In this episode of Ghost Stories, Siyabulela Nomoyi returned to the platform once more to talk about two exciting product launches at Satrix.

Of course, The Finance Ghost couldn’t resist kicking off the show with a question around whether Siya stuck to his festive season savings goals that were discussed at the end of 2023 in a previous episode!

Moving on to all things ETF related, topics of discussion included:

How Satrix approaches the product design process.

An overview of the Satrix MSCI ACWI Feeder ETF and specifically how it differs from the MSCI World Index in giving efficient exposure to developed and emerging markets.

An overview of the Satrix JSE Global Equity ETF and how this gives investors an opportunity to tilt their portfolios towards locally-listed companies with more international exposure.

Related to the Satrix JSE Global Equity ETF, an important discussion on JSE index harmonisation.

Variability in ETF costs and what the building blocks of those costs are.

There’s so much in here, underpinned by Satrix’s commitment to South African investor education. To find out more about SatrixNOW, visit this link>>>

Listen to the show here:

>

Disclosure

Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Anglo American to bulk up the Minas Rio asset in Brazil (JSE: AGL)

This announcement accompanied the results for the year ended December 2023

Let’s get the news of the deal out of the way first. Under the terms of the Minas Rio deal that Anglo American has agreed with fellow mining giant Vale, the latter will contribute Serpentina and $157.5 million in cash to acquire a 15% shareholding in the enlarged Minas-Rio operation, so this is really a merger of the two assets to create a much larger iron ore operation. Vale will have the option to acquire an additional 15% shareholding in the enlarged asset if certain events linked to future expansion occur.

There is a formula that could lead to an adjustment to the purchase price if the four-year average iron ore price is above $100/t or below $80/t.

The benefit to the parties? Scale and synergies, of course, along with shared infrastructure.

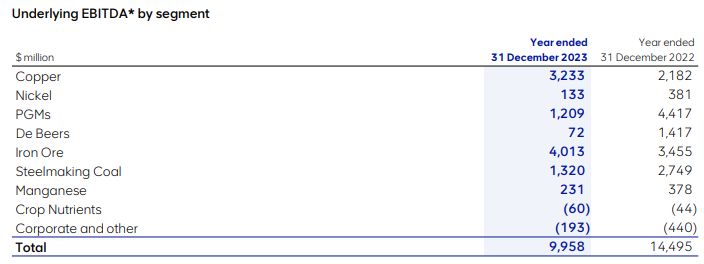

Now, we move on to the results at Anglo American for the year ended December 2023. The good news is that Quellaveco is fully ramped up and producing copper. Other good news is that Anglo American is on track to reduce annual costs by around $1 billion over the next three years. The bad news is that underlying EBITDA fell 31% in 2023, with PGMs and diamonds taking the shine off the numbers.

HEPS is down 59% to $2.06 from $4.98 in the comparable period. A 40% payout policy has been maintained, which means a dividend of $0.96 per share.

The results in subsidiaries like Anglo American Platinum and Kumba Iron Ore can be seen in the separate reports of those companies, so I’ll focus on the other stuff here, like a $1.6 billion impairment of the book value of De Beers in response to a tough market for diamonds. Rough diamond production was down 8% for the year as the group pulled back on production. EBITDA at De Beers crumbled from $1.4 billion to just $72 million.

This table does a great job of summarising the result:

Blue Label Telecoms: why I don’t buy things I don’t understand (JSE: BLU)

The share price is moving lower in response to a drop in earnings

I’m convinced that even the 4th year accounting lecturers at Wits (where I studied) don’t have it in their hearts to use Blue Label Telecoms as a case study for the students. I used to sit at varsity and wonder where the structures in the exams were dreamed up, as surely they don’t exist in practice.

They don’t exist very often, that’s for sure. Where they do, I avoid them. If it takes this much work to properly understand the numbers (as it always does at Blue Label Telecoms), then the risks are too high for me.

There are some in the market who profess to be experts on this company. I’m certainly not one of them. What I do know is that comparable core headline earnings fell 22% and core HEPS fell 23%. This is because a business called Comm Equipment Company experienced a drop in headline earnings of R119 million at a time when the rest of the group could only grew R19 million.

Here’s a perfect example of why I just cannot bring myself to even speculate here:

Here’s the share price, which is a language I think we all understand:

Caxton suffers a single-digit decrease in HEPS (JSE: CAT)

A more difficult trading environment is to blame here

Caxton and CTP Publishers and Printers has released a trading statement for the six months to December 2023 that reflects a decrease in HEPS of between 4.1% and 8.5%. That’s not bad, but it’s a move in the wrong direction. The company has noted the usual difficulties in the trading environment, leading to a decline in overall revenues and a margin squeeze, with cost control and an increase in net finance income helping to offset the problems.

The company had cash of R1.8 billion at the end of December. This has subsequently increased to R2.17 billion.

A missed opportunity at Gold Fields (JSE: GFI)

The group didn’t capitalise on the higher gold price

Gold Fields didn’t win the hearts of investors in the year ended December 2023. Profit per share came in at $0.79 per share vs. $0.80 per share in the comparable period. Production challenges in South Africa, Ghana and Peru detracted from the result, with the Australian operation only managing a flat production performance that wasn’t enough to offset the troubles elsewhere.

Adjusted free cash flow was $367 million, down from $431 million. Net debt excluding lease liabilities increased from $310 million to $588 million.

Looking ahead, there is significant capex underway at the Salares Norte project. There’s also a significant increase in sustaining capital due to a $132 million investment in a renewable microgrid project.

Attributable production is expected to increase from 2.24M0z to between 2.33Moz and 2.43Moz. Excluding the renewables project, the all-in sustaining cost guidance is $1,350/oz – $1,400/oz. This is higher than $1,295/oz in 2023, so the gold price needs to keep helping Gold Fields for the results to look better.

A HEPS increase in perfect Harmony (JSE: HAR)

When mining goes well, it goes really well

After a period of underperformance, many investors in the gold sector might have wondered where the saying “it’s a gold mine” actually comes from – particularly when used in a positive context! Harmony Gold has just reminded the market that when the yellow metal goes to plan, things get shiny very quickly.

Of course, the mining group still needs to get the stuff out the ground, so operational execution is key. In a trading statement for the six months to December, Harmony did exactly what it needed to do to take advantage of higher gold prices. Recovered grades were up, as was gold production. As a sweetener, production of silver and uranium also increased at a time when average prices for those commodities also moved up.

Naturally, there were annoyances like higher energy costs and royalties, but these couldn’t offset the strong numbers.

HEPS will be between 937 cents and 976 cents, which is a vast increase vs. the comparable period of 293 cents. Detailed results are due on 28 February.

A major disconnect between EBITDA and cash flow at Mondi (JSE: MNP)

This is an unusual result

In most cases, EBITDA and operating cash flow at least move in the same direction. These concepts aren’t the same, despite some people using EBITDA as a proxy for operating cash flow. The big difference is net working capital movement (inventory / debtors / creditors) which is captured by operating cash flow and not by EBITDA. The usual case is that working capital would increase as EBITDA moves higher, but wouldn’t offset the benefit of higher profits. Similarly, as EBITDA moves lower, some working capital would be unlocked but it wouldn’t offset the impact of lower profits.

At Mondi, we’ve just seen the unusual scenario. Underlying EBITDA fell sharply from €1.85 billion to €1.2 billion, which is a margin contraction from 20.8% to 16.4%. Return on capital employed has diminished from 23.7% to 12.8%. But despite this, cash generated from operations increased from €1.29 billion to €1.3 billion.

The reason? A net inflow of €229 million based on lower inventory levels vs. an outflow of €419 million in the comparable year. This was enough to more than offset the impact of lower profits. If nothing else, I hope this shows you that EBITDA is a poor proxy for operating cash flow and using it in that way is a risky approach. It works in some companies, but in others the balance sheet can (and does) move sharply.

The dividend of 70 euro cents per share is consistent year-on-year. A special dividend of €1.60 per share was paid on 13 February with the net proceeds from the disposal of the Russian assets.

The nightmare continues at Pick n Pay (JSE: PIK)

Or is that Pick n Pray?

Well, the speculative exuberance around the Pick n Pay share price has been smashed back down to earth. After a strong rally from mid-January levels of R21 up to R27 in a matter of weeks, the Grim Reaper of Capital Raising visited the share price and slashed it back down to R22.

Why? Because despite how badly the market wants to believe in Sean Summers, the man can’t work miracles. As I’ve written many times, retail turnarounds are much harder than people think, even if he seems to be doing the right stuff. You have to distinguish between market exuberance (a real opportunity for traders but dangerous for investors) and a real, fundamental story.

Pick n Pay has released a sales update for the 47 weeks ended 21 January 2024. They’ve done this as part of a trading statement and news of a substantial capital raise. When group like-for-like sales reported just 2.9% growth during a period of heightened inflation, things are not looking good.

Boxer grew 17.1% over the period (and 7.3% like-for-like), which is great. Pick n Pay’s core business decreased by 0.1%, which is truly awful, especially when you remember that the excellent Clothing business (up 17.5% with like-for-like growth of 8.0%) is propping up that number. Rest of Africa was up 10.3%, taking total group sales growth to 5.3%.

Special mention must go to Pick n Pay Online, which grew 75.8%.

When trading is this bad, a retailer’s balance sheet quickly works against shareholders. Inventory piles up on the shelves, hitting the working capital cycle and overall cash generation. The retailer notes that good progress was made in recent weeks to sort out the cash generation, but the problems are there for all to see. Net debt has ballooned from R3.8 billion to R7.2 billion as at 21 January. A sale of property of R0.5 billion in February helps with this, but barely touches sides if we are honest.

Lenders have waived covenants on the debt facilities to give the company a chance to sort out the balance sheet. These are desperate times, with the group now expected to report a headline loss for the year ending 25 February, attributable “entirely” to the performance of the core Pick n Pay supermarkets business.

So, guess what? There’s a rights offer of up to R4 billion to try and fix this mess, along with an intended IPO of the Boxer business. The rights offer is expected to be in mid-2024 and the IPO towards the end of 2024. Although Pick n Pay is aiming to retain a majority stake in Boxer, the company will obviously free up capital by reducing its stake considerably.

It’s a mess.

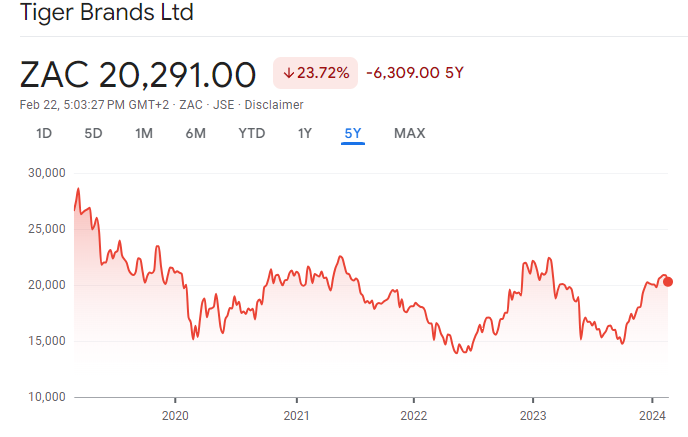

Is the Tiger Brands share price rolling over again? (JSE: TBS)

Trading conditions look incredibly difficult

The Tiger Brands share price is as volatile and dangerous as the animal that the company is named after. To me, it looks like it has run out of puff once more and could roll over from this resistance level:

The company has been significantly restructured into six business units, all reporting to the new executive management team led by Tjaart Kruger. The next restructure is focused on the shared services side of the business, with support structures moving from head office back into the different business units to improve the speed of decision making. There’s also a lot of focus being placed on rationalising SKUs (the variety of products).

In case it’s not obvious, Tiger Brands is trying to respond to a very difficult operating environment. Shockingly, prices of essentials like sugar, veggies, meat, eggs and rice are up by almost 20% according to Stats SA, which obviously puts huge pressure on consumers and their ability to spend on luxury items – where the better margins are made.

Despite promotional activity around Black Friday and the festive season, trade fell short of expectations and volumes declined. Group revenue for the four months ended January 2024 fell by 1%, with volumes down 8% and prices up 7%. There were pockets of growth in volumes (like in Snacks & Treats and in Baby), but the overall picture was firmly in the red.

The slightly silver lining is that efforts to contain costs helped to keep gross margins stable despite the drop in volumes.

If you’re hoping for a positive outlook from the company, there isn’t one. Operating income for the six months ending March will be flat or lower year-on-year, with a recovery in the second quarter dependent on improved trading ahead of the Easter period.

Little Bites

Director dealings:

The CEO of Mr Price (JSE: MRP) has sold every single one of the 16,908 shares received under the forfeitable share plan. The sale is worth R2.86 million. It’s usually the case that executives only sell the taxable portion, not the entire amount, so I see this as a strong sell signal.

The CEO of Datatec (JSE: DTC) has purchased shares worth R244k.

Joffe and Wiese are at it again, with these directors of Invicta (JSE: IVT) each buying shares worth R53k in the company.

In an announcement dealing with the results of the voting at the AGM, Tharisa (JSE: THA) also gave further information on the investment in the Karo Platinum Project. The company has noted that the total investment for its 75% stake in Karo Mining Holdings (which in turn holds 85% in Karo Platinum) has come at a cost of $135.3 million. Once you work through the shareholdings, this implies a value for Karo Platinum of $212.3 million. The important point is that the recent rights issue by Karo Mining Holdings (in which the minority shareholder renounced its right and allowed Tharisa to move from 70% to 75%) implied a value of $457.8 million for Karo Platinum. Long story short, the company believes that the investment has created value based on longer-term sustainable PGM prices, even if current spot prices look ugly.

The founders of Transaction Capital (JSE: TCP) have done some restructuring of their affairs to the value of R1 billion. It doesn’t change their indirect interest in the company (they are just reshuffling some cards here), but it does make me wonder if they are gearing up for a bigger corporate action after the WeBuyCars unbundling. Time will tell. In a separate update, the company announced that Global Credit Ratings (GCR) has downgraded the group’s credit ratings by a notch and has put them on Rating Watch Negative.

With Stephen van Coller set to step down as CEO of EOH (JSE: EOH) on 31 March, Andrew Mthembu (currently independent non-executive chairman) will take the role of interim CEO for a period of up to six months while a successor is found. Considering that the announcement of van Coller’s departure came out in October 2023, why do they seem to be struggling to find a successor?

Anglo American has agreed to acquire and integrate the contiguous Serra da Serpentina orebody owned by Vale SA into Anglo American’s Minas-Rio mine in Brazil. In terms of the transaction, Vale will contribute Serpentina and US$157,5 million in cash to acquire a 15% shareholding in the enlarged Minas-Rio and will have the option to acquire an additional 15% stake. Anglo American will continue to control, managed and operate the Minas-Rio operation, including any future expansions that relate to Serpentina.

Unlisted Companies

Global multi-asset broker XS.com has acquired locally licensed financial services provider Ubutyebi Financial Services. The acquisition enables the FinTech and financial services provider to establish XS ZA, positioning XS.com as a strong player in the local market and providing a platform for expansion across the continent. Financial details of the deal were undisclosed.

MCI, a global leader in business process outsourcing (BPO) and customer experience (CX) solutions, has acquired Cape Town-based BYC Aqua. The acquisition merges MCI’s innovative approach and BYC’s deep understanding of the region and substantial cloud offerings, including certain unique AI offerings.

Pick n Pay has released details of a strategic response to the situation in which the company finds itself. Under the leadership of Sean Summers, the group intends to implement a two-step recapitalisation plan which will comprise a Rights Offer to existing shareholders of up to R4 billion, providing near-term liquidity, followed by an offering and listing of the Boxer business on the JSE. The rights offer is expected to take place mid-2024 followed by the IPO towards the end of 2024. The group intends to retain a majority stake in Boxer after the IPO.

Vukile Property Fund has raised R1 billion via an accelerated bookbuild. The company placed 68,493,151 shares at R14.60 per share, representing a 0.75% discount to the pre-launch share price on 19 February and a 4.85% discount to the 10-day VWAP.

Copper 360 has successfully raised just short of R100 million, placing 29,411,764 shares at R3.39 per share. This represents a 9.1% discount to the VWAP for the 30 trading days up to February 14. The company has indicated that it has negotiated a buy-back option with the investor (after six months) which would reduce the dilution effect of the issue. Proceeds will be used to fund its expansion strategy and short-term working capital requirements.

Primeserv has advised that during the period 12 December 2023 to 19 February 2024, the company repurchased an aggregate of 519,473 ordinary shares for a total value of R667,033. The shares, repurchased at an average price of R1.22 per share, represent 0.45% of the issued share capital of the company.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 12 – 16 February 2024, a further 3,484,866 Prosus shares were repurchased for an aggregate €101,93 million and a further 272,075 Naspers shares for a total consideration of R913,4 million.

AB InBev has repurchased a further 562,205 shares at an average price of €58.57 per share for an aggregate €32,93 million. The shares were repurchased over the period 12 – 16 February 2024.

A2X will welcome its first inward listing when LSE-listed Neo Energy Metals plc opens for trade on the local bourse on 27 February 2024. Neo Energy Metals is a mining and development company focused solely on uranium and strategic metals supply. The company’s main project, Henkries, is a low-cost eco-friendly uranium project located in the Northern Cape.

Four companies issued profit warnings this week: Northam Platinum, Super Group, Sibanye-Stillwater and Caxton and CTP Publishers and Printers.

Four companies issued, renewed, or withdrew cautionary notices this week: Salungano, Telkom SA SOC, Tongaat Hulett and Pick n Pay,

In recent years, there has been a notable increase in sell-side auction activity in South Africa, although it has yet to reach the levels observed in the United States and European markets. There is also a growing trend of increased auction activity in other countries across the continent. In the fast-paced world of mergers and acquisitions (M&A), the sell-side auction has become a key strategy for companies aiming to enhance value and orchestrate competitive transactions.

In the context of M&A, a sell-side auction refers to a process where a company that is seeking to be acquired, or to sell a lucrative asset, solicits bids from multiple potential buyers.

Strategic evaluation: advantages and disadvantages of a sell-side auction

In the realm of M&A, the utilisation of sell-side auctions presents a nuanced landscape with distinct advantages and potential pitfalls.

Foremost among its merits is the promise of maximised value, as the competitive environment, filled by multiple bidders, often leads to more lucrative deals. The efficiency and timeliness inherent in structured auction processes can expedite transactions, allowing companies to capitalise promptly on favourable market conditions. Casting a wide net during a sell-side auction ensures a diverse pool of potential buyers, increasing the likelihood of finding a party with optimal synergies. In addition, a sell side auction process enables the seller to take the lead in the transaction, streamline the selling process and accelerate decision-making. The competitive atmosphere encourages swift responses from bidders, potentially leading to faster transactions. The inherent characteristics of sell-side auctions frequently result in the formulation of inventive deal structures. This stems from the diverse perspectives brought by each potential buyer to the transaction, and their eagerness to enhance the appeal of their bids.

However, this approach is not without its challenges, as the resource-intensive nature of organising an auction demands careful consideration, and it may strain internal resources, both human and financial.

To best present its asset, the sell-side ordinarily finds itself compelled to conduct its own due diligence investigations, spare financial resources to regularise any red-flag outcomes identified during the due diligence investigations, and spend time and money on financial, legal and tax advisers. In addition, the risk of proprietary and strategic information being disclosed, uncertain outcomes that may be influenced by various external factors beyond the seller’s control, coupled with the potential for disruption within the organisation, introduces complexities that warrant meticulous evaluation. Despite these considerations, the strategic advantages of sell-side auctions, including enhanced negotiation leverage and confidentiality control for the seller, underscores its significance in the M&A landscape. As legal practitioners navigate this dynamic terrain, a judicious assessment of these advantages and disadvantages becomes imperative to guide our clients through successful transactions.

Sell-side auction processes and timelines

The sell-side auction normally involves the following key steps:

The seller assembles professional internal and external deal teams, which consist of lawyers and investment bankers/financial advisors;

The seller conducts a vendor due diligence investigation and prepares a report (VDD);

Pursuant to the VDD, the third step involves the preparation of a value proposition in the form of a confidential information memorandum (CIM) to offer potential buyers an overview of the asset on sale. The process also includes having a non-disclosure agreement (NDA) in place to protect the proprietary interest of the selling company.

The fourth step is strategic, and involves the seller identifying potential buyers and inviting them to take part in the auction. This is to increase the likelihood of receiving bids from multiple parties.

The Seller exchanges the NDA, and distributes the CIM to potential buyers. The potential buyers would then submit non-binding indications of interest, which the seller uses to narrow the list of potential buyers.

After gauging the interest in the asset and the quality of potential buyers, the sixth step usually involves drafting a definitive agreement for comments and review by shortlisted bidders, setting up a data room to facilitate and enable potential buyers to conduct their due diligence investigations and, where the seller would like to have a ‘clean exit’, the seller will shop for warranty and indemnity insurance, and negotiate the parameters of liability and non-binding indicators with the insurer for inception by a successful bidder.

At this point, shortlisted bidders are given access to the data room to conduct a detailed due diligence investigation, review and comment on the draft definitive agreement, and submit a binding offer.

In the final step, once the shortlisted bidders have all submitted their bids, the sell-side will consider the binding offers, having regard to, amongst other things, the price offered for the asset and the nature and extent of the proposed changes to the draft definitive agreement, including conditions to implement the transaction and the likelihood of fulfilling such conditions. The Seller would then select a successful bidder and exclusively negotiate the final terms of the deal with this Buyer.

The timelines involved in a sell-side auction vary, but it can take anywhere between six and 12 months to implement such a transaction, once the seller goes out to market and there is immediate interest shown in the asset.

Risk versus reward

The decision to embark on a sell-side auction is indeed a calculated risk that warrants careful consideration. While the potential for maximising value and securing favourable terms through heightened competition is enticing, the resource-intensive nature of the process and the risk of confidential and/or sensitive information leakage during selection poses inherent risks. One must weigh these potential drawbacks against the strategic advantages, taking into account the specific goals and circumstances of the selling company. For organisations seeking swift transactions, a diverse pool of potential buyers and maximum value, the benefits may outweigh the challenges. However, for those not willing to spend resources, preferring to engage and negotiate with a single potential buyer, safeguarding their confidential information, and with minimal disruption, a traditional approach may be more suitable. Ultimately, the decision to pursue a sell-side auction should align closely with the overarching objectives of the selling company and its tolerance for the financial and resource intensive exercise inherent in a sell-side auction process. Legal and financial advisers play a crucial role in guiding clients through this evaluation, ensuring that the risks undertaken align with the potential rewards in the pursuit of successful transactions.

In conclusion, the decision to embark on a sell-side auction in M&A demands a balancing act between potential risks and rewards. Ultimately, the determination of whether a sell-side auction is a risk worth taking hinges on aligning the chosen approach with the circumstances of the selling company, its unique goals, risk tolerance, and the human and financial resources at its disposal.

Gabi Mailula is an Executive, Kamohelo Masubele, an Associate and Asanda Lembede a Candidate Legal Practitioner in Corporate and Commercial | ENS.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Deon Lewis (co-founder of Futureneers) and James Rothmann (Projects Director and Tax Innovation Officer at Futureneers) joined The Finance Ghost to talk about the 12BA Renewable Energy Partnership and the opportunity it offers investors for a tax-enhanced investment in solar.

Listen to the show here:

On this podcast, we talked about topics including:

The background of Futureneers and the investment track record.

The return profile of the solar projects both with and without the tax benefits.

The way the tax works further down the line when there’s a potential sale of the project.

Whether this opportunity is relatively more attractive for potential investors who are in higher tax brackets.

The protections in place for investors.

For more information on Futureneers and to apply for this opportunity, you can follow this link.

As always, ensure that you do your own research and consult with your financial advisor. The Finance Ghost has no affiliation with Futureneers or involvement in the underlying investments and does not accept any responsibility for the financial returns. Futureneers is a registered Financial Services Provider (FSP 46996) and registered Section 12J Venture Capital Company.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

It doesn’t get more sideways than Adcock Ingram (JSE: AIP)

If you like small percentages, here’s one for you

Look, Adcock Ingram certainly isn’t going to set your hair on fire. For the six months ended December 2023, revenue was up 1%. Exciting, hey? Gross profit fell 2%, trading profit was down 1% and HEPS increased by 1%.

I actually can’t remember seeing a cluster of such small numbers! Normally, when revenue is so sideways, trading profit takes a dive. Not so in this case.

Once you get to segmental numbers, it does get more interesting at trading profit level. The biggest segment is Prescription, thanks to a 13% increase in trading profit despite flat revenue. Conversely, OTC saw profits drop 9% off flat revenue. Consumer maintained its margins, with both revenue and trading profit up 2%. The Hospital division is the smallest part of the group and saw profits fall 16% despite a 5% increase in revenue.

In a final nod to the sideways journey, the dividend of 125 cents per share is identical to the prior period.

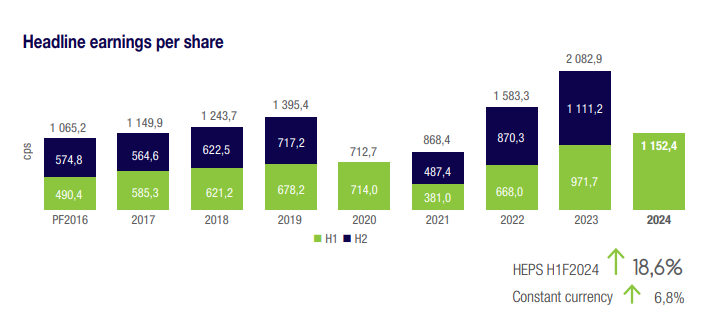

Bidcorp just keeps marching on (JSE: BID)

Growth remains strong, although there’s a question mark around margins

Global food service giant Bidcorpis an excellent way to give your money a passport without leaving the JSE. The company only earns a fraction of its income from South Africa, with the largest markets being Europe and the UK. The food service industry is lucrative once a business reaches scale, as is the case at Bidcorp.

The pandemic obviously threw quite the spanner in the works. This chart is historically significant, showing how H2’20 earnings were literally non-existent:

The other thing to take from the chart is that earnings have grown beautifully if we look through the pandemic distortions. In the six months to December 2023, revenue was up 24% and trading profit increased by 20.8%. Now, this does mean some operating margin contraction, caused by operating expenses growing slightly faster than gross profit.

Still, 18.6% growth in HEPS and a 19.3% increase in the dividend per share isn’t anything to complain about.

If you look segmentally, the trading profit story does reveal a significant headache in the UK in particular. Revenue increased by 21.2% in that market and trading profit fell 15%. Gross margin pressure in that market is a direct result of the tough conditions being faced there in the hospitality sector. Again, the grass isn’t always greener!

The strategy going forward remains the same: organic growth plus the use of bolt-on acquisitions to expand either geographic reach or product range in existing markets.

What on earth is going on at Bytes? (JSE: BYI)

The share price fell 6% on very odd news of the CEO suddenly resigning

It’s never a good thing when an executive leaves out of the blue, especially the CEO. It’s even worse when a resignation comes through with immediate effect, as it suggests that something has gone badly wrong in the background. When the SENS announcement doesn’t give a good explanation for something like this (e.g. a health problem), speculation is rife.

So, the news of Bytes CEO Neil Murphy resigning with immediate effect (and with no explanation given) isn’t a happy thing, which is why the share price closed 6% lower. To add even more spice to this story, there have been trades in the company shares that he hadn’t disclosed to the company or the market.

As Alice cried, “Curiouser and curiouser!”

The jokes write themselves about the clarity of the situation, with Sam Mudd (MD of Phoenix Software and an executive director of the company) taking the role of interim CEO.

The only positive here is that trading for the year ending 29 February 2024 has been in line with expectations, with a trading update due in March.

Choppy results at Choppies (JSE: CHP)

The per-share numbers have been significantly impacted by the rights offer in June 2023

Retail group Choppieshas released a trading statement for the six months to December 2023. Earnings actually did rather well, with profit after tax from continuing operations up by between 36% and 46%. On a per-share basis, the picture looks very different, with HEPS expected to differ by between -3% and 7%.

This is because of the rights offer that was completed in June 2023 that resulted in more shares being in issue.

Glencore’s numbers are way down year-on-year (JSE: GLN)

This is another good example of mining cycles in action

At Glencore, revenue dropped by 15% in 2023 and adjusted EBITDA was down 50%. Funds from operations tanked by 67%. Clearly, the year-on-year story is typical of the hard correction we’ve seen in the commodity sector over the past 12 months.

Glencore is quick to remind the market that although the year-on-year picture might look awful, the group remains highly cash generative. This supports the deal to acquire a 77% stake in Teck’s Elk Valley Resources business for $6.93 billion in cash is in the process of regulatory approvals, with an expected closing date no later than Q3 2024.

The focus is on deleveraging the balance sheet towards a $5 billion net debt cap before a demerger into a fossil fuels and transition metals structure could be considered. Glencore expects the deleveraging to occur within 24 months from transaction close.

This is why there is no “top-up” distribution at this point, with Glencore hoping that such distributions will happen again in the future. It’s a vague comment from the company that is surrounded by reminders that the real focus is on deleveraging, so don’t hold your breath for a high payout ratio over the next couple of years.

Profitability has collapsed at Sibanye-Stillwater (JSE: SSW)

The share price is back below R20

The good news is that Sibanye achieved revised production guidance for the year ended December 2023 at all operations other than US PGM recycling, which was impacted by deliveries of used autocatalysts remaining depressed as used vehicles are taking longer to be replaced in an environment of higher interest rates.

That’s where the good news ends.

Other than gold, commodity prices plummeted in 2023. This has led to substantial impairments being recognised on various operations, including even the SA gold operations due to the Kloof 4 shaft closure and the deferral of the Burnstone project.

Those impairments can’t even be blamed for the precipitous drop in HEPS, which will be over 90% lower year-on-year at between 60 cents and 66 cents.

The share price has lost almost half its value in the past 12 months.

Spar’s local volumes are still under pressure (JSE: SPP)

And in a shock to nobody, the SAP issues continue

Sparhas released a trading update for the 26 weeks to 16 February, showing an increase in turnover of 9.3% for the period. This number needs to be unpacked though, as Spar has operations in several countries.

SPAR Southern Africa remains the most important part of the business. Core grocery and liquor turnover growth was only 6.1% vs. internal inflation of 7.5%, so volumes moved in the wrong direction. The grocery wholesale business was only up 5.1% thanks to ongoing systems issues in the KZN region after the business gave itself the kiss of death: a SAP implementation.

To this day, I cannot think of a single SAP implementation at a retailer that hasn’t caused severe disruptions.

SPAR2U, the rather obscure online offering, is now available at 403 sites. Sales increased by 450% but that’s vs. a tiny base.

The star of the local business is TOPS at SPAR, which increased sales by 12.7%. Pharmacy at Spar was also solid, up 11.6%. Conversely, building materials and construction business Build it could only manage 0.5%.

Moving abroad, BWG Group in Ireland and South West England grew turnover by 7.1% in EUR and thus 19.1% in ZAR, with the rand depreciation helping massively here. Ditto for SPAR Switzerland, where a decline in turnover of 5.7% in CHF translated into a 9.2% increase in ZAR.

In Poland, an ongoing headache that Spar wants to sell, turnover was down 2.9% in PLN terms and up 16.1% in ZAR.

The group is considering various debt structuring options, with an optimised debt structure dependent on the outcome of the disposal of the interests in Poland.

Interim results for the six months ending March will be released on 5 June.

Stor-Age’s key metrics moved in the right direction (JSE: SSS)

The company has released a trading update for the four months to January 2024

Growth at Stor-Age comes from three sources: new developments, higher occupancy in existing developments and pricing increases charged to customers for the storage space. The company is very good at pulling all three of those levers.

In the four months to January 2024, group occupancy in the owned portfolio increased 230 basis points to 90.1%. The South African portfolio was the star here, up 280 basis points to 92.1%. The UK was up 40 basis points to 83.0%. The joint venture portfolio is a lot smaller and runs at a significantly lower occupancy rate, but this is increasing quickly as the properties mature.

Importantly, the South African portfolio saw average rentals up by 9.4% and the UK portfolio achieved 4.8% growth in that key pricing metric.

And with respect to the third lever (new developments), there are currently four developments underway – two in South Africa and two in the UK. Stor-age is also expanding certain existing properties to respond to demand.

There’s actually a bonus lever of growth which is still in its infancy: managing properties on behalf of third parties. This is a great way to increase return on equity, as the group is earning income off assets that it didn’t pay to build.

Little Bites:

Director dealings:

Sean Riskowitz, acting through Protea Asset Management, has bought more shares in Finbond (JSE: FGL) worth R758k.

A non-executive director of British American Tobacco (JSE: BTI) has acquired shares in the company worth £99k.

Brimstone Investment Corporation (JSE: BRT) released a trading statement dealing with the year ended December 2023. It’s based on EPS growing by between 49% and 59%, which really isn’t a useful measure for Brimstone’s investment holding company structure. Let’s wait and see what the movement in net asset value (NAV) is when results are released on 6 March.

Due to the process with the Prudential Authority taking longer than expected, Conduit Capital (JSE: CND) and the acquirer of the Copper Sunset Trading subsidiary (a deal worth R55 million) have agreed to extend the fulfilment date once more to no later than 31 March 2024.

The application to liquidate Afristrat Investment Holdings (JSE: ATI) was dismissed in the High Court, with costs. This has been going on for a while now and the company has earned itself some breathing room with this judgment.

Primeserv (JSE: PMV) has repurchased 0.45% of shares in issue between 12 December 2023 and 19 February 2024 for a total amount of R667k.

Following the standout performance of their initial 12BA Renewable Energy Partnership, which effortlessly hit its R135 million target,Futureneers is rolling out the much-anticipated sequel: Renewable Energy Partnership II. This isn’t just about making waves in the investment world; it’s about creating a ripple effect of change across South Africa’s energy sector.

With Partnership I rallying an impressive R96 million in debt and equity from August to December 2023 and a staggering R39 million in equity during the last 4 weeks, the stage is set for an encore that promises not only remarkable financial returns but also significant societal impact.

Your Investment, Amplified

Renewable Energy Partnership II isn’t your everyday investment. It’s a gateway to leveraging your tax in a way that contributes directly to South Africa’s green energy transition. And here’s the kicker: with the tax year concluding on 29 February 2024, this Partnership offers an exclusive chance to benefit from a 125% tax deduction. Yes, it’s a limited offer, but the potential? Limitless.

This is about putting your money where your heart is, blending financial wisdom with a commitment to sustainable development. With just R20 million up for grabs, it’s an opportunity that demands swift action, potentially achieving an Internal Rate of Return (IRR) of 21% pre-tax, and making a tangible difference in our energy crisis.

Investment Highlights:

Exclusivity at Its Finest: With only R20 million available, this opportunity is as rare as it is impactful.

Unprecedented Tax Advantage: Secure your spot for the last chance at a 125% tax deduction for this tax year, exclusively through Futureneers.

Diverse Investor Appeal: Whether you’re an individual looking to maximize tax efficiency or a corporation aiming for impactful investment, this is for you.

Solid Returns: A projected pre-tax IRR of 21% (13% post-tax) marks this as a standout choice for serious investors.

Strategic Entry: A minimum investment of R500,000 with options for early exit provides both commitment and flexibility.

Make Your Move

As we approach the tax year deadline, the window for this unique investment narrows. It’s not just an opportunity for financial growth but a step towards contributing to a sustainable and energy-secure future for South Africa.

Position yourself at the forefront of change and investment excellence. Together, let’s turn the tide towards a greener, more prosperous tomorrow.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

You need to read the BHP numbers carefully (JSE: BHG)

For one things, there are massive impairments in the results

Mining giant BHP released results for the six months to December 2023 and the words “underlying profit” appear often. The key difference between underlying profit and attributable profit is the impairment of Western Australia Nickel ($2.5 billion) and a further charge related to the Samarco dam failure ($3.2 billion). This smashes attributable profit from $6.5 billion in the comparable period to just $0.9 billion in this period.

Although these are non-cash charges for now, the reality is that the Samarco provision is an estimated future outflow and the Western Australia Nickel impairment talks to capital allocation. I wouldn’t just ignore these as being inconsequential.

To get closer to the core mining results, we can look at revenue (up 6%) and underlying EBITDA (up 5%), with slightly contraction in underlying EBITDA margin from 53.5% to 53.3%.

Net operating cash flow is a much more exciting story, up 31% thanks to the increase in EBITDA and lower income tax and royalty tax payments as well, which aren’t captured in EBITDA.

Of net operating cash flow of $8.9 billion, BHP invested $5.1 billion in various capital projects and thus generated $3.8 billion in free cash flow. Some capital expenditure was also funded from debt, which is why net debt increased from $11.2 billion as at June 2023 to $12.6 billion as at December 2023.

This is still within BHP’s targeted range for net debt of $5 billion to $15 billion.

An interim dividend of $0.72 per share has been declared, which is a 56% payout ratio.

Although there’s lots of noise in the numbers around timing of projects and other things, it’s quite fun to compare Return on Capital Employed (ROCE) across the various business units. Copper came in at 10%, iron ore 85% and coal 15%. Thankfully for BHP shareholders, iron ore is the biggest part of the business.

Kumba cuts jobs along with the production outlook (JSE: KIO)

This is the inevitable outcome of failing infrastructure

Thanks to a period of strong cost savings (R1 billion) and a rebound in iron ore prices towards the end of the year, Kumba Iron Ore pulled off a decent set of numbers for the 2023 financial year. EBITDA margin actually increased from 50% to 53%, with attributable free cash flow coming in 43% higher. Return on capital employed increased from 76% to 82%.

It all sounds really good until you dig deeper, with the group having to cut back on production because Transnet simply cannot rail the stuff to port quickly and reliably enough. This didn’t do any good for unit costs at Sishen in particular, although cost initiatives helped unit costs at Kolomela move lower.

The logistics limitations have led to a lower expected production plan for 2024 to 2026, which means the workforce at the company is too bloated for expected production levels. To ensure they remain competitive, Kumba will need to reconfigure the business and this is expected to impact 490 jobs. A further 160 service providers and contractors are impacted.

It’s one thing when commodity prices lead to job losses, like in the PGM industry. It’s another thing altogether when government absolutely fails to support the private sector, forcing a more conservative approach that loses jobs rather than creates them.

As great as the HEPS increase of 26% is, Kumba needs to look ahead and ensure it is right-sized for conditions that may not be so favourable.

Record earnings at NEPI Rockcastle (JSE: NRP)

This is the highest distributable earnings per share (DEPS) result in the company’s history

Eastern Europe (with the obvious exception of Ukraine) has turned out to be a decent place to do business as a property company, particularly when you have NEPI Rockcastle’s portfolio and balance sheet. Smaller funds are struggling with funding costs, yet here we have NEPI as the big shot in the room with record DEPS for the year ended December 2023.

DEPS was up 9.3% year-on-year, which exceeded even recent expectations at the company. If you adjust for once-offs in the base related to litigation provisions, then recurring DEPS was up 17.1%. Net operating income was the driver of this result, up 21% year-on-year thanks to a 13% like-for-like increase and the rest from acquisitions. A high inflationary environment isn’t a problem when lease clauses have indexation clauses. Even better, new lettings achieved higher uplifts than indexation thanks to the way the properties have been managed.

Retailers clearly like the properties in the portfolio, with sales and footfall metrics moving in the right direction and the vacancy rate decreasing to 2.2%.

The balance sheet was further strengthened by a scrip dividend option (shareholders could receive more shares instead of cash dividends), with the loan-to-value ratio down to 32.2%.

DEPS for 2024 is expected to be 4% higher, with no expected change to the current payout ratio of 90%. This is a fairly modest growth outlook, particularly after such a strong year.

A not-very-super update at Super Group (JSE: SPG)

With a nasty correction in the share price of 10% for good measure

Super Group released a trading update for the six months to December that reflects a 16.2% decrease in HEPS despite an 11.9% increase in revenue. This is significant margin erosion, with EBITDA margin decreasing from 13.6% to 12.8%.

There were various challenges faced throughout the group, ranging from the Southern African Supply Chain business suffering from slow turnaround times at local ports through to the UK Dealerships business dealing with a drop in consumer demand and a substantial decrease in used vehicle trading margins. The German and UK Supply Chain businesses also had a tough time as higher interest rates worked through the system. It’s not always greener on the other side, you know.

The bright spots were the SG Fleet business in Australasia in particular, as well as the South African Dealerships business in a car sales environment that has already been through the pain of normalisation.

The balance sheet remains in decent shape, with net gearing of around 36.5%.

Looking ahead, the company expects conditions in the second half of the year to be broadly in line with the first half, with some room for improvement in the UK Dealerships operations.

Vukile had no problems raising capital (JSE: VKE)

As mentioned earlier this week, Vukile is taking advantage of positive investor sentiment

In the heydays of the property market on the JSE (around 2015 – 2016), property funds could raise literally billions of rands in the time it takes you to finish your breakfast. These accelerated bookbuilds were heavily oversubscribed and in most cases, the company didn’t even tell investors exactly what the capital would be used for.

When times are tougher, it’s a lot more difficult to raise capital at all. On the rare occasions where we see an equity raise, the REIT has to submit two blood samples and a lifelong history of the asset being acquired. In short: the equity raising trends on the JSE tell us a lot about where we are in the cycle.

Vukile is certainly one of the better local REITs, so it’s not a huge surprise that it is leading the way in taking us back to the glory years of capital raising. In an equity raise that was intended to be 5% of the market cap (around R750 million), Vukile was able to increase the size of the raise to R1 billion, placing the shares at only a 0.75% discount to the pre-launch share price (and a 4.85% discount to 10-day VWAP).

Most impressively, they could place the shares and raise the money for acquisitions that haven’t even been announced yet. For now, they are just building a war chest for future deals – and the market was quite happy to provide that blank cheque.

Keep an eye on this trend as a potential sign that the best days of the property sector recovery may be behind us. Sadly, Vukile’s share price is still down 28% over the past five years. It has approximately doubled over the past three years in a post-pandemic recovery.

WBHO moves in the right direction (JSE: WBO)

HEPS from continuing operations has increased by between 5% and 15%

Wilson Bayly Holmes-Ovcon, or WBHO as everyone knows the group, has seen its profits head in the right direction for the six months to December 2023. This has been driven by a strong order book in Africa and improvements in the UK as well. For the six month period, HEPS from continuing operations should be up by between 5% and 15%. Total HEPS should be up by between 35% and 45%.

Those of you who keep falling into potholes will be pleased to learn that the roads and earthworks division has increased revenue by at least 50%, so roads are being improved somewhere at least. Operating profit is up by at least 60%.

The building and civil engineering side has grown revenue by at least 15% and profits by at least 5%.

Despite the company complaining about procurement of new work in the UK being difficult, revenue is up by between 15% and 20% and operating profit is up by at least 40%.

The construction materials and property developments segment has performed in line with the prior period at operating profit level.

Share of profits from associates and joint ventures has decreased by at least 60% due to once-off effects of the refinancing of the Gigawatt Power Station in Mozambique.

Australia remains a headache, with the loss from discontinued operations down by at least 90% but many ongoing processes in that country in relation to the exit from that country.

Little Bites:

Director dealings:

An executive director of Richemont (JSE: CFR) has sold shares worth a substantial R22 million.

Kibo Energy (JSE: KBO) has sold nearly £21k worth of shares in Mast Energy Developments, with the proceeds used to reduce the debt with RiverFort Global Opportunities PCC. Selling down an investment to reduce debt isn’t a pretty picture.

Copper 360 (JSE: CPR) has released one of those announcements that only really makes sense to geologists and perhaps mining engineers. The rest of us have to rely on the flavour of the narrative in the commentary by the CEO. Long story short, the historically mined Tweefontein Mine had the highest grade mine in the entire copper district and there could be a new copper mine adjacent to this historically mined area. Magnetic drone surveys and surface sampling results are encouraging. They have three more copper “anomalies” to test, all of which are bigger than the first anomaly that has been tested.

In the unlikely event that you are a shareholder in Marshall Monteagle PLC (JSE: MMP), one of the more unusual local stocks, you’ll want to know that the circular for the disposal of property in California worth $26.5 million has been released to shareholders.

Zeder (JSE: ZED) has reminded shareholders that the SARB approval for the special distribution of 20 cents per share hasn’t been obtained yet. The timetable will need to be revised accordingly.

This is a big year for South Africa. Load shedding returned literally straight after the State of the Nation Address, creating a difficult foundation for the Budget Speech. The headlines are full of political activity in the build-up to elections. There’s a lot going on.

Tertius Troost is in the Tax Consulting team at Mazars, so this is a busy month to say the least. He took time away from a hectic February tax diary to share insights as a preview to the Budget Speech.

Why is this important? Well, as a South African, the Budget Speech directly impacts you in many different ways, ranging from direct changes to your taxes to the way in which your taxes are spent in the country. It’s critical to understand the key pressure points for our fiscus.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")