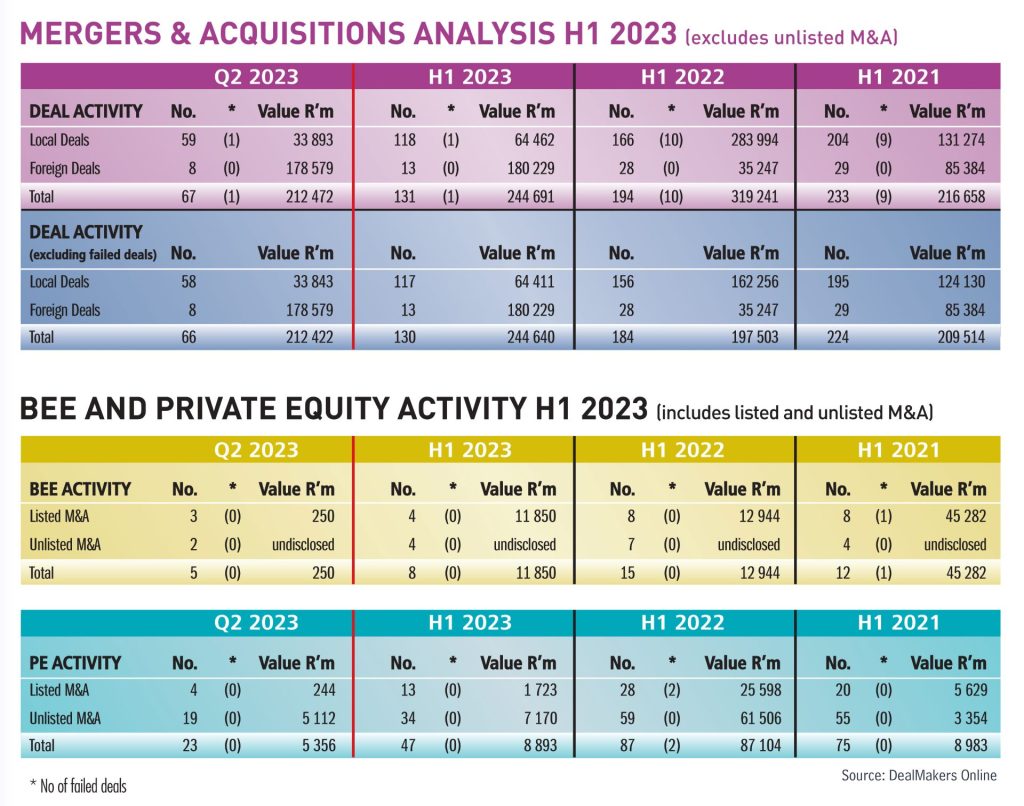

If a picture paints a thousand words, then so too do the M&A analysis tables below. The decline in merger and acquisition activity in South Africa began as far back as 2008, when the effect of the financial crisis hit home and the economy entered recession. In its hay day (2007), the industry reported 883 deals (listed and unlisted deals combined); an aggregate of some 405 for the half year. At the end of June 2023, the number was a meagre 242.

Since the release of a damaging report on state capture by the outgoing Public Protector Thuli Madonsela in 2016, and particularly in the last two years since emerging from the COVID-19 pandemic, the extent and reach of the malaise throughout the organs of government have become all too clear. This, together with uncertainties created by the war in Ukraine, inflation rates, looming recession, a weakening domestic exchange rate, foreign policy blunders, and the recent ‘greylisting’ of South Africa have forced investors to place more scrutiny on their investment domiciling decisions.

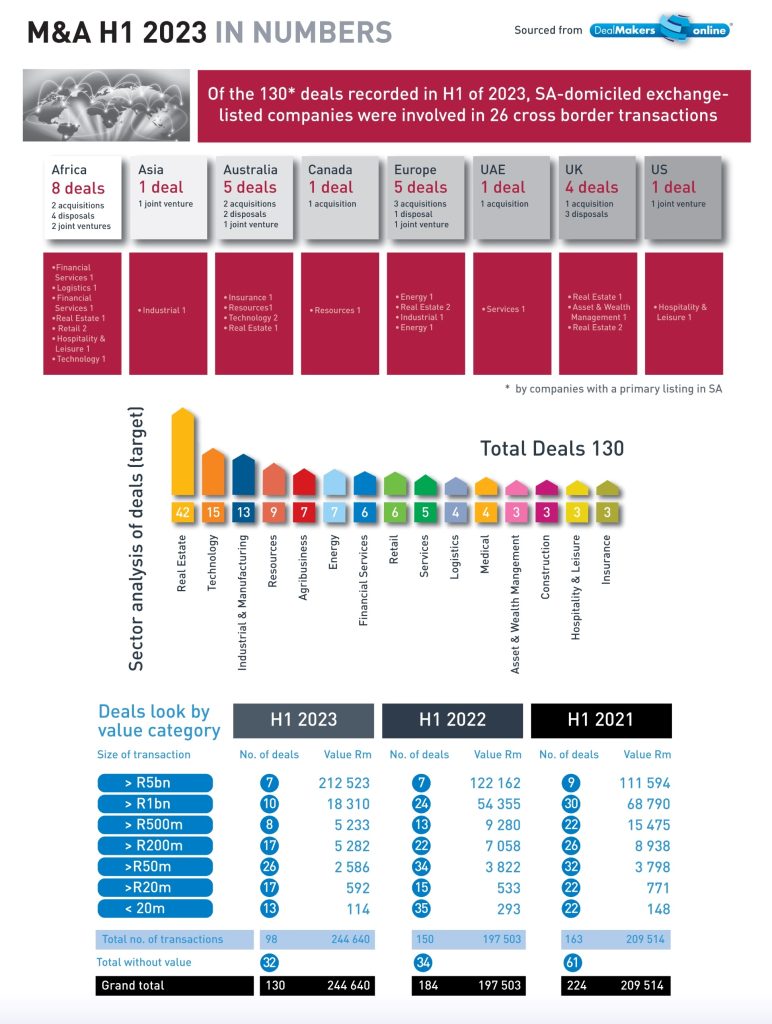

The most active sectors during H1 were Real Estate (32% of the quarter’s deals) followed by the tech sector. Deal size fell typically in the R50m to R200m bracket reflecting a third of deals recorded for the period. SA-domiciled companies were involved in 26 cross border transactions, notably within Africa (8), Australia (5) and Europe (5).

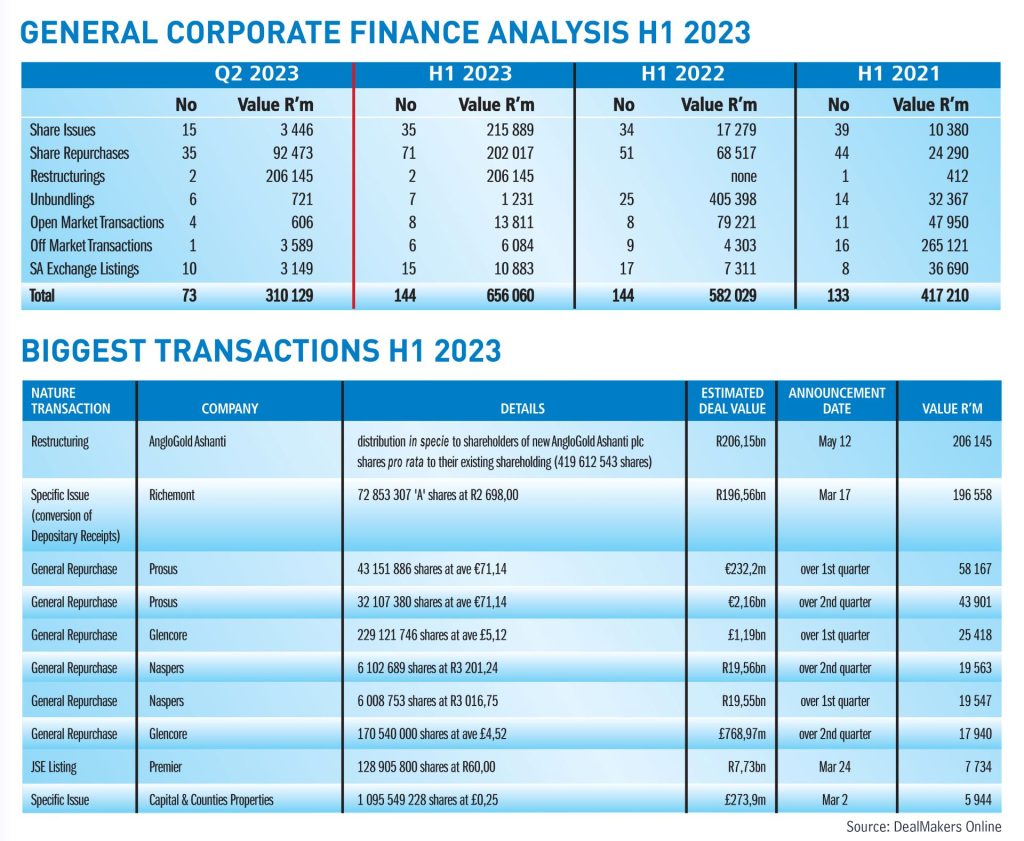

Share issues and repurchases characterised the general corporate finance activity for the first six months of 2023, with R215,89 billion raised from the issue of shares and R202 billion the value of shares repurchased. The repurchase programmes of Prosus, Naspers and Glencore account for most of this value, while the aggregate value of Richemont’s issue of A shares (conversion of depositary receipts) was R196,56 billion.

Although ratings agency, Fitch recently held SA’s credit rating at BB- (three steps below investment grade), it warned that further big increases in government’s debt-to-GDP ratio could lead to a further downgrade. The IMF is forecasting GDP growth of 0.3% in 2023, against 1.9% in 2022, due to severe power shortages – lagging far behind the 4% average at which the IMF sees emerging markets and developing economies growing in 2023. The Reserve Bank estimates that power cuts trimmed between 0.7% and 3.2% off the GDP growth rate in 2022, and that supply disruptions will cut 2% off output growth in 2023.

Looking ahead, the local equities and the SA bond markets offer value to potential investors relative to their international counterparts – but investors will continue to be circumspect, with much depending on SA’s ability to extract itself from the quagmire in the months ahead.

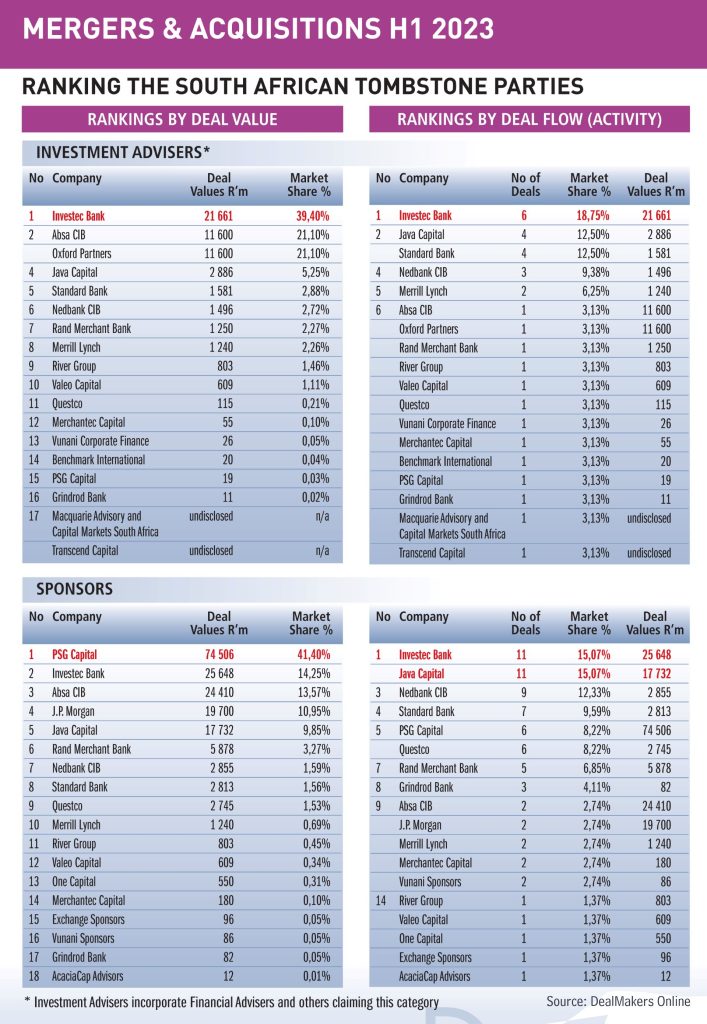

DealMakers H1 League Table – M&A activity by the top South African advisory firms (in relation to exchange-listed companies).

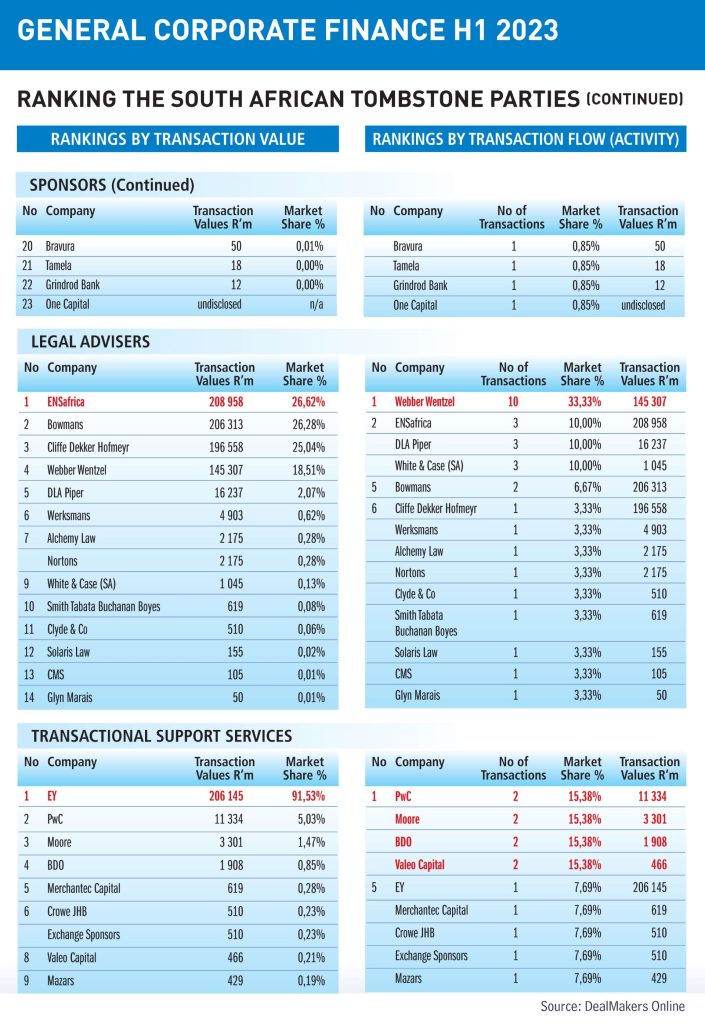

DealMakers H1 League Table – General Corporate Finance activity by the top South African advisory firms (in relation to exchange-listed companies).

Capital & Regional is to acquire The Gyle Shopping Centre in Edinburgh, Scotland for a total acquisition consideration of £40 million. The acquisition will be financed through existing funds held by the company, a new debt facility of £16 million and c. £25 million from proceeds to be received from a fully underwritten (by Growthpoint) capital raise. The capital raise is being implemented by way of an open offer of 46,278,681 open offer shares. The issue price of 54 pence/R13,03 per share represents 4 open offer shares for every 15 existing ordinary shares. Approximately £1,6 million of the proceeds will be used to pay fees and expenses incurred in connection with the proposed transactions.

STANLIB Asset Management (Standard Bank) through its Infrastructure Fund II, has acquired a controlling interest in renewable energy solutions specialist Solareff and its subsidiary, GridCars. Solareff is a commercial and industrial solar and battery platform with over 500 projects to date and a total of over 190MW of installed capacity. GridCars is the owner, operator, and supplier of charge-network infrastructure with related network software for South Africa electric vehicles. Financial details were undisclosed.

PPC has concluded an equity transaction with a newly formed PPC Employee Share Ownership Trust which has acquired 10% of PPC South Africa for a purchase consideration of R380 million. All employees not currently participating in PPC’s long-term incentive programme will be eligible and participation will be weighted in favour of the historically disadvantaged. The company will provide the Trust with a loan of R380 million which will be repaid from 75% of the dividends that it will receive from it shareholding in PPC SA, with the remaining 25% distributed to the beneficiaries.

Remgro and Vodacom have advised that the Competition Commission has recommended to the Competition Tribunal to prohibit the proposed acquisition by Vodacom of a 30% interest in Maziv. The deal, first announced in November 2021, proposed that Maziv, a newly formed entity, would house the assets owned by Community Investment Ventures which included Vumatel and Dark Fibre Africa as well as certain fibre assets of Vodacom.

Unlisted Companies

Fledge Capital, a local private equity firm, has invested an undisclosed sum in Luxury Time, an online business selling high-end watches at discounted prices. The new investment will be used to scale its inventory and enhance its online presence and customer service capabilities.

FinMeUp, a community-based platform dedicated to fostering a collaborative environment and offering a range of solutions including financial advisory, investments, insurance and credit solutions, has raised an undisclosed sum. The funding round was led by SAAD and Blue Sky Investments. The startup will use the funds to scale operations and enhance its user experience.

ADvTECH schools the market on how to grow (JSE: ADH)

All divisions have been strong contributors to this result

We will need to wait until 28 August to get all the details, but we do know that ADvTECH put in a very strong earnings performance over the six months to June.

The education group has indicated growth in HEPS of between 21% and 26%, which suggests a range of 82.3 cents to 85.7 cents. The share price closed more than 4% higher at R19.42.

CA Sales Holdings drives earnings forwards (JSE: CAA)

This really is an interesting business

CA Sales Holdings isn’t on the radar of most investors, yet the company has a fascinating business model and it is clearly working. In a trading statement for the six months ended June, the company has highlighted growth in HEPS of between 19% and 24%. This implies a range of 35.69 cents to 37.19 cents, with a current share price of around R7.15 for context. Remember, those are half-year earnings.

This news was accompanied by the release of interim results

Capital & Regional isn’t a company that you’ll regularly see in the news. This property fund is focused on community shopping centres in the UK and has announced the acquisition of The Gyle Shopping Centre in Edinburgh for £40 million.

To finance the deal, the company is raising £16 million in new debt and around £25 million in equity, so that’s a very rare thing these days: an equity raise on the JSE! There’s zero chance of the capital raise failing, as Growthpoint is underwriting the offer in full at a price of 54 pence per share. In London, the share price closed at 56.40 pence, so that’s a slight discount.

The debt is being provided by Morgan Stanley at a fixed cost of 6.5% for 5 years. The days of cheap debt in the UK (and everywhere, really) are over. The asset is being acquired at a net initial yield of 13.51%, so the days of property owners selling on a low yield also seem to be over! At that purchase price and with strong anchor tenants in place, I can see why Growthpoint is happily to put up all the capital if other shareholders don’t support the capital raise.

You have to start asking some tough questions about valuations in the local market if a mall in Scotland (a land of electricity and service delivery) is priced on a yield of 13.51%.

Alongside the news of this transaction, Capital & Regional also announced its results for the six months to June 2023. Occupancy improved, rent collections were good and like-for-like rental income increased by 13%, driving a 17% increase in adjusted earnings per share.

Net asset value increased by 2.3% as valuations finally started to stabilise.

The interim dividend has been increased by 10% to 2.75 pence per share. That’s a lower payout ratio than the prior year based on adjusted earnings per share, perhaps in response to the loan-to-value increasing from 41% to 42% and a general increase in average cost of debt in the market.

Cashbuild got hammered, but perhaps by less than expected? (JSE: CSB)

HEPS has dropped sharply, yet the share price had a good day

Cashbuild isn’t exactly an illiquid counter, so a 3.7% increase for the day isn’t just because of the spread. Yes, the broader market was also in the green today, so Cashbuild’s outperformance after the market had the entire day to consider the trading statement says something about how bad the expectations were.

For the year ended June 2023, HEPS is down by between 35% and 40%.

Although I don’t usually focus on earnings per share (EPS), I will note that the P&L Hardware business has had its goodwill impaired in response to ongoing pressure on that business.

The HEPS range for the year is R11.576 to R12.541. The share price is R168, so that still feels like a big Price/Earnings multiple for something that is struggling so much.

Life Healthcare is still exploring a deal for AMG (JSE: LHC)

Unsolicited proposals received this year are being taken seriously

Life Healthcare has been trading under cautionary since February 2023 based on unsolicited proposals received from third parties for the group’s stake in Alliance Medical Group in Europe.

Although there is still no guarantee of a sale of the stake, these are clearly serious proposals because the group has “narrowed the scope off its evaluation” and is working to see if a transaction is possible.

A big drop in the Lighthouse dividend (JSE: LTE)

Details will be released next week

You may recognise Lighthouse Properties as the company that Des de Beer always seems to be buying shares in. If you followed his strategy in the hope of happy news on the dividend, you’ll be disappointed.

The company has noted that the interim dividend is 1.35 EUR cents per share, a decrease of 16.92% year-on-year. Detailed results are due on 14 August.

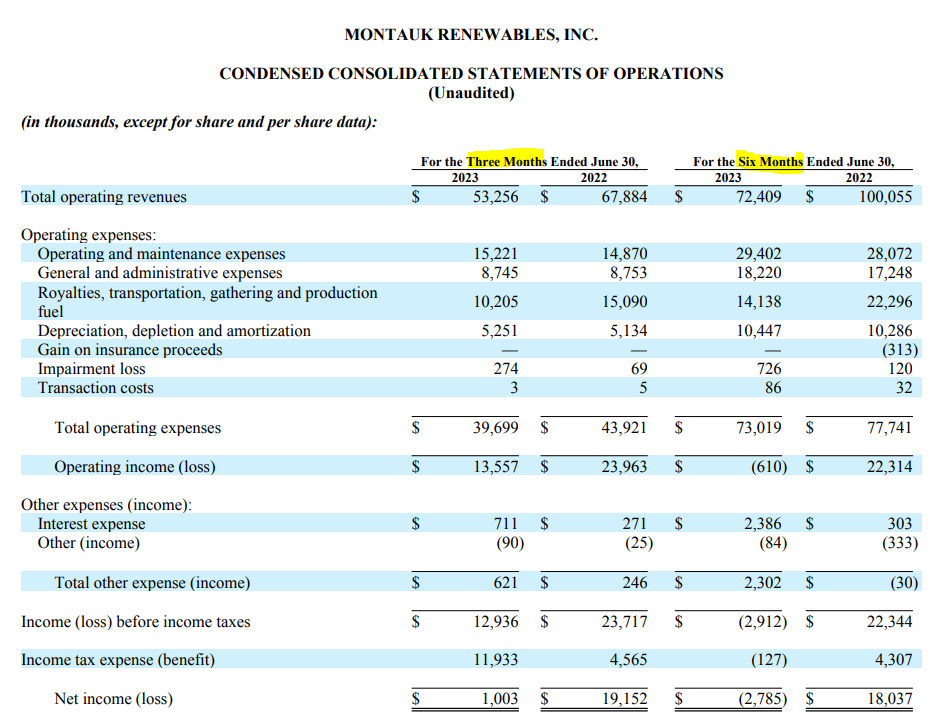

An interim loss at Montauk, but a better quarter (JSE: MKR)

There has also been extensive capex in this period

Montauk Renewables is listed on the NASDAQ in addition to the JSE, so the company reports earnings every quarter. When you see a huge swing in interim headline earnings from $0.13 to -$0.01, you can dig into the quarterly results to figure out why.

In there, you’ll find an income statement in this format:

As you can see, this lets you see the latest quarter as well as the six-month period. Although this quarter was profitable, it wasn’t enough for the performance over six months to be in the green.

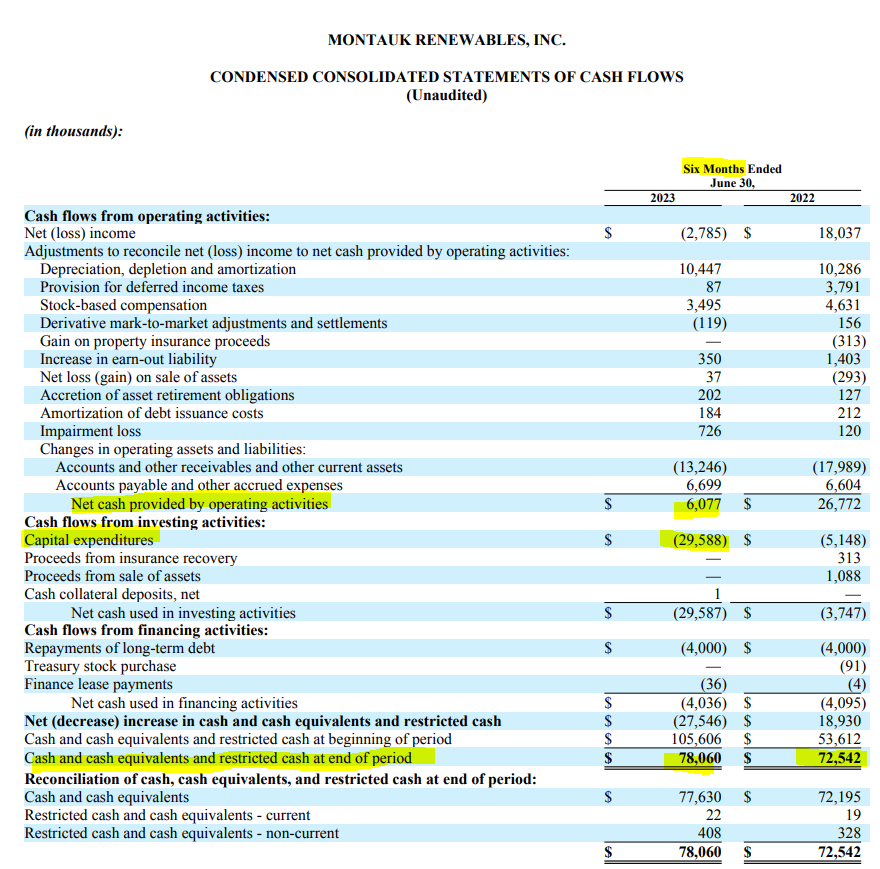

This business is very much in growth phase, which is why capital expenditure was $29.6 million in this interim period despite cash from operations being only $6 million. As the group came into this period with a lot of cash on the balance sheet, this brought the net cash balance down to where it was a year ago. Here’s how to spot the information that I just gave you:

Unsurprisingly, there’s no dividend.

In other news, Montauk continues to develop its project pipeline. The latest is an agreement with Duke Energy for a waste-to-renewable energy facility in North Carolina, with Duke agreeing to buy electricity for 15 years. The electricity is being converted from swine waste of all things! Renewable electricity and renewable natural gas is an interesting space.

Little Bites:

Director dealings:

The CEO of Argent Industrial (JSE: ART) sold shares worth nearly R18k.

For completeness, it’s worth noting that Remgro (JSE: REM) told us what we already know thanks to Vodacom (JSE: VOD) on Tuesday – that the Competition Commission doesn’t like the transaction to combine Vodacom’s fibre assets with Vumatel and Dark Fibre in a new joint venture. Remgro sits on the other side of the deal to Vodacom, so a prohibition (if decreed by the Competition Tribunal) would hurt both companies.

In rather interesting news, Orion Minerals (JSE: ORN) managed to settle R5.3 million worth of advisory fees to advisor Webb Street Capital through the issue of shares at 18 cents per share. That’s a pretty big discount to the current price of 27 cents but it does say something about their belief in the company as its advisor.

Although I’m simply picking on Spar (JSE: SPP) here because it’s a fresh example, I really do wonder how a fee like R2.76 million to the Chairman of the Board can be justified. The cost of running a corporate board is just extraordinary and it’s very debatable whether there is a net benefit to the company or its stakeholders from such bloated boards full of committees and independent directors. Of course, the counterargument is that directors carry a lot of risk, so they need to be paid accordingly. The system just feels inefficient to me.

African Equity Empowerment Investments (JSE: AEE) has been in dispute for a while with BT Limited. The dispute went to arbitration hearing in July and the parties are now working towards a settlement.

After PKF Octagon was not reappointed by shareholders as the auditor of Acsion Limited (JSE: ACS), the company will need to propose a new auditor. We don’t yet know who that will be.

Kore Potash has raised $0,8 million through the issue of 124,384,000 new ordinary shares. The proceeds will form part of its US$5 million commitment as per the Engineering, Procurement and Construction (EPC) contract for the construction of the Kola Potash Project.

Orion Minerals has issued 29,652,776 shares for a total consideration of A$444,792. The shares were issued to Webb Street Capital in lieu of fees owed by Orion for services provided.

Invicta announced the results of the odd-lot offer to the 1,510 ordinary shareholders on the share register holding less than 100 Invicta ordinary shares. The company repurchased 37,501 shares for a total consideration of R1,12 million.

Calgro M3 has repurchased 4,024,601 shares during the period 29 June 2023 to 7 August 2023. The shares, representing 3.30% of the issued ordinary share capital of the company, were repurchased for an aggregate R12,97 million. The shares will be delisted and cancelled.

Glencore has announced the commencement of another programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion with the intended completion by February 2024. The company repurchased a further 1,930,000 shares for a total consideration of £8,79 million this week. In its half year report, Glencore advised it would distribute c.$1 billion ($0.08 per share) by way of a special cash distribution to shareholders.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 31 July – 4 August 2023, a further 2,269,254 Prosus shares were repurchased for an aggregate €159,6 million and a further 473,244 Naspers shares for a total consideration of R1,65 billion.

Reunert shares will be admitted to trade on A2X as a secondary listing with effect from 15 August 2023.

Four companies issued profit warnings this week: Impala Platinum, Cashbuild, Glencore and Lighthouse Properties.

Two companies issued or withdrew a cautionary notice: African Equity Empowerment Investments and Life Healthcare.

DealMakers is SA’s M&A publication. www.dealmakerssouthafrica.com

Egypt’s B2B digital pharmacy marketplace, Grinta, has announced the acquisition of Auto-Cure. Financial details of the deal were not disclosed. Since launching in 2021, Grinta has made two acquisitions (PH Store and EME) and has raised US$8 million in seed funding (November 2022).

AI recruitment company, Talents Arena, has raised US$750,000 in pre-seed funding from UI Investments and several angel investors. The Egypt-based firm is a Flat6Labs portfolio company and an alumnus of the Plug and Play startup accelerator programme. The funds will be used to accelerate the AI hiring engine and expand its footprint in the Saudi market, which already makes up 25% of its client base.

Moove, the mobility fintech founded in Nigeria, has announced that it has raised additional funding to help with its global expansion plans. The US$76 million raised comprises $28 million in equity from new and existing investors, $10 million in debt and $38 million raised in the last year (not previously disclosed).

A15 has led a seed funding round with participation from group of angel investors, in Egypt’s Buguard. The US$500,000 investment will help the cybersecurity startup grow its team – this is the company’s first external fundraise.

Rwanda’s SOUK Farms has received an undisclosed investment from Goodwell Investments’ uMunthu II fund. The funding will provide SOUK, a grower and exporter of fresh horticultural produce from Rwanda, the capital it needs to scale up its operations.

Airtel Africa announced that its wholly owned subsidiary, Airtel Uganda intends to list on the Main Investment Market Segment of the Uganda Securities Exchange. The initial public offer will consist of 8,000,000,000 ordinary shares, representing 20% of the company.

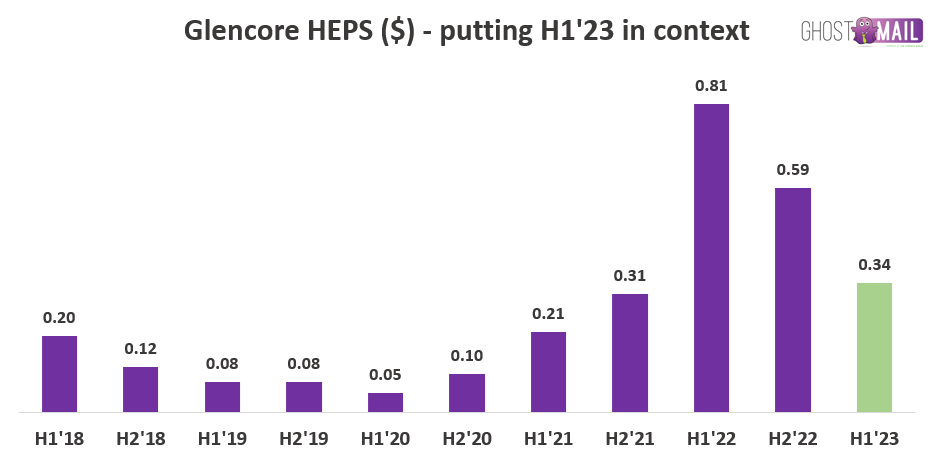

Glencore’s earnings have also taken pain (JSE: GLN)

HEPS fell by 58% year-on-year

No mining group is safe from the negative move in the mining cycle this year. In many cases, we’ve seen HEPS more than halve. Glencore finds itself in that bucket, with a drop in HEPS of 58% for the first half of the year.

To help give context to that number, here’s a chart of Glencore’s six-monthly HEPS going back to 2018:

The good news is that the group is still making a lot of money, with adjusted EBITDA of $9.4 billion and cash generated from operations of $8.4 billion, a solid cash conversion rate. Net income attributable to equity holders was $4.6 billion.

Adjusted EBITDA mining margins were 25% in the metals operations and 50% in the energy operations, in both cases well down from 43% and 66% respectively in the comparable period.

From a capital allocation perspective, the group has been focusing on investing in “transition metals” like aluminium, copper and nickel.

As the group is running a net debt balance well below its target, there will be $2.2 billion in additional returns to shareholders. This will take the form of a $1 billion special cash distribution and a $1.2 billon buyback programme running until February 2024.

Glencore isn’t everyone’s cup of tea, but they sure do know how to manage a balance sheet and drive shareholder returns. I love seeing a company actively managing the debt:equity ratio and not falling into the trap of having a lazy balance sheet.

Hooray for Hulamin (JSE: HLM)

HEPS has approximately doubled for the six months to June

Hulamin caused a buzz in the morning with the release of a terrific trading statement for the six months to June. HEPS is up by between 94% and 113%, coming in at between 91 cents and 100 cents. It’s probably safer to use normalised HEPS, which increased by between 83% and 103%, which means a range of 66 cents to 73 cents.

Either way, the share price closed the prior day at R2.63 and shot up more than 25% in morning trade in response to these numbers. As Price/Earnings multiples go, this is one of the lowest ones around!

PowerChina goes Dutch with Kore Potash (JSE: KP2)

More costs are going to be incurred to finalise the EPC contract

Those who have been following Kore Potash will know that the company has been negotiating with SEPCO for a while now to finalise an Engineering, Procurement and Construction (EPC) contract for the construction of the Kola Potash Project.

The parent company of SEPCO is PowerChina International. PowerChina stepped in earlier this year to review the design and construction schedule and has now requested further engineering design work before finalising the EPC proposal.

The cost of this is $10 million. PowerChina is willing to incur roughly half of that cost, with exposure to overruns. Kore Potash’s contribution is capped at $5 million.

To achieve this, Kore Potash needs to immediately pay $1 million. The company has already raised $0.8 million from the Chairman of the company and a related party. There are other major institutions who have up to 21 business days to top up that amount if they so desire.

The remaining contribution by Kore Potash needs to be paid in three tranches between October 2023 and 12 months from the date of signature of the EPC contract. As is always the case in junior mining, investors can expect further capital raises and dilution.

The parties are aiming to sign the EPC contract before the end of January 2024. The Summit Consortium as key financiers remain supportive of this.

Nedbank’s metrics are heading the right way (JSE: NED)

As we’ve seen across the board though, impairments are climbing sharply

Hot on the heels of the Standard Bank trading update that looked incredibly strong, we have Nedbank with a more modest but still positive earnings update. This is a detailed set of numbers rather than just a trading update, covering the six months ended June.

Headline earnings per share (HEPS) is up by 11% and so is the interim dividend, with a payout ratio of 57%. The net asset value per share (a very important metric in banking, also called NAV per share) is 8% higher to R224.58. The share price is trading at a slight premium to NAV per share, with the market looking to a return on equity of 14.2% to support this number.

I would strongly debate whether 14.2% is high enough to support a premium to NAV. Banking stocks in some cases have perhaps run too hard.

Looking deeper into the income statement, revenue growth (including associate income) grew by 14% and pre-provision operating profit was up 22%. This shows you what would’ve happened in a consistent credit quality environment. With load shedding and such a poor macroeconomic environment, this is anything but a consistent credit environment. Impairments jumped by 57%, muting the story and explaining why HEPS only grew by 11%.

We can go one step deeper and look at what the key drivers of revenue growth were. As expected, net interest income was the winner with 18% growth vs. non-interest revenue at 7%. From an efficiency perspective (a measure of cost control), the cost-to-income ratio headed in the right direction from 56.1% to 52.9%.

The outlook isn’t great, with almost no economic growth in South Africa for the remainder of the year. Nedbank does expect interest rates to stay flat for the rest of 2023 though, so consumers will be hoping that this is the correct view.

Quilter is focusing on what it can control (JSE: QLT)

And as the latest numbers show, the company is doing a great job

Asset management and advisory firms are always going to be impacted by broader asset valuations in the market. They earn fees based on assets under management. As those assets increase, so do the fees. This generally makes them high beta stocks that move in line with broader market prices.

Within that framework, it’s important to understand that they can control (1) how successfully they attract inflows and (2) their cost base. This is the right way to judge the success or failure of a company in this space.

Quilter is nailing both of those things. Don’t focus on the growth in Assets under Management and Administration of just 2% during the six months to June. Rather focus on the core net inflows of £0.7 billion, an impressive result when you consider the higher interest rates environment across the world and the impact this is having on income available for saving. Unsurprisingly, the High Net Worth and Affluent channels did well here, as those people still have money to save.

Although group revenue only increased by 3%, operating margin improved from 20% to 24% and that was good enough to boost adjusted profit before tax by 25%. Great cost discipline really helps here and there are further savings planned under the “Simplification” project.

The dividend is up by 25% as well, so the cash is following the profits.

There are some big distortions in profitability even at HEPS level. The company discloses adjusted earnings per share that increased by 34% and that’s probably the right metric for profitability. If nothing else, look at the growth in the dividend.

Tongaat Hulett updated the market on business rescue (JSE: TON)

The monthly report has more details on the preferred equity partner, Kagera

Each month, Tongaat Hulett needs to update the market on its business rescue proceedings. Although the news of Kagera as the preferred strategic equity partner isn’t new, the report does go into further details.

The idea is that Kagera will acquire the complete sugar division of the business, including the investments in Zimbabwe, Mozambique and Botswana.

Kagera is owned by Tanzanian businessman Nassor Seif. This falls under a group called Super Group, with no relation to the JSE-listed group of the same name. They have over three decades of experience in sugar and agriculture in Africa. Other operations in the group are in the logistics and industrial sectors.

The ongoing existence of Tongaat Hulett is important for reasons that go far behind the plight of current shareholders. Based on Kagera’s experience in difficult operating conditions, this plan just might work!

Business rescue is about saving a business, not saving the shareholders or even the creditors.

Vodacom drops the pre-public holiday bombshell (JSE: VOD)

The Competition Commission wants to block the deal with Vumatel and Dark Fibre

This is very big news. The telecoms sector is not a great place for shareholders right now and the companies in the sector are trying to improve their fortunes by moving into new sources of revenue. Fibre is an obvious area of expansion for a company like Vodacom, which is why the company wanted to acquire 30% in a newly formed entity that would house Vumatel and Dark Fibre Africa.

ICASA had no problem with it, but that’s a totally different regulatory framework to the Competition Commission. Despite Vodacom and Community Investment Ventures Holdings (the joint venture party) having committed to address competition related concerns through a list given to the authorities, the Competition Commission has decided to recommend to the Competition Tribunal to prohibit the transaction.

There is clearly a long way to go here, as the Commission doesn’t have the final say. The Tribunal still needs to make a decision, with the Competition Appeal Court as last chance saloon thereafter.

A big part of the argument in favour of the deal is that Vodacom is ready to invest R60 billion over 5 years in South Africa. This investment of R13 billion is over and above that number.

But then again, if South African regulators prioritised investment in our economy, don’t you think our economic growth would look a little different?

Remgro (JSE: REM) is also part of this transaction. The company hasn’t released an announcement yet. This will presumably be coming on Thursday.

Little Bites:

Director dealings:

There’s a lot of action on the Novus (JSE: NVS) share register. In what can only be another block trade, the dynamic duo at A2 Investment Partners have acquired R95.7 million worth of shares in Novus. For context, this is a company with a market cap of just over R1 billion.

A director of Lewis (JSE: LEW) has sold shares worth just under R2 million.

Brimstone Investment Corporation (JSE: BRT) has released a trading statement for the six months ended June. The reason that this is only a “Little Bite” is because the trading statement focuses on HEPS, which isn’t the right metric for an investment holding company like Brimstone. Growth in HEPS of between 234% and 244% doesn’t really tell you much about the underlying portfolio. Net asset value (NAV) per share is the right metric. As there was no mention of this in the announcement, I can only assume that the movement is less than 20%. We will find out on 4 September.

The Calgro M3 (JSE: CGR) share buybacks are marching forward, with 3.3% of the company’s share capital repurchased between 29 June and 7 August. This is an allocation of nearly R13 million worth of capital. The company has authority to repurchase up to 20% of its shares in issue until the next AGM.

Zeder’s (JSE: ZED) special dividend of 5 cents per share has still not achieved approval from the SARB, so the payment date cannot be confirmed yet.

Sygnia’s (JSE: SYG) lease agreements with related parties have been determined by PSG Capital as Independent Expert to be fair to shareholders.

Headline earnings increase of 10% driven by strong revenue growth partially offset by increases in retail impairments

Nedbank wants to ensure that Ghost Mail readers have a proper understanding of the numbers. To assist with that, CFO Mike Davis also gave me some of his time to ask whatever questions I wanted. Here’s the summary:

GHOST: Are South African consumers eating into what little savings they have, or are they managing to tread water at this interest rate level? What is driving the narrative in the market that the next rate hike is the one that breaks the story?

MIKE DAVIS: The reality is that whether there’s another 25bps hike or not, the combined effect of rates currently sitting at 11.75%, high inflation, low growth and low levels of employment means that consumers are battling. It’s not just about the next hike. We are seeing this in the Retail and Business Banking franchise in particular. There’s pressure across the board in consumer banking, including home loans, vehicle finance, personal loans and card. The most sensitive vintage in the book was originated at the low point in the interest rate cycle and those borrowers are now struggling. Consumers are drawing down on savings to meet higher levels of debt. The corporate book is stronger than the retail book, as corporates have retained strong balance sheets and sat on cash. They’ve been particularly careful.

GHOST: Let’s talk commercial property. This seems to be a focus area on Twitter (X!) when I tapped into the hive mind there. How is that book looking? Rebosis?

MIKE DAVIS: There are a few counters in business rescue, as we’ve detailed in the results. There is obviously uncertainty around this. The Rebosis process should complete in August and we acknowledge that there is risk of an outcome that is worse than expected.

GHOST: What pockets of growth can you see for Nedbank? We understand the broader macroeconomic picture, but where can Nedbank do relatively better than competitors?

MIKE DAVIS: The Nedbank brand is stronger than market share might suggest. We over-index in vehicle finance in terms of market share with our MFC business. But our retail franchise is sub-scale when viewed through that lens. One of the things we can do better is cross-sell, like getting better at selling insurance to the banking client base.

GHOST: The vehicle sales environment in South Africa doesn’t make much sense in terms of affordability. What trends are you seeing there, particularly important as MFC has been a big part of Nedbank’s success?

MIKE DAVIS: We’ve definitely seen consumers trade down into cheaper vehicles. This still supports overall growth and churn. South African consumers are unusual in that they would rather default on their home loan than vehicle finance, in many ways a function of the state of public transport in our country. We’ve lost some market share in this space by being selective on origination. The most sensitive vintage is loans that were originated at the time when rates were lowest. This is a similar trend to home loans, but not as severe as we are seeing there. This is actually a great time to originate loans. If a consumer can afford the finance in this environment, that’s high quality credit.

GHOST: Finally, what are your thoughts on competitors like Discovery and Old Mutual still to come? What about the likes of Bank Zero?

MIKE DAVIS: The broader the competitive landscape, the better for consumers. All players in this space need to compete on quality or price. The Old Mutual push isn’t a surprise to us, as we suspected a bank entry when Old Mutual was selling down Nedbank. You also need to think of the telcos and retailers and their push into financial services. What about Amazon and Google? Everyone wants a piece of the financial services pie and the competitive landscape is broader than just the obvious banks, particularly in payments and in-store credit. The big banks like Nedbank have large balance sheets and strong cash profits almost regardless of the economy, which lets them defend their positions. We have invested heavily in our digital transformation and our clients are very digitally active. So yes, there are new players in this space all the time, but Nedbank has been evolving digitally to respond to this.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this week’s episode of Ghost Wrap, we play rock paper scissors (well, almost):

Rock: AngloGold, Pan African Resources and Impala Platinum showing us that times are tough in mining.

Paper: Mondi and Sappi reflecting highly cyclical numbers, with Mpact delivering really strong results in this period.

Scissors: a sharp set of numbers came in from Spur and Standard Bank.

The company is making its largest-ever single investment

It really wasn’t that long ago that the Gemfields share price was coming under a lot of pressure from violence in Mozambique. Thanks to what is essentially terrorist activity in the region, many investors got spooked.

Perhaps thanks to the right working relationship with government, the Montepuez Ruby Mining (MRM) business has managed to escape harm. Gemfields is clearly feeling confident about its future there, as the company has committed to constructing an additional processing plant at the facility.

This project will triple MRM’s processing capacity, so the company must also be feeling good about ruby prices achieved at recent auctions.

The investment required is around $70 million but the price has actually been agreed in rands. The cost is spread over three years, starting in 2023 and on a 30% | 60% | 10% basis. The mining fleet will also need to be expanded in 2025 as this processing plant is put to work.

Impala Platinum flags a big drop in earnings (JSE: IMP)

Sales volumes and price per ounce both fell this year

This environment has been somewhat of a perfect storm for the mining industry, particularly the local platinum players although we’ve also seen pain at the likes of AngloGold. In a trading statement, Impala Platinum has flagged a drop in HEPS for the year ended June of at least 20%.

Importantly, that is the minimum required disclosure from a JSE perspective. I would wager that the earnings drop is a lot worse than that.

Group production increased by 2% (managed operations up 6% and joint ventures down 1%), hamstrung by issues ranging from load curtailment by Eskom through to cable theft challenges. Mining in South Africa is an extreme sport, with the operations in Zimbabwe also suffering load shedding.

Producing the stuff is one thing. Selling it is quite another. Sales volumes fell by 6% and the price per ounce dropped by 4% per ounce in rands. Even a 16% depreciation of our currency against the dollar wasn’t enough to offset the pressure on PGM pricing.

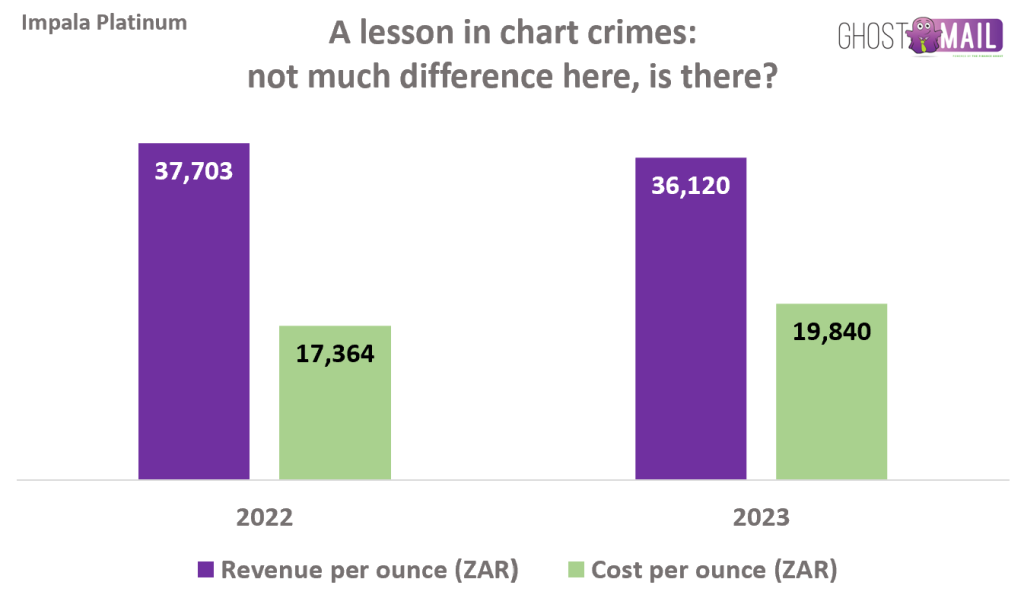

To make it worse, Impala Platinum didn’t escape the inflationary pressure on input costs. Whenever a company doesn’t disclose a comparative number, it’s because the answer is ugly. I went digging in the 2022 report and discovered a cost per 6E ounce of R17,364 vs. the cost this year of R19,840. The price per ounce sold fell from R37,703 per 6E ounce to R36,120.

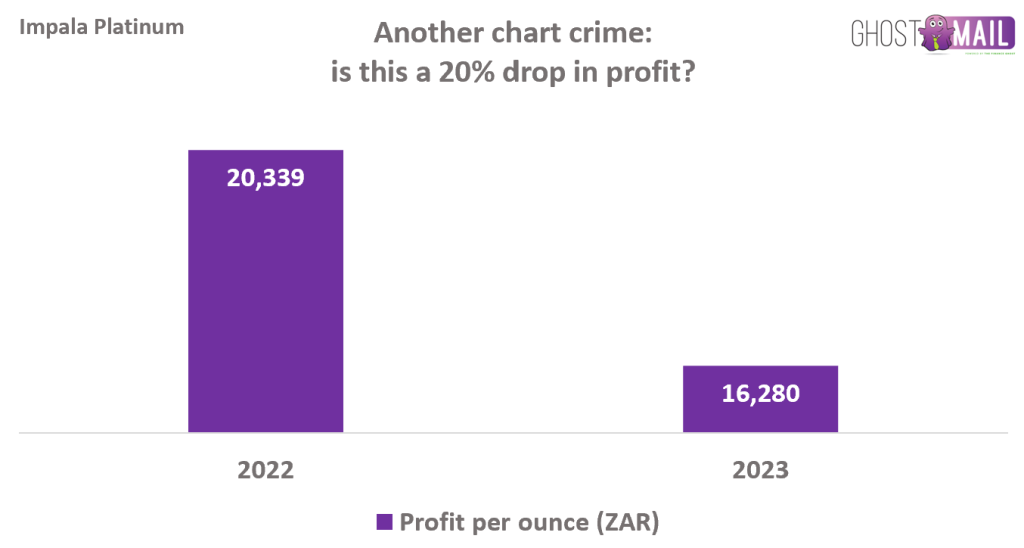

So, this tells us that profit per 6E ounce has been smashed from R20,339 per 6E ounce to R16,280 per ounce. That’s a 20% drop in profit per ounce along with a drop in sales volumes of 6%.

A 20% drop in HEPS? It’s going to be a whole lot more than that. The free cash flow is going to be even worse, with capital expenditure up from R9.1 billion to R11.5 billion.

As an aside, I decided that the Impala Platinum numbers would be perfect to use in illustrating chart crimes to you. This is no reflection on the company whatsoever – I simply used these numbers to make the point clear to you. After all, Ghost Bites is all about empowering you to be a better and more informed investor and trader.

The first crime is when a big difference is made to look like a small one:

The second crime is when a fairly big difference is made to look absolutely gigantic:

The lesson here? Be very aware of charts with a Y-axis that has been set up to trick you. This is especially problematic when the Y-axis is hidden and there are no gridlines, like in these examples!

Pan African achieved revised production guidance (JSE: PAN)

Net debt has come down significantly

Back in May, Pan African Resources gave the market revised production guidance. Considering that the year-end of June was soon thereafter, one would hope that the company would have met that guidance. This is indeed the case, with production of 175,209oz.

Sadly, this is well off the record production achieved in FY22 of 205,688oz. The group has given production guidance for FY24 of 178,000oz – 190,000oz, so that’s still not a recovery to FY22 levels.

All-in sustaining cost is between $1,325/oz and $1,350/oz, significantly higher than $1,284/oz in the prior year. When production levels come off, the cost per ounce increases.

The good news is that net debt declined from $49.9 million at the end of December 2022 to $18.9 million at the end of June.

PPC executes an employee B-BBEE deal (JSE: PPC)

This deal is for 10% of PPC South Africa, but is the funding rate too high?

There are a number of different approaches to B-BBEE transactions. Whilst I continue to wish that the universe of investable B-BBEE schemes on the JSE would improve, the reality is that most companies seem to shun this approach in favour of either employee schemes or that old favourite, a well-connected consortium.

PPC has at least taken the route of empowering employees, with a deal for 10% of PPC South Africa that will be weighted in favour of historically disadvantaged individuals. To facilitate the deal, PPC will loan R380 million plus R975k for securities transfer tax to the B-BBEE trust. The loan will be repaid through allocating 75% of dividends to the debt, with 25% distributed to the trust’s beneficiaries. As “trickle dividends” go, that’s quite high.

Those dividends have quite a mountain to climb, as the debt is priced at the South African prime rate. Unless there is a material improvement in PPC’s local business, I can’t see much value being transferred to staff through this scheme. They will get the dividend and not much else.

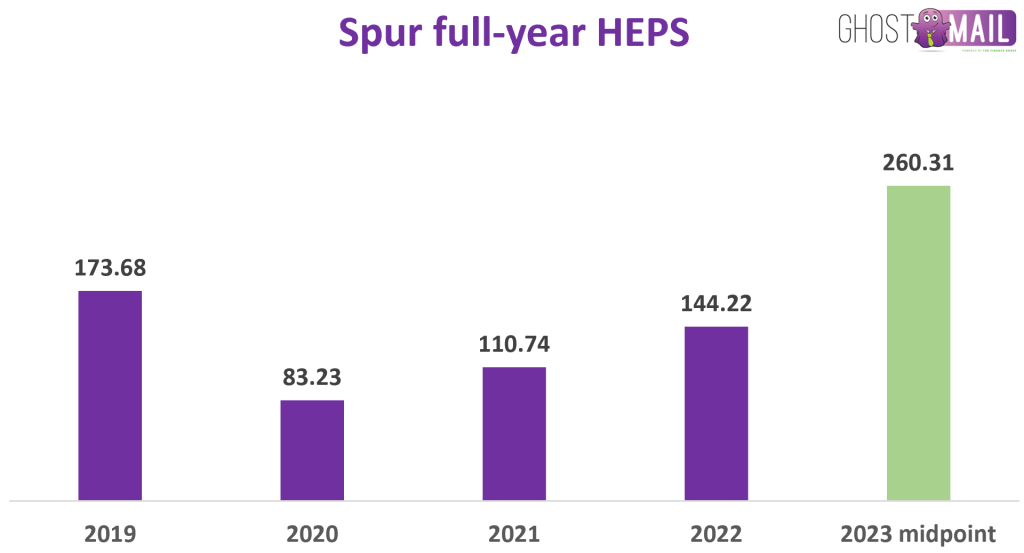

Spur: people with a taste for profits (JSE: SUR)

Even with a through-the-cycle lens, these are big numbers

Despite the pressure that South African consumers are clearly under, the kids still like ice cream and stressed out parents need calories and usually something to drink as well. Perhaps assisted by load shedding and the alternative of a cold meal at home, Spur has released exceptionally strong numbers.

In case you’re wondering whether this is just a Covid base effect, as the exact timing of lockdowns is starting to become a hazy memory, here’s a chart of HEPS over the past few years:

As you can see, the latest performance is incredibly impressive. This is more good news after Spur recently announced the acquisition of a 60% stake in the Doppio Group, a deal that seemed to be well received on Twitter / X / whatever you want to call it.

I used the midpoint of 2023 HEPS guidance in the chart. The range in the trading statement is growth of between 78% and 83%. Although there were once-offs in the base (like the settlement of a dispute with SARS), the chart shows you how strong these latest numbers are.

Share buybacks are useful in boosting HEPS but a result like this still needs a strong top-line performance. That’s exactly what Spur delivered, with total South African sales up 22.5% for the year ended June. There was a notable slowdown in the second half of the financial year, with sales growth of 14.4% vs. 31.3% in the first half. For whatever reason, John Dory’s bore the brunt of that issue with a 1% decline in the second half, a really poor performance vs. the next-worst Roco Mama’s at 4.7% growth. Panarotti’s managed 9.6% growth in the second half, with Spur as the big winner with 16.9% growth in this load shedding environment.

Although a relatively small part of the group, Speciality Brands (Hussar Grill, Casa Bella and Nikos – the segment that Doppio Zero will slot into) grew by 42.2% for the full year. The second half performance was 27.2%, which confirms that a glass of wine in a restaurant is more fun than staying home in the dark.

Little Bites:

Director dealings:

The COO of Kibo Energy (JSE: KBO) has sold shares worth roughly R540k.

The company secretary of Oceana (JSE: OCE) sold shares worth R103k.

In something that you certainly won’t see every day, 96.4% of shareholders in Acsion (JSE: ACS) voted against the reappointment of PKF Octagon as the auditor at the AGM.

In case you’re wondering just how many obscure holdings of certificated shares are in existence out there, Invicta’s (JSE: IVT) odd-lot offer achieved a repurchase of 37,501 shares of which 9,513 were still in certificated form! Yes, that literally means a situation of share certificates hiding away in your granny’s top drawer.

If you are a shareholder in Crookes Brothers (JSE: CKS), then you may want to refer to the circular for the disposal of the deciduous fruit farming business at this link.

Montauk Renewables (JSE: MKR) used SENS like a PR system with its announcement about a letter of intent signed with EE North America to deliver CO2 volumes to the company. The announcement gives no financial information whatsoever and the delivery period (assuming it goes ahead) will only begin in 2026.

AngloGold releases details behind the drop in earnings (JSE: ANG)

HEPS fell by 54% and free cash flow was negative in this period

In the six months ended June, probably the only highlight at AngloGold Ashanti is that the second quarter was better than the first quarter. If you add the two quarters together, you still get to a pretty horrible year-on-year performance.

It’s little wonder that the announcement focuses on the cadence (Q2 vs. Q1) rather than the year-on-year numbers. Production in the second quarter was 12% up on the first quarter and all-in sustaining costs were 4% better. The group is trying hard to convince investors that the second half of the year will suck a lot less than the first half, with full-year production guidance maintained and costs expected to improve.

The problem in the first half is that production was flat year-on-year and the average gold price received per ounce only increased by 2%. When all-in costs per ounce jumped by 15%, that’s a big problem for margins. Gross profit fell by 23% and HEPS tanked by 54% because of the impact of debt.

The free cash outflow of $205 million is concerning. The comparable period was an inflow of $471 million, admittedly boosted by legacy payments of $460 million from Kibali.

The challenge in the mining industry is that the capital expenditure requirements are substantial. If cash profits take a tumble, it can cause negative free cash flow and a deteriorating balance sheet. AngloGold will need to deliver a much-improved second half of the year.

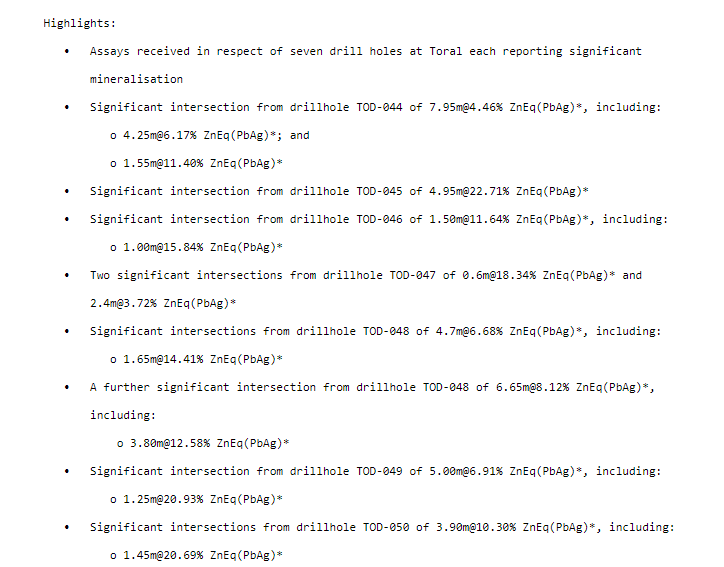

Europa Metals releases further drilling results (JSE: EUZ)

The latest results from the Toral project in Spain are available

I always joke about how drilling announcements are basically impossible to understand unless you are a geologist. Allow me to show you why, courtesy of Europa Metals:

And that, dear Ghosties, is why I skip to the management commentary section to look for clues. A comment like “intersections reported to date have correlated well with the known existing resource” is very helpful.

The company is preparing for the mining licence application, with an environmental report due for completion later this month.

MTN Rwanda and Uganda release results (JSE: MTN)

It’s just a pity that MTN Rwanda didn’t update the website

I wasted 10 minutes looking through the Rwanda Stock Exchange website in desperation, hoping to find the interim results that weren’t on the MTN Rwanda website despite MTN announcing that they were available. Perhaps they will be there by the time you read this.

Thankfully, the team in Uganda seems to know how a website works. Services revenue in the six months to June increased by 15% and EBITDA was up by 16.8%, so EBITDA margin moved in the right direction by 40 basis points to 50.6%.

The interim dividend is 19% higher, as profit after tax only increased by 17.8%. Capital expenditure was flat year-on-year, so that helped keep dividend growth roughly in line with profit growth.

In case you’re wondering what went wrong between EBITDA and profit after tax, the answer lies firmly in the net finance costs line and its whopping 34.3% increase!

Standard Bank is still loving this cycle (JSE: SBK)

If things can stay like this, banking shareholders will be thrilled

The local banking sector finds itself at an interesting point in the cycle. If interest rate hikes stop, as we saw in the pause by the SARB at the last MPC meeting, then banking earnings should be excellent. If they continue, then the impact of impairments should start to offset the benefit of higher net interest margin.

For now at least, the banking party continues. Standard Bank closed 5.7% higher on Friday after releasing a trading statement indicating HEPS growth of between 30% and 35% for the six months ended June.

After the big trades in Novus (JSE: NVS) earlier in the week, we now have confirmation that it was Value Capital Partners selling the last of its stake in the company.

The transaction between Nikkel Trading and Brikor (JSE: BIK) has been approved by the Competition Commission with certain conditions. The announcement doesn’t go into further details, only confirming that the conditions are acceptable to Nikkel Trading.

In a most unfortunate update by Kibo Energy (JSE: KBO), the joint venture that subsidiary Mast Energy Developments is working on has been delayed. This is because the principal at Seira Capital, the lead investor partner, has been involved in an accident and is in hospital in critical condition. The group obviously can’t commit to a completion date based on this.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")