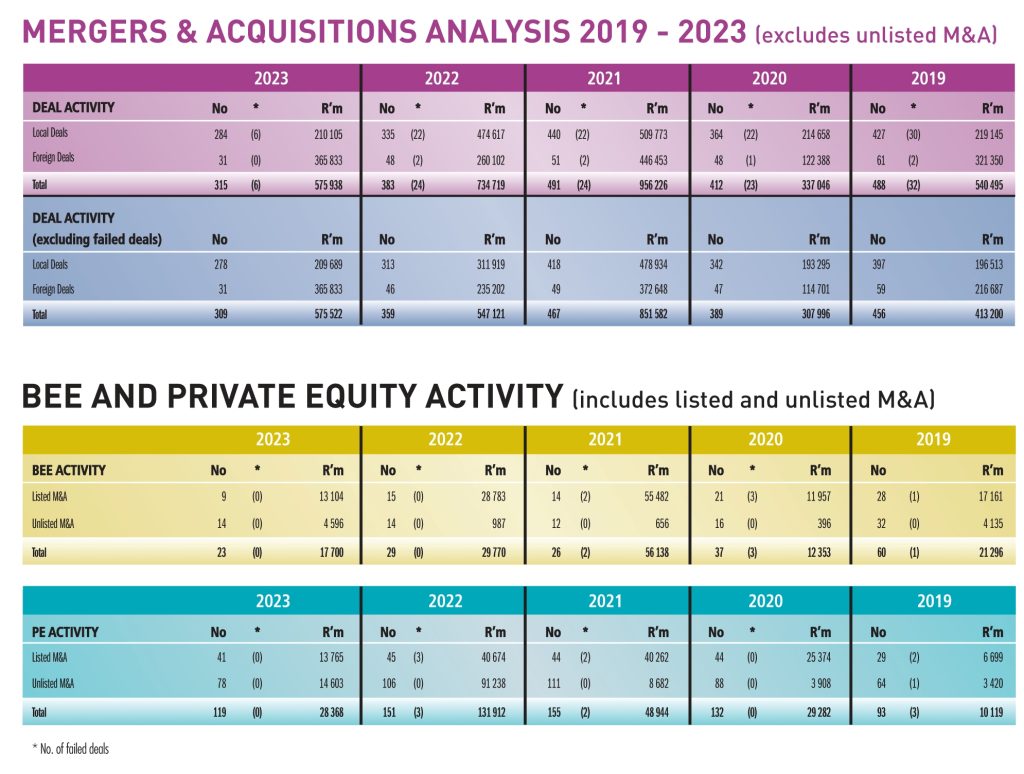

Over the past two decades, South Africa’s merger and acquisition (M&A) activity has all but halved, influenced by various factors, including regulatory changes, concerns over political stability, and local and global economic conditions, all of which have dampened investor confidence and slowed dealmaking momentum. This, is, of course, bar the blip in 2021, following the release of the bottleneck caused by the 2020 pandemic.

In 2023, total deal activity by SA-listed companies declined to 315 deals, valued at c.R576bn and that compares with 383 deals valued at R735bn in 2022. Of this 2023 total value, 64% of the deals were announced by foreign companies with secondary listings on the JSE.

Delving deeper into the numbers, the value of the 284 deals announced by SA domiciled companies in 2023 declined 44% against that of 2022 and this, despite the effect on the numbers of a weaker exchange rate. On a positive note, the number of failed deals dropped to six, against a norm of roughly 24.

Of the top 10 largest 2023 deals (by value) by a primary listed SA company, Life Healthcare’s disposal of Alliance Medical Group to entities advised by iCON Infrastructure tops the list at R19,7bn. The largest B-BBEE deal by value was Absa’s eKhaya transaction at R11,2bn. Both deals won their respective categories at the ANSARADA DealMakers Awards.

The standout theme of the general corporate finance tables, the rubric representing corporate restructurings, listings, share issues, unbundlings among others, was the return of value to shareholders by way of share buy-back programmes, special cash distributions and the secondary listing of companies on A2X providing investors with the cost-effective trading of listed shares.

The winners of the platinum medal subjective awards are as follows:

Ince Individual DealMaker of the Year – Ferdi Vorster

(L-R) Arie Maree (Ansarada), Ferdi Vorster and Laban Nyachikanda (Ince).

Brunswick Deal of the Year – Life Healthcare’s disposal of Alliance Medical Group

Life HealthCare’s disposal of Alliance Medical Group took home the Brunswick Deal of the Year award. Advising on the deal were Goldman Sachs, Barclays Bank, Rand Merchant Bank, Standard Bank, Werksmans, Webber Wentzel, Deloitte and BDO.

Exxaro BEE Deal of the Year – ABSA’s eKhaya transaction

(L-R) Arrie Maree (Ansarada) Molefi Nthoba and Jan-Hendrik du Plessis (Absa), Ling-Ling Mothapo (Exxaro), Mark Antoncich and Jason Janse van Vuuren (Absa)

Catalyst Private Equity Deal of the Year – Carlyle’s exit of Tessara

L-R Jaco Smit (Tessara), Michael Avery (Catalyst), Bruce Steen (Carlyle) and DJ Schreuder (Tessara)

Business Rescue Transaction of the Year – Cast Products South Africa

L-R: Arie Maree (Ansarada), Johan du Toit (Engaged Business Turnaround), Refilwe Ndlovu (Chrisyd Advisory Services) and Marylou Greig (DealMakers).

Special Recognition Award – African Parks

Accepting the award on behalf African Parks from Marylou Greig (DealMakers) is Yushanta Rungasammy and Sihle Bulose (CMS South Africa).

2023 M&A award winners (listed companies)

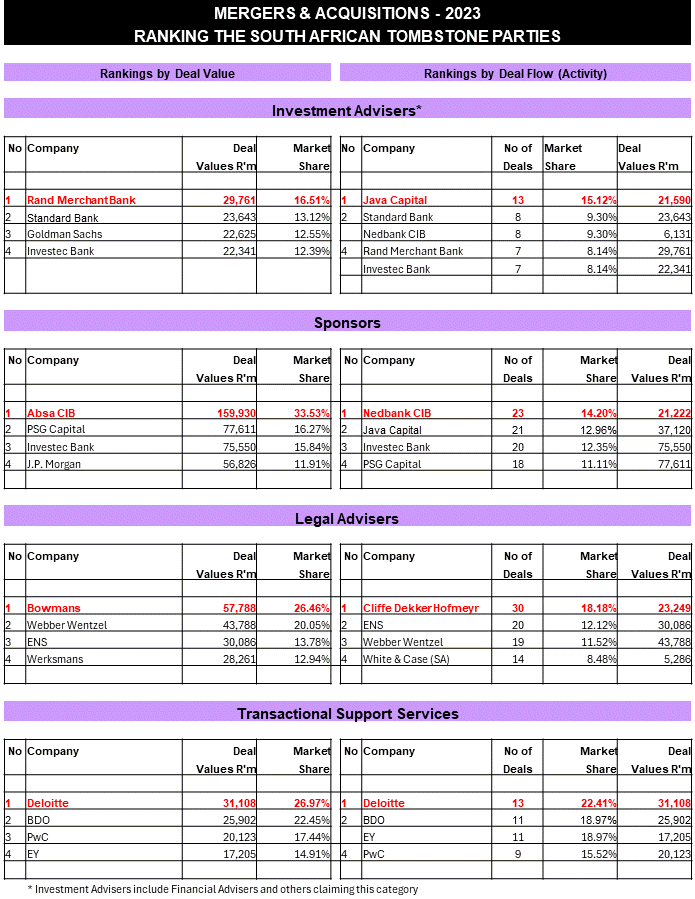

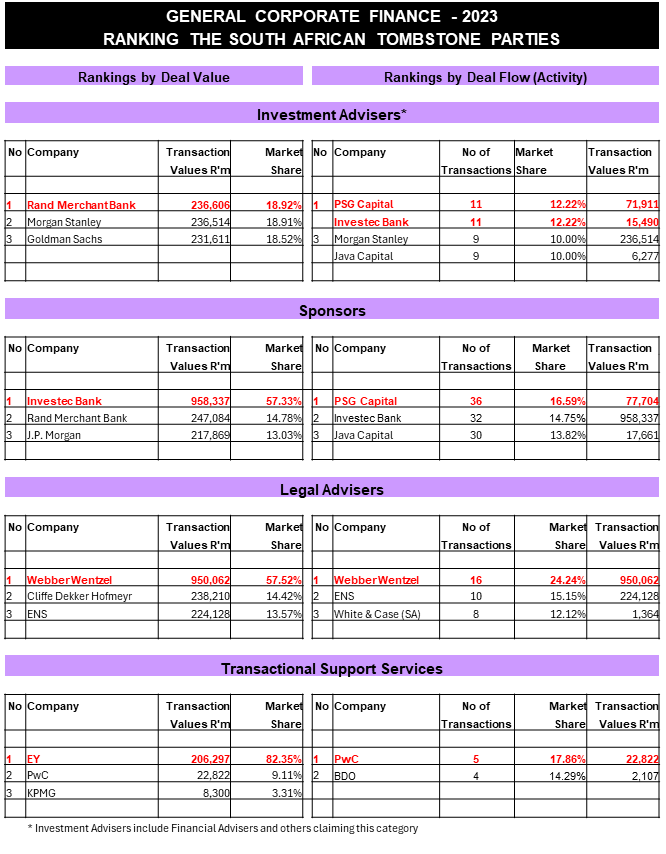

The category of Investment Adviser (by deal value) was won by Rand Merchant Bank. (L-R) Arie Marie (Ansarada), Krishna Nagar and Irshaad Paruk (RMB) and Marylou Greig (DealMakers).The category of Investment Adviser (by deal flow) was won by Java Capital. (L-R) Arie Marie (Ansarada), Wilson Baloyi and Kevin Joselowitz (Java Capital) and Marylou Greig (DealMakers).

The category of Sponsors (by deal value) was won by Absa CIB. (L-R) Kevin Brady (A2X) and Bonnie Brink.The category of Sponsor (by deal flow) was won by Nedbank CIB. (L-R) Michelle Benade (Nedbank CIB), Kevin Brady (A2X), Sujal Roy and Ryan Morrison (Nedbank CIB).The category of Legal Adviser (by deal value) was won by Bowmans. (L-R) Simla Ramdayal (WTW) and Tholinhlanhla Gcabashe.The category of Legal Adviser (by deal value) was won by Cliffe Dekker Hofmeyr. (L-R) Simla Ramdayal (WTW) and Roxanna Valayathum.The award for Transactional Support Services Adviser (by deal value) was presented to Deloitte. Thembeka Buthelezi received the award from Marylou Greig (DealMakers).Mdu Luthuli received, on behalf of Deloitte, the award for the Top Transactional Support Services Adviser (by deal flow) from Marylou Greig (DealMakers).

Winners of other awards presented on the night were:

In the category of General Corporate Finance:

Investment Adviser (by deal value): Rand Merchant Bank Investment Adviser (by deal flow) tie: PSG Capital and Investec Bank

Sponsor (by deal value): Investec Bank Sponsor (by deal flow): PSG Capital

Yet another quiet week on SENS – but this, I am told by those advising on deals, is not a true reflection of the current level of M&A activity. Well, that is good news especially as the country’s elections loom larger.

Transaction Capital has released further details of its proposed unbundling and listing of WeBuyCars (WBC). Prior to the listing, Transaction Capital plans to raise between R900 million and R1,25 billion by issuing shares in the second-hand car dealer. Shares will be issued to Coronation giving the asset manager an 11.3% stake at a cost of R760 million. New investors will be able to subscribe via a capital raising exercise of c.R750 million. This will reduce Transaction Capital’s stake from 74.9% to a range of between 57% and 67%. WBC’s founders’ shareholding will reduce from 25.1% to 10%. Proceeds from the various capital raising initiatives will be utilised by Transaction Capital for the settlement of debt at holding company level. The implementation date of the unbundling and listing is anticipated to occur during early April 2024.

Sirius Real Estate has acquired a further two business parks in Germany. The parks, one in Köln and the other in Göppingen, have been acquired for a total cost of €40 million using proceeds from the €165 million capital raise.

The Competition Commission has approved a deal which will see Sanlam’s private equity arm acquire Bacher, a distributor and wholesaler of high-quality brands such as Hugo Boss and Tommy Hilfinger.

As part of its strategic review of its investment portfolio, Brimstone Investment has disposed of 8,836,487 ordinary shares in Equites Property Fund for a total consideration of R123,9 million. The proceeds from the disposal will be applied to meet funding obligations in the near to medium term. The disposal is classified as a Category 2 transaction and accordingly does not require shareholder approval.

The logistics and fleet management company, Karooooo, will embark on a share repurchase programme to buy back up to 10% of its shares. This will be done through market purchases on the JSE and the Nasdaq.

Following the launch of the share buy-back programme announced in October 2023, AB InBev has repurchased a further 512,809 shares at an average price of €58.46 per share for an aggregate €29,98 million. The shares were repurchased over the period 5 – 9 February 2024.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 5 – 9 February 2024, a further 4,080,757 Prosus shares were repurchased for an aggregate €118,88 million and a further 493,133 Naspers shares for a total consideration of R1,48 billion.

MC Mining’s Independent Board, has again, recommended to shareholders not to accept the off-market takeover offer from Goldway warning that it is opportunistic, and does not provide an appropriate premium for control.

The JSE has warned shareholders that Ellies has failed to submit its interim report within the three-month period as stipulated in the Listing Requirements. If the company still fails to submit its interim report by 29 February, then its listing may be suspended.

Five companies issued profit warnings this week: Sasol, Insimbi Industrial, Gold Fields, Cashbuild and Kap.

Cognition was the only company to issue a cautionary notice this week.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

DRDGOLD can be very thankful for the gold price (JSE: DRD)

Without the increase, this period would’ve been a catastrophe

2023 wasn’t an easy year for DRDGOLD. The company had fallen behind on bringing new reclamation sites on stream to replace depleted sites. This was due to various external factors, ranging from delays on water usage licenses through to community interference. This forced the company to turn to legacy and clean-up sites to make 2023 a workable year – a situation made all the more frustrating by better gold prices that needed to be taken advantage of.

So, for the six months to December 2023, throughput fell 13% and production was down 7%, with better grades from the clean-up sites helping to mitigate some of the throughput pain.

Here’s an excellent summary of what life is like at mining dumps around Joburg:

Despite all this, DRDGOLD managed a 12% increase in revenue thanks to a 22% increase in the average rand gold price. Operating profit was up 15%, with operating margin expanding from 29.9% to 30.6%. A dividend of 20 cents per share has been declared.

The remainder of 2024 looks far more encouraging as all of the new sites are now up and running. There are also good reasons why costs should be better, including the completion of the solar power plant at Ergo that is scheduled for completion in March 2024.

Inflationary pressures cannot be ignored though, with cash operating cost guidance increased from R770,000/kg to R800,000/kg. This is a very tough way to make money, sadly, made all the more difficult by issues in Joburg.

The important numbers look good at Pan African Resources (JSE: PAN)

The group took advantage of the stronger gold price

The gold price doesn’t always do what we would like it to. In fact, it rarely behaves itself, seeming to move based on everything from inflation through to the gravitational pull of the moon. This means that when the price moves higher, gold mines absolutely must take advantage of this.

Pan African Resources did exactly that in the six months to December, with gold production up by 6.7% and an encouraging narrative around potentially upgrading guidance for the full year. Thanks to strong production and despite inflationary pressures, all-in sustaining costs (AISC) per ounce dipped slightly from $1,291/oz to $1,287/oz and full-year guidance has also been improved in this regard.

HEPS for the period was up 46.1%, which is obviously a strong result. Due to significant capex at the Mogale Tailings Retreatment project, net debt increased from $53.7 million to $64.3 million year-on-year. Steady state production is expected at the project by December 2024.

Universal Partners recognises a significant fair value loss (JSE: UPL)

The net asset value is down year-on-year as a result

Universal Partners holds a genuinely unique portfolio of assets, at least from a JSE perspective. They have everything from a dental roll-up business through to special toilets. No kidding.

Portman Dentex is actually a great example of a growing trend in the UK to combine fragmented services offerings into larger groups. This is now one of Europe’s largest dental care providers, fighting tooth decay across several countries. Following the merger of Portman and Dentex, Universal became a minority shareholder in the enlarged group. The business is performing ahead of budget, but higher borrowing costs have meant a shift in focus to operational efficiencies rather than lots of new acquisitions. Still, the business acquired three new practices during the quarter and how has over 400 practices in the group.

Another roll-up style play is Workwell, which doesn’t always work well. This is an accountancy and payroll business focused on contractors and freelancers as clients. That sounds like a lot of hard work to me – the exact opposite of lucrative B2B strategies. The business has struggled during a challenging labour market in the UK but is now in line with budget for the first quarter.

SC Lowy is a credit investing and lending group. The funds delivered a decent performance for the year, which is to be expected when yields are higher. The business in Italy, Solution Bank, achieved a record year.

Global recruitment business Xcede achieved the revised profit forecast for 2024. To help with working capital needs, Universal Partners subscribed for £1.5 worth of loan notes issued by Xcede.

We then arrive at Propelair, a toilet that uses just 1.5 litres of water per flush vs. 9 litres like a traditional toilet. Sounds good, but toilets turned out to be a rather kak business sadly. The company is way behind the original business plan and the investment is valued at a nominal amount.

The net asset value per share is £1.297, which equates to just over R31. The share price is R24. It is down from £1.429 a year ago, with fair value losses as a contributor to that.

Little Bites:

Director dealings:

Hot on the heels of Brimstone deciding to sell shares in Equites (JSE: EQU), the COO has also sold shares in the company. The sale is worth R6.9 million. The director has a loan agreement with Investec that is secured by shares and value of the loan has now been reduced.

Naughty, naughty: an independent non-executive director of Reunert (JSE: RLO) bought shares in the company worth R151k without obtaining prior clearance.

At Capital Appreciation Limited (JSE: CTA), the chairman, CEO and CFO only sold enough of their vested share options to pay the tax, whereas the divisional directors cashed in on share options in full. This isn’t an unusual situation given the variance in earnings at group executive vs. divisional executive levels.

Fortress Real Estate (JSE: FFA | JSE: FFB) announced that Moody’s has affirmed Fortress’ ratings and has upgraded the rating outlook from negative to stable.

Deutsche Konsum (JSE: DKR) shares literally never trade on the JSE, so I include this note just to give a data point on how German property is performing. For the quarter, net rental income (i.e. after operating expenses) fell 2.0% and FFO declined by 21.1% because of funding costs. The net loan-to-value at the fund decreased slightly from 61.6% at the end of September to 60.7% at the end of December.

In an announcement that you won’t see every day, an employee of the designated advisor of Visual International (JSE: VIS) bought shares worth R900. The designated advisor is the JSE listings requirements advisor for companies listed on the AltX.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

No sign of improvement at Cashbuild (JSE: CSB)

This sector continues to take strain

As we’ve seen at Italtile and within certain other groups, the so-called DIY sector continues to struggle. Building and construction materials only enjoy strong demand when consumers are feeling so confident about an economy that they want to invest in fixed assets. You know, the kind that are attached to the ground.

South Africa isn’t exactly filling people with confidence right now and that’s before the latest round of load shedding.

To add to the absolute lack of faith in the country’s economic future, we have high interest rates that make capital projects expensive.

The net result? A drop in HEPS at Cashbuild for the 26 weeks ended 24 December 2023 of between 15% and 25%.

Although earnings per share (EPS) is rarely an area of focus on the local market, impairments to goodwill are so large for P&L Hardware and other business units that earnings could be as low as break-even! That’s a big ouch.

Gold Fields couldn’t fully capitalise on a higher gold price (JSE: GFI)

Although within guidance, key production and cost metrics deteriorated year-on-year

Gold Fields released a trading update dealing with the year ended 31 December 2023. Full year attributable gold production is down 4% year-on-year and all-in costs are $1,512/oz, which is 15% higher year-on-year. When less gold is sold, expenses per ounce go up – especially when there are also inflationary pressures.

All-in sustaining costs (AISC) for the year were $1,295/oz, which is 17% higher year-on-year.

HEPS for the year is expected to be 18% to 24% lower, driven mainly by the once-off net proceeds for the Yamana deal break fee having been received in 2022. If you strip those out and if you use normalised earnings per share instead, it comes in between 1% and 7% higher year-on-year.

Santam’s HEPS is higher, but perhaps not for optimal reasons (JSE: SNT)

Sometimes you just have to take the wins wherever you can get them

The good news at Santam is that the year ended December 2023 saw the company achieve HEPS growth of 17% to 37%. Nobody is going to complain about that.

The “bad” news is that the jump is thanks to better investment returns on the insurance float (which gets invested in money market and fixed interest portfolios), rather than a strong result from the insurance operations themselves. The net underwriting margin is expected to be below the long-term target range of 5% to 10%. Various risk events (including exposure to earthquakes in Turkey) have impacted this margin, with the final release of Covid-related business interruption claims provisions helping to mitigate some of the issues.

Although the investment of the float is an important part of the economics of any insurance business, it would also be good to see the underwriting margin heading in the right direction, especially if we start to move into a cycle of decreasing interest rates.

Textainer releases earnings ahead of the all-important shareholder meeting (JSE: TXT)

The drop in full year HEPS reflects the cyclical nature of this industry

Textainer is literally just a few days away from the shareholder meeting to vote on the transaction that would see Stonepeak acquire all the shares in the company for $50 per share. This is why the company didn’t even host an earnings call to accompany these results.

Still, the results are important and shareholders will consider them as part of the vote. For the full year, HEPS fell from $6.14 to $4.59 as shipping cooled off vs. the post-pandemic period.

It’s interesting to note that in the nine months leading up to the Stonepeak announcement, Textainer repurchased shares at an average price of $36.31. That’s way below the Stonepeak offer, so that’s solid capital allocation from a shareholder perspective.

Stonepeak deal aside, Textainer has declared a dividend of $0.30 per share payable on 15 March 2024.

Transaction Capital lifts the lid on the WeBuyCars unbundling (JSE: TCP)

And a capital raise by the company for good measure

Transaction Capital has given the market details on the proposed structure of the WeBuyCars unbundling, which includes a few twists and turns that the market wasn’t expecting. In a separate announcement, the group also gave an update on the trading performance of WeBuyCars for the four months to 31 January.

The good news is that the positive momentum in the second half of the last financial year has continued into the new year, with revenue up 16% for the four months and core earnings up by 20%. Cash generated from operations has jumped beautifully by 57%, as the inventory value is only up by 2% despite the jump in revenue. Importantly, net interest bearing liabilities (R734 million in property finance on the vehicle supermarkets and R300 million for inventory) fell by 26%.

The blemish on this result is the finance and insurance (F&I) penetration, which was 19.4% in this period – down from 21.6% in the comparable period. Although shareholders would like to see this moving higher, it’s not enough to distract from the excellent financial results for this period.

This performance has come at the right time, as Transaction Capital needs to realise the value of a portion of its stake to help the company navigate its nightmare in SA Taxi. To achieve this, Transaction Capital will reduce its stake in WeBuyCars from 74.9% to between 57.5% and 67.5% prior to unbundling. The founders of WeBuyCars will also dilute from 25.1% to not less than 10% prior to unbundling.

On the whole, Transaction Capital plans to unlock between R900 million and R1.25 billion in cash prior to the unbundling. This will be used to settle debt and other obligations. Of great importance is that the call and put option structure with the founders of WeBuyCars will be cancelled, as they will now realise their value through the capital raising initiatives.

Note: the following section has been updated after a discussion with the management team to further understand the nuances of the deal:

The deal structure is complicated and involves various cash flows. With all said and done, the correct interpretation of the value of WeBuyCars seems to be R7.5 billion. In case you’re wondering if this view can be backed up by third party deals, the answer is that you’ve got Coronation, Stockdale Street Investment Partnership (the Oppenheimer family) and Ellvest (the Ellerine family) coming on board at this value. I initially thought the value might be more like R4 billion – R5 billion but that was without the benefit of the strong recent trading performance. As a Transaction Capital shareholder, I’m not complaining.

The market appreciated this news, sending the Transaction Capital share price 10% higher to R8.26. The announcement references a sum-of-the-parts valuation by the independent expert that values Transaction Capital at R11.86 per share, which is a great indication of just how much value was destroyed by SA Taxi in recent times. In case you’ve forgotten, Transaction Capital traded above R50 a share in early 2022.

Little Bites:

Director dealings:

Acting through Protea Asset Management, Sean Riskowitz has bought another R4.37 million worth of shares in Finbond (JSE: FGL).

Although I’m not 100% sure how the British American Tobacco (JSE: BTI) share compensation plan works, it’s notable that the interim finance director sold £250k worth of shares from the company’s share plan account.

The CEO of Datatec (JSE: DTC) bought another R4.05 million worth of shares in the company, taking his stake to 15.6% in the company. Conversely, the company secretary sold shares worth R346k.

A director of a major Dis-Chem (JSE: DCP) subsidiary sold shares worth R1.56 million.

The CEO of Sirius Real Estate (JSE: SRE) has bought shares worth £19.8k in a self-invested pension.

An associate of a director of Huge Group (JSE: HUG) has bought shares worth R28.6k.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I covered these important stories on the local market:

Sasol has seen its share price halve over the past year, with the wonderful opportunity for investors in 2020 becoming a very distant memory as infrastructure and other issues take their toll.

ArcelorMittal is perhaps the most severe rollercoaster ride of them all on the JSE, with the steel industry only for those with an exceptionally strong stomach.

Sappi demonstrates that the paper industry is also a tough place to play, with swing traders doing better than long-term holders of this stock.

Curro may be growing its earnings at a solid rate, but the company is still coming to terms with growth that is well below original expectations.

British American Tobacco is now profitable in the non-combustibles business and is still doing what it does best in the traditional smoking business: putting through pricing increases that fund dividends.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Anglo American looks to Finland for more opportunities (JSE: AGL)

If this sounds familiar, it’s because Sibanye-Stillwater has been doing the same thing

Anglo American and Finnish Minerals Group have signed a memorandum of understanding to explore opportunities around Finland’s battery metals strategy. This reminds me of when the local property funds all ran off to Eastern Europe in search of deals. Our mining houses seem to be taking a similar route in Finland!

To be fair, Anglo American already has an investment in Finland in the form of the Sakatti project, so it becomes an interesting debate around who has been copying whose homework around here.

There are various metals that form part of the “green metals” or “transition metals” groupings that are frequently written about. These metals are just as exposed to cycles as other commodities, evidenced by the Glencore news further down in Ghost Bites.

At this stage, Anglo American hasn’t released any concrete details around this memorandum of understanding.

Calgro M3 released an encouraging trading statement (JSE: CGR)

Share buybacks do wonders for earnings growth

Calgro M3 has been a comeback kid of note on the local market, with a focused strategy and capital allocation discipline that is working out very nicely. The latest trading statement is further evidence of this, with the company expecting HEPS for the year ended 29 February 2024 to be at least 20% higher.

If you’re familiar with trading statements, you’ll know that this is the minimum required disclosure under JSE rules. In other words, the increase could be significantly higher. When you consider that the number of shares in issue has decreased by 21% over the past year, even a sideways move in headline earnings would look strong at HEPS level.

Given the recent positive trajectory in operating performance, it seems fairly likely that the earnings improvement is significantly more than 20%. We will know for sure as we move closer to results being released in early May, with an updated trading statement likely to be released between now and then.

The nickel market has claimed another scalp (JSE: GLN)

Glencore isn’t prepared to carry any further losses at Koniambo Nickel

The Koniambo Nickel joint venture between Société Minière du Sud Pacifique SA and Glencore can be found in New Caledonia, a French territory in the South Pacific. Glencore has been involved since the Xstrata transaction back in 2013 and has funded more than $4 billion over the past decade without realising a profit at any stage.

This is obviously a terrible outcome for shareholders and enough is enough at some point. The mine is very important to the local economy but is simply untenable in the current market conditions for nickel. This is despite the best efforts of the French government to try and support the ongoing operation of the mine.

The operation will be moved into a state of care and maintenance, with the furnaces to remain hot for six months. All local employees will be retained for that period. Glencore will try to find a new industrial partner for the mine in an effort to avoid the economic fallout for the region.

Sirius buys two business parks in Germany (JSE: SRE)

The acquisitions have been funded from the November capital raise

Sirius Real Estate is listed on the JSE, but you won’t find any of the fund’s money flowing into local opportunities. This is a perfect example of how you can invest on the JSE and give your money a passport in the process. The fund is focused firmly on business and industrial parks in Germany and the UK.

The latest deal is to acquire two business parks in Germany for €40 million. The deals have been funded by the proceeds of the €147 million capital raise that was concluded back in November. It’s been a busy time for Sirius, as the fund acquired three UK properties in North London for €33.5 million towards the end of 2023.

The two German properties are of very similar values. The first is in Köln and was acquired for €20.0 million, with an EPRA net initial yield of 7.3%. The occupancy rate is just over 89% and the weighted average lease expiry is 2.4 years. The second property is in Göppingen and was acquired for €19.8 million. It has been acquired on an EPRA net initial yield of 6.9%. Occupancy is at 86% and the weighted average lease expiry is 2.8 years.

In both cases, Sirius will look for value-add opportunities to improve the economics of the properties. Sirius already owns other properties in the areas and so there is familiarity with both regions.

From the capital raised in November, €78 million has been committed to legally binding acquisitions and Sirius is in discussions for opportunities related to the remaining €70 million or so.

Little Bites:

Director dealings:

The CEO of Invicta (JSE: IVT), Steven Joffe, as well as Dr. Christo Wiese have been at it again with buying up shares in the company. The latest purchase is to the value of R985k for each of them.

The CEO of RH Bophelo (JSE: RHB) has bought shares in the company worth R401k.

Associates of directors of Nictus (JSE: NCS) have bought shares worth just under R24k.

This isn’t a director dealing in the usual sense as it relates to share options rather than an outright sale or purchase, but I simply had to mention a director of Naspers (JSE: NPN) selling shares worth a spectacular R79.8 million. Best of all, this only represents around 58% of the shares received under the share options that were exercised. It’s tough at the top, hey.

Cognition Holdings (JSE: CGN) released a rather amusing trading statement, noting that HEPS for the six months to December 2023 will be up by between 260% and 280%. This is thanks to returns on cash balances held over the period after the disposal of the Private Property platform. The company also renewed the cautionary announcement related to ongoing discussions with Caxton and CTP Publishers and Printers (JSE: CAT), Cognition’s holding company.

The chair of Sasfin (JSE: SFN), Deon de Kock, has unfortunately had to step down for medical reasons. Current lead independent director Richard Buchholz has been nominated as his replacement, subject to approval by the Prudential Authority.

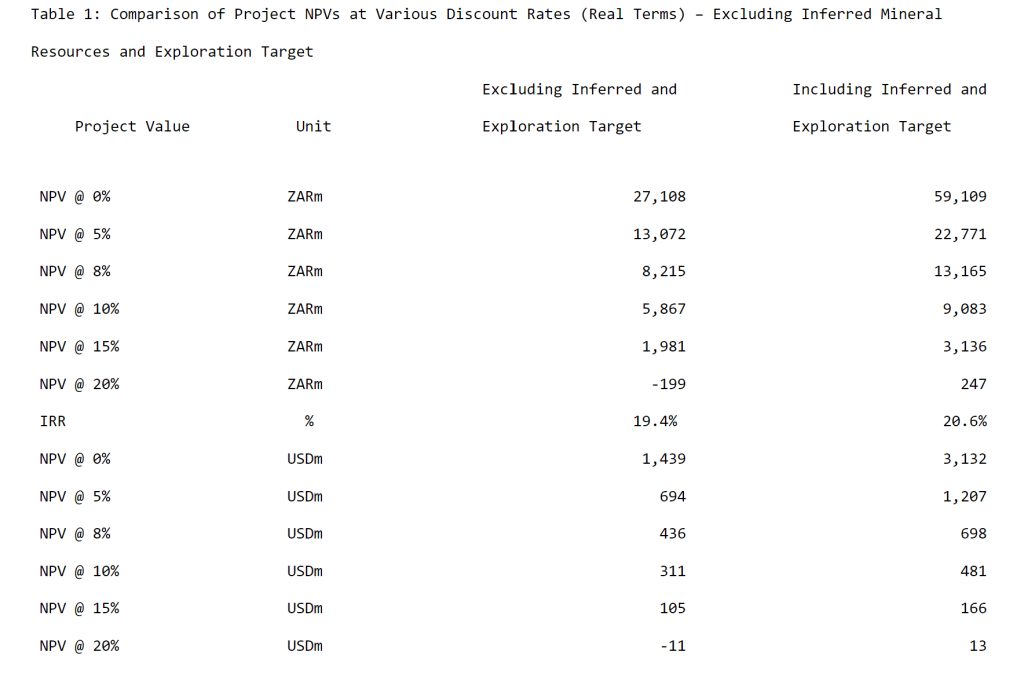

Southern Palladium (JSE: SDL) released an addendum to the Bengwenyama project study. Perhaps I’m misreading it (and very happy to be corrected), but it suggests a project IRR of roughly 20% (see table below). That doesn’t sound like anywhere near enough to make junior mining appealing, especially in PGMs!

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Brimstone reduced its stake in Equites (JSE: BRT)

The recent recovery in the Equites share price perhaps prompted this move

The Brimstone story hasn’t been very exciting, sadly. The share price has halved in value over 5 years and is down over 22% in the past year. The first problem is that the market puts a substantial discount on the intrinsic NAV. The second problem is that the intrinsic NAV hasn’t shown appealing growth. The combination means a disappointing share price performance and a market cap of just R200 million.

When trading at such a discount to NAV, turning some of the assets into cash isn’t a bad strategy (depending on what happens to the cash thereafter). Brimstone has used the recent improvement in the Equites share price to sell R123.9 million worth of shares, cutting its stake to just over a third of what it used to be.

The disposals were achieved at an average price of R13.02 per share. Hindsight is perfect obviously, but the Equites share price was trading at double this level in 2021. They must be kicking themselves about not selling sooner.

The proceeds will be used to meet funding obligations in the near to medium term. In a perfect world of course, the company would be able to use the proceeds for share buybacks, thereby helping to close the discount to intrinsic NAV.

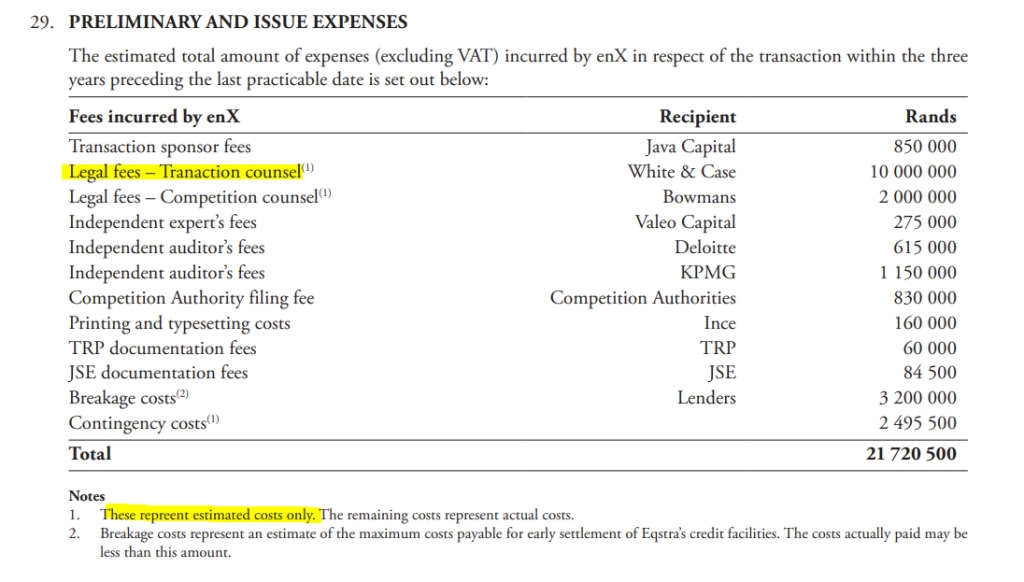

enX has distributed the Eqstra disposal circular (JSE: ENX)

Shareholders can get all the information they want on the proposal deal with Nedbank

A couple of months ago, enX announced a firm intention to dispose of Eqstra Investment Holdings to Nedbank. It’s a clever deal in my view, as the leasing and fleet management business will benefit greatly from a cheaper source of funding (and nothing is cheaper than being owned by a bank). It also gives Nedbank more scale in its fleet management business and a strong route to market. For enX, it gets a capital hungry business off the balance sheet.

Acting as independent expert, Valeo Capital has opined that the transaction is fair and reasonable to shareholders. The independent board of enX has recommended that shareholders vote in favour of the deal. You can find the full circular here.

I just hope that more attention to detail was paid to the deal than the expenses table (something I always look at). It’s not every day you’ll see a typo in the description AND the footnote:

There’s great news at Kore Potash (JSE: KP2)

Finally, there’s a meaningful step forward on the project

Kore Potash shareholders (and everyone else involved) have had to be patient on this one. For months now, we’ve been reading about PowerChina (the owner of SEPCO) and all the work that the company is doing on site to put together an Engineering, Procurement and Construction (EPC) proposal. Construction projects of this scale can easily sink construction groups if they go wrong, so immense effort is put into the contract itself. The risks are even higher when the build is in a difficult jurisdiction, like the Republic of Congo.

The excellent news is that PowerChina has finally delivered an EPC proposal and draft contract offer. Best of all, the pricing aligns with expectations and confirms the capital cost that was detailed in the original study. Full commercial terms now need to be negotiated, with a targeted signing date of April 2024. Thereafter, the Summit Consortium will need to put in a funding proposal within six weeks of the EPC documentation being signed.

The share price jumped 23% on the news. You can be sure that whether things go well or extremely badly in the next few months, each major update will drive a significant move in the share price, either up or down.

Sasol shareholders continue to take a beating (JSE: SOL)

The latest trading update isn’t helping

Sasol’s share price has halved in the past year, having decoupled considerably from the oil price in recent times. The chemicals side of the business has a substantial bearing on the share price performance, as do the operational realities in the energy business in South Africa.

Battered shareholders don’t seem to be getting any relief, with another 3.9% drop on Friday after the company released a trading statement. Results for the six months to December were hit by a bunch of issues, ranging from commodity prices through to infrastructure problems in South Africa and the weaker global growth outlook.

Adjusted EBITDA for the period will be between 8% and 18% lower. By the time you reach core HEPS level, the decrease is 19% and 33%.

Although I tend to focus on HEPS rather than EPS which is impacted by impairments (non-cash write-downs of assets), I must note that the Secunda liquid fuels refinery was written down to zero as at June 2023 and all the capital expenditure on the project in the six months to December 2023 was also fully impaired due to ongoing issues.

I would therefore argue that EPS is worth considering at the moment. That metric is down by between 29% and 43%.

Whichever way you cut it, things are not looking healthy at Sasol.

Little Bites:

Director dealings:

An associate of a director of Clicks (JSE: CLS) sold shares worth R2.7 million.

The CEO of Invicta (JSE: IVT) and Dr. Christo Wiese are both still buying up shares in the company. The latest tranche saw CEO Steven Joffe pick up R720k worth of shares and Wiese took R1.05 million.

A director of a major subsidiary of Santova (JSE: SNV) sold shares worth R1.2 million.

After buying another R820k worth of shares, Protea Asset Management (related to Sean Riskowitz) now owns just over 20% of Finbond (JSE: FGL).

An associate of a director of Afrimat (JSE: AFT) has bought shares worth R122k.

Sirius Real Estate (JSE: SRE) only achieved a modest take-up of the dividend reinvestment plan, which suggests that shareholders aren’t seeing great value in the shares at these levels. Only holders of 0.46% of shares on the UK register and 7.24% of shares on the SA register elected to receive shares instead of a cash dividend.

Having already given us significant insight into earnings earlier this month, MiX Telematics (JSE: MIX) has now released its detailed 10-Q (quarterly report under US rules) with the SEC. If you want to check out the company in detail, you’ll find it on the website.

Insimbi Industrial Holdings (JSE: ISB) released a trading statement noting that HEPS will be at least 20% lower for the year ending 29 February 2024. This is the bare minimum disclosure required by the JSE, so it’s quite possible that the actual decrease will be significantly worse. No further details have been given.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Anglo American’s Q4 production met expectations (JSE: AGL)

Thank goodness for Quellaveco and Minas-Rio

At mothership Anglo American, there are loads of moving parts that come together to deliver a group result. These range from how listed subsidiaries like Amplats and Kumba Iron Ore are performing (see both further down) through to how the South American mines are doing. Of course, De Beers is also a factor here.

It’s not hard to see why capital allocators are ignoring South Africa. Kumba had to slow down production because Transnet is so useless, whereas the Minas-Rio mine delivered its highest quarterly volume of premium high grade iron ore.

Notably, diamond production fell by 3%, but this was due to Venetia (in South Africa) transitioning to underground operations. Production from Botswana picked up as diamond prices started to improve, but rough diamond sales volumes in the quarter were still way down year-on-year.

On the copper side, production was down 6% due to lower grades and harder ore at Los Bronces in Chile, partially offset by higher production at Quellaveco in Peru.

On a full-year basis, production volumes were up 2% across all commodities. That’s not the most useful statistic though, as there are so many underlying commodities that have vastly different values.

HEPS plummeted at Anglo American Platinum (JSE: AMS)

PGMs have been having a torrid time

Anglo American Platinum released a trading statement for the year ended December 2023. HEPS will decrease by between 67% and 77%, so that’s a rather revolting year.

There’s not much that the company can do when the US$ PGM basket price fell 35%. Although the average rand/dollar exchange rate weakened by 13% and gave a small amount of relief here, it was nowhere near enough. A 2% increase in sales volumes was also woefully inadequate in saving the situation.

On top of all of this, the company has had to contend with inflationary pressures on costs.

The share price has lost 42% of its value in the past 12 months.

In a separate announcement dealing with the fourth quarter production results, guidance for 2024 was given for production (3.3 – 3.7 million ounces) and cash operating unit costs of R16,500 – R17,500 per PGM ounce. For reference, the basket price per PGM ounce was R26,111 this quarter.

ArcelorMittal signs off on an ugly financial year (JSE: ACL)

The wind down of the Longs steel product operations has been deferred

The year ended December 2023 is one that ArcelorMittal will want to forget. Although revenue increased by 2.1%, EBITDA absolutely collapsed – down 98.7%. There’s debt on the balance sheet as well, so the losses by the bottom of the income statement are eye-watering. After making headline earnings of R2.6 billion in 2022, the company swung into a headline loss of R1.89 billion in 2023.

Net borrowings increased by 14.5% to R3.2 billion and the net asset value was slashed by 33% to R7.8 billion. It’s just hideous wherever you look.

Between poor local and Chinese demand for steel and higher energy costs, things were always going to be tough. Add in the local logistics failures and a ban on scrap steel exports (thereby increasing competition with steel manufacturers using scrap rather than iron ore as inputs) and you had a recipe for disaster.

After much consultation with government, ArcelorMittal has deferred the wind down of the Longs steel business for up to six months. A clear warning shot has been fired by the company, with substantial negative impact if the wind down goes ahead. Much depends on improvements at Transnet, so I wouldn’t hold my breath.

In the outlook sector, the company notes that the current low steel prices are unlikely to remain the case going forward as global manufacturers are under pressure. Ultimately, demand in China will also play a huge role in how the market performs in 2024.

Here’s another chart for the mountain biking enthusiasts among you:

British American Tobacco achieved profitability in New Categories (JSE: BTI)

The market seemed to like these numbers

For the year ended December 2023, British American Tobacco grew revenue by 3.1% on a constant currency basis. The reported number was down 1.3% though. The big story was in New Categories, which grew revenue by 21% and finally achieved profitability – two years ahead of schedule! Revenue from non-combustibles is now 16.5% of group revenue.

The company is aiming for the non-combustibles business to be over 50% of revenue by 2035.

On the combustibles side, revenue was up just 0.6% in constant currency. Price and mix benefits were 6.1%, so that tells you how volumes dropped off. British American Tobacco literally relies on being able to put price increases through on an ever-shrinking base of smokers, all while achieving great ESG scores. In fact, the company is proud to announce that the 2023 MSCI ESG rating was upgraded from BBB to A, achieving targets for water and waste. You can tell how much faith I have in the ESG industry.

The company recognised a gigantic impairment in its US business (£27.3 billion – and take careful note of the currency there). Without that, adjusted profit from operations was up 3.9% in constant currency and margin expanded 40 basis points to 45.6%.

As is the British American Tobacco brand promise to investors, operating cash flow conversion was 100%. This helped bring net debt to adjusted EBITDA down to 2.6x and drove a 2.0% increase in the dividend.

In terms of outlook, pressures in the US (for various reasons) will impact 2024. with global tobacco industry volume expected to be down 3%. Thereafter, revenue should grow at 3% to 5%, which is all that South African investors want to see here. The only reason to buy British American Tobacco is to get a modestly growing hard currency dividend.

Oh, and to meet ESG investment requirements. I forgot.

15% of Curro’s schools are performing below expectations (JSE: COH)

This isn’t the report card that investors want to see

Curro is one of the best examples around of the exuberance on the JSE in the 2015 – 2017 period. Property companies were booming at around the same time, with Curro offering a hybrid of a real estate portfolio and the dream of filling those schools with a rising middle class over time.

Here’s how that chart panned out:

High growth expectations are dangerous in any company. As you can see, Curro shareholders were brought sharply down to earth by the realities of South Africa. Those realities are still kicking in, with the year ended December 2023 revealing that 28 of the 182 schools achieved lower than expected growth over the past two years, leading to impairments.

Impairments are non-cash charges that are excluded from HEPS but included in EPS. They are calculated with reference to the return on capital that the schools should be providing. Although it doesn’t help that Curro’s weighted average cost of capital moved from 14.5% in 2022 to 15.6% in 2023, the bigger issue is growth in the middle class in South Africa and Curro’s appeal to the people who have stayed behind in this country. The impairment for the year is between R340 million and R380 million.

The good news is that recurring HEPS moved firmly in the right direction, up between 26.3% and 37.2%. Dividends are considered based on recurring HEPS, so that’s the number to really focus on.

As a reminder of how important timing is when it comes to single stock exposure, look how different the 12-month chart looks to the longer term picture:

Impala Platinum lays bare the damage to HEPS (JSE: IMP)

The PGM sector is where dreams went to die in the past year

Impala Platinum has issued a further trading statement for the six months ended December. Nobody took the first one seriously anyway, which had the minimum required disclosure of HEPS differing by at least 20% to the prior period. Even a very quick calculation revealed a far worse scenario.

Sure enough, the company has issued a further trading statement that reflects HEPS down by between 76% and 82%. Although sales volumes were 12% higher from the interim consolidation of Impala Bafokeng and better operational performance, dollar revenue per 6E ounce sold fell by 37%.

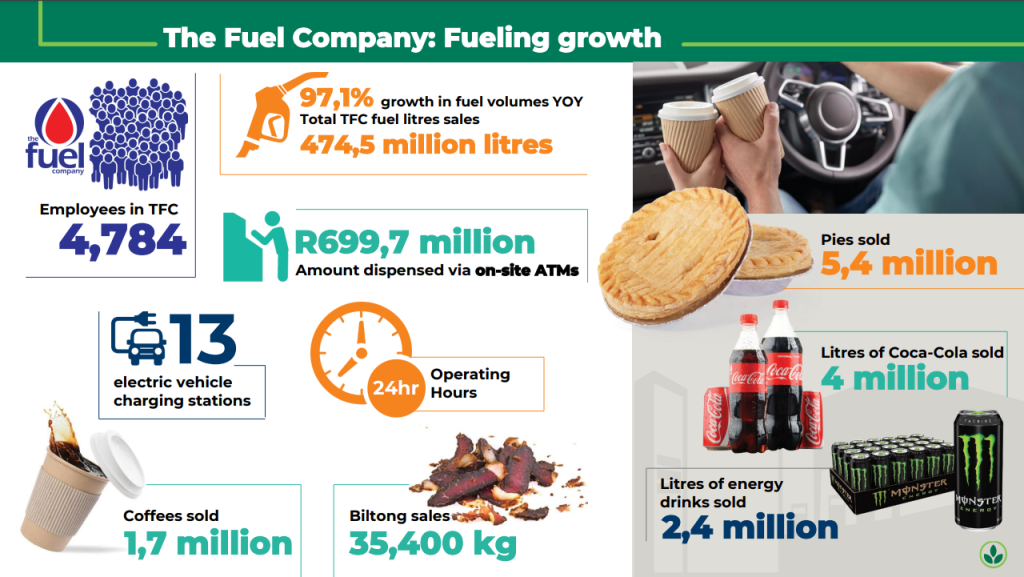

A Q1 update at the KAL Group AGM (JSE: KAL)

Fun fact: the group sold 2.4 million litres of energy drinks in 2023 – and 5.4 million pies!

In an incredibly fun presentation, KAL Group included slides like this absolute winner about forecourts business The Fuel Company:

These statistics don’t really mean anything to investors of course, but they make for interesting reading. I also found it quite fun to note that the retail outlets sold 6,400 tonnes of dog food and only 309 tonnes of cat food. Y’all need more cats out in the platteland!

The AGM deals with the full year 2023 numbers which were already known to the market. Recurring HEPS had increased 7.2% for the year and the dividend per share was 7.1% higher, so it was a solid performance.

The company used the AGM to give an update on the first quarter of the 2024 financial year, reflecting revenue growth of just 3.4% and deflation of 1.0%. You won’t see that every day! Recurring headline earnings per share is only up 5.7% for the quarter, which is a good reminder that retailers actually quite like a bit of inflation. It’s also worth highlighting that group fuel sales are down 0.8%, perhaps speaking to overall economic activity and consumers cutting back in general.

At Kumba, the Transnet issue is just getting worse (JSE: KIO)

This is the real State of the Nation– and there are no jets to make us feel better

Kumba Iron Ore has announced its production and sales report for the fourth quarter, as well as a trading statement for the year ended December 2023. Thanks to higher iron ore export prices and a weaker range, HEPS will be between 18% and 31% higher for the year. This is a lucky escape when you read about the underlying logistical challenges. We can only dream about what might have been for the company if the infrastructure was working.

Although there was a maintenance shutdown in October that obviously impacts this statistic, the decrease in ore railed to Saldanha Bay Port of 19% in Q4 2023 vs. Q3 2023 is just another example of the far bigger problems around our rail infrastructure. For the full year, ore railed improved by just 1.6% even though the base period included industrial action at Transnet.

In response to on-mine stockpiles that were far too high, production in Q4 2023 was 26% lower than in Q3 2023. Despite a 5% drop in full year production, full year unit costs actually improved to $41 per tonne, below revised guidance of $42 per tonne thanks to rand currency weakness and cost savings. They pulled off a proper performance here despite infrastructure letting them down.

Due to the extensive stockpiles, sales increased by 5% vs. Q3. Iron ore prices were higher in the fourth quarter, so this was a good time for sales to pick up. The problem is that the stockpiles are mainly at the mines rather than the Saldanha Bay Port, so there’s not much of a buffer to keep sales ticking over even when production dips.

Guidance for 2024 to 2026 has been revised to 35 – 37 Mtpa, with expected unit costs of $38 – $40 per tonne. This is the best that the company believes it can do in the context of the current Transnet rail issues, which aren’t expected to be resolved over the medium term.

Mondi has confirmed that it is sniffing around DS Smith (JSE: MNP)

Consolidation is a feature of tough industries

Mondi has announced that it is in the “early stages” of considering a merger with DS Smith, which would take the form of a share-for-share deal. The thesis here is that this would create an industry leader in European paper-based sustainable packaging solutions.

You only needed to read the Sappi results earlier this week to see how tough the paper and packaging sector can be. Consolidation makes sense in difficult industries.

If this deal were to go ahead, it would have benefits like vertical integration, enhanced security of paper supply, economies of scale (bigger businesses can sometimes be more profitable in terms of ratios) and complementary positions in products in the market.

At this point there is no guarantee that Mondi will make an offer. The company has until 5pm on 7 March 2024 to either announce a firm intention to make an offer or to confirm that it will not make an offer. This is how the UK takeover laws work.

MultiChoice settles with the Nigerian tax authorities (JSE: MCG)

South Africa vs. Nigeria is a common theme this week

Much like Bafana Bafana, a few local corporates haven’t had a happy time at the hands of Nigerians. One such example is MultiChoice, which has agreed to pay the Nigerian tax authorities a substantial $37.3 million in full and final settlement of all matters in dispute.

Interestingly, the announcement notes that this payment is offset against security deposits and “good faith payments” made to date.

Little Bites:

Director dealings:

The CEO of Invicta (JSE: IVT) bought shares worth R335k.

A non-executive director of Collins Property Group (JSE: CPP) bought shares worth R138k.

Jubilee Metals (JSE: JBL) updated the market on the progress made in the copper metals portfolio in Zambia. The goal is to reach 25,000 tonnes of copper per annum and they have a few projects underway. Aside from an unavoidable delay or two, the underlying narrative is positive.

ISA Holdings (JSE: ISA) released a trading statement noting that HEPS is expected to increase by at least 20% for the year ending February 2024. This is the minimum level of disclosure permitted by the JSE, so the difference could technically be a lot more. We won’t know until results come out.

The winners of the DealMakers subjective awards will be unveiled at the ANSARADA DealMakers Annual Awards on the 13 February 2024. The shortlisted nominees, as judged by the Independent Panel are:

Petronas’ sale of its Engen stake to Vivo Energy

Following a competitive process by Petronas to find a suitable buyer for its 74% shareholding in African-based energy group Engen, Vivo Energy emerged as the successful bidder. The transaction, the value of which is not in the public domain, is one of the largest downstream investments in Africa, and following the deal, will result in the group having more than 3,900 service stations in 27 African countries.

Local Advisers: Rothschild & Co, Standard Bank, Citigroup Global Markets, Morgan Stanley, Rand Merchant Bank, ENS, Werksmans, Webber Wentzel and EY.

Liberty Two Degrees buyout by Liberty

The buyout of minorities brought Liberty Two Degrees (L2D) fully back into the group after seven years of a separate listing on the JSE. As its major shareholder with an c.61% stake, L2D was one of the less liquid listed property stocks. The offer of R5.55 a share represented a premium of 46.4% to the 30-day volume-weighted average price at the time of announcement giving investors a favourable exit. The property REIT owns around 25% of a portfolio of landmark retail and hospitality assets in SA.

Local Advisers: Rand Merchant Bank, Java Capital, Standard Bank, Werksmans, Webber Wentzel and Mazars.

Disposal by Life Healthcare of Alliance Medical Group to iCON Infrastructure

After receiving several unsolicited proposals from third parties to acquire its European diagnostic and molecular imaging business, Life Healthcare announced its disposal of AMG just seven years after its acquisition from funds managed by M&G Investments and Talbot Hughes McKillop. The deal, valued at c.R21bn (including debt) will unlock significant value for shareholders with the company set to return c.R8,4bn to shareholders by way of a special dividend.

Local Advisers: Goldman Sachs, Barclays Bank, Rand Merchant Bank, Standard Bank, Webber Wentzel, Werksmans, Deloitte and BDO.

Sun International’s acquisition of Peermont

Announced in December the Peermont transaction, to be funded entirely by debt, provides Sun International with an opportunity to build scale and acquire a world-class and highly cash generative business. The R3,2bn equity deal brings 11 properties, located across South Africa and Botswana, including flagship Emperors Palace, and online betting platform PalaceBet. For Peermont shareholders, the deal provides an opportunity to achieve meaningful liquidity and for the combination with a respected and successful listed entity.

Local Advisers: Nedbank CIB, Rand Merchant Bank, Cliffe Dekker Hofmeyr, Bowmans, Webber Wentzel, Herbert Smith Freehills South Africa, PwC and Deloitte.

RCL Foods’ disposal of Vector Logistics to AP Møller

Remgro-owned RCL Foods sold its frozen logistics business, Vector Logistics, to a South African subsidiary of A.P. Møller Capital, a Danish fund manager and part of global shipping and logistics group A.P. Møller-Maersk. The R1,25bn deal was two years in the making following a competitive disposal process to seek a strategic partner. The deal will enable Vector Logistics to expand its supply chain expertise and logistics services to meet growing demand in Africa.

Local Advisers: Rand Merchant Bank, Baker McKenzie, White & Case (SA), Webber Wentzel and EY.

Exit by Carlyle Group of Tessara to AgroFresh

In 2018, Carlyle’s sub-Saharan Africa Fund acquired a majority stake in Cape-based Tessara. In 2023 the private equity firm exited its investment through a competitive auction process. AgroFresh is an AgTech innovator and global leader in post-harvest produce freshness and packaging solutions; Tessara specialises in SO2 generating sheets to prevent fungal decay and are sold in over 22 countries on five continents. During its tenure, Carlyle focused on strengthening Tessara’s R&D, new product innovation and on expanding the capacity of its manufacturing facilities.

Local Advisers: Bowmans, White & Case (SA), ENS, Webber Wentzel and EY.

Capitalworks’ exit of Robertson and Caine to Vox Ventures

Capitalworks, an alternative asset management firm, has exited its 2015 investment in South Africa’s largest boat builder, Robertson and Caine, to international investment company Vox Ventures, a wholly owned subsidiary of PPF, a European investment firm. The deal represents one of the most significant foreign direct investments in the marine industry in South Africa. The business has been positioned to benefit from the next phase of growth offered by a strategic investor.

Local Advisers: CMS, Werksmans, Webber Wentzel and PwC.

Absa’s eKhaya B-BBEE transaction

In March 2023, Absa announced the implementation of an R11,2bn Broad-Based Black Economic Empowerment deal allocating a 7% shareholding to staff and community beneficiaries. The deal is structured with a 4% evergreen Corporate Social Investment component (CSI Trust) and a 3% vesting staff element (ESOP). Staff employed by Absa’s subsidiaries outside of South Africa will participate equally in a cash-equivalent staff scheme, equivalent to about 1% of the Absa Group’s market capitalisation. The transaction will directly impact c.35,000 people employed by Absa and benefit a broader constituency across South Africa through the CSI Trust.

Local Advisers: Absa CIB, Oxford Partners, J.P. Morgan, ENS, PwC and KPMG.

Heineken Beverages’ Bokamoso transaction

Announced in July, almost 5,000 employees will jointly own a 6% stake in the company through an employee share ownership plan (ESOP) called the Bokamoso Workers Trust. The scheme is one of the conditions of ownership imposed by South Africa’s competition authorities in 2021, when Heineken International acquired Distell from minority shareholders. Distell’s previous empowerment deal saw the Distell Development Trust hold a 15% interest in the group’s local operations. This stake was rolled into the larger Heineken Beverages SA that was created through the merger, diluting the stake to an overall interest of 9%.

Local Advisers: Rand Merchant Bank and Webber Wentzel.

DewCrisp Western Cape

With 700 employees, the company applied to enter business rescue in July 2023. At the time, DewCrisp was facing three liquidation applications and it was in a state of severe financial distress, with virtually no working capital available. The company’s financial position was adversely affected by the COVID-19 pandemic and the lockdown measures put in place. Not only was retail income affected by the status quo, but so too were the crops which could not be harvested nor sold. The BRPs and the rescue team, assisted by management, worked on improving the profitability and sustainability of the company by undertaking an extensive operational restructuring. The business rescue process was successful in preventing the liquidation of the company, with 99% of creditors voting to adopt the business rescue plan. Additionally, the current shareholding remains intact.

Local Advisers: Engaged Business Turnaround and Werksmans.

Cast Products South Africa

Cast Products South Africa (CPSA), the largest foundry group in South Africa and 85% owned by the Industrial Development Corporation of South Africa (IDC), was placed in voluntary business rescue by its board in December 2021. In the four years until it was placed in business rescue, the company lost c.R1,7m, excluding the losses that accumulated after the IDC acquired Scaw Metals from Anglo American in 2010 as a result of pressure from escalating input costs, particularly electricity and scrap metal. The restructuring and restoration of solvency has been finalised, and the BRP’s are presently in the process of restructuring the Board and appointing a strategic management team to take the business forward. R1bn of liability has been restructured, the manufacturing capacity for South Africa has been retained, and corresponding jobs preserved under circumstances where the manufacturing industry is facing challenging economic times.

Local Advisers: Engaged Business Turnaround, Chrisyd Advisory Services and ENS.

Colin du Toit (Webber Wentzel)

Colin, a Partner at Webber Wentzel, has led on a number of high-profile deals, including MTN SA’s sale and leaseback of its SA towers portfolio. He advised Thungela Resources on its acquisition of a controlling stake in the Ensham Coal Mine and advised Safari Investments in respect of the public offer by Heriot REIT to acquire all the issued shares in Safari not already held. Colin was also a core part of the team that worked on the acquisition by Northam of an anchor stake of 34.5% of Royal Bafokeng Platinum and subsequent contested general offer for its control.

Ferdi Vorster (Rand Merchant Bank)

A member of the Rand Merchant Bank team, Ferdi advised Vivo Energy and Vitol on the acquisition of Engen from Petronas. He led the acquisition by Pick n Pay of Tomis and was involved as part of the RMB deal team that advised Life Healthcare on the sale of Alliance Medical, the buyout and delisting of Liberty Two Degrees, and RCL Foods’ sale of Vector Logistics to A.P. Møller Capital. Ferdi also worked on the sale of a 68.3% stake in Tanzanian-listed Tanga Cement by AfriSam to German multinational, Heidelberg Cement, first announced in 2021 – a deal that has taken numerous twists and turns over a few years, in terms of regulatory approvals.

Gareth Armstrong (Rand Merchant Bank)

Gareth is a Corporate Finance Executive at RMB and heads up the Consumer & Healthcare advisory business. In 2023, he helmed several market-leading including Life Healthcare’s sale of Alliance Medical Group to entities advised by iCON Infrastructure and led the RMB team that advised RCL Foods’ sale of Vector Logistics to A.P. Møller Capital. He also advised Richemont on the cancellation and replacement of its Depositary Receipts and A Warrant Receipt programmes and previously co-advised CIVH on its significant investment in Vodacom and CIVH on the acquisition of Herotel in a transformational deal for the TMT infrastructure sector.

Giles Douglas (Rothschild & Co)

Co-head of Rothschild & Co, Giles advised Petronas on its disposal of its 74% interest in Engen to Vivo Energy. He also advised ZCCM Investment Holdings and the Government of the Republic of Zambia on the restructuring and sale of a majority interest in the Mopani Copper Mine, providing various strategic initiatives in relation to the mine, and to the introduction of a strategic partner into the asset. Among other deals over the past few years, Giles has advised Ascendis Healthcare on its restructuring and debt for assets swap, and the sale of Respiratory Care Africa to ATA Capital.

Ryan Wessels (Bowmans)

Ryan is a Partner in the Bowmans M&A practice, which he joined in 2005. During the year he advised US-based AgroFresh on its entry into the South African market through the acquisition of local Tessara from The Carlyle Group. He also worked on the unbundling by Barloworld of the Zeda Group, and TotalEnergies’ divestment of its joint venture equity stake in the South African Natref refinery business to Prax Group. He advised MTN on its initial public offering of 20% of its shares in MTN Uganda and a listing of MTN on the Uganda Security Exchange.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")