in the world. Whereas a year ago or certainly two years ago, I don’t think anyone was talking about it. So, as you point out, things do change over time, and that’s why you also have to be careful with which benchmarks you’re looking at, to make sure you’re actually doing a good job of reflecting the kind of things you’re investing in and the risk you’re taking along the way.

Something else I want to ask you then is we talk about beating the benchmark, and people generally see that as a good thing, but is it always a good thing?

So, for example, can it be a bad thing because you maybe took on too much risk, or you actually walked away from your investment mandate?

In an extreme example, if your benchmark is, well, the JSE Top 40, and then you compare your gains from crypto or something to that extent, and you say, “Well, look, I smashed the benchmark”. The benchmark didn’t make sense in the first place.

But are there other examples where maybe you’ve just taken on too much risk or you’ve deviated and that “beat” is actually a bad thing?

Siyabulela Nomoyi: Yeah, definitely, Ghost. That’s part of the reason why I mentioned that if anyone is in the game of looking at fund managers that are charging performance fees, it’s very, very important that they look at the benchmark so that they can actually determine whether that makes sense or not.

Because it might be a benchmark that just completely doesn’t match what the fund or category is in. I know a few of those, but definitely not going to mention them here.

But the most fundamental pitfall is choosing a benchmark that does not match the actual objective. As an investor, you have the mandate, but then you choose the wrong benchmark for that.

The wedding and university fees example still applies, but outside that, sometimes investors actually tend to adopt a widely used index out of the convenience rather than the alignment.

And the reason why I’m saying that the wedding and varsity fees example applies is that the wedding is in six months or 12 months versus your child is going to go into varsity in 16 months. Your mandate is totally different for those two, which means you need to just make sure that you benchmark it to the right one.

Otherwise, if you think that you’re beating the benchmark, but it’s really not matching the outcome that you want, then you’re not really investing in the right place that you want to be investing in.

It can be the right thing. But outside that part, sometimes investors actually do tend to adopt widely used indices. And the problem is that it’s just convenient, right? You just look at other people or what’s the most widely used benchmark and you just adapt to that.

So as an investment manager, you might end up performing very, very well against that benchmark, but you might fail to serve the investor’s real needs, which is a big problem.

You can go to a presentation to a client and tell them, “Look, I’ve done really, really good. I’ve done positive returns for the last 10 years and I’ve given you 3% over those 10 years every year”.

But my target was inflation and looking at the inflation numbers, there’s a problem there, right? Having done exactly what I needed you to do in terms of the money that I gave you.

So, it’s same as your retail investor, you might be happy with what you see in terms of returns. Yet in terms of your mandates, something else is actually just brewing and it’s not exactly matching up to what you need.

But there’s also another side to that where if you are an active manager or a stock picker, for instance, you might also be hugging the benchmark on the fear of just blowing out your tracking error. Or maybe previously you were underperforming so you more on the side of not taking more risks. You literally just hug the benchmark in terms of your positioning. So, you take bets close to the index.

Now that would not be fair, right? Because you might as well be just tracking the index. And especially if you’re someone who’s sold themselves as a stock picker or an active manager, that means that you are probably charging more than someone who’s tracking the benchmark.

And if I go to you and you’re giving me exactly the same as the benchmark or quite close to, it while you’re charging two or three times the fee, then it’s definitely not fair. And I went to you because you can pick the winners for me.

The Finance Ghost: So much wisdom, Siya. Thank you very much for sharing it.

As we start to bring this to a close (and you’ve given us so much to think about in terms of good stuff and bad stuff around benchmarks: where it goes wrong, all of that kind of thing, we’ve touched on a lot of that); anything else you want to raise there around where things can actually go wrong in terms of choosing a benchmark? Or do you feel like you’ve landed all the key points?

Siyabulela Nomoyi: I think I’ve covered quite a lot of that.

Also, a well-constructed benchmark should offer meaningful diversification. That part is very important. When it comes to a handful of securities, or even a single company accounting for a disproportionate share of the index weight, then the investor is taking on the concentration in a single name.

It’s very important to just make sure that you understand, and you know that it is well constructed. Once you understand the benchmark, Ghost, you then automatically understand the ETF landscape, especially in South Africa, where you have to dive into a pool of 100 ETFs which track around 60 indices. They’re coming from eight different ETF providers.

You don’t want to be the guy who’s holding four Top 40 ETFs just because you’re just understanding what those indices are. So, benchmarks are quite powerful tools, Ghost. And as a fund manager, I need to make sure that I give you access to the benchmark returns and you get to as close to that as possible.

And also from your side, you need to make sure that we are able to evaluate my performance as well, relative to something. So that’s very important on both sides.

The Finance Ghost: Siya, thank you. I think we can safely leave it there. I think we’ve covered off a really important point here, which is that ETFs give you excellent access to an investable benchmark.

And if you go and understand the ETF universe, and you go and understand the underlying risk and reward characteristics of what you’ll find in each of these benchmarks, each of these indices, then you’ll be so far down the road in understanding the ETFs as well.

And I would obviously encourage listeners to go and check out the Satrix offering, which is incredibly broad. There really is just about something for everyone there, both locally and offshore.

And of course it’s all here on the JSE. So even when it’s an offshore benchmark or offshore index that they are tracking, it’s an investable instrument right here at home on the Johannesburg Stock Exchange.

Siya, thank you so much as always, for your time on what I know has been a particularly challenging day. I look forward to doing the next one with you as always.

Siyabulela Nomoyi: Awesome, Ghost, thank you so much, hey.

Disclaimer

Satrix Managers (RF) (Pty) Ltd is a registered and approved Manager in Collective Investment Schemes in Securities. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts, Exchange Traded Funds (ETFs) and Actively Managed ETFs (AMETFs), the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of ETFs and AMETFs, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs and AMETFs are registered as a Collective Investment and can be traded by any stockbroker on the stock exchange, LISP platforms and / or via online trading platforms. ETFs and AMETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance, and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions is available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF and AMETF Minimum Disclosure Document. AMETFs are ETFs are actively traded by a Portfolio Manager to adjust the AMETF holdings and asset allocation with the aim to outperform the benchmark. AMETFs differ from ETFs which only track indices. The Manager does not provide any guarantee, either with respect to the capital or the return of a portfolio. The index, the applicable tracking error and the portfolio performance relative to the index can be viewed on the ETF and AMETF Minimum Disclosure Document and/or on https://satrix.co.za/products.

Signs of life at Metair as multiple restructuring efforts take hold

Telkom’s first quarter is a strong foundation for the rest of the year

Datatec expands further in the US (JSE: DTC)

Cybersecurity is a juicy area at the moment

Datatec is a local company with an excellent global strategy. This is one of very few examples of South African companies that have successfully expanded offshore.

This strategy still has plenty of runway, evidenced by the announcement of a new acquisition in the US.

Datatec’s subsidiary, Logicalis USA, has acquired 100% of the share capital of Loial, a cybersecurity and managed services company operating in New Mexico. This expands the Southwest team in the US.

The deal is too small to be categorised, so no further details are given around numbers etc. When it comes to the US though, even a regional specialist can be a business of significant scale.

Ghost Bite: Datatec’s total return over three years is 181%. They know what they are doing when it comes to offshore deals.

Signs of life at Metair as multiple restructuring efforts take hold (JSE: MTA)

AutoZone has also achieved some profitable months

I regularly refer to Metair as the unluckiest company on the market.

They are trying to navigate the disruption of their OEM automotive manufacturer base by Chinese brands. They are dealing with huge fines in Europe that deal with issues from a time before they even owned their battery assets in that region. Heck, they’ve even had to survive floods at a major local customer in KZN!

The company deserves a break. Truly. If the latest trading statement is anything to go by, they might finally be getting it!

If you aren’t familiar with the company, the main thing to remember about Metair is that they are primarily focused on new car manufacturing in South Africa. They have other businesses and they are pushing harder into aftermarket parts, but that’s still the main focus of the business.

Now, bulls might be tempted to point to the strong growth in new car sales in South Africa as a source of revenue, as the company supplies manufacturers like Ford and Toyota with components for local manufacturing. But the problem is that the growth is coming from Chinese and Indian brands that are manufactured elsewhere. This was one of the major talking points when we hosted Metair on Unlock the Stock a few months ago:

In terms of export sales, local manufacturers are also struggling due to the impact of those new brands in export markets. Export sales fell by a nasty 7.8% year-on-year. Overall, local industry production was flat, with domestic sales helping to offset the export impact.

For Metair specifically, lower volumes from one customer were offset by growth in other customers. Revenue and EBIT increased marginally, with the latter benefitting from efficiency initiatives and the inclusion of Hesto for the full six months of the interim period.

If we dig deeper, the OEM revenue (including Hesto) increased by between 3% and 6%. EBIT margin came in slightly ahead of the prior period’s 7%. Hesto’s revenue is expected to decline by 15% to 20%, with EBIT margin expected to dip by between 1% and 2% due to lower volumes.

Then, in Aftermarket Parts and Retail Africa, revenue is expected to increase by between 5% and 7%. AutoZone is making progress on its turnaround, but First Battery is struggling. AutoZone was still loss-making for this period overall, but became profitable from May onwards (six months behind the initial plan). Rombat (the European battery business) is expected to manage steady EBIT, despite revenue decreasing by 20% to 25%.

We then move on to the balance sheet, where the extent of debt has historically driven many a sleepless night for both Metair and its bankers.

In May, Standard Bank approved a refinancing of the debt package within the South African subsidiaries (excluding Hesto). The term of the R3.3 billion in debt has been extended to five years. As leverage comes down, the interest rate will also ratchet lower.

This is one of the snowball effects in a turnaround story where debt is involved. As debt comes down, financial risk reduces and the cost of debt comes down as well. This has a significant positive effect on interest costs in years to come.

Overall, they expect HEPS from total operations for the six months to June to have increased by between 7% and 15% for the period. From continuing operations (which excludes Dynamic Batteries and First Battery Industrial division), HEPS increased by between 3% and 11%.

The HEPS from continuing operations range is between 70 cents and 75 cents, putting the share price on a P/E multiple of roughly 6.8x.

Despite an underlying feeling of improvement, there’s still never a dull moment at Metair. Due to restructuring activities at First Battery, NUMSA implemented a strike from 6 July until 23 July. That obviously isn’t captured in the numbers for the period ended June.

And although the €20.2 million fine in Europe has been fully provided for by Rombat, they are still appealing the fine. My understanding is that instalments become payable in the meantime anyway. It seems like a long shot that they will have any success in squashing it.

Ghost Bite: This is the most promising update I’ve seen from Metair in a very long time.

Telkom’s first quarter is a strong foundation for the rest of the year (JSE: TKG)

The prepaid and data growth engines are firing on all cylinders

Telkom has released a promising set of numbers for the quarter ended June 2026. There are some impressive growth engines powering this story, although group revenue growth remained modest at 2.6%

Within that number, we find a winner like group data revenue (up 8.8% and now contributing 62.4% of total revenue). Fibre-related revenue was up 4.0% and mobile data revenue rose by 11.4%.

Another critical area is prepaid service revenue growth of 9.1%. The prepaid market has been a competitive bloodbath recently, with Telkom giving the leading players a lot to think about in their home market. Total service revenue in Telkom Mobile grew by 6.4%.

The story gets more interesting when you consider profitability. Group EBITDA increased by 10% and EBITDA margin expanded by 180 basis points to 27.7%. Double-digit growth in EBITDA is impressive in a South African telcos market that is largely seen as being mature.

Telkom Mobile deserves another mention here for its performance in a competitive market, with EBITDA margin expanding by 270 basis points to 29.1%!

There’s also good news for free cash flow, with group capex down 19.4%. Capex intensity (capex as a percentage of revenue) improved from 10.2% to 8.0%. Achieving revenue growth with less capex means that there’s more cash flow for shareholders. Be warned though: Telkom has indicated that capex spend will be ramped up for the remainder of the year. They expect intensity to run between 12% and 15%.

It can’t all be good news, of course. BCX remains a difficult story with ongoing revenue pressure. Cybersecurity and cloud services might be on the up, but the legacy areas of BCX have dragged revenue down by 10.9%. Due to management initiatives, EBITDA still managed to increase by 2.6%. EBITDA margin remains painfully low at just 7.5%.

A lesser known fact about Telkom is that it’s lucrative to be their conveyancing attorneys. The group sold a whopping 100 properties during the quarter, with a further 105 properties in the conveyancing process! We are talking about R464 million in properties overall.

Looking ahead, Telkom will continue to find pockets of growth in the Telkom Mobile business. They are targeting underindexed and underserved regions, with service revenue expected to grow by mid-single digits. Having just grown the prepaid subscriber base by an impressive 7.1%, this is a strategy that is clearly working.

Ghost Bite: Despite all this progress, Telkom’s share price is down 4.7% over 12 months. The big money in this turnaround was made in early 2025, with the earnings now growing into their new boots.

Nibbles:

Director dealings:

A non-executive director of British American Tobacco (JSE: BTI) bought shares worth £247.5k (around R5.5 million)

The company secretary of Vodacom (JSE: VOD) sold shares worth R1.5 million.

A senior exec at Sirius Real Estate (JSE: SRE) and a closely associated person received shares worth £30.8k as part of the company’s dividend reinvestment plan.

A non-independent, non-executive director of Southern Palladium (JSE: SDL) bought 20,000 shares in an off-market deal with a family member. In theory that’s fine, but not if the correct process isn’t followed to get clearance for the transaction during a closed period. The director was suitably rapped over the knuckles.

Lesaka Technologies (JSE: LSK) shareholders have approved the grant of stock options to Executive Chairman, Ali Mazanderani. This is part of the broader efforts by the company to retain Mazanderani’s services for the next few years. The options cover 1 million shares at an exercise price of $5 per share. The current share price is R79, so these options are out-of-the-money on day 1 (as they should be). They vest in April 2028 and would be exercisable after April 2029. This gives him a few years to play a role in making these options as valuable as possible. The idea is obviously to align the execs with shareholders as far as possible.

Mfundo Nkuhlu is retiring from his position as COO of Nedbank (JSE: NED), having been with the bank since April 2004. That’s a 22-year innings that certainly deserves a proper farewell party! Interestingly, Nedbank will not replace him. Instead, the COO role will be discontinued and the responsibilities will be reallocated within the existing group exco structure.

Accelerate Property Fund: a cleaner balance sheet, but will the market care?

Hammerson is doing well – and raising capital accordingly

Hyprop has closed the acquisition of Galleria Burgas

Primary Health Properties lives up to its defensive promise

Stor-Age adds some Xtraspace to its portfolio

Accelerate Property Fund: a cleaner balance sheet, but will the market care? (JSE: APF)

Turnarounds are so tough

Accelerate Property Fund is one of the few exceptions I’ve made in my life when it comes to speculative stocks.

I generally avoid companies that have particularly high risk factors. With Accelerate, I got myself across the line through a combination of the underlying property exposure, the progress made in saving the balance sheet and the discounted share price relative to the assets.

The thing that I didn’t do was sell the shares when they climbed significantly in value. I tend to be much better at buying shares than selling them. I’m working on getting better at this. After all, nobody said investing was easy!

My position is still in the green, but not by much. This begs the question: should I be buying more?

There are a number of encouraging elements in the results for the year ended March 2026. For example, Accelerate sold four properties and vacant land for R788.5 million. Subsequent to the end of the reporting period (which was a few months ago), they’ve disposed of further assets for R278.2 million. This has done good things for the balance sheet.

With so many disposals of properties, looking at the movement in total revenue doesn’t make sense. It’s better to look at like-for-like revenue, in which case rentals were up by 1.4%. That’s not exciting, but it’s better than you would expect to see in a battered property company.

Accelerate doesn’t give such user-friendly disclosure when it comes to expenses. Property expenses were lower, but that’s impacted by disposals as well. It does look like they’ve made progress on reducing central costs as well, like professional fees.

Here’s more good news: vacancies have decreased from 19.4% to 10.9%. Once the post-period disposals are considered, vacancies are down at 8.4%. Notably, Fourways Mall saw vacancies decrease from 13.7% to 9.7%, while trading density increased by 8.4%. Recent letting is expected to take that vacancy rate closer to 5%.

Finance costs are critical to consider. Thanks mainly to asset disposals (R777.3 million was used to reduce debt), finance costs on interest bearing borrowings fell by 16.1%. The average cost of funding also helped, as this improved from 10.9% to 9.9%. Notably, a R50 million rights issue funded a R39.6 million capex bill at Fourways Mall. The rest was applied to working capital needs.

Looking ahead, the current funding facilities mature at the end of March 2027. The group has made a lot of progress, so I hope that negotiations with lenders will go well. The loan-to-value ratio has improved dramatically from 48.3% to 43.7% over the past 12 months.

The balance sheet isn’t out of the woods yet, so I’m not surprised that there’s no dividend for the period.

The more controversial element of these results is the fight with Azrapart, the entity linked to Michael Georgiou. This is a long and sordid tale that includes multiple agreements and even a business rescue process. The complexity is that there have been both assets and liabilities on Accelerate’s balance sheet related to this mess. The original plan to achieve a settlement of everything was much cleaner than where we stand today, as there’s a chance that either the asset or liability could be triggered (or both – or neither!). Uncertainty is never fun for investors.

In the prior year, Accelerate impaired the related party balance by R970.7 million, although they are still pursuing the claim. They took the conservative approach of keeping the R300 million liability on the balance sheet, so FY25 saw quite the mismatch on this issue. For FY26, they’ve now derecognised the liability of R300 million.

This means that the net asset value per share of R1.81 is arguably the cleanest it’s ever been. But it also means that there’s risk of a legal surprise putting a stain on the numbers. Technically, there’s potential for upside from the legal battle as well.

Ghost Bite: The current share price is R0.43, which puts this R920 million market cap fund on a price/book of around 0.25x. It’s trading close to 52-week lows. I’m not blind to how tough things are for consumers right now, but I’m very tempted to buy more.

Hammerson is doing well – and raising capital accordingly (JSE: HMN)

Footfall is growing in busy UK city centres

Hammerson, the UK-focused property fund, has had a very busy few days.

Towards the end of last week, they released results and announced an intention to raise up to £190 million in fresh capital for an acquisition. To give you context, that’s around 10% of existing share capital.

The acquisition in question is a 50% interest in Manchester Arndale, giving the fund exposure to the largest catchment area outside of London. The net initial yield based on the purchase price is 7.8%. This is in line with Hammerson’s strategy to focus on busy city centres where they can achieve growth in footfall, despite the obvious disruption of online shopping.

The placement was structured in such a way that space was made for both institutional and retail investors in the UK. I wish we saw more of this in the South African market. As a strong show of support in the raise, the CEO and CFO signed up for a combined £230k worth of shares.

The capital was raised through the placement of shares at 355 pence per share, representing a 3.8% discount to the closing price on 29 July. That’s a bigger discount than I’ve seen in recent raises by South African REITs, but I think that the UK institutional market is a tougher place to raise capital. South African institutions love throwing money at REITs at almost any price.

Alongside the push to raise fresh capital, Hammerson also released interim results for the six months to June 2026. This is where they reinforced the messaging around strong occupancy rates and growth in footfall in busy cities. Like-for-like net rental income was up 5% and the interim dividend jumped by a juicy 22%.

With the balance sheet in good shape (loan-to-value of 39%) and the portfolio performing well, Hammerson felt confident enough to increase the earnings guidance for FY26 to reflect expected growth of 27%. They have also updated medium-term guidance, with an expected compound annual growth rate (CAGR) in the dividend per share of 6% – 8%.

Ghost Bites: None of this timing is by accident. By waiting for the release of results to trigger the capital raise, Hammerson was able to take fresh (and positive) information to the market.

Hyprop has closed the acquisition of Galleria Burgas (JSE: HYP)

On the other side of this deal, we find MAS (JSE: MSP) as the seller

Back in May, Hyprop announced the acquisition of Galleria Burgas in Bulgaria. As those who follow Hyprop closely will know, the company has interests in Eastern Europe in addition to the South African portfolio of iconic shopping centres.

The underlying property was valued at €122.2 million. Due to the debt in the entity that holds the property, the purchase price of the shares was only €53.5 million. This is essentially the net asset value of the company that Hyprop has acquired.

The seller is MAS, the property company that is making a lot of noise about not really being a property company anymore. MAS has just reconstituted its various board committees. It’s anyone’s guess what assets they will buy going forwards.

Ghost Bite: Hyprop is sticking to its knitting with this deal. Nobody really knows what MAS is up to!

Primary Health Properties lives up to its defensive promise (JSE: PHP)

Despite all the macroeconomic noise, the portfolio is solid

Primary Health Properties has released an important set of financial results. The interims for the six months to June 2026 reflect the combination of this company with the business of Assura. You may remember that merger process how Primary Health had to beat off other potential buyers.