")

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Attacq and Hyprop found a buyer for the African assets (JSE: ATT | JSE: HYP)

The properties are in Nigeria and Ghana, with both local funds having been co-invested in them

After a week of plenty of South Africa vs. Nigeria noise on local social media, we saw another breaking of ties here – thankfully not in the form of a over-hyped beauty pageant. Attacq and Hyprop are both disposing of their stakes in Ikeja City Mall in Nigeria and three malls in Ghana, namely the Accra Mall, Kumasi City Mall and West Hills Mall.

The buyer is Lango Real Estate Limited. This is important information when you see how the deal is structured.

You have to read quite carefully to figure out the apportionment of value. Attacq holds 25% of the shares in the Nigerian holding company, with Hyprop holding the other 75%. On the Ghanaian side, it’s a bit more complex. Attacq and Hyprop hold 50% of the shares in the holding company, but their economic interests are actually 73.12% and 26.88% respectively. In turn, that holding company has various stakes in the malls in Ghana.

With respect to the Nigerian disposal, the total disposal price of $32 million is apportioned as $24.1 million to Hyprop and $7.9 million to Attacq. For Ghana, the total price of $27.3 million will be apportioned as $20 million to Hyprop and $7.3 million to Attacq.

But here’s the trick: the amounts are settled in shares in Lango, not in cash. 20% of the received shares will be held in escrow until the earliest of 30 June 2025 or six months after the deal is completed. This is surely a better outcome than holding those problematic properties directly, but it’s not a clean break. We will need to see if the funds can monetise these holdings.

Attacq will hold 4.3% in Lango after these deals and has confirmed that it doesn’t intend to hold the shares for the long-term. Hyprop also doesn’t intend to hold the shares and hasn’t indicated the percentage that will be held, but we can safely assume that it will be around 13%.

Aveng has swung into profitability (JSE: AEG)

We don’t know how big the profits are yet, but there are profits

Aveng has released a trading statement for the year ended June 2024. It’s a fun one, as there’s no percentage move indicated. Instead, the great news is that the group expects positive HEPS for the year vs. a headline loss per share of A$61.6 cents in the comparable period.

They do give further details on the underlying segments. McConnell Dowell, which operates in Australia, New Zealand and the Pacific Islands and Southeast Asia (i.e. where there used to be rugby teams capable of beating us), expects to see a year-on-year improvement. They highlight strong cash flows, which is important. The Building segment also operates in that part of the world and expects growth in revenue. Across both of those segments, work in hand has come off peak levels. The third segment is Mining, which operates in South Africa as Moolmans. Operating earnings have been under pressure there, with only marginal profitability expected.

The group is sitting on a net cash position of A$173 million, with previously reported term debt at McConnell Dowell settled during the year.

Investment bankers have been appointed to assist with a strategic review of the business. This suggests that more corporate activity could be on the horizon, as such bankers aren’t famous for suggesting “do nothing” as a strategy.

Results are due on 20 August.

Brait’s rights offer was well supported (JSE: BAT)

The underwriter wasn’t needed in the end – but there was some very clever structuring

Hot on the heels of a strong outcome for the rights offer at Pick n Pay, we have news of another rights offer that the market was happy to throw money at. Brait managed to get 96.1% of the available shares away to shareholders following their rights, with the remaining 3.9% going to those who put in excess applications.

Excess applications were equivalent to 66.1% of the total shares being offered, so there was plenty of headroom before the underwriter would’ve been needed.

The underwriter was one of the Dr. Christo Wiese entities and would’ve been quite happy to take up more shares I’m sure. Fascinatingly, to avoid a scenario where a mandatory offer would’ve been triggered with approval timelines that would’ve been problematic for the rights offer, Standard Bank had acquired legal ownership of Titan’s stake in Brait and entered into a total return swap with Titan. As Titan now holds a 37.4% economic interest in Brait after the excess applications went through, the unwind of this swap is presumably going to trigger a mandatory offer when the voting rights revert to Titan. That sounds like a rather cute legal solution that no doubt had a strong legal opinion sitting behind it in terms of Takeover Law.

More growth at CA Sales Holdings (JSE: CAA)

This is such a solid company

CA Sales Holdings has released a trading statement dealing with the six months to June. Unsurprisingly, given the recent performance of the company and the coherent strategy, the trading statement has been triggered for the right reasons.

HEPS will be up by between 17% and 22%, with the company highlighting that there has been organic growth across all the operations. In a group that has built a reputation for bolt-on acquisitions, this is really good news. There’s nothing better than an acquisitive strategy accompanied by solid organic growth i.e. growth in the underlying businesses that were previously acquired or built.

Detailed results are due on 2 September. The share price is up 30% this year and over 80% in the past 12 months!

Castleview’s listed subsidiary Emira must have had FOMO over the Poland opportunity (JSE: EMI | JSE: CVW)

I’m just not sure why they are doing it with indirect exposure rather than direct property deals

I get nervous when I see listed funds buying up non-controlling stakes in other funds offshore. What is the point, exactly? If institutional investors are looking for that kind of exposure, they can usually achieve it directly. The inevitable outcome of layered exposure is that the stake just trades at a discount to true underlying value.

Despite numerous examples of this happening in the market and being reversed years later in expensive “value unlock” transactions, Emira has now dived into a 25% stake in DL Invest, a property fund headquartered in Luxembourg and focused on Poland. Emira has the option to take this stake to 45%, which is just a very large non-controlling stake.

The DL Group has 50 properties in Poland across various types, with a 17-year track record. There’s little doubt that they are proper operators. It’s just the underlying rationale for the deal that is questionable for me.

The transaction structure sees DL Invest issuing B shares and loan notes to Emira for €55.5 million. The option to take the stake to 45% is also for equity and loan notes. Emira has until January 2025 to issue an exercise notice, so this option doesn’t even have much time value to it.

I find it hard to believe that this is the best way they could have gotten exposure to the Eastern European growth story.

And remember, Castleview (which is separately listed) holds 59.3% of Emira. There’s very little liquidity in Castleview though, as the shares are tightly held.

Gold Fields wants full ownership of the Windfall Project (JSE: GFI)

It’s an exciting name, if nothing else

Gold Fields currently holds a 50% interest in the Windfall Project in Canada alongside Osisko Mining, a company listed on the Toronto Stock Exchange. It won’t be listed for much longer it seems, as Gold Fields wants full ownership of the Windfall Project and has made a cash offer for all the listed Osisko shares at a price representing a 55% premium to the 20-day VWAP.

There’s a windfall alright – for the shareholders in Osisko, at least.

Gold Fields points out that the deal extinguishes certain liabilities related to the 2023 joint venture transaction, like a deferred cash payment and exploration obligation. I guess one way to extinguish a C$375 million obligation is to buy the company you owe for C$2.16 billion instead.

Jokes aside, there’s obviously a strategic rationale here around controlling an asset in a tier-1 mining jurisdiction. But after disappointing production numbers recently, I suspect that Gold Fields shareholders will probably be more interested in seeing operational improvements at the company rather than another deal – especially when Gold Fields needs to tap into bank funding to execute this deal. As if that isn’t risky enough, this isn’t even a producing asset yet. The Windfall Project is still being developed.

Another tough year for Italtile – but signs of improvement (JSE: ITE)

The second half was better than the first half, unsurprisingly

Like sector peer Cashbuild, Italtile is trying to claw its way back after an incredibly tough couple of years. A trading statement for the year ended June 2024 is a reminder that things only got a bit better very recently, with most of that year suffering through high levels of load shedding, poor consumer confidence and high interest rates. At least two of the three issues have largely gone away, with the third one hopefully improving soon.

Much as we can hopefully look forward to a better performance going forward, that doesn’t do much to save the financial year that just ended. HEPS fell by between 4.7% and 10.3%, which is pretty decent under the circumstances. Coming in at 118.7 cents to 126.2 cents, the mid-point suggests a Price/Earnings multiple of around 9.2x. With good reasons to believe that things will get better next year, that’s starting to look interesting.

Against a backdrop of full-year retail sales being down 4.7% and like-for-like sales down 2% vs. price inflation of 2.1% (i.e. volumes were slightly negative), the silver lining is that the second half was better than the first half. This is the momentum that needs to continue into the new year, along with improvements to gross margin after Italtile suffered a 260 basis points gross margin contraction in this financial year.

Another element of Italtile that is important to remember is that the group has manufacturing operations that are severely impacted by poor volumes due to the inherent fixed costs. If things improve, Italtile should get a strong upswing in that part of the business.

Merafe doesn’t have a rosy outlook for the year (JSE: MRF)

It’s a pity that a weak first half isn’t expected to get better in the second half

For the first half of the year, Merafe experienced a 17% decrease in ferrochrome production. Thanks to better chrome ore prices, revenue was only down by 0.4%. Sadly, cost pressures ensured that HEPS was far worse than that, down 33% to 28.2 cents.

Interestingly, perhaps because of the headroom in the payout ratio, the interim dividend held steady at 20 cents per share. The maintenance of the dividend at this level is made even more interesting by the expectation of a weaker second half, with downward pressure on chrome ore prices and thus the likelihood of margins being squeezed.

Montauk’s interims look good, but watch out for Q2 (JSE: MKR)

The good stuff happened in Q1

Montauk has released its numbers for the second quarter and thus the six months ended June. Over six months, it looks great. Revenue is up 13%, EBITDA increased 57% and HEPS jumped from a loss to a profit. What’s not to love?

It’s not quite so simple when you consider the second quarter (Q2) though, where revenue fell, expenses were higher and the company made a net loss rather than a net profit.

This group is headquartered in the US and focuses on Renewable Natural Gas (RNG) and Renewable Electricity. They put very little effort into their SENS announcements, so you’ll have to work through the detailed US filings if you want to know what’s going on there.

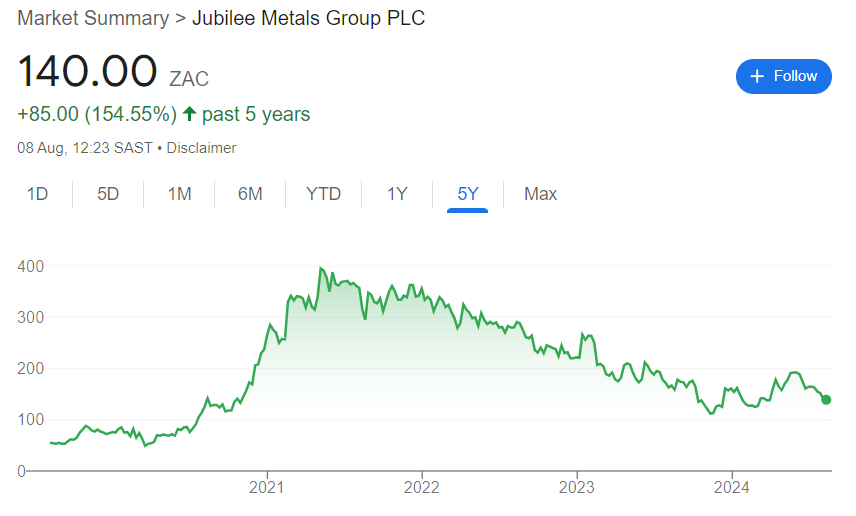

Renergen finally gives investors the news they’ve been waiting for (JSE: REN)

The stock rallied 28.5% before the market calmed down a bit

For those with the patience to believe in Renergen, there’s finally been some reward. I think it’s important to put this rally in context, as the share price has taken immense strain in the past year:

In fact, if you really want to see how frothy Renergen got before the market got cold feet and started to run away, here’s a five-year chart:

When you invest in exploratory companies, you need to be ready for immense volatility along the way. Most of all, if you buy when there is clear hype around the stock, you’re taking the most risk possible.

After a long delay in getting helium production online, the company has now announced that the OEM has handed over the keys to a fully operational liquid helium production plant. They’ve been producing helium since 19th July and the first customer Iso-container is scheduled to arrive later this month for filling.

Now the hard work really begins, as the market will start to look at the financial performance of the plant. Don’t forget that there’s still a long journey ahead until this can be considered a moderate risk investment. They need to raise capital, develop the project and get to maximum production.

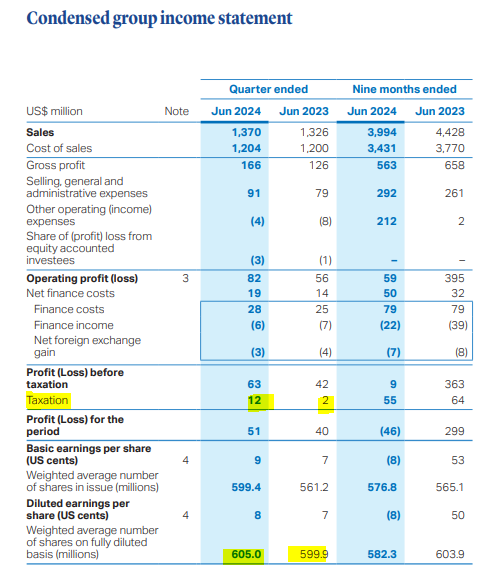

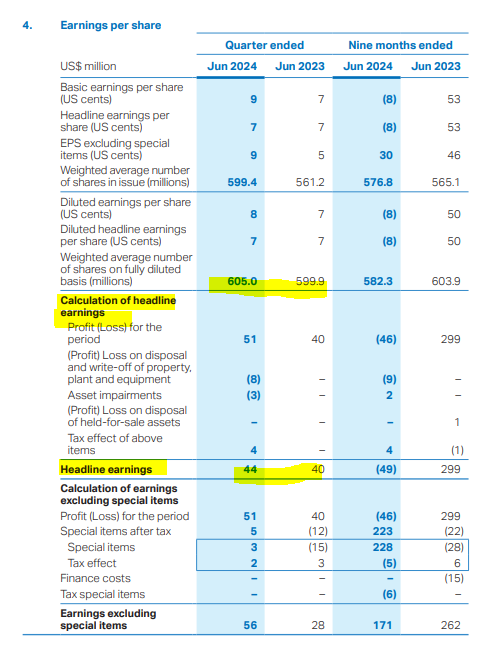

A substantial drop in profits at Sasol (JSE: SOL)

It feels like they are taking every impairment possible in this period

After releasing the annual production and sales report towards the end of July, Sasol has now released a trading statement dealing with the year ended June. The numbers were never going to be good based on what we’ve seen from the company in the past year. Adjusted EBITDA has declined by between 2% and 17%, driving a decrease in core HEPS of between 9% and 27% for the period.

The core HEPS number benefits from various adjustments that go beyond the traditional HEPS calculation. Without those adjustments, HEPS is down by between 59% and 77% – a much nastier result.

The basic loss per share is where you’ll find the result of throwing the kitchen sink at this period, as Sasol has recognised enormous impairments that led to a basic loss per share of between R68.82 and R71.48 for the period. This type of approach isn’t unusual when new leadership is in place, as they like to create the worst possible base off which to tell an excellent story of improvement. Either way, they have impaired the Chemicals business by a whopping R45.5 billion in America and R3.9 billion in South Africa. The Secunda liquid fuels refinery business was impaired by R5.7 billion and is fully impaired as at the end of June. These numbers are all net of tax. They’ve also derecognised a deferred tax asset of R15.3 billion related to Chemicals America.

Detailed results are due for release on 20 August. Have we finally reached the bottom for Sasol?

Super Group takes a major knock to earnings (JSE: SPG)

The market didn’t enjoy this update

Super Group released a trading statement for the year ended June 2024 and it makes for unpleasant reading. Revenue might have increased by up to 10%, but that hasn’t translated into a good news story at operating profit level. It only gets worse when you reach HEPS.

Operating profit before capital items will be lower by up to 10% vs. the comparable year. HEPS will be down by between 20% and 30%. As for earnings per share, which is impacted by impairments, the group is now loss-making.

To understand these numbers, we need to look deeper into the operations. Super Group has a variety of business units that operate independently, so the group result ends up being driven by the mix effect further down.

In Supply Chain Africa, they are negatively impacted by the significant decrease in coal export volumes and the general state of things at South African ports, which are now losing volumes to competing ports like Dar es Salaam and Walvis Bay. The market doesn’t care about South Africa’s sob stories on infrastructure issues. If we don’t get it right, our economy will continue to suffer. Super Group is exposed to coal miners that are financially distressed, like Wescoal Mining. It’s a really unfortunate situation.

In Supply Chain Europe, the business was hit by a decline in automotive parts distribution volumes and lower gross margins due to excess vehicle capacity in German. Combined with higher interest rates, this was a tough period for the business. inTime Germany has been impaired and is being “right-sized” for the economic conditions.

In Dealerships UK, Ford has lost market share and has made decisions that have impacted sales performance. This is why I far prefer a model like WeBuyCars (JSE: WBC) that isn’t beholden to the whims of a global manufacturer. When you own Ford dealers, you have minimal control over your own future. Combined with margin erosion in used vehicle sales and higher net finance costs, this was a period to forget.

There aren’t exactly any silver linings here, are there? The detailed results will be released on 11th September.

Little Bites:

- Director dealings:

- The selling by Richemont (JSE: CFR) directors continues, with two directors selling shares worth a total of R78 million. With everything going on in China, I wouldn’t ignore this.

- A senior manager of Investec (JSE: INL | JSE: INP) sold shares worth R15.2 million.

- An associate of a director of Acsion Limited (JSE: ACS) bought shares worth R660k.

- For the third time in the past few weeks, a director of Zeda (JSE: ZZD) has sold shares in the company. This time, the sale was worth R310k.

- Acting through Protea Asset Management, Sean Riskowitz bought shares in Finbond (JSE: FGL) worth R284k.

- Southern Palladium (JSE: SDL) has submitted the Environmental Impact Assessment report to the Department of Mineral Resource and Energy (DMRE) for the 70%-owned Bengwenyama PGM Project. This is an important milestone for the project. The DMRE acknowledged the submission, which means they will move forward with a detailed review of it.

- Following the retirement of David Nurek as chairman of Clicks (JSE: CLS), the company has announced that JJ Njeke has been appointed as the new chairman. He has been the lead independent director since 2022.

")

")

")